#Central banking

Note

If the King/Queen of Westeros decided to implement a national bank of Westeros, how would they navigate relationships with the Iron Bank and any perceived competition? Thinking of the same way that the Rogare Bank might have fallen to Faceless Man assassinations?

I would personally recommend a more cooperative policy, because there are definite ways that a Westerosi central bank could be of benefit to the Iron Bank - especially since central banks don't tend to compete with merchant or commercial banks for the same kind of business.

To begin with, the existence of a central bank acting as lender of last resort to Westerosi moneylenders and merchants is going to be good for the Iron Bank's business in Westeros, because that's going to massively reduce the risk of default, which would mean the Iron Bank's loans would see a higher rate of return even at lower interest rates, and likely would lead to an increased volume of business, as more people would be able to afford to take out loans from the Iron Bank.

If the Westerosi central bank is anything like the central banks of Early Modern Europe, it might be quite possible that the Iron Bank would become a minority shareholder in the Westerosi central bank, and quite likely would be one of the central bank's major customers when it comes to the sale of royal bonds - if only because the existence of a central bank would make Westerosi public debt a much sounder investment than under the medieval model.

#asoiaf#asoiaf meta#westerosi economic policy#medieval finance#medieval economics#iron bank#medieval banking#early modern state-building#early modern finance#central banking

35 notes

·

View notes

Text

There were 173 Banks around the World that failed this week – and went unreported by the Mainstream Media.

The Rothschild Banks in controlled collapse, including the US Federal Reserve:

Afghanistan: Bank of Afghanistan

Albania: Bank of Albania

Algeria: Bank of Algeria

Argentina: Central Bank of Argentina

Armenia: Central Bank of Armenia

Aruba: Central Bank of Aruba

Australia: Reserve Bank of Australia

Austria: Austrian National Bank

Azerbaijan: Central Bank of Azerbaijan Republic

Bahamas: Central Bank of The Bahamas

Bahrain: Central Bank of Bahrain

Bangladesh: Bangladesh Bank

Barbados: Central Bank of Barbados

Belarus: National Bank of the Republic of Belarus

Belgium: National Bank of Belgium

Belize: Central Bank of Belize

Benin: Central Bank of West African States (BCEAO)

Bermuda: Bermuda Monetary Authority

Bhutan: Royal Monetary Authority of Bhutan

Bolivia: Central Bank of Bolivia

Bosnia: Central Bank of Bosnia and Herzegovina

Botswana: Bank of Botswana

Brazil: Central Bank of Brazil

Bulgaria: Bulgarian National Bank

Burkina Faso: Central Bank of West African States (BCEAO)

Burundi: Bank of the Republic of Burundi

Cambodia: National Bank of Cambodia

Came Roon: Bank of Central African States

Canada: Bank of Canada – Banque du Canada

Cayman Islands: Cayman Islands Monetary Authority

Central African Republic: Bank of Central African States

Chad: Bank of Central African States

Chile: Central Bank of Chile

China: The People’s Bank of China

Colombia: Bank of the Republic

Comoros: Central Bank of Comoros

Congo: Bank of Central African States

Costa Rica: Central Bank of Costa Rica

Côte d’Ivoire: Central Bank of West African States (BCEAO)

Croatia: Croatian National Bank

Cuba: Central Bank of Cuba

Cyprus: Central Bank of Cyprus

Czech Republic: Czech National Bank

Denmark: National Bank of Denmark

Dominican Republic: Central Bank of the Dominican Republic

East Caribbean Area: Eastern Caribbean Central Bank

Ecuador: Central Bank of Ecuador

Egypt: Central Bank of Egypt

El Salvador: Central Reserve Bank of El Salvador

Equatorial Guinea: Bank of Central African States

Estonia: Bank of Estonia

Ethiopia: National Bank of Ethiopia

European Union: European Central Bank

Fiji: Reserve Bank of Fiji

Finland: Bank of Finland

France: Bank of France

Gabon: Bank of Central African States

The Gambia: Central Bank of The Gambia

Georgia: National Bank of Georgia

Germany: Deutsche Bundesbank

Ghana: Bank of Ghana

Greece: Bank of Greece

Guatemala: Bank of Guatemala

Guinea Bissau: Central Bank of West African States (BCEAO)

Guyana: Bank of Guyana

Haiti: Central Bank of Haiti

Honduras: Central Bank of Honduras

Hong Kong: Hong Kong Monetary Authority

Hungary: Magyar Nemzeti Bank

Iceland: Central Bank of Iceland

India: Reserve Bank of India

Indonesia: Bank Indonesia

Iran: The Central Bank of the Islamic Republic of Iran

Iraq: Central Bank of Iraq

Ireland: Central Bank and Financial Services Authority of Ireland

Israel: Bank of Israel

Italy: Bank of Italy

Jamaica: Bank of Jamaica

Japan: Bank of Japan

Jordan: Central Bank of Jordan

Kazakhstan: National Bank of Kazakhstan

Kenya: Central Bank of Kenya

Korea: Bank of Korea

Kuwait: Central Bank of Kuwait

Kyrgyzstan: National Bank of the Kyrgyz Republic

Latvia: Bank of Latvia

Lebanon: Central Bank of Lebanon

Lesotho: Central Bank of Lesotho

Libya: Central Bank of Libya (Their most recent conquest)

Uruguay: Central Bank of Uruguay

Advertisements

REPORT THIS AD

Lithuania: Bank of Lithuania

Luxembourg: Central Bank of Luxembourg

Macao: Monetary Authority of Macao

Macedonia: National Bank of the Republic of Macedonia

Madagascar: Central Bank of Madagascar

Malawi: Reserve Bank of Malawi

Malaysia: Central Bank of Malaysia

Mali: Central Bank of West African States (BCEAO)

Malta: Central Bank of Malta

Mauritius: Bank of Mauritius

Mexico: Bank of Mexico

Moldova: National Bank of Moldova

Mongolia: Bank of Mongolia

Montenegro: Central Bank of Montenegro

Morocco: Bank of Morocco

Mozambique: Bank of Mozambique

Namibia: Bank of Namibia

EVERYTHING is going to crash!

Are You Prepared? 🤔

#pay attention#educate yourself#educate yourselves#reeducate yourself#knowledge is power#reeducate yourselves#think for yourself#think for yourselves#think about it#do your homework#do your research#do your own research#question everything#ask yourself questions#ask yourself#central banking#everything is going to crash#everything is falling apart

112 notes

·

View notes

Text

Loving how all these socialists complain about how we have "free-market capitalism" despite the fact that the entire economy, the price of goods, services, and wages all teeter on the decisions of a handful of government employees.

137 notes

·

View notes

Text

Former prominent Investment Banker George Green who is sadly no longer with us explaining from his knowledge from within the inside of how the global agenda would unfold.🤔

#pay attention#wake up america#wake up people#wake up world#wake the fuck up#wake up#government lies#government corruption#central banking#educate yourselves#educate yourself#do your own research#do your research#do your homework#did you know#knowledge is power

75 notes

·

View notes

Text

[Photo source]

🇮🇱🇺🇸 🚨 CREDIT RATING ORGANIZATION, MOODY'S ANALYTICS PREDICTS HIGH DEFICITS AND INFLATION FOR ISRAEL

The credit rating agency, Moody's Analytics is predicting higher inflation and widening deficits for the Israeli State in a report released on Monday morning.

According to the Moody's report, the Israeli State can expect its deficit to widen to 3.5% by the end of 2023, and widen further to 7.8% in 2024.

Moody's further expects inflation rates to rise considerably to 6.8% in 2024, with GDP growth rates reduced to only 1.4%.

This directly contradicts predictions by the Bank of Israel, the occupation's central bank, which claimed the Israeli interest rate would remain flat at 4.75%, with expected inflation rates of 2.5% and GDP growth of 2.8%.

Last week, Moody's Analytics said it would be placing Israel's A1 foreign-currency and local-currency credit rating in review to consider how the events since October 7th are affecting the Israeli economy.

According to a separate report from the S&P, the Israeli economy can expect a 5% contraction in the Fourth Quarter of 2023.

"The change of outlook to stable from positive reflects a deterioration of Israel’s governance, as illustrated by the recent events around the government’s proposal for overhauling the country’s judiciary," the statement by Moody's Analytics said.

#source1

#source2

@WorkerSolidarityNews

#israel#israel news#bank of israel#central banking#moodys analytics#economy#israeli economy#gaza war#gaza news#gaza#gaza strip#economics#news#politics#war#war news#geopolitics#middle east news#middle east#world news#international news#global news#WorkerSolidarityNews#international affairs#international politics#global politics#latest news

8 notes

·

View notes

Text

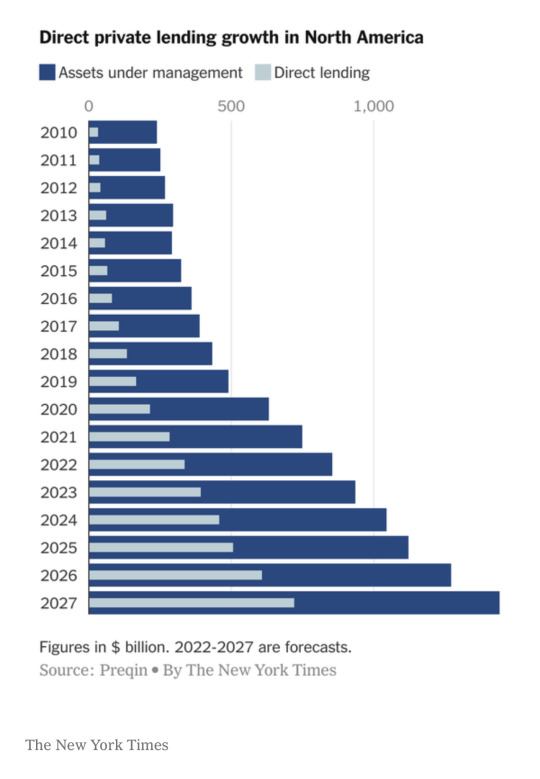

Bank Turmoil Is Paving the Way for Even Bigger ‘Shadow Banks’

The market for loans from non-bank firms like Apollo and Blackstone is booming. A crisis in regional lenders could accelerate it.

https://www.nytimes.com/2023/05/06/business/dealbook/bank-crisis-shadow-banks.html?searchResultPosition=5 #private_equity #privatedebt #privatecredit #debt #loans #Banking #investor #ennovance

#privateequity#ennovance#chemicals#investor#economy#loan#debt#equity#pe#investors#private credit#private debt#central banking#banking#credit#shadow banking

14 notes

·

View notes

Text

People causing a run on the bank because their accounts were only ensured up to $250,000.:

Me who only has two digits in my bank account:

7 notes

·

View notes

Text

youtube

When money drives almost all activity on the planet, it’s essential that we understand it. The documentary 97% Owned aims to answer questions like: Where does the money come from? Who creates it? Who decides how it gets used? And what does that mean for the millions of ordinary people who suffer when money and finance break down?

97% Owned reveals how the creation of credit and the mystery that surrounds it. The documentary goes at the root of our current social and economic crisis. Referring to the 97% of the world’s money supply that is represented by credit, this thought-provoking film presents serious research and verifiable evidence on our economic and financial system. Featuring frank interviews and commentary from economists, campaigners and former bankers, it exposes the privatized, debt-based monetary system that gives banks the power to create money, shape the economy, cause crises and push house prices out of reach. Fact-based and clearly explained, 97% Owned demonstrates how the power to create money is the piece of the puzzle that economists were missing when they failed to predict the crisis.

1 note

·

View note

Photo

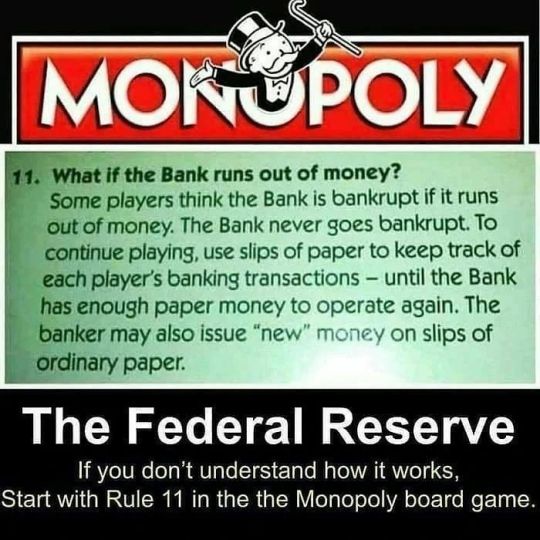

#Info - Is the bank system sound?

The institutions that are deemed “too big to fail” will always be bailed out. In his book, “Conspiracy of the Rich: The 8 New Rules of Money,” Robert Kiyosaki wrote that “bailouts are the name of the game.”

#gentlemans code#info#central banking#bank system#svb failure#finance#silicon valley bank#banking#moral hazard#economic crisis#robert kiyosaki#rich dad education#rich dad poor dad#bailout#lehman brothers#bear sterns

2 notes

·

View notes

Text

5 notes

·

View notes

Text

The Rothschilds and Rockefellers own everything. Even our own Government.

3 notes

·

View notes

Note

Could the Iron Throne be able to issue bonds, to finance its expenses, instead of going to the Iron Bank for a loan?

A government issuing bonds is the same thing as the government taking out a loan. The main difference is that, in the case of issuing a bond, the government is spreading out its borrowing between many lenders by selling bonds on the open market to anyone who wants to buy them rather than having that loan owed to a single entity like the Iron Bank. This means that the government is less beholden to any one creditor and it's less likely that the government's creditors can use their economic leverage to affect government policy.

The second advantage of structuring government debt through bonds is that it allows the government to break its total borrowing needs into smaller, more affordable units. Very few financial institutions would have had the capital to finance the £1,200,000 that made up the government's inaugural loan at the Bank of England in 1690 - but a lot more people could afford to lend the government £10, £25, £50, or £100 pounds.

Between this and later innovations in marketing bonds to the general public, the market for government debt was massively expanded. Not only did this create a class of rentiers who were now personally invested in the government's success, but it also immediately deepened the capital markets by creating a large supply of stable assets that could be bought and sold and borrowed against. While some of the shortcomings of the Hamilton musical and Chernow's biography have become more obvious in hindsight, they're not wrong about the impact of Hamilton's policies as Treasury Secretary on the development of the American economy.

The difficulty facing the Iron Throne in adapting an early modern system of government finance is that it doesn't have the state capacity to run this kind of an operation: it doesn't have a central bank to act as the government's marketer, issuer of banknotes, and lender of last resort; it doesn't have a sinking fund to manage the level and price of debt; it hasn't issued charters to merchant's guilds or joint-stock companies that could combine the small capital of individuals and thus more easily afford to buy bonds; and it doesn't have enough literate people who've studied accounting to staff a royal bureaucracy large enough to coordinate and keep records of all of this economic activity.

#asoiaf meta#asoiaf#medieval banking#medieval economics#medieval finance#early modern finance#westerosi economic development#early modern economy#central banking#westerosi economic policy#early modern state building

27 notes

·

View notes

Text

Does this sound familiar? 🤔

#pay attention#educate yourself#educate yourselves#reeducate yourself#knowledge is power#reeducate yourselves#government corruption#federal reserve#central banking

114 notes

·

View notes

Text

Bank of England....

Hire me.

2 notes

·

View notes

Link

#sick of this#free speech#free speech gone#america is fucked#american politics#jpmorgan#central banking#private banking

4 notes

·

View notes

Text

US regional banks struggle to break free from government life support

Lenders still tapping hundreds of billions of dollars of funding that shored industry up during recent crisis

https://www.ft.com/content/03f3dac0-5396-48a6-ad02-d622f748fd5d

https://twitter.com/CNBC/status/1646206923858145280/video/1

#ennovance#privateequity#economy#chemicals#debt#equity#investors#central banking#investor#pe#loan#shadow banking#bank

6 notes

·

View notes

Last Seen Blogs

bitch1301

🌺🌹🌻🌷

jessylycnh

Titleless

visceryl

A Writing Blog

aracelyadc

multishipper but always bmblb