#ppp lender

Text

I have a genuine lender from London, U.K who offer financial instrument lease and sale at a reasonable price with affordable procedure and condition. Our bank instrument lender offer Fresh Cut and Seasoned bank instrument such BG, SBLC, MTN and Confirmable Bank Draft (CBD), which can be engage into PPP Trading, Outright Discounting, signatory project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects.

With our bank instrument you can establish a line of credit with your bank or secure loan for your projects in which our bank instrument will serve as collateral in your bank to fund your project.

We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable. Below procedure is for BG/SBLC and MTN lease, other bank instrument procedure will be provided on request.

DESCRIPTION OF INSTRUMENT:

1. Instrument: Bank Guarantee {BG/SBLC}

2. Total Face Value: Eur 10M{Minimum} to Eur 10B{Maximum}

3. Issuing Bank: HSBC Bank Plc and Barclays Bank Plc {London, U.K}

4. Age: One Year and One Month

5. Leasing Price: 6%+2% =8%

6. Delivery: MT-760 {Bank-To-Bank Swift}

7. Payment: MT103/23

8. Hard Copy: Bonded Courier Service {within three banking days}

Thank you

Marty Jeffrey.

email:[email protected]

#construction#loans#personal loans#business loan#government#import export business#agriculture#avaition#sblc monetization#sblc#financial services#financial#medicalprofessionals#small business#businessowner#entrepreneur#realestate#real estate developer#investment#farmers#farmlife#organic farming#oil and gas#renewableenergy

8 notes

·

View notes

Text

Just in case some of you are skeptical about the predatory lending practices of student loans in the United States. This post is long.

Referring to the picture above this is just one account of about $70k in my student loans all broken up into ~15 or so different segments of $3k to $5k like this across multiple lenders, including multiple "accounts" with the federal government, all managed by one company (that I didn't get to choose). Every one of those accounts are like this. I've never been in deferment, I've never missed one payment. For more than half of these accounts I've paid more into a lot of these loans than the principle balance and still owe a total ~$70,000 from an initial principle of ~$61,000. Consolidating them into one loan won't change much of anything in terms of cost, payment, or interest (and last time I did the math, the little that would change wasn't in my favor) and hidden in the fine print of all of those consolidation loan offers is the disqualification of any future debt relief by the federal government.

The reason centrist-Democrats and all Republicans have brainwashed centrists and conservative US taxpayers into thinking their tax bill will go up if student loans were more significantly forgiven, and why any Democratic president hesitates to provide actual, substantial relief to anyone who wasn't very specifically defrauded by scam institutions, is because it isn't just some network of central banks that provided these loans that can just take the hit and demand a tax write-off and government subsidy for the charity: the loans are securitized; they're asset-backed by multimillion and multibillion dollar investors. These types of investment securities are called SLABS, and if you live in the U.S., especially if you vote but absolutely even if you don't, you should resolve to look up more than just that one link to educate yourself on how they came about and how they've imprisoned this country into over a trillion dollars in debt that will never get paid.

So many of these obscenely wealthy investors donate substantial amounts to our plutocratic political campaigns that if either party were responsible for cancelling a substantial amount of these loans the investors that donated to those campaigns will move their donations to the other party in retaliation for making their profitable SLABS unprofitable. It's absolutely not because our tax bills will go up, that's just what center-right Democrats and Republicans have ALWAYS used to scare conservatives into regressive fiscal decisions under the deceptive euphamism of "fiscal responsibility." If you've ever felt like it was unfair or wrong for a borrower to have the loans they willingly took out be forgiven, I promise you that it is an opinion you've been conditioned into believing that intentionally removes nuance and context from the actual issue specifically so that you'll continue to vote for politicians that they themselves then vote (on your behalf!) to give billion-dollar corporations the money you claim you're against giving away in the first place. Many of our politicians, red and blue, have had federal loans forgiven. You don't even have to look that far back as the federal government forgave PPP loans just last year and so many politicians that have been hootin and hollerin and angry that a small fraction of our loans were forgiven this week had HUNDREDS OF THOUSANDS, sometimes even MILLIONS of dollars forgiven less than a year ago.

$10,000 isn't going to help me very much. I'm not going to feel the relief (or much of it at least), and that's okay to an extent. The only reason I'm not against this loan forgiveness decision is because for the people who will have their debt cut in half or forgiven entirely, this is huge. But higher education is still unnecessarily and criminally expensive and loan interest rates need to be dropped to lower than 1%. That's what we needed to solve the crisis. Otherwise, and even if it was total forgiveness that was announced instead of $10k, this is just going to cycle back into the exact same problem with the exact same debt owed.

3 notes

·

View notes

Text

Financial technology firms at the front lines of approving loans through the Paycheck Protection Program — intended to help small businesses survive during the pandemic — lacked fraud controls, chased high fees to the detriment of some borrowers and sometimes exploited their business relationships to arrange suspect loans for the companies’ own executives. One such executive falsely claimed in loan documents to be a Black veteran and received loans through multiple business entities.

These are among the findings in a report released Thursday by the House Select Subcommittee on the Coronavirus Crisis, which investigated the role financial technology firms, known as fintech companies, played in propagating PPP loan fraud. The committee referred its findings to the Department of Justice and to the Small Business Administration’s Office of Inspector General.

“Even as these companies failed in their administration of the program, they nonetheless accrued massive profits from program administration fees, much of which was pocketed by the companies’ owners and executives,” said Rep. James Clyburn, D-S.C., the subcommittee’s chairman, in a statement released with the new report. “On top of the windfall obtained by enabling others to engage in PPP fraud, some of these individuals may have augmented their ill-gotten gains by engaging in PPP fraud themselves.”

Fintechs were often the front door to the PPP program: They processed huge quantities of loan applications and were hired in part to vet the documents for obvious signs of fraud before sending them on to lenders. But the vetting was often lacking. The investigation kicked off shortly after ProPublica reported that one fintech, Kabbage, approved hundreds of loans for fake farms, including what claimed to be a potato farm in Palm Beach, Florida, an orange grove in Minnesota and a cattle farm on a sandbar in New Jersey. “The illegitimacy of these purported farms,” Clyburn wrote in a letter to Kabbage at the time, “would have been obvious if even the bare minimum of due diligence had been conducted on the loan applications.”

The report found that Kabbage at one point had only one full-time anti-fraud employee and considered the risk of approving fraudulent loans minimal. “A fundamental difference is the risk here is not ours — it is SBAs,” said one risk manager to his team when asked about identifying fraudulent loans, according to a company email cited in the committee’s report. Kabbage’s then- head of policy wrote that “at the end of the day, it’s the SBA’s shitty rules that created fraud, not [Kabbage].”

1 note

·

View note

Text

Kinstellar Advises Banking Consortium On Telekom Srbija's Tower Deal - Kinstellar

Kinstellar’s team in Serbia, together with global law firm Paul Hastings, has successfully advised Deutsche Bank, Alpha Bank, UniCredit, and UniCredit Bank Serbia on a EUR 205 million financing for global investment firm Actis in relation to their acquisition of a carved-out tower portfolio from Telekom Srbija, a leading telecommunications operator in the Central and Eastern European (“CEE”) region.

The carved-out portfolio is comprised of approximately 1,800 macro towers across Serbia, Bosnia & Hercegovina, and Montenegro.

Kinstellar’s team, led by Petar Kojdić (Partner) and Mina Srećković (Managing Associate), played a pivotal role advising on the financing aspects of this transaction. Our services included structuring financial arrangements and negotiating financing documents.

The communication towers market in the CEE and Western Balkans regions is expected to experience substantial growth in the coming years, driven by escalating consumer demand for mobile data, the introduction of advanced technologies like 5G and 6G, and evolving mobile capacity and coverage needs.

Telekom Srbija, the leading telecommunications operator in Serbia, is a key player shaping the communication landscape in the CEE region. Decisions such as the recent sale of a carved-out tower portfolio showcase Telekom Srbija's adaptability to global trends and its focus on optimising its assets.

Petar Kojdić is a Partner in the Belgrade office and the head of the firm’s Banking & Finance service line in Serbia.

Petaradvises lenders and borrowers of all types on a wide range of cross-border and local finance transactions, including acquisition and leveraged finance, project finance, debt restructurings and re-financings as well as loan and portfolio sales transactions.

Petar also focuses on legal and regulatory advice related to structured finance, netting, derivatives, financial collateral, securitisation as well as repo and capital markets transactions. His work involves negotiating finance and hedging documents with various counterparties (banks and other financial institutions, funds, corporates and sovereign entities) and issuing netting, collateral and other legal opinions. Petar is an author of ISDA's netting opinion for Serbia.

Mina Srećković is a Managing Associate in the Belgrade office.

With over ten years of experience, Mina specialises in corporate and banking & finance, with special knowledge of PPPs, concessions, public debt financing, foreign exchange regulations and cross-border transactions, project finance, non-performing loans, equity and debt securities transactions, as well as regulatory compliance, corporate governance and licensing of institutions operating in the banking and financial sector in Serbia.

Petar Kojdić Partner

+38 11 3210 [email protected]

Mina Srećković Managing Associate

+381 69 1811 [email protected]

0 notes

Text

Exploring Alternative Financing in the Infrastructure Sector: Addressing Funding Challenges and Opportunities

The infrastructure sector serves as the backbone of economic development, enabling growth and societal progress. In the near future, this sector will be playing a major role in advancing INDIA to a 5 trillion-dollar economy. However, traditional modes of financing often fall short in meeting the colossal financial demands required for infrastructural development. Alternative finance mechanisms are emerging through digital technologies like crowdfunding and tokenization, helps transcending the limits of traditional banks and providing a lower entry cost for retail investors. They can also demonstrate community interest, sending a reassuring signal to larger institutional investors.

Several factors contribute to the urgency for alternative financing:

Insufficient Public Funding: Government budgets often prove inadequate to cover the expansive costs of infrastructure projects. Shrinking public funds and competing priorities compel exploration beyond traditional funding sources.

Challenges at Private participation: Private-sector participation in infrastructure (PPI) comes mainly through privatisation and public-private partnerships (PPPs) and it leans more on the debt market, especially bank lending. Commercial bank loans, specifically syndicated loans, are the primary mechanism to fund infrastructure; the bond market is still developing. Equity issuance and corporate bonds represent another source, but tough to have a right balance between fund and share. High dependency on debt market (banks), makes it very difficult to get the right amount of fuel required.

Banks - the major source of funding in country: The centrality of banks in funding infrastructure poses three challenges: lending duration, volume of loanable capital and community engagement. These problems arise due to multiple reasons like loanable funds are largely composed of demand deposits, the tenor of their investments is limited these investments hardly grab attention of public.

Risks and Uncertainties: The adequacy of risk assessment, particularly for large transactions like infrastructure projects, is a key consideration in promoting alternative finance. Infrastructure as an asset typically has substantial upside. However, the experience of banks in India indicates it can also be a drag on the balance sheet of lenders if vetting is weak.

Global Economic Challenges: Economic downturns, such as the recent global recession, have strained public finances. During tough economic times, governments may cut back on infrastructure spending to allocate resources to more pressing needs. In such times, alternative financing models can provide resilience and stability to infrastructure investments.

The way forward involves exploring and implementing a spectrum of alternative financing mechanisms apart from the existing ones:

Infrastructure Bonds and Green Financing: Issuing infrastructure bonds and embracing green financing initiatives attract investors interested in sustainable projects. Green bonds, for instance, fund environmentally friendly infrastructure, attracting a specific pool of investors. Although this has been introduced in the market already, but there is enough scope of scaling the financing method.

Crowdfunding and Community Investment: Engaging communities through crowdfunding platforms or local investment initiatives can garner support and funding for smaller-scale infrastructure projects. Crowdfunding can take the form of debt, equity, royalty, reward, or donation. Crowdfunding marketplaces customarily have lower investor entry cost than traditional securities markets, albeit online securities trading platforms for retail investors have proliferated. Additionally, the investors know of specific projects as opposed to general corporate needs in the traditional securities markets; recent innovations such as infrastructure bonds might be an exception.

Tokenisation: Tokenisation in the context of infrastructure divides the value of assets or the underlying securities (debt or equity) into smaller parcels before they are offered to potential investors. The tokens come in digital format to represent a claim on the physical asset or security. They are launched on blockchains guided by the terms of the smart contracts. Fraud and speculation may have dented the growth in fundraising through coin offerings, however, the concept of tokenisation can still potentially raise capital for infrastructure either through debt or equity.

Asset Recycling and Securitization: Governments can unlock capital by selling existing infrastructure assets (non performing) to private investors and then reinvesting the proceeds into new projects. Securitization involves bundling cash flows from multiple projects into tradable securities, attracting diverse investors.

In conclusion, the quest for alternative financing in the infrastructure sector is paramount to overcome funding challenges, expedite project implementation, and support sustainable development.

Reference: https://www.oecdilibrary.org/sites/0791297een/index.html?itemId=/content/component/0791297e-en

0 notes

Text

Mastering Project Financing: Strategies for Real Estate Developers By Coevolve Group

Embarking on a real estate development journey is an intricate process that demands not only a creative vision but also robust financial planning. Securing financing for real estate projects is often one of the most significant challenges that developers face. Whether you're a seasoned developer or just entering the field, mastering project financing is essential to bring your visions to life. In this blog post, we'll delve into strategies for overcoming financing hurdles and turning your real estate dreams into reality.

Understanding the Financing Landscape

The first step in mastering project financing is understanding the diverse landscape of funding options available to Top real estate builders in bangalore. Each option comes with its own benefits, risks, and considerations. Let's explore some of the most prominent funding avenues:

Traditional Bank Loans: These loans are secured through financial institutions like banks or credit unions. They typically offer competitive interest rates and longer repayment terms. However, they often require substantial collateral and a strong credit history.

Private Equity: Private equity investors provide capital in exchange for ownership shares in the project. This option can offer more flexibility and faster access to funds, but it requires giving up a portion of project ownership.

Crowdfunding: Crowdfunding platforms allow developers to raise smaller amounts of capital from a larger pool of investors. This democratized approach to funding can be particularly effective for smaller projects or niche markets.

Public-Private Partnerships (PPPs): In PPPs, developers collaborate with government bodies or agencies to fund and execute projects. These partnerships can provide access to government resources, land, and infrastructure support.

Factors Lenders Consider

When seeking financing, developers must understand the factors that lenders evaluate before extending funds. These factors play a pivotal role in determining whether a project is deemed viable and creditworthy. Here are some key considerations:

Project Feasibility: Lenders assess the viability of the project, including its location, market demand, and potential profitability. A comprehensive feasibility study demonstrating the project's potential for success is crucial.

Developer's Track Record: A developer's past successes and experience in similar projects can significantly influence a lender's decision. A strong track record indicates a developer's ability to deliver results.

Collateral and Equity: Lenders often require collateral or a certain level of equity investment from the developer. This demonstrates the developer's commitment to the project's success.

Repayment Plan: Lenders want assurance that the developer has a clear repayment plan in place. This includes detailing how the loan will be repaid, the project's cash flow projections, and the timeline for completion.

Presenting a Compelling Project Proposal

To secure financing successfully, developers must craft a compelling project proposal that resonates with lenders. Here are some tips to create a winning proposal:

Detailed Business Plan: Provide a comprehensive business plan that outlines the project's scope, objectives, timeline, and anticipated returns. Include market research, competitor analysis, and sales projections.

Financial Projections: Present accurate financial projections, including construction costs, operating expenses, and revenue projections. Clear financial data demonstrates your understanding of the project's financial aspects.

Risk Assessment: Address potential risks and challenges upfront. Present a risk mitigation strategy to show that you've thoroughly evaluated possible obstacles.

Team and Expertise: Highlight the expertise of your project team, including architects, contractors, and legal advisors. A skilled team boosts the project's credibility.

Coevolve Group: Your Trusted Partner

When it comes to securing financing and executing successful real estate projects, partnering with the right builders is paramount. Coevolve Group, recognized as one of the Plots at Sarjapur Road Bangalore, stands as a trusted partner for Eco Friendly Homes in Bangalore. With a commitment to innovation, quality, and sustainable practices, Coevolve Group offers expertise that can elevate your project from concept to reality. Whether you're envisioning Sustainable Projects in India or pioneering sustainable developments, Coevolve Group's experience can help you navigate the complexities of real estate development.

Mastering project financing is a fundamental skill for Builders In Bangalore. By understanding the financing landscape, considering factors that lenders evaluate, and presenting a compelling project proposal, developers can secure the funding needed to turn their visions into thriving realities. With the right strategies and partnerships, such as with Coevolve Group, developers can overcome financing challenges and build successful projects that leave a lasting impact.

Visit for more information: https://coevolvegroup.com/

Address: #476, 2nd Floor, 80 Feet Road,6th Block Koramangala, Bangalore - 560 095.

Call us: +91 9448694486

Mail: [email protected]

0 notes

Text

Small Banks: Advantages,Disadvantages, and a Key Role in Future Small Business Growth

By: Ken Chase.

When most people think about the banking industry, their minds tend to focus on big national and multinational financial institutions. However, America’s banks come in all sizes, and they all have their own vital roles to play in maintaining a stable and successful financial environment for the nation’s businesses and consumers. For their part, the country’s small banks continue to be one of the man drivers for ensuring small business growth across the U.S.

Defining “small bank”

To fully understand these banks’ important role in the financial ecosystem, it is critical to first define them. According to the Federal Reserve, the current definition of “small bank”applies to any banking institution that had assets of no more than $1.384 billion at the end of 2021. That definition reflects the current asset guidelines, which are updated annually to reflect changes in the inflation rate.

Small banks: advantages and disadvantages

For consumers and businesses trying to decide between various banking options, the choices can sometimes be confusing. While larger banks with greater assets may seem to be a better and more reliable option, small banks have many advantages over their larger peers. To make a sound decision, customers need to weigh those advantages against the smaller banks’ potential weaknesses. Making the wrong choice could hinder a customer’s ability to quickly get a mortgage or slow an entrepreneur’s efforts to keep a business afloat.

Smaller community banks do have some disadvantages, of course. Because they have fewer assets, they may not be able to service every type of lending activity. In addition, many of them have a limited number of branches, and may offer fewer financial services than their larger competitors. And while small, community banks have been finding creative ways to offer services like insurance and investments, the small bank niche continues to trail those larger banks in that area.

Despite those obvious disadvantages, small banks have many clear advantages over larger financial service providers. For example:

- Small banks generally provide a more personalized experience for their customers. The tellers and executives who live in the community often know their customers firsthand. They shop in the same stores. Their children go to the same schools. Those connections can be powerful and create a strong sense of community between the bank and its clientele.

- Local community bank employees may have greater autonomy when it comes to processing loan applications for individuals and businesses. While larger banks tend to rely on strict processing guidelines that focus entirely on credit scores, many small bank lending officers can review the entire loan application and exercise a greater degree of personal judgment. In many instances, local lenders can meet with a prospective borrower to ensure that they fully understand their unique circumstances and needs.

- Most small banks have access to the same levels of technology used by larger institutions, so the divide between small and large banks is scarcely noticeable. Like their larger competitors, community banks generally offer online banking services, access to ATMs, and card services that are comparable to those offered by larger firms.

Why smaller community banks continue to be trusted entities

It is also important to note that customers consistently report trust in their local banking institutions. That trend has been true for many decades but appears to have grown even stronger in recent years, largely due to the Covid-19 pandemic. According to reports, smaller banks played an outsized role in helping small businesses gain access to the critical PPP lending they needed to survive the nation’s Covid-related lockdowns. Those smaller banks’ nimble response to the crisis resulted in some businesses rethinking their relationships with larger financial entities.

Meanwhile, many of the nation’s largest banks reportedly gave priority to their wealthiest customers, who were allegedly allowed to avoid online application portals and instead submitted their applications directly to their bankers. According to reporting from the New York Times, that unequal treatment enabled almost all of the super-wealthy applicants to obtain approval for PPP loans, while only one of every-fifteen smaller retail banking clients got the help they needed.

Smaller banks across the United States appear to have served their customers better during the crisis, and that is likely to translate into even greater client trust in the future. Small business owners will continue to remember who stood by them during their most trying times, which will only serve to ensure strong bank-client relations in the coming years.

Managing growth in an ever-evolving economy

According to estimates, small banks represent a clear minority of banking institutions in the U.S. At the same time, however, these banks reportedly account for more than half of all small business lending in the country. They are also proving to be critical partners for fintech company growth, as that sector has seen a dramatic surge in startups in the last few years.

Small banks can continue to enjoy growth in the coming years by focusing on maintaining their core strengths, leveraging new technologies, and expanding their service offerings to meet changing customer expectations. Savvy banks will also increase their reliance on customer data to ensure that they provide the financial products clients want and need.

Read the full article

0 notes

Text

Denish Shadevan a.k.a. Danny Devan Pleads Guilty

Denish Shadevan, a.k.a. Danny Devan, Pleads Guilty to wire fraud, aggravated identity theft, and money laundering.

Greenbelt, MD (STL.News) Denish Sahadevan, a/k/a “Danny Devan,” age 31, of Potomac, Maryland, pleaded guilty today to wire fraud, aggravated identity theft, and money laundering, relating to his scheme to defraud lenders and the Small Business Administration (“SBA”) of more than $1.2 million in Paycheck Protection Program (“PPP”) loans and Economic Injury Disaster Loans (“EIDL”).

The guilty plea was announced by United States Attorney for the District of Maryland Erek L. Barron; Special Agent in Charge Thomas J. Sobocinski of the Federal Bureau of Investigation, Baltimore Field Office; and John T. Perez, Special Agent in Charge, Headquarters Operations, Office of Inspector General for the Board of Governors of the Federal Reserve System and the Consumer Financial Protection Bureau.

The Coronavirus Aid, Relief, and Economic Security (“CARES”) Act was a federal law enacted in March 2020 to provide emergency financial assistance to Americans suffering from the economic effects caused by the COVID-19 pandemic. Financial assistance offered through the CARES Act included forgivable loans to small businesses for job retention and certain other expenses, through the PPP, as well as EIDLs to help small businesses meet their financial obligations, both administered through the SBA.

According to the plea agreement, beginning in about March 2020, Sahadevan submitted EIDL and PPP applications on behalf of four Maryland entities that he controlled, often creating fraudulent and fabricated documents, such as tax forms and bank statements, to be used in the applications. In addition, Sahadevan used the identifying information belonging to a tax preparer that he knew, without that person’s knowledge or agreement, to legitimize the fabricated tax forms he created and submitted.

Specifically, Sahadevan admitted that he used his home in Rockville, Maryland, to create the fabricated documents and electronically apply for EIDL and PPP loans. Sahadevan applied for approximately 71 PPP loans totaling approximately $941,794.75 and successfully obtained approximately $146,000 in PPP benefits. Sahadevan applied for and received eight EIDLs totaling $283,900. On the EIDL loans, Sahadevan induced his father into becoming a co-signer for the loan, then forged his father’s signature on the loan application. Sahadevan’s father would not have agreed to sponsor the loan had he known of its fraudulent nature and contents.

As detailed in the plea agreement, Sahadevan caused the fraud proceeds to be deposited into bank accounts he opened specifically for that purpose, then laundered the funds by engaging in several monetary transactions, including purchasing and trading securities and cryptocurrency, settling personal debts, and making payments to his girlfriend.

In addition, between December 16, 2021, and January 10, 2022, Sahadevan applied to a financial institution for a $1,336,000 loan to purchase a property in Potomac, Maryland. In the loan application, Sahadevan failed to disclose the $283,900 he owed to the United States for the EIDL benefits he fraudulently received. Relying on Sahedevan’s representations, the financial institution approved the loan, which was used to purchase the Potomac property.

On February 24, 2023, law enforcement executed a search warrant at Sahadevan’s Potomac residence and recovered multiple electronic devices, a can containing approximately 18 driver’s licenses belonging to other individuals, what appeared to be a gold physical Bitcoin in a black case, and approximately $17,043 in cash found in a suitcase in a bedroom closet. Cash and Bitcoin constitute proceeds of the fraud scheme.

As part of his plea agreement, Sahadevan will forfeit the cash and Bitcoin seized during the search on February 24, 2023, and will be required to pay restitution and a forfeiture money judgment of at least $429,906.

Sahadevan faces a maximum sentence of 20 years in federal prison for wire fraud; a maximum of 10 years in federal prison for money laundering; and a mandatory sentence of two years in federal prison, consecutive to any other sentence imposed for aggravated identity theft. U.S. District Judge Deborah L. Boardman has scheduled sentencing for September 21, 2023, at 2:00 p.m.

The District of Maryland Strike Force is one of three strike forces established throughout the United States by the U.S. Department of Justice to investigate and prosecute COVID-19 fraud, including fraud relating to the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act. The CARES Act was designed to provide emergency financial assistance to Americans suffering the economic effects caused by the COVID-19 pandemic. The strike forces focus on large-scale, multi-state pandemic relief fraud perpetrated by criminal organizations and transnational actors. The strike forces are interagency law enforcement efforts, using prosecutor-led and data analyst-driven teams designed to identify and bring to justice those who stole pandemic relief funds.

SOURCE: U.S. Department of Justice

Read the full article

0 notes

Text

Approved Loans in USA

The United States has witnessed a significant rise in getting approved for a loan in recent years. As the economy recovers and financial institutions adapt to changing circumstances, more Americans are gaining access to credit. This article explores the factors contributing to this surge and highlights the impact of approved loans on individuals and the overall economy.

Economic Recovery and Financial Stability

The rebounding US economy after the global financial crisis, coupled with improved financial stability, has played a crucial role in the surge of approved loans. As businesses flourish and consumer confidence grows, financial institutions are more willing to extend credit to individuals and enterprises. The reduced risk of default and increased economic activity have created a favorable lending environment, making it easier for Americans to secure loans for various purposes.

Government Initiatives and Policy Changes

Government initiatives and policy changes have also contributed to the increase in approved loans. Programs such as the Small Business Administration's Paycheck Protection Program (PPP) and the Economic Injury Disaster Loan (EIDL) have provided crucial support to businesses, ensuring their survival during challenging times. Moreover, regulatory reforms aimed at increasing transparency and consumer protection have improved the loan approval process, instilling confidence in borrowers and lenders alike.

Technological Advancements and Digital Lending

Technological advancements have revolutionized the lending landscape in the United States. Online lending platforms, powered by algorithms and artificial intelligence, have streamlined the loan application process, making it faster, more efficient, and accessible to a broader population. These platforms analyze data points beyond traditional credit scores, enabling lenders to evaluate creditworthiness more accurately. The advent of fintech companies has increased competition among lenders, leading to more attractive loan terms and higher approval rates.

Benefits and Implications for Individuals and the Economy

The surge in approved loans brings numerous benefits to individuals and the overall economy. It allows individuals to pursue higher education, buy homes, start businesses, or invest in their professional development. By facilitating access to capital, approved loans foster entrepreneurship and innovation, generating job opportunities and economic growth. Moreover, responsible borrowing and timely loan repayments help individuals build credit and improve their financial well-being, enhancing their overall economic prospects.

Conclusion

The surge of approved loans in the USA reflects a positive economic outlook, bolstered by government initiatives, technological advancements, and an improved regulatory environment. This trend supports individual aspirations and contributes to the overall economic growth of the nation.

1 note

·

View note

Text

ch. 16

I will look at fiscal policy actions first, which is government spending through its revenues and taxation. I found a webpage that’s part of the IMF to be very useful in this. It goes over a bunch of key fiscal policy changes as of June 3rd, 2021. A big one occurred in March of 2021 when President Biden signed the American Rescue Plan. This consisted of a relief fund totaling 1.84 trillion USD, which was roughly 8 percent of the U.S. GDP. I remember when this was signed into law because I remember a lot of my friends getting stimulus checks and spending them. In addition to stimulus checks and reducing unemployment, the main goal was to invest in public health responses to U.S. citizens. We also saw money go towards creating vaccines, supporting state and local governments, and helping schools reopen.

In addition to the American Rescue Plan, there was a lot of other government spending going on before the American Rescue Plan. The CARES Act was sent through Congress in March 2020 and consisted of roughly 2.3 trillion dollars to prevent corporate bankruptcy, unemployment, tax rebates for individuals, and help with small business loans as well. This totaled roughly 11% of the country's GDP.

To show if they were successful is subjective. I would say that covid relief bills were successful, as they kept the economy afloat and kept Americans from losing everything. Many Americans struggled hard during this time, but without fiscal responses, it would have been another depression.

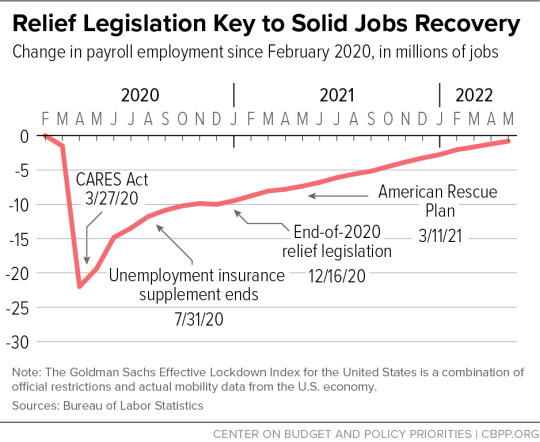

I found a great visual from the Center on Budget and Policy Priorities. It shows a drastic decline in jobs at the beginning of 2020. From Feb. to Mar. 2020, jobs declined by roughly 20 million. We then can see the CARES Act passed at the end of March and by May we see an increase in jobs again. Jobs increase until about August of 2020 then start to level off when unemployment insurance ends and continue to stay pretty level with minimal growth until around Jan. of 2021. The American Rescue Plan comes into play and increases job growth once again in March of 2021. Ever since that rescue plan was passed, we have seen a steady increase in jobs through 2021 and 2022, according to the chart. When regarding employment, I’d say that these fiscal policies proved tremendously successful. There was probably some wasted money, but most of the money got spent back into the economy.

Looking at today’s fiscal policy, I couldn’t find much as of 2023. Although, I’ve found sources that say we’ve been in an expansionary fiscal policy since 2009 to combat the great recession (UptoUs). This expansionary policy aims at tax cuts and increased spending. We saw this tremendously during the pandemic. Obviously, to limit the risk of going through another recession, the government dumped even more money into the system and cut even more taxes. So, it appears that we will continue to be in an expansionary period until taxes increase to pay all this debt.

Moving onto Monetary policy, there was a lot going on with banks. According to the IMF, banks were encouraged by federal banking supervisors to lend out their buffer money to lend people during COVID. In addition, loan modifications for borrowers would not be labeled as troubled debt restructurings. Some regulatory actions occurred with banks as well. The community bank leverage ratio was lowered to 8 percent. This would make it easier for investments to be made, but not necessarily good for the bank if something really bad happens. In addition, PPP loans have a zero percent risk weight. Lastly, Fannie Mae and Freddie Mac will be assisting borrowers by waiving late fees and mortgage forbearance, which allows borrowers to pause their fees for 12 months. Regarding monetary policy, a lot was done during Covid to reduce borrowers and lenders from folding.

Obviously, there isn’t any more loan forbearance in today’s world. We have seen a steady increase in interest rates since the pandemic and now they are at rates we haven’t quite seen in 20 years. Of course, when the deadlines for certain late fees and loan forbearance are up, people have to begin paying off their debts again. Now, we are dealing with sky-rocketing inflation levels. We have seen the federal funds rate go up as a way to combat inflation. This will make borrowing much more expensive and will slow the economy down. So, many businesses and consumers will decide to save their money in the present and upcoming periods to deal with higher interest rates and fed rates.

https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19#T

0 notes

Text

Former City of Miami Police Officer Pleads Guilty to COVID-19 Relief Fraud

MIAMI – Gregory Dennis, 45, a former police officer with the City of Miami Police Department, has pled guilty to wire fraud in connection with two fraudulent applications for Paycheck Protection Program (PPP) loans he submitted to a Small Business Administration (SBA) approved PPP lender while he was still employed with the City of Miami Police Department.

On March 28, 2021, Dennis submitted a…

View On WordPress

0 notes

Text

FEDS Paper: Bank Relationships and the Geography of PPP Lending

David Glancy

I study how bank relationships affected the timing and geographic distribution of Paycheck Protection Program (PPP) lending. Half of banks' PPP loans went to borrowers within 2 miles of a branch, mostly driven by relationship lending. Firms near less active lenders shifted to fintechs and other distant lenders, resulting in delays receiving credit but only slightly lower loan volumes. I estimate a structural model to fit the observed relationship between branch distance, bank PPP activity, and origination timing. I find that banks served relationship borrowers 5 to 9 days before other borrowers, an effect in line with reduced-form estimates using a sample of PPP borrowers with previous SBA lending relationships.

from FRB: Working Papers https://ift.tt/WOR43hm

via IFTTT

0 notes

Text

Why Brazil's streetlighting PPPs are 'consolidating at an accelerated pace'

Brazilian development banks Caixa Econômica Federal and BNDES are facilitating a rapid increase in streetlighting public-private partnerships in small and medium-size municipalities.

A call Caixa launched last year and whose results were published recently yielded numerous PPP proposals and 107 localities and 269 consortiums are now eligible to receive the lender’s structuring services.

Pedro Vicente Iacovino, president of private streetlighting concessionaires association Abcip, talks to BNamericas about the panorama and a milestone which the association will officially announce in March, among other topics.

Continue reading.

#brazil#politics#brazilian politics#economy#infrastructure#mod nise da silveira#image description in alt#bndes#caixa economica federal

0 notes

Text

What You Should Know About PPP Loans From Community Financial Institutions

Community financial institutions, or CFI's, are banks and other financial institutions that make loans for low and moderate income people. These loans are repaid through interest payments, and in some cases, the borrower can also apply for loan forgiveness. However, there are some things you should know before deciding whether or not to take out a PPP loan.

Loan forgiveness application process

If you have a loan with one of the Community financial institutions, it is important to know how the forgiveness process works. There are a number of requirements for submitting an application and you should ensure that you submit the necessary documentation.

First, you will need to verify that your PPP loan is eligible for forgiveness. The amount you are forgiven will depend on your payroll expenses and non-payroll expenses. You can apply for forgiveness through your lender or by submitting the application online.

After completing an application, you will need to submit the completed form and all supporting documents. Failure to provide proper documentation can delay processing and may impact your loan's terms.

When applying for forgiveness, the lender will need to verify your payroll costs and any mortgage interest payments. They must also determine the number of FTEEs you have received during the applicable periods.

For loans under $150,000, you are only required to submit a single page application. This may help streamline the forgiveness process and make it easier for lenders to approve your request.

Impact of the CARES Act on PPP lending by commercial banks

Banks are re-examining their role in the Paycheck Protection Program (PPP), an aid program that disbursed $525 billion in loans to help businesses cope with the COVID-19 pandemic. But the program isn't without its flaws. During its first year, PPP faced a backlash.

The government created PPP as part of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). It was designed to encourage small businesses to keep their workers on the payroll during a disease epidemic.

In August, the program closed. The Small Business Administration (SBA) has updated its guidance for PPP loans. They report that 11.8 million forgivable loans were approved as part of the program. These loans are forgiven if the loan spending criteria are met.

Some banks have restricted access to PPP loans to certain businesses, while others have restricted access to their existing customers. This is likely due to the fact that banks have pre-existing relationships with certain businesses. Moreover, some have implemented informal practices that could raise fair lending concerns.

Impact of the Riegle Act on PPP lending by commercial banks

The Riegle-Neal Act paved the way for national and state banks to branch across state lines. It also set a ten percent deposit cap for banks. However, states could opt out of the requirement. In the end, most state legislatures have opted out.

While the act's impact on banks' PPP lending is uncertain, it is clear that the act has played a significant role in shaping the nation's banking industry. This article examines how the law has shaped bank compensation and the role commercial banks play in advancing government fiscal policies.

The act's repercussions can be seen in the number of lawsuits filed against big banks. In many cases, the lawsuits accuse them of asset mismanagement. Banks can also be accused of discriminating against minority business owners.

For this reason, the government needs to use incentives to reward banks for following its fiscal agenda. These rewards can take a variety of forms, such as guaranteeing loans to foreign buyers. Alternatively, they could be more like stock options for the top managers.

FAQs for borrowers who obtained PPP loans

If you're a borrower who obtained PPP loans from a community financial institution, you may be wondering what to expect after the loan is closed. You should be aware that you have obligations after you receive the loan.

There are a number of requirements you need to meet in order to obtain a PPP loan. First, you must have less than 300 employees. This includes independent contractors, sole proprietorships, nonprofits, veterans' organizations, and tribal concerns.

Second, you must have operated during all four quarters of the year. In addition, you must have suffered a revenue reduction of at least 25%. The reduction must be demonstrated by submitting annual tax forms. For example, if your business generated $1,000,000 in revenues in 2018, you would have to prove that the revenue will be reduced to $550,000 by the end of 2019.

Third, you must have not received a PPP loan on or before December 27, 2020. However, you can obtain a PPP loan after that date if you have experienced a 25% revenue reduction.

0 notes

Last Seen Blogs

bbcaddictedteen

BBC Addicted Teen

dh901253-blog

Sin título

dreamerdrop

Dreamer Drop

aricons

ariana icons

pikachu030

피카추030