#digital pathology market 2018

Link

#market research future#digital pathology market#digital pathology market 2018#digital pathology market size#digital pathology market trend

0 notes

Link

#market research future#digital pathology market#digital pathology market 2018#digital pathology market size#digital pathology market trend

0 notes

Text

Paediatric Vaccine Market Global Industry Overview and Competitive Landscape till 2032

An annual growth rate of 3.2% is predicted for the European Laboratory Information Systems market during the next few years.

Increasing demand for improved laboratory efficiency, the need for integrated healthcare information systems, and hospitals prioritizing for laboratory information systems fuels the growth in the European laboratory information systems market. In addition, supportive government initiative and investments from healthcare IT manufacturers supplements the growth. However, scarcity experienced professionals and high maintenance & service expenses are factors hindering the growth of the market. On the other hand, demand for powerful IT systems in diagnostic and medical laboratories present opportunities in the market.

The rising demand for molecular diagnostic tests, the growing need to integrate different healthcare systems, governmental support for adoption of healthcare IT tools, continuous advancements in LIS products, and the rising incidences of chronic diseases are among the key factors driving the market growth. On the other hand, the high cost of LIS solutions, high maintenance and service expenses, and lack of skilled healthcare IT professionals are likely to restrain market growth in the coming years.

Germany dominates the European market for laboratory information system, having accounted for a 28.2% market share in 2014, followed by France. The U.K is expected to become a major market for laboratory information system (LIS) in the coming years.

The European laboratory information systems market is segmented on the basis of products, types, components, delivery mode, end users, and countries. The product segment is divided into standalone LIS and integrated LIS. The types included in the report are clinical LIS and anatomical LIS. The components covered in the report are services and software. On-premise, remotely-hosted, and cloud-based are delivery modes discussed in the report. The end users’ segment is further classified into clinical diagnostic laboratories, hospitals, anatomical pathology laboratories, blood banks, and molecular diagnostic laboratories. The countries such as Germany, Italy, Spain, U.K., and France would experience tremendous growth.

The European Commission’s new framework, Horizon 2020 has been the largest ever research and innovation programme in Europe for various fields including life sciences with a budget of $95 billion (€77 billion) from 2014-2020. In October 2017, The European Commission announced its plans to invest $37 billion (€30 billion) of this fund during 2018-2020 including $2.5 billion (€2 billion) to support Open Science, and $740 million (€600 million) for the European Open Science Cloud, European data infrastructure and high-performance computing. Horizon 2020 opened funding opportunities for future and emerging technologies and ICT Work Programme for life science researchers. Thus, increasing R&D activities and government funding will ultimately boost the demand for effective data management and hence drive the laboratory informatics market in Europe.

Key Takeaways

R&D is crucial for drug discovery and development. This in turn, boosts the demand for efficient lab and data management.

Growing number of organizations involved in R&D are shifting from traditional old systems to digital laboratory solutions.

In European region, Germany accounted for the largest share of 26.0% of the total R&D spending in 2016 in Europe as stated by R&D Magazine, 2017.

According to UNESCO Institute for Statistics, Germany is among the top 10 countries, accounting for 80% of global spending on R&D.

Germany spends 2.9% of GDP on R&D and have pledged to substantially increase public & private R&D spending as well as number of researchers by 2030, as part of the Sustainable Development Goals (SDGs).

For More Information: https://www.futuremarketinsights.com/reports/laboratory-information-systems-market

Competitive Landscape

Top companies in the laboratory information systems market are constantly releasing new products to increase their market share. They are bolstering their global reach through mergers, partnerships, and acquisitions.

Recent Developments

In September 2022, McKesson Corporation signed an agreement in principle to extend its partnership with CVS Health to distribute pharmaceuticals to mail order and specialty pharmacies, retail pharmacies and distribution centers through June 2027.

Key Companies Profiled:

ECerner Corp, Evident, McKesson, Medical Information Technology, Epic Systems Corporation, SCC Soft Computer, Roper Technologies Inc., CompuGroup Medical, and LabWare

Key Segments Covered in the Laboratory Information Systems Industry Analysis

By Components:

Software

Hardware

Services

By Delivery Mode:

On Premise

Cloud-Based

By End User:

Hospitals

Clinics

Independent Laboratories

Others

0 notes

Text

Growth with Drivers and Opportunities for Tissue Diagnostics Market

The global Tissue Diagnostics market is growing at a CAGR of 6.6% during and it is expected to reach USD 7.3 billion by 2027 from USD 5.3 billion in 2022, during the forecast period. The expansion of this market is majorly due to rising prevalence of neoplastic cases as well as high demand of oncology screening, However, Lack of skilled professionals is one of the challenge for which may inhibit the growth of this market.

According to estimates from the International Agency for Research on Cancer (IARC), globally, new cancer cases are expected to grow to 27.5 million, and 16.3 million cancer deaths are expected to occur due to the growing number of total and aged population by 2040.

The incidence of cancer is the highest in developed regions; however, cancer mortality is relatively higher in underdeveloped regions due to factors such as a lack of access to treatment facilities and the late detection of cancer in several patients. According to the WHO, for many types of cancers, the incidence rate in countries with high or very high HDI1 is generally 2 to 3 times that in countries with low or medium HDI. Also, approximately 70% of deaths due to cancer were reported in low-income and middle-income countries in 2020 (Source: ACS).

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1063949

Due to the increasing prevalence of cancer, the demand for oncology diagnostics has increased significantly. This has compelled government organizations, healthcare providers, and institutions to provide facilities for effective disease diagnosis and treatment. This is driving the demand for tissue diagnostics. In 2021, Roche launched two digital pathology image analyzers, uPath HER2 (4B5) and uPath HER2 Dual ISH, algorithms for precision patient diagnosis in breast cancer.

The demand for excised human tissue is increasing due to the growing awareness regarding personalized medicines, which depend on excised human tissue to create an innovative test for application in patient care. The demand for personalized medicine in the treatment of many disorders, mainly cancer, is increasing with the advancements in diagnostic tools. These technologies assist physicians in detecting and quantifying multiple biomarkers and dividing patients into subgroups on various disease and treatment grounds. Several advanced diagnostics are already in use for cancer treatment. For instance, the test called Oncotype DX, one of the advanced diagnostics for personalized medicine examines 21 genes and identifies the women with breast cancer who can be treated without chemotherapy. Personalized medicines accounted for over a third of new drug approvals in 2021 and 25% or more of all FDA approvals for each of the last seven years.

Major pharma companies such as AstraZeneca confirm that approximately 90% of their clinical development revenue is currently obtained by precision therapeutics. Some of the leading pharma companies for precision medicine include Novartis, Roche, Genentech, Astra Zeneca, Pfizer, BMS, Merck, and Amgen. Moreover, it has also been predicted that the personalized medicine sector is expected to reach around 98 billion USD by 2026. Likewise, the number of personalized medicines in the US market has grown from 132 in 2016 to 286 in 2020. Similarly, in vitro diagnostic reagents, test products, instrumentation, and other related products, which are widely used by both clinical and research laboratories, are an integral part of the development of personalized medicine. As a result, the in vitro diagnostic (IVD) market is expected to grow from USD 87.93 billion in 2018 to USD 68.12 billion by 2023, at a CAGR of 5.2% (Source: MarketsandMarkets—IVD Market Report), which is supposed to provide opportunities for the growth of the tissue diagnostics market (as tissue diagnostics is a part of in vitro diagnostics).

0 notes

Text

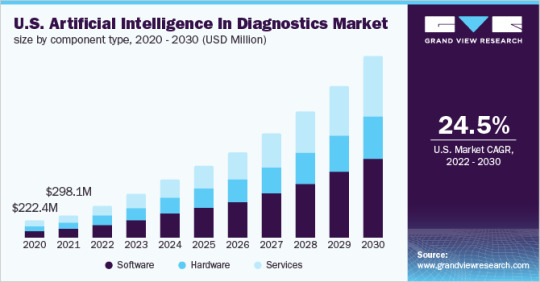

Artificial Intelligence In Diagnostics Market Size, Share And Trends 2023

The global artificial intelligence in diagnostics market size is expected to reach USD 5.5 billion by 2030, registering a CAGR of 26.3% over the forecast period, according to a new report by Grand View Research, Inc. The growing demand for integrating AI-enabled algorithms in diagnostics to provide precise and accurate diagnosis at the earliest, which enhances clinical and operational outcomes, is driving the growth of this market. The rapidly growing cases of acute & chronic disorders across the globe are driving the demand for AI-based solutions since most of these ailments could be either prevented or delayed if diagnosed early and given appropriate treatments. The shortage of healthcare personnel is also supporting the product demand.

Request Free Sample Report: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-diagnostics-market

The emergence of startups, increasing funding opportunities, and growing public-private partnerships are also boosting market growth. Furthermore, medical technology is witnessing significant transitions & transformations and is rapidly adopting advanced AI-powered solutions to provide precise diagnosis, which enables care providers to design adequate treatment plans. Radiology and pathology are widely implementing AI-based algorithms & solutions and have provided proven results. In radiology, these solutions use information collected from multiple modalities to create image datasets to run data analysis, which could be used by the radiologist in delivering an accurate and timely diagnosis. Similarly, in pathology, these solutions could be integrated to run data analysis and provide accurate results.

The growing burden of chronic conditions across the global population is also driving the demand for AI-based diagnostic solutions. The key participants in AI in diagnostics market are focusing on the development of new, innovative products and the expansion of their business offerings to gain a competitive edge over others. In addition, many startups specializing in the development of advanced AI-based technologies are receiving favorable support and funding opportunities. This will also have a positive impact on the overall market growth. For instance, in September 2018, IDx received funding of USD 33 million from Optum Ventures and 8VC and the company will use this funding for the development of innovative AI-based solutions.

Artificial Intelligence In Diagnostics Market Report Highlights

The global market is expected to be valued at 5.5 billion by 2030 owing to the growing adoption rates of AI-enabled solutions in diagnostics

The software component segment accounted for the largest revenue share of the global market in 2021

This growth was attributed to the increased demand for AI-based solutions to provide an early and accurate diagnosis

The neurology diagnosis type segment accounted for the largest share of the global revenue in 2021

The high share of the segment was credited to the increased incidence rate of neurological ailments

North America was the leading regional market in 2021 owing to the presence of well-established IT infrastructure and major players in the region

Key Companies & Market Share Insights

Key companies in this market offer diverse products & solutions and are constantly devising innovative product development strategies to gain a competitive edge over others. For instance, in November 2020, Zebra Medical Vision and Storm ID partnered to develop advanced AI-based algorithms to diagnose osteoporosis by analyzing multiple medical image datasets and electronic health information. Some of the key players in the global artificial intelligence in diagnostics market are:

Siemens Healthineers

Zebra Medical Vision, Inc.

Riverain Technologies

Vuno, Inc.

Aidoc

Neural Analytics

Imagen Technologies

Digital Diagnostics, Inc.

GE Healthcare

AliveCor Inc.

Browse Full Report: https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-diagnostics-market

#Artificial Intelligence In Diagnostics Market#Artificial Intelligence In Diagnostics Market Size#Artificial Intelligence In Diagnostics Market Trends

0 notes

Text

Digital Pathology Market : Industry Future Set To Massive Growth With High CAGR Value By 2032

The digital pathology market sizehas witnessed notable changes in terms of product innovation. One of the major reasons behind this is the scope of cloud integration with pathology outcomes in laboratory operations. According to a recent report by Future Market Insights, the global digital pathology market was valued at USD 6.19 Bn in 2021 and is expected to witness a CAGR of 13.5% during the forecast period.

The scope ofdigital pathologywith cloud integration has expanded with promising potential for numerous therapies in the healthcare industry including anti-cancer treatments. Innovation in terms of product efficiency, capabilities, and other modalities drives growth in the digital pathology market.

A number of modern hospitals are installing newly modified digital pathology systems for their laboratories which has widened the consumer base of the market globally. Manufacturers of digital pathology solutions are constantly making changes in software, to enhance the capabilities and efficacies of digital pathology devices.

This development will provide easy access to information such as images, and will also cater to specialized needs. In 2017, Glencoe Software Inc., launched a software named Path Viewer, which is used in interactive viewing and annotation of digital pathology images.

In Jan 2018, Definiens AG released Tissue Studio 4.2 software package. The updated product suite provided improved image analysis for researchers in academic medical laboratories, comprehensive cancer diagnostic and treatment centers, biotechnology, and pharmaceutical companies.

Sample of Research Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-124

Key Takeaways of Digital Pathology Market Study

Digital pathology equipment is anticipated to increase at a CAGR of 13.7% over 2021-2031, to reach US$ 12.94 Bn by 2031, aided by growing investments by hospitals and laboratories.

The clinical pathology and molecular diagnostics segment collectively have gained more than 50% of the market share in terms of revenue owing to use for a wider scope of ailments.

CROs are estimated to display high growth potential at a CAGR of 19.0% in the forecast period owing to cost benefits to end users.

Canada is reflecting high potential for growth with a 14.2% CAGR, driven by the expansion of urban centers and investments into healthcare facilities.

The U.K. will account for over 24% of the Europe value share, surpassing Germany by 2031, owing to increases in healthcare research spending.

“Growing research and development initiatives aimed towards cancer diagnosis and treatment are key factors expected to provide major growth opportunities for the digital pathology market through the end of 2031,” says the FMI Analyst.

Who is Winning? Leading players in the market are largely focused on product development launches in addition to investing in strategic acquisitions and capacity expansions, to explore previously untapped markets.

Some the digital pathology companies in the market are

Danaher Corporation,

Hoffmann-La Roche AG

Huron Technologies International Inc.

Koninklijke Philips N.V.

Olympus Corporation

Hamamatsu Photonics K.K.

Carl Zeiss

3D HISTECH Ltd.

Want more insights? Future Market Insights brings the comprehensive research report on forecasted revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2014 to 2029. The study provides compelling insights on digital pathology market on basis of component type (systems, software, and services), application (clinical pathology, molecular diagnostics, basic & applied research, drug development, others) and end users (hospitals, diagnostic laboratories, pharmaceutical & biotechnology companies, forensic laboratories, research institutes, contract research organizations, and clinics across seven major regions.

Key Segment By Product Type:

Equipment

Whole Slide Scanners

Brightfield Slide Scanners

Fluorescence Slide Scanners

Combination Slide Scanners

Clinical Microscope

Tissue Microarrays

Softwares

Image Viewing and Analysis Softwares

On-premise

Cloud-based

Digital Pathology Information Systems

On-premise

Cloud-based

Services

Installation and Integration Services

Consulting Services

Maintenance and Validation Services

By Application:

Clinical Patholog

Molecular Diagnostics

Basic & Applied Research

Drug Development

Others

End-User:

Hospitals

Diagnostic Laboratories

Pharmaceutical & Biotechnology Companies

Forensic Laboratories

Research Institutes

Contract Research Organizations (CROs)

Clinics

0 notes

Link

0 notes

Link

0 notes

Link

#market research future#digital pathology market#digital pathology market 2018#digital pathology market size#digital pathology market trend

0 notes

Text

Digital Pathology Market Set to Show a Drastic Surge with the Demand till 2026

Construing images of cells and tissues at a higher resolution than the naked human eye is the core of pathology. From a long time, microscopes has been the only instrument available which provides the live images at a higher resolution. This is achieved through never ending improvement in the optics.

In the last decades, optical pathology has been changed gradually by the introduction of digital cameras, which produces still images of slides and thus can be accessed or transported to another pathologist for examination. A further improvement in this method is through introduction of digital slide scanner. These scanners produce whole slide images that can be examined through an image viewer. The advantage of this system is that it produces live as well as high resolution images. This in turn is expected to be one of the vital factor to support the growth in digital pathology market.

North America dominates the digital pathology market over the forecast period:

Currently, North America (USA, Canada and Mexico) is the market leader of digital pathology market owing to vast number of companies. Also, increase in the inclination of the healthcare providers towards the integrated healthcare IT systems and cloud based systems to provide better interoperability in diagnostic research are the key factors of future growth in this region.

After North America, European region holds the second position for this market, which further followed by Asia-pacific and Latin America.

In the near future, Asia Pacific digital pathology industry is expected to expand at the highest CAGR with more focus on the countries like India, China and Japan. Factors for such a steep growth is growing patient population and rise in adoption rate for advanced technologies of disease diagnosis.

Key Players:

Some of the major players which are dominating the market are: Ventana Medical Systems, Inc., Definiens AG, Omnyx, LLC, Hamamatsu Photonics K.K, Corista LLC, GE Healthcare, Inspirata Co, Philips Healthcare, 3D-Histech Ltd., Olympus Corporation, Sectra AB, Perkin Elmer, Inc, etc.

Download PDF Brochure Of This Research Report @ https://www.coherentmarketinsights.com/insight/request-pdf/379

0 notes

Link

#market research future#digital pathology market#digital pathology market 2018#digital pathology market size#digital pathology market trend

0 notes

Text

The infosec apocalypse is nigh

When the Pegasus Project dropped last week, it was both an ordinary and exceptional moment. The report — from Amnesty, Citizenlab, Forbidden Stories, and 80 journalists in 10 countries — documented 50,000 uses of the NSO Group’s Pegasus malware.

https://www.occrp.org/en/the-pegasus-project/

The 50,000 targets of NSO’s cyberweapon include politicians, activists and journalists. The Israeli arms-dealer — controlled by Novalpina Capital and Francisco Partners — has gone into full spin mode.

NSO insists that the report is wrong, but also that it’s fine to spy on people, and also that terrorists will murder us all if they aren’t allowed to reap vast fortunes by helping the world’s most brutal dictators figure out whom to kidnap, imprison and murder.

As I say, all of this is rather ordinary. The NSO Group’s bloody hands, immoral practices and vicious retaliation against critics are well established.

It’s been four years since NSO’s assurances that it only sold spying tools to democratic states to hunt terrorists were revealed as lies, when Citizenlab revealed that its weapons targeted Mexican anti-sugar activists (and their children).

https://citizenlab.ca/2017/06/reckless-exploit-mexico-nso/

Then Citizenlab found 45 more countries where NSO’s Pegasus weapon had been used, and demonstrated that notorious human-rights abusers got help from NSO to target everyday citizens to neutralize justice struggles.

https://citizenlab.ca/2018/09/hide-and-seek-tracking-nso-groups-pegasus-spyware-to-operations-in-45-countries/

Outside of human rights and cybersecurity circles, the story drew little attention, but it did prick NSO’s notoriously thin skin — the company dispatched (inept) private spooks, late of the Mossad, to entrap Citizenlab’s researchers.

https://www.nytimes.com/2019/01/28/world/black-cube-nso-citizen-lab-intelligence.html

As far as we know, the company never managed to infiltrate any of Citizenlab’s systems — but their weapons were found on the devices of an Israeli lawyer suing them for their role in human rights abuses.

https://www.nytimes.com/2019/05/13/technology/nso-group-whatsapp-spying.html

That had some consequences. The attack exploited a vulnerability in Whatsapp, owned by Facebook. FB retaliated by suing — and terminating NSO Group employees’ Facebook accounts. Judging from NSO’s outraged squeals, getting kicked of FB hurt far worse.

https://www.vice.com/en/article/7x5nnz/nso-employees-take-legal-action-against-facebook-for-banning-their-accounts

Through it all, the NSO Group insisted that its tools were vital anti-terror weapons — not the playthings of rich sociopaths with long enemies lists.

They continued these claims even after Pegasus was linked to the blackmail attempt against Jeff Bezos, in a bid by Saudi royals to end the Washington Post’s investigative reporting on the murder and dismemberment of the journalist Jamal Khashoggi.

https://www.vice.com/en/article/v74v34/saudi-arabia-hacked-jeff-bezos-phone-technical-report

Despite all this — attacks on the powerful and the powerless, grisly deaths and farce-comedy entrapment attempts — NSO Group plowed on, raking in millions while undermining the security of the devices that billions of us rely on for our own safety.

Until now.

Something about the Pegasus Project shifted the narrative. Maybe it’s the ransomware epidemic, shutting down hospitals, energy infrastructure, and governments — or maybe it’s the changing tide that has turned on elite profiteers. Whatever it is, people are pissed.

Finally.

I mean, when Edward Snowden calls for the owners of a cybercrime company to be arrested, people sit up and pay attention. But Snowden’s condemnation of NSO and its industry are just for openers.

https://edwardsnowden.substack.com/p/ns-oh-god-how-is-this-legal

Snowden describes NSO as part of an “Insecurity Industry” that owes its existence to critical vulnerabilities in digital devices in widespread use. They spend huge sums discovering these vulns — and then, rather than reporting them so they can be fixed, they weaponize them.

As Snowden points out, this is not merely a private sector pathology. Governments — notably the US government, through the NSA’s Tailor Access Operations Group — engage in the same conduct.

Indeed, as with all digital surveillance, there’s no meaningful difference between private and public spying. Governments rely on tech and telecoms giants for data (which they buy, commandeer, or steal, depending on circumstances).

This, in turn, creates powerful security/public safety advocates for unlimited commercial surveillance, to ensure low-cost, high-reliability access to our private data. Those agencies stand ready to quietly scuttle comprehensive commercial privacy legislation.

This private-public partnership from hell extends into the malware industry: the NSA and CIA can’t, on their own, create enough cyber-weapons to satisfy all government agencies’ demand, so they rely on (and thus protect) the Insecurity Industry.

But as Snowden points out, none of this would be possible were it not for the vast, looming, grotesque tech-security debt that the IT industry has created for us. Everything we use is insecure, and it’s built atop more insecure foundations.

We live in an information society with catastrophic information security. If our society was a house, the walls would all be made of flaking asbestos and the attic would be stuffed with oily rags.

It’s hard to overstate just how much risk we face right now, and while the Insecurity Industry didn’t create that risk, they’re actively trying to increase it — finding every weak spot and widening it as far as possible, rather than shoring it up.

It’s a cliche: “Security is a team sport.” But I like how Snowden puts it: security is a public health matter. “To protect anyone, we must protect everyone.”

Step one is “to ban the commercial trade in intrusion software” for the same reason we “do not permit a market in biological infections-as-a-service.”

We should punish the cyber-arms dealers — but also use international courts to target the state actors who pay them.

But this fight will be a tough one. The huge sums that governments funnel to cyber arms-dealers allows them to silence their critics — I’ve been forced to remove some of my own coverage thanks to baseless threats I couldn’t afford to fight.

Writing in today’s Guardian (who also removed unfavorable coverage of NSO Group following legal threats), Arundhati Roy demolishes the company’s claims of clean hands.

https://www.theguardian.com/commentisfree/2021/jul/27/spying-pegasus-project-states-arundhati-roy

After all, NSO charges a 17% “system maintenance fee” that gives them oversight and insight into how their tools are being used by the demagogues and dictators who shower them with money.

https://www.thecitizen.in/index.php/en/newsdetail/index/9/20672/pegasus-hack-how-much-did-it-cost-to-spy-on-citizens

“There has to be something treasonous about a foreign corporation servicing and maintaining a spy network that is monitoring a country’s private citizens on behalf of that country’s government.” -Roy

The NSO Group claims that the human rights abuses it abets are exceptions that slip through the cracks, but the reality is, it has no business model without state terror — without powerful thugs who demand weapons to help jail, torture and kill their critics.

NSO, more than anyone, should know this. But as Upton Sinclair wrote, “It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

171 notes

·

View notes

Text

Laboratory Information Systems (LIS) Market In-Depth Analysis with Booming Trends Supporting Growth and Forecast 2032

An annual growth rate of 3.2% is predicted for the European Laboratory Information Systems market during the next few years.

Increasing demand for improved laboratory efficiency, the need for integrated healthcare information systems, and hospitals prioritizing for laboratory information systems fuels the growth in the European laboratory information systems market. In addition, supportive government initiative and investments from healthcare IT manufacturers supplements the growth. However, scarcity experienced professionals and high maintenance & service expenses are factors hindering the growth of the market. On the other hand, demand for powerful IT systems in diagnostic and medical laboratories present opportunities in the market.

The rising demand for molecular diagnostic tests, the growing need to integrate different healthcare systems, governmental support for adoption of healthcare IT tools, continuous advancements in LIS products, and the rising incidences of chronic diseases are among the key factors driving the market growth. On the other hand, the high cost of LIS solutions, high maintenance and service expenses, and lack of skilled healthcare IT professionals are likely to restrain market growth in the coming years.

Get Full PDF Sample Copy of Latest Reports @ https://www.futuremarketinsights.com/reports/sample/rep-gb-875

Germany dominates the European market for laboratory information system, having accounted for a 28.2% market share in 2014, followed by France. The U.K is expected to become a major market for laboratory information system (LIS) in the coming years.

The European laboratory information systems market is segmented on the basis of products, types, components, delivery mode, end users, and countries. The product segment is divided into standalone LIS and integrated LIS. The types included in the report are clinical LIS and anatomical LIS. The components covered in the report are services and software. On-premise, remotely-hosted, and cloud-based are delivery modes discussed in the report. The end users’ segment is further classified into clinical diagnostic laboratories, hospitals, anatomical pathology laboratories, blood banks, and molecular diagnostic laboratories. The countries such as Germany, Italy, Spain, U.K., and France would experience tremendous growth.

The European Commission’s new framework, Horizon 2020 has been the largest ever research and innovation programme in Europe for various fields including life sciences with a budget of $95 billion (€77 billion) from 2014-2020. In October 2017, The European Commission announced its plans to invest $37 billion (€30 billion) of this fund during 2018-2020 including $2.5 billion (€2 billion) to support Open Science, and $740 million (€600 million) for the European Open Science Cloud, European data infrastructure and high-performance computing. Horizon 2020 opened funding opportunities for future and emerging technologies and ICT Work Programme for life science researchers. Thus, increasing R&D activities and government funding will ultimately boost the demand for effective data management and hence drive the laboratory informatics market in Europe.

Are you looking for customized information related to the latest trends, drivers, and challenges? Speak to Our Analyst@ https://www.futuremarketinsights.com/ask-question/rep-gb-875

Key Takeaways

R&D is crucial for drug discovery and development. This in turn, boosts the demand for efficient lab and data management.

Growing number of organizations involved in R&D are shifting from traditional old systems to digital laboratory solutions.

In European region, Germany accounted for the largest share of 26.0% of the total R&D spending in 2016 in Europe as stated by R&D Magazine, 2017.

According to UNESCO Institute for Statistics, Germany is among the top 10 countries, accounting for 80% of global spending on R&D.

Germany spends 2.9% of GDP on R&D and have pledged to substantially increase public & private R&D spending as well as number of researchers by 2030, as part of the Sustainable Development Goals (SDGs).

Competitive Landscape

Top companies in the laboratory information systems market are constantly releasing new products to increase their market share. They are bolstering their global reach through mergers, partnerships, and acquisitions.

Recent Developments

In September 2022, McKesson Corporation signed an agreement in principle to extend its partnership with CVS Health to distribute pharmaceuticals to mail order and specialty pharmacies, retail pharmacies and distribution centers through June 2027.

Key Companies Profiled:

ECerner Corp, Evident, McKesson, Medical Information Technology, Epic Systems Corporation, SCC Soft Computer, Roper Technologies Inc., CompuGroup Medical, and LabWare

Grow your profit margin with Future Market Insights – Buy the report@ https://www.futuremarketinsights.com/checkout/875

Key Segments Covered in the Laboratory Information Systems Industry Analysis

By Components:

Software

Hardware

Services

By Delivery Mode:

On Premise

Cloud-Based

By End User:

Hospitals

Clinics

Independent Laboratories

Others

0 notes

Text

Specialty PACS Market Worth $3.45 Billion by 2024 - Exclusive Report by MarketsandMarkets™

According to the new market research report "Specialty PACS Market by Type (Radiology, Orthopedics, Oncology, Pathology, Endoscopy, Women's Health), Deployment Model (On premise, Cloud), Component (Software, Service), End User (Hospital, Clinic, Diagnostic Centers, Research) - Global Forecast to 2024", published by MarketsandMarkets™, the Specialty PACS Market is projected to reach USD 3.5 billion in 2024 from USD 2.6 billion in 2019, at a CAGR of 6.0%.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=66166054

The growth in this market is driven mainly by the increasing geriatric population and subsequent growth in the incidence of various diseases, advantages associated with specialty PACS, government initiatives to increase the adoption of healthcare IT solutions, increasing investments in medical imaging, growing adoption of medical imaging IT solutions, and increasing use of imaging equipment. On the other hand, budgetary constraints are expected to limit market growth during the forecast period.

"The Ophthalmology PACS segment is projected to grow at the highest CAGR during the forecast period."

Based on the type, the Specialty PACS Market is segmented into radiology PACS, cardiology PACS, pathology PACS, ophthalmology PACS, orthopedics PACS, oncology PACS, dermatology PACS, neurology PACS, endoscopy PACS, women's health PACS, and other specialty PACS. The ophthalmology PACS segment is expected to register the highest CAGR of during the forecast period. The increasing prevalence of eye diseases and disorders, the growing number of ophthalmic surgeries performed, and technological advancements in ophthalmology devices are some of the factors driving the growth of this segment.

Browse in-depth TOC on "Specialty PACS Market"

147 – Tables

124 – Figures

181 – Pages

Based on the component, the services segment is projected to grow at the highest CAGR during the forecast period.

Based on the component, the Specialty PACS Market is segmented into software, services, and hardware. In 2018, the software segment accounted for the largest Specialty PACS Market share. With the consistent increase in the healthcare imaging volumes, there is a growing demand for PACS software. However, services are expected to register the highest CAGR of during the forecast period primarily due to the recurring need for services such as software upgrades and maintenance.

The hospital segment is expected to dominate the Specialty PACS Market in 2018.

Based on end-user, the Specialty PACS Market is segmented into hospitals, ambulatory surgery centers (ASCs) & clinics, diagnostic imaging centers, and other end-users. In 2018, the hospital segment accounted for the largest share of the global Specialty PACS Market. The large share of this segment is attributed to factors such as the rising patient population, growing awareness about the benefits of early disease diagnosis, technological advancements in imaging modalities, increasing digitization of patient data, and rapid growth in EMR adoption.

Get 10% Customization on this Report: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=66166054

North America to dominate the market in 2018

In 2018, North America commanded the largest share of the market. The large share of this regional segment can be attributed to factors such as increasing medical imaging volumes and the number of diagnostic imaging centers, growing geriatric population, and the fast adoption of technologically advanced imaging systems.

Helped a top global diagnostic imaging leader in identifying ~ USD 200 million worth of additional revenue opportunities by tapping into AI in healthcare & pathology, ophthalmology specialty/departmental PACS solutions.

The study involved four major activities in estimating the current size of the global specialty PACS market. Exhaustive secondary research was done to collect information on the market, its peer markets, and its parent market. The next step was to validate these findings, assumptions, and sizing values with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation procedures were used to estimate the market size of segments and subsegments.

The Specialty PACS Market is marked by the presence of several big and small players. Some of the prominent players offering specialty PACS products include IBM Corporation (Merge Healthcare Incorporated) (US), McKesson Corporation (US), Agfa Healthcare (Belgium), Carestream Health (a part of Onex Corporation) (Canada), Philips Healthcare (Netherlands), Sectra AB (Sweden), Siemens Healthineers (Germany), Novarad (US), INFINITT North America (US), Intelerad Medical Systems (Canada), Topcon Corporation (Japan), Sonomed Escalon (US), Canon USA, Inc. (US) (a subsidiary of Canon Inc.), Visbion (UK), and EyePACS, LLC (US). These players have adopted various growth strategies, such as new product launches expansions; acquisitions; and partnerships, agreements, & contracts to further expand their presence in the global market.

1 note

·

View note

Text

Advance Digital Microscopes Market is Expected Growth $ 2.7 Bn by 2026

The Digital Microscope Market was valued at US$1.7 billion in the year 2018 and is estimated to reach US$2.7 billion by 2026, at a CAGR of 5.95%.

A digital microscope is a combination of a traditional optical microscope, digital multimedia, and digital processing technology. Digital microscopy imaging technology includes optical components for microscopic imaging, data acquisition component to record images produced by digital video devices, CMOS, CCD, digital cameras wherein these images are transferred to the computer storage device by graphics card interface or USB interface. The core component of digital microscopy is software control for image capture, processing, and real-time measurement to improve image quality.

Recent advancement of digital microscopes includes installation of online image acquisition, processing, and analysis systems software. Higher resolution, large field view, increased magnification, real-time view, 2D/3D image display are the main features of the digital microscope. There are both portable and desktop digital microscopes available in the global market. The sequential process of an Image sensor, analog signal, pixel conversion, digital signal and digital operation to display is driven principle in Digital Microscope. Advanced features include live imaging and snapshot, patented image analysis software, user-friendly interface and Wi-Fi. Different levels and various categories of digital microscopes include microscopes with built-in USB cameras requiring a PC (or MAC), HDMI, Wi-Fi, video or SXGA cameras and tablet PC with touch screen controls to see the live image.

The applications of digital microscopes span across fields like electronics, electricals, material science, metallurgy, mechanical, medical diagnostics, forensics, and R&D areas. Increased use of digital microscopes in R&D, material science and medical, diagnostics impact the demand during the forecast period. The evolution of microscopes over the years has been drastic. The inclusion of more features had made it essential in most of the fields to obtain key insights especially in medicine and biological research. With the inclusion of advanced features, the cost of the microscope also increases. Few microscopes with more advanced features even cost more than a million dollars. Further technical limitations and software updates also hinder market growth. However, Govt., research, and academic institutions are investing more in the latest digital microscopes to obtain more accurate data and also contribute more to education. Also, accurate identification and visualization of several pathological conditions with or without dyes have become possible with the use of digital microscopes. Further, Fluorescence-based microscopic examinations have enabled specific detection of particular proteins or clarify their localization in cells and tissues or as markers for beginning cell death, depending on particular test conditions. Besides, the use of microscope had increased in the manufacturing sectors of miniature transistor chips, nanoelectronics, quantum dots, and optoelectronics where the demand for digital microscopes is high. These factors are expected to contribute more towards the market growth in the forecast period between 2019 and 2026.

Optima Insights had segmented the key components of the report based on Modality (Desktop & Portable), Application (R&D, Healthcare, Forensics, Electrical, Electronics, Mechanical, Metallurgy & Material Sciences) and Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa).

As far as geography is concerned North American market holds the major share with more than 40% contribution towards the growth followed by Europe and the Asia Pacific. In the forthcoming years, the contribution of the Asia Pacific region is expected to increase with more focused research and transfer of technology.

The desktop microscopes hold more than 75% of the market share with portable microscopes contributing less than 20%. However, the contribution of portable microscopes in market growth is expected to increase by more than 21% during the forecast period. The major share of the microscope use is split by only four disciplines such as healthcare, R&D, Material Sciences and Electronics with more than 80% of the market share with the R&D sector alone holding more than 35% of the market share.

Totally 88 companies across geographies were identified as potential players in the market. This includes Thermo Fisher Scientific Inc, Bruker Corporation, Carl Zeiss AG, Leica microsystems, JEOL Ltd, Keyence Corporation, Olympus Corporation, Nikon Corporation, Horiba Scientific, Oxford Instruments plc, Tagarno Digital Microscope Solutions and more… The companies entitled to more than 600 products that are being used across several disciplines.

Key Technological Overview

· Synaptive Medical has a Modus V™ Fully-automated, hands-free, robotically-controlled digital microscope with advanced visualization that supports a wide range of surgical approaches and workflows

· Imec has developed on-chip lens-free microscope integrated into life sciences and biotech tools, targeting multiple applications such as label-free cell monitoring, automated cell culturing

Research Scope

· Provides detailed Analysis of the Market Structure along with forecast of the various segments and sub-segments.

· Provides a Comparative Analysis of Key Marketed and Pipeline Products.

· Provides Key Information on Players involved.

· Provides a Complete Overview of Market Segments and the Regional Outlook.

· Provides In-depth Coverage of Key News, including Major Mergers, Acquisitions and Product Development updates such as clinical trial progression updates and regulatory updates

The Report Provides Key Insights on

· History of the Digital Microscope Market, 2015 to 2017

· Forecast of the Digital Microscope Market Growth till the year 2026

· The key market drivers, restraints, challenges, future opportunities and the market dynamics driving the Digital Microscope Market

· Analysis of potential growth segments which will drive the market

· Landscape analysis of the major companies, and new market entrants and companies which possess disruptive technologies which can change the trend of the entire market

· Key market approaches adopted by the organizations and in-depth intelligence of potential strategies which could alter the market dynamics

Download Complete TOC of the Report @ https://www.optimainsights.org/request-toc/67-digital-microscope-market

About Us

Optima Insights is an innovative research and insights-driven enterprise committed to offering actionable intelligence to the global life science and healthcare market. We believe that meaningful insights and improved strategic content hold the key to improved ROI for our clients. We strike an innovative engagement model with our clients to Co-Create Intelligence that would address very specific issues facing them within their functional areas. We continuously support clients through the entire journey map to enable them to make better business decisions towards attaining market leadership.

Contact

Optima Insights Pvt Ltd.

Chucks G

+91 966 6620 365 (Asia) | +1 424 2554 365 (US)

Email: [email protected]

https://www.optimainsights.org

1 note

·

View note

Text

The digital pathology market demand has witnessed notable changes in terms of product innovation. One of the major reasons behind this is the scope of cloud integration with pathology outcomes in laboratory operations. According to a recent report by Future Market Insights, the global digital pathology market was valued at USD 6.19 Bn in 2021 and is expected to witness a CAGR of 13.5% during the forecast period (2021 – 2031).

The scope of digital pathology with cloud integration has expanded with promising potential for numerous therapies in the healthcare industry including anti-cancer treatments. Innovation in terms of product efficiency, capabilities, and other modalities drives growth in the digital pathology market.

Key Takeaways of Digital Pathology Market Study

Digital pathology equipment is anticipated to increase at a CAGR of 13.7% over 2021-2031, to reach US$ 12.94 Bn by 2031, aided by growing investments by hospitals and laboratories.

The clinical pathology and molecular diagnostics segment collectively have gained more than 50% of the market share in terms of revenue owing to use for a wider scope of ailments.

CROs are estimated to display high growth potential at a CAGR of 19.0% in the forecast period owing to cost benefits to end users.

Canada is reflecting high potential for growth with a 14.2% CAGR, driven by the expansion of urban centers and investments into healthcare facilities.

The U.K. will account for over 24% of the Europe value share, surpassing Germany by 2031, owing to increases in healthcare research spending.

A number of modern hospitals are installing newly modified digital pathology systems for their laboratories which has widened the consumer base of the market globally. Manufacturers of digital pathology solutions are constantly making changes in software, to enhance the capabilities and efficacies of digital pathology devices.

This development will provide easy access to information such as images, and will also cater to specialized needs. In 2017, Glencoe Software Inc., launched a software named Path Viewer, which is used in interactive viewing and annotation of digital pathology images.

In Jan 2018, Definiens AG released Tissue Studio 4.2 software package. The updated product suite provided improved image analysis for researchers in academic medical laboratories, comprehensive cancer diagnostic and treatment centers, biotechnology, and pharmaceutical companies.

“Growing research and development initiatives aimed towards cancer diagnosis and treatment are key factors expected to provide major growth opportunities for the digital pathology market through the end of 2031,” says the FMI Analyst.

Who is Winning? Leading players in the market are largely focused on product development launches in addition to investing in strategic acquisitions and capacity expansions, to explore previously untapped markets.

Some of the top digital pathology companies in the market are :

Danaher Corporation,

Hoffmann-La Roche AG

Huron Technologies International Inc.

Koninklijke Philips N.V.

Olympus Corporation

Hamamatsu Photonics K.K.

Carl Zeiss

3D HISTECH Ltd.

Want more insights? Future Market Insights brings the comprehensive research report on forecasted revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2014 to 2029. The study provides compelling insights on digital pathology market on basis of component type (systems, software, and services), application (clinical pathology, molecular diagnostics, basic & applied research, drug development, others) and end users (hospitals, diagnostic laboratories, pharmaceutical & biotechnology companies, forensic laboratories, research institutes, contract research organizations, and clinics across seven major regions.

Key Segment By Product Type:

Equipment

Whole Slide Scanners

Brightfield Slide Scanners

Fluorescence Slide Scanners

Combination Slide Scanners

Clinical Microscope

Tissue Microarrays

Softwares

Image Viewing and Analysis Softwares

On-premise

Cloud-based

Digital Pathology Information Systems

On-premise

Cloud-based

Services

Installation and Integration Services

Consulting Services

Maintenance and Validation Services

For more Information @ https://www.futuremarketinsights.com/reports/Global-digital-pathology-market

By Application:

Clinical Patholog

Molecular Diagnostics

Basic & Applied Research

Drug Development

Others

End-User:

Hospitals

Diagnostic Laboratories

Pharmaceutical & Biotechnology Companies

Forensic Laboratories

Research Institutes

Contract Research Organizations (CROs)

Clinics

0 notes

Last Seen Blogs