Last Seen Blogs

fitari-f

Random Stuff

thecalculus

Thecalculus

stephy-senpai

I've had a real challenge of a day.

the-oncoming-tropical-storm

Wellcome To My Personal Tropical Hell

Text

Oilfield Chemicals Market Witnessing High Demand for ‘Inhibitors’, Finds FMI Study

Future Market Insights, in its latest report titled 'Oilfield Chemicals Market: Global Industry Analysis 2014–2018 and Forecast 2019–2029,' offers key insights and analysis of the global oilfield chemicals market. The research study conducts an in-depth analysis and provides key market insights on the oilfield chemicals market for the forecast period (2019–2029).

Based on key insights, the oilfield chemicals market is expected to experience significant demand over the forecast period due to an increase in the number of exploration activities worldwide, owing to an increase in the need for energy across the world. The global oilfield chemicals market is estimated to grow at a CAGR of nearly 4% during the forecast period.

Download sample copy of this report:

https://www.futuremarketinsights.com/reports/sample/REP-GB-1479

Crude Oil Production and Processing Consumes Voluminous Oilfield Chemicals

The increasing number of exploration projects in the countries of Europe and MEA, such as Russia, Kazakhstan, Saudi Arabia, and several others, is estimated to support the demand for oilfield chemicals. These countries have oil reserves, which, in turn, support the demand for oilfield chemicals. Furthermore, APAC is a major market owing to the establishment of new refineries to cater to the growing demand for new units in the country. In addition, the increasing demand for refinery and petrochemical products across various end-use industries is an indication for the future demand for efficient crude oil.

To fulfil the demand for crude oil products, vendors have increased their refinery capacities. Attributing to this, manufacturers of crude oil are focusing on expansions as well as on increasing investments on clean fuel. Moreover, a significant volume of oilfield chemicals is utilised in the production and processing of crude oil.

Oilfield chemical act as the backbone of the refinery sector and oil & gas exploration sector across the globe. To meet this cumulative demand, key players of the oilfield chemicals market are expanding their manufacturing and production facilities to emerging regions, such as India & China, with an aim to reduce the operational cost owing to the abundance of economical raw materials and the availability of low-cost labour and in these regions.

Download Methodology :

https://www.futuremarketinsights.com/askus/rep-gb-1479

‘Inhibitors’ to Remain Preferred Type of Oilfield Chemicals

Segmentation on the basis of product type of oilfield chemicals: The inhibitors segment is projected to lead the global oilfield chemicals market in terms of value, followed by the gas well foamers segment. In terms of growth rate, the H2S scavengers equipment segment is expected to lead the market with an approximate CAGR of 5% over the forecast period

Segmentation on the basis of application of oilfield chemicals: The drilling & completion oilfield chemicals segment is projected to lead the oilfield chemicals market by application, and accounts for high demand across the world

Segmentation on the basis of terrain type: The onshore segment is estimated to capture a higher market share over the forecast period

Profitability of Asian Markets for Oilfield Chemicals Continues to Rise

North America is a mature and prominent region with significant demand for oilfield chemicals. Asia Pacific is estimated to emerge as a profitable and high-growth region in the oilfield chemicals market. The demand for oilfield chemicals in these regions is also mainly driven by the rising oil & gas exploration activities in the region. MEA, Eastern Europe, and Latin America are also projected to be above-average growth regions in terms of volume and value, owing to the presence of already established markets in these regions. The market in the Middle East & Africa (MEA) is expected to experience moderate growth over the forecast period as it is an already established market.

Buy this report @:

https://www.futuremarketinsights.com/checkout/1479

Global Oilfield Chemicals Market: Vendors Landscape

The oilfield chemicals market is moderately fragmented owing to the presence of a large number of local and established players. The report provides details of some of the key players in the global oilfield chemicals market, such as Albemarle Corporation, Akzo Nobel N.V., DowDuPont Inc., Baker Hughes, a GE Company LLC, Halliburton Co., BASF SE, Flotek Industries, Inc., Ashland Inc., Schlumberger Limited, Solvay SA, Clariant AG, GEO Drilling Fluids, Inc. Innospec Incorporated, and Chevron Phillips Chemical Company LLC.

#Oilfield Chemicals Market#Oilfield Chemicals#Oilfield Chemicals Market 2019#Oilfield Chemicals Market Trends#Oilfield Chemicals Market Growth

2 notes

·

View notes

Text

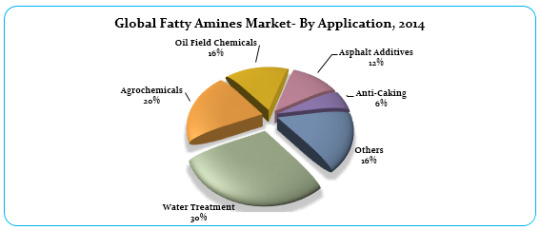

Fatty Amines Market CAGR to Grow at 4.2% During 2014 – 2020

Future Market Insights (FMI) announces the release of its latest report titled, “Fatty Amines Market: Global Industry Analysis and Opportunity Assessment 2015-2020”. According to the report, the global fatty amines market was valued at US$ 1,721 Mn in 2014 and is anticipated to reach US$ 2,193 Mn by 2020, registering a compound annual growth rate (CAGR) of 4.2% through the forecast period.

Fatty Amines Market Driven by Booming Water Treatment Chemicals Industry & Demand for Agro-chemicals

Global fatty amines market is driven by growing water treatment chemicals industry and increasing demand for agro-chemicals and asphalt additives, mainly in the developing countries. Water treatment chemicals contribute the highest in terms of demand and share to the global fatty amines market, as compared to the other application segments. Increasing usage of fatty amines in various end-user applications coupled with market expansion and development of novel applications, such as detergents, mining, paints & coatings and fabric softener are further driving the fatty amines market growth. However, fluctuations in availability and volatile raw material prices pose a challenge for the global fatty amines market.

Market Segments: The global fatty amines market is segmented on the basis of product type, application and geography.

By product type, global fatty amines market is segmented into primary fatty amines, secondary fatty amines and tertiary fatty amines. Among these segments, tertiary fatty amines accounted for approximately 48.1% of global value market share in 2014. Furthermore, it is expected to dominate the global fatty amines market throughout the forecast period, exhibiting a CAGR of 3.6% between 2015 and 2020.

Get More Information@ https://www.futuremarketinsights.com/reports/fatty-amines-market

The primary fatty amines market accounted for over 25% of the market value share in 2014 and is expected to increase at a comparatively high CAGR of 4.9%, during the forecast period, owing to its increasing consumption in water treatment chemicals and paints & coatings industry as additives to protect the paints from getting tainted while in storage.

The secondary fatty amines segment accounted for approximately 23% of the global value market share in 2014, and is expected to gain its market share and account for 23.3% of the global fatty amines market by 2020.

On the bases of application, the global fatty amines market is segmented into water treatment chemicals, agro-chemicals, oilfield chemicals, asphalt additives, anti-caking and others (used in personal care, mining, fabric softener, paints & coatings). Among the aforementioned segments, water treatment chemicals is expected to dominate the global fatty amines market with over 29% market revenue share throughout the forecast period. Growing paints & coatings industry, coupled with increasing automobile production in China, Malaysia, Indonesia and Mexico is expected to further propel the demand for fatty amines in the asphalt additives application segment. The scope of applications for fatty amines in others segment is expected to expand in the future too, due to market expansion and innovation in techniques.

On the bases of region, Asia Pacific Excluding Japan (APEJ) dominated the global fatty amines market in 2014, in terms of revenue, accounting for more than 25% of the revenue share. However, North America and Eastern Europe are foreseen to witness relatively high CAGRs of 6.4% and 5.3%, respectively.

Request Sample Pages@ https://www.futuremarketinsights.com/reports/sample/rep-gb-361

Competitive Landscape

Key players considered in the global fatty amines market include Kao Corporation, Evonik Industries AG, AkzoNobel N.V., DuPont, Clariant AG, CECA Arkema Group, Sigma-Aldrich Corporation, Volant-Chem Group, Procter & Gamble Chemicals Company and Lonza.

3 notes

·

View notes

Text

Fatty Amines Market Poised to Hit US$ 2,193 Mn by 2020

Future Market Insights (FMI) announces the release of its latest report titled, “Fatty Amines Market: Global Industry Analysis and Opportunity Assessment 2015-2020”. According to the report, the global fatty amines market was valued at US$ 1,721 Mn in 2014 and is anticipated to reach US$ 2,193 Mn by 2020, registering a compound annual growth rate (CAGR) of 4.2% through the forecast period.

Fatty Amines Market Driven by Booming Water Treatment Chemicals Industry & Demand for Agro-chemicals

Global fatty amines market is driven by growing water treatment chemicals industry and increasing demand for agro-chemicals and asphalt additives, mainly in the developing countries. Water treatment chemicals contribute the highest in terms of demand and share to the global fatty amines market, as compared to the other application segments. Increasing usage of fatty amines in various end-user applications coupled with market expansion and development of novel applications, such as detergents, mining, paints & coatings and fabric softener are further driving the fatty amines market growth. However, fluctuations in availability and volatile raw material prices pose a challenge for the global fatty amines market.

Market Segments

The global fatty amines market is segmented on the basis of product type, application and geography.

By product type, global fatty amines market is segmented into primary fatty amines, secondary fatty amines and tertiary fatty amines. Among these segments, tertiary fatty amines accounted for approximately 48.1% of global value market share in 2014. Furthermore, it is expected to dominate the global fatty amines market throughout the forecast period, exhibiting a CAGR of 3.6% between 2015 and 2020.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-361

The primary fatty amines market accounted for over 25% of the market value share in 2014 and is expected to increase at a comparatively high CAGR of 4.9%, during the forecast period, owing to its increasing consumption in water treatment chemicals and paints & coatings industry as additives to protect the paints from getting tainted while in storage.

The secondary fatty amines segment accounted for approximately 23% of the global value market share in 2014, and is expected to gain its market share and account for 23.3% of the global fatty amines market by 2020.

On the bases of application, the global fatty amines market is segmented into water treatment chemicals, agro-chemicals, oilfield chemicals, asphalt additives, anti-caking and others (used in personal care, mining, fabric softener, paints & coatings). Among the aforementioned segments, water treatment chemicals is expected to dominate the global fatty amines market with over 29% market revenue share throughout the forecast period. Growing paints & coatings industry, coupled with increasing automobile production in China, Malaysia, Indonesia and Mexico is expected to further propel the demand for fatty amines in the asphalt additives application segment. The scope of applications for fatty amines in others segment is expected to expand in the future too, due to market expansion and innovation in techniques.

On the bases of region, Asia Pacific Excluding Japan (APEJ) dominated the global fatty amines market in 2014, in terms of revenue, accounting for more than 25% of the revenue share. However, North America and Eastern Europe are foreseen to witness relatively high CAGRs of 6.4% and 5.3%, respectively.

Need More Information about Report Methodology@ https://www.futuremarketinsights.com/askus/rep-gb-361

Competitive Landscape

Key players considered in the global fatty amines market include Kao Corporation, Evonik Industries AG, AkzoNobel N.V., DuPont, Clariant AG, CECA Arkema Group, Sigma-Aldrich Corporation, Volant-Chem Group, Procter & Gamble Chemicals Company and Lonza

#Fatty Amines Market#Fatty Amines Market Trend#Fatty Amines Market Growth#Fatty Amines#Fatty Amines Demand#Chemicals

0 notes

Text

Synthetic Camphor Market Estimated to Exhibit 5.9% CAGR through 2028

According to the latest Future Market Insights (FMI) report, the volume sales of synthetic camphor are likely to exceed 36 thousand tons in 2019. Pharmaceutical industry has been a leading end-user of synthetic camphor, upheld by ongoing research activities on extending application scope of synthetic camphor in medicinal formulations.

Pharma-grade synthetic camphor is extensively used in various topical analgesic products such as ointments, oils, gels, and chest-rubs. These pharma-grade synthetic camphor for topical pain management products are witnessing significant demand owing to consumer preference for self-medication, undergird by enhanced and easy accessibility of OTC products. According to the report, pharma-grade synthetic camphor is projected to account for more than 50% volume share in 2019 in the synthetic camphor market.

Pharma-grade synthetic camphor sales are also significantly driven by growing demand for private-labelled camphorated medical products. For example, private labelled analgesic products have gained increased popularity in the US, as they are devoid of FDA approval, and witness strong promotion from retailer businesses.

A key factor restricting adoption is regulations on the use of synthetic camphor in pharmaceutical products, such as the US FDA’s classification of certain camphorated oil products would require patients to hold doctor’s prescription for consumption. Moreover, rising costs of raw materials such as turpentine oil is emerging as a key concern for manufacturers producing pharma-grade synthetic camphor.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-8704

Gains Remain Strong from Synthetic Camphor Sales in Plasticizer Production

Synthetic camphor continues to witness robust adoption in plasticizer production, which prevails as a critical component for paint and coating formulations. Additionally, demand for plasticizers in PVC and cellulose fiber production, has significantly underpinned sales of synthetic camphor. The study estimates sales of synthetic camphor in plasticizer production to surpass 13 thousand tons in 2019.

Rise in the construction sector, along with increasing demand for renovation and maintenance of existing structures, continues to drive demand for plasticizers in flooring and wall covering applications. Additionally, remarkable demand for plasticizers in flexible Polyvinyl Chloride (PVC) manufacturing, and to soften plastics used in wall covering and flooring, will remain a key sales determinant of synthetic camphor.

East Asia to Hold Pole Position in Synthetic Camphor Market

According to the FMI report, East Asia is likely to remain lucrative in the synthetic camphor market. In East Asia, China is expected to account for the highest sales of synthetic camphor, surpassing 12 thousand tons in 2019. Owing to the presence of a large number of pharma-grade synthetic camphor manufacturers in China, the country is witnessing the growing demand for synthetic camphor.

Growing overseas demand for synthetic camphor and significant growth in Chinese gum turpentine industry are the key factors influencing the market growth in the country. Additionally, with the development of Chinese gum turpentine derivatives such as synthetic camphor and synthetic borneol, overseas companies are eyeing use of these derivatives over gum turpentine.

Majority of the pharma-grade synthetic camphor manufacturers are concentrated in China and India, exporting their products to Europe and the US. Due to the availability of raw materials and synthetic camphor on a large scale in China and India, global manufacturers of camphor and other related chemical are focusing on expanding their businesses in East Asia.

Need More Information about Report Methodology@ https://www.futuremarketinsights.com/askus/rep-gb-8704

The FMI report also tracks the synthetic camphor market for the forecast period 2018 to 2028. According to the report, volume sales of synthetic camphor is likely to register 3.0% CAGR through 2028.

0 notes

Text

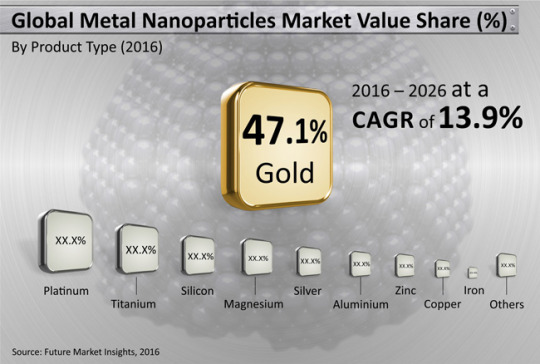

Metal & Metal Oxide Nanoparticles Market is Anticipated to Reach a Value US$ 8,000 Mn by 2026

Frontiers of nanotechnology continue to span across the globe and among diversified industrial verticals. Nanoparticles of various elements are gaining competence as crucial industrial constituents, and are witnessing a considerable rise in their applications. Future Market Insights’ recent study explores the market for nanoparticles of metals and metal oxides, and projects that application of such nanoparticles will gain traction duet to their ground-breaking properties.

According to Future Market Insights

High physical, chemical and surface properties of metal and metal oxide nanoparticles will fuel their applicability as effective bulk materials

Metal and metal oxide nanoparticles will also play an instrumental role in manufacturing of innovative products offered in the global consumer electronics industry

Versatile applicability of metal and metal oxide nanoparticles will also witness higher adoption for drugmakers and medical device manufacturers

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-508

According to the report, titled “Metal & Metal Oxide Nanoparticles Market: Global Industry Analysis and Opportunity Assessment, 2016-2026,” the demand for metal nanoparticles is projected to remain significantly higher than that of metal oxide nanoparticles. The global market for metal nanoparticles is presently valued at US$ 13.7 Bn, and will soar at 13.9% CAGR to surpass US$ 50 Bn mark by the end of 2026. During this ten-year forecast period, the US$ 1.8 Bn global market for metal oxide nanoparticle will also surge robustly at 10.4% CAGR, and will procure over US$ 5 Bn revenues towards the end of period. This clearly indicates that by the end of 2026, the global metal nanoparticles market will be worth ten times the projected value for global metal oxide nanoparticles market. Collectively, the global market for metal and metal oxide nanoparticles are bound to soar at more than 10% CAGR throughout the forecast period.

The report reveals that the demand for metal and metal oxide nanoparticles will remain considerably high in three regions – North America, Western Europe and the Asia-Pacific excluding Japan region. Towards the end of 2026, North America will dominate the global metal nanoparticles market with 30% share, while Europe will be at the forefront of global metal oxide nanoparticles market. Companies such as Meliorum Technologies, Inc., Nanostructured & Amorphous Materials Inc., American Elements, SHOWA DENKO KK, and Tekna Systemes Plasma Inc. are recognised as key manufacturers of metal and metal oxide nanoparticles in the world. Other leading participants in the global metal and metal oxide nanoparticles market include US Research & Nanomaterials Inc., Nanoshel LLC, Nanophase Technologies Corporation, Sigma-Aldrich Co. LLC and NanoComposix Inc.

Need more Information about Report Methodology@ https://www.futuremarketinsights.com/askus/rep-gb-508

The report further reveals that personal care & cosmetics industry will remain as the most lucrative end-user of metal and metal oxide nanoparticles. With over one-third revenues share for both, metal and metal oxide nanoparticles, personal care & cosmetic applications will be demanding greater use of such materials. Moreover, the demand for metal nanoparticles will also be high in defence sector, while metal oxide nanoparticles will gain traction in production of electrical and electronic products. Based on research findings, the report also estimates that by the end of 2026, nearly 50% of global metal nanoparticle revenues will be accounted by sales of iron nanoparticles. On the other hand, global revenues emanating from sales of zinc oxide nanoparticles will surge at 11% CAGR.

0 notes

Text

Global Dielectric Gases Market Key Drivers and Trend Analysis

Extensively utilized as insulating media in switchgears, gas insulated lines, transformers, and other high voltage transmission units, dielectric gases continue to witness significant demand owing to consistently surging electricity consumption worldwide. Future Market Insights, in a new research report on the global dielectric gases market, forecasts a robust revenue growth outlook for market over upcoming years. The dielectric gases marketplace will however reportedly remain a high growth-low value landscape, as indicated by the report.

Regional outlook analysis of the global dielectric gases market reveals dominance of European landscape owing to a strong manufacturing base created by a majority of leading global brands in the dielectric gases landscape. Asia Pacific, with a current market value share of over 55%, is however projected to reflect a highly lucrative growth outlook for penetration of dielectric gases in coming years, as indicated by the report.

Growth of Residential & Commercial Sectors Favoring Dielectric Gases Market

The rapidly thriving industrial sector that roughly consumes around 55% of the total generated electricity is slated to create multiple investment opportunities for suppliers of dielectric gases. Soaring demand for medium voltage substations to cater to a growing number of IT establishments, telecom organizations, manufacturing verticals, and data storage banks is foreseen to present attractive windows of opportunities to dielectric gas manufacturers at a global level.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-8514

Expanding residential and commercial construction sectors and subsequently rising installations of IT & telecommunication infrastructure, HVAC units, office equipment, and a wide range of civic utilities are accounting for surging per unit consumption of electricity. This is reportedly driving consumption of dielectric gases at a global level, as a majority of application areas continue to opt for dielectric gases as a preferred insulating medium over others.

Critical Demand for SF6 Substitutes to Create Opportunities for Fluoroketones & Fluoronitriles

Among dry air, SF6, nitrogen, fluoroketones, and fluoronitriles, consumption of SF6 currently accounts for maximum share in the global revenue represented by dielectric gases market. “Although SF6 is slated to remain the largest market shareholder in coming years owing to superior functional attributes, the fact that it is one of the key greenhouse gases and has substantial atmospheric lifetime as well as the global warming potential is making room for potential alternatives to SF6, which are relatively less popular in the dielectric gases landscape,” says a senior research analyst at the company.Fluoroketones and fluoronitriles are thus projected to encounter high adoption opportunities in the near future, says the report.

Leading manufacturers of dielectric gases are currently concentrating on R&D of SF substitutes. 3M, pioneering the way, has already been working on the development of an alternative SF6 technology. Though the substitute technology by 3M is currently in the pipeline and is likely to take time for complete commercialization, the dielectric gases market is foreseen to witness more such developments in coming years – creating a new trend wave in global dielectric gases space.

3M Company has been working in collaboration with ABB and GE, for the development of this product, i.e. Novec. The collaborative effort led to introduction of a high potential alternative to SF6 technology, in addition to technology exchange that has added value to the global landscape.

Request to Browse Report Customization@ https://www.futuremarketinsights.com/askus/rep-gb-8514

Besides 3M Company, General Electric Company, and ABB Inc., the report profiles several other prominent companies competing in global marketplace. Some of the players covered in report include Solvay S.A., Messer Group, The Linde Group, SHOWA DENKO K.K., Matheson Tri-Gas, Inc., Kanto Denka Kogyo Co., Ltd., and KPL International Limited.

0 notes

Text

Global Metal Nanoparticles Market is Anticipated to Increase to Nearly US$ 51,000 Mn by 2026 End

Frontiers of nanotechnology continue to span across the globe and among diversified industrial verticals. Nanoparticles of various elements are gaining competence as crucial industrial constituents, and are witnessing a considerable rise in their applications. Future Market Insights’ recent study explores the market for nanoparticles of metals and metal oxides, and projects that application of such nanoparticles will gain traction duet to their ground-breaking properties.

High physical, chemical and surface properties of metal and metal oxide nanoparticles will fuel their applicability as effective bulk materials

Metal and metal oxide nanoparticles will also play an instrumental role in manufacturing of innovative products offered in the global consumer electronics industry

Versatile applicability of metal and metal oxide nanoparticles will also witness higher adoption for drugmakers and medical device manufacturers

According to the report, titled “Metal & Metal Oxide Nanoparticles Market: Global Industry Analysis and Opportunity Assessment, 2016-2026,” the demand for metal nanoparticles is projected to remain significantly higher than that of metal oxide nanoparticles. The global market for metal nanoparticles is presently valued at US$ 13.7 Bn, and will soar at 13.9% CAGR to surpass US$ 50 Bn mark by the end of 2026. During this ten-year forecast period, the US$ 1.8 Bn global market for metal oxide nanoparticle will also surge robustly at 10.4% CAGR, and will procure over US$ 5 Bn revenues towards the end of period. This clearly indicates that by the end of 2026, the global metal nanoparticles market will be worth ten times the projected value for global metal oxide nanoparticles market. Collectively, the global market for metal and metal oxide nanoparticles are bound to soar at more than 10% CAGR throughout the forecast period.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb-508

The report reveals that the demand for metal and metal oxide nanoparticles will remain considerably high in three regions – North America, Western Europe and the Asia-Pacific excluding Japan region. Towards the end of 2026, North America will dominate the global metal nanoparticles market with 30% share, while Europe will be at the forefront of global metal oxide nanoparticles market. Companies such as Meliorum Technologies, Inc., Nanostructured & Amorphous Materials Inc., American Elements, SHOWA DENKO KK, and Tekna Systemes Plasma Inc. are recognised as key manufacturers of metal and metal oxide nanoparticles in the world. Other leading participants in the global metal and metal oxide nanoparticles market include US Research & Nanomaterials Inc., Nanoshel LLC, Nanophase Technologies Corporation, Sigma-Aldrich Co. LLC and NanoComposix Inc.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-508

The report further reveals that personal care & cosmetics industry will remain as the most lucrative end-user of metal and metal oxide nanoparticles. With over one-third revenues share for both, metal and metal oxide nanoparticles, personal care & cosmetic applications will be demanding greater use of such materials. Moreover, the demand for metal nanoparticles will also be high in defence sector, while metal oxide nanoparticles will gain traction in production of electrical and electronic products. Based on research findings, the report also estimates that by the end of 2026, nearly 50% of global metal nanoparticle revenues will be accounted by sales of iron nanoparticles. On the other hand, global revenues emanating from sales of zinc oxide nanoparticles will surge at 11% CAGR.

0 notes

Text

Utilization of Bamboos in Production of Beverages will be Boosting the Global Bamboo Sales during 2017-2027

Through innovative technologies, specific species of bamboos have gained applicability in production of beverages, which include popular drinks such as beers and teas. In Latin America, demand for bamboos is rising on the account of such breakthrough applications. Bamboos are no longer restrained to the image of being key resources and raw materials in paper-making and construction & building industry. Cultivation of bamboos is easy and quite profitable, grabbing the interests of agriculturists and farmers. Surplus availability of bamboos is promoting their use in such novel applications. Future Market Insights projects that towards the end of 2027, over 63,000 KT of bamboos will be sold across the globe, bringing in revenues worth over US$ 10 Bn.

According to the recently-published report, global market for bamboos is expected to be valued at US$ 3.6 Bn by the end of 2017. During the forecast period 2017-2027, the global bamboos market is projected to soar at a value CAGR of 10.6%. In terms of volume, the market is slated to record global sales of more than 24,000 KT by the end of 2017, and will reflect a 10.1% CAGR over the assessment period.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb-347

Contribution of Asia-Pacific to Global Bamboo Market

China and India are expected to continue their dominance in the global bamboos market through 2027. These Asia-Pacific countries will continue to account for about 50% resources of bamboos and their species in the world. Consequently, Asia-Pacific is expected to be the largest bamboos market in the world, both in terms of value as well as volume. Over the forecast period, the Asia-Pacific bamboos market will reflect speedy growth at 11.8% CAGR. By the end of 2027, nearly three-fourth of global bamboo revenues will be accounted by the region.

New Applications of Bamboos = Unbounded Growth Opportunities

Owing to their abundance and versatility, bamboos and bamboo-based products are used for a wide range of indoor & outdoor applications. Being a highly renewable resources in every context, bamboos have more than 1,500 recorded uses. Food production, pulp and paper, wood substitute, handicrafts, cottage industries, medicinal products, and charcoal production are some prominent applications of bamboos that have influenced the market's rampant growth.

Request Sample Report @ https://www.futuremarketinsights.com/reports/sample/rep-gb-347

The lightness, durability and tensile strength of bamboos have made them an excellent industrial raw material. Some companies are focusing towards manufacturing low-cost bicycles out of bamboos. However, expensive labour force in harvesting & procurement of bamboo is slated to restrain the market’s growth. Seasonal employment in primary processing of bamboos is also refraining manufacturers from capacity expansion. The basic application of bamboos – production of paper and pulp, however, continues to drive the global bamboo sales rapidly. By 2027, close to 48% of global bamboo market value will be accounted by end-use of bamboos in paper & pulp industry.

Majority of key players in the global bamboo market are based in Asia-Pacific region. These include companies such as Bamboo Village Company Limited, Kerala State Bamboo Corporation Ltd, Jiangxi Feiyu Industry Co. Ltd., ANJI TIANZHEN BAMBOO FLOORING CO. LTD, Dasso Industrial Group Co., Ltd, Xingli Bamboo Products Company, China Bambro Textile Company Limited, Bamboo Bio Composites Sdn Bhd, Fujian Jianou Huayu Bamboo Industry Co., Ltd., Jiangxi Shanyou Industry Co. Ltd., Tengda Bamboo-Wood Co., Ltd., and Jiangxi Kangda Bamboo Ware Group Co., Ltd. Other prominent market participants include Teragren LLC, Moso International B.V., Bamboo Australia Pty Ltd., EcoPlanet Bamboo, Smith & Fong Co Inc., Southern Bamboo Inc., and Higuera Hardwoods LLC..

Ask for Customization @ https://www.futuremarketinsights.com/customization-available/rep-gb-347

0 notes

Text

Flexible Glass Market Top Global Key Players Asahi Glass Co., Ltd., Corning Inc., Schott AG and Nippon Electric Glass Company Ltd

Future Market Insights (FMI) announces the release of its latest report titled, “Asia Pacific Flexible Glass, Market Opportunity; 2014 to 2020 Forecast." According to the report, the Asia Pacific flexible glass market is expected to account for $612.7 Mn by 2020, registering a CAGR of 36.5% during the forecast period. Incorporation of flexibility threshold in displays is expected to contribute to the growth of the Asia Pacific flexible glass market over the forecast period.

In terms of application, global flexible glass market is mainly segmented into display and solar PV (photovoltaic). Currently, display application segment dominates the Asia Pacific flexible glass market. The display segment was valued at US$ 74.2 Mn in 2013, and is expected to reach US$ 417.3 Mn by 2020, exhibiting a CAGR of 33.4% for the forecast period. Moreover, the development of Roll2Roll process is expected to create a demand for flexible glass in solar PV application. As a result, solar PV is projected to be the fastest growing application segment for the forecast period.

The display application is further sub-segmented as smartphones and tablets, curved TV, building mounted displays and, wearables. Among all the aforementioned sub-segments, smartphones & tablets segment is expected to dominate the market with 50.1% of the total revenue share by 2020. However, curved TV is anticipated to exhibit the highest CAGR of 37.1% during the forecast period. Additionally, influx of new entrants is predicted to fuel the growth of curved TV application segment over the forecast period.

Country-wise, the Asia Pacific flexible glass market is segmented into Japan, China, South Korea and others. Japan is the most lucrative market, followed by South Korea and China. Moreover, Japan is expected to contribute 40.0% market share to the Asia Pacific flexible glass market by 2020. The growth of South Korea market is supported by the strong presence of smartphone & TV manufacturers along with growing number of R&D centres in South Korea.

Assessing the various factors driving this market, FMI lead analyst, Abhishek S. said, “Incorporation of flexibility threshold in displays, development of Roll2Roll process for flexible PV and growing R&D investments in flexible glass by key glass manufacturers are expected to fuel the demand for Asia Pacific flexible glass market.”

To Know More About global flexible glass market@ https://www.futuremarketinsights.com/reports/sample/rep-gb--60

Key players in the Asia Pacific flexible glass market are Asahi Glass Co., Ltd., Corning Inc., Schott AG and Nippon Electric Glass Company Ltd.

0 notes

Text

Textile Chemicals Market by Applications(apparels, home furnishings and others), by Process Types(pre-treatment, dyeing, finishing and others) 2014 - 2020

Future Market Insights (FMI), in its recent report titled, “Asia Textile Chemicals Market Analysis & Opportunity Assessment, 2014 - 2020”, projects that the market for textile chemicals in Asia will exhibit a steady CAGR of 7.6% during 2014 to 2020. According to FMI’s in-depth analysis of textile chemicals market in Asia, the Asia textile chemicals market will reach US$ 11,626 Mn by 2020.

Textile chemicals are class of specialty chemicals and comprise chemicals and intermediates that are used in various stages of textile processing such as preparation, dyeing, printing and finishing. These are often used to enhance or impart desired properties and colour to the fabrics during the manufacturing process. As of 2014, textile chemicals accounted for nearly 2% of the overall specialty chemicals market.

FMI’s report analyses the Asia textile chemicals market in terms of market value (US$ Mn) on the basis of product types, end use applications and countries of Asia region.

The major players in textile industry across the globe are emphasising on channelising efforts towards ensuring sustainability throughout the value chain. As such, there is an ever increasing demand for eco-friendly chemicals that minimise the amount of water and energy required in various stages of textile processing and are in compliance with regional and international regulations. Textile chemicals industry is highly fragmented and comprises large number of small and big players catering to the demands of textile manufacturers. Due to this fragmented nature, developing innovative and differentiated product offerings has emerged as a key to gain competitive advantage. Moreover, growth in demand for functional finishes has resulted in a steady growth of textile finishing chemicals that impart desired specific finishes to textile and apparels.

From regional perspective, China accounted for a major share in overall Asia textile chemicals market in 2014. China textile chemicals market is expected to exhibit a CAGR of 8.6% during the forecast period 2014─2020. In terms of market value, India is the second largest market for textile chemicals in Asia. India textile chemicals market is expected to witness a steady growth at a CAGR of 9.0% in the same period. Countries like Vietnam, Bangladesh, and Indonesia also are expected to witness relatively high growth in textile chemicals market.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-as-434

From product type perspective, market size of textile auxiliaries segment is expected to grow faster than the textile colourants segment. The segments are projected to witness high single-digit growth during the forecast period.

From the process perspective, the finishing process segment is slated to experience faster growth than that of pre-treatment, dyeing and others segments. It is expected to register a CAGR of 8.6% between 2014 - 2020. This is primarily due to growth in demand for textiles and apparels with specific functional finishes.

From applications perspective, market is composed of apparels segment, home furnishings segment and others (technical & smart textiles) segment. The apparels segment accounts for largest share among these segments and is slated to register a CAGR of 6.8% during forecast period.

The key market participants covered in the report include companies covered in the report are Huntsman Corporation, Archroma and DyStar group.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-as-434

#Asia Textile Chemicals Market Textile Chemicals Market Textile Chemicals Trend Textile Chemicals Market Size Textile Chemicals Market Share#Asia Textile Chemicals Market#Textile Chemicals Market#Textile Chemicals Trend

0 notes

Text

Asia Pacific Flexible Glass Market to Witness 36.5% CAGR from 2014 to 2020

Future Market Insights (FMI) announces the release of its latest report titled, “Asia Pacific Flexible Glass, Market Opportunity; 2014 to 2020 Forecast." According to the report, the Asia Pacific flexible glass market is expected to account for $612.7 Mn by 2020, registering a CAGR of 36.5% during the forecast period. Incorporation of flexibility threshold in displays is expected to contribute to the growth of the Asia Pacific flexible glass market over the forecast period.

In terms of application, Asia Pacific flexible glass market is mainly segmented into display and solar PV (photovoltaic). Currently, display application segment dominates the Asia Pacific flexible glass market. The display segment was valued at US$ 74.2 Mn in 2013, and is expected to reach US$ 417.3 Mn by 2020, exhibiting a CAGR of 33.4% for the forecast period. Moreover, the development of Roll2Roll process is expected to create a demand for flexible glass in solar PV application. As a result, solar PV is projected to be the fastest growing application segment for the forecast period.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb--60

The display application is further sub-segmented as smartphones and tablets, curved TV, building mounted displays and, wearables. Among all the aforementioned sub-segments, smartphones & tablets segment is expected to dominate the market with 50.1% of the total revenue share by 2020. However, curved TV is anticipated to exhibit the highest CAGR of 37.1% during the forecast period. Additionally, influx of new entrants is predicted to fuel the growth of curved TV application segment over the forecast period.

Country-wise, the Asia Pacific flexible glass market is segmented into Japan, China, South Korea and others. Japan is the most lucrative market, followed by South Korea and China. Moreover, Japan is expected to contribute 40.0% market share to the Asia Pacific flexible glass market by 2020. The growth of South Korea market is supported by the strong presence of smartphone & TV manufacturers along with growing number of R&D centres in South Korea.

Get Full Report Now @ https://www.futuremarketinsights.com/checkout/60

Assessing the various factors driving this market, FMI lead analyst, Abhishek S. said, “Incorporation of flexibility threshold in displays, development of Roll2Roll process for flexible PV and growing R&D investments in flexible glass by key glass manufacturers are expected to fuel the demand for Asia Pacific flexible glass market.”

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb--60

Key players in the Asia Pacific flexible glass market are Asahi Glass Co., Ltd., Corning Inc., Schott AG and Nippon Electric Glass Company Ltd.

0 notes

Text

Ion Exchange Resins Market Worth US$ 1,830 Mn by 2026

While the global scenario of the ion exchange resins market reflecting the increasing use of ion exchange resins in power generation, followed by domestic wastewater treatment applications, the ion exchange resins market is subjected to a crunch due to the advent of alternative technologies that include electro deionization and reverse osmosis. The exceeding efficiency and advancement in technology are the major reasons why consumer preferences are shifting from conventional ion exchange resins towards these new alternatives.

Ion Exchange Resins Market to register moderate growth owing to changing preferences

This shift of preference is projected to affect the ion exchange resins market adversely and further deteriorate the pace of expansion of ion exchange resins market. Owing to this scenario, the ion exchange resins market is expected to project a moderate growth with a CAGR of 5.4% over the forecast period of 2016 to 2026. Apart from its wide utility in water treatment and various other industrial applications, the ion exchange resins account for certain drawbacks including chlorine contamination and organic contamination of resins. These factors are likely to foster the shift of consumer preference towards other alternatives available in the market. Owing to these factors the accumulation of spent ion exchange resins and their disposal is being governed by regulations to ensure that they cause no potential harm. Despite the shortcomings, the ion exchange resins market is expected to be valued at over US$ 1,830 million by 2026-end.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb-1001

Stringent regulations towards water conservation and the decreasing availability of fresh water is expected to drive the growth of the ion exchange resins market. Agencies such as Environmental Protection Agency (US) and India Water Works Association (India) are seen framing the regulations for water disposal. These actions towards water conservation and treatment are expected to fuel the demand for ion exchange resins across the globe. Water treatment process is, therefore, expected to be the major factors influencing the growth of ion exchange resins market.

Based on region, the APEJ region is projected to account for a comparatively high-value share and witness a CAGR of 7.0% over the period of forecast. In terms of volume, China is projected to dominate the ion exchange resins consumption in the APEJ region, whereas India is anticipated to witness comparatively faster growth during the forecast period. The factors influencing this market scenario are related to the growing demand for ultra-pure water in the Asian regions, especially China on account of the increasing number of power plants. As ultra-pure water is obtained by using ion exchange resins, several players in the ion exchange resins market offer resins exclusively for the power, pharmaceuticals, and electrical industries to produce ultra-pure water.

Key Developments to trigger the demand for ion exchange resins

Industry players are expected to synergize efforts towards the development of distinct and product offerings tailored for specific applications. Key players of the ion exchange resins market such as Dow Chemicals and Lanxess have indulged in differentiation strategies by emphasizing on novel products to cater to the requirements of a comparatively niche market. On account of this, Dow Chemicals introduced their next-gen Dowex marathon ion exchange resins that are re-engineered to enhance the efficiency of water treatment processes.

Ion Exchange India Ltd. provides water treatment services, predominantly in India, followed by a range of products and recycling plants for water treatment and wastewater treatment. The company has opted for a joint venture with Safic, a South-African based company for strengthening its global footprints, followed by which they marketed the water treatment equipment and chemical and resins products throughout the South-African region. Furthermore, their constant actions for expanding in the Middle-East and Africa (MEA) region are supported by their chemical blending unit in Bahrain for increasing revenue and strengthening its market share.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-1001

Ion exchange resins market participants are investing in extended research and development to cope up with the prompt application of ion exchange resins in various industries including the nuclear power generation industries that have showcased unmatched growth.

0 notes

Text

Emerging Trend in Global Germany Acid Proof Lining Market and Key Players Analysis 2016-2026

The need for protecting industrial surfaces exposed to corrosive chemicals will continue to influence the demand for acid proof lining in Germany. In 2016, the acid proof lining market in Germany is expected to reach market value of US$ 4,296.2 Mn, at a y-o-y growth of 5.1% over 2015. The rising incidences of industrial equipment damages owing to the mechanical abrasion is also anticipated to drive the demand for acid proof linings in Germany.

The industrial use of acid proof lining in coating the floor tiles of various manufacturing units is expected to fuel the growth of Germany’s acid proof lining market. The rising necessity of providing durable solutions to industrial infrastructure is observed as a key driver for the growth of the Germany acid proof lining market. Furthermore, the mounting private equity investments will continue to boost the growth of the Germany acid proof lining market. However, the high costs of veneering industrial surfaces will be a major challenge hampering the demand for expensive yet highly-durable acid proof lining types such as carbon brick coating.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-de-1751

On the basis of material-type, the acid proof lining market in Germany will witness the fastest growth in the thermoplastics lining segment. In 2015, the thermoplastics lining segment is estimated to have accounted for over 25% of total market share in Germany’s acid proof lining market. By the end of 2016, the share of thermoplastics lining segment is expected to grow at a substantial rate, closing in on the ceramic brick lining market share, which accounted for 34.8% in 2015.

The acid proof lining market in Germany is further segmented on the basis of end-use industries. Owing to the pervasive need of acid proof lining for protection against chemical abrasion, the chemical industries in Germany are expected to dominate the end-user segment with 29.3% market share in 2016. The water treatment facilities and power generation plants in Germany are also anticipated to fuel the demand for durable acid proof lining.

In order to expand the scope of application, the market for acid proof lining in Germany is undergoing reforms that favour manufacturers. Small acid proof lining manufacturers will continue to emerge, owing to the low entry barriers. The leading companies in Germany’s acid proof lining market will expand their business operations to meet the surging adoption levels of acid proof linings from end-use industrial verticals such as metallurgy, pharmaceuticals, and automotive manufacturing. The key players of the Germany acid proof lining market include AGRU Kunststofftechnik GmbH, Steuler-Kch GmbH, SKO Säureschutz und Kunststoffbau GmbH, GBT-BÜCOLIT GmbH, Christen & Laudon GmbH Kunststoff – Apparatebau, A-SPT Protective Solutions GmbH & Co. KG, Knapper Oberflächentechnik GmbH, Nittel GmbH & Co. KG, , Hurner-Funken GmbH and Simona AG, among others.

Request For Report Methodology@ https://www.futuremarketinsights.com/askus/rep-de-1751

Long-term Outlook: The Germany acid proof lining market is projected to register a CAGR of 5.9% during the forecast period 2016-2026. In terms of value, the acid proof lining market in Germany will reach US$ 7.605.3 Mn by end of the forecast period.

0 notes

Text

Why Demand For Hot Melt Adhesives Is Growing In Global Chemical Industry

Introduction:

Hot melt adhesives are 100% solid thermoplastic materials without any volatile organic compounds, which makes them safe for use in production, transportation, application and storage. They are also environment friendly and safe for use by humans. Hot melt adhesives consist of one or more polymers as well as additives such as stabilizers, pigments and resins which are carefully blended to exhibit different characteristics from base polymers. Hot melt adhesives are named after polymer bases. Various types of hot melt adhesives are ethylene vinyl acetate, polyolefin, polyamide, styrenic block copolymers, polyester, etc. Hot melt adhesives are used for applications in industries such as packaging, non-woven, automotive, product assembly, textiles, tapes and labels, woodworking, paper bonding, electronics and many more.

According to the latest market report published by Future Market Insights (FMI) titled “Hot Melt Adhesives Market: Global Industry Analysis and Opportunity Assessment 2015-2025”, the hot melt adhesives market is expected to be valued at US$ 5.4 Bn in 2015 and expand at a CAGR of 5.2% from 2015 to 2025, accounting for US$ 8.9 Bn by 2025.

A hot melt adhesive is a thermoplastic glue that is thermally melted on application and attains adhesion strength upon cooling. Hot melt adhesives consist of one or more polymers as well as additives such as stabilizers, pigments and resins, which are carefully blended to exhibit different characteristics from base polymers. Hot melt adhesives are named after polymer bases. Various types of hot melt adhesives include ethylene vinyl acetate, polyolefin, polyamide, styrenic block copolymers, polyester, etc. Hot melt adhesives are used in several industries including packaging, non-woven, automotive, product assembly, textiles, tapes and labels, woodworking, paper bonding, electronics and many more.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-1184

Hot melt adhesives are 100% solid thermoplastic materials without any volatile organic compounds, which makes them safe for use in production, transportation, application and storage. They are also environment friendly and safe for use by humans. Properties such as higher setting speeds and heat resistance and easy disposal gives hot melt adhesives a competitive advantage over water and solvent based adhesives, and is a major factor driving market growth. The setting speed of hot melt adhesives range between 5 and 30 seconds, enabling speedier production lines as compared to conventional adhesives. In addition, technological advancements in polymer bases are expected to further drive this market. Development of hydrophilic and polyamide hot melt adhesives is also gaining attention in developed countries, thereby driving growth of the hot melt adhesives market.

On the basis of polymer base, the hot melt adhesives market has been segmented into ethylene vinyl acetate, polyolefin, polyamide, styrenic block copolymers and others. The ethylene vinyl acetate segment is anticipated to account for a major share in the hot melt adhesives market by 2025. The polyolefin segment accounts for the highest market share across the globe and is expected to witness the highest CAGR of 6.4% in terms of value, during the forecast period (2015-2025). The styrenic block copolymers and ethylene vinyl acetate based hot melt adhesives are anticipated to grow at a steady rate during the forecast period.

On the basis of application, the hot melt adhesives market is segmented into packaging, automotive, construction, healthcare products and others. Others include textile, electronics, paper bonding and footwear. The packaging segment is expected to dominate the market with over 35% share in the global market. Consumption of hot melt adhesives in healthcare products is expected to increase rapidly in the near future. Application in healthcare products is expected to witness a CAGR of 5.4% during the forecast period. Increasing awareness pertaining to hygiene coupled with technological advancements in polymer bases, especially for hygiene, is expected to boost demand for hot melt adhesives during the forecast period.

The report provides detailed information about various trends driving each segment and offers insights and analysis about market trends in specific regions. The report also includes an overview of the parent market and key regulations regarding the application of these adhesives. On the basis of region, the market is segmented into seven regions. North America is expected to dominate the market with over 30% share by the end of 2015. In terms of value, Asia Pacific is anticipated to demonstrate the highest CAGR of over 9% during the forecast period.

Further, the report presents market opportunities, future outlook, trends, BPS analysis, market attractiveness analysis and competitive landscape of the key players in the hot melt adhesives market. Key players have been profiled to include a company overview, financials, operating segment share, product and service offerings, business strategies, SWOT analysis and key developments.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb-1184

Key players in the global hot melt adhesives market include Henkel AG & Co. KGaA, H. B. Fuller, Sika AG, Arkema Group, Ashland Inc., The 3M Company, Jowat AG, Sipol S.p.A., Palmetto Adhesives Company and Sealock Ltd.

0 notes

Text

Global Intelligent Pigging Services Market Overview

Future Market Insights (FMI), delivers key insights on the global intelligent pigging services market in its latest report titled, “Intelligent Pigging Services Market: Global Industry Analysis and Opportunity Assessment 2015 - 2025”. According to the report, the global intelligent pigging services market is expected to register a CAGR of 6.3% during the forecast period (2015–2025). Pipeline inspection gauges, also known as pigs, are devices used for inspection and maintenance operations of oil and gas pipelines. Intelligent pigs have an on-board electronic chip, which is used for recording the data about the condition of the pipeline. Intelligent pigs are widely used for corrosion and cracks detection.

Assessing various factors driving market growth, FMI analyst said, “Stringent government & industry regulations, expected economic revival and technological advancements in pigging services are surging demand for global intelligent pigging services market.” The analyst added that increasing awareness among pipeline operators about the benefits of regular inspection and maintenance of pipelines is expected to further fuel market growth. This is also expected to prompt original equipment manufacturers (OEMs) and vendors of intelligent pigs to introduce innovation in inspection technologies such as magnetic flux leakage (MFL) and ultrasonic test (UT) to improve efficiency of services.

The global intelligent pigging services market is segmented on the basis of technology into MFL and UT. Among these, demand for MFL is significant, accounting for 66.6% share of the global intelligent pigging segment market in 2014. As per FMI estimates, this segment is projected to register a CAGR of 6.5% during the forecast period.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-390

On the basis of end-use industry, the global intelligent pigging service market is segmented into gas industry and oil industry. The gas industry segment in the global intelligent pigging services accounted for 80.4% market share in 2014. FMI estimates the gas industry segment expected to register a CAGR of 6.2% between 2015 and 2025, to account for US$ 657.0 Mn by 2025. The oil industry segment is estimated to account for 19.8% share by the end of 2015 and is forecast to increase at a CAGR of 6.7% through 2025. Currently, the gas pipeline network is larger than that of oil, and this trend is expected to continue during the forecast period as well. Thus, the gas industry segment is projected to dominate the global intelligent pigging services market over the forecast period.

Increasing consumption of petroleum products and natural gas is expected to fuel demand for intelligent pigging services globally. In addition, economic revival in regions such as Eastern Europe, Western Europe & North America and economic growth in regions such as APEJ and Latin America are expected to propel growth of the global intelligent pigging services market over the forecast period.

The global intelligent pigging services market is segmented on the basis of regions into North America, Eastern Europe, Middle East & Africa, Asia Pacific Excluding Japan (APEJ), Western Europe, Latin America and Japan. North America accounted for 48.9% revenue share in the global intelligent pigging services market in 2014, and is expected to continue to dominate the global market over the forecast period. One of the smallest intelligent pigging services market, Latin America is expected to register the highest CAGR during the forecast period. The APEJ market is projected to register a CAGR of 7.1% over the forecast period

Key players across the supply chain in the global intelligent pigging services market include OEMs/vendor of intelligent pigging services and oil & gas explorers and producers. The OEMs/vendors that we have analysed are LIN SCAN, T.D. Williamson, Inc., Baker Hughes Incorporated, GE Oil and Gas (PII Pipeline Solutions), NDT Global and Enduro Pipeline Services Inc. The oil & gas explorers and producers analysed in the report are Petrobras, OMV Group, ConocoPhillips and Royal Dutch Shell Plc. Major OEMs/vendors operating in the global market are focused adopting advanced inspection technologies to enhance efficiency of services. Pipeline operators are entering into long-term supply contracts with OEMs/vendors to minimize effect of increasing costs of intelligent pigging services.

Need more information about Report Methodology? @ https://www.futuremarketinsights.com/askus/rep-gb-390

In future, OEMs/vendors should continue investing in the North America and Eastern Europe market. At the same time, APEJ and Latin America are expected to generate significant demand for intelligent pigging services. OEMs/vendors should focus on improving combinational technologies, as these are more effective and advanced that individual technologies currently used for pigging services.

#Intelligent Pigging Services Market#Intelligent Pigging Services#Intelligent Pigging#Intelligent Pigging Services Market 2019#Intelligent Pigging Services Market Trend#Intelligent Pigging Services Market Analysis#automation#industrial automation

0 notes

Text

North America will Remain the Most Attractive Market for HPP Equipment over 2026

In its latest report, Future Market Insights (FMI) has identified few of the major trends governing the overall market for high pressure processing equipment (HPPE). In brief, rapid adoption of high pressure processing technique among premium juice manufacturers, automation and technological innovation and growing number of HPP tolling service providers are playing a major role in shaping the market trajectories currently.

Hiperbaric S.A -- Most Successful Player in Recent Years

According to the report, Hiperbaric S.A a prominent manufacturer of high pressure processing equipment is the current leader in the global market as the company’s hold over the North American region is substantially strong.

FMI’s Insights on Growth Factors

FMI indicates that the growing demand for processed, packaged and ready-to-eat food products worldwide is encouraging the use of high pressure processing equipment in food and beverage industry.

Growing health concerns and increasing awareness amongst consumers on health benefits from “clean label” food is projected to influence the market growth during 2016 to 2026.

Implementation of stringent regulatory norms pertaining to food safety, especially in North American and West European countries are compelling food processing companies to install efficient HPP equipment in processing plants.

Request Sample Report@ https://www.futuremarketinsights.com/reports/sample/rep-gb-665

The adoption rate of HPP equipment for cold pasteurisation in F&B industry is one the major parameters based on which the global market size has been calculated. FMI forecasts the global high pressure processing equipment market to witness a CAGR of over 13 % in terms of value and a CAGR of 12.3% in terms of volume between 2016 and 2026. The US$ 133.5 Million HPP equipment market is estimated to create an incremental $ opportunity of over US$ 350.5 Million during the assessment period.

Horizontal Vessels -- Leading Arrangements Type Segment

Based on vessel arrangements type, the horizontal vessel is expected to be the predominant segment of the market in terms of value over 2026. Growing demand for horizontal vessel arrangements is expected to make a significant contribution to the overall market growth. Horizontal vessels possess easy loading and unloading operations with a high volume capacity, hence, have a higher preference in the market.

By applications, the meat is the largest segment in the market both in terms of value and volume. Whereas, the juice & beverage segment is anticipated to witness the fastest growth in terms of value during the forecast period.

Based on capacity, demand for above 300 litres vessels or containers is expected to gain traction over the next couple of years. Despite their high cost, above 300 litres vessels segment is projected to register a strong CAGR due to their high holding capacity.

Based on the regional analysis, the market in North America will continue to lead the pack during the forecast period. In 2016, the region accounted for over 40% share of the market followed by Europe. In addition, both the regions collectively accounted for nearly 75% share of the market in terms of value in 2016. Owing to a substantially high demand for HPP equipment from tolling services providers and their growing application base across various end-use industries, the HPP equipment market is flourishing in the region of North America. In Asia Pacific, particularly China is set to witness a robust adoption of HPP equipment in various industrial domains over the next few years.

Request to View TOC @ https://www.futuremarketinsights.com/askus/rep-gb-665

Competitive Dashboard

Apart from Hiperbaric S.A, Stansted Fluid Power Ltd, Multivac Group, Bao Tou KeFa High Pressure Technology Co., Ltd, Avure technologies, and Kobe Steel, Ltd., are some of other key players operating in the global market for high pressure processing equipment.

0 notes

Text

Good Growth Opportunities in Lawn and Garden Consumables Market Till 2027

Lawn and garden consumable market include products such as fertilizers, pesticides and seeds among others, which are used in lawn and gardens. Lawn and garden consumable products are primarily utilized in application areas namely residential and commercial. Fertilizer is the most dominant product segment for lawn and garden consumables and the trend is expected to continue in the near future.

Increase in the number of middle class and high income group population has been a major factor driving demand for larger lawns and gardens. In addition, rising demand for landscaping is expected to further fuel the growth of the market over the forecast period. However, environmental and health hazards associated with several products such as fertilizers and pesticides has been a major restraint for the industry. Low cost and eco-friendly products are expected to offer huge growth opportunity in the market.

North America led the global lawn and garden consumable market in terms of market share owing to the huge demand from U.S. Increasing demand for food gardening is expected to drive the market for seeds in the developed economies of North America and Europe. On account of increasing number of middle class population in the developing economies of Asia Pacific region, Asia Pacific is expected to the fastest growing region for the next six years. Increasing demand from South America and Middle East countries is expected to drive the demand for lawn and garden consumables in the RoW region.

Get Sample Pages@https://www.futuremarketinsights.com/reports/sample/rep-gb-5957

Major players in the lawn and garden consumable market include Pennington Seed Inc., Ace Hardware Corporation, Barenbrug USA Inc., BASF SE, Bayer AG, Grant Laboratories Inc., Dow Chemical Company, APEX Nursery Fertilizer, DuPont (EI) de Nemours, EM Matson Jr. Company Inc., Ferry-Morse Seed Company and Griffin Industries Inc. among others.

0 notes