#NBFCs

Link

Explore the technologies enhancing Financial Services and BFSI sector including the Financial Services cloud.

Features including account administration, financial planning tools, portfolio management, and compliance monitoring are available in the Salesforce Financial Services Cloud. To offer a complete solution for financial institutions, it also interfaces with other Salesforce products like Marketing Cloud and Sales Cloud.

#salesforce wealth management#Financial Services Cloud#Financial Services Cloud Trends#Salesforce Financial Services Cloud#Future Technolgy#Financial Services#Technolgy Trends#Artificial intelligence#Low-Code#No-Code#Low-Code Solutions#No-Code Solutions#Financial institutions#NBFCs#Assets management#Cloud implementation#Cloud-based infrastructure#Technology Adaptation#AWS financial services#Financial cloud salesforce#Cloud financial services#Salesforce for financial advisors#Financial cloud computing#Cloud based financial services#Salesforce finance#Salesforce FSC

2 notes

·

View notes

Text

Introducing Abhay Bhutada: The Recipient of the Lokmat Maharashtrian Of The Year 2024 Award

Abhay Bhutada, MD of Poonawalla Fincorp Limited (PFL), recently attained the prestigious Lokmat Maharashtrian Of The Year 2024 accolade, underscoring his exceptional leadership and profound influence on the finance industry and broader society. His narrative embodies resilience, innovation, and unwavering dedication, significantly reshaping the trajectory of finance and societal impact.

Innovative Trailblazing and Progress

Hailing from the vibrant city of Latur, Maharashtra, Abhay Bhutada embarked on his professional journey over fifteen years ago. Starting as an SME Finance Professional at Bank of India in 2010, Bhutada's entrepreneurial drive swiftly propelled him to establish TAB Capital Limited in 2016, a digital-lending Non-Banking Financial Company (NBFC) specializing in retail loans such as MSME and consumer lending.

Transitioning from traditional banking to digital finance marked a pivotal moment in Bhutada's career trajectory. Under his visionary stewardship, TAB Capital flourished, emerging as a frontrunner in the digital lending landscape. Leveraging cutting-edge technology and strategic insights, Bhutada steered TAB Capital to profitability at an unprecedented pace, culminating in its acquisition by the esteemed Poonawalla Group in 2019.

Assuming leadership as the Managing Director & CEO of Poonawalla Fincorp, Bhutada continued to spearhead innovation and transformation. His unwavering pursuit of excellence propelled Poonawalla Fincorp to unprecedented heights, securing an "AAA" external credit rating from CRISIL Ratings Limited and CARE Ratings Limited.

In the fiscal year 2023, Abhay Bhutada's salary of 78.1 crore, underscored his significant contributions to the company, solidifying his position as one of India's most highly compensated managing directors.

Also Read: Why Did Abhay Bhutada Consider Fy24 A Year Of Significant Growth Across All Business Parameters?

A Compassionate Leader

Beyond his corporate triumphs, Abhay Bhutada is deeply committed to catalyzing positive societal change. His engagement in industry forums and corporate social responsibility initiatives underscores his dedication to impactful change. Bhutada's philanthropic endeavors have earned him esteemed accolades such as Young Entrepreneur of India 2017, Promising Entrepreneur of India 2019, and Global Indian of the Year 2023.

His philanthropic initiatives encompass diverse domains, from bolstering education and healthcare programs to advocating environmental conservation efforts. Bhutada's ethos of giving back to the community epitomizes a leadership philosophy rooted in empathy and social responsibility.

Acknowledging Influence and Excellence

Abhay Bhutada's meteoric ascent in the finance sector has garnered widespread recognition. In addition to his substantial remuneration and net worth, Bhutada's influence transcends boardroom boundaries. His strategic foresight and business acumen have earned him numerous accolades, including Lokmat Maharashtrian Of The Year 2024, Young Entrepreneur of India 2017, Promising Entrepreneur of India 2019, and Global Indian of the Year 2023.

Such recognition underscores Bhutada's exceptional leadership and contributions to both the finance industry and society. His ability to navigate challenges with integrity and foresight serves as a beacon for aspiring entrepreneurs and seasoned professionals alike.

Also Read: Mastering Asset Quality in 2025: Exploring Insights and Strategies

Inspiring Future Generations

Abhay Bhutada's journey from humble beginnings to becoming a titan in the finance sector serves as an inspiration to aspiring entrepreneurs and industry veterans alike. His unwavering pursuit of excellence and commitment to leveraging technology for societal welfare set a benchmark for future generations.

As we reflect on Bhutada's journey and achievements, we are reminded of the transformative potential of vision, leadership, and purpose in sculpting a brighter future for all. His legacy promises to inspire future generations to push boundaries, both in business and in effecting positive social change.

Also Read: Why Did Abhay Bhutada Consider Fy24 A Year Of Significant Growth Across All Business Parameters?

Concluding Remarks

Abhay Bhutada's indomitable spirit, innovative mindset, and unwavering dedication position him as a pioneering force reshaping the contours of finance and society. As he continues to chart new territories and catalyze positive transformation, Bhutada's influence will echo for generations to come. With his visionary leadership at the helm, the possibilities are boundless, and the journey, endlessly inspiring.

As we celebrate Abhay Bhutada's triumphs and honor his contributions, we are reminded that true success lies not merely in personal achievements but also in the enduring impact we leave on the world. Bhutada's narrative serves as a testament to the transformative power of vision, leadership, and social responsibility—a narrative that inspires and empowers us all to strive for excellence and craft a better future.

0 notes

Text

Redefining Finance Through Innovation With Poonawalla Fincorp

In the dynamic landscape of finance, Poonawalla Fincorp emerges as a trailblazer, intertwining innovation with a profound focus on customer satisfaction to redefine success. As a premier Non-Banking Financial Company (NBFC), it spearheads the industry by prioritizing quality, embracing digital transformation, amalgamating financial models, practicing proactive risk management, and securing expert endorsements.

Elevating Quality Over Quantity

Poonawalla Fincorp distinguishes itself by placing paramount importance on its customers, adopting a targeted approach that focuses on individuals with a CIBIL score of 700 and above, complemented by formal income. This meticulous strategy ensures a clientele base with a proven track record of financial responsibility, effectively minimizing default risks and elevating the quality of its loan portfolio. Managing Director Abhay Bhutada underscores the significance of this customer-centric ethos in driving sustainable growth and nurturing enduring relationships with clients.

Also Read: The Cemented Roads Between Adar Poonawalla & Abhay Bhutada

Streamlining Processes for Enhanced Efficiency

Recognizing the transformative potential of digital innovation, Poonawalla Fincorp has embarked on a journey to revolutionize its operations. Through digital sourcing and end-to-end digital agreements, borrowers can seamlessly apply for loans from the comfort of their homes, significantly reducing paperwork and turnaround times. This unwavering commitment to digital transformation not only enhances operational efficiency but also elevates the overall customer experience, positioning Poonawalla Fincorp as an industry leader at the forefront of technological advancement.

Maximizing Competitive Advantage

Poonawalla Fincorp's success is deeply rooted in its ability to harness the strengths of diverse financial models, seamlessly blending elements of fintech, NBFC, and traditional banking services. Leveraging fintech, the company delivers a user-friendly digital experience, enhancing accessibility and convenience for borrowers. Meanwhile, its NBFC status enables flexible, cash flow-based lending, catering to a wide spectrum of financial needs. Additionally, by adopting the structural framework and client targeting strategies akin to traditional banks, Poonawalla Fincorp operates with lower overhead costs, allowing it to offer competitive interest rates and attractive loan terms to its customers. This strategic fusion of financial models not only enhances operational efficiency but also ensures that Poonawalla Fincorp remains agile and adaptable in meeting the ever-evolving demands of the market.

Also Read: Strategies For NBFCs In A Saturated Market

Safeguarding Assets and Reputation

In the volatile and unpredictable world of finance, effective risk management is paramount for ensuring long-term stability and success. Poonawalla Fincorp adopts a proactive approach to mitigate risks, employing strategies such as early write-offs and selective customer onboarding. By identifying and addressing potential risks at an early stage, the company maintains a healthy asset quality and solidifies its reputation as a reliable and trustworthy lender. Abhay Bhutada, MD, emphasizes the critical role of prudent risk management in safeguarding Poonawalla Fincorp's long-term viability and earning the trust of its stakeholders. By prioritizing risk mitigation and maintaining stringent risk assessment processes, Poonawalla Fincorp remains resilient in the face of market fluctuations and upholds its commitment to financial stability and integrity.

Endorsements From Industry Experts

The accolades and endorsements bestowed upon Poonawalla Fincorp by industry experts, such as Manish Chaudhari, Head of Retail Assets, serve as a testament to the company's innovative strategies and unwavering commitment to customer satisfaction. Chaudhari commends Poonawalla Fincorp for its forward-thinking initiatives, particularly in areas such as early write-offs and selective customer onboarding, which play a pivotal role in preserving the company's asset quality and fostering customer loyalty. With a proven track record of successful ventures, including Poonawalla Finance, Poonawalla Fincorp stands as a shining example of innovation and excellence in the financial sector. These endorsements not only reinforce the company's reputation as a leader in the industry but also inspire confidence among customers and stakeholders alike, further solidifying Poonawalla Fincorp's position as a trailblazer in the financial landscape.

Also Read: Driving Financial Inclusion: The Impact of Acquiring Magma Fincorp on Poonawalla Fincorp

Conclusion

Poonawalla Fincorp's ascent in the NBFC sector is a testament to its unwavering commitment to innovation, customer satisfaction, and prudent risk management. By prioritizing quality over quantity, embracing digital transformation, leveraging a fusion of financial strengths, and implementing proactive risk management practices, the company has established itself as a trailblazer in the financial industry. As Poonawalla Fincorp continues to push the boundaries of innovation and excellence, it is poised to redefine the standards of success and shape the future of finance for years to come.

With its customer-centric approach, innovative strategies, and unwavering commitment to excellence, Poonawalla Fincorp stands ready to lead the financial industry into a new era of growth and prosperity. As it continues to innovate and adapt to the changing landscape, Poonawalla Fincorp will undoubtedly leave an indelible mark on the world of finance, setting new standards of success and inspiring others to follow suit.

0 notes

Text

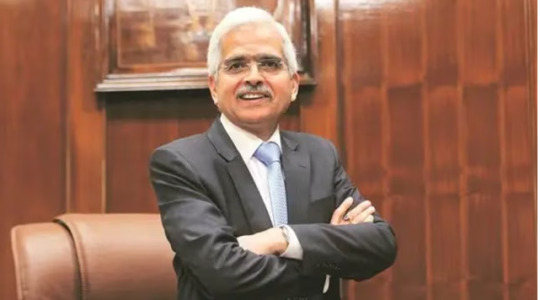

Insights from RBI Governor Shaktikanta Das

In a recent address, Reserve Bank of India (RBI) Governor Shaktikanta Das shared valuable insights on various aspects crucial to India’s economic landscape.

1. Growth Outlook: Das highlighted a positive growth trajectory for the Indian economy, with the National Statistical Office (NSO) forecasting a 7.6% growth in FY24. He emphasized that this sustained growth, averaging 8% over a three-year period, signifies an increase in the country’s potential growth.

2. Financial Stability: Addressing the importance of governance and regulatory compliance, Das stressed that Non-Banking Financial Companies (NBFCs) and other financial entities must prioritize these factors. Considering their operation with public funds, maintaining quality governance is imperative. He emphasized that ensuring financial stability is a collective responsibility, with the RBI committed to engaging with financial entities.

3. Forex Reserves Management: Das highlighted India’s record-high foreign exchange reserves, reaching $645.6 billion as of March 29. He discussed the impact of geopolitical events such as the Ukraine-Russia conflict, which led to temporary fluctuations in reserves. Emphasizing prudent management, Das assured that India’s forex reserves were utilized judiciously, serving as a robust safeguard during times of economic uncertainty.

Overall, Das’s insights provide valuable perspectives on growth, financial stability, and forex management crucial for India’s economic resilience and prosperity.

0 notes

Text

In the dynamic world of finance, staying abreast of regulatory changes and market movements is paramount. The recent actions by the Reserve Bank of India (RBI) have sent ripples across the financial sector, particularly impacting non-banking financial companies (NBFCs) like IIFL and JM Financials. Here's a comprehensive overview of these developments and their implications on the NBFCs share market.

The RBI, as the apex regulatory body in India's financial sector, plays a pivotal role in maintaining stability and fostering growth. Its recent actions have been directed towards tightening regulatory oversight, particularly in the NBFC segment, to mitigate systemic risks and safeguard investor interests.

In response to evolving market dynamics and emerging challenges, the RBI has rolled out a series of measures aimed at enhancing transparency, strengthening governance frameworks, and bolstering risk management practices within NBFCs. These initiatives seek to promote financial stability, enhance market integrity, and foster confidence among stakeholders.

0 notes

Text

A Guide To Mastering Dollar Cost Averaging

Dollar Cost Averaging (DCA) might sound like a financial jargon, but don't let that intimidate you. It's a straightforward and effective strategy that anyone can use to build wealth over time. So, without further ado, let's dive into this simple yet powerful investment technique.

What is Dollar Cost Averaging (DCA)?

DCA is a strategy where you regularly invest a fixed amount of money into an investment, such as stocks or mutual funds, regardless of the current price. It's a hands-off approach that lets you take advantage of market fluctuations without trying to time the market. Whether you're a seasoned investor or just starting, DCA can be your best friend.

Also Read: Investor's Playbook on Taxation Strategies

Why DCA Works

The beauty of DCA lies in its simplicity. Here's why it's a winning strategy:

1. Risk Mitigation

DCA spreads your investment over time, reducing the risk associated with investing a lump sum all at once. You don't have to stress about market timing, as you're buying when the market is both high and low.

2. Emotional Discipline

When you're DCA-ing, you're less likely to make impulsive decisions based on market fluctuations. You stay calm and collected, which is key to long-term success in the market.

3. Consistency Pays Off

By investing a fixed amount at regular intervals, you benefit from the power of compounding. Over time, this consistent approach can turn small, regular investments into substantial wealth.

How to Get Started with DCA

Now that you understand why DCA is a smart choice, here's how to get started:

1. Choose Your Investment

Decide what you want to invest in. It could be a particular stock, a mutual fund, or an exchange-traded fund (ETF). Make sure you've done your research and understand the basics of your chosen investment.

2. Set a Budget

Determine how much you can comfortably invest on a regular basis. Whether it's weekly, monthly, or quarterly, consistency is the key.

3. Automate Your Investments

Set up an automatic transfer from your bank account to your chosen investment. This ensures you stick to your plan, no matter what's happening in the market.

4. Stay Informed

Keep an eye on your investments, but don't obsess over them. DCA is about playing the long game, so resist the temptation to make knee-jerk reactions to market news.

Tips for Success

To master DCA, here are a few additional tips to keep in mind

1. Keep an Eye on Fees

Be mindful of any fees associated with your chosen investment. High fees can eat into your returns over time.

2. Be Patient

DCA is a long-term strategy. It might take some time to see substantial gains, so be patient and stick to your plan.

3. Reevaluate Your Strategy

Life circumstances change. As your financial situation evolves, consider adjusting your DCA plan accordingly.

Also Read: The Role of Bots, Assistants, AIs in Customer Communication

Conclusion

Dollar Cost Averaging is an easy, no-nonsense approach to building wealth through investing. It takes away the stress of market timing and helps you stay disciplined, ensuring that your financial future is on the right track. So, if you're looking for a way to grow your wealth without the complexity, DCA is your go-to strategy.

0 notes

Text

Innovation in Finance: Abhay Bhutada's Guidelines for MSME Loan Growth

Micro, Small, and Medium Enterprises (MSMEs) play a pivotal role in driving economic growth, providing employment opportunities, and fostering innovation. However, one of the significant challenges faced by MSMEs in accessing adequate financing to fuel their expansion and development initiatives. Enhancing loan prospects in the MSME sector is crucial for their sustained growth. Abhay Bhutada, a luminary in finance, provides a roadmap for MSME loan growth through groundbreaking guidelines. This article navigates through the landscape of financial innovation.

The Essence of Innovation in Finance

Innovation in finance is not merely a buzzword; it is a fundamental driver of economic progress. As markets evolve and consumer needs change, financial institutions must adapt to stay relevant. For MSMEs, often facing unique challenges in accessing credit, innovative financial solutions are crucial for survival and expansion.

Innovations in finance encompass a wide range of strategies and technologies. From fintech solutions to novel risk assessment methodologies, staying ahead of the curve is essential for financial institutions. Abhay Bhutada, MD of Poonawalla Fincorp recognizes this and emphasizes the need for continuous evolution in the financial sector to meet the diverse and evolving needs of MSMEs.

Understanding MSME Loan Growth Challenges

MSMEs form the backbone of many economies, contributing significantly to employment and GDP. However, these enterprises often struggle to secure loans due to their size, lack of collateral, and limited financial history. Traditional lending practices can be cumbersome and restrictive, hindering the growth potential of these businesses.

Abhay Bhutada identifies these challenges and stresses the importance of rethinking the approach to MSME lending. Recognizing that one size does not fit all, his guidelines advocate for flexible and tailored solutions that cater to the unique characteristics of each MSME.

Also Read: Abhay Bhutada's Plan to Lower Lending Rates at Poonawalla Fincorp

Guidelines for MSME Loan Growth

1. Data-Driven Decision Making

Abhay Bhutada places a strong emphasis on leveraging data for making informed lending decisions. In the age of big data, financial institutions can harness the power of analytics to assess creditworthiness more accurately. By analyzing transaction history, market trends, and other relevant data points, lenders can make more informed decisions, enabling them to extend credit to deserving MSMEs.

2. Fintech Integration

Integrating fintech solutions is a cornerstone of Bhutada's guidelines. Fintech platforms streamline the lending process, making it faster, more efficient, and cost-effective. From online application processes to digital documentation, embracing technology not only enhances the borrower's experience but also allows lenders to reach a broader spectrum of MSMEs.

3. Risk Mitigation Strategies

Mitigating risks is integral to successful lending, especially when dealing with smaller enterprises. Abhay Bhutada advocates for the development and implementation of robust risk assessment models. By identifying potential risks early on, financial institutions can offer more favorable terms to MSMEs without compromising their own stability.

4. Collaboration and Partnerships

Collaboration is a key theme in Bhutada's guidelines. Recognizing that no single entity has all the answers, he encourages financial institutions to collaborate with fintech companies, industry experts, and government bodies. Such partnerships can lead to innovative solutions and policy frameworks that benefit both lenders and MSMEs.

5. Regulatory Support and Advocacy

Abhay Bhutada underscores the need for a conducive regulatory environment that fosters innovation in finance. His guidelines advocate for active participation in industry forums, engaging with policymakers to shape regulations that support responsible and innovative lending practices. This ensures that the financial ecosystem remains dynamic and responsive to the needs of MSMEs.

Also Read: Abhay Bhutada Talks About Lowering Lending Rates For Customers In 2025

Conclusion

Innovation in finance, guided by Abhay Bhutada's principles, is indispensable for unlocking the full potential of MSMEs. By embracing data-driven decision-making, integrating fintech solutions, implementing robust risk mitigation strategies, fostering collaboration, and advocating for supportive regulations, financial institutions can create an environment where MSMEs thrive.

0 notes

Text

Navigating Evolution In Banking And NBFCs Amid Market Shifts

In the fast-paced world of finance, things are always changing. Banks and other financial companies are always trying to keep up with these changes. They have to adjust to new trends and shifts in the market. As everyone involved tries to find their way through these changes, it's really important to keep a good balance.

On one hand, they need to make use of new technologies that can help them work better. But at the same time, they shouldn't forget about the basic ideas that have always been important in finance. These ideas are like the foundation of the whole industry, and they need to be preserved even as things around them change.

Understanding Market Dynamics

In the whirlwind of today's financial frenzy, institutions find themselves engulfed in a storm of complexities and opportunities. The dawn of technology has unleashed a tidal wave of change, transforming the once-staid banking landscape into a dynamic and electrifying arena. Yet, amidst the clamor for digital dominance, we mustn't lose sight of the timeless essence of human connection within the realms of banking and NBFCs.

Also Read: MD Abhay Bhutada Provides Glimpse of Poonawalla’s Co-Branded Card Strategy in Q4

As the digital tsunami crashes upon our shores, it's easy to be swept away by the allure of automation and algorithms. However, amidst the cacophony of technological advancement, the age-old wisdom of personal interaction stands as a stalwart beacon of resilience. Just as the ancient mariner relied on the stars to navigate treacherous seas, so too must modern institutions harness the power of human touch to steer through the tumultuous waters of finance.

The Human Touch In Banking

Despite the surge in digital banking solutions, the human touch remains integral to building trust and rapport with customers. Hardik Shah, MD and Partner at BCG, emphasizes the significance of physical networks and personalized interactions in fostering customer confidence. In the words of Shah, the traditional brick-and-mortar branches continue to play a pivotal role in India's banking ecosystem.

Also Read: How Are NBFCs Tackling RBI’s Stance On Unsecured Loans?

Navigating Risk Management Challenges

In the wake of market uncertainties, robust risk management practices emerge as a cornerstone for financial institutions. Abhay Bhutada, MD of Poonawalla Fincorp, underscores the importance of prudent risk assessment and mitigation strategies to navigate potential pitfalls effectively. Bhutada's insights highlight the critical role of risk management in safeguarding institutions against unforeseen disruptions.

The Role Of Technology In Banking

While technology holds the promise of revolutionizing banking operations, it's essential to leverage innovation judiciously. As Reserve Bank of India Governor Shaktikanta Das aptly observes, striking a balance between algorithmic underwriting and human judgment is imperative. While Artificial Intelligence (AI) can enhance operational efficiency, it cannot replace the nuanced judgment required in risk assessment.

Upskilling The Workforce

In a rapidly evolving landscape, upskilling the workforce becomes paramount. As institutions embrace technological advancements, fostering a culture of continuous learning is indispensable. Equipping employees with the necessary skills to adapt to changing market dynamics ensures resilience and sustainability in the long run.

Also Read Abhay Bhutada Shares Insights on Poonawalla Fincorp’s Long-Term Objectives

Conclusion

As banking and NBFCs navigate through market changes, it's crucial to uphold traditional values while embracing innovation. By striking a balance between technological advancement and human-centric approach, institutions can effectively address the evolving needs of customers while mitigating risks. As Abhay Bhutada emphasizes, prudent risk management remains imperative in safeguarding against uncertainties. In this journey of evolution, fostering a culture of continuous learning and adaptation will be instrumental in driving sustainable growth and resilience in the financial sector.

0 notes

Text

NBFCs Transforming The Payment Landscape

Poonawalla Fincorp and IIFL Finance are making waves in the financial sector, signaling a paradigm shift for Non-Banking Financial Companies (NBFCs). With Poonawalla Fincorp's recent RBI approval to launch co-branded credit cards and IIFL Finance exploring bank tie-ups, these moves are reshaping the role of NBFCs. In the era of digital payments, this article explores how NBFCs can actively participate in the payment ecosystem, aligning with the changing dynamics of finance.

1. Understanding The Shift

The financial landscape is evolving, and NBFCs are embracing change. Abhay Bhutada, Poonawalla Fincorp's MD, envisions co-branded credit cards as a catalyst for transformation. These cards not only complement existing products but position NBFCs as dynamic players in the payment space. IIFL Finance, under Nirmal Jain's leadership, mirrors this shift by seeking co-branding partnerships with banks, underlining a strategic move towards innovative payment solutions.

Also Read Abhay Bhutada Shares Insights on Poonawalla Fincorp’s Long-Term Objectives

2. The Strategic Move

Co-branded credit cards are not just pieces of plastic; they represent a strategic leap for NBFCs. In a market dominated by digital transactions, these cards enable NBFCs to tap into a broader audience. By collaborating with banks, such as IIFL Finance's potential tie-up, NBFCs can leverage existing banking infrastructure and customer bases, fostering a win-win scenario.

3. Expanding Customer Reach

One of the primary advantages of co-branded credit cards is the ability to extend the reach of financial services. Warren Buffett's timeless wisdom emphasizes the importance of widening one's circle of competence. For NBFCs, this means extending their offerings beyond traditional boundaries. Co-branded credit cards provide an avenue to reach new customers and offer them convenient and innovative payment solutions.

Also Read: MD Abhay Bhutada Provides Glimpse of Poonawalla’s Co-Branded Card Strategy in Q4

4. Aligning with Digital Trends

The era of traditional banking is fading, and the rise of digital payments is undeniable. NBFCs must align with these trends to stay relevant. Abhay Bhutada's vision for Poonawalla Fincorp aligns with this reality – co-branded credit cards not only adapt to digital trends but also position NBFCs as modern financial institutions, catering to the preferences of the tech-savvy consumer.

5. Navigating Regulatory Waters

While the journey towards active participation in the payment ecosystem seems promising, NBFCs must navigate regulatory waters. The RBI nod for Poonawalla Fincorp's credit cards is a significant step, highlighting the importance of regulatory compliance. Navigating this terrain ensures a smooth transition for NBFCs into the payment space without compromising financial stability.

6. Building Trust

Trust is the currency of finance, and NBFCs must prioritize it. Collaborating with established banks, as seen in IIFL Finance's pursuit, enhances credibility. Customers trust banks for their financial needs, and NBFCs can leverage this trust through co-branded partnerships, fostering confidence and loyalty among their clientele.

Also Read: How Are NBFCs Tackling RBI’s Stance On Unsecured Loans?

Conclusion

Poonawalla Fincorp and IIFL Finance's foray into co-branded credit cards exemplifies a pivotal moment for NBFCs. The shift towards becoming active participants in the payment ecosystem is not just a strategic move but a necessity in the evolving financial landscape. As they navigate through digital trends, regulatory frameworks, and customer trust, NBFCs can unlock new opportunities, redefine their roles, and emerge as key players in shaping the future of payments.

0 notes

Text

Banking And NBFCs' Fraud Fight: Innovations For Financial Security

Standing at the forefront of the fight against financial fraud are Non-Banking Financial Companies (NBFCs). These companies go beyond regular banking, working dynamically to make our money more secure. In a time filled with clever frauds, NBFCs use smart strategies to protect us, showing how quick and dedicated they are. These companies are like key players in making sure our financial future stays secure.

The Rise Of NBFCs

The ascent of Non-Banking Financial Companies (NBFCs) signifies a transformative shift in India's financial narrative. These entities have emerged as nimble alternatives, challenging the conventional banking paradigm. With a customer-centric ethos at their core, NBFCs swiftly adapted to cater to the diverse financial needs of the populace. Their flexible lending policies, tailored solutions, and streamlined processes have bridged the gaps left by traditional banks, fostering financial inclusivity and accessibility.

As trailblazers of innovation, NBFCs have catalyzed economic growth by catering to underserved sectors, thereby reshaping the financial landscape and becoming indispensable contributors to India's evolving economy.

Understanding The Fraud Landscape

The fraud landscape is a complex terrain where perpetrators constantly morph their tactics to exploit vulnerabilities. It encompasses a myriad of deceptive practices, from identity theft and phishing scams to sophisticated cyber intrusions. Financial institutions bear the brunt of these attacks, facing a relentless onslaught of fraud attempts.

With the advent of digital transactions, the avenues for fraudulent activities have widened, making traditional security measures inadequate. Understanding this landscape is imperative for Non-Banking Financial Companies (NBFCs) to fortify their defenses and protect consumers from falling prey to evolving fraud schemes.

Also Read: Unveiling The Future Of Collections In NBFCs

Innovative Strategies In Fraud Detection

1. Advanced Analytics:

NBFCs leverage cutting-edge analytics to detect abnormal patterns in transactions. AI-driven algorithms sift through vast data, flagging suspicious activities in real-time.

2. Biometric Authentication:

Embracing biometric technology like fingerprints or facial recognition, NBFCs fortify authentication processes, minimizing identity-related frauds.

3. Blockchain Technology:

The decentralized nature of blockchain fortifies data security. NBFCs utilize this technology to ensure immutable records, reducing the risk of tampering or fraud.

4. Behavioral Analytics:

Understanding customer behavior is pivotal. NBFCs employ behavioral analytics to identify deviations, proactively mitigating potential risks.

5. Use of Machine Learning

By analyzing vast amounts of financial data, machine learning algorithms can detect patterns and anomalies that might signal fraudulent behavior. These algorithms learn from historical data, continuously refining their models to adapt to evolving fraud tactics.

Abhay Bhutada, MD of Poonawalla Fincorp highlighted the significance of machine learning in the lending sector. He also emphasized that leveraging machine learning enables online lenders to rapidly authenticate transactions' legitimacy within milliseconds.

NBFCs’ Role In Educating Consumers

NBFCs play a pivotal role in empowering consumers through education and awareness initiatives. They recognize the importance of informed customers in combating financial fraud. These institutions conduct extensive outreach programs, seminars, and digital campaigns, aiming to educate individuals about various fraud types, preventive measures, and the importance of reporting suspicious activities promptly.

Collaboration And Information Sharing

Collaboration and information sharing stand as cornerstones in the fight against financial fraud. NBFCs actively engage in collective efforts, fostering a network where insights, best practices, and threat intelligence are shared among industry peers. Through forums, consortiums, and partnerships, NBFCs exchange crucial information on emerging fraud trends and tactics. Poonawalla Fincorp is also open to partnerships according to its MD, Abhay Bhutada.

This collaborative ecosystem not only bolsters their own defenses but also fortifies the entire financial sector against evolving threats. By pooling resources and knowledge, NBFCs pave the way for a more resilient and proactive stance against fraud, safeguarding both institutions and consumers alike.

Also Read: The Crucial Role Of Trust And Transparency In Digital Borrowing

Regulatory Compliance and Vigilance

Regulatory compliance stands as the cornerstone of NBFC operations, with stringent adherence to guidelines and protocols. Vigilance is embedded within their ethos, ensuring continuous monitoring, audits, and rigorous internal controls. Embracing regulatory frameworks isn’t just a mandatory checklist; it’s a proactive stance toward fortifying defenses against potential threats. This steadfast commitment extends to staying abreast of evolving regulations, implementing robust measures, and fostering a culture of unwavering compliance at every level of operations.

Adapting to Evolving Threats

Adapting to evolving threats remains a cornerstone for NBFCs in their battle against financial fraud. The landscape of fraud is ever-shifting, with new tactics and technologies constantly emerging from the dark corners of the digital world.

NBFCs understand the imperative need for continuous evolution in their defense mechanisms. They employ agile strategies, constantly assessing, innovating, and fortifying their systems to stay ahead of the curve. By fostering a culture of adaptability, these institutions remain resilient, ready to counter the most intricate and unforeseen threats that could compromise financial security.

Deepak Parekh, the former chairman of HDFC Ltd board has highlighted the importance of proactive measures to defend assets and strengthen security frameworks within banking and NBFCs, especially in the digital era.

Conclusion

In the ever-evolving landscape of financial fraud, NBFCs emerge as stalwarts, pioneering innovative approaches to safeguard consumers and institutions. Through technological prowess, collaborative efforts, and consumer empowerment, they reinforce the pillars of financial security, forging a resilient defense against fraudulent activities.

0 notes

Text

Unsecured Loans In India: Navigating RBI's Roadmap

Unsecured loans have witnessed a surge in popularity, becoming a key component of the financial landscape for individuals seeking quick financial solutions without the need for collateral. As a novice investor, it's imperative to delve into the Reserve Bank of India's (RBI) perspective on unsecured loans to make informed decisions about your financial journey.

Understanding The Unsecured Loan Landscape

Unsecured loans, such as personal loans and credit card debt, have gained traction owing to their accessibility and minimal paperwork requirements. These loans, devoid of collateral, offer a convenient option for individuals who may lack substantial assets to pledge against borrowing.

Also Read: From Abhay Bhutada to Nirmal Jain — India’s Top Chartered Accountants

The Watchful Eye Of The RBI

In recent times, the RBI has redirected its focus towards the escalating trend of unsecured lending within the financial system. Offering valuable insights, Keki Mistry, a financial advisor at Poonawalla Fincorp, sheds light on the RBI's viewpoint. Mistry views the central bank's directives not as a sign of immediate concern but as a proactive and precautionary measure to address the substantial growth in unsecured lending across the financial sector.

Mandatory Security Measures

The recent RBI order mandates lenders to implement additional security measures to protect consumers from potential fraud and identity theft. These measures aim to fortify the lending environment, ensuring that borrowers' interests are safeguarded amidst the ever-evolving financial landscape. The RBI's commitment to enhancing security aligns with its broader goal of maintaining the integrity of the financial system.

Navigating Changes Effectively

Abhay Bhutada, Poonawalla Fincorp’s MD, provides valuable insights into the impact of these regulatory changes. Notably, the company has experienced a significant shift towards secured loans, witnessing an increase from 46% to 52% in the last quarter. Bhutada emphasizes that this shift has not only secured a major market share in products like pre-owned cars and loans against property but has also positioned them as a CRISIL AAA rated NBFC.

Highlighting the company's current leverage of 1.5%, the lowest in the industry, and a cost of borrowing ranking among the industry's lowest, Bhutada assures that Poonawalla Fincorp is well-prepared to weather the changes in the lending landscape. With a robust capital adequacy of 38%, the company anticipates that even with a growth projection of 35 to 40%, no additional capital will be required for the next three to four years.

Also Read: Abhay Bhutada Shares Insights on Poonawalla Fincorp’s Long-Term Objectives

Navigating The Intricacies Of Finance

For a beginner investor entering the dynamic realm of finance, understanding the RBI's stance on unsecured loans becomes paramount. The central bank's proactive approach in tightening regulations around these loans can be seen as a necessary step to maintain the stability and integrity of the financial system.

Looking Ahead With Informed Optimism

As a beginner, it's essential to keep an eye on how these changes unfold. The RBI's commitment to enhancing security measures should be viewed optimistically, as it signifies a positive step towards building a safer lending environment for all. The financial landscape may evolve, but with insights from seasoned financial advisors like Keki Mistry and MD of Poonawalla Fincorp, Abhay Bhutada, investors can stay informed and make sound financial decisions with confidence.

Also Read: How Are NBFCs Tackling RBI’s Stance On Unsecured Loans?

Conclusion

In conclusion, the RBI's stance on unsecured loans underscores its commitment to ensuring the financial well-being of consumers. As a beginner investor, staying informed about these developments is crucial for making prudent investment choices. The insights from industry experts, including those from Poonawalla Fincorp, provide a valuable perspective on how these changes are being navigated within the financial sector. As the financial landscape continues to evolve, being aware and adaptive will be key for any investor, whether seasoned or just starting out. Staying informed empowers investors to navigate the intricacies of the financial landscape with confidence and foresight.

0 notes

Text

"Navigating the Fixed Deposit Landscape: Tips for Effective Comparison"

Fixed Deposits have long been the core of safe and risk-free investments, providing a traditional haven for hard-earned money. In today’s financial landscape, numerous banks and Non-Banking Financial Companies (NBFCs) compete for your attention, offering alluring interest rates on fixed deposits. However, the key lies in selecting the right bank to maximize your returns. In this blog post, we’ll…

View On WordPress

#Bank#Banks#Best bank FD#Best Bank Fixed Deposit#Choose best FD#Choose Fixed Deposit#Criteria for Choosing Best FD#FD#FD in NBFC#FD interest rate#Fixed Deposit#Fixed Deposit in NBFCs#Fixed deposits#NBFC#NBFC FD#NBFC Fixed Deposit#NBFCs

0 notes

Text

Axis Finance Business Loan are the ideal solution for borrowers in need of funds to meet your immediate cash flow needs

0 notes

Text

The Extraordinary Odyssey of Abhay Bhutada: A Journey from SME to Boardroom Titan

Ascending from the humble ranks of SME to the prestigious boardroom is a journey marked by rarefied achievement. It demands not only exceptional skills but also relentless dedication and foresight. Abhay Bhutada, a distinguished Chartered Accountant (CA) and a trailblazer in the Indian financial domain, epitomizes this extraordinary trajectory with his stellar career path.

Commencing with Modest Origins: The Genesis of Entrepreneurial Spirit

Abhay Bhutada's voyage began with humble origins, characterized by a burning desire to carve his distinctive niche within India's fiercely competitive business landscape. Equipped with a robust educational foundation and a profound understanding of financial intricacies, he embarked upon his professional odyssey with unwavering determination and boundless ambition.

Starting his career as an SME Finance Professional at the Bank of India in 2010, Abhay swiftly recognized his innate inclination towards entrepreneurship and innovation. His tenure at the bank provided invaluable insights into lending nuances and financial stewardship, laying a solid foundation for his future endeavors.

The Birth of TAB Capital

Despite a successful stint at the Bank of India, Abhay's entrepreneurial spirit impelled him towards establishing his consultancy firm. Acknowledging the evolving landscape of India's Banking, Financial Services, and Insurance (BFSI) sector, coupled with the burgeoning demand for digital solutions, he ventured into entrepreneurship by founding TAB Capital.

In 2016, Abhay Bhutada's visionary leadership led to the inception of TAB Capital, a Non-Banking Financial Company (NBFC) poised to revolutionize MSME financing. Armed with a deep understanding of the lending panorama and a fervent commitment to innovation, Abhay embarked on a mission to address the longstanding challenges faced by small businesses in accessing capital.

Also Read: How does Poonawalla Fincorp stand out from other NBFCs as per their MD, Abhay Bhutada?

Pioneering Paradigms in MSME Financing: TAB Capital's Trailblazing Approach

Under Abhay Bhutada's sagacious stewardship, TAB Capital introduced a pioneering digital platform aimed at streamlining the loan application and disbursement process for MSMEs. Leveraging technology and data analytics, the company offered unparalleled accessibility and convenience to small businesses, empowering them to fuel their growth trajectory.

A notable highlight of TAB Capital's offerings was the introduction of unsecured MSME loans ranging from INR 2 lakhs to 1 crore, disbursed within just two working days. This revolutionary approach not only catered to the funding requirements of small enterprises but also catalyzed their entrepreneurial journey, thereby propelling economic advancement and prosperity.

Strategic Collaboration: The Nexus with Poonawalla Finance

Abhay Bhutada's visionary acumen and penchant for innovation caught the attention of Mr. Adar Poonawalla, a luminary figure in the business realm known for his visionary leadership. Recognizing the synergies between their respective ventures, the two stalwarts embarked on a strategic partnership poised to redefine the landscape of digital lending in India.

In 2019, this collaboration materialized with the merger of TAB Capital into Poonawalla Fincorp, marking a significant milestone in Abhay Bhutada's professional journey. Assuming key roles within the amalgamated entity, including Managing Director, CEO, and Co-founder, Abhay played a pivotal role in strengthening the lending arm of the prestigious Poonawalla Group.

Also Read: Why Is Abhay Bhutada A Big Promoter Of Digitalization In The NBFC sector?

Poonawalla Finance's Digital-Centric Approach

Under Abhay Bhutada, Poonawalla Fincorp embraced a digital-centric approach to lending, leveraging technology to enhance efficiency and customer experience. The company's innovative digital platform streamlined the loan application process, facilitating swift approvals and disbursements while ensuring transparency and convenience for borrowers.

This transformative initiative not only resonated with evolving consumer preferences but also positioned Poonawalla Fincorp as a leader in the digital lending space. Abhay's visionary leadership and strategic foresight propelled the organization towards sustainable growth and success, solidifying its stature as a trusted financial partner for businesses across India.

Recognition and Accolades: Commemorating Excellence

Abhay Bhutada's exemplary leadership and trailblazing endeavors have garnered numerous awards and accolades, underscoring his significant contributions to the business landscape. From being honored as the 'Global Indian of the Year' in 2023 to securing the 'Young Entrepreneur of India' award in 2017, Abhay's achievements have been widely recognized and applauded by industry luminaries and experts.

Furthermore, his inclusion in Asia One's '40 under 40 Most Influential Leader for 2020-21' serves as a testament to his outstanding performance and enduring impact on the financial sector. These accolades serve as a resounding endorsement of Abhay Bhutada's relentless pursuit of excellence and his steadfast commitment to fostering innovation and positive change within the industry.

Also Read: How has previous experience helped Abhay Bhutada build Business Model For Poonawalla Fincorp?

Conclusion

As Abhay Bhutada continues to redefine conventions and chart new trajectories within the financial domain, his journey serves as a beacon of inspiration to aspiring entrepreneurs and seasoned professionals alike. From SME to MD to the esteemed boardroom, his professional odyssey epitomizes the essence of success, fueled by vision, tenacity, and an unwavering commitment to excellence.

Abhay Bhutada's extraordinary journey embodies the transformative power of entrepreneurship and innovation in driving economic advancement and fostering inclusive growth. As he continues to lead by example, his legacy is poised to inspire future generations of business leaders to dare, dream, and disrupt in pursuit of their loftiest aspirations.

0 notes

Text

RBI Tightens Personal Loan Rules, Predicts Rate Increase

RBI's Latest Move on Personal Loans: The Reserve Bank of India has implemented stricter regulations on personal loans, deeming them potentially risky for both banks and non-banking financial companies (NBFCs).

Read Our Detailed article in the below link 👇- https://www.mygstrefund.com/RBI-Tightens-Personal-Loan-Rules-Predicts-Rate-Increase/

THANKS FOR READING!

We provide GST refund solutions for customers.

To know more please visit: www.mygstrefund.com

Contact Us: - +91 9205005072

Mail- [email protected]

#RBIAnnouncement#LoanRegulations#NBFCs#PersonalLoans#FinancialSecurity#BankingGuidelines#PolicyUpdates#MyGstRefund

0 notes

Text

The Buzz Around NBFC Co-Branded Credit Cards

With influential figures endorsing their potential, NBFC co-branded credit cards are emerging as the new superheroes, transforming the way we handle transactions. Their evolution from conventional plastic to personalized gateways signifies a transformative era in the payment ecosystem. As influential figures continue to champion their potential, these cards are not merely financial instruments but catalysts for a revolution that is reshaping the very fabric of how we handle transactions. It's time to embrace the magic they offer and step into a future where co-branded credit cards become an integral part of our financial journey.

The Rise Of Co-Branded Credit Cards

Co-branded credit cards are not your average pieces of plastic; they're more like personalized magic wands. What sets them apart is the collaboration between Non-Banking Financial Companies (NBFCs) and established players in various industries. This fusion brings forth a card that not only offers financial perks but also aligns with the lifestyle and preferences of the cardholder.

Abhay Bhutada, Poonawalla Fincorp’s MD, believes that co-branded credit cards are more than just a financial instrument. According to him, these cards complement the existing product basket, turning the NBFC into an active participant in the payment ecosystem. It's a strategic move that resonates with the changing dynamics of how we transact in the digital age.

Also Read: How Can Tax Relaxations Help NBFCs Come On Par With Banks?

The Paytm-SBI Connection

When Vijay Shekhar Sharma, Paytm's founder, spoke about a payment revolution during the launch of their co-branded credit card with SBI, it wasn't just rhetoric. This collaboration signifies a leap into a future where credit becomes the mainstream choice for everyday transactions. Paytm's move showcases the immense potential co-branded credit cards hold in reshaping our payment landscape.

Tailored To Perfection

One of the key features of NBFC co-branded credit cards is their personalized touch. These cards aren't one-size-fits-all; they cater to the specific needs and preferences of the cardholder. Whether it's travel, shopping, or dining, these cards come with perks that align with your lifestyle. It's like having a financial sidekick that knows your every preference.

Also Read: What Is A Repo Rate?

The Allure Of Rewards And Benefits

Imagine getting discounts on your favorite brands, exclusive access to events, and cashback on your regular expenses – that's the magic co-branded credit cards bring to the table. These cards are not just about spending; they're about enjoying a little extra for every rupee you invest. It's like having Warren Buffett's investment wisdom at your fingertips, guiding you towards financial gains.

In the words of Abhay Bhutada, co-branded credit cards will be a welcome addition to their product offerings, elevating Poonawalla Fincorp's role in the payment ecosystem. It's not merely a financial tool; it's a strategic move towards becoming an integral part of the daily financial transactions of the customers.

The Future Is Contactless

In today's world, where making things easy is super important, NBFC co-branded credit cards are doing something really cool. They've got this amazing feature called contactless payments. Imagine this: you just tap your card, and boom, your payment is done! It's like magic. This modern way of doing things fits perfectly with the fast changes happening in digital payments. Now, every time you buy something, it's quick and smooth. It's not just a tech upgrade; it's like a whole new way we deal with money stuff!

Also Read: Why Digital Lending Is A True End-to-End System

Conclusion

NBFC co-branded credit cards don't merely serve as financial tools; they manifest as true superheroes, simplifying the complex narrative surrounding our monetary transactions. Far beyond being mere pieces of plastic, these cards symbolize strategic maneuvers aimed at reshaping and redefining our relationship with credit.

As the world eagerly anticipates the impending payment revolution, the enchantment of co-branded credit cards subtly and seamlessly integrates into the fabric of our daily lives. These cards become more than just conduits for transactions; they embody a paradigm shift in our approach to financial interactions, seamlessly blending into our routines and transforming the way we perceive and utilize credit.

0 notes

Last Seen Blogs

inuyashamybeloved

Inuyasha My Beloved

huomautuksia

Huomautuksia marginaalissa

captnjacksparrow

Sasuke loves Naruto

adamruz

third time's a charm

violetasimp

✹. 。 o ༺ ˖࣪ ∗ 𓆩♡𓆪 ∗ ˖࣪ ༻ ˖࣪ ∗ ਏ