#3.18 is hitting different (which i didn’t think was possible)

Text

Oh my God.

Did anyone else forget that Eddie was literally right there keeping Buck from falling off the freeway platform as he’s telling Lola about Abby in Buck, Actually?

“You think that you have something... something special, you know? She’s the one. So you wait. And then, at some point, it hits you: you’re alone. Sh-she’s not coming back. You’re just there to collect the mail, and-and it is piling up, right? And then—and then you realize, “You know what? It’s over.” You just need to face it and move on.”

I am currently losing my mind.

52 notes

·

View notes

Text

Quantum Leap - Season Three Review

"I always do the right thing, Al. And where does it get me?"

Season three is when the formula started to wear thin a bit... and I got a little tired of "Oh, boy," even though Scott Bakula valiantly did his level best to make it sound different every single time. Al hitting his hand link also got a little old. It was also pretty obvious by this point that God has a sick sense of humor. The way Sam is dumped into ridiculous and/or dangerous situations with no knowledge of what is going on is like an ongoing practical joke. Why would God leap Sam into a magic box being pierced by swords, or just in time to sprinkle talc on a naked guy's underwear?

What works

Just like season two, the best episodes of season three are the premiere and the finale. In fact, the premiere is considered to be the best episode of the series, because Sam finally got to leap home. Sort of.

3.1 "The Leap Home, Part 1 (November 25, 1969)": How many of us would give nearly everything for a chance to go back in time and fix what went wrong in our own lives? It's tragic that when Sam leaped into himself at sixteen, he longed to save everyone in his family, but had to face the fact that it was not what God sent him there to do.

In a way, "The Leap Home" paralleled "M.I.A.", where Al refused to believe Ziggy's projections because he wanted the leap to be about saving his marriage to Beth. Here, Sam also refused to believe what Al was telling him because he was certain he was there to save his brother from dying in Vietnam, his father from dying of lung cancer, and even that he could keep his little sister Katie from ruining her life by marrying an abusive man. It's so easy for the audience to put themselves in Sam's shoes. I confess that I've often fantasized about going back in time somehow so that I could find a way to save my sister's life.

But no, you really can't go home again. With the possible exception of Al dancing with Beth in "M.I.A.," "The Leap Home" gave us the strongest scene in the series as Sam told his little sister Katie the truth about time travel and the bad stuff that was coming, and tried to prove it by singing his favorite song that hadn't been written yet. (A beautiful vocal by Scott Bakula, and by the way, "Imagine" is, coincidentally, my favorite song of all time, too.) Katie's face as she slowly realized that she'd never heard the song before and that it meant their brother Tom would die was genuinely heartbreaking, and Sam was forced to say that he was making it all up. This scene was made even more poignant, if that's possible, by Al almost wordlessly telling Sam not to share with Katie what happened to John Lennon. Honestly, I'm dripping tears just writing about it.

In the scenes that followed, Sam for the first time expressed his anger at what God was forcing him to do, to save other people but not the people that Sam himself loved. Al, who had also lost his chance to fix his life with time travel, was the one to remind Sam that God also gave him an amazing gift: the chance to spend Thanksgiving with his family one more time.

Scott Bakula played both Sam and Sam's father. That was okay, but it felt too much like a gimmick. I wonder if maybe some of the scenes might have worked better if I hadn't been distracted by Bakula playing two roles?

That's a nitpick, though. This is an excellent, emotionally resonant episode.

3.2 "The Leap Home, Part 2 (April 7, 1970)": Part two was also terrific. It felt like God was rewarding Sam for his sacrifice in part one by allowing him to save Tom's life. Andrea Thompson (Babylon 5) gave a good performance as dynamic reporter Maggie Dawson, who died for her Pulitzer. It made me think about whether or not it would be worth dying to create something that would live forever.

But I was unhappy that the unsuccessful mission was all about rescuing Al from his POW prison back in 1970. It felt like the writers were rubbing in the fact that Sam and Al couldn't use time travel to change their own lives... except that Sam actually could, this time. Why was Sam rewarded but Al punished? (Maybe I'm taking this too personally.)

3.6 "Miss Deep South (June 7, 1958)": I dislike pretty much everything about beauty pageants, but couldn't help loving this episode. Maybe I really liked the feminist slant, that Sam had to perform well in the pageant so that the young woman he'd leaped into could become a doctor and save a whole lot of lives — or maybe it was that he was also there to save another young woman from making an epically bad choice in life, like his sister Katie.

Okay, okay, it was probably Scott Bakula singing "Great Balls of Fire" while dressed like Carmen Miranda.

3.12 "8 1/2 Months (November 15, 1955)": Another excellent episode where Scott Bakula played a woman, this time an unmarried, pregnant sixteen-year-old girl. I particularly liked the emphasis on how helpless an underage pregnant girl was and how few choices she had back in the fifties. I also want to mention again what a strong actor Scott Bakula is. He's a masculine-looking guy, but he can wear women's clothing, even flowery maternity clothes, and I'm still focused on his performance instead of what he's wearing.

3.13 "Future Boy (October 6, 1957)": Sam leaped in to help Moe, the star of a children's TV show about time travel. Moe constructed a faux time machine in his own basement, and his adult daughter Irene believed that Moe was losing his marbles and wanted to have him committed. Touchingly, Moe built the machine because what he wanted more than anything was to go back in time and be a better husband and father. I don't know whether or not it was intentional, but there was some ambiguity in this Moe situation, since it was pretty clear to me that Moe really had lost touch with reality and should have been hospitalized. But it was still touching that Sam was able to bring Moe and Irene back together as family.

3.22 "Shock Theater (October 3, 1954)": As I've mentioned before, many Quantum Leap episodes feel like homages to specific movies. Here, it was One Flew Over the Cuckoo's Nest, as Sam was subjected to shock treatment against his will, which made him dissociate into various personalities. The best part was that all of those personalities were the real people that Sam leaped into, and that this time, Sam wasn't faking it -- he actually was his leapees: Tom Stratton, Jesse Tyler, Samantha Stormer, Jimmy, Kid Cody.

Nearly every episode of Quantum Leap puts Sam in some sort of danger, but we usually feel that he'll be okay in the end. In this one, it felt like things were spiraling out of control as Sam suffered abuse and was in genuine peril. In the end, Sam was forced to ask for the shock treatment that he dreaded, and he and Al somehow wound up leaping together, leaving us with a pretty serious and unusual cliffhanger.

Okay, there were a couple of problems with this one. Al rapping to teach Scott Lawrence's character to read made me uncomfortable. It was also hard not to wonder what happened to Sam's unfortunate leapee after the treatment, and how unfair that whole thing was to him.

Honorable mention

3.17 "Glitter Rock (April 12, 1974)": It's always fun when an episode features Scott Bakula singing, and for some reason, I absolutely loved the technicolor pseudo-Kiss makeup. But what the hell was Al wearing? A decorative stop sign? Wouldn't that be dangerous if he were walking down a road somewhere?

3.18 "A Hunting Will We Go (June 18, 1976)": It's hard to pull off this much slapstick in a single episode and do it well, but I thought they did: this episode was pretty darned funny. Good job by Scott Bakula as well as Jane Sibbett, who gave a vibrant performance; I always saw her as David Schwimmer's bland ex-wife on Friends, and didn't realize she was capable of stuff like this. I also appreciated the homage to the famous Clark Gable/Claudette Colbert hitchhiking scene from It Happened One Night.

What doesn't work

There are a few weak episodes, but this one's awfulness stood out from the crowd:

3.5 "The Boogieman (October 31, 1964)": This truly idiotic and poorly written episode is about a dream Sam had, while unconscious, of mysterious murders at a Halloween spook house. It included a replica of Al as the devil trying to stop Sam from fixing things while leaping — possibly Dean Stockwell's poorest performance of the series — and a teenage Stephen King with his dog Cujo.

Bits and pieces:

-- Famous people: Jack Kerouac, and as mentioned above, Stephen King.

-- Notable actors: C.C.H. Pounder, Kurt Fuller, and Peter Noone from Herman's Hermits. And Olivia Burnett, who did such a terrific job playing Sam's little sister Katie, also played another little girl named Susan in season two's "Another Mother."

-- Here's a question for those of you better at this online app stuff. Is Quantum Leap available for free at nbc.com (with commercials)? If it is, what did they do about the music replacement issue?

To conclude

I thought season three was good, but not quite as good as season two. And in fact, rewatching season three drove home for me that as a series, Quantum Leap was episodic, not serial. Honestly, I'd forgotten. But as my mother used to say, it is what it is.

On to season four.

Billie Doux loves good television and spends way too much time writing about it.

#Quantum Leap#Sam Beckett#Al Calavicci#Scott Bakula#Dean Stockwell#Quantum Leap Reviews#Doux Reviews#TV Reviews#something from the archive

15 notes

·

View notes

Text

Is OnTrajectory the best retirement calculator?

My colleagues, who are money nerds just like me, know that I'm obsessed with finding the best retirement calculator. I've been on this quest for years. As you'll learn later this week, my favorite retirement tool is (and has been) NewRetirement. But there are other great tools out there.

You really need to try OnTrajectory, Jillian from Montana Money Adventures told me last summer. It's great. She's been telling me that over and over ever since. (Meanwhile, Gwen from Fiery Millennials has also been pressuring me to try OnTrajectory.)

Last week, at long last, I had a chance to chat with Tyson Koska, the founder of OnTrajectory. During a 30-minute call, he walked me through setting up an account and playing with the tool's features. I'm impressed. NewRetirement is still my favorite tool, but OnTrajectory is damn close. And I can see how for some people, the latter may actually be a better choice.

Today, let's take a look at what makes OnTrajectory one of the best retirement calculators available on the web.

How OnTrajectory Started

The OnTrajectory origin story is similar to that of You Need a Budget.

Koska spent decades looking for a tool that would give him a high-level view of his financial future. I couldn't find one that I liked, he says. He didn't like their assumptions. He didn't like their interfaces. He didn't like their limited functionality.

Eventually, he took matters into his own hands. He built a complex spreadsheet to explore different variables and what-if scenarios. From there, he began coding Excel macros and small software tools. Over time, the current version of OnTrajectory evolved from his experimentation.

Just as YNAB grew out of Jesse Mecham's desire to build himself the perfect budgeting tool, OnTrajectory is a product of Koska's quest for the perfect retirement calculator. Over the years, it's morphed from a simple spreadsheet to a complex tool with a distinctive look and feel.

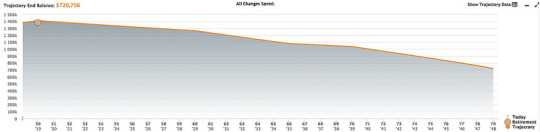

OnTrajectory is all about this graph:

That graph really dominates your tool, I told Koska on our call.

Exactly, he said. That's the whole point. That graph is always present at the top of your screen to show you your trajectory. Any time you make an adjustment to your assumptions any time that graph gets updated.

Because Koska considers himself a part of the growing FIRE community the group of folks who is interested in financial independence and early retirement OnTrajectory is built with their needs in mind. You want to retire by 40? Fine. OnTrajectory can handle that. You want some absurd saving rate like 90%? No problem. You can model pretty much any scenario you can imagine.

Getting Started

It's easy to get started with OnTrajectory. Once you provide login credentials, you're given two choices:

A quick-start wizard that asks only three questions before launching you into the tool.A more comprehensive guided entry process during which you manually enter your income, expenses, and existing investment accounts.

The former is quick and easy. The latter provides better results. As you can probably guess, I'm not a quick-start wizard sort of guy. I opted to use the longer guided entry process. It didn't take anywhere near the 30-minute projected time. (But that's probably because I already had my financial info gathered in one place.)

During the set-up process, OnTrajectory asks questions about your existing financial infrastructure and your goals for the future. It uses this info to populate three of its five navigation tabs. The guided entry asks you to:

Designate expected income, including regular salary, Social Security, pensions, rental income, and so on.Specify large, recurring expenses such as vehicle payments, housing payment, insurance premiums, property taxes, and the like.Enter current balances of major financial accounts like your Roth IRA and 401(k), regular brokerage accounts, and your bank accounts. (OnTrajectory does not automatically connect to your accounts. You must enter this info manually.)

You can add to or alter these numbers at any time. They're not set in stone, so don't be afraid of making mistakes.

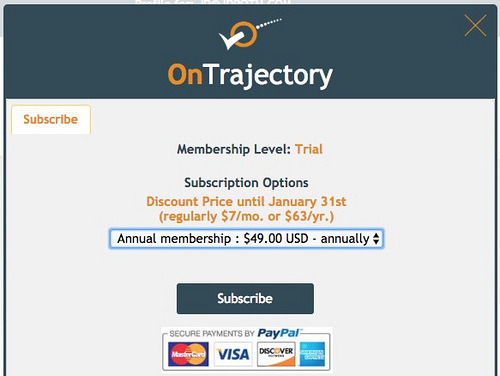

OnTrajectory is free to use for fourteen days. (You don't even need to enter credit card info, which is awesome!) If you'd like to continue using the tool, however, you have to subscribe at $4.99/month (or $49/year).

Using OnTrajectory

OnTrajectory seems simple at first, but the more I worked with it, the more I appreciated how it handles complexity.

One of its strengths, for instance, is the ability to plot a variety of possible futures.

Our lives are dominated by uncertainty. Sure, there are likely paths that lie before each one of us, but there's plenty we don't know. Plus, a few times each decade, we reach major forks in the road to our future. Do I take this job or that job? Do I move to Savannah, Georgia or do I remain in Portland, Oregon? Should I draw Social Security at age 62 or wait until I can get maximum benefits at age 70?

Normally, it's tough to predict how your decisions will affect your financial future. With OnTrajectory, however, it's simple to explore these alternate dimensions. You can toggle any parameter at any time.

Here, for instance, is a list of my potential income sources. I've included working at the family box factory, two possible income levels from this website, eventual Social Security payments, and a potential inheritance from my mother.

In Personal Capital, it's nice that you can add or remove various events to see how doing so affects your future. But if you remove an event, it's gone. You can't save it.

With OnTrajectory, you just toggle a button to see the difference. If you want to add, say, an inheritance back into the equation, you just click the button once more. What this means from a practical perspective is that you can enter several possible scenarios/events that you deem likely, then explore different possible futures. This is a very handy feature.

OnTrajectory also allows you to play with the assumptions under the hood. Three key variables are always instantly accessible: your retirement age, your Trajectory End Age (a.k.a. your projected date of death), and a projected inflation rate. (The default inflation rate in OnTrajectory is 3.00%. That's just slightly optimistic for me. I chose to change it to 3.18%, which is the U.S. long-term average. If I were extremely pessimistic, I might change it to something like 4.08%, which I think is the 50-year moving average but don't quote me.)

You can also play with tax rates, investment contributions, investment returns, and more. As you might have noticed, you can enter start ages and end ages for most line items. If you want to explore different possible paths, you can enter additional age range possibilities without deleting your original item. Then you just toggle between the two lines to see the effects of, say, working longer.

OnTrajectory allows you to set specific goals, such as I want my Trajectory to reach $1,500,000. These goals then get plotted on your Trajectory graph. For instance, if I want to know when my net worth Trajectory will hit $1,500,000, the app will plot it on the ever-present graph. In this particular case, it says I should hit that goal on 11 November 2029.

So, as you can see, OnTrajectory is very similar to a lot of other retirement calculators out there except that it takes things to the next level. Anything the Personal Capital retirement tool can do, OnTrajectory can do better.

But wait! That's not all! OnTrajectory also allows users to create and print a variety of PDF reports. It includes a handy inflation calculator. And there's a nascent OnTrajectory community on Reddit where you can ask questions and share ideas.

Having said all of that, OnTrajectory isn't perfect.

Problems with OnTrajectory

As much as I love OnTrajectory, there's one key piece of the tool that I hate: the terminology. For me, it's confusing.

In this tool's parlance, your Trajectory is your projected future financial path. And your Trajectory for any given date is your net worth on that date. That makes total sense, right?

But individual accounts can have trajectories too. If my 401(k) has a Trajectory of $246,136 today, that's its balance today. So, maybe Trajectory actually means balance? I don't know. I'm confused.

Things get more confusing after you've been using the tool for a while. Your Trajectory is based on your initial parameters, not your current situation. The tool does plot a trajectory projection based on your current situation, but your Trajectory (with a capital T) is based on your starting assumptions.

(There's a logic behind this. OnTrajectory uses the Monte Carlo method to look into the future. It assumes that your current situation is one point on many possible projected paths, and that your circumstances will very likely be subject to reversion to the mean. By basing your Trajectory on your starting circumstances rather than your current circumstances which generally improve with time it's providing a more conservative/cautious approach to retirement planning.)

I understand that OnTrajectory uses the term trajectory to stay on-brand, but for somebody like me it creates more confusion than clarity. I'd prefer that existing standard definitions were used. If your Trajectory is your net worth, then call it your net worth. If Trajectory simply means balance, then use the word balance.

OnTrajectory is a fine name for the tool, but I don't see the need to cloud the issue by getting cute with naming conventions.

That's my main beef with OnTrajectory, but it has other minor quirks too.

There's a Default Investments account that cannot be deleted. (It's meant to be a catch-all for stray cash, I think. This is sort of like the petty cash account I use in Quicken.)

While attempting to enter my Basic Expenses line item, OnTrajectory refused to let me set its End Age to 79 (my projected end of life); it only let me set it to 78. (I was able to set everything else to 79 but not my Basic Expenses. Weird.) As a result, OnTrajectory believes I have $0 expenses during the last year of my life haha.At one point, the OnTrajectory graph simply disappeared. I changed my projected date of death (or Trajectory End Age in the program's terms) and the graph vanished. I couldn't get it to come back. After trying a bunch of different things, I clicked the Undo button. I'm not sure what action I undid, but pressing the button brought back the graph.

To me, these minor quirks don't affect my overall impression of OnTrajectory. They're bugs (or features I don't like). They're likely to go away in the future. The terminology thing drives me nuts, but I suspect I might be the only person who is bothered by it. And it's not enough to dampen my enthusiasm for this tool.

The Bottom Line

So far, OnTrajectory is the best traditional retirement calculator I've found. (As I said, I like NewRetirement better, but it takes a different approach.) It's a comprehensive, complex tool but the interface is never overwhelming.

If the interface does become overwhelming or confusing, OnTrajectory features extensive (and useful) documentation. In nearly every section of the screen, you can click on a little info button to bring up the on-line manual. This guide provides answers and tips on all of the functions and features. Impressive.

For me, the killer feature is that OnTrajectory not only allows you to save your data, but also to create and save multiple scenarios. You don't have to re-enter your data each time you want to check on your progress. And if you want to play with possibilities what if I were to quit my job and take a more meaningful non-profit position? it's super simple to do sowithout trashing your existing info!

We're all about the what-ifs, Koska told me during our call last week. OnTrajectory is specifically designed to let users explore possible futures. We let people play with a lot of variables, but our goal is for the interface to never become overwhelming.

The bottom line? OnTrajectory is like the Personal Capital retirement calculator on steroids. It has everything I like about the PC tool, but is much more customizable. In fact, I like it so much that I signed up for a paid account!

Author: J.D. Roth

In 2006, J.D. founded Get Rich Slowly to document his quest to get out of debt. Over time, he learned how to save and how to invest. Today, he's managed to reach early retirement! He wants to help you master your money and your life. No scams. No gimmicks. Just smart money advice to help you reach your goals.

https://www.getrichslowly.org/ontrajectory-retirement-calculator/

0 notes

Text

The Only Thing Left

Reaction fic for 3.18 because oh my goddddddddd

The Only Thing Left

Cisco perched on Caitlin's desk. She said immediately, "Get your butt off my nice clean desk."

"What are you implying about my butt?" Without waiting for an answer, he scooped up about half the cup's worth of strawberry jello. "So, here's what I don't get about that Pandora's box story,"

"The what?" she asked absently, concentrating on her graphs. Woman was crazy for her data, and he was saying that as an engineer, okay.

"You know Pandora's box?" he said through a mouthful of sugary gelatin goodness. "The story about the old-times lady who opened up the box the gods told her not to and - "

"Released all the evils of the world, yes, Cisco, I read Bullfinch's Mythology too. What's your point?"

He knew about Pandora's box from Wishbone, not Bullfinch's Mythology, but he didn't point that out because her mom hadn't let her watch a talking dog sharing great literature. If there was one thing they'd discussed thoroughly, it was how much Mama Snow had hated joy.

"So, the end of the story? How there was one thing left in the box after war and death and famine and people who cut funding for school lunches had all been released?"

She sat back, looking up at him. "Hope," she said. "That's what was left. Hope."

"Right. What even was hope doing in the box with a bunch of evil things? That never made sense to me. Isn't hope a good thing?"

"Oh, Cisco," she said softly. "Hope is a wicked, wicked thing."

"That's cynical," he said. "Hope keeps you going."

She stood up and touched his face with her fingertips. He lost his breath, which happened sometimes with Caitlin, when he looked at her and his brain went, oh, hey, hi there. Hi, you. Another kind of hope.

"Hope lies," she told him. "It strings you along. Tells you impossible things. Keeps the agony sharp, long after you should have moved on."

"Okay," he said, voice croaking. "Yeah. It's not always good - "

"Hope might be the worst evil of all. Except maybe for me."

Her eyes went blue and her hand on his face went icy cold and -

He woke up screaming.

When his voice gave out, he found himself huddled under his blankets. He'd taken to sleeping under mounds of them, sweating through the night, but it never seemed to thaw the ice that slid through his veins ever since -

"Maybe she's in there," he said.

"She was gone," H.R. told him. "Her heart stopped."

He looked at Julian, who after all had more medical experience than H.R. To be fair, there were washcloths with more medical experience than H.R., but anyway the point stood. "Your brain doesn't die right away when your heart stops, right?" he asked. "It's why you - "

Julian stood abruptly. He looked pale. Positively waxy. "I know what I did."

"Isn't it possible - "

"Killer Frost had taken over completely," he said. His lips were tight and bloodless. "The only way she could do that is if Caitlin were - "

"But - before. You weren't here for it, but we got her back before. She was in there and we got her back, so maybe - "

"She's gone, Cisco," Julian said. He went into Caitlin's lab and slammed the door.

Cisco pressed his face into his pillow.

He and Caitlin had actually had that discussion about hope and Pandora's box and all, sometime after when Ronnie had disappeared into the singularity, before she'd gone to Mercury Labs. At the time, he'd sympathized but privately thought she was speaking out of grief.

Now he knew exactly what she'd meant.

He looked at the CCTV footage and saw Killer Frost, who looked nothing like Caitlin. Different hair, different eyes, definitely different dress sense.

But sometimes she tilted her head or moved her hands in a way that screamed Caitlin, this is Caitlin, and he had to look away.

He had her necklace, entombed in a box that sat on his desk. He hated himself sometimes for not putting it back on her when Julian had ripped it off. He'd stood there clutching it, thinking, This isn't what she wants. But there was a little part of him that was relieved Julian had done it, because maybe - maybe -

But Star Labs had thrown the dice once too often, using Caitlin, using her powers, and they'd paid the price. Caitlin had paid the price. And now Killer Frost was loose.

He dreamed about getting Caitlin back. He dreamed it a lot. He dreamed of Barry talking her out of her icy prison again. He dreamed of Julian kissing her awake, like Sleeping Beauty. He dreamed of going up to her himself, taking her hands and saying her name, and she would blink her eyes brown and throw her arms around him.

He even dreamed of Savitar, doing something totally out of character and taking her powers away like some reverse Santa Claus.

He tried to convince himself that they were vibes, that he was seeing the future, that this would all be fine, but he knew better. The colors weren't the right shade of blue. The edges didn't have the right smear. They weren't vibes, they were just dreams.

Hopes.

Killer Frost went Chaotic Evil through the city, hitting - well, pretty much anything that caught her eye, as far as Star Labs could tell. Cisco got them an advantage when he set special watches on all of Caitlin's favorite stores, particularly the ones that she only allowed herself to purchase from once in awhile - too expensive, Cisco, it's not going to fit in the budget this month.

But when it came to her, that was about the only way he was useful.

"It's not her," Julian, Iris, Joe chanted in his earpiece when he faced her down among the shattered shelves of glittering jewelry, or the wreckage of a particularly high-end shoe store. "It's not Caitlin. It's not."

But she'd spotted his weakness early, and he limped back from every confrontation battered and bruised and more than slightly frostbitten. Julian would wrap up his wrenched knee or clean out the gravel from where he'd skidded half a block, not bothering to scold him for once again trying to get through to Caitlin, through all the layers of Killer Frost -

"She's in there," Cisco said. "I believe it. She's got to be in there."

"She's gone," Julian said harshly, and turned away.

If he had, even once, said You're good to go the way Caitlin used to, Cisco would have either cried or decked him. Maybe Julian knew that, because he didn't.

They avoided each other's eyes a lot these days.

Finally, Barry and Wally sat him down and gently, kindly told him Vibe wasn't allowed to fight her anymore. That if they got a report of her, he needed to go back to Star Labs.

He didn't argue.

They didn't want to hurt her either - she'd been their friend too, even she hadn't been quite what she was to Cisco. Mostly they managed to keep her from living up to the Killer part of her name.

That seemed to be at an end when the police found a severely hypothermic man in the wreckage of his small jewelry store.

Cisco hacked into the records of Mercy General - "does patient privacy mean nothing to you lot," Julian said waspishly, and sighed at the blank faces that turned his way - to check on the patient, dreading to find that he'd died or been permanently damaged by frostbite.

What he found made him yell for everybody. They rushed in, pale, ready for another disaster. But he spun in his chair, vibrating with joy. "The guy had a history of heart attacks, and tests show he'd had another one that evening."

". . . yay?" Wally said uncertainly.

"No, no, no - " Cisco leapt to his feet. "Okay, there's this thing, right? This thing, it's called therapeutic hypothermia, when somebody has a heart attack, they chill 'em down - Back me up here," he ordered Julian, who must have learned the technique as a medic. "Isn't that something they do?"

"It is, yes," he admitted reluctantly. "In certain cases, first responders will lower the core temperature, gradually, with cold packs and such, to slow the metabolism and reduce the risk of brain damage after cardiac arrest."

"Which she knew," Cisco burst out. "We talked about it, way back before we even heard the name Killer Frost. What if the guy had a heart attack when she tried to rob his store, and she cooled him down?"

Barry pointed out, "It would be more like Killer Frost to leave him dying on the floor and walk off with most of his inventory. Which, um, she did."

"That's what I'm saying. She didn't have to hit him with the cold whammy. It would just waste her time, with the alarm already going off. Guys, this was Caitlin!"

Julian said quietly, "Cisco, mate, you're grasping."

"She's in there," he said, and watched them shake their heads. "You guys, no, it's a very exact thing, it's not gonna happen by accident - "

Iris gave him a pitying look. He looked away.

"She's in there," he said. "I know it."

Hope is the thing with feathers, perching in his soul. Its beak is razor sharp.

FINIS

42 notes

·

View notes

Text

Is OnTrajectory the best retirement calculator?

My colleagues, who are money nerds just like me, know that I'm obsessed with finding the best retirement calculator. I've been on this quest for years. As you'll learn later this week, my favorite retirement tool is (and has been) NewRetirement. But there are other great tools out there.

“You really need to try OnTrajectory,” Jillian from Montana Money Adventures told me last summer. “It's great.” She's been telling me that over and over ever since. (Meanwhile, Gwen from Fiery Millennials has also been pressuring me to try OnTrajectory.)

Last week, at long last, I had a chance to chat with Tyson Koska, the founder of OnTrajectory. During a 30-minute call, he walked me through setting up an account and playing with the tool's features. I'm impressed. NewRetirement is still my favorite tool, but OnTrajectory is damn close. And I can see how for some people, the latter may actually be a better choice.

Today, let's take a look at what makes OnTrajectory one of the best retirement calculators available on the web.

How OnTrajectory Started

The OnTrajectory origin story is similar to that of You Need a Budget.

Koska spent decades looking for a tool that would give him a high-level view of his financial future. “I couldn't find one that I liked,” he says. He didn't like their assumptions. He didn't like their interfaces. He didn't like their limited functionality.

Eventually, he took matters into his own hands. He built a complex spreadsheet to explore different variables and what-if scenarios. From there, he began coding Excel macros and small software tools. Over time, the current version of OnTrajectory evolved from his experimentation.

Just as YNAB grew out of Jesse Mecham's desire to build himself the perfect budgeting tool, OnTrajectory is a product of Koska's quest for the perfect retirement calculator. Over the years, it's morphed from a simple spreadsheet to a complex tool with a distinctive look and feel.

OnTrajectory is all about this graph:

“That graph really dominates your tool,” I told Koska on our call.

“Exactly,” he said. “That's the whole point. That graph is always present at the top of your screen to show you your trajectory. Any time you make an adjustment to your assumptions — any time — that graph gets updated.”

Because Koska considers himself a part of the growing FIRE community — the group of folks who is interested in financial independence and early retirement — OnTrajectory is built with their needs in mind. You want to retire by 40? Fine. OnTrajectory can handle that. You want some absurd saving rate like 90%? No problem. You can model pretty much any scenario you can imagine.

Getting Started

It's easy to get started with OnTrajectory. Once you provide login credentials, you're given two choices:

A quick-start wizard that asks only three questions before launching you into the tool.

A more comprehensive “guided entry” process during which you manually enter your income, expenses, and existing investment accounts.

The former is quick and easy. The latter provides better results. As you can probably guess, I'm not a quick-start wizard sort of guy. I opted to use the longer “guided entry” process. It didn't take anywhere near the 30-minute projected time. (But that's probably because I already had my financial info gathered in one place.)

During the set-up process, OnTrajectory asks questions about your existing financial infrastructure and your goals for the future. It uses this info to populate three of its five navigation tabs. The guided entry asks you to:

Designate expected income, including regular salary, Social Security, pensions, rental income, and so on.

Specify large, recurring expenses such as vehicle payments, housing payment, insurance premiums, property taxes, and the like.

Enter current balances of major financial accounts like your Roth IRA and 401(k), regular brokerage accounts, and your bank accounts. (OnTrajectory does not automatically connect to your accounts. You must enter this info manually.)

You can add to or alter these numbers at any time. They're not set in stone, so don't be afraid of making mistakes.

OnTrajectory is free to use for fourteen days. (You don't even need to enter credit card info, which is awesome!) If you'd like to continue using the tool, however, you have to subscribe at $4.99/month (or $49/year).

Using OnTrajectory

OnTrajectory seems simple at first, but the more I worked with it, the more I appreciated how it handles complexity.

One of its strengths, for instance, is the ability to plot a variety of possible futures.

Our lives are dominated by uncertainty. Sure, there are likely paths that lie before each one of us, but there's plenty we don't know. Plus, a few times each decade, we reach major forks in the road to our future. Do I take this job or that job? Do I move to Savannah, Georgia or do I remain in Portland, Oregon? Should I draw Social Security at age 62 or wait until I can get maximum benefits at age 70?

Normally, it's tough to predict how your decisions will affect your financial future. With OnTrajectory, however, it's simple to explore these “alternate dimensions”. You can toggle any parameter at any time.

Here, for instance, is a list of my potential income sources. I've included working at the family box factory, two possible income levels from this website, eventual Social Security payments, and a potential inheritance from my mother.

In Personal Capital, it's nice that you can add or remove various events to see how doing so affects your future. But if you remove an event, it's gone. You can't save it.

With OnTrajectory, you just toggle a button to see the difference. If you want to add, say, an inheritance back into the equation, you just click the button once more. What this means from a practical perspective is that you can enter several possible scenarios/events that you deem likely, then explore different possible futures. This is a very handy feature.

OnTrajectory also allows you to play with the assumptions “under the hood”. Three key variables are always instantly accessible: your retirement age, your Trajectory End Age (a.k.a. your projected date of death), and a projected inflation rate. (The default inflation rate in OnTrajectory is 3.00%. That's just slightly optimistic for me. I chose to change it to 3.18%, which is the U.S. long-term average. If I were extremely pessimistic, I might change it to something like 4.08%, which I think is the 50-year moving average — but don't quote me.)

You can also play with tax rates, investment contributions, investment returns, and more. As you might have noticed, you can enter start ages and end ages for most line items. If you want to explore different possible paths, you can enter additional age range possibilities without deleting your original item. Then you just toggle between the two lines to see the effects of, say, working longer.

OnTrajectory allows you to set specific goals, such as “I want my Trajectory to reach $1,500,000”. These goals then get plotted on your Trajectory graph. For instance, if I want to know when my net worth Trajectory will hit $1,500,000, the app will plot it on the ever-present graph. In this particular case, it says I should hit that goal on 11 November 2029.

So, as you can see, OnTrajectory is very similar to a lot of other retirement calculators out there except that it takes things to the next level. Anything the Personal Capital retirement tool can do, OnTrajectory can do better.

But wait! That's not all! OnTrajectory also allows users to create and print a variety of PDF reports. It includes a handy inflation calculator. And there's a nascent OnTrajectory community on Reddit where you can ask questions and share ideas.

Having said all of that, OnTrajectory isn't perfect.

Problems with OnTrajectory

As much as I love OnTrajectory, there's one key piece of the tool that I hate: the terminology. For me, it's confusing.

In this tool's parlance, your Trajectory is your projected future financial path. And your Trajectory for any given date is your net worth on that date. That makes total sense, right?

But individual accounts can have trajectories too. If my 401(k) has a Trajectory of $246,136 today, that's its balance today. So, maybe Trajectory actually means balance? I don't know. I'm confused.

Things get more confusing after you've been using the tool for a while. Your Trajectory is based on your initial parameters, not your current situation. The tool does plot a trajectory projection based on your current situation, but your Trajectory (with a capital T) is based on your starting assumptions.

(There's a logic behind this. OnTrajectory uses the Monte Carlo method to look into the future. It assumes that your current situation is one point on many possible projected paths, and that your circumstances will very likely be subject to “reversion to the mean”. By basing your Trajectory on your starting circumstances rather than your current circumstances — which generally improve with time — it's providing a more conservative/cautious approach to retirement planning.)

I understand that OnTrajectory uses the term “trajectory” to stay on-brand, but for somebody like me it creates more confusion than clarity. I'd prefer that existing standard definitions were used. If your Trajectory is your net worth, then call it your net worth. If Trajectory simply means “balance”, then use the word balance.

OnTrajectory is a fine name for the tool, but I don't see the need to cloud the issue by getting cute with naming conventions.

That's my main beef with OnTrajectory, but it has other minor quirks too.

There's a “Default Investments” account that cannot be deleted. (It's meant to be a catch-all for stray cash, I think. This is sort of like the “petty cash” account I use in Quicken.)

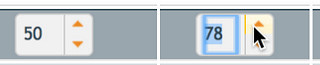

While attempting to enter my Basic Expenses line item, OnTrajectory refused to let me set its End Age to 79 (my projected end of life); it only let me set it to 78. (I was able to set everything else to 79 but not my Basic Expenses. Weird.) As a result, OnTrajectory believes I have $0 expenses during the last year of my life haha.

At one point, the OnTrajectory graph simply disappeared. I changed my projected date of death (or “Trajectory End Age” in the program's terms) and the graph vanished. I couldn't get it to come back. After trying a bunch of different things, I clicked the Undo button. I'm not sure what action I undid, but pressing the button brought back the graph.

To me, these “minor quirks” don't affect my overall impression of OnTrajectory. They're bugs (or features I don't like). They're likely to go away in the future. The terminology thing drives me nuts, but I suspect I might be the only person who is bothered by it. And it's not enough to dampen my enthusiasm for this tool.

The Bottom Line

So far, OnTrajectory is the best traditional retirement calculator I've found. (As I said, I like NewRetirement better, but it takes a different approach.) It's a comprehensive, complex tool — but the interface is never overwhelming.

If the interface does become overwhelming or confusing, OnTrajectory features extensive (and useful) documentation. In nearly every section of the screen, you can click on a little info button to bring up the on-line manual. This guide provides answers and tips on all of the functions and features. Impressive.

For me, the killer feature is that OnTrajectory not only allows you to save your data, but also to create and save multiple scenarios. You don't have to re-enter your data each time you want to check on your progress. And if you want to play with possibilities — what if I were to quit my job and take a more meaningful non-profit position? — it's super simple to do so…without trashing your existing info!

“We're all about the what-ifs,” Koska told me during our call last week. OnTrajectory is specifically designed to let users explore possible futures. “We let people play with a lot of variables, but our goal is for the interface to never become overwhelming.”

The bottom line? OnTrajectory is like the Personal Capital retirement calculator on steroids. It has everything I like about the PC tool, but is much more customizable. In fact, I like it so much that I signed up for a paid account!

The post Is OnTrajectory the best retirement calculator? appeared first on Get Rich Slowly.

from Finance https://www.getrichslowly.org/ontrajectory-retirement-calculator/

via http://www.rssmix.com/

0 notes

Text

Is OnTrajectory the best retirement calculator?

My colleagues, who are money nerds just like me, know that I'm obsessed with finding the best retirement calculator. I've been on this quest for years. As you'll learn later this week, my favorite retirement tool is (and has been) NewRetirement. But there are other great tools out there.

You really need to try OnTrajectory, Jillian from Montana Money Adventures told me last summer. It's great. She's been telling me that over and over ever since. (Meanwhile, Gwen from Fiery Millennials has also been pressuring me to try OnTrajectory.)

Last week, at long last, I had a chance to chat with Tyson Koska, the founder of OnTrajectory. During a 30-minute call, he walked me through setting up an account and playing with the tool's features. I'm impressed. NewRetirement is still my favorite tool, but OnTrajectory is damn close. And I can see how for some people, the latter may actually be a better choice.

Today, let's take a look at what makes OnTrajectory one of the best retirement calculators available on the web.

How OnTrajectory Started

The OnTrajectory origin story is similar to that of You Need a Budget.

Koska spent decades looking for a tool that would give him a high-level view of his financial future. I couldn't find one that I liked, he says. He didn't like their assumptions. He didn't like their interfaces. He didn't like their limited functionality.

Eventually, he took matters into his own hands. He built a complex spreadsheet to explore different variables and what-if scenarios. From there, he began coding Excel macros and small software tools. Over time, the current version of OnTrajectory evolved from his experimentation.

Just as YNAB grew out of Jesse Mecham's desire to build himself the perfect budgeting tool, OnTrajectory is a product of Koska's quest for the perfect retirement calculator. Over the years, it's morphed from a simple spreadsheet to a complex tool with a distinctive look and feel.

OnTrajectory is all about this graph:

That graph really dominates your tool, I told Koska on our call.

Exactly, he said. That's the whole point. That graph is always present at the top of your screen to show you your trajectory. Any time you make an adjustment to your assumptions any time that graph gets updated.

Because Koska considers himself a part of the growing FIRE community the group of folks who is interested in financial independence and early retirement OnTrajectory is built with their needs in mind. You want to retire by 40? Fine. OnTrajectory can handle that. You want some absurd saving rate like 90%? No problem. You can model pretty much any scenario you can imagine.

Getting Started

It's easy to get started with OnTrajectory. Once you provide login credentials, you're given two choices:

A quick-start wizard that asks only three questions before launching you into the tool.A more comprehensive guided entry process during which you manually enter your income, expenses, and existing investment accounts.

The former is quick and easy. The latter provides better results. As you can probably guess, I'm not a quick-start wizard sort of guy. I opted to use the longer guided entry process. It didn't take anywhere near the 30-minute projected time. (But that's probably because I already had my financial info gathered in one place.)

During the set-up process, OnTrajectory asks questions about your existing financial infrastructure and your goals for the future. It uses this info to populate three of its five navigation tabs. The guided entry asks you to:

Designate expected income, including regular salary, Social Security, pensions, rental income, and so on.Specify large, recurring expenses such as vehicle payments, housing payment, insurance premiums, property taxes, and the like.Enter current balances of major financial accounts like your Roth IRA and 401(k), regular brokerage accounts, and your bank accounts. (OnTrajectory does not automatically connect to your accounts. You must enter this info manually.)

You can add to or alter these numbers at any time. They're not set in stone, so don't be afraid of making mistakes.

OnTrajectory is free to use for fourteen days. (You don't even need to enter credit card info, which is awesome!) If you'd like to continue using the tool, however, you have to subscribe at $4.99/month (or $49/year).

Using OnTrajectory

OnTrajectory seems simple at first, but the more I worked with it, the more I appreciated how it handles complexity.

One of its strengths, for instance, is the ability to plot a variety of possible futures.

Our lives are dominated by uncertainty. Sure, there are likely paths that lie before each one of us, but there's plenty we don't know. Plus, a few times each decade, we reach major forks in the road to our future. Do I take this job or that job? Do I move to Savannah, Georgia or do I remain in Portland, Oregon? Should I draw Social Security at age 62 or wait until I can get maximum benefits at age 70?

Normally, it's tough to predict how your decisions will affect your financial future. With OnTrajectory, however, it's simple to explore these alternate dimensions. You can toggle any parameter at any time.

Here, for instance, is a list of my potential income sources. I've included working at the family box factory, two possible income levels from this website, eventual Social Security payments, and a potential inheritance from my mother.

In Personal Capital, it's nice that you can add or remove various events to see how doing so affects your future. But if you remove an event, it's gone. You can't save it.

With OnTrajectory, you just toggle a button to see the difference. If you want to add, say, an inheritance back into the equation, you just click the button once more. What this means from a practical perspective is that you can enter several possible scenarios/events that you deem likely, then explore different possible futures. This is a very handy feature.

OnTrajectory also allows you to play with the assumptions under the hood. Three key variables are always instantly accessible: your retirement age, your Trajectory End Age (a.k.a. your projected date of death), and a projected inflation rate. (The default inflation rate in OnTrajectory is 3.00%. That's just slightly optimistic for me. I chose to change it to 3.18%, which is the U.S. long-term average. If I were extremely pessimistic, I might change it to something like 4.08%, which I think is the 50-year moving average but don't quote me.)

You can also play with tax rates, investment contributions, investment returns, and more. As you might have noticed, you can enter start ages and end ages for most line items. If you want to explore different possible paths, you can enter additional age range possibilities without deleting your original item. Then you just toggle between the two lines to see the effects of, say, working longer.

OnTrajectory allows you to set specific goals, such as I want my Trajectory to reach $1,500,000. These goals then get plotted on your Trajectory graph. For instance, if I want to know when my net worth Trajectory will hit $1,500,000, the app will plot it on the ever-present graph. In this particular case, it says I should hit that goal on 11 November 2029.

So, as you can see, OnTrajectory is very similar to a lot of other retirement calculators out there except that it takes things to the next level. Anything the Personal Capital retirement tool can do, OnTrajectory can do better.

But wait! That's not all! OnTrajectory also allows users to create and print a variety of PDF reports. It includes a handy inflation calculator. And there's a nascent OnTrajectory community on Reddit where you can ask questions and share ideas.

Having said all of that, OnTrajectory isn't perfect.

Problems with OnTrajectory

As much as I love OnTrajectory, there's one key piece of the tool that I hate: the terminology. For me, it's confusing.

In this tool's parlance, your Trajectory is your projected future financial path. And your Trajectory for any given date is your net worth on that date. That makes total sense, right?

But individual accounts can have trajectories too. If my 401(k) has a Trajectory of $246,136 today, that's its balance today. So, maybe Trajectory actually means balance? I don't know. I'm confused.

Things get more confusing after you've been using the tool for a while. Your Trajectory is based on your initial parameters, not your current situation. The tool does plot a trajectory projection based on your current situation, but your Trajectory (with a capital T) is based on your starting assumptions.

(There's a logic behind this. OnTrajectory uses the Monte Carlo method to look into the future. It assumes that your current situation is one point on many possible projected paths, and that your circumstances will very likely be subject to reversion to the mean. By basing your Trajectory on your starting circumstances rather than your current circumstances which generally improve with time it's providing a more conservative/cautious approach to retirement planning.)

I understand that OnTrajectory uses the term trajectory to stay on-brand, but for somebody like me it creates more confusion than clarity. I'd prefer that existing standard definitions were used. If your Trajectory is your net worth, then call it your net worth. If Trajectory simply means balance, then use the word balance.

OnTrajectory is a fine name for the tool, but I don't see the need to cloud the issue by getting cute with naming conventions.

That's my main beef with OnTrajectory, but it has other minor quirks too.

There's a Default Investments account that cannot be deleted. (It's meant to be a catch-all for stray cash, I think. This is sort of like the petty cash account I use in Quicken.)While attempting to enter my Basic Expenses line item, OnTrajectory refused to let me set its End Age to 79 (my projected end of life); it only let me set it to 78. (I was able to set everything else to 79 but not my Basic Expenses. Weird.) As a result, OnTrajectory believes I have $0 expenses during the last year of my life haha.At one point, the OnTrajectory graph simply disappeared. I changed my projected date of death (or Trajectory End Age in the program's terms) and the graph vanished. I couldn't get it to come back. After trying a bunch of different things, I clicked the Undo button. I'm not sure what action I undid, but pressing the button brought back the graph.

To me, these minor quirks don't affect my overall impression of OnTrajectory. They're bugs (or features I don't like). They're likely to go away in the future. The terminology thing drives me nuts, but I suspect I might be the only person who is bothered by it. And it's not enough to dampen my enthusiasm for this tool.

The Bottom Line

So far, OnTrajectory is the best traditional retirement calculator I've found. (As I said, I like NewRetirement better, but it takes a different approach.) It's a comprehensive, complex tool but the interface is never overwhelming.

If the interface does become overwhelming or confusing, OnTrajectory features extensive (and useful) documentation. In nearly every section of the screen, you can click on a little info button to bring up the on-line manual. This guide provides answers and tips on all of the functions and features. Impressive.

For me, the killer feature is that OnTrajectory not only allows you to save your data, but also to create and save multiple scenarios. You don't have to re-enter your data each time you want to check on your progress. And if you want to play with possibilities what if I were to quit my job and take a more meaningful non-profit position? it's super simple to do sowithout trashing your existing info!

We're all about the what-ifs, Koska told me during our call last week. OnTrajectory is specifically designed to let users explore possible futures. We let people play with a lot of variables, but our goal is for the interface to never become overwhelming.

The bottom line? OnTrajectory is like the Personal Capital retirement calculator on steroids. It has everything I like about the PC tool, but is much more customizable. In fact, I like it so much that I signed up for a paid account!

Author: J.D. Roth

In 2006, J.D. founded Get Rich Slowly to document his quest to get out of debt. Over time, he learned how to save and how to invest. Today, he's managed to reach early retirement! He wants to help you master your money and your life. No scams. No gimmicks. Just smart money advice to help you reach your goals.

https://www.getrichslowly.org/ontrajectory-retirement-calculator/

0 notes

Last Seen Blogs

josephinebrause

Messy lines and suffering

mkrolloffsin

M & K Rolloffs

itsmadds

madds

rumiko-sama

Let me die already