#thank you pmi for this important info

Text

Why did it take a pretty much it video to find out that the josh whitehouse who plays eddie roundtree in djats is the knight from that vanessa hudgens christmas movie and also the guy from the valley girl movie with jessica rothe

#this is a josh whitehouse stan blog#thank you pmi for this important info#josh whitehouse#eddie roundtree#wordsbyalexis

13 notes

·

View notes

Text

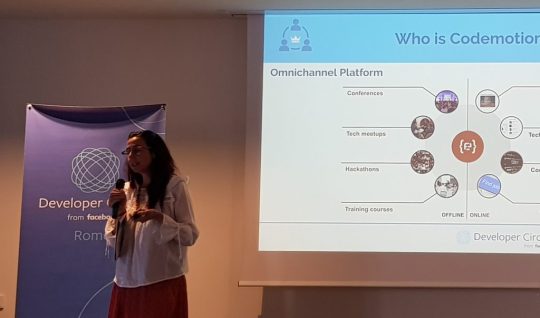

From Developer to CTO - Tech Leadership Training Bootcamp by Codemotion - Day 1

Today I was pleased to attend to the "From Developer to CTO" Bootcamp, the final phase of the Tech Leadership Training Course: an online program promoted by Facebook Developer Circles in partnership with Codemotion and designed to help developers in their journey to become Chief Technical Officers by combining strong interpersonal, influential and technical skills.

Here's a quick breakdown of the previous modules:

Module 1: Defining the CTO Role, focused on defining the role of CTOs by touching their main responsibilities and challenges.

Module 2: AI/Machine Learning, dedicated to some strategic approaches to use this technology to create real innovation for a startup or company, and also focused on giving suggestions to the CTO to correctly introduce a new technology in a company.

Module 3: Software Architecture/DevOps, based upon the concept of scaling and the analysis / review of the DevOps methodology, a modern and versatile full-stack approach that can be used to effectively deal with such problems.

The bootcamp, being the final phase of the course, is meant to be a unique opportunity to summarize and empower the knowledge about the topics covered in the previous three modules by gaining valuable insights from a highly experienced group of Codemotion and Facebook experts.

The place

The bootcamp is a 2-days event hosted by Codemotion by the LUISS EnLabs & LVenture Group venues in Rome, Italy.

LUISS EnLabs, also known as "The Startup Factory", is one of the leading startup accelerators in Europe. It was established in 2013 as a joint venture between LVenture Group - a venture capital operator listed on the Stock Exchange - and LUISS Guido Carli University, and in just a few years it has accelerated over 60 startups. Twice a year LUISS EnLabs selects them for its Acceleration Programs and also organizes Open Innovation Programs to bring corporates into the world of innovation. Overall, the startups have collected 44 million euros, 11 from LVenture Group and the remaining from other international venture capital funds and Business Angels. Thanks to the support of its network of investors, corporates and institutions - including LUISS University - and its partners Wind Tre, BNL Gruppo BNP Paribas, Accenture and Sara Assicurazioni, LUISS EnLabs has grown into a real point of reference for innovation in Italy.

The Program - First Day

8:20: check in opening

9:00: Opening by Facebook

9:10: Opening by Codemotion

9:15: Talk by Codemotion: Data-Driven Decision especially in the CTO perspective, Andrea Saltarello, CTO @Managed Designs

10:30-10:40: Small Break

10:40: Talk by Codemotion: Business / financial management, Andrea Saltarello, CTO @Managed Designs

12:15: Talk by Codemotion: Tech Team Management (pt.1), Antony Mistretta, Founder @Inglorious Coderz

13:15-14:00: Lunch break

14.00-16.30: Talk by Codemotion: Tech Team Management (pt. 2), Antony Mistretta, Founder @Inglorious Coderz

All the talks have been held in english language.

Openings

The Bootcamp started with a brief talk of Mara Marzocchi, co-founder and Codemotion and operating as Chief Content Officer since 2011. She briefly reviewed the daily program and explained the attendees a series of info related to the overall course and the Codemotion roadmap for the upcoming months - which will eventually lead to Codemotion Milan 2019, the largest italian Tech Conference (October 24-25, 2019).

It was then the turn of Willie Elamien, Facebook Product Partnership Program Manager, which explained what Facebook Developer Circles actually is: a brand-new Facebook project aiming to create an international community made from local developer groups in the various parts of the globe and connect them with startups and companies looking for developers, tech leaders and CTOs.

The main idea of Developer Circles revolves consists in helping their members to collaborate, learn, and code in the following ways:

Connect with other developers: Access an exclusive local Facebook Group community and attend meetups near you.

Engage with local experts: Each community is organized and run by local developer Leads.

Learn about new tech: Learn about Bots, AI, IoT, React and other tools.

Build with other developers: Collaborate with developers of all types using the local communities and meetups.

For additional info, you can visit the Facebook Developer Circles Presentation Video or just take a look to the official program page.

Data-Driven Decisions from the CTO perspective

The third talk was hosted by Andrea Saltarello, CTO at Managed Designs, Microsoft Regional Directors member and successful IT enterpreneur. During his long (~ 3 hours) attendance, he did a great job by bringing a lot of very interesting topics to the table.

He started defining the main aspects that helps defining a good CTO: relying to data-driven decision instead of gut feeling; acting as a translation layer between business expectations and technicians, people vs strict way of thinking; being able to calculate how much amount you can afford to invest in knowledge in order to avoid the potential losses coming from innovations and breaking changes you might miss otherwise; being able to communicate with colleagues and employees and also enforce communication between layers; countinuosly sharing feedbacks, as opposed as keeping everyone in the dark.

He clearly explained how all these concepts, if properly embodied by a competent CTO, could help him in to match what company needs with what the employees - and the customers - like the most.

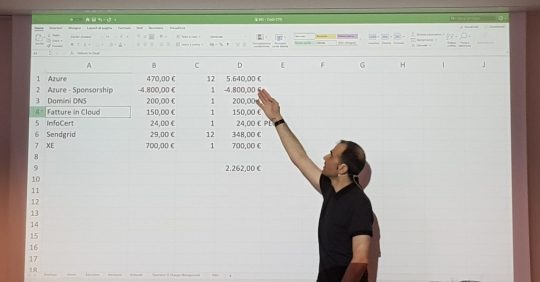

He also introduced us to feenpal, a web-based e-invoicing SaaS he's currently working with, to make real-life examples of the decision-making tasks that a CEO has to perform when he's in charge of defining the launch of a new IT product. He explained how to rely with the other executive partners - the CEO, the CIO, the marketing manager and so on: once again, communication and knowledge sharing was the ultime key to success. He emphasized this concept a lot, and I think he pretty much nailed it: despite being obvious, most companies and startups just don't have it in their DNA, thus being unable to properly design and/or succesfully launch a new project.

It definitely was a great session, with a lot of valuable concepts to learn. I really liked the fact that most of the info transmitted by Andrea perfectly applies to any scenario - including the PMI-based Italian one - since most of these talks tend to give advices that are only fit for international companies.

Business & Financial Management

After a small coffee break, Andrea got the microphone back to talk about Business & Financial Management from a CTO perspective, consisting in a rather versatile and heterogeneous set of skills such as: planning the activities ahead, thus avoiding task switching; being able to handle the various aspects of the business plan, such as: anaging assets, evaluating the budget, being able to assess and prevent the risks, considering the change management costs and evaluate the gains & losses of present and future activities; being able to properly calculate the TCO (Total Cost of Ownership) using timesheets, GANTT and all the available data.

Again, the data-driven decision approach was granted a major role here.

Tech Team Management

Right after Andrea came the turn of Matteo Anthony Mistretta, the founder of Inglorious Coderz, who hosted a two-parts talk (before and after the lunch break) about Tech Team Management.

I have to say that I literally loved his talk: during my 15 years of life spent as a lead developer, I can say I have experienced first-hand most - if not all - the scenarios, and samples that Matteo mentioned during his speech... and, most importantly, I approached them in the same way and reached the same conclusions - and, luckily enough, mostly achieved the same goals. That talk was almost a deja vu to me - to the point that I think I could also be an inglorious coder myself!

Jokes aside, Matteo made a terrific job explaining what being a Tech Team Manager actually means by making use of an enticing example-driven storytelling that encompassed the latest 20 years - roughly from the 2000s to the current days.

Practical technical leading; the importance of communicating with the management - by properly "translating" the technical terms - and to push developers to do that as well; being a a leader, not a boss; the irreplaceable role of the metrics: pertinence, customizability, innovation, freshness and application, for the technologies; architertural skills, PM skills and trasversal skills, for developers; satisfaction and happiness, for the stakeholders; speed, cost, coverage and quality, for the actual development phase. Marco introduced and explained all of these concepts with an unique, passionate approach that could only come from the heart of someone who actually did that for a good part of his life, and the audience immediately got that.

The bootcamp lunch box: two big sandwitches, an Oreo pack and free water & coke!

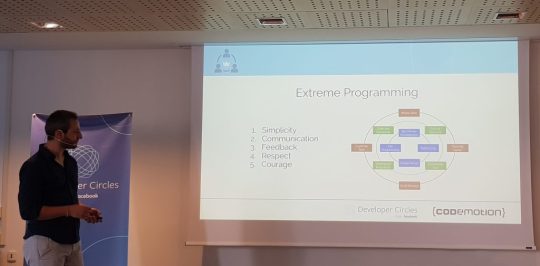

In the second part of the talk, he switched to Agile topics and introduced some key concepts of eXtreme Programming (XP), a development methodology that emphasizes software quality and code responsiveness by making and extensive use of some proven good coding practices, such as: measurable, understandable Values; Test-Driven Development; Pair Programming; steady develoment speed; frequent iterations; constant refactoring (to keep the complexity constantly low while adding new features); and so on.

He then explained his views regarding how to be a good Project Manager: planning, coordinating activities (and assigning them properly), keeping track of what goes on (with timesheet and gantt), adapting to changes, driving communication, and - yet again - feedbacks. He then did the same with the key functions of a good Team Leader: assign responsibilities, making people grow, empowering people, leading by example, motivating.

Last, but not least, he talked about licensing management, first from the "buyer" and then from the "seller" point of view. He did his best to explain the differences between open-source and closed-source software, full packaged products (FPP), original equipment manufacturer (OEM), commercial use vs proprietary use, volume licensing, and so on. Truth to be told, this was perhaps the least intere spot of the whole talk - mostly because the previous topics were a blaze!

Conclusion

This was definitely a great bootcamp: the speakers did their best to give invualuable insights. I can only imagine how beneficial such "summary" would be for a young developer: I really wish I had these kind of stuff available when I started coding myself :) Can't wait for the next part!

Read the full article

0 notes

Text

PMP® Certification Training

You may have heard about PMP Certification, but possibly you're not quite positive what it is or why you'd pursue it. If you're within the challenge management subject, here are answers to 7 of the generally asked questions in regard to in search of the PMP certification. To be able to be a PMP certified professional, you first should first be educated for it. The PMP course is essential within the preparation for the PMP Certification examination as they offer key info regarding product lifecycle, venture phases, and PMP Course of Groups. Step 1: When you log in, you will have to decide on the take a look at sponsor from the director and then press the search button. The check sponsor of PMP® exam is PMI- Project Management Institute.

PMP Certification in Abu Dhabi

As soon as you're PMP Licensed, we handle your PMP renewal and continuous learning wants (PDUs) for the lifetime and it's completely freed from value. The individual who holds this certification show their expertise in the subject of Business Analysis. It also allows the holder to work efficiently with stakeholders and gain correct necessities. PBA certificates is obtainable by PMI and is for candidates who've prior expertise in Enterprise Evaluation.

You may think about PMP classroom program from PMP Shut - PMExperto They supply a combo package of normal classroom coaching and a self-studying on-line course. The classroom coaching is good for learning & understanding ideas while the net course is nice for self-study & exam preparation. Creating content is a good way for professionals in strategy to earn Giving Again PDUs. Publishing digital content material on-line that relates again to your subject counts in the direction of your re-certification — and it provides you room to get a little creative.

Professionals who pursue project management certification are making a precious, long-term funding of their careers. The PMI requires a charge for each exams with the cost of the CAPM examination at $225 for PMI members and $300 for non-members. The price of the PMP examination is $405 for PMI members and $555 for non-members. four) Get seen by Recruiters: Organisations want to hire PMP® certified professionals over non-certified professionals. It demonstrates their proficiency in undertaking administration and catches a recruiter's eye instantly.

Step 2: When you log in, you may have to decide on the test sponsor from the director and then press the search button. The test sponsor of PMP® exam is PMI- Mission Administration Institute.

It was an exquisite Experience with GlobalSkillup. Special Thanks to trainer Hari for coaching us so well. He is not only an experienced trainer but also an important particular person. I'd recommend GlobalSkillup to all those who need to be PMP skilled. You not only get educated, but additionally construct a powerful community with everyone here. three) Greater Salary Potential: Those with a PMP® certification garner the next salary (20% higher on common) than these without a PMP® certification.

ExcelR PMP Certification in Abu Dhabi

With the intention to keep the integrity of the PMP certification and enhance the credibility of PMP Certification holders, PMI routinely conducts random audits on a certain proportion of the PMP examination applications. Although PMI doesn't publish what percentage will get audited, our sixteen years of experience exhibits about one in 4 or 5 of the functions get audited.

0 notes

Text

Trump and The Stock Markets – Weekly Market Update – CapitalistHQ

Good morning,

President Trump continues to the center for market movements, but we believe the markets are adjusting. We have included a several special reports to give you a better understanding of the markets.

What’s in this week’s Report:

Four Looming Market Catalysts

Weekly Market Preview

Weekly Economic Cheat Sheet (Inflation Is the Key)

Is Earnings Growth Losing Momentum?

Are Bank Stocks Breaking Out?

China Trade Update – What Could Go Wrong?

Futures are very slightly higher following a mostly quiet weekend.

The most notable news from the weekend was the passage of UN sanctions on North Korea, which China supported. That move reduced the chances of a trade investigation of China by the US and removes, for now, a potential negative from the market.

Economic data was mixed as Chinese Trade Balance was in-line, while German IP was soft (-1.1.% vs. (E) -0.3%) but neither number is moving markets.

Today focus will be on whether the dollar and Treasury yields can continue the post jobs report rally. If bond yields move higher that could put a mild headwind on stocks.

Economically, it should be a quiet day as there is only one economic report, Consumer Credit (E: 16.0 bln), and two Fed speakers, Bullard (11:45 a.m.) and Kashkari ( 1:25 p.m.). But, barring any shocking surprises, that data and those Fed speakers shouldn’t move markets (Consumer Credit isn’t widely followed and neither Fed speaker is part of leadership).

Trending News:

DOL Releases New Fiduciary FAQ on Retirement Plans

…MCMASTER ALLY BILL KRISTOL SCHEMING WITH JEB! ADVISER TO OUST TRUMP…

Rosenstein: Lawmakers and White House Officials Could Be Prosecuted for Leaking Classified Info

UNREAL. #NEVERTRUMP SENATOR BRAGS ON FOX NEWS SUNDAY ABOUT PUSHING BACK AGAINST TRUMP (VIDEO)

DIRTY COP: Here Are the Major Scandals that Took Place When Robert Mueller Was FBI Director

Today should be a relatively quiet day as there is just one economic report, Pending Home Sales (E: 0.9%), and no notable Fed speakers and the critical economic releases this week don’t start still tomorrow (the Core PCE Price Index). So, absent any easily identifiable catalysts this morning, we’re back to watching the tech sector – as it goes, so goes the market.

Sincerely,

CapitalistHQ.com

Market

Level

Change

% Change

S&P 500 Futures

2,474.25

2.25

0.09%

U.S. Dollar (DXY)

93.325

-0.66

-0.07%

Gold

1,256.30

-2.00

-0.16%

WTI

49.06

-0.52

1.05%

10 Year

2.27

0.00

0.00%

Stocks

Last Week (Needed Context as We Start a New Week)

Stocks were little changed last week, as multiple, conflicting elements of good vs. bad earnings; strong vs. soft data, and hawkish vs. dovish Fed outlooks all ended in a relative stalemate. The S&P 500 edged up 0.19% and is up 10.63% year to date.

Trading started quietly last week, as the S&P 500 was flat Monday amidst little news, and ahead of the first big economic report of the week… the Core PCE Price Index.

That number was released Tuesday, and was in line with expectations. As a result, the S&P 500 drifted 0.24% higher, helped by a good rally in Europe.

It looked like the rally would continue Wednesday given positive AAPL earnings, and dovish comments from Cleveland Fed President Mester. But news that President Trump was close to initiating an investigation into Chinese trade practices (a move that could lead to tariffs) pressured the S&P 500, which closed flat.

Thursday saw a modest decline in stocks thanks to a disappointing ISM Non-Manufacturing PMI, more trade worries (Trump was set to announce the investigation Friday) and a late-day headline that Special Counsel Mueller was assembling a grand jury (although that headline isn’t surprising, as it’s just the next logical step in the investigation). The S&P 500 dipped 0.22%.

Stocks drifted slightly higher Friday, helped by 1) The delay of any China trade investigation, and 2) A generally “Goldilocks” jobs report. The S&P 500 drifted slightly higher despite a rally in Treasury yields and the dollar, and closed up 0.19% on the day, and for the week.

Your Need to Know

Although most of the structurally important companies already released results, there remained a large volume of less-followed names that reported last week, and that largely drove sector trade… with two exceptions.

First, the profit-taking rotation out of tech and into banks continued. Nasdaq again lagged (-0.36%) while banks and financials outperformed (up 2% each). Again, that trend is potentially important because it implies a rotation towards more cyclical leadership, which could be a broader positive for stocks if the BKX can breakout. KRE remains our preferred bank ETF, although KBE also is becoming attractive.

Second, large, multi-national industrials continued to massively outperform. The Dow Industrials rallied 1.2% thanks to strong earnings, and a weaker dollar/rising international tide of growth. If the dollar decline is taking a breather (as Friday might imply) you should see some give back from industrials, although in general the sector remains attractive due to the global recovery.

Bottom Line

Almost all the 2017 rally has been earnings and momentum driven, but with growing signs earnings momentum is potentially fading, we’re left with the question of “What’s Next?” to power stocks higher. Expected 2018 S&P 500 EPS has risen from around $133 at the start of the year to $140, and markets have maintained a 17.75ish multiple on stocks. So, that rising earnings number has largely carried stocks higher through political noise and lack luster growth.

But, as we discussed in Friday’s report, there are signs that earnings growth momentum appears to have slowed slightly in Q2. And, if we look past the 1% pop the “Dovish” turn in the Fed provided in early July, we’re left with a broadly stalemated market that’s in need of a catalyst to decide whether this rally can continue, or fade. As we look out over the remainder of 2017, as of right now, we think that catalyst (positive or negative) could come from one of four places:

1. Economic growth. It’s not particularly good, but it’s still consistently showing around 2%-3% GDP growth. If growth stays the same and inflation drops further, it could provide a modest tailwind for stocks near term (basically an extension of the mid-July rally). However, the key to a sustained medium/longer-term rally is a reflation, i.e., economic growth accelerating along with inflation.

2. Tax Cuts. The market still expects some corporate tax cut in early 2018. If that idea is confirmed by Washington this fall, that could be a boost to stocks because 2018 EPS will rise. Conversely, if the market thinks tax cuts are in doubt, that will be a headwind because it removes possible upside from 2018 EPS.

3. Fed Policy. If the Fed stays dovish due to low inflation (as they have since July), that’s a tailwind. However, if the Fed focuses on low unemployment and gets more “hawkish” in tone again, that will pressure the broad markets (we’re going to cover the Fed outlook more in tomorrow’s report).

4. Politics. The market expects both the debt ceiling and budget to be extended, so those two events won’t really be positives (assuming they happen). However, if dysfunction in Washington grows or the Russian investigation takes a surprise turn, it could hit stocks.

Bottom line, currently this is not an environment fraught with risk, but there aren’t a lot of discernable positive catalysts looming, either… especially given valuations and potential earnings trends.

Given that, we remain cautiously positive on stocks and still hold tactical allocations that have worked all year (the “Stagnation” portfolio), including super-cap tech (FDN), healthcare (IHF/IBB/XLV), Europe (HEDJ/EZU) and emerging markets (IEMG).

Looking ahead, the most interesting question now for markets is whether this tech vs. banks rotation continues. KRE remains our preferred way to own banks, although given rising global yields KBE is getting more attractive, too (KBE has more multi-national bank exposure). We are holding the KRE position we bought several weeks ago, but we’ll need to see a breakout before adding to it or KBE.

In sum, this is a market moving towards some sort of resolution (higher or lower). For now, the prudent action remains to simply go along for the ride until we have more color on which way it looks like the break will go.

Economic Data (What You Need to Know in Plain English)

Need to Know Econ from Last Week

Friday’s jobs report caused a mild reversal of the week’s long downtrend in yields and the dollar, but that was more a function of “covering shorts” on the news rather than it was a function of the jobs report being materially hawkish (it met our “Just Right” scenario).

In total, while unemployment dipped further and wages were steady, in aggregate the economic data from last week largely reinforces the “stagnation” outlook for markets (slow-but-steady growth, low inflation).

Starting with the jobs report, as mentioned, it hit the upper end of our “Just Right” scenario. The headline job adds was stronger than expected (209k vs. 178k) while the June revisions were positive (up 9k to 231k).

Meanwhile, unemployment and wages met expectations: 4.3% unemployment and 0.3% wage gains, with a 2.5% yoy increase. In all, it’s a pretty Goldilocks jobs report, as job adds remain strong and the downtrend in wage inflation appears, at least in July, to have stopped.

That’s why we saw the rally in the 10-year Treasury yield and dollar. It wasn’t that the report was hawkish, but it did stop the trend in lower inflation stats. And, with a market as stretched to the downside as the Dollar Index and 10-year yield both are, it caused a snap-back rally.

Importantly, other than potentially making a December rate hike slightly more expected, Friday’s jobs report did nothing to alter the outlook for the Fed (still balance sheet reduction in September).

Looking at the economic data the rest of last week, it was more of the same: Not particularly impressive, but not implying a slowdown, either.

The ISM Manufacturing PMI slightly beat estimates at 56.3 vs. (E) 56.2, and that remained well above the important 50 mark. So, while there was a decline from June, it remains indicative of a manufacturing sector that is seeing growth accelerate.

The one disappointing economic data point last week was the ISM Non-Manufacturing (or service sector) PMI. It declined to 53.9 vs. (E) 56.9, and was the weakest reading since August 2016. However, the private sector Markit Services PMI rose to 54.7 from 54.2, so there is a conflicting message there (ISM is one firm that produces PMIs, and Markit is a competitor. Usually, their PMIs are generally in agreement, but not this month… and it has to do with the survey questions each use and the makeup of the final indices. It’s an oddity that there was a discrepancy, but it’s not an economic red flag (at least not at this point).

Bigger picture, economic growth through June and July appears consistent with the slow-but-steady growth we’ve become accustomed to over the past several years. It’s certainly not a negative for stocks, but it’s not going to create a rising tide that propels us to new highs.

Important Economic Data This Week

As is usually the case for the week following the jobs report and the PMIs, this week will be quieter from an economic data standpoint, although there is a very important report coming this Friday… CPI.

As we’ve said consistently, inflation is much more important right now (because it’s declining) than economic growth (which remains steady), so inflation numbers will have the potential to move markets more than growth numbers, as we saw on Friday with the jobs report.

To that end, Friday’s CPI has the potential to send bond yields and the dollar higher, if it confirms Friday’s wage number that implies inflation steadied in July. Conversely, if the CPI report is soft we’ll see Friday’s rally in bond yields and the dollar undone, quickly.

Outside of CPI Friday (and PPI on Thursday) the next most-important data point this week will be the Productivity and Costs report Wednesday. In Friday’s Report, I listed a number of events that could push stocks higher if earnings growth has peaked near term. Increased productivity was one of those events, so a strong productivity number will be positive for markets.

Beyond those two numbers, the domestic calendar is quiet this week, and none of the reports coming (NFIB Small Business Optimism Index, jobless claims) should move markets too much.

Commodities, Currencies & Bonds

In Commodities, the segment was mostly lower last week as oil prices pulled back from the $50 level, and a rally in the dollar on Friday weighed broadly on the space, especially the metals. The commodity ETF, DBC, fell 0.87% on the week.

Beginning with the precious metals, gold was in focus last week as it rallied to a six-week high on more stagnation money flows and positioning into the July jobs report. But, when the jobs report came in hot and Treasury yields spiked higher, gold came for sale and closed the week down 0.89%.

Technically speaking, the outlook for gold still is tipped in favor of the bears after futures broke down to new lows in early July. And last week’s failure to retest the $1300 level also is less than encouraging. Meanwhile, a potential hawkish shift in Fed policy outlook would be fundamentally bearish for the precious metal. If gold were able to break out through the $1300 level that would be a bullish development, and would have us reconsider our cautious stance.

It was a choppy week in copper, as futures traded in a roughly 5-cent range before closing up a modest 0.28% thanks mostly to the dollar strength on Friday. The outlook for copper remains bullish, and that is a solid indication that sentiment towards the global economy is positive (an encouraging sign for risk assets).

In the energy space, natural gas continued to trade heavy, falling 5.02% on the week as the prospects for weather-driven demand faded as most analysts and meteorologists believe the hottest portion of the summer is already behind us. Looking ahead, natural gas futures will likely continue to drift lower with the next notable support level below at $2.69.

Turning to oil, futures were rather volatile last week; however, by Friday afternoon they had not moved much. WTI finished down 0.54%. The $50 mark is acting as a substantial psychological resistance level right now, as the trend of rising US production and OPEC doubts continue to weigh on sentiment. Until we see US output begin to level off, or a materially bullish development out of overseas producers (such as a sizeable and collaborate cut), it will be hard for WTI to rally meaningfully through the low-to-mid $50s.

Looking at Currencies and Bonds, there were multiple conflicting influences on markets last week, but the net effect is that the downtrend in the dollar and bond yields may have been halted if this week’s CPI is firm. If that is the case, it’s positive for “reflation” sectors such as banks (KRE), small caps (IWM), industrials (XLI) and inverse bond funds (TBT/TBF). The Dollar Index gained 0.6% on the week while 10-year Treasury yield dipped three basis points, but finished off the lows of the week thanks to the big post-jobs-report rally.

Looking at last week’s catalysts, initially the dollar and bond yields were solidly lower on the week following lackluster US economic data (not bad, but not very strong, either), strong EU data and dovish comments by the Fed’s Mester (she lowered her the lowest level she’d tolerate unemployment to 4.75% from 5.0%, which is dovish).

But, those dovish influences (which had the Dollar Index down 0.8% and 10-year yields down 5 basis points by Friday morning), all were reversed by the jobs report. Specifically, as mentioned, it was the drop in unemployment rate to 4.3% and the firm wage number (0.3% m/m) that caused the reversal. Now, to be clear, it wasn’t that those numbers were hawkish, but they did stop the trend in lower inflation stats. And with a market as stretched to the downside as the Dollar Index and 10-year yield, it caused a snap-back rally. Now, whether last week’s rally can extend will depend on Friday’s CPI.

Looking internationally, news was relatively sparse outside of the Bank of England, which issued a “not hawkish” decision last Thursday that sent the pound down 0.7% on the week. However, we don’t see it as a shift in policy, just a correction of the market’s “too hawkish” expectations. We still expect a rate hike from the BOE some time in 2H, 2018.

Bottom line, the major question in the currency and bond markets remains: Will the dollar and the Treasury yield declines reverse? This week could provide an answer via Friday’s CPI… and that will have implications for the stock market.

Special Reports and Editorial

Are Strong Earnings Already Priced In?

Earnings have been an unsung hero of the 2017 rally, but there are some anecdotal signs that strong earnings may already be priced into stocks, leaving a lack of potential positive catalysts given the macro environment.

Now, to be clear, earnings season has been (on the surface) good. From a broad standpoint, the results have pushed expected 2018 S&P 500 EPS slightly higher (to $139) and that’s enough to justify current valuations, taken in the context of a calm macro horizon and still-low bond yields.

However, the market’s reaction to strong earnings is sending some caution throughout the investor community. Specifically, according to BAML, the vast majority of companies who reported a beat on the top line (revenues) and earnings (bottom line) saw virtually no post-earnings rally this quarter. Getting specific, by the published date of the report (early last week) 174 S&P 500 companies had beat on the top and bottom line, yet the average gain for those stocks 24 hours after the announcement was… 0%. They were flat. To boot, five days after the results, on average these 174 companies had underperformed the market!

That’s in stark contrast to the 1.6%, 24-hour gain that companies that beat on the revenues and earnings have enjoyed, on average, since 2000.

In fact, the last time we saw this type of post-earnings/sales beat non-reaction was Q2, 2000. It could be random, but that’s not exactly the best reference point.

So, the question becomes, what will spur even more earnings growth?

Potential answers are a rising tide of economic activity, although that’s not currently happening. Another is a surge in productivity that increases the bottom line. But, productivity growth has been elusive for nearly a decade, and it’s unclear what would suddenly spark a revival. Finally, another candidate is rising inflation that would allow for price and margin increases. Yet as we know, that’s not exactly threatening right now, either.

Bottom line, earnings have been the unsung hero of this market throughout 2017, but this is a, “What have you done for me lately” market, especially at nearly 18X next year’s earnings. If earnings growth begins to slow and we don’t get any uptick in economic growth or pro-growth policies from Washington, then it’s hard to see what will push this market higher beyond just general momentum (which appears to be facing a headwind, at least according to the price action in tech). The trend in stocks is higher, but the environment isn’t as benign as sentiment, the VIX or the financial media would have you believe.

China Trade Update

Last week, we listed four political events that could cause a pullback in stocks, and some movement is occurring on one of the four: Potential steel tariffs on China.

Now, there are no proposed tariffs on China yet, but according to multiple reports, President Trump is considering encouraging US Trade Representative Robert Lighthizer to launch an investigation of Chinese treatment of US corporate intellectual property and general trade practices.

The reason this is important is because Lighthizer might launch the investigation into potential Chinese infractions under the 1974 Trade Act Section 301. The reason that’s important is because if the investigation shows China violated that law, the president has unilateral authority to levy tariffs or impose trade restrictions. This is a potential legitimate first step to tariffs and escalated trade conflict with China.

That notion pressured stocks modestly Wednesday, but some context is needed. And, this is just a potential first step, not a reason to de-risk. Nonetheless, lost in the political soap opera that has been 2017 is the fact that trade has largely been a quiet topic so far in the administration. If that changes, it will be a new headwind on stocks. If this were to go through, multi-national industrials (XLI) and consumer companies (especially large-cap tech) would be the hardest hit.

EIA Analysis and Oil Update

Last week’s EIA report was much less dramatic than those of the past month, as the change in supply levels was much less significant, especially for crude oil. On the headline, crude stocks fell 1.5M bbls, which was less than expected but contradictory to the 1.8M bbl rise reported by the API on Tuesday evening (so, net slightly bullish). Gasoline and Distillate supplies both fell less than the API report, so their influence was less bullish.

Looking to the all-important production numbers, lower 48 production rose another 25K b/d last week to the highest level since mid-July 2015. The fifth-consecutive rise brought the output level in the lower 48 to 9.03M b/d, a total 2017 increase of 789 b/d. Meanwhile, Alaskan production is down 129K b/d so far this year. The reason that’s important is that the pullback in Alaskan output is not unusual for this time of year, and the potential for a rebound in the next two months is relatively high. Such a rebound amid the continued grind higher in lower 48 production would push total US production towards the 10M b/d mark, which would be very bearish for oil.

Bottom line, the oil market is buoyant right now thanks to the recent string of supply declines. However, the overarching supply and demand dynamic has still not turned bullish. With US production continuing its relentless climb; OPEC compliance dropping off, and Saudi Arabia seeming to lose its grip on the cartel, it will take a material catalyst to get oil moving up through the low-to-mid $50s, which will act as a price ceiling near term.

Are Banks About to Break Out?

Banks were a highlight last week, as BKX jumped 2%, which pulled the Financials SPDR (XLF) up 2%. The bank stock strength came despite the decline in yields, which we think is notable. In fact, last week, bank stock performance has decoupled from the daily gyrations of Treasury yields, and we think that potentially signals two important events.

First, it implies bank investors are starting to focus on the value in the sector and on the capital return plans from banks, which could boost total return. Second, it potentially implies that investors aren’t fearing a renewed plunge in Treasury yields (if right, that could be a positive for the markets).

Regardless, this price action in banks is potentially important, because this market must be led higher by either tech or banks/financials. If the former is faltering (and I’m not saying it is), then the latter must assume a leadership role in order for this rally to continue.

This remains a market broadly in search of a catalyst, but absent any news, the path of least resistance remains higher, buoyed by an incrementally dovish Fed, solid earnings growth, and ok (if unimpressive) economic data.

Nonetheless, complacency, represented via a low VIX, remains on the rise, and markets are still stretched by any valuation metric. Barring an uptick in economic growth or inflation, it remains unclear what will power stocks materially higher from here. For now, the trend remains higher.

Disclaimer: CapitalistHQ.com Weekly Market Report is protected by federal and international copyright laws. CapitalistHQ.com is the publisher of the newsletter and owner of all rights therein, and retains property rights to the newsletter. The Newsletter may not be forwarded, copied, downloaded, stored in a retrieval system or otherwise reproduced or used in any form or by any means without express written permission from CapitalistHQ.com . The information contained in CapitalistHQ.com Weekly Market Report is not necessarily complete and its accuracy is not guaranteed. Neither the information contained in CapitalistHQ.com Weekly Market Report or any opinion expressed in CapitalistHQ.com Weekly Market Report constitutes a solicitation for the purchase of any future or security referred to in the Newsletter. The Newsletter is strictly an informational publication and does not provide individual, customized investment or trading advice to its subscribers. SUBSCRIBERS SHOULD VERIFY ALL CLAIMS AND COMPLETE THEIR OWN RESEARCH AND CONSULT A REGISTERED FINANCIAL PROFESSIONAL BEFORE INVESTING IN ANY INVESTMENTS MENTIONED IN THE PUBLICATION. INVESTING IN SECURITIES, OPTIONS AND FUTURES IS SPECULATIVE AND CARRIES A HIGH DEGREE OF RISK, AND SUBSCRIBERS MAY LOSE MONEY TRADING AND INVESTING IN SUCH INVESTMENTS.

source https://capitalisthq.com/trump-and-the-stock-markets-weekly-market-update-capitalisthq/

from CapitalistHQ http://capitalisthq.blogspot.com/2017/08/trump-and-stock-markets-weekly-market.html

0 notes

Text

Trump and The Stock Markets – Weekly Market Update – CapitalistHQ

Good morning,

President Trump continues to the center for market movements, but we believe the markets are adjusting. We have included a several special reports to give you a better understanding of the markets.

What’s in this week’s Report:

Four Looming Market Catalysts

Weekly Market Preview

Weekly Economic Cheat Sheet (Inflation Is the Key)

Is Earnings Growth Losing Momentum?

Are Bank Stocks Breaking Out?

China Trade Update – What Could Go Wrong?

Futures are very slightly higher following a mostly quiet weekend.

The most notable news from the weekend was the passage of UN sanctions on North Korea, which China supported. That move reduced the chances of a trade investigation of China by the US and removes, for now, a potential negative from the market.

Economic data was mixed as Chinese Trade Balance was in-line, while German IP was soft (-1.1.% vs. (E) -0.3%) but neither number is moving markets.

Today focus will be on whether the dollar and Treasury yields can continue the post jobs report rally. If bond yields move higher that could put a mild headwind on stocks.

Economically, it should be a quiet day as there is only one economic report, Consumer Credit (E: 16.0 bln), and two Fed speakers, Bullard (11:45 a.m.) and Kashkari ( 1:25 p.m.). But, barring any shocking surprises, that data and those Fed speakers shouldn’t move markets (Consumer Credit isn’t widely followed and neither Fed speaker is part of leadership).

Trending News:

DOL Releases New Fiduciary FAQ on Retirement Plans

…MCMASTER ALLY BILL KRISTOL SCHEMING WITH JEB! ADVISER TO OUST TRUMP…

Rosenstein: Lawmakers and White House Officials Could Be Prosecuted for Leaking Classified Info

UNREAL. #NEVERTRUMP SENATOR BRAGS ON FOX NEWS SUNDAY ABOUT PUSHING BACK AGAINST TRUMP (VIDEO)

DIRTY COP: Here Are the Major Scandals that Took Place When Robert Mueller Was FBI Director

Today should be a relatively quiet day as there is just one economic report, Pending Home Sales (E: 0.9%), and no notable Fed speakers and the critical economic releases this week don’t start still tomorrow (the Core PCE Price Index). So, absent any easily identifiable catalysts this morning, we’re back to watching the tech sector – as it goes, so goes the market.

Sincerely,

CapitalistHQ.com

Market

Level

Change

% Change

S&P 500 Futures

2,474.25

2.25

0.09%

U.S. Dollar (DXY)

93.325

-0.66

-0.07%

Gold

1,256.30

-2.00

-0.16%

WTI

49.06

-0.52

1.05%

10 Year

2.27

0.00

0.00%

Stocks

Last Week (Needed Context as We Start a New Week)

Stocks were little changed last week, as multiple, conflicting elements of good vs. bad earnings; strong vs. soft data, and hawkish vs. dovish Fed outlooks all ended in a relative stalemate. The S&P 500 edged up 0.19% and is up 10.63% year to date.

Trading started quietly last week, as the S&P 500 was flat Monday amidst little news, and ahead of the first big economic report of the week… the Core PCE Price Index.

That number was released Tuesday, and was in line with expectations. As a result, the S&P 500 drifted 0.24% higher, helped by a good rally in Europe.

It looked like the rally would continue Wednesday given positive AAPL earnings, and dovish comments from Cleveland Fed President Mester. But news that President Trump was close to initiating an investigation into Chinese trade practices (a move that could lead to tariffs) pressured the S&P 500, which closed flat.

Thursday saw a modest decline in stocks thanks to a disappointing ISM Non-Manufacturing PMI, more trade worries (Trump was set to announce the investigation Friday) and a late-day headline that Special Counsel Mueller was assembling a grand jury (although that headline isn’t surprising, as it’s just the next logical step in the investigation). The S&P 500 dipped 0.22%.

Stocks drifted slightly higher Friday, helped by 1) The delay of any China trade investigation, and 2) A generally “Goldilocks” jobs report. The S&P 500 drifted slightly higher despite a rally in Treasury yields and the dollar, and closed up 0.19% on the day, and for the week.

Your Need to Know

Although most of the structurally important companies already released results, there remained a large volume of less-followed names that reported last week, and that largely drove sector trade… with two exceptions.

First, the profit-taking rotation out of tech and into banks continued. Nasdaq again lagged (-0.36%) while banks and financials outperformed (up 2% each). Again, that trend is potentially important because it implies a rotation towards more cyclical leadership, which could be a broader positive for stocks if the BKX can breakout. KRE remains our preferred bank ETF, although KBE also is becoming attractive.

Second, large, multi-national industrials continued to massively outperform. The Dow Industrials rallied 1.2% thanks to strong earnings, and a weaker dollar/rising international tide of growth. If the dollar decline is taking a breather (as Friday might imply) you should see some give back from industrials, although in general the sector remains attractive due to the global recovery.

Bottom Line

Almost all the 2017 rally has been earnings and momentum driven, but with growing signs earnings momentum is potentially fading, we’re left with the question of “What’s Next?” to power stocks higher. Expected 2018 S&P 500 EPS has risen from around $133 at the start of the year to $140, and markets have maintained a 17.75ish multiple on stocks. So, that rising earnings number has largely carried stocks higher through political noise and lack luster growth.

But, as we discussed in Friday’s report, there are signs that earnings growth momentum appears to have slowed slightly in Q2. And, if we look past the 1% pop the “Dovish” turn in the Fed provided in early July, we’re left with a broadly stalemated market that’s in need of a catalyst to decide whether this rally can continue, or fade. As we look out over the remainder of 2017, as of right now, we think that catalyst (positive or negative) could come from one of four places:

1. Economic growth. It’s not particularly good, but it’s still consistently showing around 2%-3% GDP growth. If growth stays the same and inflation drops further, it could provide a modest tailwind for stocks near term (basically an extension of the mid-July rally). However, the key to a sustained medium/longer-term rally is a reflation, i.e., economic growth accelerating along with inflation.

2. Tax Cuts. The market still expects some corporate tax cut in early 2018. If that idea is confirmed by Washington this fall, that could be a boost to stocks because 2018 EPS will rise. Conversely, if the market thinks tax cuts are in doubt, that will be a headwind because it removes possible upside from 2018 EPS.

3. Fed Policy. If the Fed stays dovish due to low inflation (as they have since July), that’s a tailwind. However, if the Fed focuses on low unemployment and gets more “hawkish” in tone again, that will pressure the broad markets (we’re going to cover the Fed outlook more in tomorrow’s report).

4. Politics. The market expects both the debt ceiling and budget to be extended, so those two events won’t really be positives (assuming they happen). However, if dysfunction in Washington grows or the Russian investigation takes a surprise turn, it could hit stocks.

Bottom line, currently this is not an environment fraught with risk, but there aren’t a lot of discernable positive catalysts looming, either… especially given valuations and potential earnings trends.

Given that, we remain cautiously positive on stocks and still hold tactical allocations that have worked all year (the “Stagnation” portfolio), including super-cap tech (FDN), healthcare (IHF/IBB/XLV), Europe (HEDJ/EZU) and emerging markets (IEMG).

Looking ahead, the most interesting question now for markets is whether this tech vs. banks rotation continues. KRE remains our preferred way to own banks, although given rising global yields KBE is getting more attractive, too (KBE has more multi-national bank exposure). We are holding the KRE position we bought several weeks ago, but we’ll need to see a breakout before adding to it or KBE.

In sum, this is a market moving towards some sort of resolution (higher or lower). For now, the prudent action remains to simply go along for the ride until we have more color on which way it looks like the break will go.

Economic Data (What You Need to Know in Plain English)

Need to Know Econ from Last Week

Friday’s jobs report caused a mild reversal of the week’s long downtrend in yields and the dollar, but that was more a function of “covering shorts” on the news rather than it was a function of the jobs report being materially hawkish (it met our “Just Right” scenario).

In total, while unemployment dipped further and wages were steady, in aggregate the economic data from last week largely reinforces the “stagnation” outlook for markets (slow-but-steady growth, low inflation).

Starting with the jobs report, as mentioned, it hit the upper end of our “Just Right” scenario. The headline job adds was stronger than expected (209k vs. 178k) while the June revisions were positive (up 9k to 231k).

Meanwhile, unemployment and wages met expectations: 4.3% unemployment and 0.3% wage gains, with a 2.5% yoy increase. In all, it’s a pretty Goldilocks jobs report, as job adds remain strong and the downtrend in wage inflation appears, at least in July, to have stopped.

That’s why we saw the rally in the 10-year Treasury yield and dollar. It wasn’t that the report was hawkish, but it did stop the trend in lower inflation stats. And, with a market as stretched to the downside as the Dollar Index and 10-year yield both are, it caused a snap-back rally.

Importantly, other than potentially making a December rate hike slightly more expected, Friday’s jobs report did nothing to alter the outlook for the Fed (still balance sheet reduction in September).

Looking at the economic data the rest of last week, it was more of the same: Not particularly impressive, but not implying a slowdown, either.

The ISM Manufacturing PMI slightly beat estimates at 56.3 vs. (E) 56.2, and that remained well above the important 50 mark. So, while there was a decline from June, it remains indicative of a manufacturing sector that is seeing growth accelerate.

The one disappointing economic data point last week was the ISM Non-Manufacturing (or service sector) PMI. It declined to 53.9 vs. (E) 56.9, and was the weakest reading since August 2016. However, the private sector Markit Services PMI rose to 54.7 from 54.2, so there is a conflicting message there (ISM is one firm that produces PMIs, and Markit is a competitor. Usually, their PMIs are generally in agreement, but not this month… and it has to do with the survey questions each use and the makeup of the final indices. It’s an oddity that there was a discrepancy, but it’s not an economic red flag (at least not at this point).

Bigger picture, economic growth through June and July appears consistent with the slow-but-steady growth we’ve become accustomed to over the past several years. It’s certainly not a negative for stocks, but it’s not going to create a rising tide that propels us to new highs.

Important Economic Data This Week

As is usually the case for the week following the jobs report and the PMIs, this week will be quieter from an economic data standpoint, although there is a very important report coming this Friday… CPI.

As we’ve said consistently, inflation is much more important right now (because it’s declining) than economic growth (which remains steady), so inflation numbers will have the potential to move markets more than growth numbers, as we saw on Friday with the jobs report.

To that end, Friday’s CPI has the potential to send bond yields and the dollar higher, if it confirms Friday’s wage number that implies inflation steadied in July. Conversely, if the CPI report is soft we’ll see Friday’s rally in bond yields and the dollar undone, quickly.

Outside of CPI Friday (and PPI on Thursday) the next most-important data point this week will be the Productivity and Costs report Wednesday. In Friday’s Report, I listed a number of events that could push stocks higher if earnings growth has peaked near term. Increased productivity was one of those events, so a strong productivity number will be positive for markets.

Beyond those two numbers, the domestic calendar is quiet this week, and none of the reports coming (NFIB Small Business Optimism Index, jobless claims) should move markets too much.

Commodities, Currencies & Bonds

In Commodities, the segment was mostly lower last week as oil prices pulled back from the $50 level, and a rally in the dollar on Friday weighed broadly on the space, especially the metals. The commodity ETF, DBC, fell 0.87% on the week.

Beginning with the precious metals, gold was in focus last week as it rallied to a six-week high on more stagnation money flows and positioning into the July jobs report. But, when the jobs report came in hot and Treasury yields spiked higher, gold came for sale and closed the week down 0.89%.

Technically speaking, the outlook for gold still is tipped in favor of the bears after futures broke down to new lows in early July. And last week’s failure to retest the $1300 level also is less than encouraging. Meanwhile, a potential hawkish shift in Fed policy outlook would be fundamentally bearish for the precious metal. If gold were able to break out through the $1300 level that would be a bullish development, and would have us reconsider our cautious stance.

It was a choppy week in copper, as futures traded in a roughly 5-cent range before closing up a modest 0.28% thanks mostly to the dollar strength on Friday. The outlook for copper remains bullish, and that is a solid indication that sentiment towards the global economy is positive (an encouraging sign for risk assets).

In the energy space, natural gas continued to trade heavy, falling 5.02% on the week as the prospects for weather-driven demand faded as most analysts and meteorologists believe the hottest portion of the summer is already behind us. Looking ahead, natural gas futures will likely continue to drift lower with the next notable support level below at $2.69.

Turning to oil, futures were rather volatile last week; however, by Friday afternoon they had not moved much. WTI finished down 0.54%. The $50 mark is acting as a substantial psychological resistance level right now, as the trend of rising US production and OPEC doubts continue to weigh on sentiment. Until we see US output begin to level off, or a materially bullish development out of overseas producers (such as a sizeable and collaborate cut), it will be hard for WTI to rally meaningfully through the low-to-mid $50s.

Looking at Currencies and Bonds, there were multiple conflicting influences on markets last week, but the net effect is that the downtrend in the dollar and bond yields may have been halted if this week’s CPI is firm. If that is the case, it’s positive for “reflation” sectors such as banks (KRE), small caps (IWM), industrials (XLI) and inverse bond funds (TBT/TBF). The Dollar Index gained 0.6% on the week while 10-year Treasury yield dipped three basis points, but finished off the lows of the week thanks to the big post-jobs-report rally.

Looking at last week’s catalysts, initially the dollar and bond yields were solidly lower on the week following lackluster US economic data (not bad, but not very strong, either), strong EU data and dovish comments by the Fed’s Mester (she lowered her the lowest level she’d tolerate unemployment to 4.75% from 5.0%, which is dovish).

But, those dovish influences (which had the Dollar Index down 0.8% and 10-year yields down 5 basis points by Friday morning), all were reversed by the jobs report. Specifically, as mentioned, it was the drop in unemployment rate to 4.3% and the firm wage number (0.3% m/m) that caused the reversal. Now, to be clear, it wasn’t that those numbers were hawkish, but they did stop the trend in lower inflation stats. And with a market as stretched to the downside as the Dollar Index and 10-year yield, it caused a snap-back rally. Now, whether last week’s rally can extend will depend on Friday’s CPI.

Looking internationally, news was relatively sparse outside of the Bank of England, which issued a “not hawkish” decision last Thursday that sent the pound down 0.7% on the week. However, we don’t see it as a shift in policy, just a correction of the market’s “too hawkish” expectations. We still expect a rate hike from the BOE some time in 2H, 2018.

Bottom line, the major question in the currency and bond markets remains: Will the dollar and the Treasury yield declines reverse? This week could provide an answer via Friday’s CPI… and that will have implications for the stock market.

Special Reports and Editorial

Are Strong Earnings Already Priced In?

Earnings have been an unsung hero of the 2017 rally, but there are some anecdotal signs that strong earnings may already be priced into stocks, leaving a lack of potential positive catalysts given the macro environment.

Now, to be clear, earnings season has been (on the surface) good. From a broad standpoint, the results have pushed expected 2018 S&P 500 EPS slightly higher (to $139) and that’s enough to justify current valuations, taken in the context of a calm macro horizon and still-low bond yields.

However, the market’s reaction to strong earnings is sending some caution throughout the investor community. Specifically, according to BAML, the vast majority of companies who reported a beat on the top line (revenues) and earnings (bottom line) saw virtually no post-earnings rally this quarter. Getting specific, by the published date of the report (early last week) 174 S&P 500 companies had beat on the top and bottom line, yet the average gain for those stocks 24 hours after the announcement was… 0%. They were flat. To boot, five days after the results, on average these 174 companies had underperformed the market!

That’s in stark contrast to the 1.6%, 24-hour gain that companies that beat on the revenues and earnings have enjoyed, on average, since 2000.

In fact, the last time we saw this type of post-earnings/sales beat non-reaction was Q2, 2000. It could be random, but that’s not exactly the best reference point.

So, the question becomes, what will spur even more earnings growth?

Potential answers are a rising tide of economic activity, although that’s not currently happening. Another is a surge in productivity that increases the bottom line. But, productivity growth has been elusive for nearly a decade, and it’s unclear what would suddenly spark a revival. Finally, another candidate is rising inflation that would allow for price and margin increases. Yet as we know, that’s not exactly threatening right now, either.

Bottom line, earnings have been the unsung hero of this market throughout 2017, but this is a, “What have you done for me lately” market, especially at nearly 18X next year’s earnings. If earnings growth begins to slow and we don’t get any uptick in economic growth or pro-growth policies from Washington, then it’s hard to see what will push this market higher beyond just general momentum (which appears to be facing a headwind, at least according to the price action in tech). The trend in stocks is higher, but the environment isn’t as benign as sentiment, the VIX or the financial media would have you believe.

China Trade Update

Last week, we listed four political events that could cause a pullback in stocks, and some movement is occurring on one of the four: Potential steel tariffs on China.

Now, there are no proposed tariffs on China yet, but according to multiple reports, President Trump is considering encouraging US Trade Representative Robert Lighthizer to launch an investigation of Chinese treatment of US corporate intellectual property and general trade practices.

The reason this is important is because Lighthizer might launch the investigation into potential Chinese infractions under the 1974 Trade Act Section 301. The reason that’s important is because if the investigation shows China violated that law, the president has unilateral authority to levy tariffs or impose trade restrictions. This is a potential legitimate first step to tariffs and escalated trade conflict with China.

That notion pressured stocks modestly Wednesday, but some context is needed. And, this is just a potential first step, not a reason to de-risk. Nonetheless, lost in the political soap opera that has been 2017 is the fact that trade has largely been a quiet topic so far in the administration. If that changes, it will be a new headwind on stocks. If this were to go through, multi-national industrials (XLI) and consumer companies (especially large-cap tech) would be the hardest hit.

EIA Analysis and Oil Update

Last week’s EIA report was much less dramatic than those of the past month, as the change in supply levels was much less significant, especially for crude oil. On the headline, crude stocks fell 1.5M bbls, which was less than expected but contradictory to the 1.8M bbl rise reported by the API on Tuesday evening (so, net slightly bullish). Gasoline and Distillate supplies both fell less than the API report, so their influence was less bullish.

Looking to the all-important production numbers, lower 48 production rose another 25K b/d last week to the highest level since mid-July 2015. The fifth-consecutive rise brought the output level in the lower 48 to 9.03M b/d, a total 2017 increase of 789 b/d. Meanwhile, Alaskan production is down 129K b/d so far this year. The reason that’s important is that the pullback in Alaskan output is not unusual for this time of year, and the potential for a rebound in the next two months is relatively high. Such a rebound amid the continued grind higher in lower 48 production would push total US production towards the 10M b/d mark, which would be very bearish for oil.

Bottom line, the oil market is buoyant right now thanks to the recent string of supply declines. However, the overarching supply and demand dynamic has still not turned bullish. With US production continuing its relentless climb; OPEC compliance dropping off, and Saudi Arabia seeming to lose its grip on the cartel, it will take a material catalyst to get oil moving up through the low-to-mid $50s, which will act as a price ceiling near term.

Are Banks About to Break Out?

Banks were a highlight last week, as BKX jumped 2%, which pulled the Financials SPDR (XLF) up 2%. The bank stock strength came despite the decline in yields, which we think is notable. In fact, last week, bank stock performance has decoupled from the daily gyrations of Treasury yields, and we think that potentially signals two important events.

First, it implies bank investors are starting to focus on the value in the sector and on the capital return plans from banks, which could boost total return. Second, it potentially implies that investors aren’t fearing a renewed plunge in Treasury yields (if right, that could be a positive for the markets).

Regardless, this price action in banks is potentially important, because this market must be led higher by either tech or banks/financials. If the former is faltering (and I’m not saying it is), then the latter must assume a leadership role in order for this rally to continue.

This remains a market broadly in search of a catalyst, but absent any news, the path of least resistance remains higher, buoyed by an incrementally dovish Fed, solid earnings growth, and ok (if unimpressive) economic data.

Nonetheless, complacency, represented via a low VIX, remains on the rise, and markets are still stretched by any valuation metric. Barring an uptick in economic growth or inflation, it remains unclear what will power stocks materially higher from here. For now, the trend remains higher.

Disclaimer: CapitalistHQ.com Weekly Market Report is protected by federal and international copyright laws. CapitalistHQ.com is the publisher of the newsletter and owner of all rights therein, and retains property rights to the newsletter. The Newsletter may not be forwarded, copied, downloaded, stored in a retrieval system or otherwise reproduced or used in any form or by any means without express written permission from CapitalistHQ.com . The information contained in CapitalistHQ.com Weekly Market Report is not necessarily complete and its accuracy is not guaranteed. Neither the information contained in CapitalistHQ.com Weekly Market Report or any opinion expressed in CapitalistHQ.com Weekly Market Report constitutes a solicitation for the purchase of any future or security referred to in the Newsletter. The Newsletter is strictly an informational publication and does not provide individual, customized investment or trading advice to its subscribers. SUBSCRIBERS SHOULD VERIFY ALL CLAIMS AND COMPLETE THEIR OWN RESEARCH AND CONSULT A REGISTERED FINANCIAL PROFESSIONAL BEFORE INVESTING IN ANY INVESTMENTS MENTIONED IN THE PUBLICATION. INVESTING IN SECURITIES, OPTIONS AND FUTURES IS SPECULATIVE AND CARRIES A HIGH DEGREE OF RISK, AND SUBSCRIBERS MAY LOSE MONEY TRADING AND INVESTING IN SUCH INVESTMENTS.

from CapitalistHQ.com https://capitalisthq.com/trump-and-the-stock-markets-weekly-market-update-capitalisthq/

0 notes

Text

No Diss, And An Upbeat FMSR Sends Kiwi Higher!

Good day… And a Wonderful Wednesday to you! Whew! I had a much better night of sleep last night! I still don’t know what the problem was on Monday night, but I certainly was glad it did not return last night! Not much going on in the currencies or metals as I fire up my laptops, and check out what went on in the overnight markets… Another loss for my beloved Cardinals. The offense has simply dropped off a cliff, and dolt me, I stayed up to watch most of that debacle last night! The Band Yes, greets me this morning with their song: Roundabout… The Big Boss, Frank Trotter, sent me a link to an article on what the song Roundabout is all about, the last time I mentioned this song…

Well, as I said in the opening, not much going on in the currencies and metals.. Although we did have one strong move overnight from kiwi, which got a clean bill of health from the Reserve Bank of New Zealand’s (RBNZ) Financial Monetary Stability Report for May. I’m waiting for the data of the day which will come from the Eurozone, where their May CPI (consumer inflation) will print. Here’s the skinny, Eurozone CPI bumped higher in March and April (up to 1.7%) and Eurozone President, Mario Draghi, shrugged it off saying that it was “short-term” and wouldn’t continue to go higher. The experts have this May CPI report as confirmation of what Draghi was saying, and they think CPI could slip back toward the 1% level that was prevalent in the Eurozone before the last two months… So, in the end this morning, the euro will be tied to “how much CPI falls in May”… Like I said, we’re waiting for the data to print as I write…

I mentioned the RBNZ’s Financial Monetary Stability Report (FMSR) above… The report was upbeat and confirmed what I kept saying, which was that the New Zealand financial system is sound, and the risks facing the system have reduced in the past 6 months… The “risks” that the RBNZ is talking about is the Housing Bubble in Auckland. You may recall me telling you a few months ago, that the RBNZ had tightened the LVR (loan to value ratio) and that has done a lot of the heavy lifting toward reducing the risks… However, RBNZ Gov. Wheeler was quick to point out that, “As sharp reversal in risk sentiment could lead to higher funding costs for N.Z. Banks and an increase in domestic borrowing costs.” Wheeler also pointed out that “the outlook for the global economy has been improving but global political and policy uncertainty remains elevated and debt burdens are high in a number of countries”…

Thanks to my friendship with the former Gov. of the RBNZ, Don Brash, who set me up to receive Reserve Bank notices a long time ago… These notices give me RBNZ insight , which is helpful, like the info on the FMSR… I have to say that I was shocked that RBNZ Gov. Wheeler, didn’t diss kiwi in the press conference following the issuance of the FMSR! And so, with RBNZ Gov. Wheeler not dissing kiwi like he usually does, and the FMSR having an upbeat tone to it, kiwi took off and gained over 1/2-cent to a 71-cent handle this morning… Remember a couple of weeks ago, when kiwi got the stuffing knocked out of it, and fell back to a 68-cent handle? I like looking at 68-cents in the rear view mirror!

Well, the risk meter should be ratcheting higher this morning on the news overnight that a bomb exploded in Kabul near the opening of the Green Zone which houses U.S. military headquarters and embassy… I was watching Gold not reacting at all to the news of the suicide bomb explosion. So, maybe I’m making more of this information than needs to be made of…

The euro has bumped up 20 ticks from where it was when I first turned on the currency screen this morning. Maybe the CPI data has printed and I’m just not seeing it yet… I’ll keep an eye out for that!

Pound sterling got whacked again last night after another poll, this time it was the YouGov poll, which showed a further narrowing of the lead for Conservatives, and the YouGov pollsters decided to make a call afterward, saying that they believe that Conservatives could lose their majority in this election… Wait! What? OK, calm down and read on… It appears that the YouGov Poll is not a broad poll and therefore they have a wide plus- minus adjustment on their numbers… So, let’s take this report with a grain of salt and move on, eh?

In China last night, their May PMI (manufacturing index) printed better than expected at 51.2 and expectations at 51… The April PMI was also 51.2, so no gain or loss for the Chinese in May, with regards to manufacturing. The Chinese renminbi was allowed to appreciate a small bit on the PMI print outcome. Stabilizing data is important to China right now… They need all the stabilizing they can get!

Well, looky there! The euro has just jumped above the 1.12 handle, I’m still not seeing any data printing, but… Even a quick check of my Eurozone economic calendar didn’t show me what I was looking for to confirm that a better than expected CPI report is responsible for the move in the euro this morning. I did see most of the CPI reports for the individual countries of the Eurozone, and most of them were reporting better than expected CPI for May, except Germany, and with Germany being the largest economy of the Eurozone, it throws a larger than the average bear, spanner in the works, so I guess I’ll have to wait-to-see the Eurozone CPI report… In the meantime, the euro has bumped higher…

The Bank of Brazil (BOB) meets today, and will announce a rate cut… At least that’s how I see it… I see the BOB cutting their Selic Rate (internal rate) 100 Basis Points today! That would bring their Selic Rate to 10.25%, and that won’t be the last of the rate cuts from Brazil going forward… Just to prove the BOB is totally removed from any influence of politics, they will cut the Selic Rate by 100 Basis Points even though the real has been getting sold like funnel cakes at a State Fair, because of Political risks in Brazil..

Earlier this month, I said something about the former President Dilma Rousseff who was impeached earlier this year. I said that current, interim President Temer, had charges brought toward him on the news that he knew about the illegal funds that went to Rousseff… Someone close to the Brazilian news sent me this when I made that error… “Rousseff has never been charged with taking bribes. She was accused of knowing about them, but there was no evidence. Edward Cunha took bribes and now we know VP Michael Temer was also involved with the bribes. Rousseff was officially impeached for providing false data about the state of the Brazilian budget just before an election. As Wikipedia puts it “finding Rousseff guilty of breaking budget laws and removing her from office.”

There has never been a claim that she took money.”

Chuck again.. that’s what I get for getting into “politics” especially in a foreign country!

It is Month-end, and there could very well be position squaring for the month-end numbers, but with May not being a (quarter-end) the position squaring probably isn’t going to mount too much, but as I said we could very well see some today. If we see any it would probably benefit the currencies with some yield differential to the dollar…

The reason I say that is that these currencies with some yield differential to the dollar had been see the most shorting, due to the rate outlook of the U.S. (higher), which would mean a narrowing of the yield differentials, and thus potentially weaken the higher yielding currencies… But that’s just for today, folks… once we turn the page on June 1, the shorts can go back on, literally and physically! It’s unofficially, summer, the kids are out of school, so it’s time to get those sharts (as our Little Christine pronounces SHORTS) out and wear them!

The price of Oil continued to slide downward in the past 24 hours… After the OPEC meeting, Oil slipped, then recovered going into the weekend, then has gone back to slipping downward again.. not a lot of stability here, and certainly not on terra firma! The Petrol Currencies have been going back and forth alongside Oil, but at least the Norwegian krone has the euro strength on one side to keep it from getting sold too much.

The U.S. Data Cupboard got things going yesterday morning with a print of Personal Income and Spending… Once again, everyone is wishin’ and hopin’ and thinkin’ and prayin’ for Consumer Spending to pick up… And it did… Here’s the skinny… Both Personal Income and Spending grew at a 0.4% clip in April… I would like to think that this is good for the economy… But I’ll have to see more of this, because March’s report wasn’t exactly stellar, even with an upward revision! This data also has a PCE component to it. (Personal Consumption Expenditures) which is the Fed’s preferred inflation report, and this component rose 0.2% putting the year on year rise at 1.7%… Still not 2%… Still not reaching the Fed’s target… And that’s just fine with me!

The Case/Shiller Home Price Index for March was unchanged at a 5.9% increase…. And Consumer Confidence which has been running at all-time highs, saw a little slippage in May from April’s 119.4 sliding down to May’s 117.9.. Still quite high… and still no call to Chuck to see how confident he is!

Today’s Data Cupboard only has Pending Home Sales for April… That’s not exactly going to move any markets… We will get the privilege to hear what two Fed members have to say today… Robert Kaplan and John Williams will speak today, and I expect both of them to walk the straight line to a Fed Rate hike… And we could get more talk about the Great Unwind…

Gold had a down day yesterday, but the close was much better than the trading during the day, which saw the price of Gold slip by $ 11 and change at one point in the day. But Gold closed down just $ 3.80 at $ 1,262.80… The shiny metal is up a buck or two this morning, no big shakes… You know, I tell you all the time about the Gold accumulation that Russia and China continue to hoard… Well, if you do the math (don’t worry someone else has for you!) these two countries are basically taking on the entire global production of physical Gold, which leaves nothing for you and me, and jewelers and so on… An asset can only hold its current price when a scenario like this comes along, for so long… And then it historically breaks out to the top side, because of the lack of supply and the strong demand… That’s why I told some folks on the Butler Patio that I see Gold moving to $ 1,300 by summer’s end… of course I told them that was just my opinion and I could be wrong!

To recap… Not much movement from the currencies & metals so far today… The euro has bumped higher on what Chuck believes is a better than expected May CPI in the Eurozone. Kiwi has jumped to a 71-cent handle on an upbeat Financial Monetary Stability Report and no dissing of the currency by RBNZ Gov. Wheeler last night. Gold lost $ 3.80 yesterday, and is up a buck or two this morning. Chuck is somewhat inquisitive about why Gold is not reacting to the news that a suicide bomb exploded in Kabul Afghanistan? The U.S. Data Cupboard told us yesterday that Personal Income & Spending both increased by 0.4% in May, that the PCE was at 1.7% year on year, and that Consumer Confidence slipped a bit in May, but is still very high…

For What It’s Worth… You know how I keep saying the U.S. economy is going nowhere? Well, this writer from MarketWatch is pointing that out.. The article can be found here: http://www.marketwatch.com/story/the-economy-seems-frozen-in-time-but-underneath-the-ice-the-water-is-warming-2017-05-28?siteid=nwtam

Or, here’s your snippet: “A new pro-business president, record stock-market prices and the highest level of consumer confidence in years shows a lot has changed for the U.S. economy in 2017. But one thing hasn’t: Headline growth appears frozen in time.

Even a pickup in gross domestic product in the spring to 3% from 1.2% in the first quarter — helped by another strong month of employment gains in May — won’t alter the bigger picture.

Read: Economy wasn’t as bad as it looked in first quarter, GDP shows