Last Seen Blogs

swordandbackpack

Sword & Backpack

lipa-home

lipa's home

el-amo-teletubbie-blog

MASTER-SLENDYTUBBIE

musicasdelmundodestacado

DESTACADO MDM

ras-homo-n

Moss

Text

Reasonable Health Insurance For Small Businesses

Medical coverage Innovative Choices are arranged so that it empowers wellbeing plans to be less expensive for minor endeavors. Diaries, rules, and data talk about on protection plans for vehicles, wellbeing, life, home, endeavors, creatures and such. There are a few spots where ventures are obligatory to give their laborers a health care coverage, if the organization has in excess of five workers. Despite occasion or work excursion; travel protection is significant in current society to guarantee your movement spending, wellbeing, properties and occasion nostalgic minutes are gotten. Assuming you are a provider, incapacity inclusion is an absolute necessity as your wards will have a back up.

Senate Bill permits little undertakings to buy health care coverage arrangements with avoidance from certain state incorporation necessities. Additionally, the Senate Bill 1955 supports the consolidation of protection buying as mass to be made for organizations under an exchange or expert association. Our esteemed providers give amazing tweaked bunch health care coverage for little undertakings, satisfying the requirements in costing, arrangement and organization. Medical coverage for little undertakings can be incredibly exorbitant and choices to reduction can be heartbreaking for laborers. Individual Californian Health Insurance Scheme, family wellbeing plans, little endeavors bunch health care coverage specialists are a portion of the models for decisions. This is unquestionably very hard for these protection firms as the contention is hardened universal health insurance scheme upsc.

The most normal protection pursued are in the scope of little office-work space (SOHO) like business products, proficient dangers, singular complaint, information base crash, robbery, realty credit, and so forth There are a lot more choices I can give. This plan incorporates individual effects which are not guaranteed at all by different organizations, cash repayments, and it is likewise covering undertaking income and extra overheads.

Use a wide scope of protection for big business possessions. Our altered plans will cover a broad extent of assets and dangers to suit your business nature. During the dynamic to purchase business protection, do consider hazard inclusion to financially guarantee your business is supporting harmed and injury to customers, workers and shops. You may likewise wish to add on all inclusive danger, worker repayment and such. This business protection plan will guarantee supervisors to have a wellbeing net in case of robberies by own laborers. Additionally, managers will be ensured little pay when there are challenges experienced because of cataclysmic events. Direct property misfortunes protection isn't sufficient really, for a private company. That is the reason a significant number of these SOHOs are made bankrupt for the time being, on the grounds that the remuneration isn't pretty much as broad as circuitous property misfortunes protection. Customary protections need to approve that the property is really spoilt before the payout happens. Business protection bars this need and repayment can be made without the need to see the real misfortunes; useful for independent companies.

The greater part of business people buy all-round hazard protection to keep away from law clashes coming about because of remissness claims. Online organizations should look for altered protection which covers misfortunes because of the demonstration of gatecrashers and infections. General danger protection is obviously strongly suggested in the event that you start a business. In spite of the fact that item hazard protection isn't modest, it is as yet a-absolute necessity thing. Item hazard protection is additionally important for thought, on the off chance that you wish to bargain underway things. On top of these, you can really request to redo your business protection to suit your itemized liabilities.

0 notes

Text

5 Reasons Why Life Insurance Is Important To You

Extra security. Doesn't it simply evoke some protection sales rep thumping on your entryway attempting to sell you a strategy that covers you for mishaps just, for a modest quantity and costs you the earth? No? It doesn't too me either on the grounds that those days are a distant memory!

I like to call it "Life Assurance" in any case, since it is guaranteeing you that your life is convered in case of death and that what your life is safeguarded for, will be paid out to your bequest or strategy proprietor.

In any case, what number of you really have this cover set up? I am aware of loads of my companions, who are in their 20's who don't have the cover since 1) they know nothing about (absence of instruction) and 2) they don't think they need it and consider it to be an additional expense. How little they know... like anything, the previous you start, the less expensive it is...

Following are 10 significant reasons why YOU ought to have life affirmation and why people around you also ought to put resources into this:

Reason 1

Hi? Do you have any bills, as perhaps a home loan?? This by itself is an appropriate motivation to have life affirmation... it implies that should you pass on, this significant bill will be paid off and not left to your survivors to manage!

Reason 2

Youthful, fit and solid? No illnesses? Then, at that point this is the best an ideal opportunity to get life confirmation! Your top notch will be little and on the off chance that you take out an arrangement that permits you to keep a similar premium until the age of 65, you will have extensive investment funds... the previous you start, the better. And afterward in the event that you foster any medical problems for the duration of your life, it doesn't make any difference, since you as of now have the cover set up!

Reason 3

It is safe to say that you are hitched? Do you think often about your mate? Then, at that point is it not insightful to ensure that your life partner doesn't need to stress over cash would it be a good idea for you to pass before they do and the other way around? I know a couple who dropped their life coverage and afterward a half year after the fact he was analyzed as having stomach malignant growth, and kicked the bucket year and a half later... leaving behind a spouse and two youngsters still at home and a home loan... furthermore, no monetry alleviation for his family. Is this what you need to put your accomplice through?

Reason 4

Need to leave a heritage for your future fantastic kids? What better way then, at that point guaranteeing your bequest will really have some inheritance to pass on! You can choose in your will to have the returns of your life affirmation paid straightforwardly to your bequest and afterward according to your will, divy up the returns importance of life insurance notes.

Reason 5

True serenity... yours that is. In the event that you can't manage the cost of health care coverage or some other protection, you can bear the cost of extra security... also, should you foster a fatal sickness... your extra security will pay out a singular endless supply of this, permitting you to satisfy any fantasies you have not accomplished or to get your issues all together.

There are a lot more reasons I could go into here, however you get the substance... actually like you wouldn't chance not having your vehicle safeguarded or your home or substance... how could you not protect your main resource... yourself?

There are a lot of incredible monetary counselors out there. On the off chance that you don't have one, an incredible spot to begin is your bank, they have prepared staff that can direct you... simply ensure you read through any statements you get and so forth and ensure you see exactly the thing you are being covered for.

0 notes

Text

Why Health Insurance Is Important To Young Individuals In Texas

Youthful people in Dallas, Houston and all through Texas are a beautiful sound gathering as a rule, however abandoning health care coverage meddles with their admittance to the medical services framework, acquaints hindrances with care when it's required, and leaves youthful people and their families in danger for high cash based expenses notwithstanding extreme sickness or injury.

All things considered, nineteenth birthday celebrations appear to be a critical achievement in many Americans' health care coverage inclusion. Both public and private protection plans treat this age as a defining moment for inclusion choices. In Texas, youthful grown-ups who are not full-time understudies lose their status as a qualified ward after 19. A full-time understudy stays a qualified ward in Texas until age 25.

Further, Texas health care coverage guideline expresses that most private health care coverage plans "may not condition inclusion for a kid more youthful than 25 years old on the kid's being enlisted at an instructive foundation. This guideline anyway doesn't help each youthful grown-up. Self-protected enormous gatherings might be excluded from the guideline. Furthermore, the guardians might be just incapable to keep paying a youthful grown-up's expenses.

At the point when youthful grown-ups lose inclusion under their folks' arrangements, paying little heed to age, their binds with essential consideration doctors might be cut exactly when they ought to shape more grounded connections to the medical services framework and assuming liability for their own consideration importance of health insurance ppt.

These are only a couple of reasons inclusion is so significant for youthful grown-ups:

o Fourteen percent of grown-ups ages 18 to 29 are corpulent. Since the 1990s, corpulence has expanded by 70% in this age bunch — the quickest pace of increment among all grown-ups.

o There are 3.5 million pregnancies every year among the 21 million ladies ages 19 to 29.

o Injury-related visits to trauma centers are undeniably more normal among youthful grown-ups than they are among kids or more established grown-ups.

A new medical coverage review shows that people who are uninsured or have not exactly sufficient health care coverage have their admittance to the medical services framework diminished. The greater part of youthful grown-ups, ages 19 to 29, who either were uninsured for the whole year or had a period without inclusion said that they had abandoned required medical services due to cost. Delinquent consideration included neglecting to fill a medicine, not seeing a specialist or expert when wiped out, or skirting a suggested clinical trial, treatment, or follow-up visit.

Also, uninsured youthful grown-ups are undeniably more outlandish than those with inclusion to have a customary specialist. Only 33% of uninsured youthful grown-ups, ages 19 to 29, had a normal specialist, contrasted and 81 percent of the individuals who were safeguarded the entire year. Uninsured female youthful grown-ups had standard specialists at about a large portion of the pace of young ladies who were protected the entire year. Male youthful grown-ups who were uninsured had the most delicate connection to the medical services framework; only 21% had a normal specialist contrasted and 75 percent of male youthful grown-ups who were protected the entire year.

Numerous youthful grown-ups likewise have issues covering hospital expenses or are taking care of clinical obligation over the long run. More than 33% of every youthful grown-up, both guaranteed and uninsured, said that they had encountered issues with hospital expenses: experiencing difficulty making installments, being reached by an assortment organization due to failure to cover bills, altogether changing their lifestyle to take care of hospital expenses, or taking care of clinical obligation over the long run. Uninsured youthful people were the most troubled with doctor's visit expenses and obligation, with practically half detailing no less than one issue.

However, in spite of mainstream thinking, youthful people appear to esteem the security that health care coverage inclusion offers. A similar review likewise found that almost 3/4 of utilized youthful grown-ups acknowledge health care coverage inclusion when it's offered, just somewhat not exactly the acknowledgment pace of laborers age 30 or more established.

0 notes

Text

Term Or Permanent Life Insurance

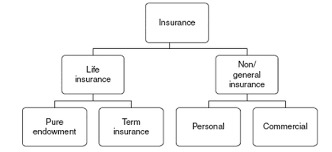

Protection is a significant apparatus of securing ourselves, our family and our resources. It is a vital piece of any venture arranging. There are different protection offices and different kinds of protection you can go in for. So how would you choose which protection is beneficial for you. Various kinds of life coverage are:

Term protection: Term life coverage keeps going as long as the residency of the approach. This is an unadulterated protection which implies there are no money benefits related with this strategy. The strategy can be taken for 1-30 years. On the off chance that the safeguarded endures the quantity of long periods of the approach no money advantage will be given once the arrangement terminates. On the off chance that the safeguarded kicks the bucket during strategy term, his/her recipient will get the total guaranteed.

Super durable Life Insurance comprises of Whole life, Variable life and Universal disaster protection.

Entire Life Insurance: This sort of protection has no time limit related with it. This approach proceeds till the demise of the safeguarded. You need to routinely pay yearly expenses for it. As well as giving life inclusion, this strategy likewise continues to assemble cash esteem. After a specific period you can even take credit against gathered money which are 'tax-exempt'. In any case, this sort of protection is somewhat unbendable as the guaranteed individual doesn't have the decision of choosing his venture portfolio.

Variable Insurance: This sort of protection gives a specific degree of deftly to the guaranteed. The guaranteed has the influence to choose where to put away his cash from a large group of choices given by the insurance agency's portfolio. This is the most costly of all money esteem protection arrangements.

All inclusive Insurance: This protection India strategy develops cash esteem as well as giving life cover. The protected has the adaptability to change the premium and reserve funds of the arrangement every now and then as per his desires. You can likewise make your yearly exceptional installments from the aggregated money esteem throughout the long term.

The least expensive protection you can get is bunch protection. This commonly is given by the organization you work for and is a term protection strategy. Your admittance to the existence cover given by bunch strategy keeps going as long as you keep on working for the organization types of life insurance policies ppt.

There are different variables which choose the general expense of the protection strategy. Like which sort of strategy you are purchasing, the sum you are getting it for, your general wellbeing, occupation and so forth Entire extra security arrangements are by and large costlier than term disaster protection. Since entire protection additionally gives you a speculation alternative, the top notch that you pay for it is significantly higher than term protection premium. You should examine the protection archives minutely prior to proceeding with buying an approach, as insurance agencies typically deduct specialist commission and an assortment of expenses from your charge paid. The specialists by and large try not to reveal all expenses and costs identified with a strategy and solely after you have purchased the arrangement do you become more acquainted with about them. Demand considering a strategy handout and understanding the arrangement exhaustively prior to submitting your well deserved cash for the approach.

0 notes

Text

Business Practice Liability Insurance (EPLI) - Is This Type Of Insurance Right For Your Company

Numerous insurance agencies currently offer what is known as work rehearses obligation protection (EPLI). Regardless of whether a business chooses for buy such protection inclusion is a choice which ought to be made with care and solely after a total survey of different alternatives open to the business.

Your protection specialist or human asset advisor might encourage your business to buy work practice responsibility protection (EPLI) in the expectation or conviction that this protection will ensure your business against the danger of substantial monetary misfortunes coming about because of work claims. Be that as it may, as most regions in the field of work law, there are seldom straightforward responses to these basic issues; there are no enchantment slugs.

The run of the mill EPLI strategy will normally cover cases of unjust release, working environment badgering, and separation. Different arrangements may likewise cover such issues as attack of protection, careless employing, slander, and deliberate curse of passionate pain. In assessing any EPLI strategy, it is important that the business knows precisely which representative cases are covered and which are not.

Identified with the issue of which sorts of cases are covered is the subject of which kinds of representative cases are not covered. The kinds of cases that are not shrouded are portrayed in a part of the protection strategy called "Rejections." Typically, the language in the approach managing prohibitions is extremely intricate, and consequently should be perused cautiously. Eventually during the time spent assessing whether to buy EPLI protection, or a specific EPLI strategy, the business should look for the exhortation of a lawyer to survey the approach language. Something else, the business may accept that the business was shielding itself from likely obligation for worker claims, when actually the arrangement covers very little employment practices examples.

Another basic issue in assessing an EPLI strategy is strategy limits and the deductibles. The EPLI strategy will for the most part contain a for each guarantee limit just as a total cutoff for all cases made under the arrangement. The business should survey these approach restricts cautiously to guarantee that the necessities of the business are being fulfilled.

Identified with the issue of strategy limits is the topic of the deductable. As in some other type of protection, the higher the deductable, the lower the exceptional installment. Assuming the business picks a high deductable, it is accepted that the business is ready to shield minor worker claims itself, while different cases with a high dollar hazard potential will be covered by the EPLI strategy.

As to lawyer charges and expenses, the costs brought about regarding the guard of a representative case are covered by the protection strategy. Notwithstanding, recollect that if a case is covered by the protection strategy, the protection transporter will generally dole out the case to a lawyer which the transporter picks. That lawyer won't really be as acquainted with your business as the lawyer who as a rule addresses the business. There is consistently the danger that the lawyer chose by the protection transporter might treat the case against your organization as essentially simply one more case that the person should deal with.

Identified with the issue of which lawyer addresses the organization in a covered case is the significant inquiry of settlement. An insurance agency manages the topic of settlement of a worker guarantee with the very methodology that is uses to think about settlement of some other case, for example, a property harm guarantee or other loss guarantee. To a protection transporter, each guarantee has a settlement esteem. This methodology overlooks the representative relations sway that settlement of a specific case might have on the labor force all in all. In the event that the business gets a standing for settling any claim documented by a fired representative, the business will confront the truth that any fired worker will anticipate some kind of money related repayment, regardless explanation has provoked their release.

0 notes

Text

Biotech Venture Capital Fund

Biotech investment reserve openings have come as a major aid for business visionaries needing to foster new medications and infection medicines. They are rewarding on the grounds that they improve inside perspective on every single living organic entity. These require assets and they are not effectively accessible from customary loaning offices. The banks we think about are designed to certain set frameworks and conditions and don't have any desire to move away from them.

Surefire benefits

Biotech adventures range a wide range as they can be about creature, human and mechanical biotechnology. It incorporates items and benefits and relying upon your fitness, you would be searching for the right region where you can bring in cash. What's more, making surefire benefits with new and out of the case thoughts are likewise the fastest method to get subsidizing for your venture. You could likewise be creating biosensors, biotech hardware and drugs.

These days, the customary financial backers have accepted a rearward sitting arrangement as they would prefer not to stop their assets in new and what they believe are unsafe endeavors. In any case, you can get all assistance from biotech investment reserve supervisors as they are not just able to accept chances as they have an eye for out of the container thoughts that can tolerate fruiting, yet additionally offer hands on help to get you on target. New pursuits in the space of biotech are promising, yet they offer a wide scope of development openings too.

The explanation is for the viewing pleasure of anyone passing by as biotech investment store finished off the rundown with almost $639 million for 66 organizations. Financing for biotech adventures have gone up 14% on the rear of expanded interest for such businesses. Asset administrators are likewise amped up for the benefits that can be created in the new field of clinical gadgets and life sciences 10 disadvantages of venture capital.

Extraordinary freedom as a business person

You have an extraordinary chance as a business visionary in these fields on the grounds that the gen X-er age has begun to age and they are burdened with a large group of infections. The new kinds of infections have caused the interest in biotech to fill significantly more over the most recent couple of years. Irresistible infections are an extraordinary concern and have additionally prompted a flood being developed of more up to date methods of battling them.

To fix them, new and further developed antibodies are required that are sponsored by state of the art research. To fuel speculations, biotech investment reserve is the solitary way out. Adventure reserves are likewise discovering the development of this new clinical exploration region rewarding as benefits are coming in quick for business people who have figured out how to get in right on time.

0 notes

Text

Get Car Gap Insurance to Avoid Negative Equity

The keep going thing that is at the forefront of your thoughts when you go to your nearby business to get your fresh out of the plastic new vehicle is the thing that would occur on the off chance that you discounted it heading out from the vendor. Many individuals imagine that with completely exhaustive protection they will not have an issue. Much of the time this couldn't possibly be more off-base. Numerous new vehicles will lose a fifth of their worth when you drive off the forecourt, sadly thorough protection won't cover this devaluation and you might end up in the circumstance where you need to track down a couple thousand just to trade your vehicle 'like for like'. This is actually the circumstance where Guaranteed Asset Protection or GAP Insurance will secure you against this conceivable misfortune.

So how precisely does Return to Invoice GAP Insurance work? Essentially because of your vehicle being discounted, RTI GAP Insurance will pay the error between your Motor Insurance Payout and the sum that you initially paid for the vehicle. Suppose you purchased another vehicle for £19,995 and after two years your engine insurance agency discounts your vehicle because of it being in a mishap. Shockingly they just offer you £10,000 as a settlement. In the event that you have RTI GAP Insurance (Subject to the general arrangement claims limit that you select when you take the strategy out) GAP Insurance would pay the £9,995 distinction between your Motor Insurance payout (£10,000) and the first receipt value you paid for the vehicle (£19,995).

Many individuals see GAP Insurance as simply one more way for the business to snag somewhat more of your well deserved money. In fact vendors can charge expense rates for their arrangements, yet don't let that put you off this protection item. Search around on the web and you will rapidly discover a lot of organizations that offer Gap Insurance at rates far lower than you might have been offered by your vendor what is zd in car insurance in hindi.

With more than 500 vehicles consistently being engaged with mishaps and up to a large portion of 1,000,000 vehicles a year being announced a complete misfortune in the UK, RTI GAP Insurance is an extraordinary method to cover yourself and get you far from that feared negative value.

Similarly as with other 'genuine feelings of serenity' protection items, there is a decent possibility you may never have to make a case, yet for the individuals who do wind up in the position that their vehicle has been discounted and the insurance agency payout misses the mark concerning their assumptions, GAP Insurance can be the solution to their supplications. Everybody knows somebody who has a shocking tale about losing cash when they've had a fender bender and in these seasons of the worldwide credit crunch, new vehicles appear to lose their worth speedier than at any other time, only one more motivation to consider GAP Insurance when you purchase another vehicle. Before you leave all necessary signatures in the vendor be that as it may, ensure you get your work done, search the web and you will most likely save yourself somewhere in the range of forty and 70% for a comparative approach.

0 notes

Text

Kinds of Property Insurance Coverage

There are Twelve kinds of Property Insurance inclusion

Substitution cost inclusion: Replacement cost inclusion is the kind of property protection that will consistently ensure that the expense of your property confirmation is being paid paying little mind to destruction or expanding of cash. Substitution cost inclusion is made simple so property protection customer, go through less cash to get new same sort of item that the affirmation organization doesn't consider to pay.

Blast Insurance: Explosion recompense inclusion is a sort of protection strategy one necessities to have, this sort of a protection is intended to secure and cover the deficiency of property because of blast.

Fire Insurance: This is a kind of property remittance that fundamentally thought to harms brought about by a fire. Fire confirmation inclusion gives the security to harm brought about by a fire into your property.

Airplane Insurance Coverage: Aircraft stipend inclusion is somewhat protection that arrangements or intended to ensure your property on the off chance that the Aircraft pulverize on your property.

Home Insurance: Home arrangement covers both property and Liability,using single expense which covers for all dangers. Home Insurance is otherwise called numerous line protection inclusion, it covers private homes likewise bond's different sorts of individual Insurance.

Robbery Insurance: Theft protection is the sort of property inclusion that covers the harm of the property because of thievery, burglary and so forth

Uproar/Civil upheaval: This is a kind of property inclusion that shield or covers your property from the harm brought about by the Riot. It takes care of the expense caused in savage unsettling influence brought about by at least four individuals in your property. kinds of arrangement incorporate a part of risk inclusion. For instance, a mortgage holder's protection strategy will regularly incorporate risk inclusion which secures the safeguarded in case of a case brought by somebody who slips and falls on the property; accident coverage additionally incorporates a part of obligation arrangement that indemninate against the mischief that a slamming vehicle can cause to others' lives, wellbeing, or property personal property insurance.

Volcanic Eruption: Volcanic Eruption is a sort of property arrangement that covers your property against the blast brought about by Volcanic Eruption.

Hail Insurance: Hail Insurance inclusion is a sort of protection cover that shield your property against misfortunes due from hail.

Tropical storms: Hurricanes Insured inclusion is the sort of protection that is intended to cover or ensure your property against the misfortunes brought about by typhoon

Flood Insurance: Flood Insurance inclusion is a sort of property protection made to cover your property from the harm brought about by floods into your property.

Tremor Insurance : This is a sort of property recompense that is configuration to cover the harm that has been brought about by a quake to your property. Rates contrast not set in stone on the area you are arranged in. Homes made of wood have less expensive rates than Homes made of block.

0 notes

Text

Try not to Make This Common Mistake in Calculating Medical Expenses

With the significant expenses of clinical consideration today, almost certainly, clinical costs involve a critical piece of your organized derivations. While a lot of derivations can prompt an enormous personal duty discount, it is significant not to incidentally exaggerate your clinical costs by including clinical repayments. Just those sums paid during the available year for which you got no protection or other repayment can be remembered for your costs for charge purposes. On the off chance that you get repayments from clinical costs from protection or different sources, like Medicare, during the year, you should diminish your absolute clinical costs for the year by the measure of the repayments. You don't have a clinical derivation in case you are repaid for the entirety of your clinical costs for the year.

Arrangements Pertaining to Specific Expenses. Some clinical and protection arrangements give repayments to just certain particular costs. On the off chance that you get repayments from such a strategy, you should utilize the aggregate sums you get to decrease your complete costs, including those the approach doesn't give repayment to. The accompanying model has been given by the IRS to clarify this kind of circumstance:

Model. You have protection strategies that cover your clinic and specialists' bills yet not your nursing bills. The protection you get for the medical clinic and specialists' bills is more than their charges. In calculating your clinical allowance, you should diminish the aggregate sum you spent for clinical consideration by the aggregate sum of protection you got, regardless of whether the arrangements don't cover a portion of your clinical costs.

Wellbeing Reimbursement Arrangement (HRA). Wellbeing repayment plans are manager financed plans that are subsidized exclusively by the worker. HRAs repay workers for clinical consideration expenses and permit unused sums to be conveyed forward. Repayments for clinical costs, up to a greatest dollar sum for an inclusion period, are excluded from the worker's pay.

Abundance Reimbursements. You might need to remember for money any sum you are repaid that is more than your connected costs.

Expenses Paid by You. By and large, you do exclude the abundance repayments in your gross pay that are from a clinical protection or comparable arrangement wherein you paid the whole premium reimbursement of medical expenses form.

Expenses Paid by You and Your Employer. Segments of overabundance repayments ought to be remembered for your gross pay if both you and your manager add to the clinical protection plan from which you got abundance repayments. This is just the situation in case your manager's commitments are excluded from your gross pay.

Repayments in a Later Year. In case you are repaid for clinical costs that you paid in an earlier year, you by and large should report the repayment as pay up to the sum you recently deducted as clinical costs. Just report as pay the sum you got that decreased your assessments in the prior year. In the event that you didn't deduct a clinical costs in a year you paid it, and later got a repayment for it, do exclude the repayment up to the measure of the cost in pay.

0 notes

Text

Why Mortgage Processing Companies Are Irreplaceable Assets for Home Loans Lenders

Home loan preparing organizations are very objective. The jobs they play empower loaning establishments focus on other beneficial spaces of their organizations. Moneylenders reevaluate credit application work to these organizations. Normally contract credits banks select, prepare and do everything to hold their advance handling staff. This method isn't just tedious yet in addition expensive. The time used to enlist and perform new representatives direction strategy could be spent all the more productively if a bank chooses to utilize handling organizations.

Representatives exploit in-the-work preparing possibly to leave startlingly when they become great credit officials. Home loan preparing organizations, then again, can be relied on for a long time until an entire year is finished. One thing that is so energizing about utilizing them is that they have a distant office. They are not subsidiary to a loan specialist as full-time workers yet as self employed entities. Therefore, they don't anticipate any commissions, advantages, month to month checks, get-away leaves, laborers' pay protection, office space, office furniture or whatever else with the exception of the concurred charge sbi property insurance for home loan.

These home loan handling organizations go into an agreement with the loaning foundations they have decided to work with. When an agreement is endorsed by the two players the arrangement formally starts. An advance handling firm performs its responsibilities in its workplaces for 24 hours per day. Its job is to confront the advance candidates in the interest of advance officials, agents, banks, and different foundations that are associated with loaning cash for purchasing a home. This implies that the home loan preparing organizations have prepared experts who are acceptable at their positions as well as proficient on issue of land. They are indispensable resources for Home Loans moneylenders that need the accompanying.

• Ability to be in charge of enlarging applications

• A totally reliable client support that reacts rapidly and precisely to customers.

0 notes

Text

Have a sense of safety With Best Travel Insurance Coverage

Bajaj Allianz life coverage is a particular corporate among the world goliaths like Bajaj auto and Allianz bunch. Bajaj auto is the biggest producer of bikes and three wheelers on the planet and Allianz bunch is one of the highest level insurance agencies on the planet. Bajaj Allianz insurance agency has in excess of 800 workplaces around the entire world and around 4 million fulfilled customers. Bajaj Allianz life coverage organization gives a broad assortment of protection plans and approaches.

Bajaj Allianz protection offers advantageous installment plans like charge cards, Visas, checks, or straightforwardly from their clients financial balances. The amicable and patient specialists of Bajaj Allianz disaster protection helps in the determinations of protection approaches, statements and terms that best suits every people needs.

Bajaj Allianz offers a wide assortment of protection in India. Sidekick, travel world class and understudy travel are the main protection designs under Bajaj Allianz. They are additionally giving other itinerary items like corporate protection, travel Asia and travel swadesh yatra. We should go in to certain subtleties of these plans.

Partner in crime is a movement protection strategy which is a far reaching bundle which gives total clinical and wellbeing cover to the worldwide explorer. You can pick an appropriate arrangement as indicated by your necessities from the partner in crime protection plan which offers modified designs for individual, family and senior resident old enough, 61-70. This strategy covers individual mishap, clinical costs and bringing home, misfortune and postponement of checked stuff, individual responsibility, loss of identification, credit only assistance, hospitalization costs, seize cover, crisis loan, trip delay, golf players opening in-one and so forth

Travel tip top is a modified online travel protection that gives the insightful voyager a decent scope of arrangements to browse, where every strategy will be redone to meet your particular necessities. One can pick the approach contingent upon whether they are an understudy, a finance manager, senior resident, corporate chief or one going with the family. There are plans for individual, family, and senior resident old enough, 61-70 and senior resident old enough, 71-75 in the movement world class protection plan offered by Bajaj Allianz policy bazaar travel insurance customer care.

Understudy travel protection plan is exceptionally intended for understudies to make their movement hazard free. This arrangement offers assurance for an understudy's just as inclusion for other fundamental necessities like clinical and hospitalization help. There are three plans which go under understudy travel. They are study buddy plan, understudy tip top arrangement and researchers guide and splendid personalities.

Corporate worldwide travel is an exhaustive arrangement which gives total clinical and wellbeing cover to the global business explorer. This arrangement covers your excursions for work abroad. Bajaj Allianz offers altered designs for all intents and purposes each necessity of corporate workers voyaging abroad. Partner, first class and age 61-70 plans go under the corporate protection plan.

0 notes

Text

The History of Life Insurance

The historical backdrop of Life Insurance is anything but an extremely hard one to comprehend. Today, Life protection is basically the agreement between a solitary individual and an insurance agency directing that the organization is to pay the approach holder's recipient if the safeguarded passes on. Be that as it may, where did being protected at death come from? Who were the principal individuals that executed this thought? How did they respond when the measures of cash were not as high as those of the organizations in the extra security industry today? When did the genuine disaster protection industry began? Every one of these are really intriguing inquiries and the truth is that some of them can't be offered an explanation to a serious degree; anyway we do know a ton about the historical backdrop of this brilliant thing that today covers individuals from one side of the planet to the other.

The First Few Signs in Life Insurance History

History specialists have been looking for the genuine beginning of extra security as far as we might be concerned, yet they have first unraveled the child steps that at long last finished in the real demise advantage installment. As indicated by the Financial Shopper Network in Ancient China mariners would keep privateers from taking every one of their products via conveying parts of different boats payloads, along these lines if a privateer took the freight of one boat, the whole burden would not be lost. Somewhat later in Babylon brokers basically gave credits that must be reimbursed when the substance of the exchange were conveyed securely history of general insurance in india.

So what does this have to do with life coverage? Well both of those civic establishments were forestalling losing everything. They were doing little small steps that would help over the long haul. Life coverage as far as we might be concerned in any case; began in the city of Rome. Individuals of this profoundly progressed human advancement chose to frame what they called "entombment clubs". These clubs were planned with one sole reason, in the event of a startling demise of a club part; every other person would pay for their funerary costs and help the group of the survivor with some cash. The idea of life coverage as far as they might be concerned finished drastically in the year 450 A.D. at the point when the Roman Empire fell and its practices were deserted for an extensive stretch of time. Feature that numerous antiquarians concur that about simultaneously of Rome, the Indian Empire and its residents additionally framed "internment clubs" to pay for memorial services and help individuals with costs. A hint of this as per the Financial Shopper Network is that the "yogakshema, the name of Life Insurance Corporation of Indian's Corporate Headquarters" alludes to the Vedas.

0 notes

Text

Significance of Bicycle Insurance for Cyclists

Inclusion Overview

When a cyclist obtains bike protection, the strategy is probably going to give pay to bicycle areas that can be fixed, such the casing and wheels, alongside the full expense for the bicycle in case it's added up to after an accident. The insurance agency can direct cyclists to believed bicycle looks for a maintenance. What's more, insurance for robbery of the bicycle might be incorporated. Approaches even join helps that are like collision protection like side of the road help and bicycle rentals.

In the event that a mishap harms the cyclist's riding garments, an arrangement might take care of the expense to supplant them. Clinical service for actual harm that others might get during a mishap is another element of many bike protection programs.

Plan Options

Bike insurance agencies offer an assortment of plans. Hence, cyclists can choose a strategy dependent on their necessities. Choices incorporate projects with various deductible cutoff points, for example, $100, $300 or $500. At the point when cyclists pick protection that secures them for actual harm to their bicycle, approaches will ordinarily safeguard the bicycle against impacts, defacing and fire.

About Bike Rental Compensation

On the off chance that a cyclist harms their bicycle during a rivalry, the protection strategy might give repayment to a rental. Accordingly, racers can in any case contend to guarantee that their many preparing hours are not squandered 5-year bike insurance price.

Charge Reimbursements

Bike protection gives repayment to rivalry charges when the cyclist can't take an interest in an occasion. Most arrangements have remuneration cutoff points, for example, $500 for every rivalry and $1000 for the strategy stretch. Remember that to fit the bill for a rivalry expense repayment, the bicycle harm should happen under conditions that the insurance agency will cover.

Bike Parts Protection

An arrangement might ensure bicycle proprietors for lost or harmed parts. The insurance agency will for the most part have a security limit. For instance, it might conceal to $500 for every episode including misfortune or harm with a complete restriction of $1000.

About Liability Insurance

Remember that obligation protection won't cover wounds that the policyholder supports during a mishap, yet it will cover individuals that they might hurt. Additionally, the program might ensure the cyclist for property harm. For example, if the safeguarded rider runs into another cyclist or through a mortgage holder's fence, then, at that point the strategy will give monetary assurance.

Wounds or Damage Caused By a Vehicle

At the point when cyclists share the street with engine vehicles, they might be engaged with a car crash. On the off chance that the driver of the vehicle doesn't have protection, the cyclist's bike strategy will give monetary inclusion. The assurance will probably highlight occurrence cutoff points, for example, $25,000 or $50,000, which will rely on the bicycle proprietor's approach.

About Roadside Assistance

Emergency aides offers many advantages. For example, it will secure cyclists during bicycle disappointments like broken chains and punctured tires. The element will give transportation to abandoned riders. Be that as it may, the program might contain a cutoff like five episodes for every strategy period.

The Importance of Bicycle Insurance

At the point when cyclists secure themselves with bike protection, they can ride straightforward as their arrangement will defend them against possible monetary episodes. Moreover, cyclists who buy protection are assuming liability for the wounds and harm that their pastime might cause to other people.

End

Bike protection offers extensive inclusion for bicycle proprietors as they will have insurance against robbery and harm. Approaches ensure cyclists monetarily by including responsibility inclusion and contest expense repayment. Additionally, genuine bicycle riders will see the value in the significant serenity that bicycle protection gives.

0 notes

Text

Outsider Car Insurance Explained

For the large numbers of drivers who have an incredible awareness of certain expectations yet have somewhat less in the method of monetary clout with regards to running a vehicle on the streets of the UK, vehicle protection is a region that pretty much rules out mobility. Outsider cover is frequently the solitary alternative accessible to those with a limited spending plan as the expense of a charge at this level is generally the least expensive on offer, even in the days when it's feasible to track down a tremendous choice of modest vehicle protection bargains on the web.

Youthful drivers or the individuals who are new to the universe of motoring are the ones probably going to be offered, or ready to manage the cost of just, outsider cover as most UK vehicle insurance agencies would believe them to be a huge danger because of variables like age as well as naiveté. A vehicle that is more than thirty years of age will likewise make certain to draw in nothing above outsider protection cites from the vast majority of the main high road and direct back up plans, except if it is of incredible worth, in which case the fitting degree of cover can be acquired from expert organizations that manage exemplary vehicle protection.

It is a lawful necessity to basically give outsider in particular (TPO) cover for any vehicle being driven on the streets of the UK.

Anything short of that would mean no protection at all which, other than being illicit is additionally narrow minded, unreasonable and shameless and could leave the uninsured's travelers and other street clients incredibly defenseless. Being found driving while uninsured would not just give a criminal record and a monetary bad dream, yet could likewise make it troublesome - if certainly feasible - to at any point discover a vehicle insurance agency willing to offer cover once more cheapest third party car insurance.

Set forth plainly, in case you were engaged with a mishap that was considered your flaw, the other vehicle and its driver would be ensured by your outsider protection despite the fact that your approach would not permit you to guarantee for any harm never really claimed vehicle. Demise or injury of outsiders would be covered, as would the arrangement holder's lawful expenses in case of such cases, however a particularly essential degree of protection ought to possibly be thought of if spending limitations or lessened vehicle esteem take into account nothing else.

0 notes

Text

The most effective method to Find the Right Life Insurance Policy For Your Family

When looking for a life coverage strategy, the main thought is normally whether you should buy a term strategy or an entire life strategy. As a rule, the private company protection specialist you talk with will recommend that families think about buying entire extra security. These approaches, all things considered, offer the specialists bigger commissions.

In this article we will investigate the contrasts between entire life and term protection. By learning the benefits and hindrances for both you can securely settle on an educated choice for your family.

Entire Life Policies

Entire disaster protection arrangements offer the shopper the chance to put their charges into a protection account from which they can later pull out the cash. These arrangements can be decent in the event that you figure you would have to acquire against your protection strategy sooner or later.

Notwithstanding, what a protection specialist may not advise you promptly is that lone a little level of your regularly scheduled installment is really viewed as a superior that you can get against. With an entire life coverage strategy, however much 80% of the main yearly installments go toward the specialist's payments. For every year from that point onward, a lot of the yearly installments likewise go into the specialist's pockets. Just little rates of entire life coverage strategies go toward the acquired against sum that you are pitched when you purchase the arrangement.

Term Life Policies

Term disaster protection arrangements permit you to purchase a set-sum strategy. Term arrangements are vastly improved arrangements than they used to be. In a very long time past, an individual couldn't discover a term strategy for more than around 15 years. Presently, you can track down a 30-year strategy with little test. The sum you pay on a term protection life strategy is additionally to some degree sensible. Normally you can buy a $500,000 term strategy for a sound 45-year-elderly person for about $500. In case you're a solid lady who's 35 years of age, you could possibly buy a similar approach for about $260 every year. Protection specialists don't push these approaches as enormously, in light of the fact that they don't procure as much commission as they do with entire life arrangements.

Settling on The Decision

At the point when you are gauging your choices with a term or entire extra security life strategy, you ought to figure out what your necessities are for the approach. In the event that you might want to have the choice of utilizing a constrained speculation include worked in to your disaster protection strategy, entire life might be something you should take a gander at. For the vast majority, be that as it may, term independent company protection approaches are the best course best health insurance for female in india.

The two arrangements permit you to buy an approach and make month to month or yearly installments. Upon your passing, your recipient is paid a set sum. The distinction between the two fundamental sorts of strategies is that with an entire life strategy, the buyer has the chance to transform his disaster protection strategy into a speculation.

When you conclude whether to buy a term or entire life strategy, the subsequent stages are to track down a solid organization to buy the arrangement from, to decide how much inclusion you need and to track down the best cost for the measure of inclusion you are looking for. To decide how much inclusion you ought to have, you ought to decide how much cash your recipient depends on you for. In case you are the sole provider in your family, you may choose to buy a higher measure of inclusion for your mate upon your passing.

Make certain to search around. Various organizations offer distinctive premium costs for term arrangements for a similar measure of inclusion. Ensure you comprehend under which conditions a strategy would pay out and under which conditions the arrangement would not pay out. Settle on an informed choice dependent on your family's particular requirements.

0 notes

Text

LIC India NAV - What Benefits You Can Expect

Have you known about LIC Mutual Funds? They are truly outstanding. Extra security Corporation of India began "LIC Mutual Fund" in 1989. They have a great deal of plans that would procure you a larger number of advantages than some other ventures like bank fixed stores. This article would assist you with getting more subtleties.

What is NAV?

NAV is classified "Net Asset Value" of the specific plan. While the asset is dispatched, the NAV of one unit would be fixed Rs 10. When the asset begins playing out, the plan NAV worth will fluctuate appropriately toward the finish of the each exchanging day and you can get the most recent NAV subtleties from related sites or LIC site lic plan 5 years double money in hindi.

Advantages:

The NAV of the specific plan would assist you with estimating the exhibition of the specific plan. That will assist you with purchasing units at a lot less expensive cost so you can bring in more cash.

On the off chance that you put resources into Systematic money growth strategies, and if the NAV of the specific unit goes down in a specific month, then, at that point you can purchase more units which would assist you with purchasing the units at a lot less expensive cost.

A portion of the plans offer Tax Benefits for the financial backers under the "Part 80 C" of personal expense act. Under this plan, you can not pull out the sum for a very long time for example there would be a lock in period for a very long time. The financial backers can guarantee tax cuts for the sum that has been contributed.

0 notes

Text

Coverages and Types of Homeowners Insurance Policies

Home insurance refers to insurance on property that you own and certain personal liability insurance affiliated with that property. In most states, home policies are referred to as (HO1, HO2, HO3, HO5, and HO8.) HO6 refers to Condo Owners, and HO4 refers to Renters insurance. There is no HO7. Some states (Texas, for example) use different classification.

• HO1 Form: Also called Named Perils Policy. This is the basic form providing limited property coverage against certain 10 named perils, all other perils are excluded. These 10 perils are [Fire or Lightning, Windstorm or Hail, Explosion, Riot or Civil Commotion, Aircraft, Vehicles (unless caused by the insured), Smoke, Vandalism or Malicious Mischief, Theft, Volcanic Eruption.

• HO2 Form: Also Called Broad Named Perils Policy. This form provides coverage for the 10 named perils listed in the HO1 plus 6 more named perils. The additional 6 perils are [Falling Objects; Weight of Ice, Snow, or Sleet; Accidental Discharge or Overflow of Water or Stream; Sudden & Accidental Tearing Apart, Cracking, Burning, or Bulging; Freezing; Sudden & Accidental Damage from Artificially Generated Electric Current. There is no other perils covered beyond the named ones.

• HO3 Form: This is a hybrid policy and is called Open Perils (All Risks) Policy. This home insurance form provides coverage for almost all perils (hence called All Risk policy) on the structure of the house or the dwelling, but only broad coverage (as in HO2) on the content of the house, or the personal property. This is the most commonly used form of homeowners insurance. Certain perils that may be excluded from this policy are [Earthquakes, Water damage, Power Failure, Ordinance or law, Any action undertaken by the Government, War, Act of negligence, Intentional loss, Wear and tear, Fungus, Vermin, rodents, insects, birds; Deterioration.

• HO5 Form is a true full Open Peril, All Risks, Policy. This form provides coverage for the dwelling and the content of the home on All Risk basis.

• HO4 Form: Renters Insurance Policy. This is a named peril (limited to the 16 coverage in HO2) that cover the personal property of the people renting a premises and their liability. No coverage is offered for the structures of the residence.

• HO6 Form: Condo Policy. Provides similar protection as in HO3 except with regard to the Dwelling Coverage (dwelling of the condo.) In condominiums, the structures of the buildings are classified as "common areas" and are normally covered through the association. The owners of the units carry certificates extending to them the coverage from the master policy carried by the association.

• HO8 Form: The Market Value Policy. Normally insurance coverages on dwelling and content are determined by either the replacement cost or by the actual cash value. Policies issued with the actual cash value get upgraded by a -rider- to the Replacement Cost, at which point the base of the loss and claim will be the Replacement Cost for the loss, not how much the lost property was worth after depreciation (actual cash value.) HO8 is different. The value of the insurance is set at the Market Value of the property. Normally this insurance is available for older homes in depressed areas. [example: 75 year old home; 3,500 square foot, possible replacement cost is about $600,000, actual cash value $275,000]. If the house has a market value of $63,000, then insurance companies will do only HO8 policies types of fire insurance policy .

Coverages offered under these forms may include:

Coverage A- Dwelling Coverage: This is the amount of coverage on the actual structure of the house, and anything that is permanently attached to it. The proper amount of coverage is based on the Replacement Cost of the structure. So, depending on the area, size of the house, cost of construction, and quality of construction material used; the value of the house(hence amount of required insurance) will vary. Standard construction costs about $150 per foot, on the average. HO4 provides no coverage for dwelling. HO6 provides either little or no coverage for the dwelling.

Coverage B- Other Structures. This is 10% of Coverage A. It covers any detached construction like detached garage, gazebo, etc.

Coverage C- Personal Property or Contents. Covers your personal belongings, furniture, home appliances, cameras, TVs, personal computers, personal articles.. etc. The amount of coverage comes between 50% to 70% of Coverage A. Notice that there is a limit on certain articles (furs, jewelry, guns, etc.)

Coverage D- Loss of Use. In case your property becomes unfit for living your company will pay you for the increase in your living expenses [normally has a time limit of one year maximum, or a specific percentage (20%) of Coverage A.]

Coverage E- Personal Liability Protection: Protects you or covered family members against lawsuits made by others because of your negligence or the negligence of your family members. Normally it comes as $100,000 each occurrence, but can be increased.

0 notes