Last Seen Blogs

soulreflectiontarot

The Soul Reflection

emozpice

Static Emo

menulislape

лисья хатка

fraiserabbit

so's your old man

selfshippy-bun

selfship blog!!!

Text

How to Complete VAT Returns

New Post has been published on https://www.fastaccountant.co.uk/how-to-complete-vat-returns/

How to Complete VAT Returns

Hey there! If you’re feeling a bit overwhelmed by the process of completing VAT returns in the UK, don’t worry – I’ve got you covered. In this guide, I’ll walk you through everything you need to know about how to complete VAT returns with ease. Let’s get started!

What is VAT?

Before we dive into the nitty-gritty details of how to complete VAT returns, let’s make sure we’re on the same page about what VAT actually is. VAT stands for Value Added Tax, and it’s a type of tax that is applied to the majority of goods and services in the UK. Essentially, VAT is a tax that is paid by consumers when they purchase goods or services, and it’s collected by businesses on behalf of the government.

Who Needs to Complete VAT Returns?

Not every business in the UK is required to complete VAT returns – the threshold for mandatory registration is £85,000 of taxable turnover. If your business’s taxable turnover exceeds this threshold over a 12-month period, you are required to register for VAT and submit regular VAT returns to HM Revenue & Customs (HMRC).

How Often Do I Need to Submit VAT Returns?

VAT returns in the UK are typically submitted quarterly. This means that you’ll need to complete and submit a VAT return to HMRC every three months. However, some businesses may be eligible to submit annual VAT returns instead, so it’s important to check with HMRC to determine which schedule applies to your business.

How to Register for VAT

If you’ve determined that your business needs to register for VAT, the next step is to actually complete the registration process. You can register for VAT online through the HMRC website, or you can use an agent or accountant to help you with the process. During the registration process, you’ll need to provide information about your business, such as its name, address, and taxable turnover.

Keeping Accurate Records

One of the keys to successfully complete VAT returns in the UK is keeping accurate and up-to-date records of your business’s transactions. You’ll need to track both the VAT that you have charged to your customers (output tax) and the VAT that you have paid on your business expenses (input tax). This information will be used to calculate the amount of VAT that you owe to HMRC.

youtube

Calculating VAT

Calculating VAT can be a bit tricky, especially if you’re not familiar with the process. Essentially, the amount of VAT that you owe to HMRC is the difference between the VAT that you have charged on your sales and the VAT that you have paid on your purchases. To calculate the amount of VAT that you owe, you can use the following formula:

VAT owed = Total output tax – Total input tax

Completing Your VAT Return

Step 1: Use Accounting Software

Most businesses are required to keep digital records and use compatible software to submit VAT returns under the Making Tax Digital (MTD) scheme. Ensure your accounting software is MTD-compatible.

Step 2: Access Your VAT Online Account

Log in to your HMRC VAT online account. If you haven’t already, sign up for MTD and link your accounting software to your HMRC account.

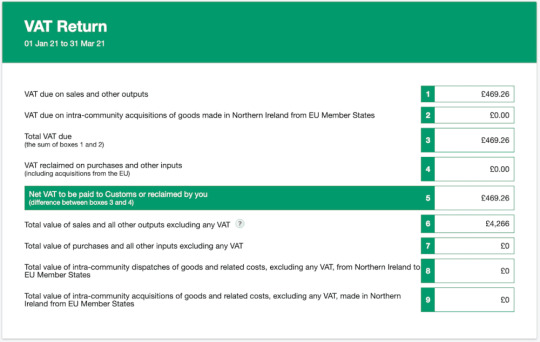

Step 3: Fill in the VAT Return Form

Using your accounting software, fill in the VAT return form. You will need to provide the following information:

Total Sales and Outputs: Include the total value of sales and other outputs (excluding VAT).

Output Tax Due: The amount of VAT due on your sales and other outputs.

Purchases and Inputs: The total value of purchases and other inputs (excluding VAT).

Input Tax Reclaimable: The amount of VAT you can reclaim on your purchases and other inputs.

Net VAT to be Paid or Reclaimed: The difference between your output tax and input tax.

Step 4: Review and Submit

Carefully review the information on your VAT return to ensure it is accurate. Once confirmed, submit your VAT return through your accounting software. Ensure you meet the deadline for submission, which is usually one calendar month and seven days after the end of the VAT accounting period.

Step 5: Pay Any VAT Due

If your VAT return shows that you owe VAT, arrange payment to HMRC by the due date. You can pay via:

Direct Debit

Bank transfer (BACS/CHAPS)

Online or telephone banking

Debit or corporate credit card

Step 6: Keep Records

After submission, keep copies of your VAT returns and the records used to complete them for at least six years. This includes:

VAT returns submitted

Calculation working papers

Sales and purchase invoices

Bank statements

Step 7: Handle Corrections

If you discover an error in a previously submitted VAT return, correct it as soon as possible. Minor errors (below £10,000) can often be corrected on your next VAT return. Significant errors or adjustments may require a formal notification to HMRC using form VAT652.

Additional Tips:

Stay Informed: Keep up-to-date with any changes to VAT regulations and requirements by regularly checking HMRC’s guidance.

Seek Assistance: If you are unsure about any part of the process, consider seeking advice from a qualified accountant or VAT specialist.

By following these steps, you can ensure that your VAT returns are completed accurately and submitted on time.

Common Mistakes to Avoid

Completing VAT returns can be complex, and it’s easy to make mistakes along the way. Some common errors to watch out for include:

Failing to keep accurate records of your transactions

Forgetting to reclaim VAT on all eligible business expenses

Miscalculating the amount of VAT owed to HMRC

Missing the deadline for submitting your VAT return

Conclusion

Completing VAT returns in the UK may seem daunting at first, but with a little bit of know-how and some careful record-keeping, you’ll be a VAT pro in no time. Remember to stay organized, keep accurate records, and reach out for help when you need it. By following the steps outlined in this guide, you’ll be well on your way to mastering the art of VAT returns in the UK. Happy filing!

0 notes

Text

How Does Employment Allowance Work?

New Post has been published on https://www.fastaccountant.co.uk/how-does-employment-allowance-work/

How Does Employment Allowance Work?

Hey there! I’m excited to share with you all about understanding Employment Allowance in the UK. It is a valuable tax relief scheme that helps businesses and charities save money on their employer National Insurance contributions. By claiming Employment Allowance, eligible employers can reduce the amount of National Insurance they have to pay each year, providing a welcomed boost to their bottom line. It’s a fantastic way to support businesses in the UK and encourage growth and employment.

What is Employment Allowance UK?

Employment Allowance is a scheme introduced by the UK government to help businesses and charities reduce the amount they pay in employer’s National Insurance contributions. The allowance is currently set at £5,000 per year, meaning that eligible employers can save up to this amount on their NI bill.

As an employer, it’s important to take advantage of it if you meet the criteria set out by HMRC. This can help you save money and reinvest it back into your business or organization.

Who is Eligible for Employment Allowance?

To be eligible for Employment Allowance, you must meet the following criteria:

You must be a business or charity that pays employer’s Class 1 National Insurance

You must have paid less than £100,000 in employer’s Class 1 National Insurance in the previous tax year

You must not be a public body or business that provides services to public bodies

If you meet these criteria, you can claim and start saving money on your National Insurance contributions.

youtube

Who cannot claim Employment Allowance?

Employment Allowance (EA) in the UK reduces an employer’s National Insurance liability by up to a specified amount each tax year. However, certain businesses and individuals are ineligible to claim it. Here are the main categories of those who cannot claim:

Single Director Companies: Companies with only one employee who is also a director cannot claim.

Employers with Class 1 liabilities of £100,000 or more: If your employers’ Class 1 National Insurance liabilities were £100,000 or more in the previous tax year, you cannot claim.

Employers with employees covered by IR35 rules: If you’re a public sector employer and have deemed payments of employment income, you cannot claim Employment Allowance for those deemed payments.

Domestic Employers: Employers of personal, household, or domestic workers, such as nannies or gardeners, unless they are employed as part of a business, are not eligible.

Service Companies: If more than half of your earnings are derived from the work of one employee who has paid work under the IR35 rules, you cannot claim.

Employers of connected companies or charities: If a group of companies is connected for Employment Allowance purposes, only one company or charity within the group can claim. Additionally, certain connected companies and charities with significant financial connections or overlaps cannot claim.

Public Authorities: Most public bodies cannot claim, including local, district, town and parish councils.

Employers of those on specific contracts: If you’re an employer who is part of a managed service company, or you employ someone for services covered by a personal service company (PSC), the allowance may not apply.

It’s important for employers to check their eligibility each tax year and ensure they meet all conditions before making a claim. If in doubt, consulting with an accountant or checking HMRC’s guidelines directly is advisable.

How to Claim Employment Allowance

To claim Employment Allowance, follow these steps:

Step 1: Check Eligibility

Ensure that your business or organization is eligible to claim. Refer to the categories of those who cannot claim, as detailed earlier.

Step 2: Use Payroll Software

Most payroll software packages will have a facility to claim Employment Allowance. Ensure your payroll software is up-to-date and supports EA claims.

Step 3: Claim via HMRC’s Basic PAYE Tools

If you do not use commercial payroll software, you can use HMRC’s Basic PAYE Tools to claim. Download and install the Basic PAYE Tools if you haven’t already.

Step 4: Indicate Your Claim

When running payroll, you will need to indicate that you are claiming the Employment Allowance:

In Payroll Software: Go to the relevant section in your payroll software where you process employer payments and look for an option to claim Employment Allowance.

In Basic PAYE Tools: Open the software, navigate to the employer section, and select the option to claim Employment Allowance.

Step 5: Submit an Employer Payment Summary (EPS)

Submit an Employer Payment Summary (EPS) to inform HMRC that you are claiming Employment Allowance. The EPS should be submitted each tax year to confirm your claim.

Step 6: Adjust Your Payments

Once your claim is processed, adjust your payments to HMRC accordingly. Your National Insurance liability will be reduced by the amount of the Employment Allowance.

Step 7: Monitor Your Allowance

Keep track of the amount of Employment Allowance used throughout the tax year to ensure you do not exceed the annual limit. Most payroll software will do this automatically.

Step 8: Renew Each Tax Year

You must claim Employment Allowance each tax year. Ensure you indicate your claim when you start the new tax year in your payroll software or Basic PAYE Tools.

Additional Notes:

Review Notices: HMRC may send notices regarding your claim. Ensure you review and comply with any additional requirements or notices.

Record Keeping: Keep detailed records of your claim and how the Allowance has been applied to your National Insurance payments.

If you encounter any difficulties or uncertainties during the process, consider consulting with an accountant or payroll specialist for assistance.

Benefits of Employment Allowance

There are several benefits to claiming Employment Allowance as an employer. Some of the key advantages include:

Saving money on your National Insurance contributions

Reinvesting the savings back into your business

Improving cash flow and profitability

Encouraging job creation and growth within your organization

By taking advantage of the Allowance, you can improve your financial situation and create a more sustainable and successful business.

Examples of Employment Allowance Savings

To help you understand the potential savings you could make with Employment Allowance, here are a few examples:

Small Business A has an annual NI bill of £3,000. By claiming Employment Allowance, they can save the full £3,000 and reinvest it in their business.

Charity B pays £7,000 in employer’s NI contributions each year. With a £5,000 allowance, they can reduce their bill to just £2,000 and allocate the savings to their charitable activities.

Start-up C is a new business with limited cash flow. By claiming Employment Allowance, they can save money on their NI contributions and use it to grow their business and hire more employees.

These examples illustrate the tangible benefits of Employment Allowance and how it can make a real difference to businesses and organizations of all sizes.

Frequently Asked Questions

As an employer looking to claim Employment Allowance, you may have some questions about how the scheme works. Here are a few common FAQs to help you better understand the process:

Can I claim if I am a sole trader?

Unfortunately, sole traders are not eligible, as it is only available to businesses and charities that pay employer’s Class 1 National Insurance.

How often can I claim Employment Allowance?

You can claim Employment Allowance once per tax year, and the allowance resets each year. Make sure to claim it at the beginning of the tax year to start saving on your NI contributions.

Conclusion

In conclusion, Employment Allowance is a valuable tax relief scheme that can benefit businesses and charities in the UK. By claiming the allowance, you can save money on your National Insurance contributions, improve your cash flow, and reinvest the savings back into your organization.

I hope this article has helped you better understand Employment Allowance and how you can take advantage of it as an employer. Remember to check your eligibility, claim the allowance, and monitor your savings to make the most of this valuable tax relief.

#employers ni allowance#Employment Allowance#employment allowance eligibility#employment allowance nic#what is employment allowance

0 notes

Text

Cost of Sales Explained

New Post has been published on https://www.fastaccountant.co.uk/cost-of-sales/

Cost of Sales Explained

Welcome, my friends! Today, I want to share with you the importance of understanding the cost of sales. Have you ever wondered what exactly cost of sales means? Well, let me break it down for you – it is a crucial aspect of business that helps determine the profitability of a company by analysing the direct costs associated with producing and selling goods or services. By delving into this concept, we can gain a deeper understanding of how businesses operate and thrive. So, join me on this journey as we unravel the mysteries of cost of sales together.

Understanding the Cost of Sales

What is the meaning of cost of sales?

When it comes to running a business, it’s essential to have a clear understanding of your financial components, including the cost of sales. The cost of sales, also known as the cost of goods sold, refers to the direct costs associated with producing goods or services that a company sells during a specific period. These costs can include materials, labour, and overhead. By understanding the cost of sales, a business can determine its profitability and make informed decisions about pricing, production, and overall strategy.

Why is it important to track the cost of sales?

Tracking the cost of sales is crucial for several reasons. First and foremost, it helps determine the gross profit margin, which is essential for assessing the overall health of the business. By understanding the cost of sales, a company can establish pricing strategies, identify areas of improvement, and make informed decisions about production and inventory management. Additionally, tracking the cost of sales is necessary for financial reporting, tax purposes, and assessing the efficiency of operations.

How to calculate the cost of sales

Calculating the cost of sales involves adding up all the direct costs associated with producing goods or services sold during a specific period. The formula for calculating the cost of sales is as follows:

Cost of Sales = Opening Inventory + Purchases – Closing Inventory

Let’s break down each component of the formula:

Opening Inventory: This refers to the value of inventory at the beginning of the accounting period.

Purchases: This includes all purchases of raw materials, labor costs, and production expenses incurred during the period.

Closing Inventory: This is the value of inventory at the end of the accounting period.

By subtracting the closing inventory from the total of the opening inventory and purchases, a business can determine the cost of sales for the period.

Understanding the components of cost of sales

To calculate the cost of sales accurately, it’s essential to understand the different components that make up this metric. These components include:

Direct Materials: The cost of raw materials used in the production of goods.

Direct Labor: The wages paid to employees directly involved in the production process.

Factory Overhead: Indirect production costs such as utilities, rent, and depreciation.

Each of these components contributes to the overall cost of sales and should be carefully tracked and monitored to ensure accurate financial reporting.

Importance of maintaining accurate records

Maintaining accurate records of the cost of sales is crucial for several reasons. First and foremost, accurate records ensure compliance with financial reporting requirements and tax laws. Additionally, having precise data on the cost of sales allows businesses to evaluate their profitability, make informed pricing decisions, and identify opportunities for cost-saving.

By keeping detailed records of direct costs such as materials and labour, as well as indirect costs like overhead expenses, a business can track its performance, make data-driven decisions, and ultimately improve its bottom line.

Ways to reduce the cost of sales

Reducing the cost of sales is a key objective for many businesses looking to improve profitability and competitiveness. There are several strategies that companies can implement to lower their cost of sales, including:

Supplier Negotiation: Negotiating better prices with suppliers can result in cost savings on raw materials and components.

Efficiency Improvements: Streamlining production processes, reducing waste, and improving operational efficiency can lower the cost of sales.

Outsourcing: Outsourcing non-core functions can help reduce labour costs and overhead expenses.

Inventory Management: Implementing efficient inventory management practices can reduce carrying costs and minimize the risk of obsolescence.

By implementing these strategies and continually evaluating the cost of sales, businesses can identify opportunities for improvement and make changes to enhance profitability.

youtube

Implications of inaccurate cost of sales

Failing to accurately track and monitor the cost of sales can have significant implications for a business. Inaccurate cost of sales figures can lead to incorrect financial reporting, misinformed decision-making, and overall financial instability. Without an accurate understanding of the cost of sales, a company may struggle to set prices effectively, manage inventory, and assess profitability.

It’s essential for businesses to invest time and resources in maintaining accurate records and conducting regular cost of sales analysis to ensure financial health and sustainability.

Conclusion

In conclusion, understanding the cost of sales is crucial for running a successful business. By calculating the cost of sales accurately, tracking its components, and maintaining precise records, a company can make informed decisions, improve profitability, and ensure financial stability. By implementing strategies to reduce the cost of sales, identifying opportunities for improvement, and monitoring performance, businesses can optimize their operations and achieve long-term success. Remember, the cost of sales is not just a financial metric—it’s a vital tool for strategic decision-making and business growth.

0 notes

Text

How to Register for PAYE

New Post has been published on https://www.fastaccountant.co.uk/how-to-register-for-paye/

How to Register for PAYE

Are you an employer in the UK? If so, it is important to understand how to register for PAYE (Pay As You Earn). PAYE is the system used by the HM Revenue and Customs (HMRC) to collect income tax and National Insurance contributions from employees’ salaries. To ensure compliance and avoid any penalties, it is essential to follow the correct process for PAYE registration. In this article, we will outline the steps you need to take to register for PAYE in a simple and straightforward manner.

Essential Information

What is PAYE?

PAYE stands for Pay As You Earn, which is a system used by the HM Revenue and Customs (HMRC) in the United Kingdom to collect income tax and National Insurance contributions from employees. Under the PAYE system, employers are responsible for deducting the correct amount of tax and NI from their employees’ salaries or wages before paying them.

Who needs to register for PAYE?

Any employer who pays one or more employees in the UK must register for PAYE. This includes businesses, organizations, and individuals who employ staff, regardless of the size of the workforce. It is important to register for PAYE as soon as you become an employer, even if you only have one employee or if you have casual or temporary staff.

What are the benefits of registering for PAYE?

Registering for PAYE not only ensures that you comply with UK tax regulations, but it also offers several benefits. Firstly, it enables you to accurately calculate and deduct the correct amount of tax and National Insurance from your employees’ pay. It also provides your employees with the reassurance that their taxes are being handled correctly and that they are contributing towards their statutory entitlements, such as state pension and sick pay. Finally, being registered for PAYE allows your employees to access other benefits, such as government-funded training and support.

When should you register for PAYE?

You should register for PAYE as soon as you become an employer, even if you don’t anticipate paying your employees immediately. It is a legal requirement to register before your first payday as an employer. In addition, you are not allowed to register more than two months before you start to employ people. Failing to register within the specified time frame may result in penalties and interest charges from HMRC.

Preparing for Registration

Gather necessary documents

Before you can register for PAYE, you will need to gather certain information. These may include:

Your National Insurance Number (If you are a sole trader)

The National insurance number of one of the directors (if you are a Ltd Company)

Your Unique Taxpayer Reference (UTR) if you are self-employed

Company registration details (if applicable)

Company UTR number (if applicable)

The date that you expect to start employing people

Registration method

The way you register for PAYE depends on the type of business. Most Limited companies can only register online through their HMRC business tax account. For other business structures such as sole traders and partnerships registration can be done through a business tax account or by completing an online registration form.

Registration Process

Through a business tax account

To register for PAYE through your business tax account, you will first need to create an online account on the HMRC website if you haven’t already got one. This account will serve as your portal for all tax-related matters. If you already have a business tax account, then log in to your account and register for PAYE.

If you are not a Ltd Company, you can choose to register via your business tax account if you have one. If you do not have a business tax account you can create one and then register your business for PAYE.

Submit online registration form

If you are not a Limited company, you have the option to complete an online registration instead of registering via a business tax account. This form will require you to provide detailed information about yourself and your business, such as your business name, your National Insurance number, your UTR Number, address, and contact details. Take your time to ensure that all the information provided is accurate and up to date, as any errors or omissions may cause delays in the registration process.

Once you have submitted the online registration form, you will receive a confirmation message from HMRC. This message will acknowledge that your registration has been received and provide you with a reference number for future correspondence. It is important to keep this reference number safe, as you will need it when communicating with HMRC regarding your PAYE scheme.

After Registration

Receive PAYE reference number

After successfully registering for PAYE, you will receive a PAYE reference number from HMRC. It can take up to 30 days for the PAYE reference number to arrive. This reference number is unique to your business and is essential for all future communications with HMRC regarding your PAYE scheme. It is important to keep this reference number safe and easily accessible for reference purposes.

Set up PAYE scheme

Once you have your PAYE reference number, you will need to set up your PAYE scheme. This involves stating the process of deducting tax and National Insurance from your employees’ salaries or wages and paying it to HMRC. You will also need to ensure that you are aware of your legal obligations and responsibilities under the PAYE system.

Submit regular payroll reports

As a registered PAYE employer, you are required to submit regular payroll reports to HMRC. These reports provide details of your employees’ earnings, deductions, and tax contributions. The frequency of these reports will depend on the size of your workforce and your PAYE scheme type. It is essential to meet the deadlines set by HMRC to avoid any penalties or fines.

Maintaining PAYE Registration

Keep payroll records up to date

To ensure compliance with PAYE regulations, it is crucial to maintain accurate and up-to-date payroll records. This includes keeping track of your employees’ salaries, benefits, deductions, and any changes in employment status. Retaining these records for at least six years is necessary to meet HMRC’s record-keeping requirements.

Notify HMRC about any changes

If there are any changes in your business, it is important to notify HMRC promptly. This may include changes to your company name, address, or contact details. Failing to notify HMRC about changes may result in incorrect tax calculations and potential penalties.

Ensure compliance with PAYE regulations

Compliance with PAYE regulations is essential to avoid penalties and fines from HMRC. This includes accurately calculating and deducting the correct amount of tax and National Insurance from your employees’ pay, making timely payments to HMRC, and submitting accurate payroll reports. Staying informed about changes in tax legislation and seeking professional advice when necessary is crucial for maintaining compliance.

youtube

Getting Help and Support

Contact HMRC helpline

If you need any assistance or have specific questions regarding PAYE registration or compliance, you can contact the HMRC helpline. The helpline is a valuable resource staffed by knowledgeable professionals who can provide guidance on various tax-related matters.

Use online resources

The HMRC website offers a wealth of online resources to help employers understand and navigate the PAYE system. You can access guides, tutorials, FAQs, and other useful information that will assist you in managing your payroll obligations effectively.

Consult an accountant or tax advisor

If you require further guidance or have complex tax matters to address, it may be beneficial to consult an accountant or tax advisor. These professionals specialize in tax matters and can provide expert advice tailored to your specific needs. They can help you understand your obligations, navigate tax legislation, and ensure compliance with PAYE regulations.

Frequently Asked Questions

What happens after registering for PAYE?

After registering for PAYE, you will receive a PAYE reference number from HMRC. You will need this reference number for all future communications with HMRC regarding your PAYE scheme. You will also need to set up your PAYE scheme and ensure that you comply with the regulations by deducting the correct amount of tax and National Insurance from your employees’ pay and submitting regular payroll reports to HMRC.

Can I register for PAYE if I have no employees?

Yes, you can register for PAYE even if you have no employees at the moment. Registering for PAYE will allow you to set up your payroll system and be ready to hire employees in the future. Additionally, registering for PAYE may be necessary if you have a director’s salary or if you are employing family members. It is important to inform HMRC if your circumstances change and you no longer have any employees.

Can I register for PAYE if I am self-employed?

No, if you are self-employed and do not have any employees, you do not need to register for PAYE. Self-employed individuals are required to report their income through the self-assessment tax system. However, if you later start employing individuals, you will need to register for PAYE and deduct the correct amount of tax and National Insurance from their salaries or wages.

0 notes

Text

What are Sundries Expenses?

New Post has been published on https://www.fastaccountant.co.uk/what-are-sundries-expenses/

What are Sundries Expenses?

Welcome to a brief overview of understanding sundries expenses! Sundries expenses are those small, miscellaneous expenses that often get overlooked but can add up quickly. From office supplies to postage fees, these little costs can sneak up on you if not carefully monitored. By being aware of these sundries expenses and tracking them diligently, you can better manage your overall budget and avoid any surprises down the road. Let’s dive in and explore how paying attention to these seemingly minor expenses can make a big difference in your financial wellness.

Understanding Sundries Expenses

Have you ever come across the term “sundries expenses” and wondered what exactly it entails? In this article, we will delve into the world of sundries expenses and help you understand what they are all about. Whether you are a business owner trying to track your expenses or just curious about financial terms, this article will provide you with valuable insights into sundries expenses.

What are Sundries Expenses?

When you hear the term “sundries expenses,” it generally refers to those small, miscellaneous expenses that do not fit into a specific category. These expenses can include a wide range of items, such as office supplies, postage, bank fees, and other incidentals that come up in the day-to-day operations of a business.

Sundries expenses are often overlooked or underestimated, but they can add up quickly and have a significant impact on your bottom line. By understanding and tracking your sundry expenses, you can gain better control over your overall financial health and make more informed decisions about your spending.

Examples of Sundries Expenses

To give you a better idea of what sundries expenses can encompass, here are some common examples:

Expense Category Description Amount Office Supplies Pens, paper, folders $150 Postage Stamps, shipping costs $100 Bank Fees Monthly maintenance fees $50 Miscellaneous Random small expenses $75

These are just a few examples of the types of expenses that fall under the category of sundry expenses. It’s important to keep track of these expenses to ensure they are accounted for in your financial records.

Why Track Sundries Expenses?

You may be wondering why it’s necessary to track sundry expenses when they seem like such small, insignificant items. However, failing to keep an eye on these expenses can lead to bigger financial challenges down the road.

Tracking your sundries expenses allows you to:

Identify Cost Savings: By monitoring your sundry expenses, you can identify areas where you may be overspending or find opportunities to cut costs. For example, you may discover that you are paying for unnecessary subscriptions or services that you can cancel to save money.

Improve Budgeting: Including sundries in your budgeting process can help you create a more accurate picture of your overall financial health. By accounting for these small expenses, you can ensure that you are not overlooking any costs that could impact your bottom line.

Enhance Financial Reporting: Keeping track of sundry expenses will make it easier to generate accurate financial reports and analyse your company’s performance. This information can be invaluable when making strategic decisions for your business.

youtube

Tips for Managing Sundries Expenses

Managing sundries expenses effectively requires attention to detail and a proactive approach to tracking your spending. Here are some tips to help you stay on top of your sundry expenses:

Keep Detailed Records: Make sure to document every sundry expense, no matter how small. This will help you have a clear view of where your money is going and make it easier to spot any discrepancies or trends in your spending.

Use Technology: Consider using accounting software or apps to track your sundries more efficiently. These tools can help automate the process and provide you with real-time insights into your finances.

Set a Budget: Establish a budget specifically for sundries expenses to ensure you are allocating enough funds to cover these costs. Having a dedicated budget will prevent you from overspending in this category.

Review Regularly: Take the time to review your sundry expenses on a regular basis to identify any areas where you can cut costs or make adjustments. This proactive approach will help you stay in control of your expenses.

Importance of Budgeting for Sundries Expenses

Budgeting for sundries expenses is crucial for maintaining financial stability and ensuring that your business operates efficiently. While it may be tempting to overlook these small expenses, they can add up over time and impact your overall financial health.

By including sundries expenses in your budgeting process, you can:

Ensure Accuracy: Including sundry expenses in your budget will help you create a more accurate financial forecast and prevent any surprises down the road. It’s essential to account for these costs to maintain the integrity of your budget.

Track Trends: Monitoring your sundries over time can help you identify spending patterns and trends within your organization. This information can be valuable for making informed decisions about where you can cut costs or reallocate resources.

Improve Financial Planning: By budgeting for sundries expenses, you can plan ahead and allocate funds strategically. This proactive approach will help you avoid any financial pitfalls and ensure that you have enough resources to cover unexpected expenses.

Strategies for Budgeting Sundries Expenses

Creating a budget specifically for sundry expenses can help you manage your finances effectively and prevent overspending. Here are some strategies to consider when budgeting for sundries expenses:

Estimate Costs: Start by estimating your sundry expenses based on historical data or industry benchmarks. This will give you a baseline to work from when creating your budget.

Allocate Funds: Set aside a specific amount of money each month for sundries expenses. Be sure to account for any expected increases or fluctuations in these costs to avoid any budgeting surprises.

Monitor Spending: Keep track of your sundries expenses throughout the month to ensure you are staying within your budget. If you notice that you are exceeding your allocated funds, take steps to adjust your spending accordingly.

Re-evaluate Regularly: Review your budget for sundries expenses on a regular basis to make any necessary adjustments. Your budget should be a living document that evolves with your business needs and financial goals.

Conclusion

In conclusion, understanding sundries expenses is essential for maintaining financial health and making informed decisions about your spending. By tracking these small, miscellaneous expenses, you can gain better control over your finances and ensure that you are not overlooking any costs that could impact your bottom line.

Whether you are a business owner or an individual looking to manage your personal finances more effectively, taking the time to understand and track your sundry expenses can help you achieve your financial goals. Remember, every penny counts, so don’t underestimate the importance of managing your sundries expenses. Start today by implementing some of the tips and strategies outlined in this article, and watch as your financial well-being improves.

0 notes

Text

Implications of the UK Minimum Wage Increase in 2024

New Post has been published on https://www.fastaccountant.co.uk/implications-of-the-uk-minimum-wage-increase-in-2024/

Implications of the UK Minimum Wage Increase in 2024

Overview of UK Minimum Wage

Hey there! Have you heard the news? In 2024, the United Kingdom is set to increase its minimum wage. This exciting development is sure to have far-reaching implications for workers across the country. From providing a boost to the economy to improving the living standards of individuals, this upcoming change is definitely something to keep an eye on. So, whether you’re an employee or an employer, let’s take a closer look at what this increase could mean for everyone involved.

The UK minimum wage serves as a legal safeguard, ensuring that workers are paid a fair and decent wage for their time and effort. It sets a baseline standard for employers, aiming to prevent exploitation and reduce income inequality. In 2024, the minimum wage in the UK is set to increase, which has sparked debates and discussions on its various implications. This article will explore the reasons for the minimum wage increase, examine the impact on workers and businesses, assess its effect on employment rates, discuss the inflationary effects, analyse the social and economic equality implications, delve into the political implications, and highlight the challenges and considerations that come with this change. Additionally, it will provide an international comparison, allowing for a broader perspective on the UK’s minimum wage policy.

Here’s a table showing the UK minimum wage rates for 2024:

Age Group Hourly Rate (2024) 21 Year Old and Over £11.44 18-20 Year Old Rate £8.60 Under 18 Rate £6.40 Apprentice Rate £6.40

These rates are subject to change on 1 April each year based on government updates, but they reflect the current values for 2024.

Reasons for Minimum Wage Increase in 2024

The decision to increase the minimum wage in 2024 is motivated by several factors. Firstly, the cost of living in the UK has been steadily rising, necessitating a wage increase to ensure workers can meet their basic needs without difficulty. Moreover, the government aims to address income inequality by narrowing the gap between the lowest and highest earners. Increasing the minimum wage is seen as a way to distribute wealth more equitably and improve the overall well-being of workers. Additionally, political pressure and public sentiment have pushed for a higher minimum wage, with individuals and organizations advocating for fairer pay and better living standards for workers.

youtube

Impact on Workers

Increased Income

One of the immediate and direct benefits of the minimum wage increase is the enhanced income for workers. This raise can make a substantial difference in the financial security and quality of life for many individuals and families. With a higher minimum wage, workers can have more disposable income, which can be spent on necessities, savings, or recreational activities. This increased earning potential can bring about a sense of empowerment and provide opportunities for self-improvement and personal growth.

Reduction in Poverty

A significant impact of the minimum wage increase is its potential to reduce levels of poverty. By lifting the wages of low-income workers, the government aims to alleviate financial hardship and lessen the reliance on social welfare programs. When individuals earn a decent wage, they are less likely to experience poverty and are better equipped to provide for their families. Moreover, reducing poverty levels benefits society as a whole by diminishing the strain on public resources and creating a more inclusive and stable economy.

Improved Standard of Living

An improved standard of living is another positive outcome of the minimum wage increase. Workers will have the means to afford essential goods and services, such as housing, food, healthcare, and education. This can lead to an overall improvement in the well-being and happiness of individuals, as they no longer have to struggle to meet their basic needs. Moreover, a higher minimum wage can provide workers with a sense of dignity and self-worth, knowing that their labour is valued and rewarded appropriately.

Impact on Businesses

Increased Labour Costs

While the minimum wage increase is beneficial for workers, it poses challenges for businesses, particularly in terms of increased labour costs. Employers will need to allocate more funds towards paying their employees, which can impact their profitability. Small businesses, in particular, may struggle to absorb these higher costs, as they often operate on slim profit margins. The additional financial burden can potentially place strains on cash flow and make it harder for businesses to invest in other areas such as expansion, innovation, or employee training.

Impact on Small Businesses

Small businesses are more likely to be negatively affected by the minimum wage increase due to their limited resources and lower profit margins compared to larger corporations. The rise in labor costs can squeeze their profit margins even further, potentially leading to difficult decisions such as reducing staff or cutting back on benefits. This can have a detrimental impact on the overall growth and sustainability of small businesses, which are essential to the UK economy. Considering the importance of small businesses in generating employment and fostering entrepreneurship, steps should be taken to support them during this transition.

Potential Job Losses

One of the main concerns surrounding a minimum wage increase is the potential for job losses. The higher labour costs can make it financially challenging for businesses to maintain their workforce, leading to downsizing or even closures. Employers may find it necessary to automate certain processes or outsource labour to countries with lower wage levels, which could result in unemployment for some workers. It is crucial for policymakers to carefully monitor the impact of the minimum wage increase on employment rates to ensure that it does not inadvertently hinder job creation.

Effect on Employment Rates

Potential Job Creation

Contrary to concerns about job losses, a minimum wage increase can also lead to potential job creation. When workers have more disposable income, they are likely to spend more, stimulating demand and subsequently creating a need for additional workers. This can particularly benefit sectors that rely heavily on consumer spending, such as retail, hospitality, and services. By increasing the purchasing power of workers, a higher minimum wage can contribute to economic growth and generate employment opportunities.

Impact on Unemployment Rates

The impact of the minimum wage increase on unemployment rates is a topic of debate among economists. Some argue that higher labor costs may discourage employers from hiring, potentially leading to higher unemployment rates. However, empirical evidence suggests that the impact on unemployment is generally modest, with no significant long-term negative effects. Policymakers need to strike a balance between ensuring fair wages and considering the potential impact on employment rates to achieve a sustainable economy.

Inflationary Effects

Rising Prices

One possible consequence of a minimum wage increase is the potential for rising prices. As businesses face higher labor costs, they may pass on these additional expenses to consumers through increased prices for goods and services. This can result in a general inflationary effect, impacting the purchasing power of not only minimum wage earners but also the wider population. It is crucial for policymakers to carefully monitor and manage inflation to prevent its detrimental effects on the economy, particularly for low-income individuals who may bear the brunt of rising prices.

Impact on Cost of Living

The increased cost of living is another consideration resulting from a minimum wage increase. While workers may earn more, the rise in prices can offset the benefits of a higher wage, especially if the increase is not substantial enough. Policymakers need to address this concern by ensuring that the minimum wage keeps pace with inflation and rising living expenses. Additionally, measures should be implemented to mitigate the potential inflationary effects of a minimum wage increase, such as providing tax incentives for businesses or implementing price control policies.

Social and Economic Equality

Reduction in Income Inequality

Addressing income inequality is a significant motivation for increasing the minimum wage. By lifting the wages of low-income workers, the government seeks to reduce the income gap between the lowest and highest earners. This can lead to a more equitable distribution of wealth and contribute to social cohesion. When individuals at the bottom of the income scale earn a fairer wage, it can alleviate feelings of injustice and resentment, fostering stronger communities and promoting social mobility.

Narrowing Gender Pay Gap

The minimum wage increase can also contribute to narrowing the gender pay gap. Women, who statistically earn less than their male counterparts, make up a significant proportion of minimum wage earners. By raising the minimum wage, more women will benefit from increased earnings and improved financial stability. This can have far-reaching effects, empowering women economically and promoting gender equality in the workforce. However, it is important to acknowledge that the minimum wage increase alone is not sufficient to fully address the complex factors contributing to the gender pay gap, and additional measures are needed to achieve substantial progress.

Political Implications

Public Perception

The minimum wage increase has implications for public perception and can shape the image of government and political parties. A higher minimum wage is often seen as a policy that prioritizes the well-being of workers and demonstrates a commitment to social justice and equality. It can improve public trust in elected officials and enhance the perception that the government is responsive to the needs of the people. Conversely, mishandling the minimum wage increase or failing to deliver on promised improvements can lead to public disillusionment and erode confidence in political leadership.

Political Parties and Policies

The minimum wage increase is an issue that political parties can leverage for electoral gain. Parties that champion workers’ rights and fair wages are likely to benefit from public support, particularly from low-income individuals and those directly affected by the minimum wage increase. Conversely, parties opposing the minimum wage increase may face backlash, particularly if their stance is perceived as favouring businesses over workers. The minimum wage policy can become a defining aspect of a political party’s platform and shape voters’ choices during elections.

Challenges and Considerations

Regional Disparities

One challenge in implementing a minimum wage increase is the regional disparities across the UK. The cost of living and average wages can vary significantly between different regions and cities. While a uniform minimum wage policy aims to provide a standard level of protection for all workers, it may not adequately address the differing economic conditions across the country. Policymakers must carefully consider the potential impact of a minimum wage increase on businesses and employment rates in regions with lower average wages to avoid exacerbating regional disparities and unintended consequences.

Potential Non-compliance

Another consideration is the potential for non-compliance with the minimum wage increase. Employers may attempt to evade their obligation to pay the higher minimum wage by engaging in illegal employment practices or underreporting hours worked. To effectively address this issue, strict enforcement measures and penalties for non-compliance should be in place. Moreover, efforts should be made to improve workers’ awareness of their rights and avenues of recourse to ensure that they receive the wages they are entitled to.

Impact on Other Benefits

A potential challenge resulting from a minimum wage increase is its impact on other benefits received by low-income individuals. Some individuals may be eligible for means-tested benefits, which are reduced as their earnings increase. Although a higher minimum wage improves income, it may simultaneously reduce or eliminate these benefits, leading to a net decrease in overall financial support. Policymakers need to consider the intricate relationship between the minimum wage and other income-related policies, ensuring that the safety net for vulnerable individuals remains intact and that the benefits system is adjusted accordingly.

International Comparison

Comparison with Other Countries’ Minimum Wages

Considering the minimum wage increase within an international context provides valuable insights. Comparisons with other countries’ minimum wages can help determine whether the UK’s minimum wage is competitive and aligned with global labor standards. It allows policymakers to assess the likely impacts of the minimum wage increase by examining the experiences of other nations. International comparisons also provide an opportunity to learn from successful implementations and adopt best practices to maximize the benefits of a higher minimum wage while mitigating potential drawbacks.

In conclusion, the minimum wage increase in the UK in 2024 has the potential to significantly impact workers, businesses, and the economy as a whole. While it aims to improve the living standards of workers and reduce income inequality, it poses challenges for businesses, particularly small enterprises. Policymakers should consider the potential inflationary effects and the impact on employment rates to ensure a sustainable economy. Moreover, addressing regional disparities, ensuring compliance, and tackling other benefits-related issues are crucial to the successful implementation of the minimum wage increase. By considering international comparisons and learning from other countries’ experiences, the UK can navigate this change effectively and achieve a fairer and more prosperous society.

0 notes

Text

How to Claim a Tax Refund for the Years 6 April 2020 to 5 April 2023

New Post has been published on https://www.fastaccountant.co.uk/how-to-claim-a-tax-refund/

How to Claim a Tax Refund for the Years 6 April 2020 to 5 April 2023

If you’re looking to claim a tax refund for the years 6 April 2020 to 5 April 2023, you’re in luck! The process is actually quite simple. If you didn’t receive a tax calculation letter from HM Revenue and Customs (HMRC) after the end of each tax year, it’s likely that you paid the right amount of tax. However, if you believe you paid too much, there are a few ways you can claim a refund. The first step to claim a tax refund is to sign in to your personal tax account and check how much tax you paid for each tax year. From there, you can inform HMRC by sending an update for each year that you believe you overpaid. If you don’t have a personal tax account, don’t worry – setting one up is easy. Alternatively, you can contact HMRC directly and explain the situation. HMRC will review your claim and let you know if you’re due a refund. If you are, you can typically expect to receive it within 3 weeks. It’s important to note that HMRC doesn’t send out details of tax refunds via email, so be cautious of any suspicious emails claiming to be from HMRC. Now that you know the steps, you’re one step closer to claiming your well-deserved tax refund!

Check if you’re eligible to claim a tax refund

If you’re wondering whether you’re eligible for a tax refund, there are a few steps you can take to find out. One way to determine if you’re due a refund is to check if you received a tax calculation letter, also known as a P800, from HM Revenue and Customs (HMRC) after the end of each tax year. If you did not receive a P800, it’s likely that you paid the right amount of tax and may not be eligible for a refund.

Another method to claim tax relief for job-related expenses, such as uniforms, tools, and professional subscriptions, is to access your personal tax account. By signing in to your personal tax account, you can check how much tax you paid for each tax year and inform HMRC by sending an update for each year you believe you overpaid tax. If you don’t have a personal tax account, you can easily set one up.

If you think you’ve paid too much tax but did not receive a P800 or if you prefer an alternative method to inform HMRC, you can contact them directly and explain the reasons for your overpaid tax. HMRC provides a calculator that you can use to estimate your Income Tax for previous tax years, which can help you determine if you’re eligible to claim a tax refund.

It is important to note that HMRC does not notify taxpayers about tax refunds via email. If you receive an email claiming to be from HMRC regarding a tax refund, it is likely a scam. You should report any suspicious emails to HMRC and exercise caution when providing personal or financial information.

Response from HMRC

Once you have informed HMRC about your overpaid tax, they will review your case and provide a response. This response could include a confirmation of your tax refund or an explanation as to why you are not eligible to claim a tax refund. In some cases, HMRC may request further information from you to clarify any details or resolve any discrepancies.

Timeline for receiving tax refund

If you are due a tax refund, you can typically expect to receive it within 3 weeks. However, it’s important to keep in mind that the exact response time may vary. To get a more accurate estimate of when you can expect a reply, you can check HMRC’s website for the estimated response time.

It’s also worth noting that if HMRC determines that you did not overpay any tax, you may not qualify for a refund. In this case, you may receive a response from HMRC explaining why you are not eligible to claim a tax refund.

Determine the reason for overpaid tax

To better understand why you have overpaid tax, it is important to specify the source of the overpaid tax. This could include income from a job, pension payments, or other sources of taxable income. By identifying the tax payment period, you can gain a clearer picture of when and why the overpayment occurred.

0 notes

Text

Companies House

New Post has been published on https://www.fastaccountant.co.uk/companies-house/

Companies House

So, you’re thinking of starting your own business in the UK but not sure where to begin? Look no further! In this article, we will guide you through the process of registering your business with UK Companies House. From understanding the importance of registration to the step-by-step process, we’ll provide you with all the necessary information to get your business up and running legally in no time. Whether you’re a budding entrepreneur or an experienced business owner, this article is here to help you navigate through the registration process with ease. So, let’s get started on your exciting journey towards establishing your very own business in the UK!

Overview of UK Companies House

What is UK Companies House?

UK Companies House is the government agency responsible for the incorporation, registration, and regulation of Limited companies in the United Kingdom. It maintains a database of all registered companies and provides a range of services to businesses and the public. The primary role of UK Companies House is to ensure transparency and accuracy in business information, enabling companies to operate legally and effectively.

Benefits of registering a business with UK Companies House

Registering your business with UK Companies House comes with a range of benefits. Firstly, it provides legal protection by establishing the company as a separate legal entity, which shields the owners and directors from personal liability for business debts. This protection offers peace of mind and reassurance to business owners. Secondly, registration with Companies House enhances the reputation and credibility of the business, as it signifies compliance with legal and financial regulations. This is particularly important when establishing relationships with suppliers, customers, and potential investors. Lastly, registering a business with Companies House enables access to various services and resources offered by the agency, such as easy access to business information, online filing services, and support for compliance with reporting obligations.

Types of Business Entities

Sole proprietorship

A sole proprietorship is the simplest and most common form of business entity. It is owned and operated by a single individual, who is personally responsible for all aspects of the business. While there is no legal distinction between the owner and the business, registering a sole proprietorship with UK Companies House is not mandatory. However, if the business is operating under a name that is not the owner’s legal name, it is advisable to register a “trading as” (T/A) name to protect the business name and establish legal recognition.

Partnership

A partnership is a business structure in which two or more individuals share ownership and management responsibilities. Partnerships can be either “general partnerships” or “limited partnerships.” In a general partnership, all partners have unlimited liability for the business’s debts and obligations. In a limited partnership, there are one or more “general partners” who have unlimited liability, and “limited partners” who have limited liability and play a passive role in the business. Registering a partnership with UK Companies House is not mandatory, but it is highly recommended to establish legal recognition and clarity on the rights, responsibilities, and liabilities of each partner.

Limited liability partnership (LLP)

A limited liability partnership (LLP) is a hybrid business structure that combines elements of a partnership and a company. It offers limited liability protection to its partners while providing the flexibility of a partnership in terms of management and taxation. LLPs are commonly favored by professional service firms, such as law firms, accounting practices, and consultancy agencies. Registering an LLP with UK Companies House is a legal requirement and involves the submission of specific documents and information, including a statement of compliance, a registered office address, and details of the designated members.

Private limited company (Ltd)

A private limited company (Ltd) is a separate legal entity from its owners (shareholders) and directors. It is the most common form of legal structure for small and medium-sized businesses in the UK. A private limited company has limited liability, meaning that the shareholders’ personal assets are not at risk if the company fails. Registering a private limited company with UK Companies House is mandatory and involves the submission of various documents, such as a Memorandum of Association, Articles of Association, details of directors and shareholders, and a registered office address.

Public limited company (PLC)

A public limited company (PLC) is a company that has shares available for public trading on a stock exchange. It offers limited liability to its shareholders and operates under stricter regulations compared to private limited companies. Registering a PLC with UK Companies House involves additional requirements, such as a minimum share capital, appointments of a company secretary and qualified auditor, and specific regulations governing the company’s operations and reporting obligations.

Requirements for Registering a Business

Choosing a business name

When registering a business with UK Companies House, choosing a suitable name is crucial. The business name should be unique, not already registered with Companies House, and should not infringe upon any trademarks. It should also reflect the nature of the business and be easily recognizable and memorable. Before finalizing a name, it is advisable to conduct a thorough search using the Companies House online database to ensure its availability.

Registered office address

A registered office address is the official address of a company, used for all formal communications and legal purposes. It must be a physical address within the same jurisdiction where the company is registered (e.g., England and Wales, Scotland, or Northern Ireland). The registered office address must be displayed on all company correspondence and must be accessible for public inspection. It can be the company’s actual place of business or a separate address provided by a registered office service.

Directors and company officers

Every business registered with UK Companies House must have at least one director who is responsible for overseeing the company’s activities and complying with legal obligations. A director must be at least 16 years old and not disqualified from acting as a director. In addition to directors, a company may also have other officers, such as a company secretary, who assists with administrative tasks and compliance with regulatory requirements. Directors and officers must provide their details, including names, addresses, and dates of birth, when registering the company.

Company shareholders

In a company limited by shares, the shareholders are the owners of the company. They own shares in the company’s capital and have certain rights and obligations associated with their ownership. When registering a company, the details of the shareholders must be provided, including their names, addresses, and the number of shares they hold. It is important to note that the shareholders’ personal details will be publicly available through the Companies House register.

Memorandum of Association

The Memorandum of Association is a legal document that sets out the company’s name, registered office address, nature of business, and details of its initial shareholders and share capital. It acts as the company’s constitution and defines the relationship between the company and its shareholders. A Memorandum of Association must be submitted to Companies House during the registration process.

Articles of Association

The Articles of Association are another legal document that governs the internal workings and management of the company. It outlines the rules and regulations for the company’s operations, including the rights, duties, and responsibilities of the directors and shareholders. While model Articles of Association are provided by Companies House, companies can also create bespoke articles tailored to their specific needs and requirements.

Steps to Register a Business

Online registration

The easiest and most convenient way to register a business with UK Companies House is through the online registration process. Companies House provides an online platform called WebFiling, which allows businesses to complete and submit the necessary forms electronically. This method ensures faster processing times and minimizes errors by providing real-time validation of information.

Completing the required forms

During the registration process, various forms must be completed and submitted to UK Companies House. These forms include Form IN01, which provides details about the company’s directors, shareholders, registered office address, and share capital structure. Other forms may be required depending on the type of business entity being registered, such as Form LLP2 for a limited liability partnership or Form SH01 for an allotment of shares.

Paying the registration fees

There are registration fees associated with registering a business with UK Companies House. The amount depends on the type of business entity being registered. The fees can be paid online using a credit or debit card, or by setting up a direct debit if multiple registrations are anticipated. It is important to note that the registration fees are non-refundable, even if the application is rejected.

Submitting the application

Once the required forms have been completed and the registration fees paid, the application can be submitted to UK Companies House. If using the online registration process, the forms can be uploaded directly to the WebFiling system. Once submitted, the application will be reviewed by Companies House, and if everything is in order, the company will be registered and receive a Certificate of Incorporation.

Processing Time and Cost

Standard processing time

The standard processing time for registering a business with UK Companies House is typically around 48 hours. This is the time it takes for Companies House to review the application, process the necessary documents, and issue the Certificate of Incorporation. However, it is important to note that the processing time can vary depending on the workload at Companies House and any additional checks or clarifications that may be required.

Fast-track processing options

For those who require a quicker registration process, UK Companies House offers several fast-track processing options. This includes same-day registration, which guarantees that the application will be processed on the day of submission. Additionally, there is a 24-hour expedited service and a same-day postal service for those who prefer to send their application via mail.

Maintaining and Updating Business Information

Annual filings

After registering a business with UK Companies House, companies have ongoing obligations to provide certain annual or periodic filings. These filings include annual financial statements and confirmation statements. The due dates for these filings are typically one year from the company’s date of incorporation, and failure to submit them on time can result in penalties and potential legal consequences.

Changes to business details

It is essential to keep the information registered with Companies House up to date. This includes notifying Companies House of any changes to the company’s registered office address, directors, shareholders, and other company officers. Updates can be made through the WebFiling system or by submitting the necessary forms by mail. Failure to update the information within a reasonable timeframe can lead to administrative issues and potential penalties.

Reporting obligations

Registered companies have reporting obligations to various government agencies, including HM Revenue and Customs (HMRC) and Companies House. These obligations include filing annual financial statements with Companies House, submitting tax returns to HMRC, and complying with other regulatory requirements specific to the industry in which the business operates. Understanding and fulfilling these reporting obligations is essential to ensure compliance with legal and financial regulations.

youtube

Documents and Records

Certificate of Incorporation

The Certificate of Incorporation is a legal document issued by Companies House after a business has been successfully registered. It certifies that the company exists as a separate legal entity and provides its unique company registration number. The Certificate of Incorporation is an important document that may be required when opening a business bank account, entering into contracts, or dealing with other organizations.

Statutory registers

Companies registered with UK Companies House must maintain various statutory registers. These registers include the register of members (shareholders), register of directors, register of charges, and register of persons with significant control (PSC). These registers must be up to date and available for public inspection upon request. Failure to maintain these registers can result in penalties and potential legal consequences.

Annual financial statements

Every year, registered companies must prepare and file annual financial statements with Companies House. These statements include a balance sheet, profit and loss statement, cash flow statement, and accompanying notes. The financial statements provide an overview of the company’s financial performance, position, and cash flows, allowing stakeholders to assess the company’s financial health and performance.

Shareholder and director resolutions

Shareholder and director resolutions are formal decisions made by the company’s shareholders or directors. They are required for certain significant actions, such as appointing directors, changing the company’s articles of association, amending share capital, or distributing dividends. Resolutions must be properly recorded and kept in the company’s records as they serve as evidence of the decision-making process.

Taxation and Legal Obligations

Corporation Tax

Registered companies in the UK have a legal obligation to pay Corporation Tax on their profits. Corporation Tax is based on the company’s taxable profits, which are calculated by deducting allowable expenses and reliefs from the company’s total income. It is important for companies to understand their tax obligations, keep accurate and up-to-date financial records, and submit their Corporation Tax returns to HMRC within the specified timeframe.

VAT registration

Value Added Tax (VAT) is a consumption tax that is added to the price of most goods and services in the UK. Businesses with an annual turnover above the VAT threshold (currently £85,000) are required to register for VAT with HMRC. VAT-registered businesses must charge VAT on their sales, file regular VAT returns, and make payments to HMRC accordingly. Registering for VAT can provide benefit to companies that sell goods or services to other VAT-registered businesses, as they can reclaim VAT on their purchases and expenses.

Employment law and payroll

Registered companies in the UK have specific legal obligations when it comes to employment law and payroll. These obligations include registering as an employer with HMRC, operating a payroll system, deducting and paying taxes and National Insurance contributions from employees’ salaries, and providing employees with certain statutory employment rights and benefits. Failure to comply with employment law can result in penalties and potential legal consequences.

Financial reporting requirements

Registered companies must comply with financial reporting requirements, which include preparing and filing annual financial statements with Companies House. The financial statements must comply with Generally Accepted Accounting Principles (GAAP) and provide a true and fair view of the company’s financial position and performance. Certain companies may also be required to have their financial statements audited by a qualified auditor.

Data protection and privacy

Registered companies must comply with data protection and privacy regulations, especially the General Data Protection Regulation (GDPR). This includes obtaining consent from individuals to collect and process their personal data, handling personal data securely, and providing individuals with certain rights to access and control their personal data. Compliance with data protection and privacy regulations is essential to protect the rights and privacy of individuals and to avoid potential legal consequences.

Additional Services Offered by UK Companies House

Company name availability checker

Before registering a business with UK Companies House, it is advisable to use the company name availability checker provided on the Companies House website. This free online tool allows businesses to search for existing registered company names and trademarks to ensure that the desired name is unique and available for use.

Companies House WebFiling service

The Companies House WebFiling service is an online platform that allows businesses to easily file and submit various documents and forms electronically. The service provides real-time validation of information, reducing errors and improving efficiency. It also offers additional features such as electronic signatures for certain documents and the ability to track the progress of submissions.

Company search services

Companies House provides various company search services that allow individuals and businesses to access information about registered companies. These services include searching for company details, such as registered address, directors, and shareholders, as well as obtaining copies of company documents, such as annual financial statements and resolutions. The information provided by these services can be valuable for due diligence, research, and decision-making processes.

Guidance and support

UK Companies House offers guidance and support to businesses throughout the registration process and beyond. This includes providing comprehensive guidance on the registration requirements, offering support in completing the necessary forms, and assisting with any queries or issues that may arise. Companies House also provides online resources, webinars, and workshops to help businesses understand and fulfil their legal and regulatory obligations.

Conclusion

Registering a business with UK Companies House is a crucial step for any business operating in the United Kingdom. It offers legal recognition and protection, enhances credibility and reputation, and provides access to various resources and services. By understanding the registration process, requirements, and obligations, businesses can ensure compliance with regulatory and reporting obligations and lay a solid foundation for their success. Whether it is a sole proprietorship, partnership, limited liability partnership, private limited company, or public limited company, UK Companies House is a valuable resource and partner in the journey of running a successful business.

0 notes

Text

All About The 40% Tax Bracket

New Post has been published on https://www.fastaccountant.co.uk/all-about-the-40-tax-bracket/

All About The 40% Tax Bracket

Let’s demystify the 40% tax bracket in the UK. In simple terms, the 40% tax bracket refers to the income range where individuals in the UK are subject to a higher tax rate. It’s important to understand how this bracket works, as it can significantly affect your earnings and financial planning. By gaining a clear understanding of the 40% tax bracket, you can make informed decisions about your finances and ensure that you are making the most of your hard-earned money.

What is the 40% Tax Bracket in UK?

The 40% tax bracket in the UK refers to the income range where individuals are subject to a tax rate of 40%. This means that any income earned within this bracket will be taxed at a higher rate compared to the lower income brackets. Understanding how tax brackets work and the implications of being in the 40% tax bracket is important for individuals in the UK who fall within this category. In this article, we will explore the ins and outs of the 40% tax bracket, its impact on take-home pay, the concept of marginal tax rates, who typically falls into this bracket, tax planning strategies to mitigate tax liability, and the potential impact on savings and investments.

Understanding Tax Brackets

Defining tax brackets