#personal debt

Text

📢🗣️ In case anyone doesn't know, in the UK, warm home discount has changed & you have to ring 0800 107 8004 to apply for the £150 discount, instead of going via your supplier 📢🗣️

You will need your electricity account information available & you only have until the 28th February 2023.

Lines open 8am to 6pm.

✨Share to your low income friends & family so they can stay warm for the rest of the winter without having to worry about debt. We can do this together✨

#energy crisis#Benefits#uk government#disabled#disability#cripple punk#electricity#save lives#discount#energy bills#Bills#personal debt#help out

252 notes

·

View notes

Text

She did that

Even though it may be sad, many of us are starting to realize that student loans are not going to be paid off. Before the pandemmy I had over $16,355 in student loans. And like many others I didn’t receive a degree from the loans I took out. After talking with a neighbor and just thinking about my life. I decided to start paying them while they had no interest. I started paying off my debt in March. Keep in mind I am not a high earner (yet) and as of this day 6-15-23 I only have $6,957 left to pay off. I worked so much overtime. I didn’t buy new clothes. I don’t have a sugar daddy. I didn’t side hustle myself to death. I didn’t start a business. I didn’t scam anyone. I JUST WORKED MY 9-5. It was hard, but I will be done paying of my loans before September. I will be writing a post of how and why I decided to take this path. I may even start posting on TikTok. I want to be more open and I stepped away from this platform because I was struggling with some personal issues. Idk if anyone will read this, but if anyone does I want to just say, just start! Whether it’s student loans, taking charge of your health, making meaningful relationships. Just start you’ll mess up and when you do keep going. We’re all human, mess ups happen, and even giving up temporarily by taking breaks. But don’t don’t give up forever you got this! Till next time. Level Up on a Buck, but don’t stay stuck! >>>>> NEXT MANIFESTATION, OR MONEY GRAB?

#NextLevel#Next Level#Level Up#leveling up#level up on a buck#level up advice#debtfreejourney#debtfree#debtmanagement#personal debt#student loan#student loans#debt repayment#more money#money monday#money in the bank#make that money#money#Budget#cash#just girlboss things#bosslady#self sabotage#self love#self care#self improvement#self esteem

11 notes

·

View notes

Text

Fundraising for some debt relief for my wife and myself !!

TL;DR

We’ve been in debt a long time. We want out. We’re trying to improve our future by working it out now but we could use a little help !!

Looking to shovel ourselves out by the end of the year !! Anything helps including shares !!!

Need: $18,500

https://gofund.me/11c4ba7a

8 notes

·

View notes

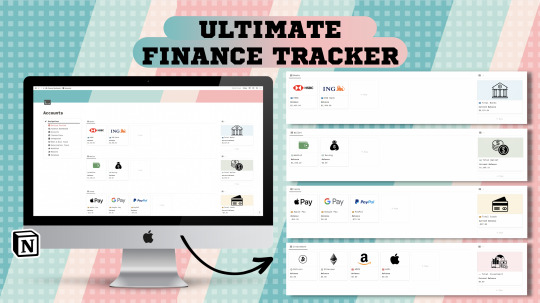

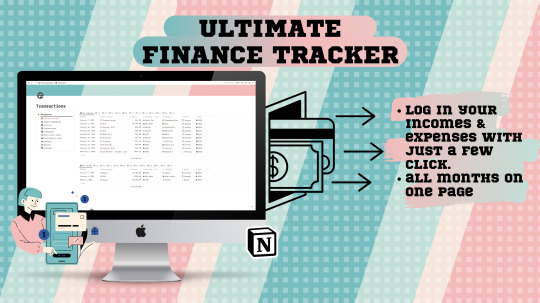

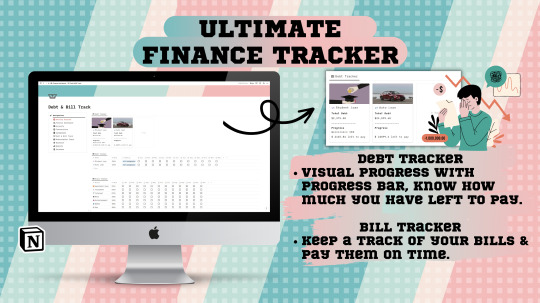

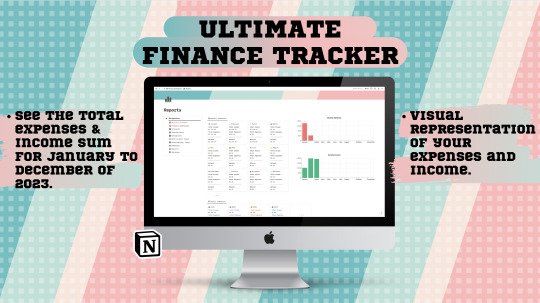

Photo

Ultimate Finance Tracker Notion Template | Finance Dashboard | Notion Personal & Business Finance Tracker for 2023 | Debt and Bill Tracker | Subscription Tracker | Digital Finance Planner | Finance Tracker

This dashboard will help you manage all your finances in one place. Register expenses, and income & make transfers on multiple accounts. Track your debt, set expense categories, and income; manage subscriptions, wishlist & more.

▷ WHAT IS NOTION?

◉ Notion is an all-in-one workspace where you plan, write, organize, and collaborate. It provides its users the building blocks to create customized layouts to get work done. Notion is free for a personal plan and is accessible through any device connected to the Internet - be it a smartphone, tablet, laptop, or computer.

▷ WHAT'S INCLUDED?

➜ Accounts

✵ Banks

✵ Cash

✵ Credit Cards

✵ Investment

➜ Transactions

✵ Expenses

✵ Income

✵ Transfer

➜ Categories

✵ Income Categories

✵ Expenses Categories

➜ Debt & Bill Tracker

➜ Subscription Tracker

✵ Upcoming Reminder

✵ Next Month Reminder

➜ Wishlist

➜ Months at a Glance

➜ Reports

➜ Database

#Notion#notion template#notion finance#finance tracker#finance#planner#template#digital planner#etsy#etsyseller#etsystore#account#transactions#debt#personal debt#wishlist#debt tracker#subscription#subscription tracker#finance dashboard#dashboard#notion dashboard

16 notes

·

View notes

Text

"If you think nobody cares if you're alive try missing a couple car payments." -Earl Wilson

#personal debt#credit card debt#student loan debt#street photografie#street photographer#streetsnap#street photography#quotes#quotations#life quotes#quoteoftheday#urban photography#photographer#streetleaks#streetphotography

9 notes

·

View notes

Text

#go fund me#go fund me campaign#debt trap#debts#personal debt#debt help#debt#tory cunts#tory britain#tory scum#energy crisis#cost of living crisis#charity ninja#charity case#charity#signal boost#mutual aid#mutuals#lost in new who dis#lost in new#please consider helping#help us out#we need help#help#grateful#thank you#funny#humor#humour#funny cos it's true

4 notes

·

View notes

Text

https://gofund.me/4529c4a9

Please help out!!. Share this or donate. I desperately need help.

2 notes

·

View notes

Text

The Most Important Information to Give the IRS to Settle Your IRS Tax Debts

If you Owe Back Taxes, if you are suffering from an Economic Hardship and if can’t pay your Monthly Living Expenses, you May be in Luck!☘️

When you owe back taxes to the IRS, May suddenly become very interested in your monthly income and expenses!

In fact you may want the IRS to know about your personal financial situation!

You may want to share your monthly expenses, such as your;

• Housing costs

• Car payment, gas, and insurance

• Gas, water, electric and other utility bills

• Medical insurance

• Cell phone

• Groceries and dining out

…and much more.

Why would you share this information with the IRS?

It all comes down to what the IRS calls Allowable Living Expenses.

The second you become a tax debtor, the IRS has a Secret tax lien against everything you own, including your future income. This is a feature of federal law, and it’s the basis for all the other collection actions that the IRS can take against you, such as a Wage Garnishment or Bank Levy.

Because of the lien, the IRS legally has a say in how you spend your money. Nobody likes this, but it’s the reality of how the US tax code works.

As with most laws, there is a long and complicated list of rules that go into determining what place the IRS holds in line behind or ahead of your other creditors, but the bottom line is that the IRS wants to get paid, and they have power to make your life a living nightmare by enforcing the tax laws over your money and assets.

It’s not all bad, however. There are specific legal protections that exist to prevent the IRS from taking everything you own. In simple terms, the IRS is not allowed to make you destitute. In other words, they are not allowed to put your family out on the street or force your children to starve if it creates an Financial Hardship on you and your family.

This is where those Allowable Living Expenses (ALE) come in. The IRS must allow you to pay all your basic living expenses, even if it means you cannot pay the IRS what you owe them. Sounds Great! Mostly, other than the tax lien they may file.

The IRS has legal standards that is required to follow and allow you and your family to pay before the IRS can collect anything. These are the usual categories:

• Food, clothing, personal care products, and “miscellaneous”

• Out of pocket health care costs

• Vehicle ownership and operating costs

• Rent or mortgage

• Utilities, including gas, water, electric, cell phone, Internet, and more

For vehicle operating costs, housing, and utilities, they do take into account regional variations for these costs. The rest are all based on national numbers. All the numbers also have adjustments based on family size.

These numbers “dictate” what the IRS will allow you to spend every month to live. Your income, when compared to these allowable standards, is what determines which IRS tax relief options you may be eligible for.

If your income is less than the total monthly allowable living expenses for Honolulu or where you live and family size, you might be eligible for a program that allows you to pay the IRS nothing. Yes, nothing. Zero. Nada. Zilch.

If your income is also less than the total monthly allowable living expenses, the IRS calculate for you, but you have assets – such as lots of equity in your home, stocks, bonds, classic cars, crypto, or the world’s most valuable Vinyl Record collection – then they’re going to take into consideration the value of those assets, too. But, in such a situation, you may be able to settle your tax debt for less than what you owe, and walk away from the rest.

If your income is more than the allowable living expense calculation, then the IRS is going to take that “excess” income into consideration for a reduced settlement. If you’re not eligible for a reduced settlement – which most people are not – then this “excess” income becomes the monthly minimal payment the IRS can require as a monthly payment.

One of the first things that Tax Relief Services can help our clients when they hire us to help them with a tax debt problem is to conduct a detailed Preliminary Analysis the exact same detailed financial analysis that the IRS should do but most of the time will not. We do the Preliminary Analysis for a number of reasons, such as:

1. Determining which IRS programs you’re eligible for.

2. Seek opportunities to legally increase your allowable living expenses.

3. Determine if the IRS balances are correct.

4. Look for unique circumstances that might open doors to outside-the-box resolution options.

This preliminary financial analysis is crucial for us to be able to get the best possible deal for our clients. Since the vast majority of tax debtors will end up on a monthly payment plan to the IRS, our job is to help get you the smallest possible monthly payment and help you minimize the short-term financial impact on your budget.

The IRS is NOT LOOKING OUR FOR YOU, BUT TAX RELIEF SERVICES IS!

If you’re in a situation where the IRS is hounding your, then we should chat. You don’t want to wind up in a situation where the IRS simply pigeon-holes you into the situation that is most convenient for them, leaving you unable to pay other monthly bills. Just schedule a time to chat:

WWW.TAXRELIEFSERVICES.COM

CALL TODAY!

TAX PROBLEMS DON’T GO AWAY!

808.589.232

#accounting#tax relief#taxreduction#tax#personal debt#tax expert#tax help#taxprofessional#tax reprieve#taxpayers#irs#financial#taxes#business#tax return#tax preparation

5 notes

·

View notes

Text

The Fault in our Financial Institutions (Attempt # 1)

(You might be wondering why I placed attempt numbers. My thoughts and opinions about things, over time, could change. I am more than open to learning from others. Enjoy!)

I hate mathematics, but I love learning about how stakeholders of different financial institutions behave. I could talk about it all day, like how I could spend more than 24 hours discussing why Heartstopper is a book that I would carry with me for the rest of my life.

For this post, I will be talking about The Fault in our Financial Institutions. Our financial institutions in the Philippines have so much growth potential, given the emergence of Financial Technologies. Apart from the fact that we are still gradually transitioning to digital financial transactions, mobile ownership and internet usage are also high. Despite the growth of FinTech, there is still so much room for improvement in terms of financial inclusivity.

I'll start with a mini introduction.

If there is something that I personally am tired of hearing from up-and-coming FinTech companies in the Philippines, it is this:

"Here in [Insert Name Here], we came up with this business/application to promote financial inclusion in the Philippines."

For some financial institutions, I would agree--But for some? Not so much. Problems with financial inclusion in the Philippines are more than what is seen on the surface. The problem is that there are more problems underneath these surface problems. More often than not, the remedy to these problems could be solved already by existing solutions.

I listed down some of the problems of financial institutions in the Philippines. Some problems are already common sense, but these problems are those that are rarely addressed, thinking that it is normal. Here are some of those problems:

#1) Transparency is not enough. Financial institutions should make a conscious effort to explain the fine print before a consumer avails of a financial product.

Yes, and by explaining the fine print, it means having to explain every word or detail in written agreements. This is one thing that most businesses from Big Tech fail to do. I am not quite sure if it was designed this way for these companies to take advantage of their users, but I would like to believe otherwise for now.

Contracts could be lengthy and incomprehensible, and even people like me dislike reading them at times. There could be a jargon that is difficult to understand, a sentence that is unclear, or an agreement that one half-heartedly agrees with. However, users and customers are forced to agree with the business either way, which is why they choose to not read these contracts. Furthermore, the inability of most Filipinos to fully understand the texts in black and white right away leaves them at a disadvantage more often than not. This information asymmetry then becomes a source of concern in the long run. Service fees are not explicitly mentioned, and penalties for violations are not thoroughly explained.

It is about time that financial institutions take a step back and look at agreements from an average person's perspective. They must be able to answer the following questions:

Can a person without financial background understand the agreement?

Do customers have any resources that they could check to read about it more?

Would anyone be available to answer their queries shortly?

#2) No customer should be begging for active and responsive customer support.

Let us address the elephant in the room: Customer services for most companies are inefficient. No, they are not because of the employees that work in this part of the business. Instead, customer service inefficiencies are often caused by businesses that put customers at the bottom of their priorities.

This applies to all industries, but I would like to specifically call out financial services businesses. They are all so quick keeping deposited money. Financial institutions have to make sure that the speed of their customer service is at par. They should not just shove people away without providing them an answer and be responsible for addressing queries.

Yes, customer services also have costs. This is why financial institutions should explain financial products and services in detail. It avoids several issues, which include:

Angry customers screaming at your phones for not knowing about what was supposed to be explained in the agreement;

Confused customers inquiring about the different fees and charges applied to their accounts; and

Unaware customers who are not knowledgeable about some terms in the agreement.

Fewer costs and better customer service? Yes, please!

#3) Lastly, no one should be taken advantage of because of emotional distress.

Yes, I am talking about you, Payday Loan Providers. Providing people with instant loans with astronomically high-interest rates. I am bad at Calculus, but I know my Economics, and I am aware that the rates should cover the risks and the costs of doing business. However, some of these high rates are becoming unreasonable and unjustifiable.

If you are a decent person with empathy and consideration in mind, you would understand that charging high on loans taken out of emergency are those who are left with no more choice but to resort to borrowing. While high profits are the goals of most businesses, empathy is equally just as important.

A bit of storytime, the most out-of-touch comment I have heard from a borrower in my entire existence has to be this one: "If they could not afford to pay their loans, then they do not have every right to bring their parents to a hospital." From then on, I blocked that person from all my social media accounts. I did not need toxic people like that in my life. I do not need those types of people in my life.

Okay, I suddenly am mentally drained after all this typing. I also have schoolwork to do for now. I will probably continue writing and commenting about this tomorrow.

3 notes

·

View notes

Text

Personal Debt in the UK: A Comprehensive Overview

New Post has been published on https://www.fastaccountant.co.uk/personal-debt-in-the-uk/

Personal Debt in the UK: A Comprehensive Overview

In this comprehensive overview, you will explore the current landscape of personal debt in the UK. As of June 2023, the average personal debt for adults stands at £34,597, while households carry an even greater burden of £65,529. The United Kingdom’s collective interest payments on individual debts are projected to reach a staggering £67,313 million over the span of 12 months, averaging £184 million each day. Unsecured debt, amounting to £4,087 on average, contributes significantly to this national predicament. The article also sheds light on the primary factors leading to such high levels of debt, including unemployment, reduced income or benefits, and a lack of financial control. Delving further, it is evident that over 51% of UK adults have relied on consumer credit within the past year, underscoring the dependence on borrowed funds. Among specific demographics, young adults aged 18 to 34 face the greatest non-mortgage debt, averaging around £10,400. Additionally, men carry higher levels of personal financial debt compared to women, with an average of £2,800 and £1,800, respectively. Amidst these concerning figures, it becomes apparent that the average savings rate in the UK remains low, leaving many households with less than £1,500 in savings. Through this exploration, you will gain a comprehensive understanding of the personal debt landscape in the UK.

Definition of Personal Debt in the UK

Personal debt in the UK refers to the amount of money owed by individuals, encompassing various forms of debt such as credit card debt, mortgage debt, financing debt, and unsecured debt. It is a financial obligation that individuals incur, often as a result of borrowing money from lenders or financial institutions. These debts can accrue interest over time and can have significant implications for individuals’ financial well-being.

Types of personal debt

Credit card debt: Credit card debt is one of the most common forms of personal debt in the UK. It refers to the outstanding balances individuals have on their credit cards, which they are required to repay either in full or through monthly instalments. Credit card debt often incurs high interest rates, making it challenging for individuals to repay their debts efficiently.

Mortgage debt: Mortgage debt is another prevalent type of personal debt in the UK. It primarily pertains to the outstanding balance individuals owe on their mortgages. Mortgages are long-term loans taken out to finance the purchase of a property. The debt is repaid through monthly mortgage payments, which typically consist of both principal and interest.

Financing debt: Financing debt refers to debts that individuals incur when purchasing big-ticket items, such as vehicles, furniture, or appliances, through financing options such as hire purchase or personal loans. Financing debt allows individuals to spread the cost of their purchases over a specified period but often incurs interest charges.

Unsecured debt: Unsecured debt encompasses various forms of debt that are not secured against any specific asset, such as personal loans, payday loans, or overdrafts. Unlike secured debt, unsecured debt does not require collateral. However, unsecured debt often carries higher interest rates due to the increased risk associated with lending money without collateral.

Statistics on Personal Debt in the UK

Average personal debt in the UK (as of June 2023)

As of June 2023, the average personal debt in the UK stood at £34,597 for adults. This figure represents the average debt burden faced by individuals across different age groups, income levels, and socioeconomic backgrounds. Additionally, the average personal debt for UK households was £65,529 during the same period. These statistics indicate the significant financial obligations individuals and households face in the UK.

Average personal debt for adults

The average personal debt for adults in the UK is an essential indicator of the financial landscape and the debt burden individuals carry. With an average debt of £34,597, individuals may encounter challenges in meeting their financial obligations, repaying their debts, and achieving financial stability.

Average personal debt for households

The average personal debt for households provides a comprehensive picture of the overall debt burden families face in the UK. With an average debt of £65,529, households may face difficulties in managing their debts and balancing their budgets effectively. High levels of personal debt within households can lead to financial stress, strained relationships, and limited economic mobility.

Increase in personal debt since 2022

Personal debt in the UK has seen an increase of £1,187 since 2022. This rise in debt suggests that individuals and households are taking on additional financial obligations or struggling to repay their existing debts. The increase in personal debt highlights the need for effective financial management and debt repayment strategies to avoid further financial hardships.

Aggregate interest payments on individual debts

The United Kingdom’s aggregate interest payments on individual debts were projected to reach £67,313 million over a 12-month period. This staggering figure represents the accrued interest paid by individuals on their various debts, further adding to their overall financial burden. The substantial sums directed towards interest payments highlight the importance of understanding the terms and conditions of borrowing and the potential long-term implications.

Daily average interest payments on individual debts

On a daily basis, the United Kingdom sees an average interest payment of £184 million on individual debts. This figure illustrates the significant amount of money directed solely towards interest payments. The daily interest payments underscore the ongoing financial strain faced by individuals in managing their debts effectively and highlight the need for improved financial literacy and debt management practices.

youtube

Causes of Personal Debt in the UK

Personal debt in the UK can arise from various circumstances and factors. Understanding the causes of personal debt is crucial in addressing and mitigating these issues effectively.

Unemployment or redundancy

One of the primary causes of personal debt in the UK is unemployment or redundancy. When individuals lose their jobs or experience a reduction in income due to redundancy, they may struggle to meet their financial obligations, leading to increased reliance on credit cards or loans to cover essential expenses.

Diminished income or benefits

Diminished income or benefits can significantly impact individuals’ ability to manage their finances and repay their debts. Factors such as job loss, reduced working hours, or changes in government welfare policies can all contribute to a decrease in income or benefits. When individuals face a significant reduction in their financial resources, they may resort to borrowing to maintain their standard of living.

Lack of financial control

A lack of financial control is another significant factor contributing to personal debt in the UK. Poor budgeting skills, overspending, and a lack of financial discipline can result in individuals accumulating debt beyond their means. This lack of control can lead to a cycle of borrowing and indebtedness.

Unforeseen circumstances

Unforeseen circumstances, such as medical emergencies, accidents, or unexpected expenses, can also contribute to personal debt. When faced with unexpected financial burdens, individuals may turn to credit cards or loans to cover the costs. These unforeseen expenses can disrupt individuals’ financial stability and lead to long-term debt.

Consumer Credit Usage in the UK

Percentage of UK adults using consumer credit

Over 51% of UK adults have used consumer credit in the past year. This indicates a significant reliance on borrowed money to finance various purchases and expenses. The high percentage of adults utilizing consumer credit signifies the importance of accessible credit options in the UK.

Reliance on borrowed money

The reliance on borrowed money among UK adults highlights the challenges many individuals face in maintaining their desired standard of living. With rising living costs and stagnant wages, individuals may turn to credit cards, personal loans, or other forms of consumer credit to bridge the gap between income and expenses.

Types of consumer credit

Consumer credit encompasses various types of borrowing, including credit cards, personal loans, payday loans, store cards, and hire purchase agreements. These forms of credit allow individuals to finance purchases, manage cash flow, and cover immediate expenses. Understanding the different types of consumer credit is vital in making informed borrowing decisions and avoiding excessive debt.

Non-mortgage Debt among Young Adults

High levels of non-mortgage debt among young adults (18-34 years old)

Young adults between the ages of 18 and 34 face the highest levels of non-mortgage debt in the UK. Factors such as student loans, credit card debt, and financing debt contribute to the financial burden faced by young adults. The high levels of non-mortgage debt among this age group highlight the challenges they encounter in establishing financial stability and planning for the future.

Average non-mortgage debt among young adults

The average non-mortgage debt among young adults in the UK is approximately £10,400. This significant amount of debt can impose long-term financial constraints, hinder savings growth, and limit young adults’ ability to achieve their financial goals. Addressing the issue of non-mortgage debt among young adults is essential for promoting financial well-being and economic mobility.

Gender Differences in Personal Debt

Men with personal financial debt

On average, men in the UK carry higher levels of personal financial debt compared to women. The average personal financial debt for men is £2,800, reflecting the additional financial obligations men often bear. Factors such as higher average incomes, different spending patterns, and financial decision-making contribute to the higher levels of personal financial debt among men.

Women with personal financial debt

Women in the UK also face personal financial debt, albeit at slightly lower levels compared to men. The average personal financial debt for women is £1,800. Gender-specific factors, including lower average incomes, unequal pay, and societal norms, contribute to the disparities in personal financial debt between men and women.

Average financial debt for men

The average financial debt for men in the UK is £2,800. This debt burden can have significant implications for men’s financial well-being, economic mobility, and overall financial stability. Understanding the average financial debt for men is crucial in addressing the unique challenges and opportunities they face in managing their debts and achieving financial security.

Average financial debt for women

Women in the UK face an average financial debt of £1,800. This lower average debt highlights the different financial circumstances women encounter and the challenges they face in managing their debts effectively. Addressing the average financial debt for women is vital in promoting financial equality, empowerment, and economic well-being.

Low Savings Rate in the UK

Average savings rate in the UK

The average savings rate in the UK is low, with many households failing to maintain an adequate level of savings. On average, individuals save a small percentage of their income, leading to a lack of financial security and a limited cushion for unexpected expenses or emergencies. The low savings rate indicates the need for improved financial planning, budgeting, and savings habits.

Low savings rate among households

UK households, on average, have minimal savings, with many struggling to accumulate sufficient funds for future needs. This low savings rate can contribute to financial vulnerability and limited opportunities for households. Addressing the low savings rate among households is essential in promoting financial resilience, stability, and long-term financial well-being.

Amount of savings in UK households

Many UK households have less than £1,500 in savings, highlighting the limited financial resources available to confront unforeseen expenses, retire comfortably, or make significant investments. The low amount of savings further emphasizes the need for improved financial literacy, savings habits, and long-term financial planning.

Impact of Personal Debt on Mental Health

Link between personal debt and mental health

There is a significant link between personal debt and mental health. High levels of personal debt can contribute to increased stress, anxiety, and depression, impacting individuals’ overall mental well-being. Financial worries and the strain of managing debt can impose a heavy psychological toll on individuals, affecting their mental health and overall quality of life.

Effects of personal debt on mental well-being

Personal debt can have wide-ranging effects on an individual’s mental well-being. It can lead to feelings of hopelessness, a sense of being trapped, and constant worry about finances. These effects can disrupt personal relationships, work productivity, and overall life satisfaction. Managing the psychological impact of personal debt is crucial in promoting mental health and overall well-being.

Strategies for managing personal debt and mental health

Managing personal debt and promoting positive mental health requires individuals to adopt strategies that address both financial and psychological aspects. Seeking professional financial advice, creating realistic budgets, engaging in self-care activities, and accessing mental health support services can be beneficial in reducing the impact of personal debt on mental well-being. Implementing these strategies can help individuals regain a sense of control over their finances and improve their overall mental health.

Government Initiatives and Regulations

Efforts by the UK government to address personal debt

The UK government has implemented various initiatives to address personal debt and support individuals facing financial difficulties. These efforts include the provision of debt advice services, financial education programs, and debt management plans. The government aims to enhance individuals’ financial literacy, promote responsible borrowing, and provide support structures for those struggling with personal debt.

Regulations on lenders and credit providers

The UK government has also established regulations on lenders and credit providers to ensure responsible lending practices and protect individuals from predatory lending. These regulations include caps on interest rates, restrictions on advertising and marketing practices, and requirements for lenders to assess borrowers’ affordability. The aim is to create a fair and transparent lending environment that minimizes the risks associated with personal debt.

Debt counselling and support services

Debt counselling and support services play a vital role in helping individuals manage their personal debt and improve their financial well-being. These services provide professional guidance, debt management strategies, and emotional support to individuals struggling with debt. Debt counselling services aim to empower individuals, develop effective debt repayment plans, and restore financial stability.

Conclusion

Personal debt in the UK encompasses various forms of financial obligations that individuals incur, including credit card debt, mortgage debt, financing debt, and unsecured debt. The average personal debt for adults and households in the UK is significant, with an increase observed since 2022. Factors such as unemployment, diminished income, lack of financial control, and unforeseen circumstances contribute to personal debt. The reliance on consumer credit, especially among young adults, highlights the need for effective debt management practices and financial literacy. The gender differences in personal debt, low savings rate, and the impact of personal debt on mental health call for government initiatives, regulations, and the provision of debt counselling and support services. By addressing these issues and promoting responsible borrowing and financial management, individuals can strive towards achieving financial stability, reducing personal debt, and improving overall well-being.

0 notes

Text

Personal Debt in the UK: A Comprehensive Overview

In this comprehensive overview, you will explore the current landscape of personal debt in the UK. As of June 2023, the average personal debt for adults stands at £34,597, while households carry an even greater burden of £65,529. The United Kingdom’s collective interest payments on individual debts are projected to reach a staggering £67,313 million over the span of 12 months, averaging £184…

View On WordPress

0 notes

Text

When Does Car Refinancing Make Sense?

Learn how car refinancing can lower interest rates, reduce monthly payments, and offer access to equity. Understand when it makes sense and how it benefits you. Consider factors, costs, and long-term implications. Make an informed decision with expert advice. Read More

#debtfree#debt review#debtmanagement#personal debt#credit score#debt#struggling to pay debt#CarRefinancing#SaveMoney#LowerInterestRates#FinancialGoals#ExpertAdvice

0 notes

Text

I have fallen into the trap of debt. It’s a very cliche story, college debt, family tragedy, financially illiterate, and buying into the idea that borrowing more will allow me more cash to spend. I used to care about my accounts going negative, I used to make sure I knew how much I owed and just lived with not having money til I got paid. But here I am in the opposite situation I’m so embarrassed and feel so stupid. I have no money to spend after paying off things and I know this is an inherent fault of my perception of shopping and money.

I am a trash person

0 notes

Text

Please PLEASE help if you can. Even if you just reblog. I have so many followers on here if you all just reblogged it might reach a bigger audience.

A little background info - I left my abusive partner when my little girl turned one. He’s left me in debt, with bailiffs chasing me. Now with the energy crisis I’ve got bailiffs from them too.

He pays no support - outright refuses. I’m trying to get back into work as I can’t afford to survive like this but I have no family that can help out and the times she’s in nursery don’t help in the job search.

Anyway. Please donate if you can. Reblog if you can. Or tag people that you know can help

Thank you. Amanda & Isabelle

#donationsblog#please consider donating#donate if you can#please consider helping#we need help#charity ninja#charity case#charity#go fund me#fund me#reblog#charity blog#debt trap#personal debt#debts#debt help#energy crisis#cost of living crisis#lost in new#boost#signal boost#financial aid#mutual aid#crowdfunding#crowdsourcing

2 notes

·

View notes

Text

Update #2

I was able to file my response at the courthouse and Mail the certified copy to the lawyer today.

The cost of all that came out to about $25 so I am extremely grateful for the person who donated to my gofundme.

I was an anxious mess when I got home, and I am super grateful for living with my friend group so that upon getting home they helped a lot in my decompressing.

Thank you for boosting my posts and thank you for the people helping me!

CashApp: $DresdenOHaraGray

PayPal: @Dresdenohg

GoFundMe:

#debt collection#go fund me#money#personal debt#credit cards#dumpster fire#credit#law#i'm being sued#im being sued#financial assistance#finance#financial#how to earn money#gofundme#raising funds#fundraising#update

0 notes

Last Seen Blogs

half-drag

boys in pretty makeup

whiteclawx

simple hawkfrost enjoyer

fatalfendi

𝕳𝖔𝖔𝖉 𝕭𝖗𝖆𝖙.

majonsaraysalamat

Untitled