maxihealth

Maxi Health

An experienced and dynamic public speaker with participation in countless seminars and workshops all over the country. I am also the panelist on health care topics at many events. I have presented many symposiums, which gave me a great opportunity to share with the audience education on health and its impact. I also serves on the Board of Directors for Health and Wellness Foundation. I am also a consultant for the food and beverage industry, corporate wellness, weight loss surgery, menu and product development, and has written numerous articles in an array of venues.

1833 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

aalleeexx

HardCore Life

xaviersfandomwriting

Fanfics, you say?

e2ropa

ارشدني

dialectlearn

Dialect Learn

demonictreegremlin

i live in the trees and speak for the mushrooms i will bite you

Text

On behavioral change, health and age

A Health Affairs article (Meyer 2021) discusses the potential benefits of Medicare Diabetes Prevention Programs (MDPP). MDPP aims to reduce patient weight and prevent patients from becoming diabetic. Commenting on her Medicare clientele enrolled in the program, one instructor noted:

“I’ve seen a lot of Medicare people do really well with the program because they have more time than younger people who are working or raising children,” she said. “But Medicare folks may have a harder time making [lifestyle] changes because they’ve been doing things the same way for a long time.”

MDPP was the first Center for Medicare and Medicaid Innovation (a.k.a., CMMI; a.k.a., the CMS Innovation Center) demonstration of a preventive care model that was expanded to program available to al Medicare beneficiaries. However, uptake of the program is poor; only 3,600 Medicare beneficiaries across the nation have taken advantage of the MDPP benefit.

On behavioral change, health and age posted first on https://carilloncitydental.blogspot.com

2 notes

·

View notes

Text

How much money should governments spend to incentivize the development of new antibiotics?

As the number of infections that are anti-biotic resistant grows, we need to have more novel antibiotics in our arsenal. The problem is that many antibiotics are not commercially viable. For instance, if a new antibiotic is marginally better than the existing one, few payers will be willing to cover this cost. However, if new bacteria become resistant to the standard of care antibiotic, then the novel antibiotic would be highly valued. In short, antibiotics have a very high option value.

There have been a number of approaches to try to incentivize new R&D on antibiotics, including various prizes and subscription models.

The most prominent examples of antibacterial subscriptions are the pilot program created in 2019 by the National Health Service England (the UK pilot)14,15 and the Pioneering Antibiotic Subscriptions to End Upsurging Resistance (PASTEUR) Act, which was reintroduced in 2021 in the US Congress.16 In a subscription, the company is paid an annual subscription amount and agrees to provide as much of the antibacterial as is needed by the subscriber at no additional cost. As with earlier proposals to offer prizes for successful antibacterial R&D,17–20 one key question is the appropriate size of the pull incentive

A key question is how large these incentives should be. Some previous literature have proposed the following amounts:

Department of Health and Human Services. Push and pull incentives should be $919m (2012 USD) for a single indication. (Sertkaya et al. 2014)

Review on Antimicrobial Resistance (AMR Review): Market entry rewards should be $800m to $1.3 billion USD, plus an additional $400m per year in research grants. (O’Neill 2016)

German Federal Ministry of Health’s Global Union for Antibiotics Research and Development report. $1 billion global launch reward–similar to a market entry award–plus $400 million in push incentives per year. Half of the $400m would go to preclinical research and the other half to clinical research. (Bundesministerium für Gesundheit 2011)

DRIVE-AB. The acronym stands for “Driving reinvestment in research and development for antibiotics and advocating their responsible use”; DRIVE-AB was a consortium of academics and industry experts. It was funded by the European Commission’s Innovative Medicines Initiative. DRIVE-AB recommended a $1 billion global market entry reward (pull), plus $800m in research funding (push) and ideally peak year sales of >$1 billion would lead to 18 new antibacterial medications over 3 decades. (Årdal et al. 2018; Okhravi et al. 2018)

World Health Organization (WHO) report. This report largely averages the estimates from previous reports. (Breyer et al. 2020; WHO 2020)

A paper by Outterson (2021) in Health Affairs published today aimed to update these estimates. He creates a net present value (NPV) calculation which depends on development cost (i.e., cost, duration and probability of success for any phase in the drug development process); revenues and expenses after antimicrobial approval; and the discount rate. The authors models different approaches to reach the NPV: based on global peak year sales (GPYS); based on a market entry reward paid in one year (MER1); based on subscription paid over ten years (SUB10); of based on the acquisition of a Phase II-ready asset (AQ). Using these approaches, Outterson finds that:

The partially delinked market entry reward required for an asset acquired at the initiation of Phase II was $1.6 billion (best estimate), with the upper and lower-bound estimates being $2.6 billion and $900 million, respectively (MER1 + ACQ). For a fully delinked subscription, the results are $3.1 billion (best estimate), with the upper and lower bounds being $4.8 billion and $2.2 billion, respectively.

The level of global peak year sales (GPYS) required for profitable antibiotic R&D is $1.9 billion (range: $1.6–$3.8 billion), which is a significantly higher sales amount than that achieved by any recent antibacterial. Only two antibacterials launched since 2000 have achieved $1 billion in peak sales: linezolid (Zyvox), with $1.353 billion in 2015 (launched in April 2000), and daptomycin (Cubicin), with $1.312 billion in 2016 (launched in November 2003)…

The partially delinked global market entry reward required (MER1) is $2.2 billion (best estimate), with lower- and upper-bound estimates of $1.5 billion and $4.8 billion, respectively…

The fully delinked global subscription required over the course of ten years (SUB10) is $4.2 billion (best estimate), with lower- and upper-bound estimates of $3.3 billion and $8.9 billion, respectively

The authors find that subscriptions are more expensive because (i) subscriptions are delinked from actual volumes and thus manufacturers must make the drugs without potentially any compensation (beyond the subscription); and (ii) payments are pushed into the future and thus additional funds must be found to compensate for the reduced time-cost of revenues received in the future. They also find that push incentives alone are typically insufficient to bring new antimicrobials to market.

The article is interesting throughout and do read the whole article here.

How much money should governments spend to incentivize the development of new antibiotics? posted first on https://carilloncitydental.blogspot.com

2 notes

·

View notes

Text

Health Consumers, Health Citizens, and Wearable Tech – My Chat with João Bocas

The most effective, engaging, and enchanting digital health innovations speak to patients beyond their role as health consumers and caregivers: digital health is at its best when it addresses peoples’ health citizenship.

I had the great experience brainstorming the convergence of digital health, wearable tech, user-centered (UX) design, and health citizenship with João Bocas, @WearablesExpert, in a on his podcast.

And if those topics weren’t enough, I wove in the role of LEGO for our well-being, “playing well,” and inspiring STEM- and science-thinking.

João and I started our chat first defining health citizenship, which is a phrase I first learned from European Commission bioinformatics leader Jean-Claude Healy whom I met when I first worked in Europe. After hearing the words “health citizenship,” the concept stayed with me over the years I’d been working as an advisor to the health/tech industry across every part of the health ecosystem.

Once I actually became a health citizen in the EU, I’ve made the personal professional, incorporating the concept as part of my work on ESG principles in health care with my clients and collaborators.

The coronavirus pandemic has surely revealed the importance of public health and the nature of the fragile safety net for people under-served and left out of health/care access.

Our chat then segued to how digital health tools and platforms can help scale health and well-being to address barriers to the social determinants of health and well-being, when well-intended and enchanting design can do good and do well at the same time. THINK: food security, transportation, on-line scheduling, expanding access to mental and behavioral health programs, and bolstering peoples’ digital access and literacy especially among people long under-served by the brick-and-mortar health care system.

We concluded with João’s signature question of “1 Minute of Fame,” an open-ended ask for me to riff on anything I felt like riffing on. I noted that the day before was International Day of the Girl, giving a shout-out to my daughter (a delightful digital designer herself) as well as LEGO and our family’s LEGOmaniacal ways.

“LEGO” from its Danish roots was named as such based on the words “Leg Godt,” meaning “Play Well.” My end-note was a call-to-action for all of us in the health care ecosystem to Play Well.

Health Populi’s Hot Points: Part of Playing Well in health care, globally, is to keep Health Citizenship in mind when conceiving, planning for, and designing health care products and services.

There are four key pillars to Health Citizenship, as I discuss in my book titled just that (with the sub-title: “How a virus opened hearts and minds”).

First, healthcare access for all — as a civil right.

Second: digital citizenship, bolstering privacy (a la the GDPR or California’s CCPA) which ensures people as health citizens (and citizens overall) have a right to be forgotten and to control their personal data.

Third: trust as a precursor to civil engagement. Without trust, there’s no commons or collective respect to nurture public health and other broad commitments and objectives to making life better for everyone.

Fourth, finally, let’s imagine together a new social contract of love, as in Love Thy Neighbor as Thyself.

The post Health Consumers, Health Citizens, and Wearable Tech – My Chat with João Bocas appeared first on HealthPopuli.com.

Health Consumers, Health Citizens, and Wearable Tech – My Chat with João Bocas posted first on https://carilloncitydental.blogspot.com

1 note

·

View note

Text

Vaccine hesitancy in low- and middle-income countries

While the recently developed COVID-19 vaccines offer the hope of ending the pandemic, ending the pandemic is only feasible if individuals take the vaccine. In the US, a large portion of individuals report being hesitant to receive the vaccine. A key question then is whether individuals living in low and middle-income countries (LMIC) are have high rates of vaccine hesitancy.

A paper by Solís Arce et al. 2021 answers this question by conducting a survey of nearly 45,000 individuals living in 10 LMICs, Russia and the United States. The authors find that: , including a total of 44,260 individuals

The average acceptance rate across the full set of LMIC studies is 80.3% (95% confidence interval (CI) 74.9–85.6%), with a median of 78%…The acceptance rate in every LMIC sample is higher than in the United States (64.6%, CI 61.8–67.3%) and Russia (30.4%, CI 29.1–31.7%). Reported acceptance is lowest in Burkina Faso (66.5%, CI 63.5–69.5%) and Pakistan (survey 2; 66.5%, CI 64.1–68.9%).

Across individuals who were willing to take the vaccine, the main reason for taking the vaccine was personal protection, with family protection typically coming in second place. Across individuals who were not willing ot take the vaccine, the main reason was concern over side effects, although some countries (Mozambique, Uganda and Pakistan) noted skepticism over vaccine efficacy.

Vaccine hesitancy in low- and middle-income countries posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Why CrossFit and 23andMe Are Moving from Health to Primary Care

As we see the medical and acute care sector moving toward health and wellness, there’s a sort of equal and opposite reaction moving from the other end of the continuum of health/care: that is, wellness and fitness companies blurring into health care.

Let’s start with the news about CrossFit and 23andMe, then synthesize some key market forces that will help us anticipate more ecosystem change for 2022 and beyond.

CrossFit announced the company’s launch of CrossFit Precision Care, described as primary care that provides personalized, data-driven services for “lifelong health,” according to the press release for the program.

The service is based on four components:

Genomic testing to identify a consumer’s genetic advantages, disadvantages and predispositions

Blood testing to assess cardiovascular risks, hormone status, lipids, minerals, thyroid function, and other factors that shape health and performance

Longevity analysis to estimate a person’s biologic age (using a DNA methylation test kit, adding in the genomic and blood tests), and

Lifestyle review which formulates eating plans, exercises, family and social life, sleep, hobbies, recreation, and personal goals.

The program was developed by Dr. Julie Foucher and fellow CrossFit-trained physicians collaborating with Wild Health, which has developed what it calls a “platform for personalized medicine” with which the CrossFit Precision Care looks to be linked. Wild Health calls its Clarity algorithm “the world’s first true precision medicine algorithm” applying machine learning to DNA analysis, biometrics, microbiome studies, and phenotype data.

Dr. Foucher, a family medicine physicians, is a former CrossFit Games athlete.

Speaking of genomic testing….how does 23andMe fit into the health-to-healthcare scenario? The company acquired Lemonaid Health this week, bringing together the consumer-facing genomics company with a prescription drug distribution channel for the purpose of channeling personalized medicine to consumers. This combination is meant to deliver, in the words of 23andme, “individualized primary care that empowers consumers to live healthier lives.”

Lemonaid Health has married prescription drug deliver with telemedicine, one of the group of companies akin to Ro, Hims & Hers, and Nurx, among others.

Anne Wojcicki, the CEO and Co-Founder of 23andMe, explained that the merging of Lemonaid Health’s telehealth platform, underpinned with its team of medical professionals and pharmacy services, will combine with 23andme’s genetics expertise to bring personalized healthcare, “empowering people to take control of their health.”

Together, these two cases — occurring within days of each other — tell us a lot about how U.S. healthcare is accelerating into peoples’ hands, homes, and hearts. The converging factors are:

Primary care

Telehealth

Retail health

Genetic testing, and

Collaboration and combination.

It’s that #1 pillar we’ll focus on in the Hot Points, below.

Health Populi’s Hot Points: We only have to look back a matter of here days to understand how profoundly the new-new primary care acceleration is happening. Just last week, Walgreens Boots Alliance announced a doubling down on primary care, mental health services, and telehealth including a $5 billion further investment in VillageMD (giving the company a larger share of the clinic firm). Per the press release, WBA is “reimagining retail through expanded health and wellness offerings and mass personalization.”

CVS Health, which has been building its own primary care vision for several years through the HealthHub, Aetna, and other investments, has a new vision for “SuperClinics” as coined by Karen Lynch, CEO, in a profile of her in Fortune magazine’s Most Powerful Women of 2021.

And, several other news items further paint the current portrait of primary-care-in-motion…

One Medical’s acquisition of Iora Health

The launch of Marley Medical, to fill the gaps in primary care for people managing chronic conditions (important to mention initial investors in the company are “OGs” [as the press release says) including digital health pioneers like Anne Wojcicki, David Van Sickle, Halle Tecco, Thomas Goeta, among others who know how to build sustainable digital health ventures}

Health plans launching “virtual first” plans, such as Humana working with Doctor on Demand, UnitedHealthcare and Optum, Oscar, and Cigna aligned with MDLive, and

Teladoc’s expanding its virtual primary care program, Primary360, growing from its core telehealth roots,

among many other primary care-focused ventures leveraging virtual care and collaborations.

Finally, never under-estimate what Amazon Care and the company’s other health care workflows can/will do in primary care.

The fact is that nations that invest in resilient, strong primary care backbones ultimately spend less per health citizen than the U.S., with a fragmented on-ramp to primary care for millions of consumers lacking access to upstream, preventive and early-detecting services. This current bullish phrase for new primary care suppliers and business models will add chaos before creation and consolidation where we learn which models work toward the Quintuple Aim.

We will continue to see the mashup and blurring of primary care with personalized medicine, with models built on omnichannel approaches designed for every kind of people if suppliers are design-ful.

The post Why CrossFit and 23andMe Are Moving from Health to Primary Care appeared first on HealthPopuli.com.

Why CrossFit and 23andMe Are Moving from Health to Primary Care posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Mid-week reading

CBO analysis of the Build Back Better Act.

Information frictions helps explain why there isn’t more behavioral response to government interventions.

Wealth = networks, not assets.

Impact of same sex legalization on mental health.

Patient selection in CJR.

Mid-week reading posted first on https://carilloncitydental.blogspot.com

0 notes

Text

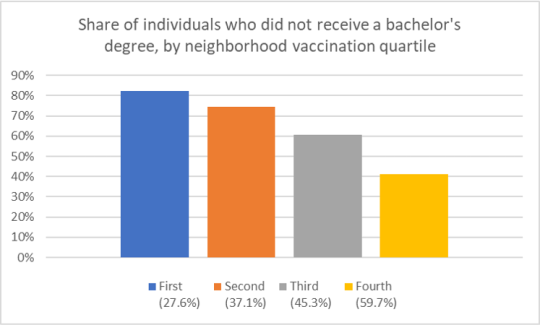

Characteristics of neighborhoods with high and low COVID-19 vaccination rates

What do the vaccination rates look like in the largest U.S. cities? In these cities, how do the characteristics of individuals in neighborhoods with low vs. high vaccination rates differ?

To answer this question, a paper by Sacarny and Daw (2021) use data from 9 large US cities: New York, Los Angeles, Chicago, Houston, Phoenix, Philadelphia, San Antonio, San Diego, and Dallas. Specifically, they gather data on COVID-19 vaccination and death rates for these cites from health authority websites and sociodemographic information from the American Community Survey (ACS).

They find that neighborhood with high vaccination rates have: (i) more Whites and Asians and fewer Blacks and Hispanics, (ii) more people who received a bachelor’s degree or higher, and (iii) higher income levels, (iv) a higher share of individuals aged 65 and above. Unsurprisingly, COVID-19 deaths are lower in the highly vaccinated neighborhoods in these cities.

Characteristics of neighborhoods with high and low COVID-19 vaccination rates posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Still Struggling with Stress in America in 2021

“Americans remain in limbo between lives once lived and whatever the post-pandemic future holds,” the American Psychological Association observes in their latest read into Stress in America 2021, with this phase of the perennial study focused on Stress and Decision-Making During the Pandemic.

The top-line: people face a daily web of risk assessment, up-ended routines, and endless news about the coronavirus locally and globally.

While most people in the U.S. believe that “everything will work out” after the pandemic ends, the mental, emotional, and logistical daily distance between “now” and “then” brings uncertainty and indeed, prolonged stress.

More Millennials, who generationally are sandwiched between older and younger people. feel the stress compared with other age groups — with Gen Z and Gen Xers following. Boomers and older people in America are less likely to feel so stressed by the pandemic, they struggle to make even the most basic decisions.

Those basic decisions, the APA details, can be as seemingly simple as what to eat, where to eat, or what to wear.

One in two people said the COVID-19 pandemic has made their planning for the future feel impossible.

For parents, the strain has grown from 2020 into 2021: family responsibilities are a significant source of stress, and relationships are a source of stress. Thus, 4 in 5 parents said that they could have used more emotional support than they received over the past year.

Furthermore, pandemic stress among people of color continues to be greater than stress on white Americans overall — especially among Hispanic adults who reported the highest levels of stress related to the pandemic. Their stress index topped at 5.6 versus 5.1 for Black as well as Asian adults, and 4.8 for non-Hispanic white adults in the U.S.

Why would Hispanic adults in the U.S. be hit disproportionately with stress in the pandemic era? Because of the unequal burden Hispanic people carry in the wake of COVID-19: more Hispanic adults were more likely to struggle with stress int he pandemic, more likely to know someone who had been sick or died of complications due to the coronavirus (42% versus 25% of non-Hispanic white adults).

The second chart details the most significant sources of stress from 2019 into 2021. Those stress sources that increases in the three years were, in terms of statistical significance:

The economy, increasing from 46% stressed to 59% stressed

Housing costs, growing from 45% stressed to 51% stressed

Personal safety, increasing from 35% stressed to 44% stressed, and,

Discrimination, climbing from 25% stressed to 32%.

As a result, three in four U.S. adults have experienced some behavioral impact due to stress, such as headaches (34%), feeling overwhelmed (34%), fatigued (32%), or changes in sleep (32%). These were more likely to impact younger people than older folks in the U.S.

The APA’s August/COVID Resilience Survey was conducted online by The Harris Poll in August 2021 among 3,035 U.S. adults 18 and over.

Health Populi’s Hot Points: Those pandemic-era headaches and sleep habit changes have been impacting more younger people than older people in America, shown in the last chart.

In addition to pain and sleep impacts, over one-third of people said they are eating to manage stress, roughly the same percentage in 2021 as recorded in 2020.

This study crafted a Resilience Scale to measure how people responded to stress in 2021. Over one-half of people said they are struggling with the “ups and downs” of the pandemic: one-fourth were considered being of low resistance in the APA scale, measured as 1.00 to 2.99 out of 10.0. 48% of people in America had an average resilience index of 4.31 to 5.00.

Younger people, parents, and people with less than $50,000 in household income were more likely to have low resilience scores. These people were more likely to say their stress was higher in the past month than earlier in the pandemic, as well as higher than before the pandemic.

This group of highly-stressed people were also more likely to say they struggled to make basic daily decisions.

They also felt they could have used more emotional support than they received over the past year.

The pandemic certainly gave us the gift of knowledge in having to face the ubiquity of mental health in Americans’ overall health and well-being….or lack thereof. Most people in the U.S. have been faced with mental and behavioral stressors and subsequent physical manifestations of that stress in eating, sleeping, and daily decision making fog.

The growing supply of teletherapy serving more people at scale who need and want to access services has been encouraging to see, with investments in digital mental health hitting $3.1 billion and $793mm for substance use disorder for the first three quarters of 2021 based on Rock Health’s numbers. Galen Growth calculated that some $6.12 billion has been invested in mental health digital health cumulatively from 2017 to H1 2021.

The leader of the ATA (American Telemedicine Association), Ann Mond Johnson, has a mantra that #TelehealthIsHealth.

That is indeed the case. Now, on to scaling this for all who need access to quality, truly accessible mental and behavioral health services. For health citizen/patient demand to meet up with that growing supply side will require health plans, payment designs, and social barriers to align.

The post Still Struggling with Stress in America in 2021 appeared first on HealthPopuli.com.

Still Struggling with Stress in America in 2021 posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Cato supports public option?

A white paper from Cannon and Pohida (2021) calls for applying “public option principles” to Medicare. Who would have thought that the Cato Institute would call for a public option?

Well in fact, the do not really call for a public option. The proposal should be called introducing a voucher system into Medicare. Under the proposals, Medicare beneficiaries would receive a fixed voucher–adjusted for income and health status–that individuals could used to pay for premiums for whatever insurance they choose, public (Medicare Fee-for-service) or private (Medicare Advantage). The approach is not too dissimilar from one previously proposed by the American Enterprise Institute (AEI) titled “The Best of Both Worlds.” The authors authors explain why they believe this would be a useful system, writing:

Economists have proposed eliminating these perverse incentives by having Medicare directly pay each enrollee a fixed subsidy the enrollee can apply to either traditional Medicare or private insurance. Program administrators would take the money Medicare otherwise would pay to providers and insurers and give those funds directly to enrollees as a monthly payment, just as Social Security does. In 2022, they would divide $783 billion among the program’s 66 million enrollees, such that enrollees would receive an average subsidy of $11,900. Medicare would then adjust individual allotments according to each enrollee’s health status and income (see below), such that all enrollees could afford a standard health insurance plan comparable to traditional Medicare. The net effect is that enrollees would receive approximately the same subsidy they would under current law.

A key issue is how well can people shop across plans. Are quality measures clear? Are the meaningful? Are they free from provider gaming?

The authors cite a paper where Don Berwick–a former CMS administrator–notes that the current provider payment schemes may not incentivize quality.

Even if payment schemes were sensitive to quality, and even if consumers could see the difference between better and worse care, [incentives for quality] improvement would be weakened by the distance between the patients and the payment rules. People and payers who might be quite willing to pay a premium for more fully integrated chronic disease care, for the option of a group visit, or for detailed management of their lipid medications do not have the option to do so because of fixed fee schedules and complex payment rules. This is particularly true under Medicare. In effect, people do not have the option to pay for what they want, even if what they want is better than what they have.

As I posted recently, Medicare now has a large number of value-based programs, but not many of these alternative payment models have had a large impact on quality.

The authors claim that the voucher-based system will lead to more creative ways to pay providers.

…public-option principles require eliminating favoritism toward fee-for-service payment, or whatever payment rules the government plan happens to employ. Applying that principle to Medicare would increase demand for prepaid group plans and other non-fee-for-service arrangements, promoting dimensions of quality Medicare currently discourages

Also, more standardization of health plans makes it easier to shop across plans; standardizing, however, leads to less innovation as well. The major underlying assumption is that by allowing more competition, cost should fall and outcomes should rise. Skeptics would point out that administrative costs will likely rise as health plans compete and there could be more cost savings with a single payer option. While the later point is valid in a static setting; over the long-run competition tends to be the most effective way to bring down cost.

Another key issue is, how does one adjust for health status and income? While in principle this is easy to do (Medicare Advantage already has their subsidies from CMS risk-adjusted for health status), in practice health systems and insurers may have more information than does the government when making this adjustment. Further, transitory employment shocks–while less of an issue for the Medicare population–can make estimating individual income a challenge.

Despite these numerous challenges, the idea is interesting and the white paper is worth read.

Cato supports public option? posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Weekend Reading

Here are some questions to get your weekend reading started.

Can Yelp predict hospital mortality?

Can AI solve a radiologist shortage in the UK?

How do we get the LA/Long Beach port back up and running?

Why is CMS in Baltimore rather than DC?

What to do when you’re down to your last diaper?

Weekend Reading posted first on https://carilloncitydental.blogspot.com

0 notes

Text

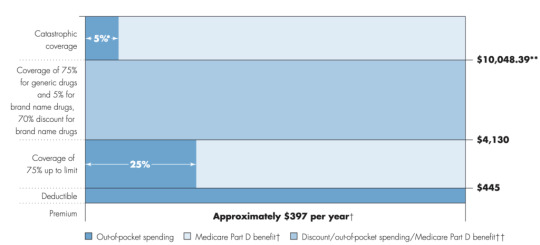

Part D Senior Savings Model: What is it?

If you are on Medicare, how much will you pay for insulin? The answer is in the graph below (via MedPAC’s Payment Basics)

Seem confusing? Well it is. Medicare Part D beneficiaries have a deductible, then the standard coverage phase with 25% cost sharing, then a coverage gap where beneficiaries pay 25% of cost (manufacturers cover 70% of the cost for branded drugs in this coverage gap), and then a catastrophic phase where beneficiaries pay 5%. Wouldn’t it be easier if there were simple copayments like many commercial plans?

That is what CMS has been trying out in their Part D Senior Savings Model. The model includes fixed copayments for certain enhanced Part D plans. CMS writes:

The voluntary Model tests the impact of offering beneficiaries an increased choice of enhanced alternative Part D plan options that offer lower out-of-pocket costs for insulin. CMS is testing a change to the Manufacturer Coverage Gap Discount Program (the “discount program”) to allow Part D sponsors, through eligible enhanced alternative plans, to offer a Part D benefit design that includes predictable copays in the deductible, initial coverage, and coverage gap phases by offering supplemental benefits that apply after manufacturers provide a discounted price for a broad range of insulins included in the Model.

As described by former CMS administrator Seema Verma in the Health Affairs blog:

MS’s Part D Senior Savings Model is designed to lower prescription drug costs by providing Medicare patients with Part D plans that offer the broad set of insulins that beneficiaries use at a stable, affordable, and predictable cost of no more than $35 for a 30-day supply…beneficiaries who do not qualify for the low-income subsidy (LIS) currently pay 5 percent of the negotiated price when they reach the catastrophic phase, which should be lower than $35 in most cases. Part D sponsors could offer lower copays than $35 and still maintain all formulary flexibilities and choices.

Sharon Jhawar, Chief Pharmacy Officer at the SCAN Health Plan argues that the Senior Savings Model is working, should be made permanent, and should be expanded to both other diabetes medications and medications used to treat other common chronic conditions. Previous research shows that cost is a barrier to medication adherence, and she writes:

Let’s accelerate the timeline for making the Model permanent and use the expected cost-savings ($250 million per year) to advance other health initiatives for Medicare beneficiaries with diabetes…Yet diabetes is only the fifth most common chronic condition among Medicare beneficiaries. People with other chronic conditions, such as heart conditions, neurological conditions, or auto-immune diseases, will encounter the same financial challenges we see in the diabetes medication scenario. With a successful template in place to manage costs, we have a unique opportunity to reduce prescription costs across the board.

For more information, read the CMS Senior Savings Program Fact Sheet and visit their website.

Part D Senior Savings Model: What is it? posted first on https://carilloncitydental.blogspot.com

0 notes

Text

CMMI and its revised strategy

Created by Section 3021 of the Affordable Care Act (ACA), the Centers for Medicare and Medicaid Innovation (CMMI; aka The CMS Innovation Center) has been tasked with creating new reimbursement strategies to improve quality and decrease costs. Over the past decade, CMMI has tested over 50 new payment models, and in just the last 3 years (2018-2020) CMMI models have reached almost 28 million patients and over half a million health care providers and plans.

Despite these ambitious goals, CMMI reports that “only six out of more than 50 models launched generated statistically significant savings to Medicare and to taxpayers and four of these met the requirements to be expanded in duration and scope.”

In their recently released white paper “Innovation Center Strategy Refresh.” CMMI claims to have learned the following lessons:

Ensure health equity is embedded in every model

Streamline the model portfolio and reduce complexity and overlap to help scale what works.

Tools to support transformation in care delivery can assist providers in assuming financial risk.

Design of models may not consistently ensure broad provider participation.

Complexity of financial benchmarks have undermined model effectiveness.

Models should encourage lasting care delivery transformation.

Some interesting points from the report include:

Medicare FFS beneficiaries will be in an accountable care relationship with providers and will have the opportunity to select who will be responsible for assessing and coordinating their care needs and the cost and quality of their care.

The above seems obvious, but previously, beneficiaries were attributed to physicians typically based on the number of physician visits (often just evaluation and management [E&M] visits). This meant that some patients who would be overseen by a specialist during an acute bout of a disease would be then held responsible for all of a patient’s cost. Further, neither the patient nor the provider would know to which physician the patient would be attributed. While this approach may seem confusing, the benefit was attribution could be done passively; while more active attribution probably makes sense, it is unclear whether patients will actively select providers to manage their care or what will be needed to incentivize patients to do so.

The CMS Innovation Center will address barriers to participation for providers that serve a high proportion of underserved and rural beneficiaries, such as those in Health Professional Shortage Areas (HPSAs) and Medically Underserved Areas (MUAs), and designated provider types such as Federally Qualified Health Centers (FQHCs), rural health clinics (RHCs), and other

safety net providers and create more opportunities for them to join models with supports needed to be successful.

A key question is how CMS will do this. One approach would be to set lower quality or less strict cost evaluations for these types of providers. While doing so would make participation in alternative payment models more attractive, it would also create a two-tiered system with lower quality standards for disadvantaged beneficiaries in HPSA and MUAs who are often treated at FQHCs, HCS and other safety net providers. CMMI have not spelled out explicitly how they plan to accomplish this equity quote. The only concrete action CMMI mentions is collecting data on race, ethnicity and geography to examine health disparities.

Drawing on more diverse beneficiary, caregiver, and patient perspectives will systematically inform development of models that test care delivery changes and innovations that are meaningful and understandable to them….Providers participating in models, particularly total cost of care models, will have access to more payment flexibilities that support accountable care, such as telehealth, remote patient monitoring, and home-based care.

This is clearly a good idea. How to implement more patient-centered care, however, is a challenge. It is good to see that CMS is considering allowing for payment flexibilities around telehealth going forward, but it is not clear why this flexibility would only be extended to providers in total cost of care models; all providers should be able to leverage telehealth to improve patient access and outcomes, not just those in total cost of care models.

CMMI also proposes to lower beneficiary out-of-pocket cost spending, but focuses only on increased use of generic and biosimilars. The Innovation Center also calls for the use of value-based insurance design (VBID). While VBID is sensible, health economic analysis will be needed to determine what treatments qualify as “high-value” and would be subject to low patient cost sharing.

To achieve some of these goals, the CMS Innovation Center aims to go ‘all-in’ on value-based reimbursement and is attempting to expand these payment schemes beyond Medicare. Specifically, they aim to measure their progress as follows:

All Medicare beneficiaries with Parts A and B and most Medicaid beneficiaries will be in a care relationship with accountability for quality and total cost of care by 2030.

Where applicable, all new models will make multi-payer alignment available by 2030.

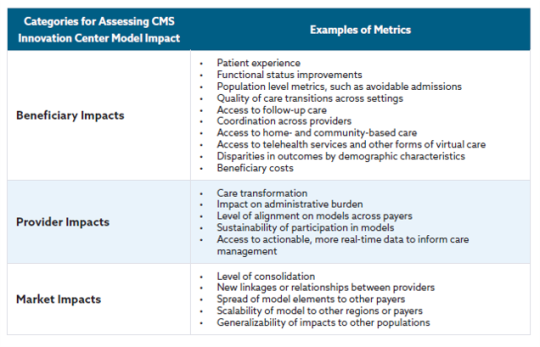

Below is a table describing how CMS will measure success for different stakeholder groups.

There is much more in the white paper and you can read the full document here.

CMMI and its revised strategy posted first on https://carilloncitydental.blogspot.com

0 notes

Text

“Complexity is Profitable” in U.S. Healthcare – How to Save a Quarter-Trillion Dollars

In the U.S., “Health care is complicated because complexity is profitable.”

So explain Bob Kocher, MD, and Anuraag Chigurupati, in a viewpoint on Economic Incentives for Administrative Simplification, published this week in JAMA.

Dr. Kocher, a physician who is a venture capitalist, and Chigurupati, head of member experience at Devoted Health, explain the misaligned incentives that impede progress in reducing administrative spending.

This essay joins two others in the October 20, 2021 issue of JAMA which highlight administrative spending in American health care:

Administrative Simplification and the Potential for Saving a Quarter-Trillion Dollars in Health Care by Nikhil Sahni, Brandon Carrus, and David Cutler (from Harvard and McKinsey); and,

Administrative Expenses in the US Health Care System – Why So High? asked and answered by Michael Chernew and Harrison Mintz, both of Harvard Medical School.

Sahni and colleagues published the data-details in an article published by McKinsey & Company, the top-line of which appears in the first graphic from the publication.

Administrative spending comprise 25% of the $3.8 trillion of health care spending in 2019; medical spending received 75% of the U.S. health care dollar.

What’s included in that admin spend includes:

“Industry-agnostic” corporate functions such as general administration, human resources, nonclinical IT, sales and marketing and finance;

Financial transactions, such as claims processing, revenue cycle management, and prior authorization (about $200 bn annually); and,

Customer and patient services (such as call centers, all together worth about $80 bn/year).

The team noted in their JAMA viewpoint that over 1 million administrative employees were added to U.S. health care employment since 2001, today accounting for twice as many staff as physicians and nurses.

Addressing administrative flows both inside and outside health care organizations can save money; take the lack of interoperability between claims systems between payers and hospitals and other aspects of lack of standardization and fragmented data systems. This represents a $210 billion savings opportunity, shown in the McKinsey model.

At the industry level, Sahni’s team calculated a potential $105 bn of savings each year by streamlining the financial transactions ecosystem and operational functions like clinical credentialing.

Taken in aggregate, the administrative cost conserving potential is over one-quarter of a trillion (with a “T”) dollars each year — equal to about $1300 per U.S. adult.

Health Populi’s Hot Points: Consider just the line item of “customer and patient services,” and one of all of our least-favorite patient experiences: the dreaded call center.

This last graphic from the McKinsey report illustrates the pain points for patients engaging with payers’ call centers. There’s lot of friction and unpleasantness in this experience.

At the same time, patients-as-consumers are clamoring for delightful digital journeys on par with their best retail experiences, from health care and every touchpoint they encounter.

Sadly, the latest ACSI Index gauging customers’ satisfaction with health plans and hospitals found these experience to be on par with the US Postal Service, gas stations, and other less-than-stellar experience performers with the Net Promoter Scores to prove it.

As it turns out, the health plans that served up the best digital experiences via well designed apps and websites garnered higher experience scores.

Holding health care back is the lack of digitization in general, and then the under-investment in user-centered design to engage and then retain patients beyond an initial download or visit to a patient portal.

This diagram from the McKinsey study organizes data from a project with which I’d been long affiliated, the CAQH Index of electronic adoption of claims transactions. We’re talking claims here — not an app to manage a complex condition like diabetes or even a medication adherence tool.

Claims — that’s the paper-based workflow that eats up some of the $billion U.S. health care administrative spend that could be freed up to, for example, cover more peoples’ health insurance or extend food benefits to bolster nutrition security and prevent physical wasting during cancer treatment for a person enrolled in Medicaid.

Paper Kills, as Newt Gingrich asserted in 2005 talking about the importance of electronic medical records about the time we started the CAQH Index project. It still does.

The post “Complexity is Profitable” in U.S. Healthcare – How to Save a Quarter-Trillion Dollars appeared first on HealthPopuli.com.

“Complexity is Profitable” in U.S. Healthcare – How to Save a Quarter-Trillion Dollars posted first on https://carilloncitydental.blogspot.com

0 notes

Text

The Pitfalls of Cost Sharing in Healthcare

Cost sharing is just that, sharing in the cost of providing a health care service. While health insurers often pay for a large share of health care cost (for those covered), individuals also contribute through deductibles, copayments and coinsurance. The goal of cost sharing is to reduce moral hazard. Moral hazard occurs when the price of a good is below its marginal cost, people will consume more of it. However, because the benefits of health care treatment are often long-term, can be difficult to observe, and often come with side effects, the costs and benefits that a patient observes may not be the same as the actual cost of production and cost sharing may discourage the use of cost-effective, high-value medical or pharmaceutical interventions.

Aaron Carroll at Incidental Economist provides nice overview summary of the potential benefits and key pitfalls of cost sharing.

youtube

This video was adapted from a column written at the Upshot and links to sources can be found there.

The Pitfalls of Cost Sharing in Healthcare posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Health Plan Consumer Experience Scores Reflect Peoples’ Digital Transformation – ACSI Speaks

In the U.S., peoples’ expectations of their health care experience is melding with their best retail experience — and that’s taken a turn toward their digital and ecommerce life-flows.

The American Customer Satisfaction Index Insurance and Health Care Study 2020-2021 published today, recognizing consumers’ value for the quality of health insurance companies’ mobile apps and reliability of those apps.

Those digital health expectations surpass peoples’ benchmarks for accessing primary care doctors and specialty care doctors and hospitals, based on ACSI’s survey conducted among 12,274 customers via email. The study was fielded between October 2020 and September 2021.

Year on year, few experience benchmarks significantly shifted between 2020 and 2021, the first bar chart shows.

Other key experience metrics for health insurance companies address the website, coverage of services, prescription drug coverage, ease of claims submission, experience with the call center, ease of understanding statements, range of available plans, and timeliness of claims processing.

The study also gauged consumers’ satisfaction with ambulatory care and hospitals, whose benchmarks barely shifted between 2020 and 2021:

Inpatient care remained flat at an index of 70

Outpatient care inched up from 73 to 74

Emergency room experience stayed at an index of a (low) 66.

Health consumer satisfaction scores with health plans average out at 73 on the ACSI index in 2021, up slightly from 2020. This varied by health insurer, with the Blue Cross and Blue Shield brand (rising 4%) and Kaiser Permanente (rising 3%) tops at 75, followed by Humana and UnitedHealthcare a point lower at 74.

Cigna fell the most in this health plan field, dropping from the index of 71 in 2020 to 68 in 2021.

All other plans landed at 73.

The ACSI study covering health care annually includes property & casualty insurance as well as life insurance companies. For comparison,

P&C insurance companies average a satisfaction index at 78, led by GEICO and State Farm at 79 in 2021

Life insurance companies garnered a satisfaction index overall at 78, with Allstate and State Farm at 79.

Health Populi’s Hot Points: Consumers’ health care experiences rank relatively lower than peoples’ satisfaction with grocery stores, full-service restaurants, soft drink brands, mobile phones and personal and home cleaning care, ACSI found. This last table organizes that data by consumer-facing industry for 2021.

Health insurance experience ranks in line with hotels and just above gas stations, landline phone services, and the US Postal Service. Hospitals sit between social media and video-on-demand services, just above internet service providers and subscription TV at the bottom of consumers’ industry sector experiences.

One of the most interesting career news items in our field I recognized this month was Dr Adrienne Boissy’s announcement that she was leaving her long-time leadership role at Cleveland Clinic as Chief Experience Officer, to take a Chief Medical Officer position with Qualtrics, the consumer experience company.

Qualtrics’ press release discussing Dr. Boissy’s appointment would “help industries, including healthcare institutions, deliver exceptional experiences for patients, customers and employees.”

Aside from the fact that I’m very excited for Dr. Boissy on a personal level for career development and a fascinating new chapter, I’m energized and hopeful that this is a milestone for the health care industry recognizing the importance of experience design for patients, caregivers, and staff (with burnout at a high).

Design-thinking in health care has several important lenses:

In the U.S., the financial experience in health care is front-of-mind for health care consumers

The clinical experience is central — note Philips new Pediatric Coaching experience for children undergoing imaging encounters

The administrative work-flows for patients are also big influences on the experience, recognizing the importance of the mobile app for health plans in the ACSI survey findings

Finally, privacy-by-design and health data access has emerged as a growing patient and caregiver demand.

As experienced experience leaders like Dr. Boissy scale their expertise across the health care ecosystem, we could see hospitals and health plans move up the consumer satisfaction index to rival the likes of our favorite grocers and banks. As patients continue to morph into health consumers paying more out-of-pocket facing greater financial risk and administrative flows via digital on-ramps, their medical lives are blurring into an evolving retail health ecosystem.

The post Health Plan Consumer Experience Scores Reflect Peoples’ Digital Transformation – ACSI Speaks appeared first on HealthPopuli.com.

Health Plan Consumer Experience Scores Reflect Peoples’ Digital Transformation – ACSI Speaks posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Center for Healthcare Economics and Policy brochure

Check out FTI Consulting’s Center for Healthcare Economics and Policy‘s new services sheet here. The cover page and overview of some of our HEOR services are below.

More details on the full scope of health economics services that we offer can be found here.

Center for Healthcare Economics and Policy brochure posted first on https://carilloncitydental.blogspot.com

0 notes

Text

Be Mindful About What Makes Health at HLTH

“More than a year and a half into the COVID-19 outbreak, the recent spread of the highly transmissible delta variant in the United States has extended severe financial and health problems in the lives of many households across the country — disproportionately impacting people of color and people with low income,” reports Household Experiences in America During the Delta Variant Outbreak, a new analysis from the Robert Wood Johnson Foundation, NPR, and the Harvard Chan School of Public Health.

As the HLTH conference convenes over 6,000 digital health innovators live, in person, in Boston in the wake of the delta variant, what should attendees keep in mind to help HLTH make health?

The top-line in the report, and the bottom-line for health citizens, was that 38% of U.S. households faced serious financial problems in 2020 in the delta variant phase of the pandemic.

This financial hit affected lower-income people earning under $50,000 a year harder than those with higher incomes, and especially impacted people who rented their homes and people of color.

The survey informing the report was conducted between August 2 and September 7, 2021, among 3,616 adults 18 and older (in English, Spanish, Mandarin, Cantonese, Korean, and Vietnamese based on consumers’ language preferences). The survey broke out race and ethnicity in terms of white, Hispanic/Latino, African American/Black, Asian, and Native American/American Indian/Alaska Native.

The major financial problems people faced in the past few months included making credit card and loan payments (among 1 in 5 people), affording medical care (for 17%), paying utilities, paying mortgage or rent, and affording food, shown in the first graph from the report (“Figure 4”).

Fifty percent of households without health insurance reported trouble affording medical care compared with 13% of people with health insurance.

One-half of U.S. households overall also said someone had experienced serious problems with depression, anxiety, stress, or sleeping in the past few months.

Health Populi’s Hot Points: This week during the HLTH conference, we’ll learn about exciting developments in new digital health products and services embedding AI, leveraging virtual care and telehealth, serving up new models of primary care, and a growing supply of mental health services that can scale beyond traditional face-to-face synchronous therapy encounters between patient and therapist.

That’s the supply side of HLTH. But there are opportunities to learn from patients and advocacy groups at the meeting to inform the demand side of the health/care equation, and that’s crucial to understanding consumer experience, values and sense of value that enables people to get the care they need.

Particularly for those health citizens who have been long under-served by healthcare and digital health tools.

The fact is that the best-designed digital health innovations can’t, themselves, address the root causes of un-wellbeing and poor health outcomes which are influenced, from pre-birth through our early childhoods.

Those social determinants are intimately, inextricably linked to socioeconomics — household income, education, job and income security, safe and clean physical environments in the home and in our neighborhoods. And as the RWJF/NPR/Harvard Chan study shows, these social determinants risks travel in groups and double-down on those health risks for people who rent, people of color, those without access to healthy food, and folks who earn lower incomes.

At the same time, the coronavirus pandemic accelerated the trend-already-in-place at the start of 2020 with our homes evolving into our health care spaces: ideally hygienic, safe, with nutritious food in the fridge, and connected online.

This month’s announcement launching the Advanced Care at Home Initiative bolsters this phenomenon. This alliance brings together the founding members Kaiser Permanente, Mayo Clinic, and Medically Home joined by new stakeholders including Adventist Health, ChristianaCare, Geisinger Health, Integris, Johns Hopkins Medicine, Michigan Medicine (University of Michigan), Novant Health, ProMedica, Sharp Rees-Stealy Medical Group, UNC Health, and UnityPoint Health.

One of the founding members Dr. Stephen Parodi of The Permanente Foundation noted, “Offering acute-level, hospital-quality care at home allows physicians and care teams to treat a whole person to meet their individualized care goals, while also helping address some of the social determinants of health….[and] supports a policy foundation for this more equitable future of health care.”

As we are amazed and exuberant about the digital future of health care this week at HLTH, let’s keep health — equitable, accessible, culturally compatible, high-value — in our hearts and minds.

The post Be Mindful About What Makes Health at HLTH appeared first on HealthPopuli.com.

Be Mindful About What Makes Health at HLTH posted first on https://carilloncitydental.blogspot.com

0 notes