#studentloans

Text

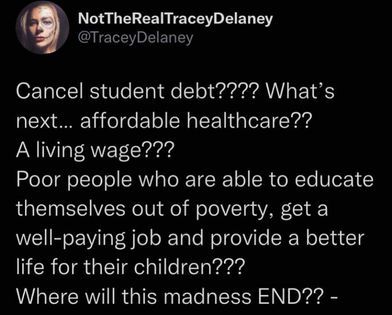

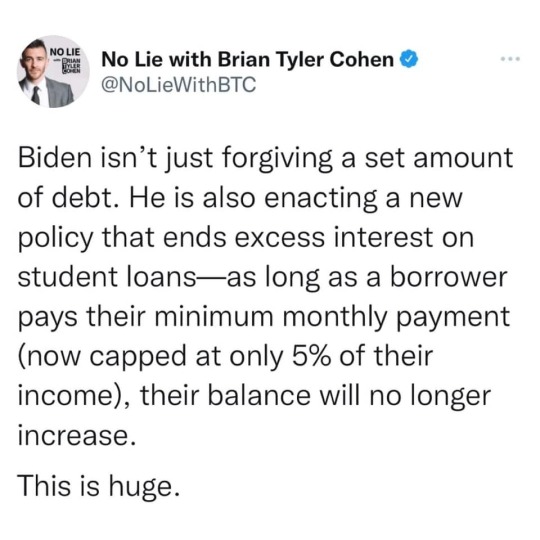

I just need to share the White House official Twitter account going absolutely feral on congressmen against student debt relief.

#studentloans#ppploans#loan relief#student loans#white house#us politics#as a taxpayer who has bailed out multiple businesses banks and churches id appreciate personal debt relief

2K notes

·

View notes

Text

So something I'm just confused about...

I'm all for this student loan cancelation, I come from a low income family. But unfortunately I was coaxed into a private loan because federal loans would NOT cover my school expenses for some odd reason and I was told a private loan would. But I was in such need of money for my private loan for my private art school I was accepted to that I also received Pell Grant money.

So I have a private loan but I also got a Pell Grant. The money needed to pay my loan would be more then enough to pay off what I have in debt and I'm am under government financial help.

Why is no one talking about the Private Loan side of this? I'm so happy that federal loans are being forgiven and I wish everyone who has those the best of luck, but us low income kids who took out private loans because their family was uneducated in the fact or had no support and can't pay it off due to circumstances such as disability.

Private loans are still loans.

7 notes

·

View notes

Text

Studying abroad seems costlier?

Don't let it scare you away from chasing your dreams. Find out the financial aid options 👆🏻 that makes your education abroad far easier.

Go to cademy1.com and search for scholarships, student loans, government grants and much more affordable options. 🙌🏻

To receive the expert guidance, sign up for a free account and get access to all the educational resources at your fingertips. ✅

#studyabroad#affordableeducation#scholarship#fellowship#governmentgrants#studentloans#financialaid#financingoptions#FAFSA#educationcounselor#edtech#collegeconsulting

2 notes

·

View notes

Text

Guys! Two more weeks and I’m done with my Master’s program! Oh I’m so happy! I’ll have loans, but I’ll be done! God I’m so tired!!!! FUCK!

2 notes

·

View notes

Text

The Controversy Over Student Loan Forgiveness: Is It the Right Thing To Do?

The Controversy Over Student Loan Forgiveness: Is It the Right Thing To Do?

Walk Away From Your Student Loans Without Filing Bankruptcy? It Can Be Done, but….

(Nehemiah chapter 5, verses 1-12) by Rev. Paul J. Bern

Has anyone else noticed that there is a lot of conflict and controversy surrounding President Biden’s proposed student loan bailout program? Hundreds of thousands of college graduates are buried under mountains of debt that they cannot repay, due to predatory…

View On WordPress

#Christian blogs#discipleship#forgiveness#God#Jesus#Jesus Christ#Progressive Christianity#real Christianity#religion#social justice#studentloans#truth

3 notes

·

View notes

Link

MSME Helpline is now assisting the businesses in getting Unsecured Loans in 7 days. To avail this facility, please provide the details in the below form:

Click Here-: Unsecured Loans in 7 Days

#loanofficer#studentloans#boloaniversario#anniesloanchalkpaint#mortgageloans#valoans#carloan#loanofficers#loansigningagent#loanoriginator#loanofficerlife#loanapproval#autoloan#conventional loans#loanoriginators#loanapproved#unsecured loans#unsecuredbusinessloan#unsecuredpersonalloan#unsecuredloans#unsecuredbusinessloans#unsecuredloanagent

2 notes

·

View notes

Video

youtube

Who said money doesn't make you happy? Cashcpr.com for all your money wi...

0 notes

Text

6 Ways to Pay for Your Teen Child's College Tuition

Learn effective ways to cover your teenager's tuition fees. Explore 6 practical solutions to secure their higher education future.

#CollegeTuitionFees#StudentScholarships#WorkStudyPrograms#StudentLoans#EmployerTuitionAssistance#CommunityCollegeFunding

0 notes

Text

Navigating the Landscape of Private Student Loans: A Comprehensive Guide

The rising costs of tuition and associated expenses have made financing higher education a daunting task for many students. While federal student loans are a common choice, they may not always cover the entire cost of education. This is where private student loans come into play. In this comprehensive guide, we will delve into the intricacies of private student loans, exploring their features, advantages, and potential pitfalls.

Understanding Private Student Loans:

1. Definition and Basics

Private student loans are financial tools offered by private lenders, such as banks or credit unions, to help students cover educational expenses. Unlike federal student loans, which are backed by the government, private loans are obtained through a credit check and typically require a co-signer if the borrower has limited credit history or income.

2. Eligibility Criteria

Private lenders evaluate applicants based on creditworthiness and income. Students with a strong credit history may secure loans with more favorable terms, while those without may need a co-signer. Understanding the eligibility criteria is crucial before applying for a private student loan.

3. Interest Rates

Interest rates on private student loans can be fixed or variable. It’s essential to comprehend how interest accrues over the life of the loan and how it impacts overall repayment. Variable rates may start lower but can increase, leading to higher costs over time.

Features of Private Student Loans:

1. Eligibility Criteria

Private student loans often require a credit check and a co-signer, typically a parent or guardian, who is equally responsible for loan repayment. This can be a significant barrier for students with limited credit history or those without a willing co-signer.

2. Interest Rates

Interest rates on private student loans can be fixed or variable. While fixed rates remain constant throughout the life of the loan, variable rates may fluctuate based on market conditions. Borrowers must understand the terms and implications of each option.

3. Loan Limits

Private student loans may offer higher borrowing limits compared to federal loans. However, it’s essential to borrow responsibly and only what is necessary to cover educational expenses. Excessive borrowing can lead to financial challenges after graduation.

4. Repayment Terms

Private loans often have shorter repayment terms than federal loans. While federal loans may offer income-driven repayment plans and loan forgiveness options, private loans may have less flexible repayment terms.

Advantages:

1. Higher Borrowing Limits

Private student loans can provide more substantial funding compared to federal loans, making them a viable option for students attending expensive institutions or pursuing advanced degrees.

2. Flexible Use of Funds

Student loans can be used to cover various education-related expenses, including tuition, books, housing, and even living expenses. This flexibility allows students to tailor the loan to their specific needs.

3. Potentially Lower Interest Rates for Well-Qualified Borrowers

Students with a strong credit history and a co-signer may qualify for competitive interest rates on private loans. This can result in lower overall costs compared to federal loans for some borrowers.

Considerations and Potential Pitfalls:

1. Creditworthiness and Co-Signers

The eligibility criteria for student loans heavily depend on the borrower’s creditworthiness. Students with limited credit history may find it challenging to secure a private loan without a co-signer. The co-signer’s credit history is also crucial, as it directly impacts the interest rate offered.

2. Variable Interest Rates

While variable interest rates may start lower than fixed rates, they can increase over time, leading to higher overall costs. Borrowers need to carefully weigh the potential savings in the short term against the long-term risks associated with variable rates.

3. Limited Repayment Options

Private loans generally have fewer repayment options than federal loans. Borrowers may not have access to income-driven repayment plans, loan forgiveness, or other federal benefits. This lack of flexibility can pose challenges, especially during periods of financial hardship.

4. Interest Accrual During School and Grace Periods

Unlike federally subsidized loans, where the government covers interest during certain periods, private student loans often accrue interest from the disbursement date. This means that interest can accumulate while the student is in school or during the grace period after graduation, increasing the overall repayment amount.

The Impact on Financial Health

1. Credit Score Implications

Taking out loans can have a significant impact on a borrower’s credit score. Timely payments contribute positively to credit history, but missed payments or defaults can harm credit scores, affecting future financial opportunities such as obtaining a mortgage or car loan.

2. Financial Stress and Mental Health

The burden of student loan debt, particularly private loans with higher interest rates, can lead to financial stress and impact mental health. Students and graduates may experience anxiety and pressure as they navigate repayment, influencing overall well-being.

3. Loan Refinancing Opportunities

Borrowers with private student loans should explore opportunities for loan refinancing. Refinancing can lead to lower interest rates, reduced monthly payments, and potentially more favorable terms, providing financial relief and aiding in long-term financial planning.

Conclusion:

Private student loans can be a valuable tool for financing higher education, offering flexibility and higher borrowing limits. However, students and their families must approach private loans with a clear understanding of the terms, potential risks, and alternatives available. Thorough research, comparison of lenders, and careful consideration of individual financial situations are essential steps in making informed decisions about student loans. As the education financing landscape continues to evolve, being well-informed empowers students to navigate the complexities and pursue their academic goals with financial confidence.

#studentdebt#studentloans#financialliteracy#PrivateStudentLoans#educationfinance#highereducation#studentlife

0 notes

Text

My education Story

Support

About Me

Portfolio

Your help with my student debt goals would mean the world to me! I’m raising $80,000 to pay off my student debts as well as start fresh with my new wellness business.

I’m tired of the cycle of borrowing from one source to pay off another and essentially never getting ahead. The hardships in my life so far aren’t going to stop me from reaching my goals.

Throughout…

View On WordPress

1 note

·

View note

Link

Student Loans: Building Credit History Made Easy

0 notes

Text

Increased Loan Requests as Schools Gear Up for Reopening: Banks Projections

Increased Loan Requests as Schools Gear Up for Reopening: Banks Projections

Financial institutions predict an increase in loan demand in January due to a variety of causes, including the anticipated reopening of schools.

Banks forecasted four primary scenarios that will be experienced in the first quarter of 2024 in a Market Perceptions Survey done by the Central Bank of Kenya (CBK), as mentioned below.

ALSO READ: HELB Announces Ksh500,000 Loans for Kenyan Nurses: How to Apply

Demand has increased.

Financial organizations anticipate that parents may seek loans to meet financial responsibilities in schools.

Notably, the reopening of schools comes directly after the holiday season, during which many families spent a lot of money on food and travel. Basic education institutes will reopen on January 8.

Form One students, on the other hand, are required to report to various schools on January 15. In addition to school fees, parents will be required to purchase personal boarding things for their children.

ALSO READ: HELB Mandates eCitizen for All Payment Transactions; How to Pay Via eCitizen

Competition

Aside from their parents, business owners are obliged to seek loans to stock their stores. This might make it more competitive for people looking for loans.

The CBK report indicated that, according to bank respondents, there was an anticipation of moderate to high demand for credit in December 2023 and January 2024.

This demand was attributed to various factors, including businesses preparing for the festive season and meeting financial obligations for the new school year.

Additionally, the need for working capital financing to address the high costs of inputs and businesses seeking to safeguard themselves against delays in collections and payments by customers were identified as contributing factors.

ALSO READ: Revised University Funding Model: Loans, Fees, Scholarships & Debt

Cautions Lending

The CBK research also stated that financial institutions will be careful with their lending due to default fears.

The expected increase in non-performing loans has been attributed to the situation of the economy, which has stressed many firms and affected people's ability to satisfy their obligations.

According to the report, respondents highlighted potential risks to the anticipated credit growth. These concerns encompassed economic uncertainty arising from elevated inflation levels, leading to a decrease in disposable income and diminished demand for credit.

Additionally, the high cost of conducting business was identified as a factor prompting banks to exercise increased caution in their lending practices to the private sector. This cautious approach aimed at minimizing the risk of default in the face of challenging economic conditions.

ALSO READ: Students to Apply Yearly for University Loans and Scholarships

Loan Recovery

As the number of non-performing loans (NPLs) rises, banks and financial institutions are anticipated to ramp up their efforts to recover the loans.

This could result in people losing their property through auctions. The statement indicated that the heightened efforts in credit recovery aim to enhance the overall quality of the asset portfolio.

Banks plan to concentrate these intensified recovery initiatives primarily in the personal and household sector, with a notable percentage of 92. Other sectors identified for increased credit recovery efforts include trade (87 per cent), manufacturing (78 per cent), transport and communication (76 per cent), and real estate (73 per cent).

This strategic focus reflects a concerted effort by banks to address and improve credit conditions across various key sectors.

ALSO READ: Top 10 Foundations Offering Full Sponsorship To KCSE, KCPE Candidates After Exams

Increased Loan Requests as Schools Gear Up for Reopening: Banks Projections

Read the full article

0 notes

Last Seen Blogs

graysonshmayson

robbob

escaperooms782323

квест в киеве

escaperooms782323

квест в киеве

yorkbro2066-blog

SupplementLifeStyle

demon-of-depth

Sin bin =owo=