#5G System Integration Market Growth Forecast

Text

5G Systems Integration Market Driven By Increase Investments In U.S., China, And Japan

The global 5G systems integration market size is estimated to reach USD 62.69 billion by 2030, registering a CAGR of 27.3% from 2022 to 2030, according to a new study by Grand View Research, Inc. Robust increase in the investments to deploy 5G network infrastructures across key countries, such as U.S., China, and Japan, has created the demand for integrating entire fifth generation infrastructure and applications across enterprises. This process will help enterprises to work as a centralized platform that will assist in reducing overall complexity. Thus, robust investments in building fifth-generation infrastructure, coupled with the growing need to set up a 5G-enabled ecosystem, are estimated to propel market growth.

Rapidly building smart cities have surged the adoption of numerous Internet of Things (IoT) devices across the globe. IoT devices require enhanced bandwidth to function appropriately. Thus, in order to provide high-speed broadband by supporting fifth-generation New Radio (NR), such as sub-6GHz and mmWave frequency bands, the entire infrastructure across these smart cities need to be upgraded in line with supporting fifth-generation radio network. Therefore, it is further estimated to boost the market growth from 2022 to 2030.

Gain deeper insights on the market and receive your free copy with TOC now @: 5G Systems Integration Market Report

Moreover, with the evolution of industry 4.0, the adoption of industrial sensors and collaborative robots is gaining popularity in the manufacturing sector across the globe. Therefore, to deliver seamless network connectivity to these above-mentioned devices, it is anticipated to raise the demand for 5G system integration services to make entire manufacturing facilities compatible with supporting next-generation 5G NR.

Rapidly rising digital transformation has disrupted the entire operation of the manufacturing industry. This has increased the trend of the machine-to-machine (M2M) communications to increase overall productivity as well as streamline the whole process. As a result, this has further expanded the need for high broadband to deliver uninterrupted connectivity to industrial sensors and robots. Therefore, the growing need for high broadband connectivity to establish seamless communication between machines is expected to elevate the demand for 5G system integration services in the next few years.

Furthermore, with the emergence of new technologies, such as network slicing and software-defined networking (SDN), the adoption of 5G system integration will witness a rapid surge to reduce overall enterprise infrastructure costs. Moreover, highly trained professionals must implement and manage the fifth-generation system integration services. This is anticipated to hinder market growth over the forecast period.

#5G System Integration Market Size & Share#Global 5G System Integration Market#5G System Integration Market Latest Trends#5G System Integration Market Growth Forecast#COVID-19 Impacts On 5G System Integration Market#5G System Integration Market Revenue Value

2 notes

·

View notes

Text

Navigating the Telecom Power System Market: Global Industry Outlook

Increasing demand for compact and modular telecom power systems and the growing adoption of virtualization in telecom power systems are likely to drive the Market in the forecast period.

According to TechSci Research report, “Telecom Power System Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2028”, the Global Telecom Power System Market is experiencing a surge in demand in the forecast period. A primary driver propelling the global Telecom Power System market is the widespread deployment of 5G technology. The advent of 5G has ushered in a new era of connectivity, offering faster data speeds, reduced latency, and increased network capacity. The implementation of 5G networks requires a significant upgrade of telecom infrastructure, driving the demand for advanced Telecom Power Systems. These systems play a pivotal role in providing the reliable and efficient power necessary to support the denser network of small cells characteristic of 5G deployment.

Telecom Power Systems must adapt to the unique requirements of 5G, accommodating the increased number of small cells and ensuring seamless integration into diverse environments. As the global demand for higher data speeds and enhanced connectivity continues to grow, the deployment of 5G technology acts as a potent driver, pushing the Telecom Power System market to innovate and evolve to meet the challenges of this next-generation network.

The exponential growth of the Internet of Things (IoT) is a significant driver fueling the global Telecom Power System market. The increasing prevalence of connected devices, from smart sensors to industrial machinery, demands a robust and reliable telecommunication infrastructure. Telecom Power Systems play a critical role in supporting the communication needs of IoT applications, providing the necessary power to base stations and data centers.

As industries across sectors embrace IoT for improved efficiency and real-time monitoring, the demand for Telecom Power Systems that can handle the unique challenges posed by IoT deployments is on the rise. These power systems must be scalable, energy-efficient, and capable of adapting to the diverse needs of IoT, contributing to the seamless integration and functionality of connected devices. The proliferation of IoT applications worldwide acts as a driving force, compelling Telecom Power System providers to develop innovative solutions to meet the evolving demands of this interconnected era.

Browse over XX Market data Figures spread through XX Pages and an in-depth TOC on "Global Telecom Power System Market.”

https://www.techsciresearch.com/report/telecom-power-system-market/23070.html

The Global Telecom Power System Market is segmented into grid type, component, power source, and region.

Based on grid type, The On Grid segment held the largest Market share in 2022. On-Grid systems are well-suited for urban and developed areas where the power grid infrastructure is stable and reliable. In these regions, there is a consistent and uninterrupted power supply, making on-grid solutions a cost-effective and practical choice.

Connecting telecom infrastructure to an existing power grid is often more cost-effective than setting up independent power systems. The infrastructure is already in place, reducing the need for additional investment in off-grid or backup power solutions.

On-Grid systems benefit from the reliability and consistency of power supply from the main electrical grid. Telecom operations in areas with a stable grid connection experience minimal disruptions, ensuring continuous communication services.

Maintenance and servicing of on-grid power systems are generally more straightforward. The infrastructure is readily accessible, and any issues can be addressed without the complexity associated with off-grid solutions, where remote locations may pose logistical challenges.

In regions where the cost of energy from the grid is competitive or economical, telecom operators may opt for on-grid solutions. The availability of affordable grid electricity can make on-grid Telecom Power Systems a financially viable choice.

Regulatory frameworks and permitting processes often favor on-grid solutions, especially in urban areas. Connecting to the existing power grid may involve fewer regulatory hurdles compared to establishing off-grid or hybrid solutions with renewable energy sources.

On-Grid systems offer scalability, allowing telecom operators to easily expand their networks without significant modifications to the power infrastructure. This scalability is particularly beneficial in densely populated urban areas experiencing high demand for telecommunication services.

Based on power source, The diesel-Battery segment held the largest Market share in 2022. Diesel generators are known for their reliability and can provide a constant power supply. This is crucial for telecom infrastructure, where uninterrupted power is essential to ensure continuous communication.

Diesel generators can operate in various environmental conditions, making them suitable for telecom installations in diverse locations, including remote or challenging terrains.

Diesel generators can operate for extended periods without refueling, providing an autonomous power source. This is particularly important in areas with unreliable or no access to the electrical grid.

Combining diesel generators with battery systems allows for better energy management. Batteries can store excess energy generated by the diesel generator and release it during peak demand or in case of generator failure, providing a seamless power supply.

Modern diesel generators are designed to be fuel-efficient, reducing operational costs over time. The combination of diesel and battery systems allows for optimization of fuel usage.

While diesel generators are known for their emissions, advancements in technology have led to more fuel-efficient and environmentally friendly models. Additionally, the integration of battery systems helps reduce reliance on diesel power during periods of lower demand.

In regions with unreliable or underdeveloped power grids, telecom installations often need to operate independently. Diesel-battery systems provide a reliable off-grid solution.

Major companies operating in the Global Telecom Power System Market are:

Huawei Technologies Co., Ltd.

Ericsson AB

Nokia Corporation

ABB Ltd.

Emerson Electric Co.

Siemens AG

Eaton Corporation PLC

Schneider Electric SE

Hitachi Ltd.

Samsung Electronics Co., Ltd.

Download Free Sample Report

https://www.techsciresearch.com/sample-report.aspx?cid=23070

Customers can also request for 10% free customization on this report.

“The Global Telecom Power System Market is expected to rise in the upcoming years and register a significant CAGR during the forecast period. The growth of the telecom power systems market is being driven by several factors, including the increasing demand for reliable and efficient power systems for telecommunications networks, the growing adoption of 5G networks, and the increasing need for renewable energy sources. Also, The Asia Pacific region is expected to be the fastest-growing market for telecom power systems, due to the rapid growth of the telecommunications industry in the region.

The Middle East and Africa region is also expected to witness significant growth, as countries in the region invest in upgrading their telecommunications infrastructure. The telecom power systems market is a fragmented market, with a large number of players. Some of the leading players in the market include Huawei, Ericsson, Nokia, ABB, and Emerson Electric. Therefore, the Market of Telecom Power System is expected to boost in the upcoming years.,” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based management consulting firm.

“Telecom Power System Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, 2018-2028 Segmented By Grid Type (On Grid, Off Grid, Bad Grid), By Component (Rectifier, Inverter, Converter, Controller, Heat Management Systems, Generators, Others), By Power Source (Diesel-Battery, Diesel-Solar, Diesel-Wind, Multiple Sources), By Region, By Competition”, has evaluated the future growth potential of Global Telecom Power System Market and provides statistics & information on Market size, structure and future Market growth. The report intends to provide cutting-edge Market intelligence and help decision-makers make sound investment decisions., The report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in the Global Telecom Power System Market.

Browse Related Reports

Air-Operated Grease Market

https://www.techsciresearch.com/report/air-operated-grease-market/23568.html

Portable Grease Pumps Market

https://www.techsciresearch.com/report/portable-grease-pumps-market/23569.html

Industrial Belt Drives Market

https://www.techsciresearch.com/report/industrial-belt-drives-market/23573.html

Contact Us-

TechSci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Telecom Power System Market#Telecom Power System Market Size#Telecom Power System Market Share#Telecom Power System Market Trends#Telecom Power System Market Growth

0 notes

Text

Accelerating Growth: Base Station Antenna Market Set to Reach $14.75 Billion by 2028 with a Remarkable CAGR of 14.9%

Overview and Scope

The base station antenna is used as a connection point for a wireless device to communicate. These antennas are base stations mounted on the towers to provide cellular connectivity to users. These antennas are used to cover single-frequency bands or multiple-frequency bands.

Sizing and Forecast

The base station antenna market size has grown rapidly in recent years. It will grow from $7.33 billion in 2023 to $8.46 billion in 2024 at a compound annual growth rate (CAGR) of 15.4%. The growth in the historic period can be attributed to expansion of mobile networks, increased mobile data usage, rise in smartphone penetration, network upgrades and modernization, introduction of carrier aggregation, globalization of mobile services, focus on rural connectivity, demand for high-speed connectivity..

The base station antenna market size is expected to see rapid growth in the next few years. It will grow to $14.75 billion in 2028 at a compound annual growth rate (CAGR) of 14.9%. The growth in the forecast period can be attributed to demand for indoor connectivity solutions, edge computing integration, focus on energy-efficient solutions, demand for smart antenna systems, urbanization and smart city initiatives, advanced antenna beamforming techniques, focus on network security.

To access more details regarding this report, visit the link:

https://www.thebusinessresearchcompany.com/report/base-station-antenna-global-market-report

Segmentation & Regional Insights

The base station antenna market covered in this report is segmented –

1) By Type: Omni Antenna, Dipole Antenna, Multibeam Antenna, Small Cell, Other Types

2) By Technology: 3G, 4G or LTE, 5G

3) By Application: Mobile Communication, Intelligent Transport, Industrial, Smart City, Military and Defense, Other Applications

Asia-Pacific was the largest region in the base station antenna market in 2023. North America was the second largest region in the base station antenna market analysis. The regions covered in the base station antenna market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.thebusinessresearchcompany.com/sample.aspx?id=8576&type=smp

Major Driver Impacting Market Growth

The increasing usage of mobile devices will boost the demand for base station antenna. The demand and usage for mobile devices are increasing to access the internet and stay connected virtually. Base station antenna provides cellular connectivity to users for their mobile devices.

Key Industry Players

Major companies operating in the base station antenna market report are CommScope Holding Company Inc., Amphenol Corporation, Ace Technologies Corporation, Comba Telecom, Huawei Technologies Co. Ltd., Rosenberger Hochfrequenztechnik GmbH & Co. KG,

The base station antenna market report table of contents includes:

1. Executive Summary

2. Market Characteristics

3. Market Trends And Strategies

4. Impact Of COVID-19

5. Market Size And Growth

6. Segmentation

7. Regional And Country Analysis

.

.

.

27. Competitive Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

KVM and PRO AV Market Is Estimated to Witness High Growth Owing to Growing Demand from Enterprises and Increasing Technological Development

The KVM and PRO AV market involves devices and technology that control equipment and transfer audio and video. KVM switches allow IT administrators to access and control multiple computers from a single console like a keyboard, monitor and mouse. They provide cost-effective and secure access to servers located in data centers and wiring closets. PRO AV equipment includes projectors, flat panel displays, audio equipment and video wall mounts that are used for digital signage, video conferencing rooms, board rooms and other commercial purposes. The demand for these products is driven by enterprises increasingly adopting digital signage systems and video conferencing solutions to enhance communication and marketing initiatives. Technological developments are allowing higher resolutions, wireless connectivity and integration of appliances to deliver more immersive experiences.

The Global KVM and PRO AV Market is estimated to be valued at US$ 402391.05 Bn in 2024 and is expected to exhibit a CAGR of 8.0% over the forecast period 2024 To 2031.

Key Takeaways

Key players operating in the KVM And PRO AV Market are Mondi PLC, Ahlstrom-Munksjö Oyj, Autajon CS, Huhtamaki Flexible Packaging (Huhtamaki Oyj) and Avery Dennison Corporation. These companies are focusing on new product development through investments in R&D to capitalize on emerging opportunities.

There is rising demand for wireless and cloud-based KVM solutions owing to the adoption of BYOD trend and need for flexible infrastructure in enterprises. 4K and 8K resolution displays are gaining popularity due to vivid picture quality and ability to support multiple simultaneous video sources. Integration of IoT capabilities in PRO AV solutions is allowing remote monitoring and management of systems.

The market is witnessing high growth in Asia Pacific due to rapid digital transformation of businesses and infrastructure development projects in the region. North America and Europe continue to be the largest markets while Middle East and Latin America offer lucrative prospects. Innovation and digital services are driving global expansion of KVM and PRO AV market.

Social: Younger demographics are more receptive to new collaboration technologies that facilitate remote work. Growing emphasis on hybrid work models post-pandemic is creating opportunities for vendors offering flexible and scalable AV integration solutions.

Technological: Innovation in audio-visual codecs, connectivity standards, and processing capabilities are enhancing the functionalities of digital signage, video walls, and conference room solutions. The integration of advanced technologies such as AI, 5G, and edge computing is allowing real-time interactivity in larger virtual environments.

Get More Insights On This Topic: KVM and PRO AV market

0 notes

Text

Over-the-air (OTA) Market - Global Opportunity Analysis and Industry Forecast (2024-2031)

Meticulous Research®—a leading global market research company, published a research report titled, ‘Over-the-air (OTA) Market by Offering (Solutions (FOTA, SOTA), Services), Application (OTA Testing, Wireless Communication, Software & Firmware Update, Regulatory Compliance), Industry (Automotive, BFSI, Retail), and Geography - Global Forecast to 2031.’

According to this latest publication from Meticulous Research®, the global over-the-air (OTA) market is projected to reach $20.7 billion by 2031, at a CAGR of 14.7% from 2024 to 2031. The growth of this market is driven by factors such as the proliferation of IoT devices, the growing need to reduce the costs associated with manual updates and device recalls, and the increasing demand for connected features in vehicles. Additionally, the integration of edge computing & blockchain technology for OTA updates and the emergence of vehicle-to-everything (V2X) connectivity are expected to create market growth opportunities. However, limited network bandwidth may restrain the growth of this market. Furthermore, concerns regarding data security are major challenges for the players operating in this market.

Additionally, the deployment of 5G networks for faster OTA updates is a key trend in the over-the-air (OTA) market.

The global over-the-air (OTA) market is segmented by offering, application, and end-use industry. The study also evaluates end-use industry competitors and analyzes the market at the region/country level.

Based on offering, the global over-the-air (OTA) market is broadly segmented into solutions and services. The solutions segment is further segmented into firmware over-the-air (FOTA) and software over-the-air (SOTA). In 2024, the solutions segment is expected to account for the larger share of the global over-the-air (OTA) market. The large market share of this segment is attributed to the increasing need to manage software upgrades, cybersecurity patches, and mission-critical updates and the growing demand for OTA solutions to deliver software updates to devices, including operating system upgrades, firmware updates, and performance improvements.

However, the services segment is projected to register a higher CAGR during the forecast period due to the increasing need for OTA services for updating applications and software components installed on devices, the rising need to manage network infrastructure, optimize performance, remotely manage devices, and deliver new services effectively, and growing use of 5G OTA services to evaluate the performance, reliability, and functionality of 5G wireless devices and systems in real-world conditions.

Based on application, the global over-the-air (OTA) market is broadly segmented into OTA testing, software & firmware updates, wireless communication, and regulatory compliance. In 2024, the software & firmware update segment is expected to account for the largest share of the global over-the-air (OTA) market. The large market share of this segment is attributed to the proliferation of connected devices, including smartphones, IoT devices, and automotive systems, the increasing need to deploy security patches, encryption updates, and privacy enhancements to protect against cyber threats and safeguard sensitive data, and the growing need to keep up with evolving software and hardware capabilities to ensure products remain competitive and up-to-date.

However, the OTA testing segment is projected to register the highest CAGR during the forecast period due to the growing need for OTA testing to assess the antenna performance, ensure wireless devices comply with end-use industry standards and regulatory requirements, evaluate the MIMO performance in wireless devices, and measure the throughput and data rates of 5G devices.

Based on end-use industry, the global over-the-air (OTA) market is broadly segmented into IT & telecommunications, automotive, consumer electronics, manufacturing, BFSI, transportation & logistics, energy & power, aerospace & defense, retail, healthcare, and other end-use industries. In 2024, the IT & telecommunications segment is expected to account for the largest share of the global over-the-air (OTA) market. The large market share of this segment is attributed to factors such as the growing need to extend the lifecycle of varying devices, including servers, routers, switches, and network devices, by providing software upgrades and patches, the increasing need for remote device management, configuration, and monitoring, and the growing demand for OTA solutions to ensure the reliability, performance, and security of network infrastructure.

However, the automotive segment is projected to register the highest CAGR during the forecast period due to the increasing need to reduce the need for physical recalls due to software-related issues, the growing adoption of autonomous electric vehicles, the proliferation of connected car services, including telematics and vehicle-to-everything communication (V2X), and the growing demand for OTA updates to maintain and upgrade vehicle systems and ensure compliance with evolving regulations and standards.

Based on geography, the global over-the-air (OTA) market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2024, North America is expected to account for the largest share of the global over-the-air (OTA) market, followed by Europe and Asia-Pacific. North America’s significant market share can be attributed to the increasing advancements in connected car technologies, autonomous vehicles, and electric vehicles, the increasing use of OTA updates to ensure compliance with regulatory requirements and standards for data privacy, security, and safety, the growing adoption of OTA technology in aerospace & defense systems, the increasing adoption of software-defined infrastructure and systems, and the growing adoption of IoT devices including smart home devices, industrial sensors, healthcare monitors, and agricultural sensors.

However, the market in Asia-Pacific is projected to register the highest CAGR during the forecast period. The growing number of smartphone users and connected devices, the emergence of 5G networks, the increasing need to reduce manual intervention, physical recalls, and on-site maintenance, the increasing adoption of digital technologies, including cloud computing and online services, and the growing demand for consumer electronics, including smart TVs, streaming devices, gaming consoles, and home appliances in the region are expected to support the growth of this market.

Key Players:

The key players operating in the over-the-air (OTA) market are Thales (France), T-Systems International GmbH (Germany), HARMAN International (U.S.), NXP Semiconductors N.V. (Netherlands), BlackBerry Limited (Canada), Intertek Group plc (U.K.), TÜV SÜD (Germany), Airbiquity Inc. (U.S.), Nokia (Finland), Cyient Limited (India), IDEMIA (France), Microwave Vision, SA. (MVG) (France), Excelfore Corporation (U.S.), Sibros Technologies Inc. (U.S.), Memfault Inc. (U.S.), UL LLC (U.S.), Keysight Technologies, Inc. (U.S.), EMITE Ing.S.L. (Spain), Microchip Technology Inc. (U.S.), shanghai Facom Technology CO., LTD. (HBTE) (China), Advantal Technologies Private Limited (India), and Carota Corp (Taiwan).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5789

Key questions answered in the report-

What are the high-growth market segments in terms of offering, application, end-use industry, and geography?

What was the historical market of the over-the-air (OTA) market?

What are the market forecasts and estimates for the period 2024–2031?

What are the major drivers, restraints, opportunities, and challenges in the over-the-air (OTA) market?

Who are the major players, and what shares do they hold in the over-the-air (OTA) market?

What is the competitive landscape like in the over-the-air (OTA) market?

What are the recent developments in the over-the-air (OTA) market?

What are the different strategies adopted by the major players in the over-the-air (OTA) market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the global over-the-air (OTA) market, and how do they compete with the other players?

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#OvertheairMarket#OTAMarket#OverAWirelessNetwork#Firmwareovertheair(FOTA)#Softwareovertheair(SOTA)#5GOTATesting#OTATesting#AutomotiveOverTheAir(OTA)

0 notes

Text

Semiconductor Capital Equipment Market: A Comprehensive Guide to Growth Factors

Introduction

The semiconductor capital equipment market is a vital component of the semiconductor industry, which serves as the foundation for various electronic devices and technologies. As the world becomes increasingly reliant on electronics, ranging from smartphones and laptops to automotive systems and medical devices, the demand for semiconductors continues to escalate. This surge in demand necessitates advanced semiconductor manufacturing equipment capable of producing high-quality chips efficiently and cost-effectively.

According to the study by Next Move Strategy Consulting, the global Semiconductor Capital Equipment Market size is predicted to reach USD 35.31 billion with a CAGR of 6.3% by 2030. In light of this forecast, understanding the growth factors driving this market becomes crucial for stakeholders, investors, and industry players alike.

Request for a sample, here: https://www.nextmsc.com/semiconductor-capital-equipment-market/request-sample

Technological Advancements Driving Market Growth

One of the primary drivers of growth in the semiconductor capital equipment market is technological advancements. Semiconductor manufacturers are continuously innovating and upgrading their equipment to keep pace with the rapidly evolving demands of the industry. Advanced technologies such as Artificial Intelligence (AI), Internet of Things (IoT), and machine learning are being integrated into semiconductor manufacturing equipment to enhance process control, improve yields, and reduce production costs.

For instance, AI and machine learning algorithms are being deployed to optimize process parameters, detect defects, and predict equipment failures in real-time, thereby improving overall equipment effectiveness (OEE) and reducing downtime. Similarly, IoT-enabled sensors and connectivity solutions are being used to collect and analyze data from semiconductor manufacturing equipment, enabling proactive maintenance and predictive analytics.

Moreover, advancements in lithography, etching, deposition, and metrology technologies are driving innovation in semiconductor capital equipment. For example, extreme ultraviolet (EUV) lithography is revolutionizing the semiconductor manufacturing process by enabling the production of smaller, more complex chips with higher precision and accuracy. Similarly, atomic layer deposition (ALD) and chemical vapor deposition (CVD) techniques are being refined to deposit thin films with atomic-level precision, essential for next-generation semiconductor devices.

Increasing Demand for Semiconductor Chips

Another significant growth driver for the semiconductor capital equipment market is the increasing demand for semiconductor chips across various industries and applications. The proliferation of smart devices, Internet of Things (IoT) devices, and connected technologies has fueled the demand for semiconductor chips used in sensors, microcontrollers, and communication modules.

Moreover, the rapid expansion of 5G networks, the development of autonomous vehicles, and the adoption of artificial intelligence (AI) and machine learning (ML) technologies are driving the demand for high-performance semiconductor chips. These chips require advanced manufacturing processes and sophisticated capital equipment to meet the stringent performance and reliability requirements of modern applications.

Furthermore, the pandemic has accelerated the digital transformation across industries, leading to a surge in demand for semiconductor chips used in cloud computing, data centers, and remote work technologies. As organizations increasingly rely on digital infrastructure to support remote work, e-commerce, and telemedicine, the demand for semiconductor chips and the capital equipment used to manufacture them continues to rise.

Government Initiatives and Policies

In addition to technological advancements and increasing demand, government initiatives and policies aimed at promoting domestic semiconductor manufacturing are playing a crucial role in driving market growth. Governments around the world are recognizing the strategic importance of the semiconductor industry and implementing policies to strengthen domestic semiconductor capabilities and reduce dependency on imports.

For example, the U.S. government recently announced initiatives such as the CHIPS Act (Creating Helpful Incentives to Produce Semiconductors for America) to incentivize semiconductor manufacturers to invest in domestic production capacity. Similarly, the European Union has launched initiatives such as the European Chips Act to support semiconductor research, development, and manufacturing in the region.

Furthermore, countries like China, South Korea, and Japan are investing heavily in semiconductor manufacturing infrastructure to enhance their global competitiveness in the semiconductor industry. These government-led initiatives are expected to drive investments in semiconductor capital equipment and stimulate market growth in the coming years.

Inquire before buying, here: https://www.nextmsc.com/semiconductor-capital-equipment-market/inquire-before-buying

Strategic Collaborations and Mergers & Acquisitions

Strategic collaborations, partnerships, and mergers and acquisitions (M&A) within the semiconductor industry are also contributing to market growth by facilitating technology transfer, knowledge exchange, and innovation. Semiconductor companies are increasingly forming alliances and partnerships with equipment manufacturers, research institutions, and other stakeholders to leverage synergies and accelerate product development.

For instance, semiconductor manufacturers often collaborate with equipment suppliers to co-develop customized solutions tailored to their specific manufacturing requirements. These collaborations enable semiconductor companies to access cutting-edge technologies and expertise while allowing equipment suppliers to gain insights into market trends and customer needs.

Moreover, mergers and acquisitions (M&A) are reshaping the competitive landscape of the semiconductor capital equipment market by enabling companies to expand their product portfolios, enter new markets, and achieve economies of scale. For example, recent acquisitions in the semiconductor capital equipment market have focused on enhancing capabilities in areas such as process control, materials deposition, and metrology.

Challenges and Opportunities

Despite the promising growth prospects, the semiconductor capital equipment market faces several challenges that could impede its growth trajectory. One such challenge is the cyclical nature of the semiconductor industry, characterized by periods of boom and bust driven by fluctuations in demand, supply, and technological advancements.

Moreover, geopolitical tensions, trade disputes, and supply chain disruptions pose risks to the semiconductor industry by disrupting global supply chains and hindering cross-border trade. For example, the ongoing trade tensions between the U.S. and China have led to restrictions on the export of semiconductor equipment and materials, affecting the global semiconductor supply chain.

Furthermore, the semiconductor capital equipment market is highly competitive, with numerous players vying for market share and technological leadership. As a result, companies must continuously innovate and differentiate their products to stay ahead of the competition and capture emerging opportunities in the market.

However, despite these challenges, the semiconductor capital equipment market offers immense opportunities for growth and innovation. The increasing demand for semiconductor chips driven by emerging technologies such as 5G, artificial intelligence, and the Internet of Things (IoT) is expected to fuel investments in semiconductor manufacturing equipment.

Moreover, the growing emphasis on sustainability and environmental conservation is driving demand for energy-efficient and eco-friendly semiconductor manufacturing equipment. Companies that can develop innovative solutions to address these challenges while meeting the evolving needs of the semiconductor industry stand to gain a competitive advantage and capitalize on the growth opportunities in the market.

Conclusion

In conclusion, the semiconductor capital equipment market is poised for robust growth driven by technological advancements, increasing demand for semiconductor chips, government initiatives, and strategic collaborations within the industry. As the semiconductor industry continues to evolve and innovate, stakeholders must stay abreast of these growth factors to capitalize on emerging opportunities and navigate the competitive landscape effectively.

By leveraging advanced technologies, collaborating with industry partners, and adapting to changing market dynamics, semiconductor capital equipment manufacturers can position themselves for long-term success and contribute to the advancement of the semiconductor industry as a whole.

0 notes

Text

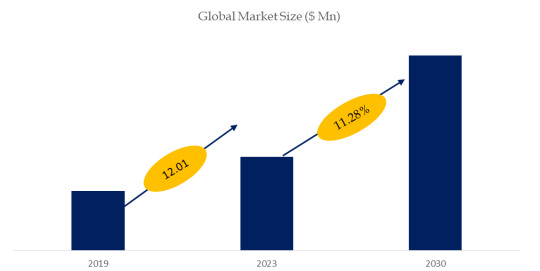

Digital Power Control Chip, Global Market Size Forecast, Top 8 Players Rank and Market Share

Digital Power Control Chip Market Summary

According to the new market research report “Global Digital Power Control Chip Market Report 2023-2029”, published by QYResearch, the global Digital Power Control Chip market size is projected to reach USD 3.63 billion by 2029, at a CAGR of 11.3% during the forecast period.

Figure. Global Digital Power Control Chip Market Size (US$ Million), 2019-2030

Above data is based on report from QYResearch: Global Digital Power Control Chip Market Report 2024-2030 (published in 2024). If you need the latest data, plaese contact QYResearch.

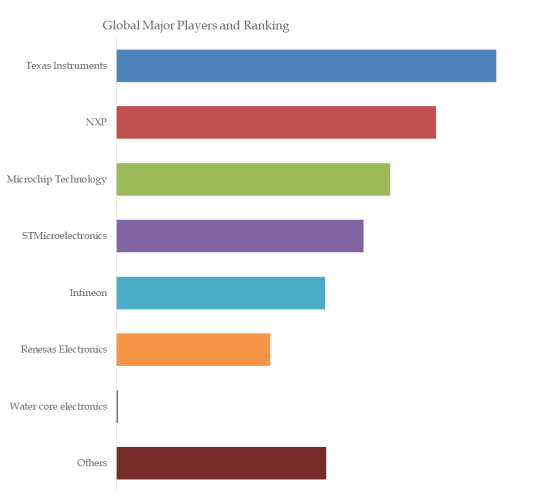

Figure. Global Digital Power Control Chip Top 15 Players Ranking and Market Share (Ranking is based on the revenue of 2023, continually updated)

Above data is based on report from QYResearch: Global Digital Power Control Chip Market Report 2024-2030 (published in 2024). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Digital Power Control Chip include Texas Instruments, NXP, Microchip Technology, STMicroelectronics, Infineon, etc. In 2022, the global top four players had a share approximately 68.0% in terms of revenue.

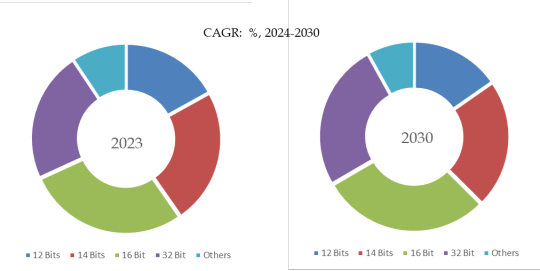

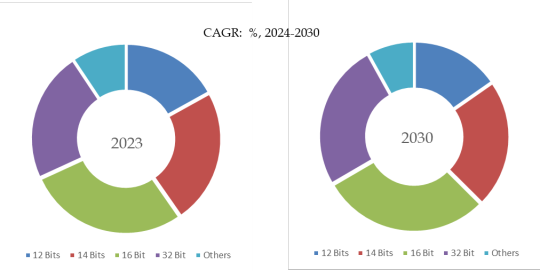

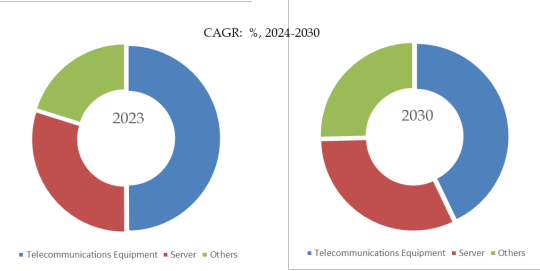

Figure. Digital Power Control Chip, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Digital Power Control Chip Market Report 2024-2030.

In terms of product type, currently 12 Bits is the largest segment, hold a share of 16.9%.

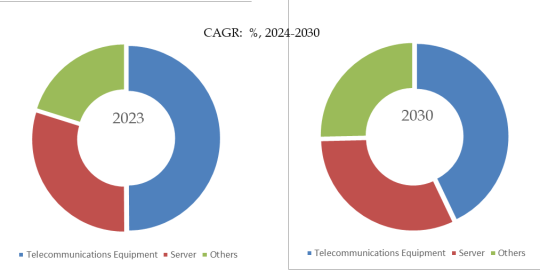

Figure. Digital Power Control Chip, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Digital Power Control Chip Market Report 2024-2030.

In terms of product application, currently Telecommunications Equipment is the largest segment, hold a share of 49.9%.

Market Drivers:

Technological progress and market demand: With the rapid development of science and technology, especially the popularization of 5G technology, the demand for Digital Power Control Chips has increased significantly. 5G equipment requires more efficient and stable power management chips to support its high-speed, low-latency communication requirements. In addition, the rapid development of the new energy vehicle market has also promoted the growth in demand for Digital Power Control Chips, because new energy vehicles use battery power systems and require digital power ICs to control and manage power.

Programmability and reconfigurability: One of the biggest advantages of Digital Power Control Chips is its programmability and reconfigurability, which allows the power system to be more flexibly adapted to different application needs, further expanding its market application scope. .

Energy efficiency and performance optimization: Digital Power Control Chips can improve the energy efficiency and performance of equipment and reduce power consumption through precise power management and control, which is very critical for modern electronic equipment that pursues high performance and low energy consumption.

Policy support and investment drive: The government's policy support for new energy, energy conservation and emission reduction, as well as the capital market's enthusiasm for investment in the semiconductor industry, have provided a strong driver for the development of Digital Power Control Chips.

Challenge:

Technical challenges: As an integrated circuit product, Digital Power Control Chips face many technical challenges during their design and manufacturing process. With the improvement of chip integration, the requirements for manufacturing accuracy and stability are also getting higher and higher. At the same time, Digital Power Control Chips need to have efficient, stable, and reliable power management capabilities, which places extremely high requirements on the design and manufacturing process of the chip. In addition, as new technologies continue to emerge, how to maintain technological leadership and innovation is also an important challenge faced by Digital Power Control Chips.

Market challenges: As market competition intensifies, Digital Power Control Chip companies are facing pressure from competitors. In order to win market share, companies need to continuously improve the performance and quality of their products while reducing costs. In addition, as market demand continues to change, companies need to quickly respond to market changes and flexibly adjust product strategies to meet customer needs.

Industry chain challenges: The manufacturing of Digital Power Control Chips involves multiple links, including chip design, manufacturing, packaging and testing, etc. The lack or instability of any link may affect the operation of the entire industrial chain. Therefore, Digital Power Control Chip companies need to work closely with upstream and downstream companies in the industry chain to jointly respond to various challenges.

Safety and reliability challenges: Digital Power Control Chips play a vital role in equipment. Once a failure occurs, it may lead to the failure of the entire equipment. Therefore, Digital Power Control Chips need to have a high degree of safety and reliability. Enterprises need to strengthen quality management and control to ensure product stability and reliability.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Application Transformation Market: A Compelling Long-Term Growth Story

Global Application Transformation Market Report from AMA Research highlights deep analysis on market characteristics, sizing, estimates and growth by segmentation, regional breakdowns & country along with competitive landscape, player’s market shares, and strategies that are key in the market. The exploration provides a 360° view and insights, highlighting major outcomes of the industry. These insights help the business decision-makers to formulate better business plans and make informed decisions to improved profitability. In addition, the study helps venture or private players in understanding the companies in more detail to make better informed decisions.

Major Players in This Report Include,

IBM Corporation (United States), Microsoft Corporation (United States), Oracle Corporation (United States), Bell Integrator (United States), Cognizant (United States), Pivotal Software (United States), Salesforce.com, Inc. (United States), Unisys (United States), Accenture PLC (Ireland), Atos SA (France).

Free Sample Report + All Related Graphs & Charts @: https://www.advancemarketanalytics.com/sample-report/163396-global-application-transformation-market

Application transformation is the process of modernizing dated applications to meet current demands, by bringing business-critical legacy applications to modern infrastructures and technology utilization. The process involves the establishment of an application portfolio and management program. With the help of application transformation services, the enterprises able to accelerate digital transformation initiatives, enhance the developer experience, and automate deployments that will further increase productivity. North America accounted for the major revenue share of over 27% in 2019 owing to the early adoption of application transformation solutions. High investments in research and developments in countries such as the United States and Canada make the application transformation market in North America highly competitive. Moreover, the increasing pressure for reducing IT costs and the large size of the outsourcing industry in the region are compelling companies to find alternative ways to control spending.

Market Drivers

The rapid increase in digitalization among industries, the growing penetration of the internet and mobile devices across the world, and an increase in the consumption of big data are the primary factors fostering the market growth.

Low Maintenance Cost As Compared To the Other Application

Technological Advancement and Development in Application Transformation Services

Increasing Modernization in Legacy System

Market Trend

Growing Use of Mobile Computing and Social Media in Enterprise

Use of Technologies Such As Cloud and Big Data, As Well As Principles of DevOps and Agile Development

Opportunities

Technological Advancements Such As Internet of Things (IoT), 5G, Edge Computing

Use of Real-Time Analytics Enabled By Machine Learning and Artificial Intelligence

Challenges

Lack of Skilled Workforce

Intense Competition among Industry Players

Enquire for customization in Report @: https://www.advancemarketanalytics.com/enquiry-before-buy/163396-global-application-transformation-market

In this research study, the prime factors that are impelling the growth of the Global Application Transformation market report have been studied thoroughly in a bid to estimate the overall value and the size of this market by the end of the forecast period. The impact of the driving forces, limitations, challenges, and opportunities has been examined extensively. The key trends that manage the interest of the customers have also been interpreted accurately for the benefit of the readers.

The Application Transformation market study is being classified by Services (Application Integration, Cloud Application Migration, Application Portfolio Assessment, Application Replatforming, UI Modernization, Others), Enterprise Size (Large Enterprises, Small and Medium Enterprises), Deployment (Public Cloud, Private Cloud, Others), End User (BFSI, Retail, Healthcare, IT & Telecom, Government, Manufacturing, Others)

The report concludes with in-depth details on the business operations and financial structure of leading vendors in the Global Application Transformation market report, Overview of Key trends in the past and present are in reports that are reported to be beneficial for companies looking for venture businesses in this market. Information about the various marketing channels and well-known distributors in this market was also provided here. This study serves as a rich guide for established players and new players in this market.

Get Reasonable Discount on This Premium Report @ https://www.advancemarketanalytics.com/request-discount/163396-global-application-transformation-market

Extracts from Table of Contents

Application Transformation Market Research Report

Chapter 1 Application Transformation Market Overview

Chapter 2 Global Economic Impact on Industry

Chapter 3 Global Market Competition by Manufacturers

Chapter 4 Global Revenue (Value, Volume*) by Region

Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions

Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type

Chapter 7 Global Market Analysis by Application

………………….continued

This report also analyzes the regulatory framework of the Global Markets Application Transformation Market Report to inform stakeholders about the various norms, regulations, this can have an impact. It also collects in-depth information from the detailed primary and secondary research techniques analyzed using the most efficient analysis tools. Based on the statistics gained from this systematic study, market research provides estimates for market participants and readers.

Contact US :

Craig Francis (PR & Marketing Manager)

AMA Research & Media LLP

Unit No. 429, Parsonage Road Edison, NJ

New Jersey USA – 08837

Phone: +1 201 565 3262, +44 161 818 8166

[email protected]

#Global Application Transformation Market#Application Transformation Market Demand#Application Transformation Market Trends#Application Transformation Market Analysis#Application Transformation Market Growth#Application Transformation Market Share#Application Transformation Market Forecast#Application Transformation Market Challenges

0 notes

Text

Revealing Growth of 2G & 3G Switch off

According to HTF Market Intelligence, theGlobal 2G & 3G Switch off market to witness a CAGR of 2.87% during forecast period of 2024-2030. by Application (Message, Voice, Data, Video) by Type (2G, 3G) by Material (Natural Shutdown, Constrained Shutdown, Anticipated Shutdown) and by Geography (North America, South America, Europe, Asia Pacific, MEA). The 2G & 3G Switch off market size is estimated to increase by USD Million at a CAGR of 2.87% from 2024 to 2030.. Currently, market value is pegged at USD 160.179,12 Million.

Get Detailed TOC and Overview of Report @

This refers to the process of phasing out or discontinuing 2G (second-generation) and 3G (third-generation) cellular networks. As newer generations of mobile technology, such as 4G and 5G, become more prevalent, older networks may be decommissioned to allocate resources for newer technologies and improve network efficiency.

Some of the key players profiled in the study are APC by Schneider Electric, Newton Instrument Company, Alpha Technologies Inc., Tripp Lite, Amphenol Network Solutions, Storage Battery Systems, LLC, Sackett Systems, Inc., EnviroGuard, Outback Power Inc..

Book Latest Edition of Global 2G & 3G Switch off Market Study @ https://www.htfmarketintelligence.com/buy-now?format=1&report=2098

About Us:

HTF Market Intelligence is a leading market research company providing end-to-end syndicated and custom market reports, consulting services, and insightful information across the globe. HTF MI integrates History, Trends, and Forecasts to identify the highest value opportunities, cope with the most critical business challenges and transform the businesses. Analysts at HTF MI focuses on comprehending the unique needs of each client to deliver insights that are most suited to his particular requirements.

Contact Us:

Craig Francis (PR & Marketing Manager)

HTF Market Intelligence Consulting Private Limited

Phone: +15075562445

[email protected]

0 notes

Text

Data Center Interconnect Market: Global Demand Analysis & Opportunity Outlook 2036

Research Nester’s recent market research analysis on “Data Center Interconnect Market: Global Demand Analysis & Opportunity Outlook 2036” delivers a detailed competitors analysis and a detailed overview of the global data center interconnect market in terms of market segmentation by type, application, end-user, and by region.

Request Report Sample@

Increased Advancements by Data Center Providers to Promote Global Market Share of Data Center Interconnect

Data center providers are improving their cloud and co-location offerings, which is one of the major factors propelling the growth of the market. The public, financial, OTT, and ISP sectors will all be developing use cases for DCI networks as a result of the expansion and dispersion of data centers, increased fiber consumption, and affordable pluggable modules. Product innovation is a crucial way for market players to set themselves apart. Vendors like Ciena, Infinera, Huawei, and Nokia have been pushing the limits of contemporary optics since the beginning of 2020. For instance, in 2022, one of the top digital network integrators in the country, STL unveiled India's first multicore fiber and cable. This innovative breakthrough will transform India's optical connection environment. This has been conceptualized and developed in-house with leading interdisciplinary R&D specialists at STL's Centre of Excellence in Maharashtra. Using space division multiplexing, STL's Multiverse increases transmission capacity per fiber by 4X while maintaining the same diameter.

Some of the major growth factors and challenges that are associated with the growth of the global data center interconnect market are:

Growth Drivers:

Increase in the Number of Data Centers

Surge in the Global Demand for 5G Network

Challenges:

Several factors must be considered when preparing for the construction of the data center. Some of these aspects are engineering, authorizations and approvals, power systems, insulated generators, conduits or cables for electrical equipment, data center lighting, illumination protection, air quality control, fire suppression, etc. These expenses may soon be compensated for by capital investments. Consequently, the growth of the data center interconnect market may be hindered by this factor.

Some other factors such as data privacy issues and capacity limitations may impede the growth of the data center interconnect market.

By end-user, the global Data Center Interconnect market is segmented into communication service providers, internet content providers/ carrier-neutral providers, governments, and enterprises. The internet content providers/carrier neutral providers segment is expected to hold a share of 32% during the forecast period. Several of the biggest ICPs, like Microsoft, Google, and Facebook (Meta), are producing enormous amounts of internet traffic. For this reason, to connect their data centers, many ICPs are also choosing to construct fiber networks. Several carrier-neutral colocation facilities are making significant investments in DCI technology since flexibility is crucial for these types of facilities. Therefore, this factor is accelerating the growth of the segment.

By region, the Middle East & Africa data center interconnect market is anticipated to hold a share of 15% by the end of 2036. Major international cloud service providers are present in the Middle East and Africa (MENA) region. These providers include Amazon Web Services, Tencent, Microsoft, Google, Alibaba, Oracle, and Huawei Technologies. Microsoft, for example, plans to set up a cloud region in Saudi Arabia. Operators in several Middle Eastern and African nations are encouraged to build data centers by the availability of industrial parks, land, and government assistance. With the introduction of new submarines, the connectivity of the Middle East and Africa data center interconnect market is continuously expanding. It is anticipated that these factors will bolster the market growth in the region.

Access our detailed report at:

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

Japan Smart Cities Market: Global Industry Analysis and Forecast 2023 – 2030

Japan's Smart Cities are Expected to Grow at a Significant Growth Rate, and the Forecast Period is 2023-2030, Considering the Base Year as 2022.

Japan has been aggressively attempting to turn its cities into smart cities by incorporating cutting-edge technology and data solutions to enhance citizen quality of life and local services. The nation has made significant investments in 5G networks, Internet of Things (IoT) devices, and high-speed internet connections as part of its technology infrastructure investments. These technologies are essential for gathering and evaluating data from the city's diverse sources.

Japan's smart city initiatives are mostly focused on sustainable energy solutions, with an emphasis on the advancement of renewable energy sources like solar and wind power in addition to the implementation of smart grid technologies to improve energy distribution. Furthermore, smart transit systems are being used by Japanese towns to lessen traffic jams and enhance public transportation, all in an effort to increase mobility and traffic. This involves encouraging the use of electric vehicles and integrating intelligent traffic management.

In Japan, planning and urban design are crucial to the development of smart cities. The nation employs data analytics to develop energy-efficient buildings, enhance urban planning, and generate green spaces. Real-time data on a range of urban elements, including trash management, water use, energy consumption, and air quality, is gathered through the widespread use of IoT devices and sensor networks.

Japan emphasizes the significance of citizen interaction for developing smart cities. The objective is to use digital platforms, feedback mechanisms, and participatory planning to involve inhabitants in decision-making. Furthermore, the nation gives top priority to deploying smart technologies for public safety, security, surveillance, emergency coordination, and disaster management strategy deployment.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Leading players involved in the Japan Smart Cities Market include:

Panasonic Corporation (Japan), Hitachi Ltd. (Japan), Mitsubishi Electric Corporation (Japan), Siemens AG (Germany), Toshiba Corporation (Japan), NEC Corporation (Japan), Fujitsu Limited (Japan), Sumitomo Mitsui Construction Co., Ltd. (Japan), NTT Group (Japan), Schneider Electric SE (France), Toyota Motor Corporation (Japan), Ericsson (Sweden), ABB Group (Switzerland), SoftBank Group Corp. (Japan), Honda Motor Co. Ltd. (Japan), Shimizu Corporation (Japan), Sekisui House Ltd. (Japan), Daikin Industries Ltd. (Japan), ORIX Corporation (Japan), Yokogawa Electric Corporation (Japan), and Other Major Players

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

If You Have Any Query Japan Smart Cities Market Report, Visit:

https://pristineintelligence.com/inquiry/japan-smart-cities-market-113

Segmentation of Japan Smart Cities Market:

By Solution and Service

Smart Mobility Management

Smart Public Safety

Smart Healthcare

Smart Building

Smart Utilities

Others

By Component

Hardware

Software

Service

By Level

Emerging Smart Cities

Developing Smart Cities

Mature Smart Cities

By End-user

Government & Municipalities

Transportation & Logistics

Energy & Utilities

Healthcare

Education

Others

Importance of the Report :

• Qualitative and quantitative analysis of current trends, dynamics and estimates;

• Provides additional highlights and key points on various Japan Smart Cities market segments and their impact in the coming years.

• The sample report includes the latest drivers and trends in the Japan Smart Cities market.

• The report analyzes the market competitive environment and provides information about several market vendors.

• The report provides forecasts of future trends and changes in consumer behavior.

• Comprehensive fragmentation by product type, end use and geography.

• The study identifies many growth opportunities in the global Japan Smart Cities market.

• The market study also highlights the expected revenue growth of the Japan Smart Cities market.

Our study encompasses major growth determinants and drivers, along with extensive segmentation areas. Through in-depth analysis of supply and sales channels, including upstream and downstream fundamentals, we present a complete market ecosystem.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Acquire This Reports: -

https://pristineintelligence.com/buy-now/113

About Us:

We are technocratic market research and consulting company that provides comprehensive and data-driven market insights. We hold the expertise in demand analysis and estimation of multidomain industries with encyclopedic competitive and landscape analysis. Also, our in-depth macro-economic analysis gives a bird's eye view of a market to our esteemed client. Our team at Pristine Intelligence focuses on result-oriented methodologies which are based on historic and present data to produce authentic foretelling about the industry. Pristine Intelligence's extensive studies help our clients to make righteous decisions that make a positive impact on their business. Our customer-oriented business model firmly follows satisfactory service through which our brand name is recognized in the market.

Contact Us:

Office No 101, Saudamini Commercial Complex,

Right Bhusari Colony,

Kothrud, Pune,

Maharashtra, India - 411038 (+1) 773 382 1049 +91 - 81800 - 96367

Email: [email protected]

#IoT (Internet of Things)#Urban Mobility#Smart Infrastructure#DigitalGovernance#BigDataandAnalytics#Renewable Energy#5G Technology#Cybersecurity#Environmental Sustainability#Smart Healthcare#Smart Education#Waste Management#Smart Water Management#Augmented Reality (AR) and Virtual Reality (VR)#AI (Artificial Intelligence)#Blockchain#SmartSensors#SmartAgriculture

0 notes

Text

District Heating Market: Regulatory Framework and Impact Analysis

The global district heating market is estimated to be valued at US$ 50.8 Bn in 2024 and is expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030.

District heating, also known as teleheating, involves the distribution of steam, hot water or hot air to multiple buildings in a designated area for space or water heating purposes. District heating plants produce steam or hot water at a centralized location and deliver it through a system of insulated pipes in order to supply space heating and hot water to residential and commercial buildings in the area. It is an efficient way of sourcing heat for communities as it reduces infrastructure costs involved in individual heating systems. Rising awareness about carbon footprint reduction and the need for sustainable heating solutions have boosted the adoption of district heating across both developed and developing economies.

Key Takeaways

Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, FVB Energy. Vattenfall AB and SP Group collectively account for over 30% share of the global market.

Growing focus on reducing carbon emissions from the building sector has significantly boosted the demand for district heating systems. Stringent regulations pertaining to energy efficiency and use of renewable energy are encouraging utilities as well as commercial and residential complexes to adopt district heating.

Technological advancements such as integration of IoT capabilities and advanced sensing equipment in district heating systems allow for improved monitoring and control of the entire network. This has enhanced the operational efficiency and reliability of district heating infrastructure. Use of 4G/5G based communication technologies is also enabling utilities to implement predictive analytics for predictive maintenance.

Market Trends

Use of renewable and waste heat sources: Growing focus on utilizing renewable and untapped waste heat sources like solar thermal, geothermal, biomass and industrial waste heat for district heating applications presents significant opportunities. Countries like Denmark have successfully demonstrated the potential of renewable district heating.

Digitalization of infrastructure: Integration of sensors, IoT, cloud computing, data analytics and automation enables utilities to remotely monitor heat networks and optimize operations. This helps improve efficiency, flexibility and reliability of district heating services. Ongoing development of advanced smart grids supports the use of smart technologies.

Market Opportunities

Combined heat and power (CHP) plants: Widening scope of cogeneration/CHP technology enables further recovery of waste heat from power generation for district heating. It provides an environment-friendly and cost-effective option for utilities.

Renovation of aging infrastructure: As a significant part of the installed district heating systems in Europe and North America is approaching end of life, renovation and modernization of existing pipelines and equipment provides lucrative opportunities.

Impact of COVID-19 on the District Heating Market

The COVID-19 pandemic has adversely impacted the growth of the district heating market globally. During the outbreak, commercial and industrial activities came to a halt which lowered the demand for district heating from these sectors. This led to a substantial decline in sales revenue for district heating companies in 2020. Many planned projects were deferred or delayed due to supply chain disruptions and halted construction activities during the peak pandemic phase.

0 notes

Text

The Growing Active Electronic Components Market Is Driven By Rising Demand For Consumer Electronics

The active electronic components market involves the manufacturing and sale of semiconductors, transistors, and microchips that can actively amplify or switch electronic signals. Some key products in this space include integrated circuits, LEDs, sensors and optoelectronics. Active electronic components find applications in various consumer electronics devices like smartphones, computers, gaming consoles and industrial devices. Integrated circuits allow manufacturers to pack more functions into smaller devices with lower power consumption.

The Global Active Electronic Components Market is estimated to be valued at US$ 661.18 Bn in 2024 and is expected to exhibit a CAGR of 8.9% over the forecast period from 2024 to 2031.

Key Takeaways

Key players operating in the Active Electronic Components Market Growth are Infineon Technologies AG, Advanced Micro Devices, Inc., STMicroelectronics N.V., Microchip Technology, Inc., Analog Devices, Inc., Broadcom Inc., NXP Semiconductors N.V., Intel Corporation, Monolithic Power Systems, Inc., Texas Instruments Incorporated, Qualcomm Inc., Renesas Electronics Corporation, Semiconductor Components Industries, LLC, and Toshiba Corporation.

Key players operating in the active electronic components market are focusing on development of more efficient and compact components to meet the increasing power and performance needs of applications. Companies are also investing in new fabrication technologies like 7nm node for manufacturing integrated circuits with greater transistor densities.

The growing demand for battery-powered portable consumer electronics is driving the need for components with lower power consumption. With innovation in areas like 5G, artificial intelligence and autonomous vehicles, applications requiring high processing capabilities are rising rapidly.

Active electronic component manufacturers are expanding their global reach through strategic partnerships and acquisitions. This allows companies to address new markets, gain new capabilities and better serve customers across major regions.

Market drivers

The rising demand for consumer electronics across the world is a key driver for the active electronic components market. Advanced chips with more processing power are fundamental to enabling technologies in smartphones, laptops, wearables and other devices. Increasing digitization and internet penetration are also driving the need for high-performance components in data centers, networking infrastructure and communication applications. Furthermore, growth in industries like automotive, healthcare, manufacturing and industrial automation creates steady demand for sensors, power modules and other specialized components. The advent of new paradigms like Industry 4.0 and the industrial internet of things requires reliable electronic components for implementation.

Impact of Geopolitical Situation on Active Electronic Component Market Growth

The Active Electronic Component Market is facing uncertainties due to the geopolitical situation across various regions. The ongoing war between Russia and Ukraine has disrupted the supply chains and trade relations between Europe and Eastern markets. This is negatively impacting the demand and availability of key raw materials for IC manufacturing in the European Union. Manufacturers are facing higher costs and production issues.

Get More Insights On This Topic: Active Electronic Components Market

#Active Electronic Components Market#Active Electronic Components Market Size#Active Electronic Components Market Share#Active Electronic Components Market Trends#Active Electronic Components#Consumer Electronics

0 notes

Text

Over-the-air (OTA) Market - Global Opportunity Analysis and Industry Forecast (2024-2031)

Meticulous Research®—a leading global market research company, published a research report titled, ‘Over-the-air (OTA) Market by Offering (Solutions (FOTA, SOTA), Services), Application (OTA Testing, Wireless Communication, Software & Firmware Update, Regulatory Compliance), Industry (Automotive, BFSI, Retail), and Geography - Global Forecast to 2031.’

According to this latest publication from Meticulous Research®, the global over-the-air (OTA) market is projected to reach $20.7 billion by 2031, at a CAGR of 14.7% from 2024 to 2031. The growth of this market is driven by factors such as the proliferation of IoT devices, the growing need to reduce the costs associated with manual updates and device recalls, and the increasing demand for connected features in vehicles. Additionally, the integration of edge computing & blockchain technology for OTA updates and the emergence of vehicle-to-everything (V2X) connectivity are expected to create market growth opportunities. However, limited network bandwidth may restrain the growth of this market. Furthermore, concerns regarding data security are major challenges for the players operating in this market.

Additionally, the deployment of 5G networks for faster OTA updates is a key trend in the over-the-air (OTA) market.

The global over-the-air (OTA) market is segmented by offering, application, and end-use industry. The study also evaluates end-use industry competitors and analyzes the market at the region/country level.

Based on offering, the global over-the-air (OTA) market is broadly segmented into solutions and services. The solutions segment is further segmented into firmware over-the-air (FOTA) and software over-the-air (SOTA). In 2024, the solutions segment is expected to account for the larger share of the global over-the-air (OTA) market. The large market share of this segment is attributed to the increasing need to manage software upgrades, cybersecurity patches, and mission-critical updates and the growing demand for OTA solutions to deliver software updates to devices, including operating system upgrades, firmware updates, and performance improvements.

However, the services segment is projected to register a higher CAGR during the forecast period due to the increasing need for OTA services for updating applications and software components installed on devices, the rising need to manage network infrastructure, optimize performance, remotely manage devices, and deliver new services effectively, and growing use of 5G OTA services to evaluate the performance, reliability, and functionality of 5G wireless devices and systems in real-world conditions.

Based on application, the global over-the-air (OTA) market is broadly segmented into OTA testing, software & firmware updates, wireless communication, and regulatory compliance. In 2024, the software & firmware update segment is expected to account for the largest share of the global over-the-air (OTA) market. The large market share of this segment is attributed to the proliferation of connected devices, including smartphones, IoT devices, and automotive systems, the increasing need to deploy security patches, encryption updates, and privacy enhancements to protect against cyber threats and safeguard sensitive data, and the growing need to keep up with evolving software and hardware capabilities to ensure products remain competitive and up-to-date.

However, the OTA testing segment is projected to register the highest CAGR during the forecast period due to the growing need for OTA testing to assess the antenna performance, ensure wireless devices comply with end-use industry standards and regulatory requirements, evaluate the MIMO performance in wireless devices, and measure the throughput and data rates of 5G devices.

Based on end-use industry, the global over-the-air (OTA) market is broadly segmented into IT & telecommunications, automotive, consumer electronics, manufacturing, BFSI, transportation & logistics, energy & power, aerospace & defense, retail, healthcare, and other end-use industries. In 2024, the IT & telecommunications segment is expected to account for the largest share of the global over-the-air (OTA) market. The large market share of this segment is attributed to factors such as the growing need to extend the lifecycle of varying devices, including servers, routers, switches, and network devices, by providing software upgrades and patches, the increasing need for remote device management, configuration, and monitoring, and the growing demand for OTA solutions to ensure the reliability, performance, and security of network infrastructure.

However, the automotive segment is projected to register the highest CAGR during the forecast period due to the increasing need to reduce the need for physical recalls due to software-related issues, the growing adoption of autonomous electric vehicles, the proliferation of connected car services, including telematics and vehicle-to-everything communication (V2X), and the growing demand for OTA updates to maintain and upgrade vehicle systems and ensure compliance with evolving regulations and standards.