#crop insurance

Text

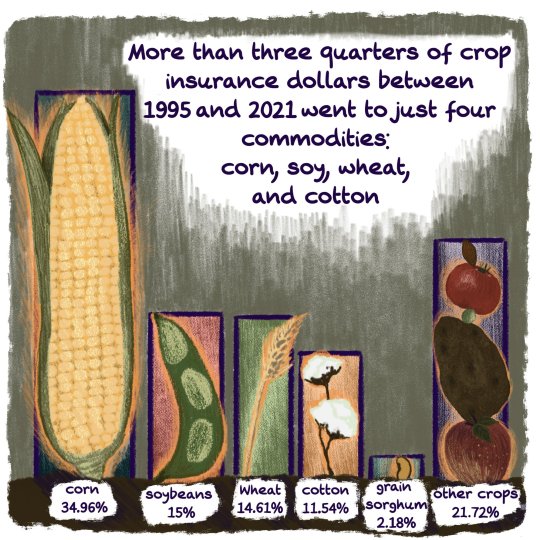

Agricultural production is worth protecting; food and fiber are too important to be subject to the increasingly cruel vagaries of the weather and global trade. But as it stands, the [Federal Crop Insurance Program] is maladapted to the challenges of our modern world, where places like Arizona are routinely smashing through high heat records and water in the West is becoming increasingly scarce. While home insurers like State Farm are pulling out of California and Florida due to the mounting costs of climate disasters, the FCIP is doing the opposite: insulating farmers from the true cost of doing business.

The average return for home and auto policies is about 60 cents per dollar spent on premiums. Farmers receive an average of $2.22 for every dollar they put into crop insurance. As a result, between 2000 and 2016, farming businesses—mostly large ones—collectively pocketed $65 billion more in claim payments than they paid in premiums. They were paid to plant crops that never came to market.

218 notes

·

View notes

Text

Over 1.7-crore farmers have been given the benefit of crop insurance at Re 1 but who will ensure that the insurance companies compensate them judiciously for the crop losses farmers suffer? We have seen reports of Rs 15, Rs 100 and Rs 200 and so on, paid to farmers for crop losses. Crop insurance is touted as a big benefit for farmers, but the data shows that private insurance firms have walked away with profits of Rs 57,619-crore since the scheme began in 2016. In reality, PM Fasal Bima Yojna (PMFBY) seems to be a scheme that ensures large profits for the bima companies.

Devinder Sharma, ‘Incredible India! Wilful defaulters buy properties; farmers offer to sell body organs to pay-off loans’, Bizz Buzz

2 notes

·

View notes

Photo

the majority of [united states] government funding and taxpayer-backed programs in agriculture support corporate-controlled livestock and poultry operations and the production of grains (like corn and soybeans) to feed their animals

[x][x]

1 note

·

View note

Text

Navigating the Complexities of Crop Insurance Claims: Tips for Farmers

Farming is an essential and intricate aspect of our global economy, providing sustenance and raw materials for countless industries. However, the agricultural sector is inherently vulnerable to various risks, including unpredictable weather patterns, pests, and diseases. In order to mitigate these risks and safeguard the livelihoods of farmers, crop insurance has emerged as a crucial financial tool. Crop insurance offers a safety net for farmers, providing financial support in the event of crop failure or significant yield losses. It plays a pivotal role in promoting stability within the agricultural sector by offering a measure of financial security, allowing farmers to recover from unforeseen challenges and continue contributing to food production. The symbiotic relationship between farming and crop insurance underscores the importance of a resilient agricultural system, one that can adapt to the uncertainties posed by nature, ultimately ensuring food security for communities worldwide.

In this blog, we'll explore practical tips to help farmers navigate the claims process smoothly, ensuring they receive fair compensation for their losses.

Tips to Help Farmers Navigate Farm Insurance Claims

Navigating farm crop insurance claims can be a complex process, and farmers need to be well-prepared to ensure a smooth and successful experience. Here are some tips to help farmers navigate farm insurance claims:

Understand Your Policy: Thoroughly review and understand the terms and conditions of your farm insurance policy. Familiarise yourself with coverage limits, exclusions, and any specific requirements related to claims.

Maintain Detailed Records: Keep meticulous records of all relevant information, including crop details, planting dates, input costs, and any actions taken to mitigate losses. Accurate documentation is essential during the claims process.

Prompt Reporting of Losses: Report any losses or damage to your crops promptly. Delays in reporting may lead to complications during the claims evaluation. Timely communication with your insurance provider is crucial.

Communication with Insurance Agent: Establish and maintain open communication with your insurance agent. Your agent can guide you through the claims process, provide essential information, and address any concerns or questions you may have.

Follow Proper Procedures: Adhere to the prescribed procedures for filing and processing claims. Familiarise yourself with the necessary paperwork, deadlines, and any specific steps outlined by your insurance provider.

Accurate and Honest Information: Provide honest and accurate information about the extent of the damage and losses incurred. Misrepresentation can lead to claim denials and may have legal implications.

Document Communication: Keep records of all communications with your insurance provider. This includes emails, phone calls, and in-person meetings. Having a documented trail can be valuable in case of disputes or discrepancies.

Stay Informed About Updates: Stay informed about any updates or changes in farm insurance policies, regulations, or procedures. Regularly check for updates from your insurance provider to ensure you are aware of any modifications that may affect your claim.

Cooperate with Inspections: Cooperate fully during inspections or assessments conducted by the insurance company. Provide access to the affected areas and provide any additional information requested in a timely manner.

Consult Legal Advice if Needed: In complex situations or if disputes arise, consider seeking legal advice. A legal professional with expertise in agriculture and insurance can provide guidance on navigating challenging scenarios.

By following these tips, farmers can enhance their ability to navigate farm insurance claims effectively. Proactive communication, accurate documentation, and a thorough understanding of the insurance policy are key elements in ensuring a successful claims process for farmers facing the challenges of crop losses or damage.

Future Trends in Crop Insurance

The landscape of crop insurance is evolving rapidly, driven by advancements in technology, shifts in farming practices, and changing market dynamics. Predicting and discussing upcoming trends in crop insurance involves considering these factors that shape the future of agricultural risk management:

Integration of Technology: Remote Sensing and Satellite Imagery: Advancements in remote sensing technologies and satellite imagery are transforming the way insurers assess and manage risks. High-resolution imagery allows for more accurate monitoring of crop health and damage, facilitating quicker claims processing.

Data Analytics and Artificial Intelligence: The integration of data analytics and artificial intelligence enables insurers to analyse vast amounts of data, providing more accurate risk assessments. Predictive modelling can help anticipate potential risks and optimise insurance premiums.

Precision Agriculture: IoT and Sensor Technologies: The adoption of Internet of Things (IoT) devices and sensor technologies in precision agriculture allows for real-time monitoring of crop conditions. This data can contribute to more precise risk assessments and customised insurance solutions based on individual farm characteristics.

Parametric Insurance Models: Weather-Based Index Insurance: With climate change affecting weather patterns, weather-based index insurance is gaining prominence. These parametric insurance models payout based on predefined weather parameters, offering a more straightforward and faster claim process.

Blockchain for Transparency: Blockchain Technology: Blockchain is being explored to enhance transparency and traceability in the crop insurance process. Smart contracts on blockchain platforms can automate claims settlements, reducing the administrative burden and minimising the risk of fraud.

Tailored Insurance Products: Customised Coverage: Insurers are increasingly offering tailored insurance products to meet the specific needs of different crops, regions, and farming practices. This trend allows farmers to choose coverage that aligns more closely with their individual risk profiles.

Climate-Resilient Agriculture: Focus on Sustainable Practices: As sustainability becomes a central theme, crop insurance is likely to align with climate-resilient farming practices. Insurers may incentivise or provide discounts for farmers adopting sustainable and environmentally friendly agricultural methods.

Market-Based Risk Transfer: Integration with Financial Markets: The integration of crop insurance with financial markets, including the use of catastrophe bonds, enables the transfer of agricultural risks to a broader set of investors. This approach diversifies risk and can potentially lead to more stable and competitive insurance markets.

Policy and Regulatory Developments: Government Initiatives: Anticipated changes in government policies and regulations may influence the direction of crop insurance. Governments may introduce incentives or reforms to encourage broader participation and adoption of insurance in the agricultural sector.

Global Collaboration and Partnerships: International Cooperation: Collaborations and partnerships between insurers, governments, and international organisations may lead to the development of standardised frameworks and best practices, fostering a more globally interconnected crop insurance ecosystem.

Consumer Education and Awareness: Empowering Farmers: Increasing efforts to educate farmers about the benefits of crop insurance and how to navigate the claims process can contribute to higher adoption rates and improved resilience within the farming community.

Wrapping Up,

Navigating the complexities of crop insurance claims requires careful planning, thorough documentation, and effective communication with your insurance provider. By following these practical tips, farmers can enhance their chances of a smooth and successful claims process, ensuring they receive fair compensation for their losses. Remember, your insurance agent is there to assist you, so don't hesitate to reach out for guidance throughout the entire claims journey. If you require help navigating the complexities of farm crop insurance, get in touch with us at KG2 Australia today!

0 notes

Text

Tana River Farmers Receive 14Million Flood Compensation: The Rise of Disaster Insurance After Successful Pilot in Kenya

Disaster insurance in the agriculture sector has begun picking up steam in East Africa after a group of small-scale farmers in Kenya received compensation for flood-related losses. Over 300 flood-affected households in Kenya’s Tana River county received more than $91,264 as compensation for their losses.

The first-of-its-kind compensation, under the flood parametric policy in Kenya, was part of…

View On WordPress

#climate insurance#crop insurance#effects of floods#flood insurance#Index-Based Flood Insurance (IBFI) policy#insurance#oxfam#Swiss Re

0 notes

Text

India things!

Recently, the Ministry of Fisheries, Animal Husbandry & Dairying has discussed the technical challenges in the implementation of the Aquaculture Crop Insurance scheme for Shrimp and Fish farming under the Pradhan Mantri Matsya Sampada Yojana (PMMSY) scheme.

To mitigate the risks faced by aqua farmers, NFDB (National Fisheries Development Board), which is the nodal agency for implementation of PMMSY, proposeed to implement the Aquaculture Crop Insurance scheme.

The Scheme aims to provide basic cover for brackish water shrimp and fish on pilot basis for one year in the selected States of Andhra Pradesh, Bihar, Gujarat, Madhya Pradesh and Odisha.

The term aquaculture broadly refers to the cultivation of aquatic organisms in controlled aquatic environments for any commercial, recreational or public purpose.

The breeding, rearing and harvesting of plants and animals takes place in all types of water environments including ponds, rivers, lakes, the ocean and man-made “closed” systems on land.

#general knowledge#affairsmastery#india#generalknowledge#current events#current news#aquaculture#fishery#shrimp#crop insurance#ocean#environment

0 notes

Link

Marine Policy not Crop Insurance

Lloyd’s Marine Policy Only Insured Against Loss of Property in Transit

Barry Zalma

Apr 25, 2023

Read the full article at https://lnkd.in/gTJjXtie and see the full video at https://lnkd.in/gmasQvMB and at https://lnkd.in/gFMHfmY2 and at https://zalma.com/blog plus more than 4500 posts.

Lloyd’s Marine Policy Only Insured Against Loss of Property in Transit

After Hurricane Irma damaged its property, Pero Family Farm filed an insurance claim. Lloyd’s accepted coverage for part of the claim but denied coverage for the rest. Lloyd’s sued seeking declaratory judgment that the insurance policy did not cover the denied portion of the claim. The district court granted summary judgment to Lloyd’s.

In Certain Underwriters At Lloyd’s London Subscribing To Policy No. B0799MC029630K v. Pero Family Farm Food Co., Ltd., No. 20-12711, United States Court of Appeals, Eleventh Circuit (April 10, 2023) the Eleventh Circuit interpreted the policy.

FACTUAL BACKGROUND

Pero grows vegetables (primarily peppers and beans) that it prepares and packages for either retail sale at grocery stores or wholesale by food service companies. The seeds Pero uses are either prepared by Pero from its own vegetables or purchased from third-party seed providers. Pero plants some of its seeds in fields it owns or leases in Florida. But Pero also sends seeds to Trans Gro, a third-party plant grower. Trans Gro plants the seeds and grows the seedlings in its greenhouses in Immokalee, Florida, until the seedlings are mature enough to be transported to Pero’s fields and planted in the ground.

Once Pero harvests its vegetables, it transports them to its cooled storage facility in Delray Beach, Florida, where it cleans, sorts, stores, and packages the vegetables. Pero packages some of its vegetables in plastic packaging. It then transports the vegetables from the Delray Beach facility to its final customers.

The Policy

In its 2015 insurance application, Pero stated that its “primary operations” were “[g]rower, [p]acker, [s]eller of vegetables[,] mainly [p]eppers and [g]reen [b]eans”; that the “[t]ype of [g]oods to be [i]nsured” was “produce, primarily peppers [and] beans”; and that it sought to insure “[d]omestic shipments” of “[g]reen beans [and] peppers on vehicles (dump trucks) moving from field to packing house[;] seed is also stored on location.” The policy contained a Florida choice of law provision.

Subject-Matter Insured

All goods and/or merchandise of every description incidental to the business of the Assured or in connection therewith.

The policy limits were $150,000 for “[a]ny one domestic inland conveyance” and $5,000,000 for “[a]ny one location.”

Pero’s Insurance Claim

On September 10, 2017, Hurricane Irma struck South Florida. Pero submitted a claim to Lloyd’s for the damage it suffered as a result of the hurricane. Pero sought coverage for the loss of vegetables stored in the coolers at its packing house in Delray Beach, as well as: (1) seedlings that had been growing in Trans Gro’s greenhouses in Immokalee; (2) plants that had been growing in Pero’s fields; and (3) plastic coverings that had been placed over the plants growing in Pero’s fields.

Lloyd’s accepted coverage (and issued payment) for Pero’s loss of the vegetables in its coolers that were in transit but denied coverage for the damage to the seedlings growing in Trans Gro’s greenhouse, the plantings in Pero’s fields, and the plastic coverings on Pero’s fields that were not in transit.

The Lawsuit

Lloyd’s sued Pero seeking a declaration that the policy did not cover the damage to the seedlings, plantings, or plastic coverings. Lloyd’s alleged that coverage was not due under the policy because:

1 “[t]he seedlings, planted crops, and crop covers were not in transit at the time of the loss,” so “there [was] no ‘in transit’ coverage”;

2 “[t]he seedlings, planted crops, and crop covers were not in storage at any location as defined by the [policy],” so “there [was] no ‘location’ coverage”; and

3 “[s]eedlings and immature plants are crops and the [policy] d[id] not provide crop coverage”-because Pero “specifically sought cargo coverage for the transit and storage of fresh harvested produce, dry seeds[,] and packaging from field to storage and while in storage,” not “crop insurance.”

Summary Judgment for Lloyd’s

The district court granted summary judgment for Lloyd’s and denied Pero’s motion because “the unambiguous language in the [p]olicy d[id] not provide coverage for Pero’s damaged seedlings, plantings, and plastic coverings.”

DISCUSSION

The Eleventh Circuit agreed with Pero that the policy’s language was clear and unambiguous. But it also agreed with Lloyd’s and the district court that the policy did not cover Pero’s damaged seedlings, plantings, and plastic coverings.

The policy unambiguously covered goods or merchandise only while they were in transit or, by extension, “in store” as “stock” at a “location” during the transit process:

"Within the geographical limits of this policy, cover hereunder shall attach from the time the Assured assumes an interest in and/or responsibility for the subject [-] matter insured and continues uninterrupted, including transit, stock[,] and location coverage until that interest and/or responsibility ceases."

The geographical limits of the policy were from a beginning point to an end location, and anywhere goods or merchandise stopped in between. Coverage “continue[d] uninterrupted, including transit, stock [,] and location coverage,” during that trek.

The policy was titled “Marine Cargo Insurance,” and “cargo,” although not defined in the policy, was generally understood, at the time, to mean “[g]oods transported by a vessel, airplane, or vehicle.”

Consistent with the “Duration of Voyage Clause,” the policy’s title, and the claims procedure, the policy’s other provisions showed that it covered goods or merchandise only while in transit or in storage during the transit process.

The policy’s “Information” section said that the policy covered “[t]ransits from field to packing house.” And the statement of value attached to the policy noted that Pero’s Delray Beach “packing house” held “[s]tock/[i]nventory” valued at $5,000,000-the same amount as the policy’s per “location” coverage limit.

Pero’s 2015 insurance application which was attached to and made a part of the effective policy, which the Eleventh Circuit must treat as part of the contract, explained that the policy covered only goods or merchandise in transit or in storage during the transit process. Specifically, the application documents showed that Pero sought to insure “[d]omestic shipments” of “[g]reen beans [and] peppers on vehicles (dump trucks) moving from field to packing house” and the “seed . . . stored on location.”

Because the insurance policy clearly and unambiguously did not cover the portion of Pero’s claim that Lloyd’s denied, the district court properly granted summary judgment for Lloyd’s and denied partial summary judgment for Pero.

ZALMA OPINION

Insurance policies are contracts and must be interpreted as written if unambiguous. The policy obtained by Pero was not insurance of its crop but was limited to coverage for that portion of its crop while it was in transit. The hurricane caused damage to some of the crop and merchandise in transit but did not insure other damages caused by the hurricane to property not in transit. Lloyd’s used simple, clear, unambiguous language that both parties agreed was unambiguous and the Eleventh Circuit applied the insurance contract as written.

(c) 2023 Barry Zalma & ClaimSchool, Inc.

Subscribe and receive videos limited to subscribers of Excellence in Claims Handling at locals.com https://zalmaoninsurance.locals.com/subscribe.

Consider subscribing to my publications at substack at https://barryzalma.substack.com/publish/post/107007808

Barry Zalma, Esq., CFE, now limits his practice to service as an insurance consultant specializing in insurance coverage, insurance claims handling, insurance bad faith and insurance fraud almost equally for insurers and policyholders. He practiced law in California for more than 44 years as an insurance coverage and claims handling lawyer and more than 54 years in the insurance business. He is available at http://www.zalma.com and [email protected]

Follow me on LinkedIn: www.linkedin.com/comm/mynetwork/discovery-see-all?usecase=PEOPLE_FOLLOWS&followMember=barry-zalma-esq-cfe-a6b5257

Write to Mr. Zalma at [email protected]; http://www.zalma.com; http://zalma.com/blog; daily articles are published at https://zalma.substack.com. Go to the podcast Zalma On Insurance at https://podcasters.spotify.com/pod/show/barry-zalma; Follow Mr. Zalma on Twitter at https://twitter.com/bzalma; Go to Barry Zalma videos at Rumble.com at https://rumble.com/c/c-262921; Go to Barry Zalma on YouTube- https://www.youtube.com/channel/UCysiZklEtxZsSF9DfC0Expg; https://creators.newsbreak.com/home/content/post; Go to the Insurance Claims Library – https://zalma.com/blog/insurance-claims-library.

Subscribe and receive videos limited to subscribers of Excellence in Claims Handling at locals.com https://lnkd.in/gfFKUaTf.

Consider subscribing to my publications at substack at https://lnkd.in/gcZKhG6g

Go to the Insurance Claims Library – https://lnkd.in/gWVSBde.

#insurance#claims#insurance claims#marine#marine insurance#transit#lloyd's#hurricane#crops#crop insurance#transit insurance#insurance books#amazon.com

0 notes

Text

Philippines Crop Insurance Helps Farmers When Hurricane Strikes

An average of the closing costs for every day throughout the brand new interval of discovery is then calculated. Once the harvest value is established, it is compared to the base value to discover out if there's a distinction. RMA tracks the deadlines of trading for corn and soybeans in the course of the month of February.

The next amendment to the Act, in 1973, supplied two choices for the federal-provincial-producer cost-sharing preparations. In one choice, the federal and provincial governments every contributed 25% of whole premiums and 50% of administrative prices. In the other choice, the federal government contributed a total crop insurance coverage of 50% of premiums and the provinces paid all administrative prices. In the 1990 modification, the utmost coverage was elevated to 90% for low threat crops. Furthermore, the only cost-sharing formula was adopted, the place the federal government and provinces every pay 25% of whole premiums and 50% of administration costs.

The improvement of new, or expansion of existing, income insurance policies for citrus fruit commodities and commodity varieties. The time frames described in subparagraphs and of section 1508 of this title shall apply to the evaluate of idea proposals beneath this subparagraph. The Board shall establish procedures for approving advance fee of affordable analysis and growth costs to applicants. 110–246, §§12002, 12033, substituted "this subchapter" for "this chapter" wherever showing and struck out at end "The authority offered by this section shall be in addition to, and shall not supplant, the authority offered by part 1506 of this title." 106–224 struck out "livestock and" earlier than "stored grain" and "beneath subsection or of section 1508 of this title" after "by the Board".

Department of Agriculture's Risk Management Agency , presents several plans for crops and livestock. Availability and plans differ by state and county. In growing countries, only 20% of smallholder farmers have access to agricultural insurance coverage, and in sub-Saharan Africa this falls additional to just crop insurance for farmers 3%. Provides monetary assistance to producers of non-insurable crops when low yields, loss of inventory, or prevented planting occur because of pure disasters. This program is administered by the USDA Farm Service Agency, with workplaces in plenty of counties across the state.

The term "insurable commodity" means an agricultural commodity for which the producer on a farm is eligible to obtain a policy or plan of insurance underneath subchapter I. " Authority.—The Secretary shall present value share assistance to producers, in a way decided by the Secretary, in not lower than 10, nor greater than 15, States during which participation within the Federal crop insurance program is traditionally low, as decided by the Secretary. In no case shall a policy crop insurance or plan of insurance made out there under this subsection present coverage considerably similar to privately available hail insurance. Subject to subparagraphs and , the premium subsidy beneath this subsection shall be paid by the Corporation in the same manner and beneath the same phrases and conditions as premium subsidy for other policies and plans of insurance.

Finally, the courtroom ruled that there was no substantial proof to assist the director’s decision. First South additionally offers competitively priced life insurance designed to cover a borrower's entire debt. Policies defend dependents from the financial burden of excellent debt. Coverage relies on the experience of the grid somewhat than the complete farm.

Table2 shows that the two hottest coverage ranges for corn manufacturing in 2020 are 75% and 70%, respectively, accounting for 37.3% and 31% of insured corn acres beneath RP. The federal authorities spends a median of $8 billion per year on subsidizing the crop insurance system. In 2019, based on lower crop yields, decrease prices, and numerous prevented plantings, the USDA estimates the government will spend $10.5 billion, which might be the very best pay-out because the drought years of 2012 and 2013. In contrast, the farm invoice allotted $1.seventy five billion for EQIP financial and technical help for agricultural conservation practices and only $400 million over ten years for analysis on organic manufacturing techniques.

Ntukamazina, Onwonga examined challenges, potentials and alternatives with insurance uptake of index-based insurance in sub-Saharan Africa. Over the years, the dimensions and scope of the federal crop insurance program has expanded dramatically. The passage of the Federal Crop Insurance Act of 1980 inspired participation by authorizing a subsidy for premiums. The Federal Crop Insurance Act of 1980 also added coverage for added crops and areas of the country.

Since the identical enter could be both risk-increasing and risk-decreasing at completely different levels of utility , it's challenging to assign an indication of equation only based on producers’ threat aversion ranges. Option three is when the “harvest price” is larger than the “projected price.” In this case, the producer’s revenue farm credit crop insurance guarantee will increase to replicate the upper “harvest price” at no extra premium. If the producer purchases the 70% safety stage, then 70 bushel will be what we name their “trigger yield.” (100 X 70%.) To calculate the revenue assure, we would multiply the “trigger yield”, 70, instances the “established price”, $6.00 per bushel.

0 notes

Photo

Best Farmer App to increase your income. Get real-time mandi price information, detailed crop information, access to soil testing labs & many more. Download the app now!

https://outgrow.onelink.me/ChJN/ASOB

0 notes

Text

Karz insurance 10 process

Karz insurance 10 process

Karz Insurance

Karz Insurance is a full-service insurance company that provides coverage for cars, homes, and businesses. Karz Insurance was founded in 1991 and is based in Omaha, Nebraska. The company has over 700 employees and offers a variety of insurance products, including car, home, and business insurance. Karz Insurance is a member of the National Association of Insurance Commissioners…

View On WordPress

#auto insurance#bad insurance#car insurance#car insurance agent#car insurance explained#car insurance scams#crop insurance#hdfc insurance agent#health insurance#insurance#insurance advisor#insurance agents#insurance business#insurance claim#insurance company#insurance cover#insurance for car#insurance policy#insurance scammer#insurance scams#karz#Karz insurance#life insurance agent#life insurance sales#process#term insurance agent

0 notes

Text

फसल नुकसान की जानकारी देने के लिए इस राज्य सरकार ने जारी किये बीमा कंपनियों के टोल फ्री नंबर

फसल नुकसान की जानकारी देने के लिए इस राज्य सरकार ने जारी किये बीमा कंपनियों के टोल फ्री नंबर

बारिश समेत प्राकृतिक आपदा से खराब हुई बीमित फसलों के मुआवाजे के संबंध में राजस्थान सरकार की तरफ से 29 सितंबर को आदेश जारी किया गया है.

बारिश की वजह से कई राज्यों में खरीफ फसलों को नुकसान पहुंचा है.

Image Credit source: File Photo

खरीफ सीजन अपने पीक पर है. लेकिन, बीते दिनों खरीफ सीजन की इन फसलों पर मौसम की मार पड़ी थी. असल में बीते दिनों कई राज्यों में भारी बारिश हुई थी. इस वजह से खरीफ सीजन की…

View On WordPress

0 notes

Link

#organic farming#carbon farming#crop insurance#agriculture market#mixed farming#farming#commercial farming#agribussiness

0 notes

Text

1 What Is Weather Index Insurance?

If you choose this endorsement, such exclusions should be shown yearly in your acreage report and will be relevant to all acreage of the excluded varieties, sorts, or groups for the crop 12 months. You might change your coverage level or share of worth election for dry pea varieties till the spring sales closing date if you have chosen this feature, but do not have any insured fall-planted acreage or your fall-planted acreage just isn't eligible for this option. In all states except Arizona and California, you might choose only one coverage degree and price election for each grape kind within the county as specified within the Special Provisions. The coverage stage you choose for each grape kind is not required to have the same share relationship. You should notify us no less than 15 days earlier than any production from any unit will be offered by direct advertising or sold as fresh fruit.

The adjustment can't lead to a yield greater than the higher of your permitted actual manufacturing historical past yield or the actual yield of the manufacturing harvested after full maturity from the unit. In addition to the definition contained within the Basic Provisions, sugar beets should initially be planted in rows, except in any other case supplied by the Special Provisions, actuarial documents, or by written settlement. Inability to market the citrus fruit for any cause other than actual physical injury from an insurable cause specified in this part. In addition to the provisions of part 7 of the Basic Provisions (§ 457.8), for the 1998 crop 12 months, the premium quantity in any other case payable for the 1998 crop year will be elevated by 46 percent as a end result of the extra six months of coverage for that crop yr. If eligible for quality adjustment, the amount of production to be counted shall be decided by multiplying the number of pounds of such manufacturing by the issue derived from dividing Price A by eighty five p.c of Price B. All harvested manufacturing from the insurable acreage, together with any mature cotton retrieved from the ground.

Final records of sugar production might be used to discover out the amount of production to rely. You must request an appraisal if any time in the course of the crop yr sugarcane acreage minimize for seed won't produce at least the manufacturing assure so we will determine the production to count. If you don't request an appraisal, the manufacturing to rely for such acreage will be the manufacturing assure. In lieu of the definition contained within the Basic Provisions, an quantity FCIC determines to be representative of the yield that the feminine father or mother plants are expected to supply when grown under a selected production practice.

crop insurance company

Without protections in place to assist farmers recover quickly from losses, meals provide turns into stilted and society pays the price. Federally funded crop insurance has provided a security internet for farmers since 1938, but even this program just isn't an ideal resolution. To seize these elements, consider a continuum of agricultural producers differing in the stage of their aversion to threat which have the selection between self-insuring, buying a low-coverage insurance policy, and buying a high-coverage policy. Note that, in actuality, there are a number of insurance policies with different levels of risk coverage out there to producers. While our model could be simply adapted to contemplate numerous crop insurance contracts, such consideration would complicate the analysis without affecting the qualitative nature of our outcomes.

The coverage must include at least two crops that every make up 10% or more of the entire insured planted acres. The assured revenue and actual income ranges are a mean for the two crops, weighted by the variety of acres in every crop. It is worth noting that agricultural insurance just isn't and shouldn't be considered as a singular magic reply to all weather-related problems that farmers face. It is rather a half of a variety of risk management choices, alongside other instruments corresponding to money transfers and casual risk-sharing and danger administration strategies. Comparing it with money transfers, the evaluation invitations policymakers to consider the prices and opportunities between what Janzen et al. discuss with as ‘reactive’ social protection versus ‘proactive’ social protection with a long run view.

You might be supplied, in writing, a replica of the modifications to the Basic Provisions, Crop Provisions, and a duplicate of the Special Provisions. If modifications are made that will be efficient for the second yr of the two-year coverage module, such copies might be offered not later than 30 days prior to the termination date. If adjustments are made that shall be effective for a subsequent two-year coverage module, such copies shall be supplied not later than 30 days prior to the cancellation date.

After a significant drought in 1988, “ad hoc disaster assistance” was approved to provide relief to eligible farmers. Another ad hoc catastrophe bill was handed in 1989, a third in 1992, and a fourth in 1993. The agent receives a commission, outlined in an annual contract between the agent and the insurance company. In return, the agent offers product and premium information to the insured and collects info from the insured as required by the coverage all yr long. When planting “green,” a technique where farmers plant their commodity cash crop right into a still residing cover crop, fifty four.3% said they planted sooner in planting green fields than their different fields , while solely 9.7% mentioned they planted later.

Additionally, it should be noted that on these farms the quantity of subsidies for working actions was the very best. This is of great significance for strengthening the position of farms and their capability to cope with unforeseen events. It may point out a possible complementarity between crop insurance and the use of particular productivity-enhancing practices, and the potential of self-insurance as a risk management device.

If your coverage is terminated after insurance has hooked up for the next crop yr, coverage shall be deemed to not have attached to the acreage for the following crop yr. In addition to the definition within the Basic Provisions, land in which mint stolons have been positioned in a manner applicable for the planting technique and on the correct depth right into a seedbed that has been correctly prepared. Any other uninsurable mustard manufacturing that is delivered to fulfill the processor contract.

#crop insurance#crop insurance coverage#kansas crop insurance#crop insurance companies#crop insurance company#how does crop insurance work

1 note

·

View note

Text

Kshema is India’s Digital Insurance Company For Agriculture & Food Sectors

Kshema is India’s digital Insurance company that caters predominantly to cultivators of the Agriculture & Food Sectors. Our mission is to enable resilience among cultivators across the country, from income shocks due to extreme climate events and other vagaries, with insurance.

I AGRI — our proprietary location-aware platform that assesses and prices risk adequately allows us to address pre-harvest risks at a farm level. Developed in partnership with leading global experts in Spatial data sciences, actuaries, financial engineers and remote sensing experts among others, the platform allows us the benefit of drawing evidence-based results to expand the scope of our services beyond traditional risk analyses.

• A D2C rural insurance company with emphasis on creating products for cultivators.

• Kshema would create insurance solutions, through geo-tagging for many location-specific pre-harvest risks faced by cultivators.

• We aim to incentivize sustainable cultivation practices contributing to a ‘Net Zero Emissions Planet’ and Sustainable development Goals in the future.

• A well-capitalized company led by promoters with a progressive vision and a growth mindset.

• Kshema is an equal opportunities provider. Whether it’s our employees, vendors or partners, we only consider their merit and the value they create.We are changing the world, one farmer at a time — if you are passionate about creating impact on a global scale — join our journey.

2 notes

·

View notes

Text

hahaha ok i know the emergency funding thing is a way for powerless partisan authorities in legislative bodies to have a modicum of control and selectivity over which govt services and oversight are maintained as well as to skirt FED loan hikes and funnel new federal surplus into imperialist investment without the carte blanche they usually get from actual "wartime economy" but like. can we take the farm bill off the shelf please please please

1 note

·

View note

Last Seen Blogs

tentler

inside digital revolution

hogistindia-blog

Hogist-Bulk Food Order

myeyessawit

My eyes saw it

dooodle-ducky

Can't I stay here with you?

angel-nee

Furby Quest