#equifax

Text

At long last, a meaningful step to protect Americans' privacy

This Saturday (19 Aug), I'm appearing at the San Diego Union-Tribune Festival of Books. I'm on a 2:30PM panel called "Return From Retirement," followed by a signing:

https://www.sandiegouniontribune.com/festivalofbooks

Privacy raises some thorny, subtle and complex issues. It also raises some stupid-simple ones. The American surveillance industry's shell-game is founded on the deliberate confusion of the two, so that the most modest and sensible actions are posed as reductive, simplistic and unworkable.

Two pillars of the American surveillance industry are credit reporting bureaux and data brokers. Both are unbelievably sleazy, reckless and dangerous, and neither faces any real accountability, let alone regulation.

Remember Equifax, the company that doxed every adult in America and was given a mere wrist-slap, and now continues to assemble nonconsensual dossiers on every one of us, without any material oversight improvements?

https://memex.craphound.com/2019/07/20/equifax-settles-with-ftc-cfpb-states-and-consumer-class-actions-for-700m/

Equifax's competitors are no better. Experian doxed the nation again, in 2021:

https://pluralistic.net/2021/04/30/dox-the-world/#experian

It's hard to overstate how fucking scummy the credit reporting world is. Equifax invented the business in 1899, when, as the Retail Credit Company, it used private spies to track queers, political dissidents and "race mixers" so that banks and merchants could discriminate against them:

https://jacobin.com/2017/09/equifax-retail-credit-company-discrimination-loans

As awful as credit reporting is, the data broker industry makes it look like a paragon of virtue. If you want to target an ad to "Rural and Barely Making It" consumers, the brokers have you covered:

https://pluralistic.net/2021/04/13/public-interest-pharma/#axciom

More than 650,000 of these categories exist, allowing advertisers to target substance abusers, depressed teens, and people on the brink of bankruptcy:

https://themarkup.org/privacy/2023/06/08/from-heavy-purchasers-of-pregnancy-tests-to-the-depression-prone-we-found-650000-ways-advertisers-label-you

These companies follow you everywhere, including to abortion clinics, and sell the data to just about anyone:

https://pluralistic.net/2022/05/07/safegraph-spies-and-lies/#theres-no-i-in-uterus

There are zillions of these data brokers, operating in an unregulated wild west industry. Many of them have been rolled up into tech giants (Oracle owns more than 80 brokers), while others merely do business with ad-tech giants like Google and Meta, who are some of their best customers.

As bad as these two sectors are, they're even worse in combination – the harms data brokers (sloppy, invasive) inflict on us when they supply credit bureaux (consequential, secretive, intransigent) are far worse than the sum of the harms of each.

And now for some good news. The Consumer Finance Protection Bureau, under the leadership of Rohit Chopra, has declared war on this alliance:

https://www.techdirt.com/2023/08/16/cfpb-looks-to-restrict-the-sleazy-link-between-credit-reporting-agencies-and-data-brokers/

They've proposed new rules limiting the trade between brokers and bureaux, under the Fair Credit Reporting Act, putting strict restrictions on the transfer of information between the two:

https://www.cnn.com/2023/08/15/tech/privacy-rules-data-brokers/index.html

As Karl Bode writes for Techdirt, this is long overdue and meaningful. Remember all the handwringing and chest-thumping about Tiktok stealing Americans' data to the Chinese military? China doesn't need Tiktok to get that data – it can buy it from data-brokers. For peanuts.

The CFPB action is part of a muscular style of governance that is characteristic of the best Biden appointees, who are some of the most principled and competent in living memory. These regulators have scoured the legislation that gives them the power to act on behalf of the American people and discovered an arsenal of action they can take:

https://pluralistic.net/2022/10/18/administrative-competence/#i-know-stuff

Alas, not all the Biden appointees have the will or the skill to pull this trick off. The corporate Dems' darlings are mired in #LearnedHelplessness, convinced that they can't – or shouldn't – use their prodigious powers to step in to curb corporate power:

https://pluralistic.net/2023/01/10/the-courage-to-govern/#whos-in-charge

And it's true that privacy regulation faces stiff headwinds. Surveillance is a public-private partnership from hell. Cops and spies love to raid the surveillance industries' dossiers, treating them as an off-the-books, warrantless source of unconstitutional personal data on their targets:

https://pluralistic.net/2021/02/16/ring-ring-lapd-calling/#ring

These powerful state actors reliably intervene to hamstring attempts at privacy law, defending the massive profits raked in by data brokers and credit bureaux. These profits, meanwhile, can be mobilized as lobbying dollars that work lawmakers and regulators from the private sector side. Caught in the squeeze between powerful government actors (the true "Deep State") and a cartel of filthy rich private spies, lawmakers and regulators are frozen in place.

Or, at least, they were. The CFPB's discovery that it had the power all along to curb commercial surveillance follows on from the FTC's similar realization last summer:

https://pluralistic.net/2022/08/12/regulatory-uncapture/#conscious-uncoupling

I don't want to pretend that all privacy questions can be resolved with simple, bright-line rules. It's not clear who "owns" many classes of private data – does your mother own the fact that she gave birth to you, or do you? What if you disagree about such a disclosure – say, if you want to identify your mother as an abusive parent and she objects?

But there are so many stupid-simple privacy questions. Credit bureaux and data-brokers don't inhabit any kind of grey area. They simply should not exist. Getting rid of them is a project of years, but it starts with hacking away at their sources of profits, stripping them of defenses so we can finally annihilate them.

I'm kickstarting the audiobook for "The Internet Con: How To Seize the Means of Computation," a Big Tech disassembly manual to disenshittify the web and make a new, good internet to succeed the old, good internet. It's a DRM-free book, which means Audible won't carry it, so this crowdfunder is essential. Back now to get the audio, Verso hardcover and ebook:

http://seizethemeansofcomputation.org

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/08/16/the-second-best-time-is-now/#the-point-of-a-system-is-what-it-does

Image:

Cryteria (modified)

https://commons.wikimedia.org/wiki/File:HAL9000.svg

CC BY 3.0 https://creativecommons.org/licenses/by-sa/3.0/deed.en

#pluralistic#privacy#data brokers#cfpb#consumer finance protection bureau#regulation#regulatory nihilism#regulatory capture#trustbusting#monopoly#antitrust#private public partnerships from hell#deep state#photocopier kickers#rohit chopra#learned helplessness#equifax#credit reporting#credit reporting bureaux#experian

308 notes

·

View notes

Text

More than half of Americans admit to lying on a resume at least once. It's such a common practice that no wonder services are popping up to help employers find out about workers' previous job history.

A viral video from TikToker Morgan (@wfhmuva), who comments on work-from-home topics, informs viewers about one such service.

…

One viewer shared, "I used to work for Equifax and got hired somewhere else they found out so fast."

"Yes girl, they can see down to your gross and net income from each job from equifax," a second wrote.

Another expressed concern they may be in trouble. "wait so they'll know if im a job hopper?" the viewer asked. Morgan responded, "It's possible."

"Every company does not report to the work number!!!" one viewer noted. "Walmart does though. Also it costs to use this service. Most companies not paying for it."

Late last year, a Human Resources worker referenced the service as a reason employers are sometimes aware that a worker is about to leave. She noted that job seekers can check a box asking interviewers not to contact their current place of employment.

(continue reading)

#advice#jobs#jobsearch#equifax#the work number#job hopping#resumes#employment#employment resumes#employment research#employment advice#job history

184 notes

·

View notes

Text

Beyond the U.S. credit score system being blatantly unconstitutional, with the corporations running it sometimes pretending to have government authority, it also needs to be gotten rid of or extremely overhauled because of it recently including China-style social credit algorithms into its system.

2 notes

·

View notes

Text

My Credit Scores

I was ecstatic until I asked a friend, who informed me that his was 840. The competitive side of me is trying to figure out how to improve mine. Any suggestions? Maybe there is more I can do.

6 notes

·

View notes

Text

Abstract:The Financial Conduct Authority (FCA) of the United Kingdom has fined Equifax Ltd (Equifax) £11,164,400 for failing to maintain and monitor the security of UK consumer data it had outsourced to its parent company in the United States. The breach gave hackers access to millions of people's personal information,

0 notes

Text

Equifax fined $13.4 million following data breach

Credit bureau company, Equifax, has been fined US$13.4 million by The Financial Conduct Authority (FCA), a UK financial watchdog, following its involvement in “one of the largest” data breaches ever.

This cyber security incident took place in 2017 and saw Equifax’s US-based parent company, Equifax Inc., suffer a data breach that saw the personal data of up to 147.9 million customers accessed by…

View On WordPress

0 notes

Text

Deciphering Your Credit Score by Experian: A Comprehensive Guide

In the contemporary financial landscape, comprehending your credit score is paramount. Experian, a prominent credit bureau in India, plays a pivotal role in assessing your creditworthiness. This comprehensive guide is designed to illuminate the intricacies of the credit score by Experian, why it holds significance, and practical steps to enhance your financial standing.

Understanding the Credit Score by Experian:

Experian is one of India's leading credit bureaus, specializing in collecting and maintaining credit information for individuals and businesses. They utilize this data to calculate credit scores, which fall within a range typically from 300 to 850, with a higher score indicating stronger creditworthiness.

Why Your Credit Score by Experian Matters:

Your credit score by Experian carries immense weight because it directly influences the decisions of lenders when you apply for loans or credit cards. Lenders rely on these scores to gauge the risk of lending to you. A robust credit score can open doors to loans with more favorable terms, while a lower score can result in loan rejections or higher interest rates.

Tips to Improve Your Credit Score by Experian:

Punctual Bill Payments: Timely payment of bills, including credit card dues and loan EMIs, can significantly boost your credit score. Consider setting up reminders or automatic payments to ensure you never miss a due date.

Manage Credit Utilization: Aim to keep your credit card balances below 30% of your available credit limit. High credit card utilization can have a negative impact on your Experian credit score.

Diversify Your Credit Portfolio: A diverse mix of credit types, such as credit cards, loans, and mortgages, can positively affect your creditworthiness.

Regularly Review Your Credit Report: Periodically scrutinize your credit report provided by Experian for inaccuracies and discrepancies. If you come across any errors, take swift action to dispute and rectify them.

Exercise Caution with New Credit Applications: Avoid making numerous credit applications within a short timeframe, as this can raise red flags to potential lenders.

Maintain a Lengthy Credit History: The length of your credit history is another crucial factor. Keeping older accounts open and active can demonstrate a responsible credit track record.

In conclusion, your credit score by Experian is a vital instrument that significantly shapes your financial prospects. By grasping the mechanics behind this score and adhering to best practices to elevate it, you can bolster your creditworthiness. This, in turn, makes it easier to achieve your financial goals and secure loans with more favorable terms. Empower yourself to seize control of your financial future by managing your credit wisely and understanding the nuances of your credit score by Experian.

#credit#bank#finance#budgeting#loans#financialplanning#debtfree#personalloan#marketing#money#credit score by Experian#Experian credit score#experian#equifax#credit bureaus#credit reports#transunion#adulting

0 notes

Text

Big important wins 🙏🏼

0 notes

Text

Equifax “accidentally” sent out harmful, inaccurate credit scores on “certain” people 🤔

👉🏿 https://www.wsj.com/articles/equifax-sent-lenders-inaccurate-credit-scores-on-millions-of-consumers-11659467483

108 notes

·

View notes

Text

मेरे क्रेडिट स्कोर सिबिल, और अन्य 3 ब्यूरो में भिन्न क्यों हैं?

प्रत्येक ब्यूरो भुगतान इतिहास और खाता उपयोग सहित विभिन्न कारकों पर विचार करके क्रेडिट स्कोर की गणना करने के लिए अपने स्वयं के स्वामित्व वाले स्कोरिंग मॉडल का उपयोग करता है। प्रत्येक क्रेडिट ब्यूरो के पास आपके क्रेडिट इतिहास के बारे में समान जानकारी नहीं हो सकती है। अलग-अलग स्कोरिंग मॉडल और डेटा विसंगतियां अलग-अलग क्रेडिट स्कोर में योगदान करती हैं।

क्रेडिट स्कोर को स्वीकार्य या अस्वीकार्य मानने…

View On WordPress

0 notes

Text

US-Aufsichtsbehörde kündigt Pläne zur Regulierung der „Überwachungsindustrie“ an

Die führende US-Behörde für finanziellen Verbraucherschutz wird am Dienstag im Weißen Haus bekannt geben, dass sie Pläne zur Regulierung von Unternehmen vorantreibt, die personenbezogene Daten von Menschen verfolgen und verkaufen. Dies ist Teil der umfassenderen Prüfung der Datenschutzpraktiken dieser Branche durch die Biden-Regierung. Insbesondere das Verhalten von Datenbrokern bereitet Sorgen,…

View On WordPress

0 notes

Text

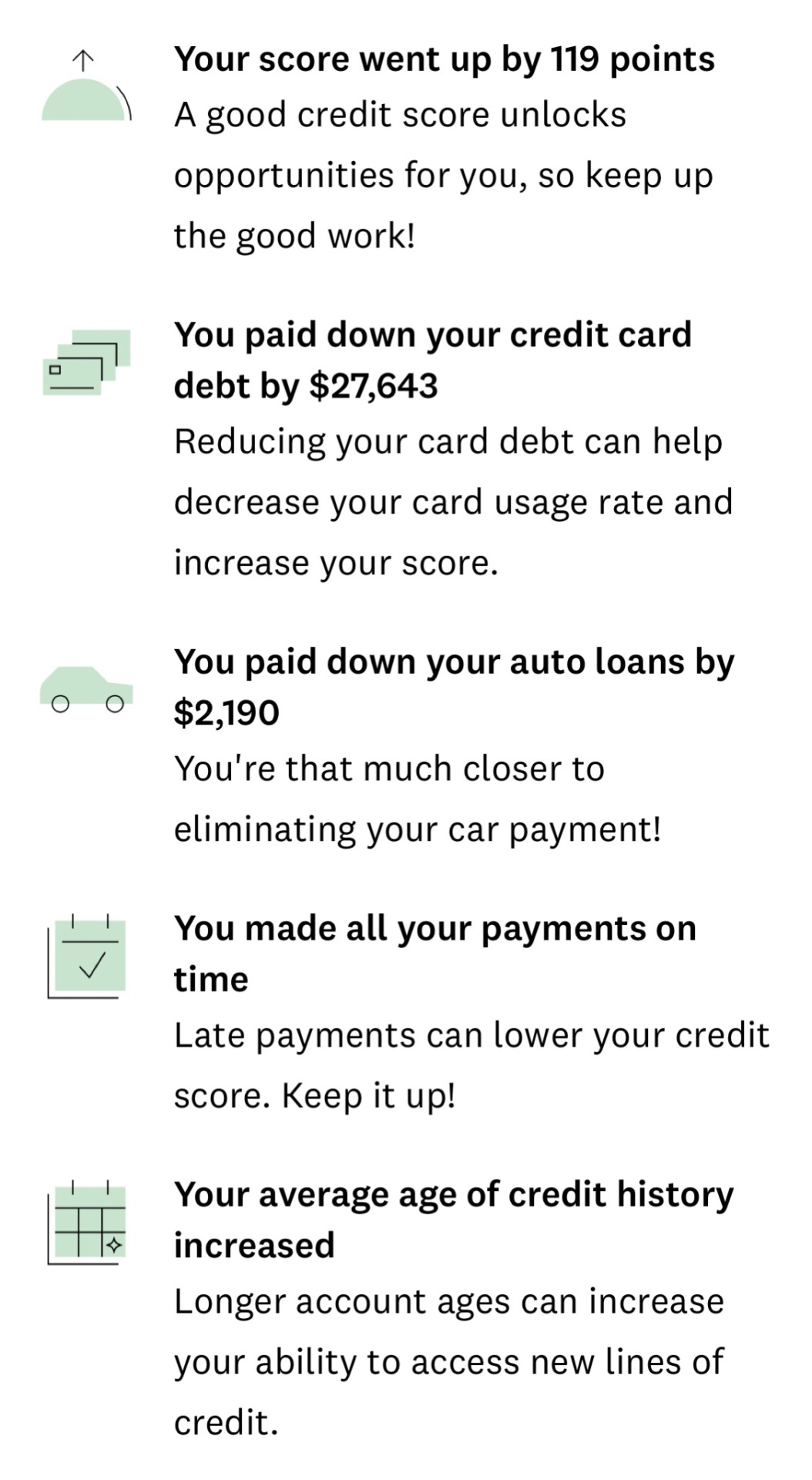

Credit Scores

Disclaimer: Some of this advice may not be immediately applicable to people who are struggling financially.

On the other hand, if you are responsible with money & lucky, your credit score will pretty much take care of itself.

I just don't want anyone to be accidentally lowering their credit score because they don't know the "rules of the game."

.......................................................................................................................

Dos:

--Pay off all your debt owed every single month - car loan, mortgage and yes credit card. (It's a common falsehood that carrying a credit card balance helps your score, it only does harm plus wastes your money on interest.)

--Keep your credit card spending below 30% of your official spending limit for that card; lower% is even better.

--For an credit card bill above the 30%, pay your balance before the "statement date" and don't wait until the due date.

--If you get a significant raise or other financial boon, contact your credit card company to request a raise to your spending limit.

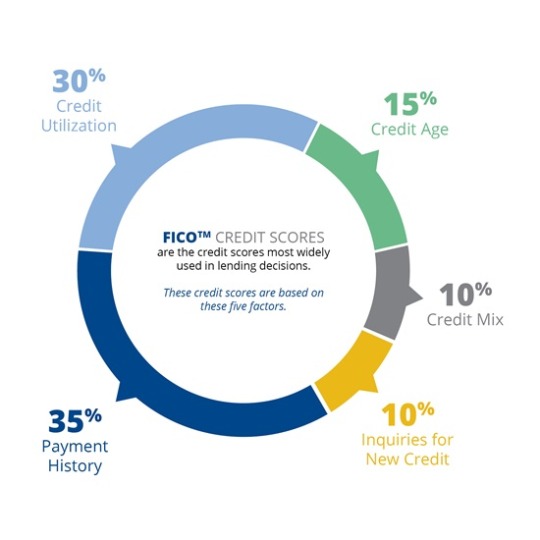

--Focus on your FICO credit score, and don't worry about any other credit score calculators.

--Avoid "hard inquiries" into your credit unless you expect to be approved for an imminent large purchase (vehicles, rental/mortgage, etc.)

--Only take out credit if you know you won't abuse it. A "thin file" is better than a file full of financial red flags.

Don'ts:

--Cancel your oldest credit card. Keep it going, set it up to autopay a small monthly bill (netflix, water, or the like)

--Apply for new credit cards unless you really need them. The hard credit check, the newness of the credit line, any overdue payments, and any spending near that card's credit limit can ALL harm your credit score.

--Expect a credit score change to change immediately or directly due to increased income or increased savings. Those factors are not a part of your credit score (though of course if you budget that money well, your credit score will eventually reflect your better financial stability).

--Fuss if your credit score is 740 instead of 850; 740 is the low end of the "perfect" range, you'll be approved for basically anything.

--Worry if your starting credit score is below 740. Nothing is wrong and you are not being penalized. Credit scores include 5 components: payment history, amounts owed, length of credit history, credit mix - these will all improve over time if you don't miss payments. The 5th component, new credit, may be lowering your score when you open your first credit line, but this too will fade with time (as long as you don't quickly open additional credit lines).

How to find your credit score for free from trusted sources:

1) Check with your bank or credit union.

2) Request your score through these three companies only: Experian, TransUnion, and Equifax.

3) use Consumer Financial Protection Bureau links:

(Note that you may have slightly different FICO credit scores across different financial websites, this is normal.)

Sources

#credit score#fico#npr#npr life kit#cfpb#equifax#transunion#experian#personal finance#financial awareness#financial literacy#what they should have taught in high school#credit cards#credit history#credit utilization

0 notes

Text

The Future of Passwords: Do We Really Need Them?

Passwords are one of the most common and widely used methods of authentication on the internet. They are supposed to protect our online accounts and data from unauthorised access and misuse. Passwords are increasingly becoming a source of frustration and insecurity for users and organisations alike. They are often easy to guess, hard to remember, and reused across multiple sites, making them…

View On WordPress

#2022 Data Breach Investigations Report#alternative authentication methods#biometrics#cybersecurity#Dashlane#Equifax#Google#IBM#LastPass#MFAs#passkeys#passwordless#Passwords#Verizon

0 notes

Text

Best Credit Reporting Sites!

There are several credit reporting sites that can provide you with access to your credit reports and scores. Here are some of the best credit reporting sites:

AnnualCreditReport.com: This is the official website mandated by federal law where you can access a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months. It’s…

View On WordPress

0 notes

Text

Financial Planning Before Buying a Home

Becoming a homeowner is one of the most significant goals for many people. However, home ownership comes with a significant financial burden.

For the majority of homeowners, the mortgage payments are their biggest outgoings each month. A large portion of a disposable income may go toward paying off the mortgage.

If you want to make the most significant investment most people ever make count,…

View On WordPress

#buying a condo#buying a home#canadian personal finance#closing costs#equifax#fhsa#mortgage#mortgage broker#personal finance#personal finance blog#real estate vancouver#transunion

0 notes

Last Seen Blogs

madcravings

mimi

definitelymaybe1

IN A WORLD OF MY OWN

eccedentesiastsunset-blog

— about me and you

whatdidshesayyy

HERE WE GO 🤦🏾♀️

lukes-smurf

Keep dreaming