#TWTR analyst estimates

Text

TWTR Stock Price | Twitter Inc. Stock Quote (U.S.: NYSE) | MarketWatch

TWTR Stock Price | Twitter Inc. Stock Quote (U.S.: NYSE) | MarketWatch

Twitter Inc.

Twitter, Inc. is a global platform for public self-expression and conversation in real time. It provides a network that connects users to people, information, ideas, opinions and news. The company’s services include live commentary, live connections and live conversations. Its application provides social networking services and micro-blogging services through mobile devices and the…

View On WordPress

#Twitter Inc. analyst estimates#Twitter Inc. analyst ratings#Twitter Inc. analyst recommendations#Twitter Inc. earnings estimates#TWTR#TWTR analyst estimates#TWTR analyst recommendations#TWTR earnings estimates#TWTR ratings#TWTR share estimates

0 notes

Text

US Stock Futures Gain; All Eyes On Consumer Price Index - Applied Materials (NASDAQ:AMAT), Delta Air Lines (NYSE:DAL)

New Post has been published on https://medianwire.com/us-stock-futures-gain-all-eyes-on-consumer-price-index-applied-materials-nasdaqamat-delta-air-lines-nysedal/

US Stock Futures Gain; All Eyes On Consumer Price Index - Applied Materials (NASDAQ:AMAT), Delta Air Lines (NYSE:DAL)

Pre-open movers

U.S. stock futures traded higher in early pre-market trade on Thursday after closing slightly lower in the previous session.

The consumer price index for September is scheduled for release at 8:30 a.m. ET. Core prices increased 0.6% in August with analysts expecting prices slowing to 0.4% for September. Overall prices might rise 0.2% in September following August’s 0.1% gain.

Data on initial jobless claims for the latest week will be released at 8:30 a.m. ET, while the U.S. Treasury budget report for September will be released at 2:00 p.m. ET. Federal Reserve Bank of Atlanta President Raphael Bostic is set to speak at 1:00 p.m. ET.

Investors are also awaiting earnings results from Domino’s Pizza, Inc. DPZ, Delta Air Lines, Inc. DAL, Walgreens Boots Alliance, Inc. WBA and The Progressive Corporation PGR

Check out this: Cameco, Kinnate Biopharma And Other Big Losers From Wednesday

Futures for the Dow Jones Industrial Average climbed 158 points to 29,419.00 while the Standard & Poor’s 500 index futures rose 19.75 points to 3,608.25. Futures for the Nasdaq index rose 35.50 points to 10,876.00.

Commodities

Oil prices traded slightly higher as Brent crude futures rose 0.4% to trade at $92.81 per barrel, while US WTI crude futures rose 0.1% to trade at $87.29 a barrel. The Energy Information Administration’s weekly report on natural gas stocks in underground storage is scheduled for release at 10:30 a.m. ET, while the EIA’s weekly report on petroleum inventories in the U.S. will be released at 11:00 a.m. ET.

Gold futures rose 0.3% to trade at $1,682.10 an ounce, while silver traded up 0.9% at $19.11 an ounce on Thursday.

A Peek Into Global Markets

Europe Markets

European markets were higher today. The STOXX Europe 600 Index rose 0.2%, London’s FTSE 100 rose 0.2% while Spain’s IBEX 35 Index rose 0.4%. The French CAC 40 Index gained 0.5%, while German DAX climbed 0.8%.

Annual inflation rate in Germany was confirmed at a rate of 10% for the month September.

Asia-Pacific Markets

Asian markets traded lower today. Japan’s Nikkei 225 fell 0.6%, China’s Composite Index fell 0.3%, while Hong Kong’s Hang Seng Index fell 1.87%. Australia’s S&P/ASX 200 slipped 0.1%, while India’s BSE Sensex fell 0.4%.

The value of loans in Japan rose 2.3% year-over-year in September, while producer prices in Japan climbed by 9.7% year-over-year in September.

Broker Recommendation

Raymond James initiated coverage on Nike Inc NKE with an Outperform rating and announced a price target of $99.

Nike shares rose 0.5% to $89.00 in pre-market trading.

Check out this: Ethereum Drops Below $13,000; Here Are The Top Crypto Movers For Thursday

Breaking News

Applied Materials Inc AMAT lowered its fourth-quarter guidance. Applied Materials now expects fourth-quarter revenue of approximately $6.4 billion, plus or minus $250 million versus average analyst estimates of $6.67 billion.

Taiwan Semiconductor Manufacturing Company Limited TSM reported a Q3 net profit of T$280.9 billion ($8.81 billion), versus estimates of T$265.64 billion. Revenue for the quarter surged 36% to $20.23 billion.

India-based car-sharing platform Zoomcar Inc. is likely to go public through a merger with blank-check company Innovative International Acquisition Corp. IOAC reported Bloomberg, citing sources.

Twitter Inc TWTR is reportedly reviewing its permanent ban policies to bring moderation of its platform more in line with Tesla Inc TSLA CEO Elon Musk’s point of view.

Check out other breaking news here

Read full article here

0 notes

Text

Twitter (TWTR) earnings Q2 2022

Twitter (TWTR) earnings Q2 2022

Musk would have been appointed to Twitter’s board on Saturday, but the world’s richest man informed the company on the day that he would not, in fact, be taking the board seat.

Andrew Burton | Getty Images News | Getty Images

Twitter reported earnings for the second quarter on Friday that missed analyst estimates on earnings, revenue and user growth.

Shares of Twitter fell as much as 2% in pre…

View On WordPress

0 notes

Link

#AlibabaGroupHoldingLtd#BaiduInc#BreakingNews:Markets#Business#businessnews#China#DollarGeneralCorp#DollarTreeInc#Earnings#Economy#Macy'sInc#Macys#MarketInsider#Markets#Medtronic#MedtronicPLC#NutanixInc#NVIDIACorp#SnowflakeInc.#Stockmarkets#Twitter#TwitterInc#Williams-SonomaInc

1 note

·

View note

Photo

What to know this week

Traders are gearing up for a busy week of corporate earnings results from the mega-cap technology stocks this week. This will come alongside a slew of economic data reports and a monetary policy decision from the Federal Reserve.

The biggest names in the S&P 500 — including Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Facebook (FB) and Alphabet (GOOGL) — are set to report second-quarter results this week. The reports will add to what has already been an exceptional earnings season: So far, 24% of companies in the S&P 500 have reported second-quarter results, and of these, 88% have topped Wall Street’s earnings per shares estimates, according to an analysis from FactSet. The blended earnings growth rate for the blue-chip index, which includes both companies’ reported growth rates and the estimated rates for the companies have yet to report, stands at 74.2%, which would be the highest since the fourth quarter of 2009.

Earnings results from technology companies Snap (SNAP) and Twitter (TWTR) last week underscored the strength in the internet advertising market, suggesting a strong backdrop that likely also benefitted bigger ad-driven companies like Facebook and Alphabet. Snap’s second-quarter revenue growth came in at 116%, or the biggest jump in four years, and the stock rocketed to a record high following the results. Both Snap and Twitter grew active users more than expected, and their estimates topping second-quarter revenues suggested better monetization of these increased users.

According to JPMorgan analyst Doug Anmuth, Snap’s results especially “will likely raise the bar for other ad names,” including Alphabet and Facebook. The companies report results on Tuesday and Wednesday, respectively.

“GOOGL shares are well-owned, but GOOGL remains one of our Top Ideas in 2021 as we believe: 1) reopening will remain a tailwind for Search and YouTube ads, especially as overall spend continues to shift online and travel continues to recover; 2) overall margins will remain meaningfully above pre-pandemic levels … 3) Cloud growth will remain solid at 40%+ while profit losses continue to improve; and 4) greater capital returns are likely on the heels of the $50 billion incremental buyback authorization last quarter,” Anmuth wrote in a note published July 22.

Story continues

As for Facebook, “advertising should continue to benefit from reopening and we are encouraged by newer initiatives around Reels and Shops, as well as the creator economy, audio, and AR/VR [augmented reality/virtual reality] a bit further out,” Anmuth added.

An illustration picture taken in London on December 18, 2020 shows the logos of Google, Apple, Facebook, Amazon and Microsoft displayed on a mobile phone and a laptop screen. (Photo by JUSTIN TALLIS / AFP) (Photo by JUSTIN TALLIS/AFP via Getty Images)

Alphabet has been the best performer of the Big Tech FAANG stocks so far in 2021, with shares rising 52% compared to the S&P 500’s 17.5% gain for the year-to-date. As a company that derives meaningful revenue from travel-related advertising revenue, Alphabet has been viewed as a key beneficiary of the broader economic reopening that began to occur in the spring of this year. Other software names, by contrast, have generally been viewed as bigger beneficiaries of a stay-at-home and work-from-home environment.

Alphabet’s second-quarter revenue, excluding traffic acquisition costs (TAC), is expected to grow 46% to $46.1 billion, according to Bloomberg data, which would mark the fastest top-line growth for the company since the fourth quarter of 2012.

Still, other online advertisers are also poised to get a boost from the reopening environment, with marketers more open to spend as pandemic-related uncertainty eased. Facebook’s revenues likely grew 49% over last year to $27.9 billion for the second quarter, accelerating slightly from the 48% rate in the first three months of 2021. That growth would come even as the company continues to contend with some decreased ad-targeting abilities after a recent Apple update that allowed users to opt out of tracking in apps including Facebook on iOS devices.

And Apple, for its part, likely also had a strong fiscal third-quarter, according to Wall Street’s estimates. Though consensus analysts expect to see that revenue growth slowed sequentially to 24% from the second quarter’s 54%, a boost from Apple’s latest iPhone upgrade cycle will likely still be at play, according to Wedbush analyst Dan Ives.

“While the chip shortage was an overhang for Apple during the quarter, we believe the iPhone and Services strength in the quarter neutralized any short term weakness that the Street was anticipating three months ago,” Ives said in a note published July 21. “Taking a step back we believe based on our recent Asia supply chain checks that iPhone 13 demand will be similar/slightly stronger than iPhone 12 out of the gates which speaks to our thesis that this elongated ‘supercycle’ will continue for Cupertino well into 2022.”

Meanwhile, e-commerce behemoth Amazon is heading into its first-ever earnings report without founder Jeff Bezos at the helm. The stock has underperformed so far in 2021, rising 12.3% for the year-to-date, after jumping by more than 76% in 2020 amid a pandemic-fueled boom in e-commerce demand.

“We expect strong top-line growth in ’21, albeit decelerating versus pandemic-charged ’20, led by e-commerce growth of +27% y/y (vs. +42% y/y), including a strong 2Q and solid growth in 3Q-4Q as AMZN comps the pandemic surge,” Cowen analyst John Blackledge wrote in a note.

An early Prime Day sales extravaganza is poised to help boost Amazon’s second-quarter top-line growth. The two-day event took place in late June this year, or at the end of the second quarter, compared to July 2019 and October 2020. And on the bottom-line, Amazon’s faster-growing, high-margin Amazon Web Services (AWS) cloud computing platform likely continued to help boost profitability.

Federal Reserve decision

The Federal Reserve kicks off its latest two-day meeting on Tuesday, with a monetary policy decision and press conference from Fed Chair Jerome Powell set to take place Wednesday afternoon.

The Fed’s June monetary policy statement and updated Summary of Economic Projections were taken as much less accommodative than many market participants expected, with the central bank raising its median forecasts for U.S. economic growth and core inflation over the next two years. The projections suggested the Fed might be more inclined to adjust policy in light of a fast-recovering economy experiencing rising inflation.

Federal Reserve Board Chair Jerome Powell testifies before Senate Banking, Housing, and Urban Affairs hearing to examine the Semiannual Monetary Policy Report to Congress, Thursday, July 15, 2021, on Capitol Hill in Washington. (AP Photo/Jose Luis Magana)

The Fed’s first monetary policy move would impact the central bank’s quantitative easing program, with asset purchases still taking place at a rate of $120 billion per month. Powell’s discussions around these purchases have shifted throughout his recent public appearances, suggesting more serious consideration among FOMC members to announce the start of tapering. In April, for instance, Powell said the economy was “a long way from” achieving the Fed’s employment and inflation targets that would trigger a pivot to less accommodative monetary policy. But after the Fed’s June meeting, Powell said the economy was “still a ways off” from the central bank’s goals.

“Next week’s FOMC meeting should be less eventful than June’s hawkishly-perceived meeting. There will be no new interest rate forecasts ‘dots’ so attention will focus on the post-meeting statement and Chair Powell’s press conference,” JPMorgan economist Michael Feroli wrote in a note. “We believe the statement’s wording around asset purchases will be unchanged, but we expect that Powell will relate that the Committee discussed tapering again and that the economy is slowly getting closer to passing the ‘substantial further progress’ test to actually start tapering.

However, in the weeks since the Fed’s June meeting, more concerns arose around the Delta variant of the coronavirus, which triggered a sell-off in markets last week and which might increase monetary policymakers’ perceptions of the risks still present in the economy. At the same time, however, the risk that fast-rising inflation might need to be curbed with a monetary policy adjustment has also increased, with core consumer prices and producer prices each rising faster-than-expected in June.

But on net, the Fed is likely to maintain a wait-and-see approach before making any adjustments, according to Feroli.

“Powell’s mid-July Congressional testimony raised the prospect that the FOMC statement would introduce an asymmetric policy bias: standing prepared to adjust policy if the Fed ‘saw signs that the path of inflation or longer-term inflation expectations were moving materially and persistently beyond levels consistent with our goal,'” Feroli said. “Since that testimony the rise of the Delta variant has injected some downside growth risks into the outlook, and this should help the doves argue for retaining the current symmetric policy bias.”

Earnings Calendar

Monday: Lockheed Martin (LMT) before market open; Tesla (TSLA) after market close

Tuesday: Centene (CNC), UPS (UPS), 3M (MMM), SiriusXM Holdings (SIRI), Sherwin-Williams (SHW), General Electric (GE), Stanley Black & Decker (SWK), Polaris (PII), Waste Management Inc (WM), Boston Scientific Corp (BSX), JetBlue (JBLU), Fiserv (FISV), Raytheon Technologies (RTX), Invesco (IVZ), Lamb Weston Holdings (LW) before market open; Apple (AAPL), Starbucks (SBUX), Advanced Micro Devices (AMD), Alphabet (GOOGL), Teladoc Health (TDOC), Visa (V), Microsoft (MSFT), Mondelez International (MDLZ), Juniper Networks (JNPR), The Cheesecake Factory (CAKE) after market close

Wednesday: Humana (HUM), CME Group (CME), Pfizer (PFE), McDonald’s (MCD), Six Flags Entertainment (SIX), Boeing (BA), Moody’s Corp (MCO), General Dynamics Corp (GD), Teledyne Technologies (TDY), Bristol-Myers Squibb (BMY) before market open; Facebook (FB), Ford (F), Xilinx (XLNX), PayPal (PYPL), ServiceNow (NOW), Lam Research Corp (LRCX), Align Technology (ALGN) after market close

Thursday: Merck & Co (MRK), Intercontinental Exchange (ICE), T Rowe Price Group (TROW), Comcast Corp (CMCSA), Spirit Airlines (SAVE), Valero Energy (VLO), Hilton Worldwide Holdings (HLT), The Carlyle Group (CG), Mastercard (MA), Molson Coors Beverage Co (TAP), Keurig Dr. Pepper (KDP), Yum! Brands (YUM), PG&E (PCG), Citrix Systems (CTXS), S&P Global Inc (SPGI) before market open; Amazon (AMZN), Overstock.com (OSTK), Albertsons Co (ACI), Altria Group (MO), T-Mobile (TMUS), World Wrestling Entertainment (WWE), Twilio (TWLO), Pinterest (PINS), Mohawk Industries (MHK), Upwork (UPWK), Skyworks Solutions (SWKS), United States Steel (X), Gilead Sciences (GILD),

Friday: Caterpillar (CAT), VF Corp (VFC), Exxon Mobil Corp (XOM), Chevron Corp (CVX), Danimer Scientific (DNMR), Procter & Gamble (PG), AbbVie (ABBV), Charter Communications (CHTR) before market open

Economic Calendar

Monday: New home sales, month-on-month, June (4.0% expected, -5.9% in May); Dallas Fed Manufacturing Activity Index, July (32.3 expected, 31.1 in June)

Tuesday: Durable goods orders, June preliminary (2.0% expected, 2.3% in May); Durable goods orders excluding transportation, June preliminary (0.8% expected, 0.3% in May); Non-defense capital goods orders excluding aircraft, June preliminary (0.8% expected, 0.1% in May); Non-defense capital goods shipments excluding aircraft, June preliminary (0.8% expected, 1.1% in May); FHFA House Price Index, month-on-month, May (1.6% expected, 1.8% in April); S&P CoreLogic Case-Shiller 20-City Composite Index, month-on-month, May (1.50% expected, 1.62% in April); S&P CoreLogic Case-Shiller 20-City Composite Index, year-on-year, May (16.20% expected, 14.88% in April); Conference Board Consumer Confidence, July (124.0 expected, 127.3 in June); Richmond Federal Reserve Manufacturing Index, July (20 expected, 22 in June)

Wednesday: MBA Mortgage Applications, week ended July 23 (-4.0% during prior week); Advance Goods Trade Balance, June (-$88.0 billion expected, -$88.1 billion in May); Wholesale Inventories, month-on-month, June preliminary (1.1% expected, 1.3% in May); FOMC Monetary Policy Decision

Thursday: Initial jobless claims, week ended July 24 (380,000 expected, 419,000 during prior week); Continuing claims, week ended July 17 (3.192 million expected, 3.236 million during prior week; GDP annualized, quarter-on-quarter, second quarter (8.5% expected, 6.4% in first quarter); Personal consumption, second quarter (10.5% expected, 11.4% in first quarter); Core personal consumption expenditures, quarter-over-quarter, second quarter (6.0% expected, 2.5% in first quarter); Pending home sales, month-on-month, June (0.5% expected, 8.0% in May)

Friday: Personal income, June (-0.4% expected, -2.0% in May); Personal spending, June (0.7% expected, 0.0% in May); PCE deflator, month-on-month, June (0.6% expected, 0.4% in May); PCE deflator, year-on-year, June (4.0% expected, 3.9% in May); PCE core deflator, month-on-month, June (0.6% expected, 0.4% in May); PCE core deflator, year-on-year, June (3.7% expected, 3.4% in May); University of Michigan Sentiment, July final (80.8 expected, 80.8 in prior print)

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Read more from Emily:

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, YouTube, and reddit

0 notes

Text

These toymakers are expected to miss big this week, and 5 other earnings surprises for the first peak week of Q2 earnings season

Keeping with the trend of the early earnings season (and with historical trends), far more companies reporting this week are expected to beat on EPS expectations than miss. There are seven names in particular this first peak week of earnings that are on our radar. Four are anticipated to be beats and three are expected to be misses.

The Beats

To determine possible positive surprises we look for companies that have the following characteristics: 1. Large positive deltas vs. Wall Street 2. Significant upward revisions momentum into the report 3. Positive YoY growth expectations 4. A long history of beating 5. A long history of Estimize accuracy vs. the Street

GrubHub (GRUB)

Information Technology - Information Technology & Services | Reports July 25, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.45 when GrubHub reports on Wednesday, revised upward by 14% in the last 3 months and 11% higher than Wall Street’s $0.41. Revenues are also expected to come in higher at $234.6M as compared to the sell side’s consensus of $232.6M. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 75% and 48%, respectively. GRUB tends to move up an average of 7% in the 30-days post earnings release. This is also a name that tends to beat the Estimize consensus 67% of the time on EPS and 73% on revenues, and that Estimize is more accurate than Wall Street on 60% of the time on EPS and 73% on Revenue.

While EPS and revenues are important for GRUB, it’s Active Diners that investors will be eager to hear about. Right now the Estimize community is anticipating Active Diners to come in at 15.6M for Q2, an increase of 70% YoY. While this metric came in better than expected last quarter, food sales and daily active orders did not. Still, the company raise guidance for Q2, and hopes to benefit from a healthy US consumer as well as partnerships such as the recent one with Yum! Brands.

Advanced Micro Devices (AMD)

Information Technology - Semiconductors | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of $0.14 when AMD reports on Wednesday, revised upward by 38% in the last 3 months and 12% higher than Wall Street’s $0.12. Revenues are also expected to come in higher at $1.759B as compared to the sell side’s consensus of $1.718.B, a number that has been revised upward by 14% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 595% and 44%, respectively. AMD tends to move up an average of 6% in the 30-days post earnings release. This is also a name that tends to beat the Estimize EPS consensus 58% of the time, and that Estimize is more accurate than Wall Street on 58% of the time.

Competition between Advanced Micro Devices and Nvidia has started to heat up, with sales of AMD’s brand of APUs and CPUs, Ryzen, up 60% last quarter. Gross margins will also be important to watch again this quarter, with Estimize expecting them to come in at 37.16%, demonstrating a continual upward growth pattern over the last 4 quarters. The one area of concern revolves around their graphic card segment which has been hurting due to declining cryptocurrency prices.

Twitter (TWTR)

Information Technology - Internet Software & Services | Reports July 27, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.19 when Twitter reports on Friday, revised upward by 35% in the last 3 months and 9% higher than Wall Street’s $0.17. Revenues are also expected to come in higher at $708M as compared to the sell side’s consensus of $700M, a number that has been revised upward by 11% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 132% and 23%, respectively. Twitter tends to beat the Estimize EPS consensus 85% of the time, and Estimize is more accurate than Wall Street 95% of the time.

The big number to watch with the social media names is always monthly active users (MAUs). This quarter the Estimize community is looking for TWTR to report MAUs of 340.3M, a slight increase of only 4% YoY, keeping in line with their longtime trend. Those estimates have remained mostly steady, even after analysts and investors worried that a recent move to suspend millions of accounts in order to remove malicious actors from the social network and improve the “health of the service” according to CFO Ned Segal.

Align (ALGN)

Health Care - Health Care Equipment & Supplies | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of $1.17 when Align reports on Wednesday, only revised upward by 2% in the last 3 months and 7% higher than Wall Street’s $1.09. Revenues are also expected to come in higher at $479.2M as compared to the sell side’s consensus of $469.2M, a number that has been revised upward by 5% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in healthy at 38% and 34%, respectively. ALGN tends to move up an average of 4% in the 30-days post earnings release. This is also a name that tends to beat the Estimize EPS consensus 74% of the time, and that Estimize is more accurate than Wall Street on 87% of the time.

Align is expected to continue to benefit from a healthy US consumer that is willing to spend discretionary income on health and wellness products. Total Invisalign shipments for Q2 are anticipated to come in atl 302,590, an increase of 11% QoQ and 29% YoY.

The Misses

To determine possible negative surprises we look for companies that have the following characteristics: 1. Large negative deltas vs. Wall Street 2. Significant downward revisions momentum into the report 3. Negative YoY growth expectations 4. A long history of missing 5. A long history of Estimize accuracy vs. the Street

The toymakers - while Hasbro and Mattel have been suffering for several quarters now, the bankruptcy of Toys R Us earlier this year has really exacerbated those losses, and both are expected to be two of the worst reporting companies this week.

Hasbro (HAS)

Consumer Discretionary - Leisure Equipment & Products | Reports July 23, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.29 when Hasbro reports tomorrow morning, revised down by 49% in the last 3 months and lower than Wall Street’s $0.30. Revenues are also expected to come in lower at $837.9M as compared to the sell side’s consensus of $844.2M, a number that has been revised downward by 14% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in at -46% and -14%, respectively. This name tends to beat the Estimize EPS consensus 69% of the time, but only beats on revenues 42% of the time. Estimize is more accurate on EPS 69% of the time, an 58% of the time on revenues.

Mattel (MAT)

Consumer Discretionary - Leisure Equipment & Products | Reports July 25, after the close.

The Estimize community is looking for earnings per share (EPS) of -$0.35 when Mattel reports tomorrow morning, revised down by 163% in the last 3 months and lower than Wall Street’s -$0.32. Revenues are also expected to come in lower at $859.7M as compared to the sell side’s consensus of $863M. Year-over-year (YoY) EPS and revenue growth are expected to come in at -149% and -12%, respectively. This name tends to beat the Estimize EPS and revenue consensus only 42% of the time.

Spirit Airlines (SAVE)

Industrials - Airlines | Reports July 26, before the open.

The Estimize community is looking for earnings per share (EPS) of $0.99 when Spirit Airlines reports on Thursday, revised downward by 5% in the last 3 months and 9% lower than Wall Street’s $1.09. Revenues are also expected to come in lower at $845.5M as compared to the sell side’s consensus of $851.8M, a number that has been revised downward by 1% since last quarter. Year-over-year (YoY) EPS and revenue growth are expected to come in at -13% and 21%, respectively. SAVE tends to beat the Estimize EPS consensus 70% of the time but revenues only 35% of the time. Estimize is more accurate on both 60% of the time.

While most of the the major airlines beat Wall Street expectations already this quarter, Delta, United and American all mentioned the pinch of higher oil costs. While those larger carriers have options to hedge against higher oil prices such as passing those costs along to the consumer, Spirit really has no way to hedge as an ultra low cost carrier that counts fuel as it’s biggest expense.

1 note

·

View note

Text

Buy Twitter number Is Twitter a Buy or Sell After Its Post-Earnings Plunge? Twitter is getting crushed after reporting disappointing user growth. Is that a buying opportunity or should investors stay clear of this one?

It’s been a mixed bag for social media stocks this quarter as Twitter (TWTR) - Get Report wraps up earnings from the Big Four.

Facebook (FB) - Get Report ripped to new all-time highs after easily clearing top- and bottom-line estimates, while Pinterest (PINS) - Get Report sank 14.5% Buy Twitter verification number despite what was actually a pretty strong report.

In a volatile session last week, Snap (SNAP) - Get Report opened higher by 8.7% and gave up virtually all of its gains before the stock finished higher by roughly 7.5% after its quarterly results.

For Twitter’s part, the stock has been following the path of Pinterest, with shares currently down 14% on the day.

While the company beat on earnings Buy Twitter verification code expectations, user growth disappointed Wall Street.

The analysts weren’t impressed either, causing a number of them to cut their price targets on the stock. One investor even called the stock a long-term secular short.

Let’s have a look at the charts to see what the technicals might suggest.

Facebook is a holding in Jim Cramer's Action Alerts PLUS member club. Want to be alerted before Jim Cramer buys or sells FB? Learn more now.

how to get Twitter verification code, Twitter phone verification bypass, Twitter verifying your number, Twitter verify phone number, skip Twitter verify, your phone Twitter phone number login Twitter login code text Twitter sms verification error 2018 how to get Twitter verification code Twitter verifying your number Twitter verification failed how to get Twitter verify number random verification code text text how to get Twitter verify number how to get Twitter verification code Twitter phone verification bypass Twitter verifying your number Twitter verify phone number skip Twitter verify your phone Twitter phone number login Twitter login code text Twitter ms verification error 2018 how to get Twitter verification code Twitter verifying your number Twitter verification failed how to get Twitter verify number random verification code text like verification code flurv verification code your Twitter verification code is verification code spam tfs verification code text atom verification code Twitter verification code not working random verification code, text like verification code, flurv verification code, your Twitter verification code, is how to get Twitter verify number, Twitter verifying your number Twitter verification failed Twitter login code text Twitter verification code not working Twitter sms verification error 2019 Twitter verification failed tap to try again Twitter verify your phone Twitter login code text Twitter sms verification error 2018 Twitter verification code not on Twitter but received login code via text message how to get Twitter verification code Twitter verification failed Twitter error bypass Twitter sms Twitter verifying your number Twitter no sms verification Twitter login code text how to get Twitter verify number how to get Twitter app verification code Twitter app phone verification bypass MoneyLion app verifying your number Twitter app verify phone number skip Twitter app verify your phone Twitter app phone number login Twitter app login code text Twitter app sms verification error 2018 how to get Twitter app verification code Twitter app verifying your number, Twitter app verification failed, how to get Twitter app verify number, random verification code text like verification code, flurv verification code your Twitter app verification code is Twitter app verification code spam tfs verification code text atom verification code Twitter app verification code not working random verification code text like verification code flurv verification code your Twitter app verification code is how to get Twitter app verify number Twitter app verifying your number Twitter app verification failed Twitter app login code text Twitter app verification code not working Twitter app sms verification error 2019 Twitter app verification failed tap to try again Twitter app verify your phone Twitter app login code text Twitter app sms verification error 2018 Twitter app verification code not on Twitter app but received login code via text message how to get Twitter app verification code Twitter app verification failed Twitter app error bypass Twitter app sms Twitter app verifying your number Twitter app, no sms verification Twitter app, login code text, how to get Twitter app verify number.

Web: Pvapins

0 notes

Text

Corporate America can't avoid one question. It's Tesla's fault

New Post has been published on https://appradab.com/corporate-america-cant-avoid-one-question-its-teslas-fault/

Corporate America can't avoid one question. It's Tesla's fault

Wall Street analysts have peppered executives at other high-profile companies about possible bitcoin forays during recent earnings conference calls.

GM (GM) CEO Mary Barra said during the automaker’s earnings presentation earlier this month that GM didn’t have any plans to buy bitcoin just yet.

“We don’t have any plans to invest in bitcoin, so full stop there,” she said in response to a question from Morgan Stanley auto analyst Adam Jonas.

But she did not rule out the possibility of customers one day being able to buy Chevrolets, Buicks or Cadilllacs with cryptocurrency — just as Tesla is planning to let customers use bitcoin to buy its electric cars and trucks.

“This is something we’ll monitor and we’ll evaluate. And if there’s strong customer demand for it in the future, there’s nothing that precludes us from doing that,” Barra added.

But executives at other companies, particularly financial corporatins, remain unconvinced that bitcoin should be part of their cash-management strategies.

“We’re not currently investing in cryptocurrency,” said Leslie Barbi, chief investment officer with Reinsurance Group of America (RGA), during an earnings conference call last week.

“My understanding is currently the accounting is different than other currencies and can create more volatility,” she added.

Volatility is a problem. The big swings in price will probably keep other major companies from putting corporate money into bitcoin.

Sure, the returns have been enormous as of late. But companies want stability from their corporate investments -— not an asset that has swung from a low of just above $4,000 to nearly $50,000 in the past year.

“We watch cryptocurrencies,” said Christine Hurtsellers, CEO of Voya Financial’s investment management unit during an earnings call. But she added that factors driving the big price swings can “still tend to be somewhat opaque at times.” That’s the reason why Voya (VOYA) won’t invest for now.

Taking the crypto plunge

Other companies are willing to embrace the risk.

So far, Tesla (TSLA) and software company MicroStrategy (MSTR) are the two most prominent firms to buy bitcoin. Payments giants Square (SQ) and PayPal (PYPL) now let customers buy and sell bitcoin (XBT) and use the cryptocurrency for e-commerce transactions. MasterCard (MA) and Bank of New York Mellon (BK) are dipping their toes in the digital currency waters too.

Twitter (TWTR), which like Square is run by Jack Dorsey, is also looking more at bitcoin and other cryptocurrencies.

“We have done a lot of the upfront thinking to consider how we might pay employees should they ask to be paid in bitcoin, how we might pay a vendor if they asked to be paid in bitcoin and whether we need to have bitcoin on our balance sheet,” said Twitter CFO Ned Segal in an interview with CNBC after the company reported earnings last week.

Visa (V) CEO Al Kelly also noted during his company’s most recent earnings call that “there’s a growing interest in digital currencies.”

But he differentiated between assets like bitcoin and so-called stable coins that are backed by existing government currencies. Kelly said that bitcoin and other crytpocurrencies are more like “digital gold.”

“They are predominantly held as assets that are not used as a form of payment in a significant way at this point,” Kelly said, adding that “fiat-backed digital currencies, including stable coins and central bank digital currencies…are an emerging payments innovation that could have the potential to be used for global commerce.”

In other words, Tesla’s purchase may lead more companies to consider buying bitcoin, but it’s not likely to create a massive groundswell of support just yet.

The biggest wild card

Some are hoping that Apple (AAPL), the world’s most valuable company, could be next. Apple could let buyers and sellers trade bitcoin, and also invest directly in the cryptocurency like Tesla is.

RBC analyst Mitch Steves said in a report earlier this month that if Apple decided to set up its own cryptocurrency exchange business (potentially through its Apple Wallet feature) then Apple “could immediately gain market share and disrupt the industry.”

Based on how much money Square derives from bitcoin-related revenue, Steves estimates that Apple could eventually generate more than $40 billion in revenue tied to bitcoin.

He also noted that Apple could fund any bitcoin exchange plans by adding about $1 billion to its balance sheet, saying that an Apple purchase of bitcoin would help validate it further and that “the price of the underlying asset would then go up in a substantial manner.”

Apple has not publicly discussed any plans to invest in bitcoin and the company did not respond to requests for comment.

0 notes

Text

TWTR Stock Price | Twitter Inc. Stock Quote (U.S.: NYSE) | MarketWatch

TWTR Stock Price | Twitter Inc. Stock Quote (U.S.: NYSE) | MarketWatch

Twitter (TWTR) Receives a Hold from Wedbush

In a report released today, Daniel Ives from Wedbush maintained a Hold rating on Twitter (TWTR – Research Report), with a price target of $50.00. The company’s shares opened today at $42.81.According to TipRanks, Ives is a…

Oct. 4, 2022 at 12:35 p.m. ET

on TipRanks.com

Source link

View On WordPress

#Twitter Inc. analyst estimates#Twitter Inc. analyst ratings#Twitter Inc. analyst recommendations#Twitter Inc. earnings estimates#TWTR#TWTR analyst estimates#TWTR analyst recommendations#TWTR earnings estimates#TWTR ratings#TWTR share estimates

0 notes

Text

Twitter Inc (NYSE: TWTR) Misses Its Earnings Estimates Despite Growth Strategy

Twitter Inc (NYSE: TWTR) missed its quarterly estimates showing that its growth plan has still not been beneficial. However, the company has stated it is on its way to achieving a $7.5 billion revenue and 315 million users by 2023. Moreover, the company expects increased user growth in the US in 2022.

Analysts expected more growth for Twitter

Analysts expected the company to achieve growth faster since it took on more significant projects such as newsletters and audio chat rooms. While Twitter gained 6 million new followers this quarter, it will have to get about 12 million each quarter to reach its goal.

According to the CEO of Twitter, Parag Agrawal, its performance allows it to improve its exception and achieve its 2023 goals. He adds that the company doesn’t intend to adjust its plans.

The company’s revenue for 2021 increased by 37% to reach $5.08 billion. It also has an operating loss of $493 million. This amount includes current investments and a one-time litigation charge of $766 million.

Additionally, Twitter's Board of Directors has approved a share buyback program of $4 billion. This program replaces the company’s 2020 share repurchase program of $2 billion. About $819 million remained from the previous program.

Twitter has also announced the testing of the video playback speed feature on the web and android. The platform’s users will watch videos from ×0.25 to ×2. Furthermore, Twitter will expand the feature to iOS users.

Affirm Holdings Inc (NASDAQ: AFRM) drops after accidental tweet

Affirm Holdings Inc (NASDAQ: AFRM) declined by 33% after releasing partial and errant financial results before the actual results, which has missed estimates. The company has missed the $100.3 million estimates that analysts sets.

The company had accidentally posted on Twitter that it was another excellent year causing their shares to start plunging. Affirm had to explain itself over Twitter when trading stopped. It also explained that its results had leaked previously due to human error.

Meanwhile, NBA fans on Twitter are reacting to the end of the Golden State Warriors winning streak after the team lost to Utah Jazz. The Warriors had won nine consecutive games before this.

Read the full article

0 notes

Photo

What to know this week

This week, second-quarter earnings season will ramp up, offering investors a fuller picture of the extent of the rebound in corporate profits as social distancing standards eased. Data on the housing market will also be in focus.

So far, companies have been topping already-elevated expectations for second-quarter results. About 8% of S&P 500 companies have reported results so far, mostly comprising banks. And of those reporting, 85% have topped estimates, according to FactSet data.

One of the most closely watched quarterly reports this week will come from Netflix (NFLX) on Tuesday. As the first of the “FAANG” names to post results, the report will set the tone for the other Big Tech companies still left to post their quarterly earnings.

Investors are nervously eyeing Netflix’s second-quarter earnings report after a sharply disappointing first quarter, during which the streaming giant added fewer than 4 million new paying subscribers versus the 6.3 million expected. At its peak during the pandemic, Netflix had added nearly 15.8 million new subscribers in a single quarter. In April, Netflix attributed the first-quarter subscriber miss to “the big COVID-19 pull forward in 2020 and a lighter content slate in the first half of this year, due to COVID-19 production delays.”

Netflix said it only expected to add 1 million new subscribers for the April through June quarter. The company added more than 10 million new paying users during the same period in 2020 when the pandemic still kept consumers mostly confined to their homes in search of entertainment.

But the slowing rate of new subscriber additions for Netflix has come alongside the maturation of the platform in major markets. With nearly 208 million global subscribers, Netflix is still the clear U.S. leader in streaming content, followed by a wide margin by Disney+ with 103.6 million subscribers. And Disney’s streaming competitor also missed estimates for new subscriber additions at the start of the year, underscoring the industry-wide slowdown following the record droves of customer sign-ups during the height of the pandemic.

Story continues

SPAIN – 2021/07/13: In this photo illustration a close-up of a hand holding a TV remote control seen displayed in front of the Netflix logo. (Photo Illustration by Thiago Prudencio/SOPA Images/LightRocket via Getty Images)

“Netflix has a considerable first-mover advantage, with nearly 210 million global subscribers. This figure, however, belies the fact that Netflix is approaching market saturation in North America, with its nearly 75 million members comprising around 60% of all households,” Wedbush analyst Michael Pachter wrote in a note.

“Its first-mover advantage will only take it so far, as it must continue to produce new content in order to retain existing subscribers, and must continue to renew licensed content in order to attract new subscribers,” he added. “Netflix’s opportunities overseas remain compelling, and we think this will support high single digit percentage user growth for the foreseeable future.”

But in terms of new content, Netflix is reportedly pushing to expand its content outside of its core television and film programming. The company said last week that it hired Mike Verdu, former Electronic Arts (EA) and Facebook-owned (FB) Oculus executive, as vice president of game development. According to a report from Bloomberg, Netflix is aiming to offer video games to users in the next year. Investors are poised to eye Netflix’s earnings report this week for more details about the strategy for the new business offering.

According to Truist Securities analyst Matthew Thornton, Netflix’s foray into gaming would be “an extension of their content strategy,” much like the streaming platform’s other recent moves into unscripted content, premium films and children’s programming.

“There is an opportunity here, at least at the margin, to differentiate the service versus some of their direct peers and help drive engagement, retention, and of course, subscriber growth and revenue growth,” Thornton told Yahoo Finance Live. “What the content strategy will be here still remains to be seen. Are they going to keep this to their own first party content only, build their own content?”

“I think, you know, the biggest opportunity, of course, would be to actually open up to third party content as well, which would put them a little more head to head and comparable to the platforms out there that are offered by Microsoft, or Sony, or Nintendo, Google, Amazon, and others,” he added.

In terms of top- and bottom-line results, Netflix is expected to deliver earnings of $3.16 per share on revenue of $7.32 billion, which would represent growth of 19% over last year.

Shares of Netflix have declined by about 1% for the year-to-date, underperforming against the S&P 500’s nearly 16% rise over the same period.

Housing data

A slew of housing market data is also due for release this week.

These will include the Commerce Department’s report on housing starts and building permits, highlighting the pace of new home construction and future construction as tight inventory levels continue to weigh on housing market activity. Housing starts are expected to rise by 1.2% month-on-month in June for a back-to-back monthly gain, albeit while slowing from May’s 3.6% monthly rise.

A drop in lumber prices after a spring surge is poised to help alleviate building costs and stoke construction. However, last week’s retail sales report showed that both furniture and building material sales dipped in June, extending May’s drop. The declines, however, may at least partially reflect drops in the actual price of building inputs like lumber, rather than or in addition to a pull-back in sales volume.

Other closely watched housing data this week will include the National Association of Realtors’ monthly existing home sales report for June. This will likely register the first monthly increase in sales since January, with sales of previously owned homes anticipated to rise by 1.7% in June, according to Bloomberg consensus data. In May, existing home sales fell by 0.9%.

“We take positive signal from the 8% surge in May pending home sales, which hit the highest level since 2005. Existing home sales dropped for the fourth consecutive month in May, partly due to the high home prices squeezing out potential buyers in the market,” Michelle Meyer, U.S. economist at Bank of America, wrote in a note on Friday. “The median price of an existing home in May marked the highest ever recorded at $350k, which was 23.6% higher compared with May 2020. That said, the inventory uptick in June and lowering lumber prices could bode well for buyers, potentially alleviating the pressure from the persistent high prices and tight inventory.”

Earnings Calendar

Monday: NAHB Housing Market Index, July (82 expected, 81 in June)

Tuesday: Housing starts, month-on-month, June (+1.2% expected, +3.6% in May); Building permits, month-on-month, June (+1.0% expected, -2.9% in May)

Wednesday: MBA Mortgage Applications, week ended July 16 (+16.0% during prior week)

Thursday: Chicago Federal Reserve National Activity index, June (0.30 expected, 0.29 in May); Initial jobless claims, week ended July 15 (350,000 expected, 360,000 during prior week); Continuing claims, week ended July 10 (3.241 million during prior week); Leading index, June (0.9% expected, 1.3% in May); Existing home sales, June (5.90 million expected, 5.80 million in May); Kansas City Federal Reserve Manufacturing Activity index, July (25 expected, 27 in June)

Friday: Markit U.S. Manufacturing PMI, July preliminary (62.0 expected, 62.1 in June); Markit U.S. Services PMI, July preliminary (64.5 expected, 64.6 in June); Markit U.S. Composite PMI, July preliminary (63.7 in June)

Economic Calendar

Monday: AutoNation (AN) before market open; IBM (IBM) after market close

Tuesday: Synchrony Financial (SYF), Philip Morris International (PM), Halliburton (HAL), Ally Financial (ALLY) before market open; Netflix (NFLX), Chipotle Mexican Grill (CMG), United Airlines (UAL) after market close

Wednesday: Anthem (ANTM), Johnson & Johnson (JNJ), Nasdaq (NDAQ), Coca-Cola (KO), Harley-Davidson (HOG), Verizon (VZ) before market open; Las Vegas Sands (LVS), Whirlpool (WHR), Texas Instruments (TXN), Equifax (EFX) after market close

Thursday: Danaher (DHR), DR Horton (DHI), AT&T (T), Newmont Corp (NEM), Dow Inc. (DOW), Abbott Laboratories (ABT), Alaska Air Group (ALK), Biogen (BIIB), American Airlines (AAL), Domino’s Pizza (DPZ), The Blackstone Group (BX), Crocs (CROX), Southwest Airlines (LUV), Union Pacific (UNP), Capital One Financial (COF), Intel Corp (INTC), Boston Beer Co (SAM), Twitter (TWTR), Snap (SNAP)

Friday: American Express (AXP), Schlumberger (SLB), Honeywell (HON), Kimberly-Clark (KMB) before market open

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Read more from Emily:

0 notes

Link

As GameStop fizzles, one hot part of the market gets even hotter What’s happening: Former San Francisco 49ers quarterback Colin Kaepernick is among the latest to get in on the trend, in which investors back “blank check” companies that then go hunting for acquisition targets. Kaepernick will serve as co-chair of Mission Advancement Corp., which is seeking to raise about $250 million to invest in socially-conscious consumer brands. “We believe a company’s clarity around its values can transform a business and rally a movement around social causes that benefits all stakeholders,” the firm said in a regulatory filing published Tuesday. Big picture: Blank check companies like Kaepernick’s have cropped up left and right over the past year, as investors — flush with cash and searching for returns, thanks to loose central bank policies — look for more creative places to park their money. Once an obscure part of the market, 229 SPACs raised $76 billion in 2020, according to Goldman Sachs. That’s up from just $13 billion in 2019. Enthusiasm has only increased in 2021. Per Goldman, SPACs raised $16 billion during the first three weeks of 2021 — and a spate of new filings since then indicates the pace isn’t letting up. Former New York Yankees star Alex Rodriguez is looking to raise about $500 million for his SPAC, Slam Corp, according to documents filed with the Securities and Exchange Commission last week. On Tuesday, Rocket Internet co-founder Oliver Samwer said his SPAC would raise $250 million for deals outside the United States. There’s more: Hedge fund Elliott Management has been meeting with bankers about potentially raising more than $1 billion via its own blank check firm, the Wall Street Journal reports. Some SPACs have already identified takeover targets. Many have been in the transportation sector. Wheels Up announced last week it would go public by merging with a SPAC in a deal that values the private aviation company at $2.1 billion. Hyzon Motors, which makes hydrogen-powered trucks, buses and coaches, announced its public market debut via a SPAC merger on Tuesday. But analysts worry there are now too many people trying to nail down a limited number of solid investment opportunities. At the end of January, Goldman warned that there were an estimated 265 SPACs with $82 billion to blow searching for acquisitions. That’s causing some hand-wringing among those watching markets for signs that sentiment is getting out of control. “In our portfolio manager conversations, the boom in SPAC issuance has often been cited as an example of exuberant investor behavior,” David Kostin, Goldman Sachs’ chief US equity strategist, recently told clients. Kostin acknowledges that SPACs have a “low opportunity cost” with US interest rates near zero. But the space is undoubtedly getting more crowded by the day, as hedge fund managers, tech bosses and athletes throw their hats in the ring. Twitter’s election policies cost it users Twitter’s efforts to tackle misleading content around the US elections hurt the platform’s business, my CNN Business colleague Kaya Yurieff reports. The company said Tuesday that it had 192 million users who can be served ads on the platform at the end of last year, up 27% from the year prior, but lower than what Wall Street analysts were expecting. In a letter to shareholders, Twitter (TWTR) said product changes around the election dented its user numbers last quarter. Remember: Ahead of November, the company introduced a number of changes to its product in an effort to clamp down on misinformation. Twitter acknowledged that some of the changes were “very effective,” while others were “less effective and, as a result, have been discontinued.” That said: The platform continued to add users even after it banned former President Donald Trump last month, bolstering Wall Street’s confidence. CEO Jack Dorsey emphasized Tuesday that Twitter “is obviously much larger than any one topic or any one account,” adding that 80% of its audience is outside the United States. Investor insight: Shares are up nearly 7% in premarket trading, and have climbed nearly 67% in the past 12 months. User growth could slow in the coming quarters, however, as the pandemic-related boost wears off. GameStop shares plunge back to Earth Shares of GameStop (GME), which captured global attention after social media hype helped drive a massive price spike, are rapidly losing steam. The latest: GameStop’s stock plunged 16% on Tuesday to $50.31. It’s now 90% below the record high of $483 reached on Jan. 28. Meanwhile, attention is shifting to regulators, who are trying to determine what, if anything, can be done. Treasury Secretary Janet Yellen has been meeting with federal officials to examine what happened and ensure “recent activities are consistent with investor protection and fair and efficient markets.” Robinhood CEO Vlad Tenev, whose company is under the microscope after it restricted GameStop trades in the middle of the melee, defended the app’s business model in a blog post Tuesday — including what’s known as “payment for order flow,” where market makers like Citadel Securities pay Robinhood to execute trades. “A handful of large firms now execute the majority of trades in financial markets. Those so-called market makers can more efficiently process trades at a narrower band of prices. Among those who benefit? The everyday investor,” Tenev wrote. It’s an issue that could come up during a virtual hearing convened by the House Financial Services Committee scheduled for next week. Rep. Maxine Waters, who chairs the committee, has not yet announced if witnesses will appear, but Politico reports that Tenev is expected to testify. Up next Coca-Cola (KO), GM (GM) and Under Armour (UA) report results before US markets open. Uber (UBER) and Zillow (Z) follow after the close. Also today: US inflation data for January posts at 8:30 a.m. ET as policymakers debate whether another round of stimulus could boost prices. Coming tomorrow: Markets in China close for the Lunar New Year holiday. Source link Orbem News #fizzles #GameStop #Hot #Hotter #investing #market #onehotpartofthemarketgetsevenhotter-CNN #Part #Premarketstocks:AsGameStopfizzles

0 notes

Text

Hard industries to learn but with moat

Chemicals

Healthcare

Financial Institutions

https://ftalphaville.ft.com/2017/01/26/2177854/the-curious-case-of-constellation-health-and-blackstones-former-top-deal-maker/

I would say you want to find industries where there is a lot of alpha available. Energy, insurance (financials in general), REITs are all very macro oriented. They depend on commodity prices and the yield curve.

I think that tech is a phenomenal choice right now. There is so much happening as we embrace the digital world. If you take a couple of months to dig deeply into AMZN, GOOGL, FB, AAPL and MSFT, you will have an overview of where society is going. Some will say that it is difficult to have a differentiated view on such well-covered companies. That may have some truth to it (although I find that there is still a decent amount of skepticism out there), but these companies spend a combined $50B+ on capex and a similar amount on COS.

Find the datacenter beneficiaries, the component suppliers, the content purveyors, whatever. There is so much emanating from the wakes of these five companies.

My votes are industrials and healthcare. You'll learn to do actual primary research, and learn how to model fixed/variable costs properly. As implausible as it sounds, those are two skills that genuinely differentiate you as an analyst. Healthcare also teaches you how to trade/invest around news flow.

Generalist analysts frequently get burned in these sectors ('industrials look cheap' - end up buying at the peak of the cycle / 'healthcare is simple' - end up buying Valeant). This increases the value of specialists.

Tech is fun, but most tech, esp. the consumer-facing stuff is just guessing TAM , penetration rates, ARPU, etc. Very difficult to build repeatable edge. Let's say you 'estimated' FB's growth correctly in the past - how does that make you a better investor in TWTR or SNAP in the future?

I will add a slightly contrarian perspective/ insight: you also want to choose a sector where you will be differentiated and competition will be relatively limited.

Tech is incredibly crowded because it is the 'obvious' choice. The products are highly visible in popular culture and the space is constantly evolving. The downside is that every schmuck thinks they can have a differentiated understanding of FANG (or is willing to try).

Add to that the fact that much of internet/ growth tech requires limited 'deep' analysis and is 'finger in the air' 'secular growth vs. secular decliner' stuff. While a lot of industrials are 'gdp +/- growth' and you focus on the rest of the model, a lot of growth tech is largely about getting the revenue growth rate correct. This kind of directional guesswork is relatively easy to do (though almost impossible to be particularly accurate at), attracting a lot of people that aren't really about that modelling stuff.

What sectors aren't easily crowded by lazy 'generalist' schmucks? Financials, healthcare, and energy - all require some significant domain expertise.

Overall though, I think I would put my vote on industrial. It's the best of both worlds - a big space that has a lot of things you interact with / understand intuitively (cars, trains, planes, houses, furniture). However, it also involves some domain knowledge asnd some serious analysis below the top line (i.e. cost structures, incremental margins and returns, etc).

Someone above also said 'try to be a generalist as long as possible.' This sounds like a good idea, but often just results in you being not quite as smart as the reserve investor across a number of fields. Its harder to pull off, but I might recommend trying to spend time specializing across multiple sectors (i.e. make at least 1 or 2 sector moves in your career)

The commentary from below on tech vs. industrials isn't as simple/complicated as people believe.

Tech is incredibly varied

Semiconductors, for example, are very similar to industrials in they are cyclical businesses with GDP+- end demand markets and very detailed focus on incremental margins, fixed/variable costs and inventory accounting.

Outside of NVDA and AMD most semis are not pie in the sky revenue growth models that are based on some intangible addressable market in the future.

Then you have software. Do you know why half of software trades at infinite earnings multiples? It's because they basically represent NPVs of recurring revenue streams and the best companies can reinvest 100% of their proceeds to get additional revenue.

Software is basically a series of present value equations based on growth, churn, pricing and incremental/decremental margins from that pricing. Generalists investors thus get destroyed in software if they are buying/shorting based on multiples on their models.

Then look at internet.

Amazon is a capex intensive businesses where there is a ton of modeling you can do on the incremental margins and capacity utilization on new fulfillment centers (on the retail side) and data centers (on the AWS side).

The best analysts on AMZN were the ones who can understand the unit economics of new data centers and how to think about the flow through of the various business lines to both gross margins and operating income.

GOOG has the same dynamic as AMZN. FB and NFLX are a little bit softer but you can definitely do in-depth work on the margin side by looking at the new engineers, cost per new engineer, and think about how the costs can truly grow with revenue based on the limited pool of demand in the valley.

Then on primary research, tech has ton of opportunities. Talk to the software resellers and partners and see how they are doing and what trends they are seeing. Talk to the fabs in Taiwan to gauge end market supply/demand. Talk to the people at AWS reinvent and Strata to figure out what is happening in the database environment.

Tech is a great space and definitely not just about clicks, eyeballs, and buzzwords like AI. Ultimately, the best part about tech is that outside of certain segments like semis, they are predominantly high quality businesses ("compounders" though I hate that phrase as it has become a catch all for everything that is 15x ebitda these days) with long-term growth opportunities. Unlike industrials, you do not need to time a cycle right to do well because over a long enough period of time your stocks typically go up because the intrinsic value of the businesses are growing and the multiples are not high enough where the multiple compression will mask the underlying growth of the businesses over a multi year holding period - as a result you see a ton of the top LT investors have big weightings in tech

My prior criticisms were meant to be somewhat contrarian and focused on a particular set of investors that has really grown in the last ~10 years. These are the 'tech' investors that only do internet/ software (dead giveaway when someone says I do 'tech', but not 'hard tech') and are not particularly thoughtful ('finger in the air' ). Even some of the sharper ones have a hard time avoiding 'VC-ization (where they start thinking of themselves as visionaries instead of analysts). Don't be one of these.

It might be cyclical (pun intended), but I've also realized as I move more into mid-career/ trying to get sector head/ PM jobs that there are a ton of TMT people out there (especially media/telecom/ internet, much less so hardware) and very few industrial. I would honestly expect that to remain the case going forward, with more analysts/ investable name (though not necessarily per unit of market cap) focused on internet and software in particular. From a headcount perspective U.S. public equities is not a growth industry, so this is important to take into account

HFs typically don’t care too much about your industry expertise because, to be frank, you don’t really have any coming out of banking.

Covering several industries is definitely more challenging, regardless of your background, but it often turns out to be better for your career in the long run. You retain optionality over time, you spot themes across spaces, you’re better suited to be a PM, and you get diversification so you can shift your focus over time as industries change in attractiveness.

TMT

Internet

Gaming

Software

Semis

Media

Telecom

0 notes

Text

As GameStop fizzles, one hot part of the market gets even hotter

New Post has been published on https://appradab.com/as-gamestop-fizzles-one-hot-part-of-the-market-gets-even-hotter/

As GameStop fizzles, one hot part of the market gets even hotter

What’s happening: Former San Francisco 49ers quarterback Colin Kaepernick is among the latest to get in on the trend, in which investors back “blank check” companies that then go hunting for acquisition targets.

Kaepernick will serve as co-chair of Mission Advancement Corp., which is seeking to raise about $250 million to invest in socially-conscious consumer brands.

“We believe a company’s clarity around its values can transform a business and rally a movement around social causes that benefits all stakeholders,” the firm said in a regulatory filing published Tuesday.

Big picture: Blank check companies like Kaepernick’s have cropped up left and right over the past year, as investors — flush with cash and searching for returns, thanks to loose central bank policies — look for more creative places to park their money.

Once an obscure part of the market, 229 SPACs raised $76 billion in 2020, according to Goldman Sachs. That’s up from just $13 billion in 2019.

Enthusiasm has only increased in 2021. Per Goldman, SPACs raised $16 billion during the first three weeks of 2021 — and a spate of new filings since then indicates the pace isn’t letting up.

Former New York Yankees star Alex Rodriguez is looking to raise about $500 million for his SPAC, Slam Corp, according to documents filed with the Securities and Exchange Commission last week. On Tuesday, Rocket Internet co-founder Oliver Samwer said his SPAC would raise $250 million for deals outside the United States.

There’s more: Hedge fund Elliott Management has been meeting with bankers about potentially raising more than $1 billion via its own blank check firm, the Wall Street Journal reports.

Some SPACs have already identified takeover targets. Many have been in the transportation sector. Wheels Up announced last week it would go public by merging with a SPAC in a deal that values the private aviation company at $2.1 billion. Hyzon Motors, which makes hydrogen-powered trucks, buses and coaches, announced its public market debut via a SPAC merger on Tuesday.

But analysts worry there are now too many people trying to nail down a limited number of solid investment opportunities. At the end of January, Goldman warned that there were an estimated 265 SPACs with $82 billion to blow searching for acquisitions.

That’s causing some hand-wringing among those watching markets for signs that sentiment is getting out of control.

“In our portfolio manager conversations, the boom in SPAC issuance has often been cited as an example of exuberant investor behavior,” David Kostin, Goldman Sachs’ chief US equity strategist, recently told clients.

Kostin acknowledges that SPACs have a “low opportunity cost” with US interest rates near zero. But the space is undoubtedly getting more crowded by the day, as hedge fund managers, tech bosses and athletes throw their hats in the ring.

Twitter’s election policies cost it users

Twitter’s efforts to tackle misleading content around the US elections hurt the platform’s business, my Appradab Business colleague Kaya Yurieff reports.

The company said Tuesday that it had 192 million users who can be served ads on the platform at the end of last year, up 27% from the year prior, but lower than what Wall Street analysts were expecting.

In a letter to shareholders, Twitter (TWTR) said product changes around the election dented its user numbers last quarter.

Remember: Ahead of November, the company introduced a number of changes to its product in an effort to clamp down on misinformation.

Twitter acknowledged that some of the changes were “very effective,” while others were “less effective and, as a result, have been discontinued.”

That said: The platform continued to add users even after it banned former President Donald Trump last month, bolstering Wall Street’s confidence.

CEO Jack Dorsey emphasized Tuesday that Twitter “is obviously much larger than any one topic or any one account,” adding that 80% of its audience is outside the United States.

Investor insight: Shares are up nearly 7% in premarket trading, and have climbed nearly 67% in the past 12 months. User growth could slow in the coming quarters, however, as the pandemic-related boost wears off.

GameStop shares plunge back to Earth

Shares of GameStop (GME), which captured global attention after social media hype helped drive a massive price spike, are rapidly losing steam.

The latest: GameStop’s stock plunged 16% on Tuesday to $50.31. It’s now 90% below the record high of $483 reached on Jan. 28.

Meanwhile, attention is shifting to regulators, who are trying to determine what, if anything, can be done. Treasury Secretary Janet Yellen has been meeting with federal officials to examine what happened and ensure “recent activities are consistent with investor protection and fair and efficient markets.”

Robinhood CEO Vlad Tenev, whose company is under the microscope after it restricted GameStop trades in the middle of the melee, defended the app’s business model in a blog post Tuesday — including what’s known as “payment for order flow,” where market makers like Citadel Securities pay Robinhood to execute trades.

“A handful of large firms now execute the majority of trades in financial markets. Those so-called market makers can more efficiently process trades at a narrower band of prices. Among those who benefit? The everyday investor,” Tenev wrote.

It’s an issue that could come up during a virtual hearing convened by the House Financial Services Committee scheduled for next week. Rep. Maxine Waters, who chairs the committee, has not yet announced if witnesses will appear, but Politico reports that Tenev is expected to testify.

Up next

Coca-Cola (KO), GM (GM) and Under Armour (UA) report results before US markets open. Uber (UBER) and Zillow (Z) follow after the close.

Also today: US inflation data for January posts at 8:30 a.m. ET as policymakers debate whether another round of stimulus could boost prices.

Coming tomorrow: Markets in China close for the Lunar New Year holiday.

0 notes

Text

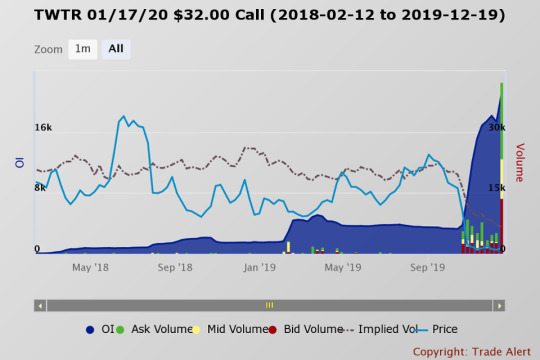

Twitter’s Stock May Catch A Short-Term Bounce

Twitter’s Inc.’s (TWTR) stock plunged following its third quarter results at the end of October. It has made 2019 a horrible year, with the shares rising by about 11%, massively underperforming the S&P 500 gain of 27.7%. The good news is that the stock may start chipping away at that wide gap, but don’t expect any rally to be long-lasting.

Some options traders are betting the stock rises to around $33 by the middle of January. Should the stock move higher as the option traders are betting, the technical chart suggests the stock could climb by almost 8%.

Betting That The Share Rise

The $32 call options that expire on January 17 saw their open interest levels climb by approximately 11,300 contracts on December 19, to a total open interest of about 30,000 contracts. As of December 19, the calls trade for around $1 per contract, and that means for a buyer of the calls to earn a profit the stock would need to rise to approximately $33 by the middle of January.

One reason why the traders may be getting bullish is that the stock is trading near a level of technical resistance at $31.90. Should the stock rise above that price, it could climb to around $34.35, or 7.7% higher than its current price of approximately $31.85. That could trigger the process of filling the gap, a technical term used to describe a hole in the chart created from the sharp plunge in the stock following the company’s third quarter earnings report. It could result in the stock rising back to where it was before the sharp decline.

Another bullish indication is that the relative strength index is now changing direction. The RSI has been trending lower since peaking at overbought levels in April when it reached 85. Currently, the RSI is rising above that downtrend. It suggests that momentum in the stock has shifted from bearish to bullish.

Earnings Outlook Plunges

But any rally in the stock isn’t likely to last. That’s because the outlook for the company hasn’t improved based on analysts' consensus estimates. Currently, analysts estimate that earnings for Twitter will plunge in 2020 by 60% to just $0.91 per share from $2.28 per share in 2019. Additionally, earnings are forecast to rise by only 21% in 2021 to $1.10 per share.

It is worth noting that one reason for the sharp decline in Twitter's earnings from 2019 to 2020, is because earnings estimates for Twitter rose sharply following the company’s better than expected second-quarter results in July. The strong second-quarter results, followed by the weak third quarter results, add one more layer of uncertainty for investors to contend with.

Given the stock’s sharp declines over the past few months, a rebound for the equity seems possible. How long that rebound last will largely depend on what happens during the company’s next quarterly results and the forward-looking guidance they provide.

You can get affordable Digital Marketing services from best SEO services in Pagosa Springs and can increase your visibility and rankings in search results.

0 notes

Photo

TWTR (NASDAQ) Twitter got Wall Street analysts attention as it said it could turn a quarterly profit for the first time ever since its IPO — despite admitting it has been overstating monthly user numbers for the past three years. The social network has never had a profitable quarter based on generally accepted accounting principles, but it said Thursday it “will likely be GAAP profitable” in the fourth quarter if it reaches the high end of its own estimates. The news sent Twitter’s stock soaring 18 percent, to $20.31. #twitter #twinning #socialmediamarketing #earnings #investment #retirement

1 note

·

View note

Last Seen Blogs

lillianuwu

♡ Lilly ♡

kpopaestheticcs

KPOP EDITS

kaia-tershowski-blog

Untitled

shelbypeake

Shelby Peake

gerardoolivaresr

Bitácora