#apis

Text

Wait, what?

Charging for access to APIs? Not on our watch.

Tumblr will always offer free access to our APIs of all kinds. No matter if the APIs are in the water, out of the water, and even half in and out of the water. Adorable Platypus Images are a cornerstone of the internet. It's a mammalian right to gaze upon these billed wonders.

Tumblr won't stop at total access to Adorable Platypus Images. Not only are we highlighting the entire Platypus community on Tumblr, we also hear Brick Whartley’s Crab Emporium (@emporium) may be dropping an entire line of Platypus goods...if that's what the people want.

3K notes

·

View notes

Text

#opedit#opgraphics#onepiecesource#oldanimeedit#animangahive#one piece#monkey d luffy#sanji#sanji vinsmoke#roronoa zoro#apis#warship island arc#i think i should have a tag for all these luffy moments. it's just hilarious

451 notes

·

View notes

Photo

Nest of the Asian Honeybee

Here we have the poisoned nest of the Asian Honeybee (Apis cerana). If you’re wondering why the nest was poisoned, it’s because this species is actually quite damaging to this area. The Asian Honeybee not only leaves in competition with native bees over nesting areas and food, but they may also carry a certain nasty mite known as the ‘Varroa mite’ (genus Varroa), which can be detrimental to European Honeybee populations (Apis mellifera) (1).

Lets take a closer look at this nest shall we. First we’ll start off with the eggs. You can see an egg inside a brood cell in picture 9. The eggs are very small, and take about three days to develop. After which the fat little larvae emerge, curling up and waiting to be fed by the worker bees. When the larva becomes large enough, the brood cell will be sealed, so the larva’s pupation will be undisturbed. The adult bee will chew its way out of the cell after emerging from the pupae (2).

You can tell which brood cell belongs to which kind of bee based on its appearance. The drones have a distinctly dome-shaped cap with a large pour in the center (pic. 7). Then, of course, there’s the queen’s brood cell, which is large, round and on the edge of the nest (pics 5-6) (3).

When it comes to this species, it’s important to stay informed about the ways in which they are damaging for the environment.

Source (1)

Source (2)

Source (3)

Apis cerana

14/07/22

#Apis cerana#Asian Honey Bee#Apis#Cavity-nesting Honey Bees#Honey Bees#Apini#Anthophila#Bees#Hymenoptera#Varroa#Varroa Mites#Acari#Mites#invasive species#bugs#bugblr#bugs tw#bug#insects#insecta#insectblr#insects tw#entomology#insect#Arthropods#Arthropoda#beehive#hives#nests#invertblr

598 notes

·

View notes

Text

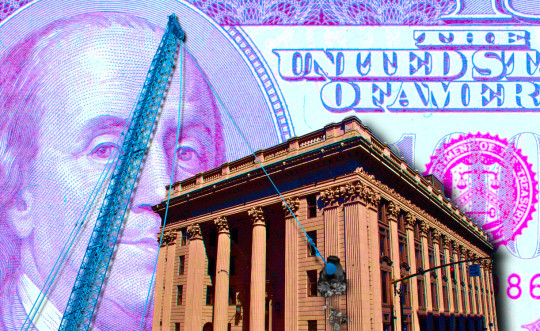

An interoperability rule for your money

This is the final weekend to back the Kickstarter campaign for the audiobook of my next novel, The Lost Cause. These kickstarters are how I pay my bills, which lets me publish my free essays nearly every day. If you enjoy my work, please consider backing!

"If you don't like it, why don't you take your business elsewhere?" It's the motto of the corporate apologist, someone so Hayek-pilled that they see every purchase as a ballot cast in the only election that matters – the one where you vote with your wallet.

Voting with your wallet is a pretty undignified way to go through life. For one thing, the people with the thickest wallets get the most votes, and for another, no matter who you vote for in that election, the Monopoly Party always wins, because that's the part of the thick-wallet set.

Contrary to the just-so fantasies of Milton-Friedman-poisoned bootlickers, there are plenty of reasons that one might stick with a business that one dislikes – even one that actively harms you.

The biggest reason for staying with a bad company is if they've figured out a way to punish you for leaving. Businesses are keenly attuned to ways to impose switching costs on disloyal customers. "Switching costs" are all the things you have to give up when you take your business elsewhere.

Businesses love high switching costs – think of your gym forcing you to pay to cancel your subscription or Apple turning off your groupchat checkmark when you switch to Android. The more it costs you to move to a rival vendor, the worse your existing vendor can treat you without worrying about losing your business.

Capitalists genuinely hate capitalism. As the FBI informant Peter Thiel says, "competition is for losers." The ideal 21st century "market" is something like Amazon, a platform that gets 45-51 cents out of every dollar earned by its sellers. Sure, those sellers all compete with one another, but no matter who wins, Amazon gets a cut:

https://pluralistic.net/2023/09/28/cloudalists/#cloud-capital

Think of how Facebook keeps users glued to its platform by making the price of leaving cutting of contact with your friends, family, communities and customers. Facebook tells its customers – advertisers – that people who hate the platform stick around because Facebook is so good at manipulating its users (this is a good sales pitch for a company that sells ads!). But there's a far simpler explanation for peoples' continued willingness to let Mark Zuckerberg spy on them: they hate Zuck, but they love their friends, so they stay:

https://www.eff.org/deeplinks/2021/08/facebooks-secret-war-switching-costs

One of the most important ways that regulators can help the public is by reducing switching costs. The easier it is for you to leave a company, the more likely it is they'll treat you well, and if they don't, you can walk away from them. That's just what the Consumer Finance Protection Bureau wants to do with its new Personal Financial Data Rights rule:

https://www.consumerfinance.gov/about-us/newsroom/cfpb-proposes-rule-to-jumpstart-competition-and-accelerate-shift-to-open-banking/

The new rule is aimed at banks, some of the rottenest businesses around. Remember when Wells Fargo ripped off millions of its customers by ordering its tellers to open fake accounts in their name, firing and blacklisting tellers who refused to break the law?

https://www.npr.org/sections/money/2016/10/07/497084491/episode-728-the-wells-fargo-hustle

While there are alternatives to banks – local credit unions are great – a lot of us end up with a bank by default and then struggle to switch, even though the banks give us progressively worse service, collectively rip us off for billions in junk fees, and even defraud us. But because the banks keep our data locked up, it can be hard to shop for better alternatives. And if we do go elsewhere, we're stuck with hours of tedious clerical work to replicate all our account data, payees, digital wallets, etc.

That's where the new CFPB order comes in: the Bureau will force banks to "share data at the person’s direction with other companies offering better products." So if you tell your bank to give your data to a competitor – or a comparison shopping site – it will have to do so…or else.

Banks often claim that they block account migration and comparison shopping sites because they want to protect their customers from ripoff artists. There are certainly plenty of ripoff artists (notwithstanding that some of them run banks). But banks have an irreconcilable conflict of interest here: they might want to stop (other) con-artists from robbing you, but they also want to make leaving as painful as possible.

Instead of letting shareholder-accountable bank execs in back rooms decide what the people you share your financial data are allowed to do with it, the CFPB is shouldering that responsibility, shifting those deliberations to the public activities of a democratically accountable agency. Under the new rule, the businesses you connect to your account data will be "prohibited from misusing or wrongfully monetizing the sensitive personal financial data."

This is an approach that my EFF colleague Bennett Cyphers and I first laid our in our 2021 paper, "Privacy Without Monopoly," where we describe how and why we should shift determinations about who is and isn't allowed to get your data from giant, monopolistic tech companies to democratic institutions, based on privacy law, not corporate whim:

https://www.eff.org/wp/interoperability-and-privacy

The new CFPB rule is aimed squarely at reducing switching costs. As CFPB Director Rohit Chopra says, "Today, we are proposing a rule to give consumers the power to walk away from bad service and choose the financial institutions that offer the best products and prices."

The rule bans banks from charging their customers junk fees to access their data, and bans businesses you give that data to from "collecting, using, or retaining data to advance their own commercial interests through actions like targeted or behavioral advertising." It also guarantees you the unrestricted right to revoke access to your data.

The rule is intended to replace the current state-of-the-art for data sharing, which is giving your banking password to third parties who go and scrape that data on your behalf. This is a tactic that comparison sites and financial dashboards have used since 2006, when Mint pioneered it:

https://www.eff.org/deeplinks/2019/12/mint-late-stage-adversarial-interoperability-demonstrates-what-we-had-and-what-we

A lot's happened since 2006. It's past time for American bank customers to have the right to access and share their data, so they can leave rotten banks and go to better ones.

The new rule is made possible by Section 1033 of the Consumer Financial Protection Act, which was passed in 2010. Chopra is one of the many Biden administrative appointees who have acquainted themselves with all the powers they already have, and then used those powers to help the American people:

https://pluralistic.net/2022/10/18/administrative-competence/#i-know-stuff

It's pretty wild that the first digital interoperability mandate is going to come from the CFPB, but it's also really cool. As Tim Wu demonstrated in 2021 when he wrote Biden's Executive Order on Promoting Competition in the American Economy, the administrative agencies have sweeping, grossly underutilized powers that can make a huge difference to everyday Americans' lives:

https://www.eff.org/de/deeplinks/2021/08/party-its-1979-og-antitrust-back-baby

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/10/21/let-my-dollars-go/#personal-financial-data-rights

My next novel is The Lost Cause, a hopeful novel of the climate emergency. Amazon won't sell the audiobook, so I made my own and I'm pre-selling it on Kickstarter!

Image:

Steve Morgan (modified)

https://commons.wikimedia.org/wiki/File:U.S._National_Bank_Building_-_Portland,_Oregon.jpg

Stefan Kühn (modified)

https://commons.wikimedia.org/wiki/File:Abrissbirne.jpg

CC BY-SA 3.0

https://creativecommons.org/licenses/by-sa/3.0/deed.en

-

Rhys A. (modified)

https://www.flickr.com/photos/rhysasplundh/5201859761/in/photostream/

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/

#pluralistic#cfpb#interoperability mandates#mint#scraping#apis#privacy#privacy without monopoly#consumer finance protection bureau#Personal Financial Data Rights#interop#data hoarding#junk fees#switching costs#section 1033#interoperability

157 notes

·

View notes

Text

more scenes from my father's garden

#digital photography#sonya7r4#sonya7riv#photographers on tumblr#color photography#photography#photographers of tumblr#original photography#flora#green#garden#gardening#tomatoes#succulents#bees#bee#apis#sunflowers#helianthus#vines#lensblr#photoblog#photooftheday#photoset#photographer

107 notes

·

View notes

Text

Introduction to APIs and Web APIs

The illustration above is the best way you can think of how APIs work and I talk more about it in my new article about APIs. I really love the concept and logic of APIs, it proves that collaboration is a huge part of programming and APIs solidify that. I hope you enjoy the read and also this is my first article and I intend to write more about technologies that interest me and maybe tips and tricks in the future.

110 notes

·

View notes

Note

[LIVE BROADCAST]

PRIVATE - A Golden Rock within a Pebble; [APIS]; No Reluctant Epiphany.

<GRP> ......

<GRP> .........:}

<APIS> ...

<APIS> ...Uh.

<APIS> Hey, there, Goldy's best friend guy???

NRE: Hi!

NRE: im NRE, as you can see from the username

NRE: its very nice to meet you!

51 notes

·

View notes

Text

Honey Bees (Apis mellifera)

Photo by Simon Colmer

#honey bees#bees#apis#apis mellifera#hymenoptera#apidae#insects#entomology#honeycomb#bee photography#insect photography#animals#yellow

82 notes

·

View notes

Text

Western honey bee (Apis mellifera) in central Pennsylvania

#yes it's adorable#cute bee#bee#buzz buzz#honey bee#apis#apis mellifera#honey#pollinator#although sadly an introduced species#psa: native pollinators are important too#that includes flies#wasps#moths#of course butterflies#beetles#insects#nature#bugs#nature photography#biodiversity#animals#inaturalist#arthropods#bugblr#entomology#insect appreciation#hymenoptera#flower#garden

22 notes

·

View notes

Text

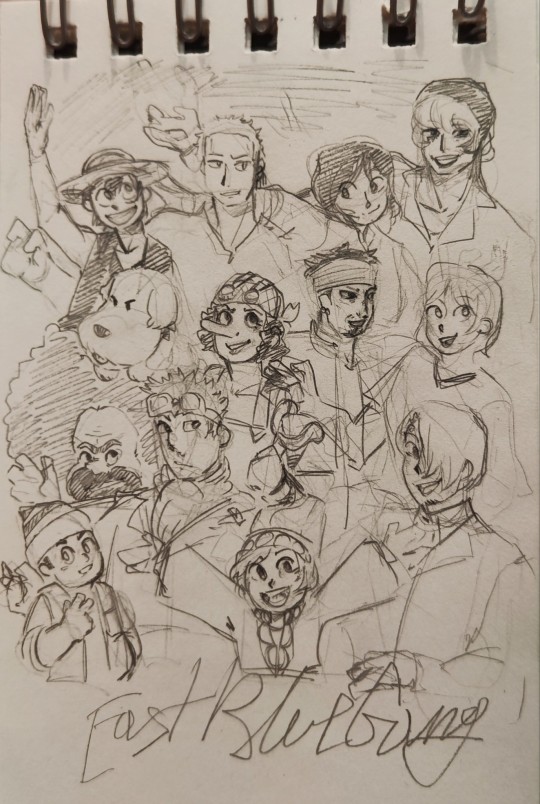

A chaotic little one piece au i made up. It goes like this: what if Luffy got more people into his crew? Well, there's the extended east blue gang!

Additional note: Also this au is kind of everyone(or almost everyone) is alive that's why Cora-san and Kuina are there.

#one piece#one piece au#the more the merrier au#luffy#monkey d. luffy#zoro#roronoa zoro#kuina#shimotsuki kuina#corazon#donquixote corazon#donquixote rosinante#chouchou#gaimon#usopp#gin#nami#borodo#akisu#apis#sanji

55 notes

·

View notes

Text

Day 15: Apis Bull

#akhtober #egyptian #deities #drawing #mythology #art #apisbull #apis #bull #day15 #digitaldrawing #magic #pagan #witchcraft #illustration #simple #kemetic #firealpaca #artist #artistoninstagram #myart #dahkyarts #artistoftales #artistonig

#akhtober#egyptian#deities#drawing#mythology#art#apisbull#apis#bull#day15#digitaldrawing#magic#pagan#witchcraft#illustration#simple#kemetic#firealpaca#artist#artistoninstagram#myart#dahkyarts#artistoftales#artistonig

37 notes

·

View notes

Note

What is Apis' and Arte's relationship? Are they friends or do they not get along?

There's a lot to Static Emotion. Not everything can or will get explained, but still.~

36 notes

·

View notes

Text

This stela is pretty awful, which is why I love it. Not everyone had loads of silver to fork out for great art, but everyone needed hope. I'm guessing this is a chap and his son, asking the gods for their protection -- but which gods, exactly? Thoth and Tutu are pretty clearly there, but is that the Apis bull, as the Louvre says, or does the animal on the plinth have curly horns and a beard? And who is the small humanoid figure near Thoth? I'm always trying to put a name to figures -- gods, demons, etc -- but perhaps ultimately it doesn't matter; the stela's commissioner knew whose help they wanted.

When: Ptolemaic Egypt

Where: Louvre

17 notes

·

View notes

Photo

Honey Bee Apis Melifera hovering by a Red Hot Poker by Barrie J Brown CPAGB https://flic.kr/p/2o8qfJg

118 notes

·

View notes

Text

"As with the new Reddit, [Twitter's] inflated fees for accessing the API are not really about passing real world costs onto developers who have been effectively subsidized in the past. It's the DJ turning on all the lights and playing a certain song at maximum volume."

-Rob Beschizza

64 notes

·

View notes