Last Seen Blogs

ezhuththu

எழுத்து🖋️

deletelaugh90

پمپ وکیوم سرمایش

via-vai

Mikannie

ksbeditor

Marblehead Musings

vasfasan

from misha with hate

Text

0 notes

Text

0 notes

Text

0 notes

Text

Machine Vision Camera Market - Forecast 2022 - 2027

Machine Vision Camera Market Overview

Machine Vision Camera Market Size is forecast to reach $2.2 billion by 2027, at a CAGR of 9.9% during the forecast period 2022-2027. The need for inspection of flaws and controlling a specific task of industrial operations is motivating the utilization of Machine Vision Cameras in process control and quality control applications. Additionally, the growing penetration of automation, machine monitoring, real time process control solutions and robotics across various industries and rapid advancements in industrial technologies along with the need for higher productivity are boosting the deployment of Machine Vision Cameras. Machine vision cameras depend on digital sensors with specialized optics to capture images, in order to process, analyze, and measure various characteristics by using computer hardware and software for accurate decision making. The rising online shopping and e-commerce sales have contributed to the growth of the market in this region. According to Australian Bureau of Statistics data, online sales in Australia recorded a 55% rise in December 2020, when compared to last year data. Also, According to Australia Post’s Online Shopping Report published in January 2021, that over 5.6 million households shopped online in December 2020, a 21.3% higher when compared to 2019 data. A machine vision camera can easily inspect minute object details which are too small to be seen by human eye if it is built around the right resolution and optics. These systems based on both Complementary Metal-Oxide Semiconductor sensor and Charged Coupled device sensor encounter a wide range of applications in various industry verticals including oil& gas, aerospace, transportation, automotive among others and are able to serve their inspection needs with the available types such as PC-based and smart camera-based Machine Vision Cameras.

Request Sample

Report Coverage

The report: “Machine Vision Camera Market Report– Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Brushless DC Motor market Report.

By Sensor Type: CCD, CMOS, MIG Sensor, N-Type MOS Sensor

By Platform: Smart Camera, PC Based Camera, Wireless Camera, Wearable Camera

By Camera Type: Line Scan Camera, Area Scan Camera

By Process Type: 1D, 2D, 3D

By Pixel Type: Less than 1MP, 1-3MP, 3-5MP, 5-8MP, 8-12MP, More than 12MP

By Spectrum Type: Infrared, X-Ray, Visible Light and Others

By Lens Type: Wide Angle Lens, Normal Lens, Telephoto Lens

By Application: Quality Assurance and Inspection, Position Guidance, Measurement, Identification, Pattern Recognition and Others

By End Users: Automotive, Electrical and Electronics, Healthcare, Consumer Electronics, Aerospace and Defense, Logistics, Security and Surveillance, Printing, ITS, Machinery, Packaging, Food and Beverage and Others

By Geography: North America (U.S, Canada, Mexico), South America (Brazil, Argentina, Chile, Colombia and Others), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC (China, Japan India, Australia and Others), and RoW (Middle East and Africa)

Key Takeaways

The rising need for advanced manufacturing in the U.S have increasingly demanded the use of Machine Vision Cameras.

The market players are majorly opting for various strategies such as product launch, partnership and agreements and collaborations to gain market traction and further penetration to explore the hidden opportunities in upcoming trends including Industry4.0

Recognizing trends and irregularities in production processes early on machine vision paves the way for realizing the smart factory of the future. Machine vision ensures safety in production process as well as quality in the end product.

Machine Vision Camera Market Segment Analysis - By Lens Type

Based on the Lens type the Machine Vision Camera Market is segmented into wide-angle lens, normal lens, and telephoto lens. Wide Area Lens dominates the market with share of 39.4% in 2021. Growth in various machine vision applications such as mobile mapping, UAV-based inspections of power lines or facilities, and advanced automotive ADAS systems has driven demand for a wide-angle lens that provides a large field of view and high resolution. Telephoto lenses are dominating the market among the other lenses. This is owing to the increasing demand automotive and electronics industries for inspection of three-dimensional parts using machine vision.

Inquiry Before Buying

Machine Vision Camera Market Segment Analysis - By End Use Industry

Automotive industry is expected to witness a highest CAGR of 14.1% the forecast period 2022-2027, owing to increasing investments, and funds for semiconductors offering opportunities for the adoption of automation technology which is further set to drive the demand of connectors in semiconductor industry. These systems encounter wide range of applications in various industry verticals including oil& gas, aerospace, transportation, automotive among others and are able to serve their inspection needs with the available types such as PC-based and smart camera based Machine Vision Cameras. Investments by the U.S automakers for strengthening of the manufacturing of automobiles with increasing integration of recent robotic vision technologies in vehicles is accompanying the growth of the robotic vision market in the U.S. Industry revenue is projected to continue grow due to this development.

Machine Vision Camera Market Segment Analysis - By Geography

Machine Vision Camera market in Europe region held significant market share of 38% in 2021. The investments are rising for electric, connected and autonomous vehicles and this in turn The U.S. accounted a huge market base for Machine Vision due to the growing adoption of Machine Vision Camera technology by vision companies, and the companies continue to witness exploration for new applications in a variety of industries, thus driving the machine vision market driven by a push from companies such as Google and Verizon. The rising initiatives in Middle East and Africa for the increasing need of automation is set to propel the machine vision market. The growth of manufacturing industry in Africa and Middle East (AME) is expected to grow at a rate of 14.2% between 2021 and 2025 thereby significantly driving the market

Schedule a Call

Machine Vision Camera Market Drivers

Growing Demand for Smart Cameras

Smart cameras often support a Machine Vision Camera by digitizing and transferring frames for computer analysis. A smart camera has a single embedded image sensor. They are usually tailored-built for specialized applications where space constraints require a compact footprint. Smart cameras are employed for a number of automated functions, whether complementing a multipart Machine Vision Camera, or as standalone image-processing units. Smart cameras are considered to be an effective option for streamlining automation methods or integrating vision systems into manufacturing operations as they are cost-efficient and relatively easy to use. There is a huge demand for smart cameras in industrial production as manufacturers often use them for inspection and quality assurance purposes. Smart cameras are growing at a 9.7% CAGR with Machine vision being a premier use case. Thus, increasing demand for smart cameras will drive the Machine Vision Cameras market growth in various industrial applications.

Increasing need for quality products, high manufacturing capacity

Machine Vision Cameras perform quality tests, guide machines, control processes, identify components, read codes and deliver valuable data for optimizing production. Modern production line are advanced and automated. Machine vision enables manufacturing companies to remain competitive and prevent an exodus of key technologies. Recognizing trends and irregularities in production processes early on machine vision paves the way for realizing the smart factory of the future. Machine vision ensures safety in production process as well as quality in the end product. As a result of this, according to an IDG survey by Insight, 96% of Companies surveyed think computer vision has the capability to boost revenue, with 97% saying this technology will save their organization time and money across the board.

Buy Now

Machine Vision Camera Market Challenges

Lack of awareness among users and inadequate expertise

The robotic vision technology is rapidly changing, with new technologies emerging constantly, and new tools coming to market incredibly fast to make tackling automation problems easier. In the past decade alone, the robotic vision market has seen the introduction of more advanced sensors in terms of both smaller pixels and larger sensors, software platforms that continues to be more accurate, and lighting which is growing brighter and becoming more efficient. The high cost of the research and development in robotic vision and the lack of awareness among users about the rapidly advancing robotic vision technology are key factors likely to hinder the market to an extent.

Machine Vision Camera Industry Outlook

Product launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the market. Machine Vision Camera top companies includeCognex

Omron Corp

Sony Corp.

Panasonic Corp.

Hitachi

Basler AG

Keyence Corp.

National Instruments

Sick AG

Teledyne Technologies

FLIR

Recent Developments

In April 2021, Sick AG launched its first machine vision camera P621 2D equipped with AI technology for complex imaging tasks in surface mount assemblies.

In March 2020, Sony launched GS CMOS cameras equipped with CMOS sensors used in integrated transport systems and biometrics.

In June 2020, The company launched FH Series Vision system equipped with AI technology for the growing demand for labor-saving automated visual inspection during COVID-19 pandemic.

0 notes

Text

Machine Vision System & Components Market - Forecast 2022 - 2027

Machine Vision System & Components Market Overview

Machine Vision System & Components Market Size is forecast to reach $17.2 billion by 2027, at a CAGR of 7.1% during forecast period 2022-2027. The need for inspection of flaws and controlling a specific task of industrial operations is motivating the utilization of machine vision systems in process control and quality control applications. Additionally, the growing penetration of automation and robotics across various industries and rapid advancements in industrial technologies along with the need for higher productivity are boosting the deployment of Computer vision technology systems. These systems based on image sensors, vision sensors and vision controllers encounter a wide range of applications in various industry verticals including oil & gas, aerospace, transportation, automotive among others and are able to serve their inspection needs with the available types such as PC-based and smart camera-based machine vision systems. In the past several years, AI has become a top priority for enterprises across private industry sectors. Regarding the logistics industry, McKinsey predicts that almost a third of the value to be created by AI in the next 20 years will result from applying the technology to supply chains alone. For a high-volume, margin-constrained industry, a 5% improvement can significantly empower logistics organizations to advance digitalization, efficiency, and resilience in their supply chains. This shows the importance and global adoption of machine vision solutions in private parcel/postal service companies. These trends are analysed to uplift the standalone vision system demand during the forecast period.

Request Sample

Machine Vision System & Components Market Report Coverage

The report: “Machine Vision System & Components Market Report– Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Machine Vision System & Components Market Report

By Product Type: PC Based, Smart Camera Based.

By Component: Hardware (Camera, Frame Grabber, Lighting, Processor, Optics), Software (Application Specific, Deep Learning)

By Application: Quality Assurance and Inspection, Position Guidance, Measurement, Identification, Pattern Recognition and Others.

By End Users: Automotive, Electrical and Electronics, Healthcare, Consumer Electronics, Aerospace and Defense, Logistics, Security and Surveillance, Printing, ITS, Machinery, Packaging, Food and Beverage and Others.

By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC (China, Japan India, Australia and Others), and RoW (Middle East and Africa, South America).

Key Takeaways

The rising need for advanced manufacturing in the U.S has increasingly demanded the use of machine vision systems.

The market players are majorly opting for various strategies such as product launch, partnership and agreements and collaborations to gain market traction and further penetration to explore the hidden opportunities in upcoming trends including Industry4.0

Recognizing trends and irregularities in production processes early on machine vision paves the way for realizing the smart factory of the future. Machine vision ensures safety in production process as well as quality in the end product.

Inquiry Before Buying

Machine Vision System & Components Market Segment Analysis - By Component

Machine Vision System & components market is led by cameras which are estimated to surpass $7.9 billion by 2027 majorly driven by the advancements in imaging technology. The machine vision system industry is expected to grow during the forecast period due to continued evolution of CMOS image sensors, rise in demand for automation in industrial applications and increased investments in R&D of smart camera and software by key players, such as Cognex Corporation, Teledyne Technologies, Inc., Keyence Corporation, and others. The global machine vision systems and components market has increased due to the rapid penetration of automation across several industry verticals. Moreover, the development of advanced sensors and software algorithms capable of offering precise and microscopic inspection in high-speed production lines is escalating the growth rate of the market. Machine Vision market is estimated to witness significant growth in the coming years, on account of increased adoption in various industries for automatic inspection and control of machines or processes by capturing and interpreting and analyzing an image.

Machine Vision System & Components Market Segment Analysis - By End Use Industry

Automotive industry is expected to witness a highest CAGR of 9.6% in the forecast period 2022-2027. Owing to increasing investments and funds for semiconductors has been providing opportunities for adoption of automation technology which further set to drive the demand of connectors in semiconductor industry. These systems encounter a wide range of applications in various industry verticals including oil& gas, aerospace, transportation, automotive among others and are able to serve their inspection needs with the available types such as PC-based and smart camera-based machine vision systems. Investments by the U.S automakers for strengthening of the manufacturing of automobiles with increasing integration of recent robotic vision technologies in vehicles is accompanying the growth of the robotic vision market in the U.S. Industry revenue is projected to continue grow due to this development.

Schedule a Call

Machine Vision System & Components Market Segment Analysis - By Geography

Machine Vision System & Components Market in Europe region held significant market share of 41% in 2021. The investments are rising for electric, connected and autonomous vehicles, and this in turn U.S. accounted a huge market base for Machine Vision due to the growing adoption of machine vision system technology by vision companies. The companies continue to witness exploration for new applications in a variety of industries that are driving the machine vision market driven by a push from companies such as Google and Verizon. The rising initiatives in Middle East and Africa for the increasing need of automation is set to propel the machine vision market. The manufacturing industry in Africa and Middle East (AME) is expected to grow at a CAGR of 13.1% between 2019 and 2025 thereby significantly driving the market

Machine Vision System & Components Market Drivers

Growing E-Commerce Industry Fuels the Growth of the Global Parcel and Postal Machine Vision Market

The growing popularity of e-commerce is bringing an increasing number of people online, and the e-commerce and logistics industries have a difficult challenge in processing millions of orders every day. By 2020, worldwide electronic retail sales have surpassed $4 trillion, accounting for about 15% of all retail expenditure. Forbes predicts $7 trillion in B2B e-commerce sales by the year 2022. Furthermore, according to the Wall Street Journal, these online sales necessitate reverse logistics since around one-third of all items are returned by customers, with the percentage reaching to around 40% in the garment business. A rising number of package transfers has definitely spurred postal operators' desire to automate parcel and mail processing in order to deliver products more efficiently. E-commerce is a booming market and more sales means many more packages to ship. For instance, according to the US Department of Commerce, in the first quarter of 2019, the share of e-commerce in total U.S. retail sales was 10.7%, which increased as compared to 9.8% in the first quarter in 2018. As of that quarter, retail e-commerce sales in the United States amounted to almost USD 146.2 billion. According to IBEF, Indian e-commerce is projected to increase from 4% of the total food and grocery, apparel and consumer electronics retail trade in 2020 to 8% by 2025. India's e-commerce orders volume increased by 36% in the last quarter of 2020, with the personal care, beauty and wellness (PCB&W) segment being the largest beneficiary. The rising complexity of cross-border e-commerce is one of the main drivers driving market growth. Compliance, tariffs and taxes, as well as the issue of satisfying consumer expectations for rapid and cheap delivery throughout the globe, are all factors to consider when shipping cross-border. Shippers can save time and money by optimizing parcel sorting management, increasing fulfillment efficiency and improving shipment accuracy, as well as tracking and visibility, which is boosting the parcel and postal machine vision industry.

Buy Now

Increasing need for quality products, high manufacturing capacity

3D Machine Vision Systems perform quality tests, guide machines, control processes, identify components, read codes and deliver valuable data for optimizing production. Modern production lines are advanced and automated. Machine vision enables manufacturing companies to remain competitive and prevent an exodus of key technologies. Recognizing trends and irregularities in production processes early on Image Based bar code reader through machine vision paves the way for realizing the smart factory of the future. Machine vision ensures safety in the production process as well as quality in the end product. As a result of this, according to an IDG survey by Insight, 96% of Companies surveyed think computer vision has the capability to boost revenue, with 97% saying this technology will save their organization time and money across the board.

Machine Vision System & Components Market Challenges

Lack of awareness among users and inadequate expertise

The robotic vision technology is rapidly changing, with new technologies emerging constantly, and new tools coming to market incredibly fast to make tackling automation problems easier. In the past decade alone, the robotic vision market has seen the introduction of more advanced sensors in terms of both smaller pixels and larger sensors, software platforms that continues to be more accurate, and lighting which is growing brighter and becoming more efficient. The high cost of the research and development in robotic vision and the lack of awareness among users about the rapidly advancing robotic vision technology are key factors likely to hinder the market to an extent.

Machine Vision System & Components Market Landscape

Product launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Machine Vision System & Components Market. Machine Vision System top companies include

Cognex

Omron Corp

Sony Corp.

Panasonic Corp.

Microscan

Basler AG

Keyence Corp.

Sick AG

Teledyne Technologies

FLIR

Recent Developments

In July 2021, Cognex launched its new series of vision software “VisionPro” for industrial machine vision enabling customers to combine deep learning and traditional vision tools in the same application.

In March 2021, FH-SMD Series 3D Vision sensors for robotic arms enabling space-saving assembly, inspection, and pick & place and other applications.

In May 2020, Sony corporation announced that it is about to launch two vision image sensors for use in AI processing equipped with AI functionality in perse range of applications.

0 notes

Text

Control Valves Market - Forecast 2022 - 2027

Control Valves Market Overview

The Control Valves market size was $6.6 billion in 2021 and is expected to grow at a CAGR of 6.0% during the forecast period 2022-2027. Growth of the Control Valves market can be attributed to the increasing application of control valves in food & beverage, oil and gas, utilities, pharmaceutical, chemical and other industries and adoption of Internet of Things (IoT) technology in the process industries. The Global process automation control valve market is poised to witness significant growth during the forecast period. With the emergence of industry 4.0, there is high adoption of actuator valves, pneumatic solenoid valves and other valves for process automation. According to IoT Analytics, Less than 30% of manufacturers report extensive adoption for Industry 4.0 in 2021. However, this number is expected to rise rapidly. The growing demand for plant safety in manufacturing industries coupled with growing concern for personnel safety has led to the increasing deployment of hydaulic Control Valves and flow control devices. Automatic hydronic balancing, temperature stability, high control authority and pnematic actuator longevity by reducing the amount of movement are the main aspects that are projected to boost the demand for pressure-independent control ball valves and axial flow valves during the forecast period. Increasing demand for HVAC systems from a number of industries contributes to the increased market size of the control diaphragm valves and plug valves.

Request Sample

Report Coverage

The report: “Control Valves Market – Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Control Valves Market Report.

By Valve Body – Linear Valve (Globe, Diaphragm, Pinch and Others, Rotary Valve (Ball, Butterfly, Plug and Others).

By Accessories – Actuator, Controller, Positioner and Others.

By End Use Industry – Oil and Gas, Chemicals, Food and Beverage, Water and Wastewater, Energy and Power, Pharmaceutical, Automotive, Aerospace and Defense, Paper and Pulp, Agriculture, HVAC and Others.

By Geography - North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, SK, Australia and Others), South America(Brazil, Argentina and others),and RoW (Middle East and Africa).

Key Takeaways

North America dominated the Control Valves market owing to high adoption of automation technologies in industries combined with stringent regulations in 2021.

Implementation of advanced technologies such as IoT, artificial intelligence and automation technologies in manufacturing industries have been increasing the deployment of control valves. Integration of control valve actuators with these technologies set to drive the market.

Growing trend for digitalization and automation in conventional plants is leading to higher demand for control valves, thereby increasing the market growth.

High investment for adoption of automation technologies in industries is a major challenge which hampers the growth of the market.

Inquiry Before Buying

Control Valves Market Segment Analysis- By Accessories

Actuators dominated the process automation control market with a major share 43.6% in 2021. Introduction of IoT and automation technologies in various industries is set to propel the demand for Control Valves. In control valves, the actuators can fully rotate its head by 360° which allows flexible installation and optimization. This helps in reducing overall installation cost and optimizes the incorporation of actuators in manufacturing processes, thereby fueling the market growth. The linear-style valve is presently the most common type of valve. It is famous for its compact architecture and easy maintenance. Linear valves, also known as multi-turn valves, are equipped with a sliding mechanism that moves a closing feature into an open or closed position.

Control Valves Market Segment Analysis- By End Use Industry

The Food & Beverage (F&B) Industry segment is projected to grow at a CAGR of 7.9% during the forecast period 2022-2027. In this industry, control valves are used mainly for managing steam which is the most critical component in food processing. There has been growing adoption of automation technology in this industry as it is required to maintain critical control points such as hazard Analysis and critical control point (HACCP) to meet safety standards of food safety authorities. Regulations by the Food and Drug Administration (FDA) for the valves which come into direct contact with food, should be smooth enough to avoid trapping particles or bacterial accumulation which create opportunities for the up-gradation of food plants with new infrastructure. These types of regulations have been forcing to use aseptic control valves and implement process automation in the food & beverage industry. Monitoring and operating the control valves manually is a difficult task. So, implementing process automation in food and beverage industry to increase production efficiency is set to fuel the Control Valves market. The demand for a high degree of consistency in quality of food and beverages is prompting the Food and beverage industry to improve their production processes. These factors are pushing the Food and beverage industry to opt for process automation which is set to drive the Control Valves market.

Schedule a Call

Control Valves Market Segment Analysis- By Geography

North America region led the Control Valves market in terms of revenue share, and held 35.4% share in 2021 due to technological advancements and growing demand for cutting edge instrument across different industry verticals in the region. In the U.S., Environmental Protection Agency (EPA) has mandated to limit the use of traditional spring diaphragm actuators in order to reduce greenhouse gas emissions. The replacement of these actuators with pneumatic actuator valves has been reducing methane and volatile organic compounds emissions. Government regulations and early adoption of advanced technologies have been escalating the demand for Control Valves in this region.

Control Valves Market Drivers

Adoption of IoT Technology is enhancing the performance of control Valves in process Industries

In recent years, the processing industries such as oil & gas, chemical and others have started exploiting IoT technology. IoT helps in improving operational efficiency of control valves. There has been increasing demand for adoption of IoT System in industries as this system is integrated with smart valves which are equipped with intelligent control systems, wireless vibration sensors and embedded processors. These sensors send notifications and data to a centralized monitoring system. In addition to these, IoT is also used for real time remote access, predictive control valve maintenance. Thus, IoT can be applied to improve the performance and efficiency of control valves, which in turn, will save maintenance costs and create a more secure work environment, thereby fueling the Control Valves industry. In spite of high adoption rates, only 54% of all the devices deployed in the adopter organizations are IIoT technology-enabled This will drive market growth.

Advancements in Technology

Advancements in technology have created innovative solutions that can help process plants to become increasingly more efficient through streamlining of their operations. Incorporating sensor technology to control valves in order to provide safe operation along with high performance in industries is creating demand for process automation. Another technology digital field bus protocol has been playing crucial role in manufacturing industries. Industrial field bus network systems are used to connect instruments in manufacturing plants that require considerably less wiring. Adoption of advanced technologies in manufacturing industries for controlling the valves is set to drive the Control Valves market size. This also forces independent control principles to eradicate the situation at a partial level that has a direct impact on the constancy of the room temperature. As the actuators are connected to them, Control Valves often ensure impeccable working conditions, which requires less movements to stay stable at temperature. This helps to improve the life of the actuators and reduces maintenance costs. This will drive market adoption.

Buy Now

Control Valves Market Challenges

High Cost for investment

The major challenge for Control Valves is the high cost for investment. Implementing a process automation solution for control valves involves a considerable initial investment. However, this factor should be contrasted to the benefits in terms of productivity and compliance. The initial investment associated with switching from a human production line to an automatic production line is very high. Also, substantial costs involved in training employees to handle this new sophisticated equipment is hampering growth of the Control Valves market. For example in the automotive sector, the replacement cost of an idle control valve is anywhere from $120 to $500. The cost of the parts alone will be between $70 and $400+ thus, driving up investment.

Control Valves Market Landscape

Acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Control Valves market. Control Valves top 10 companies include

Emerson Electric Co

Flowserve Corporation

Weir Group

Curtiss-Wright Corporation

Honeywell International Inc

Schlumberger Limited

IMI plc

Crane Co

KITZ Corporation

Metso Corporation

Recent Developments

In February 2020, Weir Group PLC announced three new additions to the industry-leading Lewis series of sulphuric, sulphuric and phosphoric acid pumps and valves. A new chapter in the brand's proud history of ground breaking product and material engineering is the introduction of the Lewis VL Axial Pump, Lewis Horizontal Process Pump and Lewis Vertical High Pressure Molten Salt Pump.

In June, 2021 Spirax Sarco Introduced the Spira-trol Steam-Tight control valve. The secure steam control with class VI isolation in one valve with a flip over seat to double the life, providing the customer with a reduced total cost of ownership.

In April, 2021 GEMÜ, launched the GEMÜ R563 eSyStep, a new control valve with a motorised actuator. The valve specialist has also expanded the GEMÜ 566 control valve with the GEMÜ eSyStep actuator.

#Control Valves Market#Control Valves Market size#Control Valves industry#Control Valves Market share

0 notes

Text

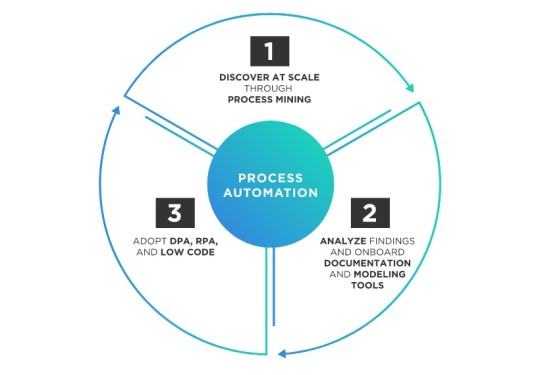

Process Automation Market

Process Automation Market Overview

Process automation companies are currently the eye candies of investors. Couple of quick examples can be UiPath and Automation Anywhere. While the former raised its value to $3 billion through Series C funding in September 2018, the latter gained $300 million from SoftBank Vision Fund in November 2018 to climb up to $2.6 billion value. With such an influx of investments, the process automation market companies are employing the cumulative capital for the development of various automation equipment, and the market for the same is flourishing.

As per the findings of this IndustryARC report, the global process automation market size was at $65 billion in FY 2018. And, the demand is increasing at a progressive CAGR of 7% during the forecast period of 2019 to 2025. Although process automation market is flourishing throughout the world, the Asia-Pacific region has managed to grab the largest demand share of around 30% to 35% as of 2018. According to the IndustryARC market research report, the pharmaceutical sector is the key end-use industry where process automation is flourishing. The process automation market in the pharmaceutical industry projected to grow at a relatively higher CAGR of 8% during the aforementioned forecast period.

Request Sample

Process Automation Market Outlook

The aim to limit human interaction to achieve optimum accuracy has emerged as the prime reason for the process automation market growth. Technologies such as distributed control systems (DCS), manufacturing execution system (MES), local area network (LAN), remote terminal units (RTUs), programmable logic controller (PLC) and most importantly supervisory control and data acquisition (SCADA) are the leading aspects for the process automation market. Process automation plays an important role in business process management (BPM) and enterprise resource planning (ERP).

Process Automation Market Growth Drivers

Industrial automation or factory automation are some of the most prolific growth drivers of the process automation market. The emerging requirement for reducing human interaction in various processes in order to cut down labor costs as well as minimize errors has opened a room full of opportunities for automated systems in the industrial sector.

The imminent need for achieving the best possible results concerning accuracy is also one of the growth drivers for the process automation market. Various automation equipment installed in multiple industries such as pharmaceutical, electrical, manufacturing, and other sectors has achieved prominent results which are much more precise than the human implied operations.

Inquiry Before Buying

Process Automation Market Trends

Technical giant Intel acquired Itseez Inc and Yogitech to bolster its automotive IoT profile. Furthermore, Microsoft acquired Italy originated company Solair, and Cisco acquired the start-up from California named Jasper for $1.4 billion. Evidently, acquisitions are in full force, showcasing major companies’ zest to stay ahead of the curve.

Process Automation Market Challenges

Process automation is estimated to reduce a significant amount of jobs for the regional population. Process automation in areas with industrial based employment will replace the man-force with automated equipment, which further will lead to unemployment among the people. This leap could affect the regional inhabitants at a massive scale.

Incorporating process automation in the manufacturing chain sometimes requires building high-level algorithms, and these algorithms are programmed to target a specific dataset. If there comes a data gap in the agile development process or automation, it could lead to an ambiguous process or development.

Schedule a Call

Key Players in the Process Automation Market

With a great wave of start-ups emerging in the process automation market, some of the dominating key players are :- Mitsubishi Corporation, Robert Bosch GmBH, ABB Ltd, Eaton Corporation, Dassault Systems, Emerson Electric Co., Honeywell International, Inc., Johnson Controls, Inc., Rockwell Automation, Inc., and Schneider Electric SE.

Process Automation Market Research Scope:

The base year of the study is 2018, with forecast done up to 2025. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. It also provides information on unit shipments. These provide the key market participants with the necessary business intelligence and help them understand the future of the Process automation market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats. The key areas of focus include the types of Process automation market, and their specific applications in different types of vehicles.

Buy Now

Process Automation Market Report: Industry Coverage

The Process automation market report also analyzes the major geographic regions as well as the major countries in these regions. The regions and countries covered in the study include:

North America: The U.S., Canada, Mexico

South America: Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, Costa Rica

Europe: The U.K., Germany, Italy, France, The Netherlands, Belgium, Spain, Denmark

APAC: China, Japan, Australia, South Korea, India, Taiwan, Malaysia, Hong Kong

Middle East and Africa: Israel, South Africa, Saudi Arabia

#process automation market#process automation devices#process automation market size#process automation companies#process automation sales

0 notes

Text

Ozone Sensor Market - Forecast(2022 - 2027)

Ozone Sensor Market Report Overview

Ozone Sensor Market size is analyzed to grow at a CAGR of 5.5% during the forecast 2022-2027 to reach $76.18 Million. The growing demand for ozone sensors from various industries, primarily from food & beverage and water & wastewater treatment, is driving the market growth. In 2019, Aeroqual, a leading ozone sensor manufacturer, supplied an S930 ozone monitor to Jimco, which was used for accurate measurement of ozone levels within its food facilities during as well as after sterilizing procedures. In wastewater treatment and sewage treatment, the ozone system is utilized as comprehensive and effective disinfection for organic stuff contained in wastewater. During the process, pesticides, organics (such as organic nitrogen), biological oxygen demand (BOD), chemical oxygen demand (COD), volatile fatty acids (VFA), and sulfur are all eliminated, significantly eliminating odors while being both cost-effective and environment friendly. With higher ozone concentrations being considered harmful to human health, there is significant adoption of ozone sensors for monitoring ozone levels in wastewater treatment plants. A result of the rising sewage treatment connections, which is directed coupled with a surge in wastewater treatment facility expansion or new projects, is further set to accelerate the market growth in the coming years.

Request Sample

Ozone Sensor Market Report Coverage

The report: “Ozone Sensor Market Industry Outlook – Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Ozone Sensor Market industry.

By Product Type: Portable, Handheld, Tabletop, Wall Mounted.

By Function: Ozone Sensor, Multi-Gas Sensor.

By Sample: Liquid, Gaseous.

By Range: Up to 10 ppm, 10-50 ppm, 50-100 ppm, 100-250 ppm, 250-500 ppm, Above 500 ppm.

By Response time: < 10s, 10-20s,20-40s,40-100s,Above 100s.

By Industry Vertical: Food and Beverage, Water and Wastewater Treatment, Manufacturing, Medical and Pharma, Environment and Government, FMCG, Agriculture, Others.

By Geography: North America (US, Canada, Mexico), South America (Brazil, Argentina, Chile, Colombia, Others), Europe (Germany, France, UK, Italy, Spain, Russia, Netherlands, Others), APAC (China, Japan, South Korea, India, Australia, Indonesia, Malaysia, Others), and RoW (Middle East, Africa).

Key Takeaways

In 2021, the portable ozone sensor held the largest market value of $29.52 Million, owing to various factors like wider adoptability from a variety of end-use industries including manufacturing, healthcare and so on.

Ozone sensor held the largest share of 68.6% in 2021, and is anticipated to have a significant market growth over the forecast period 2022-2027, attributed to factors including increasing development towards food and beverage facilities, water & wastewater treatment plants and others.

North America dominated the global Ozone sensor market with a share of 35.2% in 2021, owing to a variety of factors such as the development of new wastewater treatment plants along with investments on construction of food processing facilities.

Increasing number of water & wastewater treatment projects along with growing development towards new healthcare facilities is analyzed to significantly drive the market growth of ozone sensors during 2022-2027.

Inquiry Before Buying

Ozone Sensor Market Segment Analysis – By Product Type

Portable segment dominated the global ozone sensor market with the largest share of $29.52 Million in 2021, and is anticipated to grow with the highest CAGR of 5.9% through the forecast period 2022-2027. Portable ozone sensors are widely used by a variety of end-use industries as if the ozone concentration in the air is too high, the detector will emit a triple alert signal of sound, light, and vibration, effectively preventing poisoning accidents caused by excessive ozone gas concentration in the air. Ozone sensors are frequently used in healthcare, manufacturing, and other industries in order to verify fixed ozone monitor readings, spot-check ozone concentrations, monitor health and safety along with indoor air quality. Development of new portable ozone sensor products for usage in hospitals, manufacturing facilities, wastewater treatment, and other related end use sectors, intended to monitor ozone concentration levels more efficiently have been eventually driving market expansion in the ozone sensor industry. In October 2020 Aeroqual, a New Zealand-based ozone sensor manufacturer, developed and launched a new ozone sensor, named EOZH capable of monitoring 0-30 ppm ozone concentration. These sensors were designed specifically for use in hospitals to clean equipment and reduce or eliminate pathogen spread. Additionally, growing number of wastewater treatment projects across the globe is also expected to increase demand for ozone sensors, thus driving the market forward in the coming years.

Ozone Sensor Market Segment Analysis - By Function

Ozone sensor held the largest market share of 68.6% in 2021, and is anticipated to have a significant growth over the forecast period 2022-2027. Ozone sensors are utilised within range of applications, including sanitization, food processing, wastewater treatment, and more, for serving industries such as water & wastewater treatment, food & beverage, and so on. As higher ozone levels can lead to major health repercussions, ozone sensors are getting widely used within these facilities to measure ozone concentrations more accurately, efficiently and reliably. Furthermore, as people's purchasing power increases around the world, impacting the need for prepared and hygienic meals, thus resulting in more new food and beverage facilities being constructed. In 2021, construction projects on Kerry Group's new food processing factory in Indonesia began and is expected to be completed by the end of 2022, while construction on Nestle Food Processing in Ohio, U.S, is expected to be completed by 2023. As a result, rising food and beverage facilities are likely to increase demand for ozone sensors to conduct processes like odour removal, disinfection, sanitation, thereby boosting its market growth during the forecast period.

Schedule a Call

Ozone Sensor Market Share Segment Analysis - Geography

North America dominated the global Ozone sensor market with a 35.2% share in 2021, due to growing development of new wastewater treatment plants in the United States, which in turn drives the need of ozone sensors as they are used in controlling ozone content to remove viruses, bacteria, and other organic matter found in wastewater. For instance, in August 2021, Pennsylvania American Water announced the commencement of the development of a new wastewater treatment plant in U.S. worth around US$ 8.7 million. The wastewater treatment plant is scheduled to be completed by the end of 2022. Such new development of wastewater treatment plants is expected to increase the demand for ozone sensors, thus, driving the market growth in the region. In 2021, the development of new food & beverage and wastewater treatment facilities already began in the United States, in comparison to 2020 during the Covid-19 pandemic, which resulted in gradual recovery of the market. In October 2021, Nestle invested around US$ 550 million for the development of a new food processing facility in Ohio, U.S. The new facility is expected to increase the company’s production capacity and is scheduled to be completed by the end of 2023. Thus, an increase in the development of such new food processing facilities is expected to increase demand for ozone sensors to measure ozone concentration used in food processing applications be it sanitation, disinfection odour removal, thus, accelerating the market growth.

Ozone Sensor Market Drivers

Increasing number of water & wastewater treatment projects act as a prime factor driving the market growth for ozone sensors:

Ozone systems are used in wastewater and sewage treatment in order to provide complete and effective disinfection of the organic material found in wastewater. Pesticides, organics (like organic nitrogen), biological oxygen demand (BOD), chemical oxygen demand (COD), volatile fatty acids (VFA), and sulphur are all removed during this procedure. Higher ozone concentrations, on the other hand, are considered to be harmful to human health, thus these sensors are extensively used in wastewater treatment plants to monitor ozone levels. Around the world, the rate at which sewage treatment plants are connected to wastewater treatment plants is increasing, while necessitating a greater demand for ozone treatment technology. Because such facilities require ozone monitoring, the market for ozone sensors is likely to increase. Also, in 2020, the Philippines government awarded the Aglipay Sewage Treatment Plant in Mandaluyong to SUEZ a French-based wastewater utility company for design and construction, as well as one year of operation and maintenance, making it the country's largest. This facility will provide a daily capacity of 60,000 m3, capable of meeting high national criteria which go above and beyond EU norms in terms of reducing negative impacts on Manila Bay and Pasig River, as well as its environmental imprint. The project is currently under construction and is projected to be completed in early 2024, further driving the market demands for ozone sensors in long run.

Buy Now

Growing development toward new healthcare facilities is projected to drive market growth throughout the forecast period:

In hospitals, ozone sterilization is routinely used to disinfect equipment and prevent the spread of bacteria. Furthermore, in ozone sterilization applications, time is a consideration, and a higher ozone dosage may be required to reduce sterilization time while maintaining efficacy. Since this can lead to disastrous consequences for patients and healthcare personnel, ozone sensor is widely adopted. Ozone sensors are used in hospitals to monitor the amount of ozone provided, ensuring that the required level is met and maintained for a set period of time before the ozone generator is turned off. Usage of these sensors help in making processes more consistent. There have been a surge in the construction of new healthcare facilities, which is expected to increase demand for the ozone sensor, boosting the market growth. As in January 2022, construction on the second phase of St. Paul's hospital in Canada began, with plans of the second phase projected to be completed by 2023, followed by third phase of the hospital development completion by 2025. The total cost of the project is expected to be around $2.2 billion, and such factors are bound to raise the market demand towards ozone sensors in the coming years.

Ozone Sensor Market Challenges

The global Ozone Sensor market is being impeded by the market's availability of substitutes:

Alternative products for detecting ozone concentrations include electrode oxygen sensors, heated metal oxide sensors (HMOS), chemiluminescence sensors, and others. Oxygen electrode sensors, with detection levels as low as a few parts per billion, are dependable sensors for use in air quality networks (ppb). High sensor gain, fourth electrode compensation, advanced filtering, and electrodes adjusted for long-term repeatability give the needed sensitivity, selectivity, and stability. These sensors have a lower average price than ozone sensors, ranging from US$100 to US$300 per unit. Even after several sterilising cycles, electrode structure maintains exceptional stability. As a result, oxygen electrode sensors can be found in a variety of settings, including medical, food and beverage, and other industries. Additionally, chemiluminescence sensors have higher accuracy for the monitoring of ozone gas, which makes it ideal for use in wastewater treatment, manufacturing, and other such facilities. Owing to such advantages of alternative substitutes like electrode oxygen sensor, heated metal oxide sensors (HMOS), chemiluminescence sensor, and others, application for ozone sensing is increasing, which is restricting the growth of the ozone sensor market.

Ozone Sensor Market Landscape

Technology launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Ozone Sensor Market. In 2021, the market of Ozone Sensor Market share has been fragmented by several companies. Ozone Sensor Market top 10 companies include:

Honeywell

Mettler Toledo

Emerson

DKK-TOA Corporation

Hach Company

ProMinent

PCE Instruments

BMT Messtechnik GMBH

KWJ Engineering Inc

Aeroqual

Acquisitions/Technology Launches/Partnerships

In March 2021, Mettler-Toledo International Inc acquired PendoTECH, a manufacturer and distributor of single-use sensors, transmitters, control systems and software for measuring, monitoring, and data collection primarily in bioprocess applications.

In September 2020, Aeroqual launched a new high-range ozone sensor gas-sensitive electrochemical (GSE) type for ozone sterilization applications. With linear and fast response, these sensors are capable of measuring upto 30 ppm along with a low cross-interference from volatile organic compounds (VOC’s) that may be found in the types of environments being sterilized.

0 notes

Text

Control Transformer Market - Forecast(2022 - 2027)

Overview

Control Transformer Market is forecast to reach $9.04 billion by 2025, growing at a CAGR 5.67% from 2020 to 2025. Control transformer provides stepped-down voltages to machine tool control devices to separate control circuits from all lighting and power circuits and allow ungrounded or grounded circuits to be worked. The use of control transformer is important for the control devices to work efficiently and safely. With the concern for safety in electrical equipment, the need for control transformers has increased considerably to prevent the equipment from any accidents. Control transformer is expected to play an important role in helping countries achieve their energy-efficiency goals, as energy saving is the primary feature of these devices. Utilities need to boost the efficiency of electricity and eventually increase the quality of power supplied to customers. Control transformer provides a high degree of secondary voltage stability in less time, which is expected to increase market growth over the forecast period of the control transformer.

Request Sample

Key Takeaways

The need for control transformers has increased with this concern for protection in electrical equipment. These transformers are used to protect the equipment from any incidents.

Control transformers are expected to play an important role in helping countries meet their energy efficiency goals, because energy saving is the primary feature of these devices.

The three phase dominates the market, due to the need for improved results in different applications. The three-phase Control transformers are used for many general equipment applications in manufacturing, power plants, chemical and other industries.

Over 1500 VA transformers are primarily used in heavy-duty industries such as oil & gas, metal & mining, and heavy-duty machinery power generation.

Due to industrialization and infrastructural developments in China and India, the Asia Pacific market is projected to hold the largest share of the control transformer market.

By Phase- Segment Analysis

During the forecast period the three phase segment is expected to grow at a CAGR 6.9%. Owing to improved performance in industrial applications compared to the single phase segment, the three-phase segment held the largest share of the control transformer market. The three phase controls the market, owing to the need for better performance in various applications. The three-phase control transformers are used to operate many general equipment in mining, power plants, chemical, and other industries, such as pumps, compressors, crushers, and other mechanical devices.

Inquiry Before Buying

By Power Rating - Segment Analysis

500-1000 VA Segment is expected to grow at a higher CAGR 8.2% during the forecast period. The control transformers are designed specifically for industrial applications where electromagnetic components such as relays, solenoids and magnetic motor starters are used. The 500-100 VA Control Transformers are designed to sustain high voltage inputs with efficiency. Basically, these control transformers are used for electrical devices & systems. With today's growing popularity of cost-saving benefits of high-voltage delivery of modern buildings, 500-1000 VA power transformers are projected to increase and this increase is anticipated to help in growth of control transformer market.

By Geography - Segment Analysis

APAC currently dominates the global Control Transformer market with a share of more than 37.2%. Due to industrialization and infrastructural developments in China and India, the Asia Pacific market is projected to hold the largest share of the control transformer market. Power and distribution infrastructure gradation, aging equipment standby, growing heavy industry development, and renewable energy growth are some of the factors driving demand for control transformers in this region. The increasing need to expand and develop the existing transmission and distribution network to meet rising electricity demand is projected to lead to positive growth of the transformers market during the forecast period. Furthermore, evolving Asia-Pacific markets are expanding many prospects for the introduction of wind power capacity in these nations. Asia's offshore wind capacity is expected to rise 20 times to 43 GW, by 2027. Such factors will eventually fuel the growth of the control transformer market.

Schedule a Call

Drivers – Control Transformer Market

Need to reduce system failures triggered by frequent spikes in voltage

Electricity dependency and the proliferation of highly sensitive electrical equipment make it important to have reliable, high-quality power sources. Transient flickering and voltage instability are significant causes of system failure and operational disruption. Such interruptions can damage critical power equipment including transformers, switchgears, condensers, overhead lines, inductors. Operational losses of USD 80 billion per annum are sustained in the US due to power interruption. High maintenance and manufacturing costs, production delays, loss of revenue, late deliveries, idle workers and increased spoilage and scrap are among the major effects of voltage instability on operations. In addition, uncontrolled voltage stability can cause damage to sensitive electronic equipment by sudden accidents, long-term damage or industrial process interruptions. Control transformers minimize the possibility of voltage instability and ensure safe and reliable performance of the equipment.

Stability for secondary voltage in less time period

Stability for secondary voltage in less time period is a key factor for the growth of the industrial Control Transformer. It helps in keeping the voltage driving system at a steady level when there is high current. It helps prevent issues like short circuiting and technological problems. Targets for electricity generation, increasing the introduction of emerging technology, increasing clean coal, and a share of renewable energy resources provide enormous opportunities for key players as they are significantly driving the need for control transformer for secondary voltage stability.

Buy Now

Challenges – Control Transformer Market

Dependent on other Devices for voltage regulation

During the past few years, voltage regulation has become a major control issue, especially at distribution level and for a twofold reason. Voltage control is a function of voltage magnitude difference between a component's sending and receiving ends. The percentage voltage difference between no load and maximum load voltage distribution lines, transmission lines, and transformers is commonly used in power engineering. Control transformers depend upon other devices for voltage regulation which is a major concern and is anticipated to hinder the market growth of control transformer.

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in Control Transformer Market. Control Transformer Market is expected to be dominated by major companies such as ABB, Siemens, Schneider Electric, Emerson Electric Co., Hammond Power Solutions (HPS), Dongan Electric Manufacturing Co., Eaton, GE, Hubbell, Rockwell Automation, Broadman Transformers, MCI Transformers.

Acquisitions/Technology Launches

In October 2016, ABB introduced a free Total Cost of Ownership (TCO) tool to help customers determine loss capitalization factors, and compare different transformer alternatives from the point of view of total cost and environmental impact.

In March 2016, ABB launched a new production facility for transformers in Lodz, Poland. The investment's reach was to support ABB's existing transformer manufacturing facilities in Lodz by providing support workers for machine operators and logistics, buying, efficiency, and engineering.

#control transformer market#control transformer market size#control transformer market shape#control transformer market forecast

0 notes

Text

Load Cell Market - Forecast(2022 - 2027)

Load Cell Market Overview:

The load cell market for looks promising due to several reasons such as increased use of load cells in mining activities, and logistics and metal industries; increase in production of heavy manufacturing/industrial machinery, and rapid industrialization across the globe. Load Cells are classified into various products such as single-point, dual-shear, shear-beam, and others. The Load Cell Market is estimated to grow at a CAGR of 3.73% during the forecast period 2018–2023. APAC is forecast to be the fastest-growing market with a CAGR of 5.87%, which can be mainly attributed to the adoption of the distributed ledger technology for controlling weights in tanks, hoppers, mills, vehicles, and so on.

Request Sample

Load Cell Market Outlook

Load cells are connected to various measuring devices for measuring purposes, and to display, record, control, and keep track of the loads. Applications are diverse varying from small sensors for use in electronic scales, bath scales, game consoles and home electronics to those for general industrial uses such as truck scales, measuring systems in production lines, and tank scales.

Load Cell Market Growth Drivers

Increasing demand for load cells from industries such as healthcare and oil & gas is driving the Load Cell market. Load cells are used in healthcare devices and equipment such as infusion pumps and surgical instruments, and also in a wide range of delicate fluid-monitoring applications including blood transfusions, kidney dialysis, and blood donation. In such applications, the load cells ensure that the amount of fluids entering, leaving, or being replaced in the body are started, stopped, or recirculated at the right time and in the proper dosage or ratios.

Inquiry Before Buying

Load Cell Market Challenges

Meeting the required regulatory standards is a major challenge for the load cell market. The companies that manufacture load cells need to ensure that their devices really do perform as proposed. Most countries have a set of legal requirements that manufacturers have to follow. The regulations that are adopted by many countries outside the U.S. have as their basis a recommendation made by an intergovernmental organization called the International Organization of Legal Metrology.

Load Cell Market Research Scope

The base year of the study is 2017, with forecast done up to 2023. The study presents a thorough analysis of the competitive landscape, taking into account the market shares of the leading companies. These provide the key market participants with the necessary business intelligence and help them understand the future of the Load Cell market. The assessment includes the forecast, an overview of the competitive structure, the market shares of the competitors, as well as the market trends, market demands, market drivers, market challenges, and product analysis. The market drivers and restraints have been assessed to fathom their impact over the forecast period. This report further identifies the key opportunities for growth while also detailing the key challenges and possible threats.

Schedule a Call

Load Cell Market Report: Industry Coverage

Types of Products in the Load Cell Market: S-Type, Dual-Shear, Single-Point, Shear-Beam, Bending-Beam, and Others

The Load Cell market report also analyzes the major geographic regions for the market as well as the major countries for the market in these regions. The regions and countries covered in the study include:

North America: U.S, Canada, Mexico

South America: Brazil, Argentina, Colombia

Europe: U.K, Germany, Italy, France, Poland, Belgium, Spain, Russia

APAC: China, Australia, South Korea, India, Japan

Rest of the World: Middle East, Africa

Load Cell Market Key Players Perspective

ABB Group is a major manufacturer of Load Cells. The company has its headquarters in the Switzerland and operates in Europe, The Americas, Asia-Pacific, Middle East and Africa. ABB Group, through its broad range of products, constant product launches, and innovation has been successful in catering to a variety of customers, consequently maintaining its hold over the market.

Spectris, headquartered in the U.K, is the next leading player in the Load Cell market. The company offers load cells through its 100% owned subsidiary HBM.

Buy Now

Load Cell Market Trends

Automation and artificial intelligence (AI) are changing the nature of industries. Advances in robotics, artificial intelligence, and machine learning are ushering in a new age of automation, as machines match or outperform human performance in a range of activities, including ones requiring cognitive capabilities. The growing demand for industrial robots is expected to fuel the demand for load cells in the market. According to Industry experts, smart automation will power the fourth industrial revolution, combining the innovation in industrial and IT processes to drive global manufacturing productivity gains. Another industry revolution is now underway, which industry experts believe will transform the future of manufacturing. It is powered by smart automation (SA). As Industry 4.0 rises in importance, the market for load cell is forecast to thrive.

#load cell market#load cell market price#load cell market research#load cell market report#load cell market analysis#load cell market forecast

0 notes

Text

Warehouse Robotics Market - Forecast(2022 - 2027)

Warehouse Robotics Market Overview

The Global Warehouse Robotics Market size is projected to reach US$9.5 billion by 2027, growing at a CAGR of 14% from 2022 to 2027. The lucrative benefits of automated warehouse robots offer intelligent warehousing. In other words, it offers increased safety, efficiency, improved order accuracy and reduced labor costs which are the primary factors propelling the growth of the Warehouse Robotics Market during the forecast period. Additionally, the growing proliferation of the Industrial Internet of Things, Artificial Intelligence, machine learning and other technologies are expected to fuel overall market growth. The growing e-commerce industry and the introduction of advanced technologies in robotics such as robotics in logistics, automated warehouse robots, sortation robots and the rising need for intelligent warehousing, warehouse digitalization and inventory management are fostering the demand for the Warehouse Robotics market. Growing demand for distribution center automation and fulfillment automation, as well as increased awareness of quality and safety products, would drive market growth in the coming years. These aforementioned factors would positively influence the Warehouse Robotics Industry outlook during the forecast period.

Request Sample

Report Coverage

The report: “Warehouse Robotics Industry Outlook – Forecast (2022-2027)” by IndustryARC, covers an in-depth analysis of the following segments in the Warehouse Robotics industry.

By Product Type: Autonomous Mobile Robot (AMR), Articulated Robots, Cylindrical Robots, SCARA Robots, Collaborative Robots, Parallel Robots, Cartesian Robots and Others.

By Payload Capacity: less than 20Kg, 20-100Kg, 100-300Kg and greater than 300Kg.

By System Type: Knapp Open Shuttle, Locus Robotics System, Fetch Robotics Freight, Scallog System and Swisslog Carrypick.

By Components: Programmable Logic Controller, Microprocessors and Microcontrollers, Actuators, Sensors and RF Module.

By Software: Warehouse management system, Warehouse execution system, Warehouse control system and Others.

By Function: Pick & Place, Assembling & Dissembling, Transportation, Sorting & Packaging and Others.

By End-use Industry: E-commerce, Automotive, Consumer Electronics, Food & Beverages, Healthcare, Metal & Machinery, Textile, Chemical and Others.

By Geography: North America (the US, Canada and Mexico), South America (Brazil, Argentina and Others), Europe (the UK, Germany, France, Italy, Spain and Others), APAC (China, Japan, South Korea, India, Australia and Others) and RoW (the Middle East and Africa).

Key Takeaways

In the Warehouse Robotics market report, the autonomous mobile robots segment is analyzed to grow at a significant CAGR of 14.9% due to its high accuracy, increased efficiency and widespread applications across industry verticals.

The E-commerce industry is expected to grow at the highest rate with a CAGR of 15.2% owing to factors such as rising demand for distribution center automation, fulfillment automation, growing demand for order accuracy and rising competition among the companies.

North America held the largest market share of 34% in 2021 in the global Warehouse Robotics Market, owing to factors such as rapid R&D investments towards robotics and increasing adoption of robots for process automation.

Inquiry Before Buying

Warehouse Robotics Market Segment Analysis - by Product Type

Based on Product Type, the autonomous mobile robots segment in the Warehouse Robotics Market report is analyzed to grow with the highest CAGR of 14.9% during the forecast period 2022-2027. The growing adoption of these automated warehouse robots can be attributed to their widespread benefits such as high accuracy, increased efficiency and safer transportation of materials as they are equipped with sensors to avoid any collisions. In June 2021, DHL and Locus Robotics agreed to add 2000 autonomous mobile robots to the DHL supply chain by the end of 2022. This growing demand for AMRs would eventually increase the Warehouse Robotics market size.

Warehouse Robotics Market Segment Analysis - by End-use Industry

Based on End-user Industry, the E-commerce industry in the Warehouse Robotics Market report is analyzed to have the highest share. It is also expected to grow at a significant CAGR of 15.2% during the forecast period 2022-2027. The growing need for order accuracy, increased competition in the e-commerce industry, the rising need for fulfillment automation, distribution center automation and the proliferation of internet purchases are expected to propel the demand for automated warehouse robotics in the E-commerce industry. In June 2022, Epson introduced the GX Series SCARA robots to deliver next-level performance and flexibility. These GX4 and GX8 robots offer high throughput, smooth motion control and heavy payloads, thereby boosting the Warehouse Robotics Industry in the E-commerce segment.

Schedule a Call

Warehouse Robotics Market Segment Analysis - by Geography

North America dominated the global market for Warehouse Robotics Market with a 34% market share in 2021. It is also analyzed to have significant growth over the forecasting period. This growth is due to increased demand for distribution center automation, fulfillment automation, intelligent warehouse, warehouse digitalization across industries and a rise in R&D investments by the manufacturers towards warehouse robotics. In 2020, according to an Amazon report, the company installed more than 200,000 mobile robots that work inside its warehouse networks alongside human workers in the U.S. These developments positively influence the Warehouse Robotics Industry outlook during the forecast period.

Warehouse Robotics Market Drivers

An increase in R&D investments toward robots for process automation in warehouses:

In the past few years, the Warehouse Robotics ecosystem has seen a significant rise in investments. Due to this rising investment, new cost-effective, flexible and efficient robots are being installed across warehouses for process automation. These robots are automating various warehouse operations such as storage and retrieval, palletizing and de-palletizing, transportation and packaging. For instance, in May 2022, GreyOrange secured funding of US$110 million from Mithril Capital for improving its technology and expanding its business in the Warehouse Robotics industry.

Buy Now

Rapid technological advancements in robotics sensors and the incorporation of AI and ML:

Owing to the onset of Industry 4.0 and rising warehouse digitization across industries, the deployment of robots has significantly increased in the period of study. The incorporation of artificial intelligence and machine learning further enabled the robots with superior functionality, efficiency and accuracy. Technological advancements in robotic sensors are also facilitating the deployment of robots across end-use industries. These sensors provide the robots with higher precision and accuracy while operating. In February 2022, Celera Motion and ATI Industrial Automation partnered with MassRobotics for robotics sensors innovation. These developments would positively influence the Warehouse Robotics industry outlook over the forecast period.

Warehouse Robotics Market Challenges

Lack of a skilled workforce to operate the robots:

Warehouse Robotics is a multidisciplinary field where acquiring and retaining qualified workers is a major issue. There is a huge scarcity of individuals with specific backgrounds and skills, especially to develop high-value-added robots integrated with advanced technologies. Additionally, higher costs related to training & deployment and the difficulty interacting with robots are hampering the growth of the Warehouse Robotics Market during the forecast period.

Warehouse Robotics Industry Outlook

Product launches, collaborations and R&D activities are key strategies adopted by players in the Warehouse Robotics Market. The top 10 companies in the Warehouse Robotics market include:

ABB Ltd

Kuka AG

FANUC

Omron Automation

Yaskawa

River Systems

Honeywell International Inc.

Toshiba Corporation

Locus Robotics

Daifuku

Recent Developments

In May 2022, ABB launched the ABB Robotic Depalletizer, a solution for handling complex de-palletizing tasks in e-commerce, healthcare and logistics industries by enabling customers to efficiently process assorted loads. This is poised to increase the company’s share in the Warehouse Robotics Market.

In March 2022, FANUC introduced the new CRX-5iA, CRX-20iA/L and CRX-25iA collaborative robots. These robots can handle payloads weighing 4-35kgs. This feature boosts the adoption of these Warehouse Robotics across industry verticals.

In July 2021, Omron Automation launched a heavy-duty mobile robot with a payload capacity of 1500kgs. The HD-1500 mobile robot can handle bulky objects allowing manufacturers to expand their options for autonomous material transport.

0 notes

Text

Water Treatment Systems Market - Forecast(2022 - 2027)

Water Treatment Systems Market size in 2019 is estimated to be $5.85 billion and is projected to grow at a CAGR of 7.56% during the forecast period 2020-2025. Water is an essential constituent in the food and beverage industry. It is being used for cleaning raw materials and for the formulation of food and beverage products. Water scarcity and rising demand for water are increasing the demand for cost-effective water treatment technologies. Increased efforts from regulatory bodies to conserve and recycle water is also contributing to the growth of this market. In the food and beverage industry, water treatment systems are used to help achieve sustainable and clean drinking water as well as to manage wastewater.

Request Sample

Key Takeaways

Increasing demand for water treatment in the food and beverage industry to remove bacteria, brine and other contaminants, is a major factor driving the water treatment systems market.

The high cost of water treatment equipment is a major factor limiting the growth of the market during the forecast period 2020-2025.

By region, Asia Pacific accounts for a major share of the Water Treatment Systems Market, in 2019.

By Treatment Process - Segment Analysis

By the treatment process, the reverse osmosis systems segment is the fastest growing and is projected to grow at a CAGR of 7% during the forecast period 2020-2025. This is owing to the increasing use of reverse osmosis in the food industry to remove bacteria and brine in meat, or for alcohol removal from spirits. Reverse osmosis allows water to pass through a semi-permeable membrane, which acts as a filter and prevents harmful chemicals, organic materials, sediments, and other impurities to pass through. The resulting water is fresh and free from any contaminants. This treatment process also offers additional advantages such as removal of color, odor, chemicals or taste, and ensuring that there are no residual products. It is also fast, efficient and environmentally friendly, making this method’s usage very popular in various applications.

The treatment processes vary with the quantity of water to be purified and the end-use. For instance, countertop water filters are commonly used in residential water treatment equipment whereas inline filters are more efficient for industrial processes. On the other hand, UV water purifiers and charcoal water filters can be used in small-scale as well as large-scale applications.

Inquiry Before Buying

By Application- Segment Analysis

By application, the Beverage Industry is estimated to account for a major share of the Water Treatment Systems market during 2019. This is owing to the rising usage of water to manufacture mineral water, fruit juices, sodas, soft drinks, energy drinks, alcoholic beverages, and others. Every beverage requires a specific water treatment procedure. The beverage industry requires a large amount of water to manufacture their products. Furthermore, stringent manufacturing regulations to ensure hygienic beverages and increased efficiency of production processes are increasing the demand for these systems. Growing consumption of energy drinks with the rising health concern is set to contribute to the growth of the Water Treatment System Market during the forecast period 2020-2025.

Geography- Segment Analysis