Last Seen Blogs

definitelyincorrectffbequotes

Paladia is a wacky place they could have said this before

eliotquillon

—good for getting out of locked rooms

thewearhouse

THE WEARHOUSE

fem-jerma

scroll… scroll….

bgwhitephoto

Beaniedub

Text

Ford to slash thousands of jobs in Europe as part of a turnaround plan

© Alan Diaz/AP Ford said on Thursday it will cut thousands of jobs, exit unprofitable markets and discontinue loss-making vehicle lines as part of a turnaround effort aimed at achieving a 6 percent operating margin in Europe.

The carmaker is under pressure to restructure its European operations after archrival General Motors raised profits by selling its European Opel and Vauxhall brand to France's Peugeot SA.

Ford said it will seek to exit the multivan segment, stop manufacturing automatic transmissions in Bordeaux in August, review its operations in Russia, and combine the headquarters of Ford U.K. and Ford Credit to a site in Dunton, Essex.

"We are taking decisive action to transform the Ford business in Europe," Steven Armstrong, group vice president, Europe, Middle East and Africa, said in a statement.

Ford's announcement on layoffs came as Britain's biggest carmaker Jaguar Land Rover (JLR) is also set to announce "substantial" job cuts in the thousands, a source told Reuters.

Ford Europe, which currently employs 53,000 people, has struggled to turn a profit, reporting a 245 million euro ($282 million) loss before interest and taxes in the third quarter, equivalent to a negative 3.3 percent EBIT margin.

Armstrong declined to quantify the scale of job cuts, pending negotiations with labor leaders, but said staff reductions would run into the "thousands."

"Ford aims to achieve the labor cost reductions as far as possible through voluntary employee separations in Europe," the carmaker said in a statement on Thursday.

Armstrong said the company is in negotiations with worker representatives about potential job cuts at its Saarlouis plant in Germany, where 6,190 staff assemble cars, as the carmaker considers discontinuing production of its Ford C-Max model.

"We will migrate out of the MPV segment," Armstrong said, referring to the family vans segment. Ford will focus instead on developing more profitable "crossover" vehicles.

The company is unlikely to develop next-generation diesel engines for smaller vehicles, Armstrong said, explaining that customers have been abandoning the segment more aggressively than anticipated. ($1 = 0.8678 euros) (Reporting by Edward Taylor; Editing by Christoph Steitz and Susan Fenton)

Source: http://www.msn.com/en-us/money/companies/ford-europe-to-slash-thousands-of-jobs-in-turnaround-plan/ar-BBS3wW9?srcref=rss

0 notes

Text

Michael Hudson: The Shape of the Venezuelan Economy, from Chavez to Maduro and Beyond

Interview conducted by The Saker with Michael Hudson, a research professor of Economics at University of Missouri, Kansas City, and a research associate at the Levy Economics Institute of Bard College. His latest book is J is for Junk Economics. Cross-posted from Hudson’s site.

1. Could you summarize the state of Venezuela’s economy when Chavez came to power?

Venezuela was an oil monoculture. Its export revenue was spent largely on importing food and other necessities that it could have produced at home. Its trade was largely with the United States. So despite its oil wealth, it ran up foreign debt.

From the outset, U.S. oil companies have feared that Venezuela might someday use its oil revenues to benefit its overall population instead of letting the U.S. oil industry and its local comprador aristocracy siphon off its wealth. So the oil industry – backed by U.S. diplomacy – held Venezuela hostage in two ways.

First of all, oil refineries were not built in Venezuela, but in Trinidad and in the southern U.S. Gulf Coast states. This enabled U.S. oil companies – or the U.S. Government – to leave Venezuela without a means of “going it alone” and pursuing an independent policy with its oil, as it needed to have this oil refined. It doesn’t help to have oil reserves if you are unable to get this oil refined so as to be usable.

Second, Venezuela’s central bankers were persuaded to pledge their oil reserves and all assets of the state oil sector (including Citgo) as collateral for its foreign debt. This meant that if Venezuela defaulted (or was forced into default by U.S. banks refusing to make timely payment on its foreign debt), bondholders and U.S. oil majors would be in a legal position to take possession of Venezuelan oil assets.

These pro-U.S. policies made Venezuela a typically polarized Latin American oligarchy. Despite being nominally rich in oil revenue, its wealth was concentrated in the hands of a pro-U.S. oligarchy that let its domestic development be steered by the World Bank and IMF. The indigenous population, especially its rural racial minority as well as the urban underclass, was excluded from sharing in the country’s oil wealth. The oligarchy’s arrogant refusal to share the wealth, or even to make Venezuela self-sufficient in essentials, made the election of Hugo Chavez a natural outcome.

2. Could you outline the various reforms and changes introduced by Hugo Chavez? What did he do right, and what did he do wrong?

Chavez sought to restore a mixed economy to Venezuela, using its government revenue – mainly from oil, of course – to develop infrastructure and domestic spending on health care, education, employment to raise living standards and productivity for his electoral constituency.

What he was unable to do was to clean up the embezzlement and built-in rake-off of income from the oil sector. And he was unable to stem the capital flight of the oligarchy, taking its wealth and moving it abroad – while running away themselves.

This was not “wrong”. It merely takes a long time to change an economy’s disruption – while the U.S. is using sanctions and “dirty tricks” to stop that process.

3. What are, in your opinion, the causes of the current economic crisis in Venezuela – is it primarily due to mistakes by Chavez and Maduro or is the main cause US sabotage, subversion and sanctions?

There is no way that’s Chavez and Maduro could have pursued a pro-Venezuelan policy aimed at achieving economic independence without inciting fury, subversion and sanctions from the United States. American foreign policy remains as focused on oil as it was when it invaded Iraq under Dick Cheney’s regime. U.S. policy is to treat Venezuela as an extension of the U.S. economy, running a trade surplus in oil to spend in the United States or transfer its savings to U.S. banks.

By imposing sanctions that prevent Venezuela from gaining access to its U.S. bank deposits and the assets of its state-owned Citco, the United States is making it impossible for Venezuela to pay its foreign debt. This is forcing it into default, which U.S. diplomats hope to use as an excuse to foreclose on Venezuela’s oil resources and seize its foreign assets much as Paul Singer’s hedge fund sought to do with Argentina’s foreign assets.

Just as U.S. policy under Kissinger was to make Chile’s “economy scream,” so the U.S. is following the same path against Venezuela. It is using that country as a “demonstration effect” to warn other countries not to act in their self-interest in any way that prevents their economic surplus from being siphoned off by U.S. investors.

4. What in your opinion should Maduro do next (assuming he stays in power and the USA does not overthrow him) to rescue the Venezuelan economy?

I cannot think of anything that President Maduro can do that he is not doing. At best, he can seek foreign support – and demonstrate to the world the need for an alternative international financial and economic system.

He already has begun to do this by trying to withdraw Venezuela’s gold from the Bank of England and Federal Reserve. This is turning into “asymmetrical warfare,” threatening what to de-sanctify the dollar standard in international finance. The refusal of England and the United States to grant an elected government control of its foreign assets demonstrates to the entire world that U.S. diplomats and courts alone can and will control foreign countries as an extension of U.S. nationalism.

The price of the U.S. economic attack on Venezuela is thus to fracture the global monetary system. Maduro’s defensive move is showing other countries the need to protect themselves from becoming “another Venezuela” by finding a new safe haven and paying agent for their gold, foreign exchange reserves and foreign debt financing, away from the dollar, sterling and euro areas.

The only way that Maduro can fight successfully is on the institutional level, upping the ante to move “outside the box.” His plan – and of course it is a longer-term plan – is to help catalyze a new international economic order independent of the U.S. dollar standard. It will work in the short run only if the United States believes that it can emerge from this fight as an honest financial broker, honest banking system and supporter of democratically elected regimes. The Trump administration is destroying illusion more thoroughly than any anti-imperialist critic or economic rival could do!

Over the longer run, Maduro also must develop Venezuelan agriculture, along much the same lines that the United States protected and developed its agriculture under the New Deal legislation of the 1930s – rural extension services, rural credit, seed advice, state marketing organizations for crop purchase and supply of mechanization, and the same kind of price supports that the United States has long used to subsidize domestic farm investment to increase productivity.

What about the plan to introduce a oil-based crypto currency? Will that be an effective alternative to the dying Venezuelan Bolivar?

Only a national government can issue a currency. A “crypto” currency tied to the price of oil would become a hedging vehicle, prone to manipulation and price swings by forward sellers and buyers. A national currency must be based on the ability to tax, and Venezuela’s main tax source is oil revenue, which is being blocked from the United States. So Venezuela’s position is like that of the German mark coming out of its hyperinflation of the early 1920s. The only solution involves balance-of-payments support. It looks like the only such support will come from outside the dollar sphere.

The solution to any hyperinflation must be negotiated diplomatically and be supported by other governments. My history of international trade and financial theory, Trade, Development and Foreign Debt, describes the German reparations problem and how its hyperinflation was solved by the Rentenmark.

Venezuela’s economic-rent tax would fall on oil, and luxury real estate sites, as well as monopoly prices, and on high incomes (mainly financial and monopoly income). This requires a logic to frame such tax and monetary policy. I have tried to explain how to achieve monetary and hence political independence for the past half-century. China is applying such policy most effectively. It is able to do so because it is a large and self-sufficient economy in essentials, running a large enough export surplus to pay for its food imports. Venezuela is in no such position. That is why it is looking to China for support at this time.

5. How much assistance do China, Russia and Iran provide and how much can they do to help? Do you think that these three countries together can help counter-act US sabotage, subversion and sanctions?

None of these countries have a current capacity to refine Venezuelan oil. This makes it difficult for them to take payment in Venezuelan oil. Only a long-term supply contract (paid for in advance) would be workable. And even in that case, what would China and Russia do if the United States simply grabbed their property in Venezuela, or refused to let Russia’s oil company take possession of Citco? In that case, the only response would be to seize U.S. investments in their own country as compensation.

At least China and Russia can provide an alternative bank clearing mechanism to SWIFT, so that Venezuela can bypass the U.S. financial system and keep its assets from being grabbed at will by U.S. authorities or bondholders. And of course, they can provide safe-keeping for however much of Venezuela’s gold it can get back from New York and London.

Looking ahead, therefore, China, Russia, Iran and other countries need to set up a new international court to adjudicate the coming diplomatic crisis and its financial and military consequences. Such a court – and its associated international bank as an alternative to the U.S.-controlled IMF and World Bank – needs a clear ideology to frame a set of principles of nationhood and international rights with power to implement and enforce its judgments.

This would confront U.S. financial strategists with a choice: if they continue to treat the IMF, World Bank, ITO and NATO as extensions of increasingly aggressive U.S. foreign policy, they will risk isolating the United States. Europe will have to choose whether to remain a U.S. economic and military satellite, or to throw in its lot with Eurasia.

However, Daniel Yergin reports in the Wall Street Journal (Feb. 7) that China is trying to hedge its bets by opening a back-door negotiation with Guaido’s group, apparently to get the same deal that it has negotiated with Maduro’s government. But any such deal seems unlikely to be honored in practice, given U.S. animosity toward China and Guaido’s total reliance on U.S. covert support.

6. Venezuela kept a lot of its gold in the UK and money in the USA. How could Chavez and Maduro trust these countries or did they not have another choice? Are there viable alternatives to New York and London or are they still the “only game in town” for the world’s central banks?

There was never real trust in the Bank of England or Federal Reserve, but it seemed unthinkable that they would refuse to permit an official depositor from withdrawing its own gold. The usual motto is “Trust but verify.” But the unwillingness (or inability) of the Bank of England to verify means that the formerly unthinkable has now arrived: Have these central banks sold this gold forward in the post-London Gold Pool and its successor commodity markets in their attempt to keep down the price so as to maintain the appearance of a solvent U.S. dollar standard?

Paul Craig Roberts has described how this system works. There are forward markets for currencies, stocks and bonds. The Federal Reserve can offer to buy a stock in three months at, say, 10% over the current price. Speculators will by the stock, bidding up the price, so as to take advantage of “the market’s” promise to buy the stock. So by the time three months have passed, the price will have risen. That is largely how the U.S. “Plunge Protection Team” has supported the U.S. stock market.

The system works in reverse to hold down gold prices. The central banks holding gold can get together and offer to sell gold at a low price in three months. “The market” will realize that with low-priced gold being sold, there’s no point in buying more gold and bidding its price up. So the forward-settlement market shapes today’s market.

The question is, have gold buyers (such as the Russian and Chinese government) bought so much gold that the U.S. Fed and the Bank of England have actually had to “make good” on their forward sales, and steadily depleted their gold? In this case, they would have been “living for the moment,” keeping down gold prices for as long as they could, knowing that once the world returns to the pre-1971 gold-exchange standard for intergovernmental balance-of-payments deficits, the U.S. will run out of gold and be unable to maintain its overseas military spending (not to mention its trade deficit and foreign disinvestment in the U.S. stock and bond markets). My book on Super-Imperialism explains why running out of gold forced the Vietnam War to an end. The same logic would apply today to America’s vast network of military bases throughout the world.

Refusal of England and the U.S. to pay Venezuela means that other countries means that foreign official gold reserves can be held hostage to U.S. foreign policy, and even to judgments by U.S. courts to award this gold to foreign creditors or to whoever might bring a lawsuit under U.S. law against these countries.

This hostage-taking now makes it urgent for other countries to develop a viable alternative, especially as the world de-dedollarizes and a gold-exchange standard remains the only way of constraining the military-induced balance of payments deficit of the United States or any other country mounting a military attack. A military empire is very expensive – and gold is a “peaceful” constraint on military-induced payments deficits. (I spell out the details in my Super Imperialism: The Economic Strategy of American Empire (1972), updated in German as Finanzimperium (2017).

The U.S. has overplayed its hand in destroying the foundation of the dollar-centered global financial order. That order has enabled the United States to be “the exceptional nation” able to run balance-of-payments deficits and foreign debt that it has no intention (or ability) to pay, claiming that the dollars thrown off by its foreign military spending “supply” other countries with their central bank reserves (held in the form of loans to the U.S. Treasury – Treasury bonds and bills – to finance the U.S. budget deficit and its military spending, as well as the largely military U.S. balance-of-payments deficit.

Given the fact that the EU is acting as a branch of NATO and the U.S. banking system, that alternative would have to be associated with the Shanghai Cooperation Organization, and the gold would have to be kept in Russia and/or China.

7. What can other Latin American countries such as Bolivia, Nicaragua, Cuba and, maybe, Uruguay and Mexico do to help Venezuela?

The best thing neighboring Latin American countries can do is to join in creating a vehicle to promote de-dollarization and, with it, an international institution to oversee the writedown of debts that are beyond the ability of countries to pay without imposing austerity and thereby destroying their economies.

An alternative also is needed to the World Bank that would make loans in domestic currency, above all to subsidize investment in domestic food production so as to protect the economy against foreign food-sanctions – the equivalent of a military siege to force surrender by imposing famine conditions. This World Bank for Economic Acceleration would put the development of self-reliance for its members first, instead of promoting export competition while loading borrowers down with foreign debt that would make them prone to the kind of financial blackmail that Venezuela is experiencing.

Being a Roman Catholic country, Venezuela might ask for papal support for a debt write-down and an international institution to oversee the ability to pay by debtor countries without imposing austerity, emigration, depopulation and forced privatization of the public domain.

Two international principles are needed. First, no country should be obliged to pay foreign debt in a currency (such as the dollar or its satellites) whose banking system acts to prevents payment.

Second, no country should be obliged to pay foreign debt at the price of losing its domestic autonomy as a state: the right to determine its own foreign policy, to tax and to create its own money, and to be free of having to privatize its public assets to pay foreign creditors. Any such debt is a “bad loan” reflecting the creditor’s own irresponsibility or, even worse, pernicious asset grab in a foreclosure that was the whole point of the loan.

This entry was posted in Guest Post on February 8, 2019 by Lambert Strether.

About Lambert Strether

Readers, I have had a correspondent characterize my views as realistic cynical. Let me briefly explain them. I believe in universal programs that provide concrete material benefits, especially to the working class. Medicare for All is the prime example, but tuition-free college and a Post Office Bank also fall under this heading. So do a Jobs Guarantee and a Debt Jubilee. Clearly, neither liberal Democrats nor conservative Republicans can deliver on such programs, because the two are different flavors of neoliberalism (“Because markets”). I don’t much care about the “ism” that delivers the benefits, although whichever one does have to put common humanity first, as opposed to markets. Could be a second FDR saving capitalism, democratic socialism leashing and collaring it, or communism razing it. I don’t much care, as long as the benefits are delivered. To me, the key issue — and this is why Medicare for All is always first with me — is the tens of thousands of excess “deaths from despair,” as described by the Case-Deaton study, and other recent studies. That enormous body count makes Medicare for All, at the very least, a moral and strategic imperative. And that level of suffering and organic damage makes the concerns of identity politics — even the worthy fight to help the refugees Bush, Obama, and Clinton’s wars created — bright shiny objects by comparison. Hence my frustration with the news flow — currently in my view the swirling intersection of two, separate Shock Doctrine campaigns, one by the Administration, and the other by out-of-power liberals and their allies in the State and in the press — a news flow that constantly forces me to focus on matters that I regard as of secondary importance to the excess deaths. What kind of political economy is it that halts or even reverses the increases in life expectancy that civilized societies have achieved? I am also very hopeful that the continuing destruction of both party establishments will open the space for voices supporting programs similar to those I have listed; let’s call such voices “the left.” Volatility creates opportunity, especially if the Democrat establishment, which puts markets first and opposes all such programs, isn’t allowed to get back into the saddle. Eyes on the prize! I love the tactical level, and secretly love even the horse race, since I’ve been blogging about it daily for fourteen years, but everything I write has this perspective at the back of it.

Post navigation

← PR Powerhouse to Democrats: Don’t Be Mean to Starbucks Cisco Joins Other Tech Giants in Calling for a Federal Privacy Law →

Source: https://www.nakedcapitalism.com/2019/02/michael-hudson-shape-venezuelan-economy-chavez-maduro-beyond.html

0 notes

Text

Wall Street dips with Apple, other tech shares

NEW YORK (Reuters) - U.S. stocks edged lower on Wednesday, weighed down by a decline in Apple as it unveiled larger iPhones but made just minor changes to its offerings, and other technology shares.

Traders work on the floor of the New York Stock Exchange (NYSE) in New York, U.S., September 12, 2018. REUTERS/Brendan McDermid

Apple (AAPL.O) shares were down 1.4 percent. The company also unveiled health-oriented watches based on the design of current models.

Shares of fitness device rival Fitbit Inc (FIT.N) fell 5.9 while shares of Garmin Ltd (GRMN.O) lost some earlier gains and were flat after the launch of Apple’s latest Apple Watch.

“You had the (Apple) announcement, and the typical trader reaction was there wasn’t anything that wasn’t already rumored or expected from the announcement, so some of yesterday’s gains are being given back today,” said Michael James, managing director of equity trading at Wedbush Securities in Los Angeles.

Traders work on the floor of the New York Stock Exchange (NYSE) in New York, U.S., September 12, 2018. REUTERS/Brendan McDermid

The S&P technology index .SPLRCT was down about 0.7 percent, reversing Tuesday’s gains, with fears of further deregulation also hurting Apple as well as social media names.

Six major Web and Internet service companies, including Apple, are to detail their consumer data privacy practices to a U.S. Senate panel on Sept. 26, raising the specter of the possibility of stricter regulation.

The Dow was essentially flat as a report of fresh U.S.-China trade talks helped some industrial companies.

At 2:48PM ET, the Dow Jones Industrial Average .DJI fell 6.24 points, or 0.02 percent, to 25,964.82, the S&P 500 .SPX lost 1.84 points, or 0.06 percent, to 2,886.05 and the Nasdaq Composite .IXIC dropped 37.27 points, or 0.47 percent, to 7,935.21.

“Some of the industrial names, Boeing being the most notable, are what’s leading the outperformance of the Dow,” James said. Boeing (BA.N) shares were up 2.1 percent.

The Wall Street Journal reported that Washington has proposed a new round of trade talks with Beijing before the Trump administration implements additional tariffs on Chinese imports.

Among the six companies to testify later this month, Twitter (TWTR.N) shares were down 4 percent, while Alphabet (GOOGL.O) was down 1.9 percent and Amazon.com (AMZN.O) was down down 0.4 percent.

Facebook (FB.O), not among the companies to testify, was down 2.4 percent.

The Philadelphia Semiconductor index .SOX was down 1.7 percent after Goldman Sachs became the latest brokerage to warn of lower prices for memory chips due to an oversupply of DRAM and NAND chips.

Micron (MU.O) slid 5.2 percent, while Applied Materials (AMAT.O) was down 2.3 percent.

Advancing issues outnumbered declining ones on the NYSE by a 1.31-to-1 ratio; on Nasdaq, a 1.24-to-1 ratio favored decliners.

The S&P 500 posted 29 new 52-week highs and 6 new lows; the Nasdaq Composite recorded 67 new highs and 82 new lows.

Additional reporting by Shreyashi Sanyal in Bengaluru; Editing by Shounak Dasgupta and Cynthia Osterman

Source: https://www.reuters.com/article/us-usa-stocks/wall-street-dips-with-apple-other-tech-shares-idUSKCN1LS1UI?feedType=RSS&feedName=businessNews

0 notes

Text

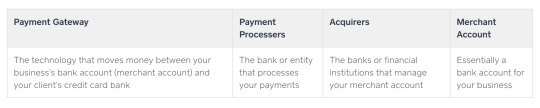

Payment Processor Showdown: Stripe vs. PayPal

Online business all starts with a simple transaction.

Back in the day, in order to complete that transaction, you needed a merchant account—a special bank account that allows you to accept credit card payments—and loads of cumbersome equipment. Today, all you need is a standard checking account and an online service that accepts payments and transfers them to your bank account. Those online services are called payment processors or payment gateways.

Image via Square

Here, we're going to examine two of the most popular payment processor options out there: Stripe and PayPal. Both have distinct advantages and disadvantages, so let's see how they stack up.

Common Features and What We Looked For

PayPal and Stripe each carry unique benefits and challenges. How hard is it to set up for your website? Can you take payments in person? What about using your mobile phone to accept payments? What if you have to type in a credit card number by hand? Is it secure? These are all questions you should be asking before kicking off the decision-making process.

Here are the 10 factors we considered in our showdown. Click on the section that matters most to your business, or jump to the end to see our complete comparison table.

Cost

Stripe has a slight edge on international orders

Stripe and PayPal both allow you to start with no monthly fees. That means that if you aren't selling anything, then you aren't paying anything. This is hugely important for micro-businesses that might not be able to foot even a tiny monthly bill for a payment processor.

They also both have similar pricing structures beyond that:

Sales within the U.S. for both processors are 2.9 percent per transaction plus $0.30. So, if you made a sale for $100, you'd pay $3.20 to Stripe or PayPal. This likely isn't a coincidence and demonstrates just how competitive the two companies are with each other.

For tiny transactions, these fees are quite expensive. That means there's some effort needed on the business owner's part to hit the sweet spot where you're charging enough to outpace fees without running off a customer.

For international sales, the transaction fee goes up to 4.4 percent for PayPal but only 3.9 percent for Stripe, which gives Stripe an advantage if you're doing a lot of international business. And one other note: If you use the PayPal Here card reader from your phone, you'll get away with a 2.7 percent transaction cost, which is a slight advantage over online sales.

Bottom line: The pricing is pretty similar, so this isn't a make-or-break category.

For complete pricing, see PayPal's and Stripe's pricing pages.

Transactions

PayPal is easier unless you use a third-party shopping cart

If you're selling a product or service online, you need at least two pieces to make it work:

The payment processor

A shopping cart application

To get that shopping cart application, you have a couple options. First, you could integrate with a third-party service; e.g., the website builder you used to make your website. Stripe and PayPal both integrate with all the big eCommerce website builders like Shopify, WooCommerce, BigCommerce, Wix, and Squarespace. Sometimes it's as simple as logging in to both accounts, and other times you need to get an API key from Stripe or PayPal. But either way, If you go that route, it's equally as easy to connect either payment processor with whatever shopping cart you use.

Not familiar with APIs? They're what allow companies to link their systems together. You don't need to be an API expert in order to use Stripe and PayPal, but if you want to learn more, take a look at our introduction to APIs.

But if you've built your own website from scratch and you want to embed the shopping cart using only PayPal or Stripe, that's where PayPal starts to pull into the lead. PayPal offers a shopping cart solution that you use on any website where you can paste HTML code. Just click on the Business Setup link from your dashboard and choose "On your website." Then follow the prompts to get a block of code that will render as a button that directs users to a shopping cart. Stripe, on the other hand, requires some JavaScript and HTML experience to get the job done. There's a decent amount of sample code available in the documentation, but without some basic coding knowledge, you might feel lost.

So if you're not working with a third-party solution and you're a coding newbie, PayPal is probably your best bet.

Testing Your Website

Stripe and PayPal both offer robust testing options

Adding a checkout solution to your site, flipping the switch, and getting paid sounds tempting—but don't get ahead of yourself. Especially when there's money involved, you don't want want any "oops" moments. So first, you need to test.

But how do you test a payment system without using real money? The solution is what's called a sandbox, i.e., a testing site that mirrors your actual site. Much like the childhood image evokes, the sandbox is a place to play around. In this case, you're playing around with your site, testing different features to be sure that everything works before making it live to your customers.

PayPal allows testing through sandbox accounts that can be accessed through their developer site. Once you've created your sandbox account, you can log in to a sandbox version of PayPal and experiment. Create checkout buttons and use test credit card numbers provided by PayPal (or the sample buyer PayPal account that comes with the sandbox) to check that everything works from initial click through to purchase.

For the same purpose, Stripe offers a test API key alongside the live API key, and any transactions made using the test key are considered dummy transactions. They also provide sample credit card numbers, along with a suggested series of tests to be sure that any errors are handled properly before taking your site live. As you test, full logs are kept so you can review any errors; and while some errors require development knowledge to understand at a glance, there are thorough explanations available in the documentation. Plus, the dashboard can be switched to view test or live data with a toggle button on the left pane at any time. This is in contrast to PayPal, where it's necessary to log in to a completely separate sandbox site in order to test.

Stripe and PayPal both provide a robust set of tools to check that your site's payment system is working well before you let real customers at it. They go about it a bit differently, but they offer sufficient ways to test your site without using any real data.

Security

PayPal handles Payment Card Industry (PCI) compliance internally

When conducting business of any kind online, trust plays a huge role. How do you show that you are a trustworthy seller, and how do you know that your buyers are protected?

Both Stripe and PayPal offer standard user protections like two-factor authentication. The major difference between the two is how they address Payment Card Industry (PCI) compliance. Launched in 2006, the Payment Card Industry Data Security Standards (PCI DSS) are basically a checklist for you to follow that ensures that you perform regular security checks, handle transmission of payment data securely, and don't store credit card data. They're not legally binding, but following these practices keeps your buyers safe—and that's good for business.

Both Stripe and PayPal address the compliance standards, but the task of adhering to them will partially or completely fall on you depending on how and where you conduct your business. Specifics can be found on the PCI site.

PayPal, in general, handles PCI compliance internally as long as you use their own checkout button solution. You give up a little bit of freedom in how it looks, but you're spared the headache of ensuring that buyer credit card information is being handled appropriately.

Stripe is also a PCI DSS compliant organization, but as they point out, it's is a shared responsibility between you and them. They provide a thorough guide—including a self-assessment—to help you confirm that your organization and software are PCI compliant. So if you manage the transactions directly, Stripe requires you to place some additional emphasis on your own security based on the PCI guidelines.

If you're using third-party shopping cart solutions, PayPal and Stripe both defer to that solution to bear the burden of PCI compliance, so you'll need to confirm that your chosen service is doing the work for you.

If you're looking for the easiest route to security and compliance without a third-party checkout solution, PayPal takes care of the heavy lifting for you.

Subscriptions and Recurring Billing

PayPal has everything you need

Many online stores are selling a service (like Zapier), not a product (like Amazon). When that's the case, you're much more likely to need recurring billing, i.e., you need to be able to charge your customers on a regular basis. That also means you need to be able to handle different subscription periods, renewals, and cancellations.

If you use PayPal's button wizard—the same one you used to set up the shopping cart—setting up and managing subscriptions is a breeze. You define a few pieces: what the subscription is for, the billing frequency, and the pricing; and you can add a dropdown menu if you offer multiple subscription options. If you want, you can assign a unique identifier to the subscription to make it easier to track. Users can manage and cancel their own subscriptions from within their PayPal account, but you can also easily create cancellation buttons for them.

In Stripe, on the other hand, you need to manually subscribe users to your services through the dashboard. When subscribing users, you'll define the customer record by entering their personal information, a product, pricing, and terms up front. Because you're handling all this personal information, you risk not being PCI compliant. And if you want users to be able to subscribe and manage the subscription without your intervention, you'll need to invest in some third-party applications that support subscription management—or build your own.

Virtual Terminal

PayPal has a complete but pricey solution

You know when you swipe/insert your credit card at the grocery store? The thing you're swiping the card through is called a terminal. So a virtual terminal is the same thing—but without the physical aspect. It's a spot where you can manually enter credit card numbers in order to process a sale. It's not common practice for eCommerce—since usually customers are entering their own credit card information—but if you take orders over the phone or through the mail, you'll need a virtual terminal. And if you do, both Stripe and PayPal have you covered, but in different ways and with different payment structures.

PayPal's virtual terminal is simple and easy to use. You enter order details including the buyer's name, address, and credit card information, and the items or services being purchased. Then you can print any related receipts, shipping labels, or packing slips for the customer. It's actually quite reminiscent of working at a cash register in a brick-and-mortar store. The catch? It requires signing up for PayPal Payments Pro, which has a $30/month fee, whether or not you make any money.

Stripe doesn't offer a virtual terminal application, but there are various third-party services available, each of which carries its own charges and requirements.

Under exceptional circumstances, you can enter payments directly through the Stripe dashboard, but you're suddenly on the hook again for ensuring that you're following PCI requirements.

Bottom line: You can potentially get a cost advantage by looking for third-party options with Stripe, but PayPal has a solution ready to go.

Invoicing

Stripe has the better interface

If you're selling a product or a subscription, your customers will usually pay upfront. But many consultants, freelancers, and other service-oriented businesses don't charge clients up front. In some cases, the cost of the work isn't even clear until the project is complete. That's where invoices come in: They're essentially bills that you send to your customers to let them know how much they owe you. Most accounting software takes care of this for you, but both Stripe and PayPal also have built-in solutions.

PayPal's invoicing system covers all the bases. It's easy to establish payment terms and line items and specify a purchase order number if appropriate. You can attach a file to an invoice and you can even bill multiple customers at once. An especially nice touch is that you can customize the invoice by adding a company logo. Plus, customer records don't need to be added in advance: You'll need an email address for your customer, at minimum, but you can fill out their name, phone number, address, and other important items with a simple popup.

Stripe requires you to create your customer records in advance with all of their contact details, but once they're in the system, it's a simple process to send them an invoice via email. It's one of the few instances where Stripe doesn't rely on third-party services and applications to get the job done, and it's extremely well designed. There are also lots of places to select triggers for emails at various stages of payment; for example, you can receive notifications when there are successful payments or refunds. Unlike PayPal, Stripe doesn't allow for file attachments or the ability to bill multiple customers at once, but you can customize a few basic items such as color and logo.

When it comes down to it, both services offer a simple and effective method of sending invoices, but Stripe's UI is just a bit friendlier.

Disputes, Refunds, and Chargebacks

It depends who you want to decide the outcome

PayPal is a fairly comprehensive online payment system—not just a payment processor. People keep money in PayPal, can pay directly from their PayPal balance, and so on. For that reason, PayPal deals with disputes, refunds, and chargebacks internally. And PayPal is notorious for their refund policy. Refunds can be requested by buyers up to 180 days after the sale is made, regardless of the seller's own individual refund policy. Even if you as the seller decline the refund, PayPal anecdotally tends to rule in favor of the buyer if they use the Resolution Center to dispute your refund decision. Having said that, PayPal makes the process easy for you. Whenever there's an action for you to take, you'll receive an email with a link. Just follow the link and the prompts in the resolution center, and PayPal handles the rest.

Stripe, on the other hand, is primarily a payment processor, which means you can't store money there: It's just there in a holding pattern until it ultimately goes to your bank. As such, it doesn't have a refund policy of its own and doesn't decide the outcome of disputes. If someone wants a refund and you don't provide it, the buyer has to go to their credit card company to dispute it directly.

Although Stripe doesn't make any decisions, it does capture and facilitate the arbitration conducted by the credit card company. If a dispute occurs, it can be accessed from the dashboard under Payments and Disputes, and you can submit evidence to the credit card company through that Stripe interface. But be careful when refusing refunds: If the dispute doesn't fall in your favor, you're on the hook for a $15 dispute charge.

In the case of fraud, Stripe helps minimize charges with a feature called Radar, which uses machine learning to automatically flag and block credit card numbers often used in fraudulent activity.

In the end, both Stripe and PayPal offer an easy way to manage and resolve disputes. Which one you choose will depend on who you want rendering verdicts: the payment processor or the credit card company.

Mobile Payment Processing

PayPal has its own app and card reader

When it comes to payment processors, a combination of app, hardware, and service puts a credit card terminal in your pocket. Mobile payment processing gives you the ability to conduct in-person sales with only a card reader and your mobile phone or tablet. It's like a virtual terminal but without the added expense.

PayPal has a mobile app called PayPal Here that's supported on iOS and Android, and once you sign in, you'll get an easy-to-use card reader shipped to you. Stripe, on the other hand, doesn't have their own app, but they do recommend a number of third-party alternatives. Many of them are competitive with the PayPal app, but you'll likely spend a fair amount of time finding the one that works for you—and paying extra for it.

Tracking and Reporting

PayPal has a wider range of accounting reports

For tracking and reporting, we're looking at two questions:

How easy is it to find and download data?

How much additional work does it take to get common accounting reports?

Stripe has the definite edge in terms of ease-of-use. Simply navigate to the Payments and Customers section to download a list of transactions in a certain date range. Finding records is similarly straightforward thanks to the freeform search box. And if you need to be a bit more formal, there's a filter button with some common items to search for, such as the created date or whether it was a delinquent charge. There's also a sophisticated customer-specific page: It only takes a few seconds to pull up a customer, check to see if they had any recent orders, or verify their personal information.

PayPal also has a robust method of searching transactions through their Activity view. While the search bar isn't quite as freeform, you can still find what you need between that and a dropdown that tells the system the kind of information you're looking for. You can also look at customer-specific information, but unlike in Stripe, customer details are typically tied to a PayPal account that you can't edit, so it's only for reference.

In terms of formal reporting, PayPal has a plethora of accounting reports that'll make you feel confident that come tax time or quarterly review. Stripe, on the other hand, doesn't offer any formal accounting reports.

Which App Should I Use?

The good news: Choosing between Stripe and PayPal is a win-win. They're both reliable and scalable payment processors. The main difference: In certain areas, Stripe is dependent on other applications, which can be a barrier to sellers who are just getting started. PayPal, on the other hand, is a more complete solution on its own.

Our final recommendation? If you're looking to get into business online without any fuss or extra software, it's hard to go wrong with PayPal. If you're already well established and don't mind using third-party services to tie up loose ends, Stripe is a robust and smart choice.

Finally, here's an at-a-glance feature comparison.

Stripe PayPal Cost2.9% per transaction plus $0.302.9% per transaction plus $0.30TransactionsRequires a third-party shopping cartSimple checkout buttons that can be used on any websiteWebsite testingAlternate between test and live mode via toggleComplete sandbox buyer and seller accountSecurityRelies on third-party compliance, but provides guidanceHandles PCI compliance internally if you use their checkout solutionRecurring billingSubscriptions can be entered manually, but otherwise requires a third-party toolSubscription controls can be defined as buttons for any websiteVirtual terminalRequires a third-party solutionProvides a complete but pricey solutionInvoicingProvides a modern interface with fewer options than PayPalProvides a complete solution with a dated interfaceDisputes, refunds, and chargebacksBuyer's credit card company decides outcomes based on evidence provided through dispute sectionPayPal decides outcomes through resolution centerMobile payment processingProvides the service, but requires third-party hardware and appProvides a complete app and credit card scanner for a mobile deviceTracking and reportingEasy-to-use customer and sale tracking, but lacks full accounting reportsEasy-to-use customer and tracking features with full accounting reportsCustomer Service24/7 phone and chat supportBusiness hours, seven days a week

Automate Stripe and PayPal

Whichever payment processor you choose, save yourself time by automating all your workflows related to that software.

Mitchell Parsons, Operations Manager at Atlanta nonprofit Midtown Assistance Center, automates the transfer of data from PayPal to Salesforce when accepting donations. He says, "It automates the records and creates or updates the contact and opportunity records. It is a great time saver in helping us generate our thank you letters and receipts."

Here are some other ways you can automate your workflows with Stripe and PayPal:

Keep your team in the loop. Zapier will automatically notify you via email or Slack whenever a new payment is processed:

Don't miss a beat on your bookkeeping. Send all new charges to your recordkeeping app of choice:

Add customers who use your payment processor to your CRM or email list:

Don't see the workflow you're looking for? Create your own with our Zap editor.

Source: https://zapier.com/blog/stripe-vs-paypal/

0 notes

Text

Trump and Warren are Both Wrong

Jesse Fried is the Dane Professor of Law at Harvard Law School. This post was authored by Professor Fried. Related research from the Program on Corporate Governance includes Short-Termism and Capital Flows by Professor Fried and Charles C. Y. Wang (discussed on the Forum here).

President Donald Trump and Senator Elizabeth Warren rarely see eye-to-eye on policy, and frequently attack each other personally. But they have finally found common ground: both seem to believe that investors in public firms are too powerful, and the solution is to better insulate corporate directors from shareholders.

In August, each offered a proposal aimed at shielding boards from investor pressure. Senator Warren introduced legislation—the Accountable Capitalism Act—that would federalize corporate law and force all U.S.-domiciled firms with revenues exceeding $1 billion to hand over at least 40% of board seats to employees. The Act would also alter fiduciary duties to require directors to consider all stakeholders, not just shareholders. President Trump, in turn, asked the Securities and Exchange Commission to study the possibility of eliminating quarterly reporting for public firms and allowing boards to share the information with investors only semi-annually.

Bipartisanship is generally a good thing, especially in this era of hyper-polarized politics. But the consensus view that public shareholders are distorting firm behavior—a phenomenon often labelled “quarterly capitalism” or “short-termism”—is very wrong-headed. And the remedies emerging from this consensus, particularly Senator Warren’s, could profoundly damage the U.S. economy.

In the absence of any solid evidence that shareholders harm firms, the case for weakening investors has been based on myths, misconceptions, and misleading figures. For example, the press release for Senator Warren’s Accountable Capitalism Act recycles the erroneous claim that America’s biggest companies dedicate 93% of their profits to shareholders—funds that supposedly would have gone to workers or long-term investment.

But as my research with Charles Wang shows, the 93% payout figure is gross—it includes dividends and stock repurchases, but excludes equity issuances that move capital in the opposite direction. Net shareholder payouts are much lower. Figure 1 below displays both shareholder payouts (dividends and repurchases) and net shareholder payouts (dividends and repurchases, less issuances) for all public firms during 2007-2016, against a backdrop of net income. As Figure 1 makes clear, net shareholder payouts are only about 40% of shareholder payouts during the period. (Our research focuses on 2007-2016 but the results are almost identical for 2008-2017, the latest decade for which data are available.)

Another problem with this 93% figure is that the denominator—net income or profits—reflects what’s left after the firm has allocated a portion of its income to deductible expenses, including wages and R&D. For understanding the effect of net shareholder payouts on investment capacity, a better denominator is “income available for investment”: net income plus a firm’s after-tax R&D costs. Across all public U.S. firms, our research shows, net shareholder payouts during the period 2007-2016 were only about 33% of income available for investment, leaving approximately $7 trillion for that purpose.

In fact, my research with Charles Wang shows that much of this $7 trillion has gone into long-term investment. As Figure 2 below illustrates, the overall investment intensity at public firms, as measured by the ratio of capital expenditures (CAPEX) and R&D to revenue, was higher during 2012-2016 than during any other five-year period since the late 1990s boom. R&D intensity, the ratio of R&D to revenue, ended the period at an all-time high.

Nor are public firms financially constrained from engaging in additional investment; they had ample dry powder. Indeed, cash balances climbed from about $3.3 trillion in 2007 to about $5 trillion at the end of 2016. The misleading 93% figure and others like it paint a picture of shareholders starving firms of capital, crippling their ability to invest; the real figures do not.

Decisions about how to deploy capital in public firms—whether to invest it, store it for the future, or pay it out to investors—occur within the context of a market-based system. Investors provide capital to corporate managers under an agreed-upon allocation of decision-making power. If managers have a credible plan for long-term investment, investors can sit patiently as the firm spends years running up losses (such as Amazon, in its early years). When a firm can’t profitably deploy capital, investors want the cash returned to them so it can be invested in other firms, public and private. Overall, the market generally works, allocating financial resources to where they are most needed.

The ironically-titled Accountable Capitalism Act would endanger this system by making corporate insiders accountable to nobody but themselves. When 40% of a firm’s board consists of managers or their direct or indirect reports, outside investors would need to win almost every other seat to wrest control from incumbents. While this feat would be difficult even under existing arrangements, the Act’s new stakeholder-oriented fiduciary duties could make it all but impossible—by justifying directors’ use of extreme anti-takeover defenses to protect their board seats. And even if investors could gain a majority of board seats, these fiduciary duties could be used to prevent the investors from rationally allocating firm capital from inside the boardroom.

The Act’s effects can easily be predicted: capital would be trapped in cash-rich firms and mis-spent, the flow of capital from larger public firms to smaller public and private firms would dry up, and wealth would be transferred from public investors to corporate insiders. Firms looking to raise cash would find it harder. After all, why would investors hand funds over to unaccountable directors? Over time, capital would flee the country, followed by jobs. To be sure, employees of existing firms may feel more secure, at least in the short run. But there will be fewer opportunities in the U.S. for their children.

Of course, some firms may succeed in escaping the Act’s reach, either by domiciling outside the U.S. or by splitting themselves into smaller pieces. But these circumventions would give rise to other costs to the American economy, such as reduced operational efficiencies and a transfer of corporate tax revenues to other jurisdictions.

The Act could also be expected to lead to additional distortions down the road. Once corporate law is federalized, Congress will be tempted to use its foot-hold in corporate governance to add more mandates and restrictions, ostensibly to address other “problems” in corporate America, but actually to benefit key voting constituencies and campaign financiers. In short, the Act would put American crony capitalism on steroids.

President Trump’s proposal—which he tweeted after chatting with CEOs at his golf course—would also reduce corporate accountability, but through a different channel: by depriving shareholders of up-to-date information needed to monitor management. The CEOs whispering in Trump’s ear apparently told him that moving from quarterly to semi-annual disclosures would encourage boards to focus more on long-term investment. But, as my research with Charles Wang shows, R&D is at a record high and overall investment spending by public firms appears quite robust. Thus, it’s far from clear such encouragement is needed. In any event, evidence from the U.K. suggests that a reduction in disclosure frequency does not increase investment.

For most firms, the main effects of moving to semi-annual reporting will be profoundly negative: investors will find it harder to assess management and the value of their shares, and corporate insiders—and their tippees—will have more non-public information on which to trade. As a result, stock prices will be lower and firms going public will find it harder to raise capital.

To be sure, there could be certain public firms where both managers and outside investors prefer semi-annual over quarterly reporting, because the costs of more frequent disclosures exceed the benefits. Thus, the SEC should consider permitting firms to adopt semi-annual reporting after managers obtain approval by outside investors or at the IPO stage. But the CEOs pushing for semi-annual disclosures want the SEC to let them unilaterally reduce reporting frequency, even when it would hurt investors.

Perhaps President Trump and Senator Warren offered these ideas during the summer doldrums to rally their bases, or to provide material for Twitter, without actually expecting them to go anywhere. But there is a growing bipartisan consensus that excessive shareholder power is a critical problem facing America—notwithstanding the absence of any compelling evidence. This consensus creates a real risk that one or both of their policy proposals could be adopted, either in this administration or the next one.

Source: https://corpgov.law.harvard.edu/2018/09/06/trump-and-warren-are-both-wrong/

0 notes

Text

The Top 2 Advertising Mistakes According to a Man Who Spends $800,000 Per Month on Ads

To be successful in the new age of small business, you need to think about things in new ways, you need to do things in new ways, as well as say goodbye to habits and dogmas that no longer serve you.

One of the biggest concepts that needs to change is how you view work. No longer are you confined by corporate policies or expectations around the hours you work. Most business owners are paid for the end product, the services they provide, their expertise and their knowledge.

In order to continue to innovate and evolve in business, you need to understand why working more does not work for small business. Read the 5 reasons below:

1. It is not about working more or harder, it is about working smarter

The great American work ethic is defined by ‘hard work’, and in true American fashion, if a little is good, then more must be better! That’s not so in business.

Dedication, determination and consistency are important to being successful in small business – but working smarter means you get to your goals quicker with more resources, energy and brainpower to take things to the next level.

One of the biggest reasons businesses fail is because they physically reach a point where the business owner and their staff just can not work more. There are no more hours to work because the resource of time has been exhausted.

Working smarter is a key habit that creates scalability in your small business, which benefits your employees, your clients and your family. Scalability is the gateway to building a legacy that contributes and impacts everyone who touches your business. Scalability brings profits and freedom.

2. It is not about doing the work, it is about ensuring the work gets done

Most business owners start their business because they find that they were really good at their corporate careers, but want the freedom that entrepreneurship can bring.

You are used to doing the work, so it is really hard to let it go. It’s not surprising that you may find value in doing a ‘good job’ or by doing the work that ‘no one can do like me’. This is a trap that will forever limit your ability to grow and scale. Gone are the days where you can be successful in a silo.

While you are working on building the stability of predictable cash and clients in the business, you most likely will be doing the work of servicing those clients, while still carrying out the responsibilities of being the owner. This is what you do in this stage of business growth. When you reach cash stability, it is time to define how the work gets done so that you can work ‘on’ the business, not just ‘in’ the business.

In order to scale richly in your business, you’ll need to transition out of the ‘worker’ role in order to transition into the ‘manager’ role, and eventually transition into the true role as an entrepreneur leading an organization into profits.

“Focus on being productive instead of busy.” – Tim Ferriss

3. Busyness does not make a good business

You can get a little lost in business to the point where you aren’t sure what to do next. Or sometimes, you know what to do – you just don’t want to. So you avoid it by getting caught up in the busyness of the business. Busyness is energy and time wasted on unimportant and non-urgent tasks that do not move the needle in your business.

As an employee, you are often rewarded when you ‘look busy’ – so you get really good at it. The average productivity of a working day is a mere 3 hours. What you are doing with the rest of your time matters. Your time is precious, spend it on revenue or result-oriented action. Scaling your business is knowing the difference between what there is to do and what needs to be done.

4. Hustle and Grind leads to Broke & Tired

“Hustle and Grind” makes for a great motivational poster and shareable quote, but hustling without clear goals and results, often leads to burnout. Women business owners have a special gift to take ‘Hustle and Grind’ to a whole other level, and not in a good way. When you spend every single moment working, you often lose your health, your joy and get lost in a circular loop that leads nowhere.

There’s also this ‘unspoken’ belief that you have to earn your way and pay your dues which drives many owners to ‘Hustle and Grind’. That creates a negative space that does not create success. ‘Inspired Action’ and the KISS method tend to produce more gains than ‘Hustle and Grind’. When in doubt, see #1.

Scaling your small business successfully means that there are time periods of intensity, launching and pushing – but they are periods. They are not meant to be the status quo. You are not a machine, you are a human.

“Balance isn’t something you achieve “someday.” – Nick Vujicic

5. All work and no play makes Jane a cranky girl

The most unhappy small business owners are the ones working the hardest. Their faces say it all – bags under their eyes, dull skin and cranky attitudes. Overworking and not enjoying life leads to resentment. The saying that, “Entrepreneurs give up working 40 hour jobs, so they can work 80 hours in their business”, is an unfortunate story for many business owners.

If you really want the freedom that can come along with owning your business, you need to live it from day one. You need to design your business to deliver that freedom. Waiting for ‘someday’ winds up becoming ‘never’ for many entrepreneurs because they can’t break the habit.

Positivity in a business owner is contagious. People want to be around it in whatever way they can. When you lead a more balanced life, you encourage others to do so as well. Think of it as an attractive form of marketing.

6. Even Formula 1 racers take pit stops

Learn to value the “in-between.” Ever wonder why you have your best ideas in the shower, or in the middle of the night? Chances are, that’s because you are not working. The biggest value you can have in the success of your small business is to solve problems. It is the inspired ideas, the simple solutions that come to you in these moments that drive you forward.

This also speaks to the fact that to be successful in business you need to take care of your physical and spiritual health, so when you do reach your finish line, there is enough of you left over to enjoy the success. Just like the racers, learn to take pit stops. Sometimes, in order to speed up, you need to slow down.

The more successful you are in your business, the more demands you have on your time. The greatest asset in your business becomes you. You need moments of rest, recovery and ‘in-between’ to allow your greatness to flourish.

You do not earn a gold star for ‘working more’ in business, yet so many business owners let busyness become their distraction of choice and wonder why they are not able to grow and scale their businesses.

The best businesses are often simple. The most successful businesses are singularly focused. The wealthiest people say no the most. These are the skills you need to be able to scale your business richly.

What is one thing you learned from this article? Share your thoughts below!

Source: https://addicted2success.com/success-advice/the-top-2-advertising-mistakes-according-to-a-man-who-spends-800000-per-month-on-ads/

0 notes

Text

IDFC Bank is now IDFC First Bank

IDFC Bank has changed its name to IDFC First Bank following the merger of Capital First with the private sector lender. “…the name of the Bank has been changed from IDFC Bank Limited to IDFC First Bank Limited with effect from January 12, 2019 by virtue of Certificate of Incorporation pursuant to change of name issued by the Registrar of Companies, Chennai,” it said in a regulatory filing. IDFC Bank and non-banking financial company Capital First had announced completion of their merger on December 18, creating a combined loan asset book of ₹1.03 lakh crore for the merged entity.

Source: https://www.thehindubusinessline.com/news/idfc-bank-is-now-idfc-first-bank/article25986723.ece?_escaped_fragment_=

0 notes

Text

Mexican economy strengthens in third quarter

Mexican economic activity accelerated during the third quarter as services and primary activities like agriculture picked up pace.

The national statistics agency on Tuesday said preliminary estimates showed gross domestic product expanded 0.9 per cent in seasonally adjusted terms versus the previous three-month period.

Compared to the same quarter a year earlier, the economy grew by 2.7 per cent.

The Mexican peso strengthened 0.6 per cent against the US dollar to 19.9465 on the news.

The peso has come under pressure this week after incoming Mexican president Andrés Manuel López Obrador said he plans to cancel the capital’s new $13bn airport, which is one-third built, when he takes office on December 1.

JPMorgan has reduced its economic growth forecast for Mexico in 2019 by 0.5 per cent to 1.9 per cent, saying the cancellation “raises a thick cloud of uncertainty” and is likely to have important macroeconomic ramifications. The bank expects that subdued business confidence and other knock-on effects from policy uncertainty will hit GDP next year.

Jim Barrineau, co-head of emerging markets debt and a portfolio manager at Schroders, said while Mexico’s third-quarter growth was better than expected, all eyes are now on López Obrador.

“The decision to walk away from the ongoing construction of the new airport definitely dents investor confidence, which translates into a more volatile currency and better odds for an additional rate hike. Coupled with slowing US growth, that would likely trim near-term Mexican growth meaningfully,” Mr Barrineau said.

Source: https://www.ft.com/content/c684d806-dc50-11e8-9f04-38d397e6661c

0 notes

Text

Patanjali Ayurved revises offer for bankrupt Ruchi Soya

The revised offer will mean the lenders will have to write off 60 per cent of their dues.

Baba Ramdev's Patanjali Ayurved has sweetened its offer for bankrupt Ruchi Soya to Rs 4,350 crore as upfront cash to banks.

As earlier offered, it will also infuse Rs 1,700 crore into the company.

The revised offer will mean the lenders will have to write off 60 per cent of their dues.

Adani Wilmar had reportedly offered Rs 4,300 crore in August last year, but withdrew this January, citing delay in the resolution process.

Patanjali's earlier offer was for Rs 4,100 crore.

Adani had proposed an additional Rs 1,700 crore, as Patanjali did, for fund infusion.

Adani was declared the highest bidder but Patanjali objected, saying its offer was better.

A source said the Adani offer was earlier selected as settlement of bank loans has higher weight in the evaluation (of the lenders) than infusion of funds into the debtor company.

Indore-headquartered Ruchi Soya, once one of the largest processors of edible oils, filed for bankruptcy in December 2017.

Its accumulated debt was Rs 12,000 crore; sales had fallen from Rs 31,500 crore in 2014-15 to Rs 12,000 crore in 2017-18.

A banking source said with the revised offer, the stage was finally set for acquisition of Ruchi Soya.

It had attracted over two dozen bids.

These were from private equity majors KKR and Aion Capital, beside consumer goods entities ITC, Godrej Agrovet and Emami, apart from Patanjali and Adani Wilmar.

Experts said the firm's five port-based refining plants were the key reason for bidder interest.

Photograph: Adnan Abidi/Reuters

Source: https://www.rediff.com/business/report/patanjali-ayurved-revises-offer-for-bankrupt-ruchi-soya/20190313.htm

0 notes

Text

296: Blogging for Multiple Income Streams – How a Part-Time Blog Became a Diverse Revenue Engine

This post may contain affiliate links. Please read my disclosure for more info.

“I feel like this is the most important project I’ve ever worked on,” Mike said about his blog YoungArchitect.com.

Mike Riscica runs a blog, podcast, and has built a thriving community for young professionals in the architecture field.

The idea for the blog came from a pain point in Mike’s life, and for many others – passing the Architect Registration Examination (ARE).

After failing to pass the exam 4 times (before passing) and seeing his peers struggling, Mike started blogging about his challenges.

“[My story] resonated with people in a pretty serious way,” he said, and he started seeing traction within the community.

He started monetizing his blog from day one with affiliate products and continued to add more revenue streams to scale up his business with courses, speaking gigs, books, videos, and more as his traffic grew.

Today his blog in a full-time business. He’s had the opportunity to travel the country with his dog doing speaking gigs, has helped hundreds of students pass their ARE, and has some interesting plans for the future.

Tune in to hear how Mike grew his blog, how it rings the cash register in at least half a dozen different ways, and the strategies you may be able to lift for your own project.

The Idea for the Blog

Growing up, Mike struggled with school. He was a special ed student and didn’t do too well in school.

It was after he had left school and started working for an interior design company that Mike said, “I realized I had a lot of skill I’d never tapped into before, like thinking three-dimensionally, and I didn’t know I loved to draw.”

He decided to go to architecture school when he was around 21 years old. Mike said he struggled with the Architect Registration Examination (ARE). He actually failed it 4 times, and he also saw his peers struggling to pass.

Looking back, he said there was a lot of bad information and not enough quality information available from people who had passed the ARE.

In need of a creative project to work on, Mike started the Young Architect blog right after his exams. His goal was to help others with their studies to pass the 7-part ARE to get their architecture license.

Mike’s Content and Marketing Strategies

Mike saw some traction early on just from writing about his story and how he had struggled with the exams.

There were a lot of stories online from people who had done well and passed their exams — making it sound easy. Hearing a different perspective “resonated with people in a pretty serious way,” Mike said.

How His Blog Makes Money

He started monetizing his blog from day one, and has been expanding his revenue streams ever since.

Affiliate Marketing

Mike was recommending books and study materials, so he signed up with the Amazon Affiliate program and started collecting commissions on any sales he referred.

It wasn’t long before the blog was generating $250 per month in affiliate income.

His Own Products

Mike started producing more content, started to notice more traction from the community, his peers, and decided to put a book together called, How to Pass the Architecture Registration Exam.

It’s available digitally, in paperback, and even in audiobook format. He said his book sales account for 5-10% of his overall revenue.

Group Coaching

After reading his book, people started reaching out to Mike asking for personal coaching. Mike didn’t want to start coaching people 1-on-1, but it gave him the idea to start a group coaching group.

Mike put together a program that takes students through all the study material, connects them with other students to help them learn from each other, and holds meetings online.

Hundreds of people have now been through this program, The ARE Bootcamp. It’s a 10-week program he first charged $300 for, but now sells at $700 per person, and it’s one of his largest income streams.

The Young Architect Podcast

After he had felt like he’d told his story enough times, Mike decided to start an interview-style podcast to put the spotlight on architects and other figures in the community.

He reached out to companies in the industry, such as those who make the study materials, offer further education, governing boards, etc, and secured sponsors for the show that way.

Video Courses

He has also recently started producing video content on The Young Architect Academy and said these have been selling well at $10 each using the Thinkific platform.

Freelance Architecture and Consulting

While not a main focus, clients occasionally ask Mike to take on a design project or other architecture work on a contract basis.

Public Speaking

Mike also does public speaking. He arranged a 30-day tour starting in New York, going to New Orleans, then Indianapolis, and back to New York. Mike gave 26 lectures in 22 cities over the 30 days.

He charged $150-200 per lecture (not all were paid), but more importantly this was a great way for him to promote his brand, courses, and network.

Job Board

One of the latest revenue streams Mike is working on is a job board. Mike was receiving lots of emails from companies recruiting architects asking for his help spreading the word.

So, he has built a job board on his site and is currently focusing on getting it as active as possible before monetizing it.

Live Events?

The closing night of a big architecture conference, Mike decided to host a party of his own at a local bar. At one point, there was a line out the door!

That inspired him to start thinking of his own live event, perhaps to coincide with the next industry conference in Las Vegas.

When the Blog Became a Full-Time Focus

Mike said he got to the point where something needed to give. He was working 80-hour weeks with both his full-time day job and spending evenings and weekends working on the YoungArchitect.

He had started doing some retail arbitrage selling products via Amazon’s FBA program, and although he said he didn’t enjoy this side hustle, it helped accelerate the growth of his blog.

Mike also said he wasn’t being challenged or growing at his day job, and with the blog making enough to support his lifestyle, it was a good time to take the leap.

Next Steps

Sponsors

Skillshare – Get two months of unlimited access to 20,000 Skillshare courses for just $0.99!

Want More Side Hustle Show?

Subscribe to The Side Hustle Show on iTunes!

Subscribe to The Side Hustle Show on Android!

Subscribe to The Side Hustle Show via RSS!

Or use the player app above to listen right in your browser.

Pin it for later:

Source: https://www.sidehustlenation.com/blogging-for-multiple-income-streams/

0 notes

Text

SEC Proposes Amendments to Codify Exemption to Credit Rating Agency Rule

Washington D.C., Sept. 26, 2018 —

The Securities and Exchange Commission today announced that it has voted to propose rule amendments to codify an existing temporary exemption for credit rating agencies registered with the Commission as nationally recognized statistical rating organizations (NRSROs).

Rule 17g-5(a)(3) under the Securities Exchange Act established a program to provide information necessary to determine a structured finance product’s credit rating to NRSROs that were not hired by the issuer, sponsor, or underwriter of the structured finance product. Prior to the compliance date for Rule 17g‑5(a)(3), the Commission granted a temporary conditional exemption to the rule for certain structured finance products issued by non-U.S. persons and offered and sold outside the United States. The Commission subsequently extended this exemption.

The amendments proposed by the Commission today would codify the existing temporary exemption to Rule 17g-5(a)(3) and clarify the exemption’s conditions. The proposed amendments would also clarify the conditions applicable to similar exemptions in Exchange Act Rules 17g-7(a) and 15Ga-2 so that the approach among these exemptions remains consistent. Rule 17g-7(a) requires an NRSRO to disclose certain information when it publishes a rating action. Rule 15Ga-2 requires an issuer or underwriter to disclose the findings and conclusions of any third-party due diligence report it obtains with respect to an asset-backed security that is to be rated by an NRSRO.

“Proposing permanent relief in this area is a common sense step,” said Chairman Jay Clayton. “The relief applies to products that are issued by non-U.S. persons and are offered and sold outside of the United States, and is consistent with the approach taken by the Commission in other contexts.”

The public comment period will remain open for 30 days following publication of the proposing release in the Federal Register.

* * *

FACT SHEET

Action

The Commission today proposed amendments that would codify an existing exemption to Exchange Act Rule 17g-5(a)(3) relating to ratings of structured finance products. The proposed amendments would also clarify that the exemptions to Exchange Act Rules 17g-5(a)(3), 17g-7(a), and 15Ga-2 apply only if all offers and sales of a security or money market instrument by any issuer, sponsor, or underwriter linked to the security or money market instrument will occur outside the United States.

Highlights

The proposed amendment to Rule 17g-5(a)(3) would add a new paragraph to the rule to provide that the rule will not apply to an NRSRO when issuing or maintaining a credit rating for a security or money market instrument issued by an asset pool or as part of any asset-backed securities transaction, if:

the issuer of the security or money market instrument is not a U.S. person (as defined in Securities Act Rule 902(k)); and