johnmauldin

John Mauldin

John Mauldin is a noted financial expert, a New York Times best-selling author, a pioneering online commentator, and the publisher of one of the first publications to provide investors with free, unbiased information and guidance—Thoughts from the...

538 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

dogzylife

DogzyLife

bob4647

Untitled

ladynearthelake

The Lady Near The Lake

throne-of-glass

Throne of Glass

Text

We Can’t Wait Any Longer for More Coronavirus Relief

The Federal Reserve acted quickly last March, cutting rates and launching a massive asset purchase program. Congress helped with a giant fiscal aid package.

Together, these jolted the economy back to life. The jolt wasn’t permanent, however.

The economic patient is now wavering again. This time, despite pleas from Fed Chairman Jerome Powell that monetary policy has reached its limits, the fiscal part of the cure is not forthcoming.

Ah, but “limits” don’t really apply to central bankers. Not the central bank of the world’s largest economy and issuer of the global reserve currency.

The Fed has constraints—some practical, some legal—but is highly creative in overcoming both. Powell repeated this quite clearly just last month.

Speaking to a San Francisco business group on November 17, he said, “The Fed will stay here and be strongly committed to using all of our tools to support the recovery for as long as it takes until the job is well and truly done.”

This was not the usual equivocating Fedspeak.

Powell promised to use all the Fed’s tools, for as long as it takes, until they are well and truly done.

No mention of any limits.

Powell isn’t one to make promises he doesn’t plan to keep.

So if the economy begins slipping into a double-dip recession, I believe he will open the spigot again. What the barrage will look like, I don’t know, but it is probably coming.

A quick note on all the angst surrounding Treasury Secretary Steve Mnuchin taking back some of the Federal Reserve’s CARES Act funding. First, the Fed used a little bit in the beginning, but much of that money was just sitting there.

My sources say Mnuchin is looking for a way to make a deal with Democrats more palatable to Republican senators. Recovering unused Fed money gives him almost $500 billion to soften their frustration with the price tag.

The Senate seems to want a number below $1 trillion.

With the recovered money, they could pass a “new bill” for less than $1 trillion, while actually spending more.

Whoever you blame for the deadlock, the simple fact is a bill needs to pass soon. I believe there is a serious risk of a double-dip recession without some major unemployment funding.

We have about reached the limits of jobs recovery absent a vaccine. That leaves us with a real-world unemployment rate higher than the Great Recession’s worst.

Waiting until February to pass a stimulus bill simply tempts the recession gods to strike again.

I wish they would just get a bill done. Forget about waiting for the Georgia elections; if Democrats take the Senate, they can pass a bigger bill later.

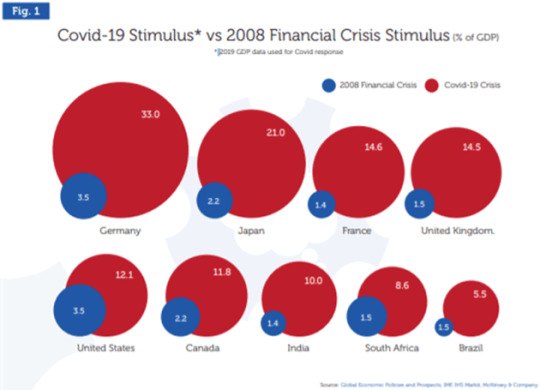

The US has done nowhere near what the largest developed world economies have done relative to their GDP. From Grant Williams’ latest letter:

Source: TTMYGH

Further, when you combine all the stimulus from around the world, it is a rather staggering amount in both size and variety. The Western European countries alone have provided 30 times more stimulus (in current dollars) than the Marshall plan after World War II.

Source: TTMYGH

Total global debt will be close to $300 trillion by the end of the first quarter 2021, and global GDP will have been decimated. Every major central bank, not just the Fed, has opened the monetary spigots. It is no wonder the market is levitating.

Unlike 2008, this crisis has an identifiable end point.

That is, if the new vaccines work as well as expected and are distributed in the next few months.

I worry more about the damage already done. Many of those lost jobs aren’t coming back. Millions of small businesses will never reopen.

Other new businesses will open, but that will take time and probably an effective, widely distributed vaccine. Some property owners will never again collect the kind of rent they used to.

All that adds up, and it will take a long time to repair and adjust to. Once we do, we’ll still have the preexisting debt and other problems.

But, this being the season when we give thanks, let’s also remember the good news. The crash efforts to develop COVID-19 treatments and vaccines are about to bear other fruit in the form of some amazing new biotechnologies. This is going to pull a lot of new health and medical technology forward from the future.

Change is happening swiftly and not always comfortably. Events that would have stretched over years seem to be happening all at once, which makes it a little unsettling.

I firmly believe we’re going to get through this and find a better world on the other side. And a relief package for those who help us get there is a good next step.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

This Was All Predicted 10 Years Ago

In 2010, the scientific journal Nature published a collection of opinions looking ahead 10 years, i.e., where we are right now.

Nature then published a short response from zoologist Peter Turchin in its February 2010 issue.

Quantitative historical analysis reveals that complex human societies are affected by recurrent — and predictable — waves of political instability (P. Turchin and S. A. Nefedov Secular Cycles Princeton Univ. Press; 2009). In the United States, we have stagnating or declining real wages, a growing gap between rich and poor, overproduction of young graduates with advanced degrees, and exploding public debt. These seemingly disparate social indicators are actually related to each other dynamically. They all experienced turning points during the 1970s. Historically, such developments have served as leading indicators of looming political instability.

Very long "secular cycles" interact with shorter-term processes. In the United States, 50-year instability spikes occurred around 1870, 1920 and 1970, so another could be due around 2020.

We are also entering a dip in the so-called Kondratiev wave, which traces 40- to 60-year economic-growth cycles. This could mean that future recessions will be severe.

In addition, the next decade will see a rapid growth in the number of people in their 20s, like the youth bulge that accompanied the turbulence of the 1960s and 1970s.

All these cycles look set to peak in the years around 2020.

Again, that was from 2010. Right on schedule, we are experiencing the “instability spike” Turchin says tends to come along every 50 years.

Why 50 years? It relates to the human lifespan.

Consider who was “in charge” during the period around 1970. Baby Boomers were all 25 or younger at the time. Managing the chaos fell on older generations, who remembered it well and spent the rest of their lives trying to prevent more of it.

But after 50 years or so, they are mostly gone. We who remain must learn the lesson again.

I’ve talked before about Neil Howe’s “Fourth Turning” idea, and George Friedman’s geopolitical cycles, both of which are peaking in this decade.

Interestingly, Friedman also sees a different geopolitical 50-year cycle playing out in the mid to late '20s. This overlaps with his 80-year geopolitical cycle for the first time. The mid- to late '20s should see the climax of Neil Howe’s Fourth Turning.

Now we see Peter Turchin postulating a similar time frame for different reasons. None of them, to my knowledge, expected the pandemic we are now experiencing. What is its effect?

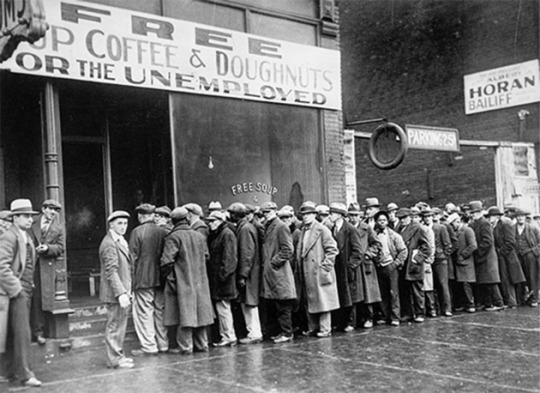

Well, we know the pandemic triggered a recession that may, before it's over, rival the Great Depression. For millions of Americans, it is not just something they read about. They feel it.

You’ve probably seen this famous 1931 photo of Al Capone’s Chicago soup kitchen.

Source: Wikimedia

The 2020 equivalent is happening in my former hometown Dallas. This photo from November brought a tear to my eye.

Source: CBSDFW via Twitter

We do see progress was made between these images. The people obviously have cars and fuel. Those were elite luxuries in 1931. Some of these people may be educated and intelligent, but they’re not elites.

Actual elites don’t have to wait in line for food. They call Whole Foods or DoorDash and have it delivered.

The problem, borrowing Turchin’s framework, is that some thought they were elites. Even if they didn't exactly think of themselves as elite, they did enjoy the benefits of good jobs. At least, until recently.

This year took away that illusion, and they’re naturally disappointed. They may join the “counter-elites” and seek more power.

This is where we are. The hard times we’ve long anticipated are here. That 1931 soup kitchen photo was just the beginning of a long, dark period. It got a lot worse.

Pay attention when you see multiple smart people reaching similar conclusions for different reasons. We are now at Turchin calls the final stage, when elites try to pacify the masses with bread and circuses. Doing so racks up the debt and suppresses economic growth.

Debt is accumulating faster than I expected, so The Great Reset may happen sooner than I expected. This pandemic and recession may push us there faster because they are making the debt grow faster.

Whenever it comes, we should welcome it. The alternatives may be even worse.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

4 notes

·

View notes

Text

A ‘Great Reset’ Is Coming… But Not for Capitalism

The Great Reset is my term for climactic events that resolve our global debt overload while at the same time dealing with slow economic growth, high unemployment and social unrest.

I've talked about this concept for many years. I expected this would happen after we hit a debt wall, likely in the late 2020s. But, like many other things that have been accelerated by current events, this type of Great Reset is coming even sooner.

More recently, others have started using this term for their own purposes. The World Economic Forum sees the coronavirus pandemic as an opportunity to completely reset capitalism.

"COVID-19 lockdowns may be gradually easing, but anxiety about the world’s social and economic prospects is only intensifying. There is good reason to worry: A sharp economic downturn has already begun, and we could be facing the worst depression since the 1930s. But, while this outcome is likely, it is not unavoidable.

"To achieve a better outcome, the world must act jointly and swiftly to revamp all aspects of our societies and economies, from education to social contracts and working conditions. Every country, from the United States to China, must participate, and every industry, from oil and gas to tech, must be transformed.

"In short, we need a 'Great Reset' of capitalism."

WEF calls this effort its “Great Reset Initiative.”

For the record, I think much of what they propose will make the version that I see even worse.

I agree capitalism has gone off track and needs some adjustments, and not just minor ones. The current morass of crony capitalism and lobbying for special government favors is abhorrent.

But “revamp all aspects of our societies and economies” sounds ominous. Especially coming from the WEF—the people who nominally run the global economy.

Further, what they really propose is that maybe they pay a little more in taxes while those further down the food chain carry the brunt of change.

When you start talking about resetting the educational and social contracts and working conditions, you are talking a radical social agenda. I believe we must—and will—have considerable change in the social structure of this country.

That is what the current partisan politics is telling us. Too many people on both sides feel the current “social contract,” however they define it, is not working for them. Income and wealth inequality are very real.

I am not convinced a WEF-style “Great Reset” is the answer.

Fortunately, I don’t think WEF will get very far. More likely, this is another example of wealthy, powerful elites salving their consciences with faux efforts to help the masses, and in the process make themselves even wealthier and more powerful.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

4 notes

·

View notes

Text

Election 2020: ‘A Major Bear Market of Political Decency’

I know many of you are wondering what happens if Joe Biden wins the 2020 presidential election? What happens if Donald Trump wins?

So, I called my friend Doug Kass to basically “wargame” the next 12 to 24 months. He’s a veteran trader and investor, one George Soros tried to hire on several occasions. So, when he has something to say, I listen closely.

Doug and I went back and forth on a few issues, but the bottom line is the same: We are in for a very rough ride.

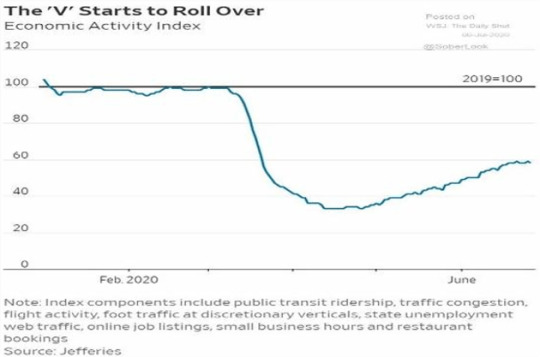

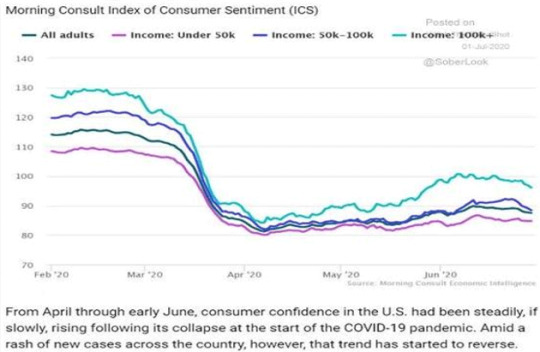

There is no magic recovery formula no matter who controls the government. Doug gave me a great quote that is appropriate for our times: “We are in a major bear market of political decency.”

Doug sent me one of his latest letters (and kindly let me share it with Over My Shoulder members). The two charts below show economic activity and consumer sentiment appear to be rolling over.

Source: RealMoney

Quoting Doug:

In aggregate terms, COVID-19 will likely have a sustained impact on the domestic economy—in reduced production and profitability—for several years, and in some industries, forever.

At the core of my concerns: important industries gutted.

Several key labor-intensive industries—education, lodging, entertainment (Broadway events, concerts, movie theatres, sporting events), restaurant, travel, retail, nonresidential real estate, etc.—face an existential threat to their core.

For these industries, the damage is done, as they simply cannot survive the conditions they face. For these gutted industries, we face, at best, an 80% to 85% recovery in the years to come.

It should be emphasized that, in the case of some of these sectors, like retail, COVID-19 sped up what was already a secular decline.

It is not a pretty picture. Government programs and safety nets can help, but they don’t magically produce GDP and jobs.

Doug and I agree that investors will be seriously disappointed in corporate earnings over the next two years. However, given the Fed’s money-printing, the market can keep rising even as the economy rolls over.

But at some point, lower earnings will have a market impact. Don’t ask me when, because I don’t know. But we shouldn’t be surprised when they do.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

3 notes

·

View notes

Text

Where the Jobs Aren’t

A century or two ago, industries would shrink and disappear over decades, while others arose at a similar pace.

Today, consumer preferences change before our eyes. Companies and entire industries spring up overnight… and can collapse just as quickly, as we saw with the arrival of the coronavirus in America.

As recently as February, Americans were getting on planes and eating in restaurants without a second thought. Now, many are not… and don’t intend to anytime soon.

That’s a giant problem for employment in those sectors—and for everyone else who depends on spending by those workers and their families. Non-government data also suggests any jobs recovery will take time… maybe even until 2026.

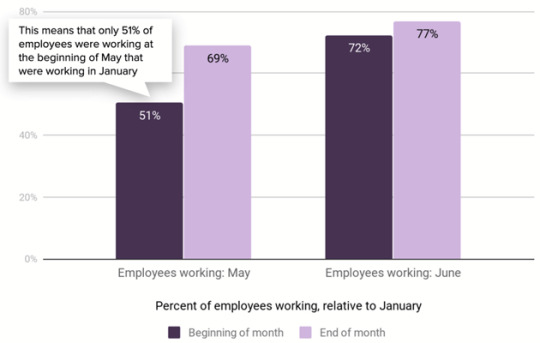

Homebase, an online provider of employee time tracking software, shows that only 51% of the employees who were working at the beginning of January were working four months later, at the beginning of May.

Source: Homebase

It improved considerably as businesses reopened, reaching 77% by the end of June. But in absolute terms, it remains disastrous to have 23% of workers still jobless.

The Homebase data was an early and accurate tip-off back in March, revealing a significant business slowdown even before mandatory closures. It may be doing the same now, as coronavirus cases surge across states that were in the process of reopening.

That’s bad news generally, and especially for the permanent job losers who need to find new work and those who had gotten called back, only to be cut loose again.

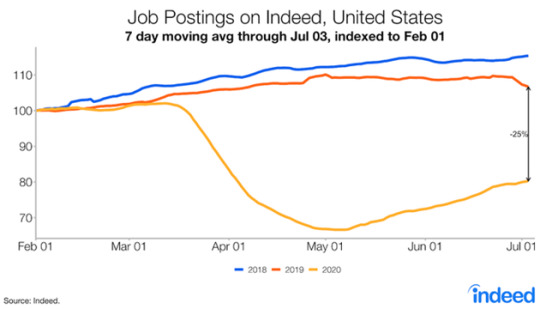

Indeed.com, a top job search site, is a good barometer for hiring activity. Fewer job postings mean fewer job opportunities for those seeking them. And that is indeed (pun intended) what has happened.

Source: Indeed

Job postings collapsed in March, bottomed in early May (consistent with the Homebase data) and have been rising slowly since them. But they remain fully 25% lower than February.

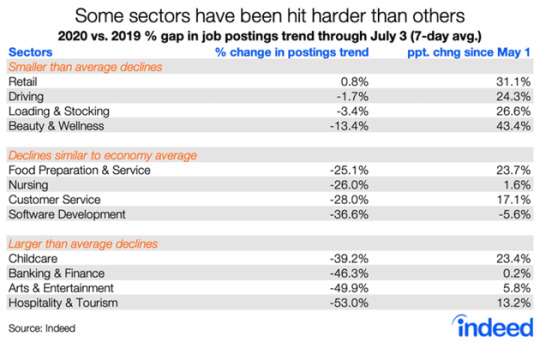

The kind of job openings tells us something, too. Indeed’s data shows which industries have the worst hiring non-activity.

Source: Indeed

As you might expect, hospitality and tourism are at the bottom of the list. Hotels are hurting badly. The fall in banking and finance listings is a bit mysterious. I suspect it might relate to mortgages, but we know banks have been closing and consolidating branches, too.

On the other end, “smaller than average declines” (since no sector was especially good) in job listings occurred in retail, driving, loading, stocking, beauty and wellness.

Those may be clues about where the economy is headed.

Retail, already changing rapidly, is now moving at lightspeed to online and hybrid distribution. “Order online and pick up at the store” is gaining popularity. Driving and warehouse work relates to this as well.

The beauty and wellness part? Obviously, most of us need haircuts. Beyond that, the virus seems to be making people pay more attention to their health. Wellness can include weight loss, nutrition, supplements, etc.

Yes, some specific areas and industries might do well. But consumer spending, consumer confidence, and business capital spending will be nowhere near normal. Neither will GDP growth.

And if we manage to recover from all that, we will still face a global recession and a slowdown in trade and travel.

Countries that have beaten down the coronavirus are understandably not going to admit travelers from places where it is rampant. This makes international commerce difficult, at best.

You might say we need to be less dependent on other countries like China, anyway. I agree. But cold turkey isn’t the best way to make that transition.

Last month I retired my longtime “muddle-through” paradigm and said we are in a stumble-through economy. Similarly, millions of workers are set to stumble through the next few years, looking for jobs that don’t exist.

They’ll be trying to gain new skills, juggling the checkbook as they try to stay afloat. Ditto for many business owners and managers.

This won’t be easy for anyone. We will stumble through, but not without some deep scratches and scraped knees.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

The Six-Year Jobs Recession

Most of us work for some form of paycheck, even the self-employed. Few subsist on their own efforts. Even retirees, politicians, and welfare recipients live off someone’s labor, if not their own.

Savings, if you have any, are the result of past labor. That makes a job shortage problematic for everyone, not just the jobless.

The June US employment report showed some welcome improvement. Businesses brought back many workers as parts of the country reopened. That’s great but it was only a start. We need several more months like that, and it’s not at all clear they are coming.

To be fair, there isn’t a lot of clarity when we look back at past data, either.

One little-noticed effect of COVID-19 is the havoc it wrought on our employment data. Government statistics have always had their quirks, and often measure the wrong things, but the bureaucracy is at least consistent. It collects the same numbers, the same way, over and over again.

Not anymore.

When is someone unemployed, exactly? Suddenly we have workers who are/were:

Temporarily furloughed, with the employer intending (but not promising) to bring them back. Meanwhile they might or might not be collecting unemployment benefits.

Effectively furloughed. They aren’t working, but still on their employer’s payroll with help from the PPP program.

Working for fewer hours and/or for lower wages. Not jobless, but rather in some sort of limbo.

Never formally “employees” but independent contractors, like Uber drivers. In previous recessions, they wouldn’t have received any benefits but this time, thanks to the CARES Act, they do… maybe. Some states are implementing that program slowly, if at all.

Historically, the Bureau of Labor Statistics considered someone “unemployed” if they were able to work and seeking work, but not currently working. Yet now millions can work, but aren’t looking, because they expect to be called back but may not be. How do we classify them?

There’s a vast difference between the numbers filing unemployment benefit claims vs. the surveys BLS conducts for the monthly employment report. Those benefit claims are also questionable, since state agencies were inundated with claims they couldn’t process.

Then there is the question of how extra benefits have affected people’s willingness to work. If you can make more money staying home than by working, staying home is perfectly rational. But will you admit that in a government survey?

Clearly, many businesses are closed and many workers jobless. Some will go back, but some jobs will be permanently lost. That’s true in any recession.

The difference now is that this one happened very suddenly, with a depth and severity unseen in 90 years, accompanied by a swift and generous fiscal response.

Many people (though far from all) were made comfortable. They thought their jobs were safe and expected to go back.

That means we haven’t had the kind of pain signals a situation of this magnitude would normally generate.

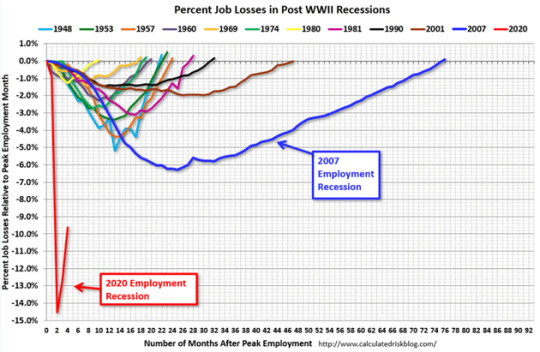

Those signals may be coming, though. Here’s a chart comparing this year’s percentage job losses with prior recessions.

Source: Calculated Risk

That bright red waterfall is where we are right now. It appears to have hit bottom and splashed a bit, but there’s a lot of white water ahead. You can see in the 2007 line how long it took employment to recover after the last recession.

At that pace, all the jobs will be back sometime in 2026. (Not a typo.) To assume the “V” seen above will continue in the same direction means thinking there will be a quick return to normalcy.

Maybe this time is different, since at least some of the layoffs were temporary. The BLS data tries to distinguish between temporary and permanent job losses.

That’s a moving target, though, because employers don’t always know. They furlough people with the intent of bringing them back, but then find conditions don’t allow it. At some point, temporary job losses can turn into permanent ones.

Even when jobs reappear, we still don’t have a good idea of how many furloughed and unemployed workers want to go back, or are even able to.

Some have health concerns, for either themselves or a vulnerable family member.

Others have young children who may or may not go back to school this fall.

And some who are making more from unemployment benefits than they would by working will keep doing so as long as they can.

Take a look at this chart from Philippa Dunne:

Source: TLRanalytics

Unemployment benefits are skyrocketing as a percentage of personal income while wages and salaries are dropping hard.

We will get some more insight this month because Congress will extend, modify, or expire the enhanced unemployment benefits.

One thing we know for sure: An economy with double-digit-percentage unemployment isn’t going to have a V-shaped recovery. It just can’t.

There is every reason to think it will get worse before getting better. And it will get better… but probably not soon.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

1 note

·

View note

Text

As the Economic Cycles Turn

I had a chance to catch up with my friend Neil Howe at my recent Strategic Investment Conference about the “Fourth Turning”—a recurring generational cycles theory that Neil helped to write the book on, quite literally.

In his view, it’s ongoing right now. Specifically, in the cycles of history, we are in a crisis era that’s comparable to the 1930s and 1940s. Neil believes it began in 2007-‘08 and will climax in the coming decade.

Fourth Turnings usually include a war, but these are not all gloom and doom. Neil said it’s possible our current problems will get resolved in a “kinetic” way, as Fourth Turnings tend to spur great thinking and creative problem-solving.

I probed Neil on whether we will see a larger and more intrusive government arise from this period. He thinks absolutely so, but may not intrusively “big” with big, semi-contractual spending commitments like Social Security—a child of the last Fourth Turning.

This period could spawn more such programs because very few people, and clearly most voters, don’t think of them as “intrusive” or big government.

Don’t think of it an entitlement. Or a depression, for that matter.

My friend Felix Zulauf is watching what’s happening in the world with great interest from his hedge fund in Switzerland. He isn’t bullish, but he also doesn’t foresee a Great Depression-like scenario here in the US.

He listed three key differences between then and now.

There was no social welfare in the 1930s. Now transfer payments are as much as 40% of GDP in some countries.

We entered this recession with much larger government deficits than at the bottom of the Great Depression.

The demographic picture is quite different, with low birth rates and/or negative population growth in some places today.

Felix expects to see something more like post-1989 Japan, with essentially no growth for many years and a nationalized bond market. Attempts to increase employment will make the economy less efficient. He also pointed out that, with negative bond yields, many pension funds having to pay out more than they earn.

This means we are redistributing wealth from future generations to current retirees. The result will be a population that, in real terms, gets poorer over time.

Trying to summarize Neil and Felix, or any of the 40 all-star speakers at Mauldin Economics’ recent virtual Strategic Investment Conference, is impossible. These investing, economic and political experts are people whose every word overflows with meaning. You really need to hear them for yourself.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

Let’s Make Sure This Crisis Doesn’t Go to Waste

A stock market crash wasn’t 1929’s only big event. Coca-Cola (KO) launched a new slogan: “The Pause That Refreshes.”

Coke’s marketers sensed the economy was headed down. How do you sell a completely unnecessary beverage to a struggling country? It’s simple, really: You remind consumers that treating themselves is important, too.

Now, in 2020, the entire world is paused. COVID-19 is horrible in more ways than I can count: lost lives, suffering, job destruction, shattered dreams and more.

None of it is refreshing. But the word has other meanings.

For instance, if you are working on a spreadsheet and refresh your screen, you see new, and possibly better, numbers.

Could this crisis, as bad as it is, “refresh” the world and solve some of our problems? Maybe.

Speaking at Mauldin Economics’ first-ever virtual Strategic Investment Conference in May, Eurasia Group and G-Zero Media’s Ian Bremmer said it’s possible.

Long before this pandemic, Ian was saying the world is in a “geopolitical recession.” The old order has been breaking down without a clear replacement, leaving what he calls a “G-Zero World.”

Part of the problem relates to a Milton Friedman quote: “Nothing is so permanent as a temporary government program.”

Think of the global institutions that arose from World War II and its aftermath: NATO, the UN, the World Bank, International Monetary Fund, the EU, etc.

Some have outlived their usefulness. Other need major reforms. But all still exist because over time they developed constituencies that fight hard to preserve them.

The same is true within national governments. In the US, we have institutions like the Federal Reserve, Social Security, Medicare and assorted regulatory agencies.

They do some good things and could do more. But none work as originally intended.

Ian suggested the pandemic might have a silver lining if the failures it exposes let us replace failed institutions with better ones, more suited to current needs.

Which institutions to whom? Take your pick.

The Federal Reserve is trying to control market outcomes. Which means we don’t really have “markets” as such anymore. This has to stop but I see no chance the Fed will change course voluntarily.

The sudden ejection of millions from their jobs exposed huge shortcomings in the US safety net programs. A top-to-bottom overhaul might let them work better and cost less.

Our inability to provide adequate COVID-19 testing and get protective gear to medical workers revealed serious problems. Not just in the healthcare industry, but also the agencies like the CDC and FDA that govern it. The regulatory processes clearly impede progress, and it has been made manifest for all to see.

Across the pond, the EU’s prized openness and solidarity proved less so in a crisis. Members like Italy had to largely fend for themselves. The alliance needs a major overhaul if it is to survive.

Numerous emerging market states are heavily indebted and completely unprepared to handle this crisis in large part because the IMF made them so. That has to change.

Those are just a few things we could “refresh” in the coming months and years. I don’t know if it will happen but, as Rahm Emmanuel famously said, we shouldn’t let a good crisis go to waste.

Heck, this one could still bring positive change.

Just ask any of the 40 economic and investing all-stars who presented at Mauldin Economics’ recent virtual Strategic Investment Conference. We have all the video footage, slides and transcripts in one easy-to-access space. You really need to hear for yourself what’s in store for our post-coronavirus world.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

The Service Sector Still Awaits Its Second Chance

In 1920, 26% of the US population worked in the service sector of the economy. Today it is 86%. At least, it was before coronavirus prevention measures shuttered a large part of our economy.

Now, 30 million people have filed for unemployment in the last few weeks, and potentially 10 million more in the gig economy have lost part or all of their income.

Unlike manufacturing, retailing or agriculture, service businesses can’t hold inventory. They can’t just close for a few weeks and then make up for lost time. There is no second chance to sell that hotel room night, plane seat, restaurant meal, haircut, Uber ride, or cocktail.

Revenue has been vaporized, not deferred. So, having permanently lost weeks or months of revenue while many fixed expenses continued, service businesses are deeply in the red.

There will be no return to business as usual as long as the virus remains a health threat. Service business can’t simply open their doors again. They have to reengineer everything they do. Processes that took years or even decades to design and optimize are now unworkable. Replacing them isn’t going to happen in a few weeks. And making processes efficient enough to match previous profit margins will take even longer.

Restaurants and other service businesses make money by filling a defined number of chairs with a defined number of people who spend a defined amount of money in a defined length of time.

Interrupt any part of that formula, and everything falls apart. That is what these businesses will return to when they’re allowed to reopen.

Everything will be a lot of extra work now. Customers have to feel safe. Governors can lift their lockdown orders, but they can’t make people shop. Nor can they make businesses open.

In parts of the US, restaurants are being allowed to reopen at lower capacity, usually 25% or 50%. They can’t turn a profit that way, even without all the extra costs.

So, perhaps the financially smartest thing they can do is stay closed, and many are. Maybe they will open in a few weeks, if the virus and associated restrictions ease.

Meanwhile, workers stay unemployed and everyone’s spending remains muted.

What will the impact be on the post-vaccine society? At my first-ever virtual Strategic Investment Conference, we have a stellar lineup of experts who will present and take your questions LIVE. It all happens May 11-21. I have designed this conference to be the best roadmap I can possibly imagine for our journey into the future. Learn more, and register to attend from the safety of your home or office, here.

0 notes

Text

What I Am Most Bullish on Right Now

It feels like sentiment about the coronavirus is starting to change. There’s a new sense of hope where there was little just a month ago.

New drug therapies are being announced and dozens of vaccines are in development. There is a high probability one or more will work by the end of the year. Deployment will be difficult, but doable.

This change in sentiment, combined with generous fiscal support and liquidity injections, is giving investor confidence a boost, too. So, we see stocks rising.

There is reason for hope, and we should celebrate that. But we still haven’t overcome all the reasons for caution.

Looking at it not as an investor, but as an entrepreneur and small business owner, I think some are greatly overestimating how fast the economy can recover. Entire industries, no longer viable in their current forms, must now figure out new ways to do business.

I am bullish on the American entrepreneur. Betting against not only the American entrepreneur, but entrepreneurs worldwide in relatively free-market societies, has always been a losing proposition.

They will figure it out; that’s what entrepreneurs do. But they won’t do it overnight, or even in a few months—nor will they take direct paths from here to there. The rules have changed.

As I wrote two weeks ago, we are in the process of repricing the world. Everything will get repriced; it’s a matter of when and how. Will landlords be forced (by the market) to take lower rents from restaurants? Will the cost of our restaurant food go up? Haircuts? A thousand other things we buy, like stocks?

We see this in the latest Barron’s Big Money Poll of 107 top money managers. Asked to forecast the stock market this year, 39% were bullish, 20% bearish, and 41% neutral.

So adding together the bullish and neutral, eight out of 10 money managers see at least some chance of positive equity returns between now and year-end. They are even more confident for 2021, with 82% bullish and only 4% bearish.

The Barron’s panel has tons of bullish quotes, arguing that things will go back to normal and now is the time to buy. Which is the same thing people said in 2007-’08.

My friend Ed Yardeni is similarly bullish, largely due to Federal Reserve actions. He also thinks analysts will probably overshoot their revenue and earnings estimates to the downside, then revise them upward later in a grandly bullish surprise.

As a natural optimist myself, I admire people who show confidence in tough situations. But I also think recovery will take more than a year or two.

I talk to small business owners and corporate leaders all the time, and they all say it will be a long, hard climb out of this hole.

To help you navigate this new world, this month I’m gathering some of the brightest minds to talk geopolitics, technology, specific investment ideas, and so much more. Watch these presentations LIVE during five full days between May 11–21, for four to five hours a day. Ask questions or watch at your leisure from your home or office. You’ll get written transcripts, too. Secure your spot at my virtual Strategic Investment Conference here.

0 notes

Text

3 Things to Watch When the Jet Fuel Runs Out

Main Street needs customers. The Fed, for as much as it is trying to flood the markets with money, can’t create them.

And yet, the jet fuel has succeeded in pushing stock benchmarks and valuations back near their old highs. Clearly, and probably rightly, investors are willing to look past the second- and possibly even third-quarter earnings, which everyone acknowledges will be dismal.

But what happens when earnings are dismal in the fourth quarter?

With the Fed in the mix, I suppose new market highs are possible this year or next, but I can’t imagine it lasting long. The animal spirits that drove well-known names higher are seriously weaker than they were in February, and I don’t foresee them coming back.

Here’s what I do see.

Some businesses, small and large, will do extremely well in this environment. Their earnings will rise and help pull the indexes up. Likewise, we are going to lose more businesses than most currently think. They will have the opposite effect. This is going to be a stock-picker’s market. Index investors, as I have been saying for several years, will get their heads and their 401(k)s handed to them.

The market is looking past the next two quarters. But are investors going to look past the fourth quarter? Even if we get a vaccine by year-end, it will be a miracle if we all get it by the end of 2021’s first quarter. And balance sheets have been destroyed for so many businesses. There will be opportunities for startups everywhere, as seasoned management will need capital.

It is entirely possible that investors simply become disillusioned with looking past the next few quarters’ earnings. At some point, the attitude will change to, “Show me the money!” Then again, who knows what the Fed will do. If the market starts turning down will they start buying stock ETFs like Japan is? Dear gods, I hope not. But right now, there is simply no way to predict what they will do.

I will bet that over 100 companies currently in the S&P 500 will not be there 12 to 15 months from now. The big indexes are composed of the biggest companies. Which means that we are looking at not only a whole new economy, but perhaps an entirely new market landscape.

Just a reminder: Bull markets like this one don’t just retreat to reasonable valuations. They usually overshoot to the downside, just as they did on the upside. The lower bound is probably lower than many “worst-case” scenarios suggest.

That will not be good for Baby Boomers’ retirement plans.

This experience is going to leave deep scars on the economy, and on consumer/investor/business sentiment. This is going to scar a generation just as deeply as the Great Depression scarred our parents and grandparents.

Things we once took for granted—a leisurely restaurant meal, catching a movie, sharing a concert or a ballgame with other fans—are gone now and will come back in a different form.

But they will come back. We’re moving from one world to the next—an Age of Transformation—whether we want to or not.

We are all going to need that roadmap, and I want you on the journey with me. At my first-ever live virtual Strategic Investment Conference this month, we’ll focus on what the economy will look like over the next six months and in a post-vaccine world. You’ll hear from thought leaders who can show you what’s important, where the opportunities are and what to avoid. Learn more here.

0 notes

Text

How the Coronavirus is Already Repricing the World

What will be the longer-term fallout of the coronavirus be on the economy, the markets and society? We’re starting to catch glimpses of it already. And the world looks a lot different than the one we knew.

As my friend Dave Rosenberg, the chief economist and strategist of Rosenberg Research, wrote in a recent client letter …

“We are going to be in for a prolonged period of social distancing and our personal and commercial lives will remain restricted. The focus will be on savings, cash conservation, ensuring adequate essentials on a personal basis, and inventory/working capital on a corporate basis. The government dis-saving via massive deficits will be offset by rising precautionary savings rates in the private sector.”

Economic change begins with individual changes in behavior. People respond to new incentives, and eventually their responses add up.

I have written about the Paradox of Thrift, where individual savings are good but everybody saving actually reduces GDP. After this current crisis/recession, I think Americans’ propensity to save will be much higher. Our spending incentives will be different.

So what are those new spending incentives, and how will they change us?

Most obviously, we see that personal safety isn’t easy or guaranteed. It is no longer enough to drive carefully, take your vitamins, and avoid rough neighborhoods.

The coronavirus threat is invisible and anyone, even the people you love, could be carrying it right now. This will have a deep and long-lasting effect on personal relations and spending patterns.

We are also going to think very differently about the value of some previously well-established things. Right now, crowded concerts or sporting events are simply off-limits. Soon we may allow them with modifications: Wear a mask, stay six feet apart, and so on. But being in a crowd, shoulder-to-shoulder with your fellow fans, is part of the experience. It won’t be the same.

And because the product has changed, the price will likely change, too.

That’s a problem not only for artists and athletes, but also the many people whose jobs revolve around such events. Ditto for restaurants, hotels, many other businesses.

Those will all be repriced, and probably downward.

But right now, the Federal Reserve is spending trillions to make sure companies don’t default. In some cases, that makes sense. But it also calls into question who is bearing the credit risk. Why should bondholders get paid for risk someone else is bearing?

Then again, if we allow the high-yield and leveraged loan market to collapse, we guarantee a deeper recession.

The same is true for stocks.

This month, the U.S. government spent billions bailing out airlines. What should have happened—and did happen in the past—is the airlines go bankrupt and the courts sort out their obligations. Not this time, and maybe not ever again.

If so, there is no reason stock valuations should reflect the risks shareholders aren’t taking.

We don’t know how this will develop, or how quickly. But I think it is far more likely to bring asset price deflation than inflation.

We are going to reprice the world. Probably including your part of it.

That’s why I am planning our first-ever live virtual Strategic Investment Conference in May. We’ll focus on what the economy will look like over the next six months and in a post-vaccine world. You’ll hear from thought leaders who can show you what’s important, where the opportunities are and what to avoid. View my announcement message here.

0 notes

Text

How Soon Can the Coronavirus Economic Chokehold End?

My friend Dave Rosenberg, who practices independently at Rosenberg Research, notes that when and how to reopen the US economy is a tough call—one that depends on many medical variables.

“If I had to guess, we will be seeing a partial reopening in some areas beginning in May. I sense the one metric that is really important here is healthcare capacity (hospital beds, ICUs, ventilators).”

I believe easing the business and movement restrictions will depend highly on local conditions. The viral outbreaks spread in ways we don’t fully understand. Keeping so many people out of circulation seems to have helped, but these closures aren’t sustainable indefinitely.

Top priority goes to keeping the healthcare system ready for the worst; Dave and I agree on that. We can’t allow more of these “overwhelm” situations like Italy and New York.

Rather, we need facilities, equipment, supplies, and staff available to treat a (still-high) number of coronavirus patients … plus all the other medical needs that have been sidelined.

Some have suggested we just isolate the most vulnerable people: those over age 60, and/or with immune system, lung or other problems. That would probably help, but wouldn’t be simple.

You’re still talking about a big part of the population, plus the younger caregivers who would come in contact with them, plus the caregivers’ families. That’s not sustainable for long, either.

Dr. Michael Roizen of the Cleveland Clinic is helping prepare a paper for Ohio and other states about how to think about reopening their states. He includes this chart about death rates in Ohio; clearly the risk of death rises dramatically with age.

But that changes if you factor in other health issues. High blood pressure, smoking, being overweight, lack of exercise, all contribute to increased morbidity. So you can be younger and still be in a high-risk category because of your health.

The US still needs to sharply ramp up testing before we can ease the restrictions. It is getting better, and some private labs even report excess capacity now that they’ve worked through the initial backlog. But we need much more to be confident, probably millions of tests a day.

We just have to bite the bullet and make it happen.

With the caveat that local schedules will vary, I think Dave is right that we can begin reopening in May. But note how carefully Dave said it (my emphasis):

“A partial reopening in some areas beginning in May.”

We are not all going to emerge from our holes, blink at the sunlight, and proceed merrily into spring. I expect a drawn-out process, possibly interrupted in some places if new cases begin growing again.

Some governors are talking about allowing restaurants to open at 50% capacity. How’s that going to work for their cash flow? Not to mention jobs?

Governments can’t simply order the economy reopened. Consumers and businesses have to agree, and all will make their own choices. Like everything else, it will be a cost-benefit analysis.

In the nearer term, it’s going to look quite different. Masks will be mandatory some places and socially expected in others. Most people will stay close to home. Even if you’re willing to get on a plane or train, you’ll risk being caught in someone else’s outbreak and unable to get home.

Is the benefit of going to that restaurant worth the risks of going out in public, in proximity to possibly infected strangers? Maybe so, but fewer will want to as long as this virus is still a threat.

Life will be nothing like the “normal” we knew just a few months ago until we have an effective vaccine and most people are inoculated. That’s at least eight months away, maybe longer.

We aren’t going to just pick up where we left off. Social distancing is incompatible with the kind of economy we have always known.

As long as it persists, the old economy is gone.

What will the economy look like over the next six months and in a post-vaccine world? I’m gathering thought leaders at my first-ever live virtual conference who can help you separate the signal from noise. It takes place over five days between May 11 and 21. Learn more here.

0 notes

Text

Bending the Inflation Curve

Our responses to the coronavirus threat, necessary though they may be, are creating massive supply and demand shocks, the rapidity of which is like nothing seen in centuries, if ever.

The Federal Reserve and other central banks are doing unprecedented things. Some think inflation will be the result. While that may happen eventually, I believe we will first go through the most massive deflationary shock of all time.

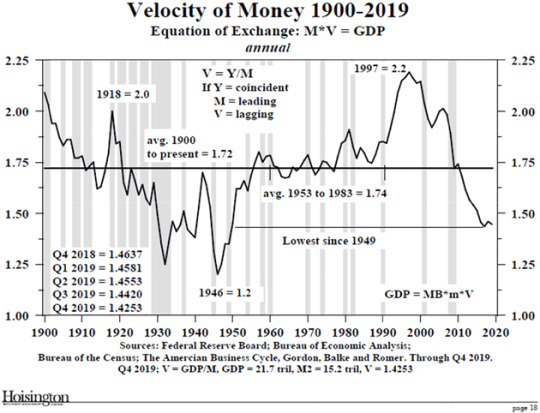

Milton Friedman famously said, “… inflation is always and everywhere a monetary phenomenon.” During the timeframe in which he and his colleague Anna Schwartz did their famous study, there was clearly a correlation between money supply and inflation. What is not often noted is that the velocity of money (i.e., the rate at which money changes hands) was stable during that time.

When the velocity of money is falling, monetary policy which would otherwise cause inflation doesn’t seem to do so.

Here is Lacy Hunt’s latest velocity chart. You have to go back to 1949 to find a time when it was lower than today, and it was actually rising rapidly off the postwar lows. This was before the coronavirus shutdowns. Let me crawl out on a limb and suggest that the velocity of money is now going to drop even further. Deflation is not your friend.

Source: Hoisington Investment Management

Let me offer Mauldin’s corollary to Milton Friedman’s famous statement:

Inflation Is Always and Everywhere a Function of Demand

We have simply destroyed demand by locking down the country. And it should be clear that we cannot turn a switch to bring it back. How soon will we feel like going back into large crowds, restaurants, movie theaters, sporting events, hotels, vacation destinations, and all the other areas where we congregate as human beings? Certainly, some of the economy will start looking normal. But how many workers will it need?

How have our buying patterns changed? We are learning that we can work from home. Zoom and other services have had their weaknesses exposed, but they will improve. This is going to make working from home easier and more common.

Multiplied across thousands of large companies, that means the demand for office space will drop, which means prices for office space will drop. That is deflation, gentle reader. Even if the Federal Reserve decides to buy office space (which it won’t), that is not going to increase demand. Ditto for 100 other industries. Think about restaurant buildings. Builders and tenants go to tremendous expense to create the kitchens, which means if a restaurant goes out of business, the property owner typically has to find another restaurant. How likely is that to happen today?

At some point supply and demand will balance, but I don’t think it will be in three months. Three years? Maybe. Lacy Hunt thinks it will be a few years longer. So do some of my other economically brilliant friends.

But whether it is three months or three quarters or 3+ years, it will happen. At that point we have the potential for an inflationary episode if the Federal Reserve keeps stimulating and the government keeps running massive deficits. If they act responsibly, inflation could rise to the 2 to 3% level and hopefully not higher. If they don’t act responsibly? All bets are off.

But understand this: Demand has to come back, and in size, in order to spark inflation. Yet in this situation people will want to save, perhaps more than they ever have in their lives. Purchases are going to be put off if they can be.

Now, many economists would not talk about supply and demand so much as about the “output gap.” As businesses go away, potential output also drops. How will that take? No one knows.

We have never seen anything like this. Nor have we seen the last of it, and we probably won’t until there’s a vaccine.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

The Post-Virus New Normal

I don’t think anyone believes we will go to back to anything like January 2020 normalcy anytime soon. We have no idea, even if restaurants and everything open, what shopping patterns will look like.

Are we learning to live on less in our isolation? Seeing your 401(k) become a 201(k) may postpone a car-buying decision or two.

My daughter (see below) works for a cheerleading gymnastics company. Nationwide this is a multi-hundred-million-dollar industry. Will they just open back up and expect all the girls go back on day one? Will their parents be able to afford it? We’re talking many tens of thousands of jobs. Personal trainers? Many jobs will be under pressure.

There are 47,000 retail stores just in the U.S. We already knew there were too many as closings were becoming more frequent. My friend Professor Michael Pettis in Beijing (who has lived there for 20+ years) has been documenting the return of life in Beijing. He sees people on the streets but not many in the shops, except where the young go to hang out rather than buy. Will that be the case in America and Europe?

Speaking of stores, many have already stopped paying their rent. Cheesecake Factory for one. Ryanair, EasyJet and British Airways have stopped paying most rents and vendors. Group 1 Automotive reports a 50% to 70% decline in March sales across its 428 dealerships in the U.S. and the UK. The company has laid off 3,000 U.S. employees and 2,800 UK employees.

How fast do we start traveling and vacationing again? That matters to hotels, airlines and their employees. I believe this experience will emotionally scar a generation. It is going to make the political divide even worse, especially along wealth and income lines.

The U.S. and other governments can artificially prop up GDP, but for how long? At some point, it really does start affecting the currency’s buying power. We just don’t know what that point is in the developed world.

The Federal Reserve has properly opened swap lines with many emerging markets, as they need dollars in order to pay bills and buy necessary supplies. But many of their citizens are going to want a “safer” fiat currency.

I think many emerging markets will enact capital controls sooner rather than later. That will really screw with their markets. But what else can they do?

Next month’s earnings season will be truly abysmal. Close to half of S&P 500 profits come from outside the U.S. Every business is going to have a new valuation.

It is just my guess, but I doubt we have seen the stock market bottom yet.

Let me close with some good news.

Even though the number of deaths is rising in the U.S. and the developed markets every day, the rate of increase is slowing in many places. I think we will see a giant collective sigh of relief when the infection and death rates are not only dropping but the drop is accelerating.

That will be the time to think about gradually getting back into the markets. Meanwhile, maintain your watchlist of things you want to buy at cheaper prices.

Let me leave you with this link to a letter from F. Scott Fitzgerald during his quarantine during the Spanish flu virus. It is a short read but poignant, except for these humorous few sentences:

“The officials have alerted us to ensure we have a month’s worth of necessities. Zelda and I have stocked up on red wine, whiskey, rum, vermouth, absinthe, white wine, sherry, gin, and lord, if we need it, brandy. Please pray for us.”

This quarantine is so very real, and some are rightfully very worried for their future. Will their jobs even exist? Others are seeing their work hours rise due to the “essential” nature of their jobs, but how long will that last?

I do know that we will adjust and that we will all Muddle Through. I will be with here with you.

We are all being forced to adjust to a New Normal. And one day -- although it seems far away -- it will become a Post-Virus New Normal. It will be one where friends and family will still be as important as ever.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

1 note

·

View note

Text

Federal Budget Deficits: To $30T and Beyond

In my decade forecast, I projected that in the next recession that the deficit would climb to over $2 trillion. Clearly, that demonstrates I am an optimist. Here’s a chart I shared back in January.

Between reduced tax revenues and increased spending, I now expect this year’s deficit will be at least $4 trillion.

I will bet you a dollar to 40 doughnuts that we will see at least another $1 trillion emergency spending bill to be spent in the third quarter. My logic is as follows.

The following equation is used to calculate the GDP: GDP = C + I + G + (X – M) or GDP = private consumption + gross investment + government investment + government spending + (exports – imports).

This transforms the money-value measure, nominal GDP, into an index for quantity of total output.

I wrote recently about the long-ago political decision to include government spending in the GDP numbers. U.S. GDP is roughly $20 trillion a year (using numbers that are easy to divide). That means $5 trillion per quarter.

If the economy falls 20% in the third quarter (not a prediction, but work with me) adding an additional $1 trillion worth of government spending will restore the GDP equation.

The first estimate of that number will come out in late October, shortly before the Nov. 3 election. Both parties in Congress will want to see it positive. Care to bet we don’t see another stimulus package?

We could have 2020 and 2021 deficits of a combined $6 trillion-plus. Add off-budget spending, and we should see $30 trillion total national debt by the end of 2021.

I naïvely projected total national debt to be $39 trillion by 2030. See, I keep telling you I’m an optimist.

We will be in that $40 trillion range somewhere around 2026-‘27.

We are experiencing a practice round for The Great Reset. Sometime late this year or early next, we need to look at what happened and then think what it will look like in the late 2020s.

A number of factors will all converge to give us a true Fourth Turning generational crisis, part of which will be The Great Reset.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes

Text

The Unintended Consequences of Doing Good

The Federal Reserve is buying mortgage-backed securities with the best of intentions. But there are unintended consequences.

Last week, I had a truly horrifying phone call with good friend and real estate expert, Barry Habib. He knows the mortgage business inside and out and he’s very concerned right now.

Briefly, the Federal Reserve and other bank regulators have relaxed some rules so lenders can be more patient with people who fall behind on their loan payments. It’s called “forbearance.” I think we all agree that’s necessary under the circumstances.

The problem is, they didn’t grant forbearance to mortgage servicers. That is, the companies who collect payments, handle tax escrows, etc. They also take risk as mortgages wind through the system from origination to the investors who actually own them.

The servicer must make payments to Fannie Mae, Freddie Mac, and especially Ginnie Mae even if the mortgage is delinquent.

Normally the risk is small. Suddenly it is not.

Mortgage service providers are the fan belt of the economic engine. It is a $3 part (or, it was when I was a kid and installed them myself), but the entire engine freezes up if it breaks.

The mortgage belt has snapped, and we are weeks away from the entire housing engine collapsing.

Late last week, we learned that Treasury Secretary Steven Mnuchin is aware of this “minor issue” and is trying to decide what to do.

He needs to decide quickly.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

0 notes