tomblomfield

Tom Blomfield

Partner at Y Combinator.

Co-founded Monzo and GoCardless. Based in San Francisco.

25 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

apointoforder-blog

Point of Order!

dragoon11792

Chuunibyou-ish

mgxestrabaut

~My Little Sketchbook~

shakeatradefeather

ShakeATradeFeather

threecheersfortyranny

(un)believers

Text

Taking Risk

I just spent a week talking with some exceptional students from three of the UK's top universities; Cambridge, Oxford and Imperial College. Along with UCL, these British universities represent 4 of the top 10 universities in the world. The US - a country with 5x more people and 8x higher GDP - has the same number of universities in the global top 10.

On these visits, I was struck by the world-class quality of technical talent, especially in AI and biosciences. But I was also struck by something else. After their studies, most of these smart young people wanted to go and work at companies like McKinsey, Goldman Sachs or Google.

I now live in San Francisco and invest in early-stage startups at Y Combinator, and it's striking how undergraduates at top US universities start companies at more than 5x the rate of their British-educated peers. Oxford is ranked 50th in the world, while Cambridge is 61st. Imperial just makes the list at #100. I have been thinking a lot about why this is. The UK certainly doesn't lack the talent or education, and I don't think it's any longer about access to capital.

People like to talk about the role of government incentives, but San Francisco politicians certainly haven't done much to help the startup ecosystem over the last few years, while the UK government has passed a raft of supportive measures.

Instead, I think it's something more deep-rooted - in the UK, the ideas of taking risk and of brazen, commercial ambition are seen as negatives. The American dream is the belief that anyone can be successful if they are smart enough and work hard enough. Whether or not it is the reality for most Americans, Silicon Valley thrives on this optimism.

The US has a positive-sum mindset that business growth will create more wealth and prosperity and that most people overall will benefit as a result. The approach to business in the UK and Europe feels zero-sum. Our instinct is to regulate and tax the technologies that are being pioneered in California, in the misguided belief that it will give us some kind of competitive advantage.

Young people who consider starting businesses are discouraged and the vast majority of our smart, technical graduates take "safe" jobs at prestigious employers. I am trying to figure out why that is.

___

Growing up, every successful adult in my life seemed to be a banker, a lawyer or perhaps a civil engineer, like my father. I didn't know a single person who programmed computers as a job. I taught myself to code entirely from books and the internet in the late 1990s. The pinnacle of my parents' ambition for me was to go to Oxford and study law.

And so I did. While at university, the high-status thing was to work for a prestigious law firm, an investment bank or a management consultancy, and then perhaps move to Private Equity after 3 or 4 years. But while other students were getting summer internships, I launched a startup with two friends. It was an online student marketplace - a bit like eBay - for students. We tried to raise money in the UK in 2006, but found it impossible. One of my cofounders, Kulveer, had a full-time job at Deutsche Bank in London which he left to focus on the startup. His friends were incredulous - they were worried he'd become homeless. My two cofounders eventually got sick of trying to raise money in the UK and moved out to San Francisco. I was too risk-averse to join them - I quit the startup to finish my law degree and then became a management consultant - it seemed like the thing that smart, ambitious students should do. The idea that I could launch a startup instead of getting a "real" job seemed totally implausible.

But in 2011, I turned down a job at McKinsey to start a company, a payments business called GoCardless, with two more friends from university. We managed to get an offer of investment (in the US) just days before my start date at McKinsey, which finally gave me the confidence to choose the startup over a prestigious job offer. My parents were very worried and a friend of my father, who was an investment banker at the time, took me to one side to warn me that this would be the worst decision I ever made. Thirteen years later, GoCardless is worth $2.3bn.

I had a similar experience in 2016, when I was starting Monzo, I had to go through regulatory interviews before I was allowed to work as the CEO of a bank. We hired lawyers and consultants to run mock interviews - and they told me plainly that I was wasting my time. It was inconceivable that the Bank of England would authorise me, a 31 year old who'd never even worked in a bank, to act as the CEO of the UK's newest bank. (It turned out they did.) So much of the UK felt like it was pushing against me as an aspiring entrepreneur. It was like an immune system fighting against a foreign body. The reception I got in the US was dramatically different - people were overwhelmingly encouraging, supportive and helpful. For the benefit of readers who aren't from the UK, I hope it's fair to say that Monzo is now quite successful as well.

___

I don't think I was any smarter or harder working than many of the recent law graduates around me at Oxford. But I probably had an unusual attitude to risk. When we started GoCardless, we were 25 years old, had good degrees, no kids and supportive families. When fundraising was going poorly, we discussed using my parents' garage as an office. McKinsey had told me to contact them if I ever wanted a job in future. I wonder if the offer still stands.

Of course, I benefitted from immense privilege. I had a supportive family whose garage I could have used as an office. I had a good, state-funded education. I lived in a safe, democratic country with free healthcare. And I had a job offer if things didn't work out. And so the downside of the risks we were taking just didn't seem that great.

But there's a pessimism in the UK that often makes people believe they're destined to fail before they start. That it's wrong to even think about being different. Our smartest, most technical young people aspire to work for big companies with prestigious brands, rather than take a risk and start something of their own.

And I still believe the downside risk is small, especially for privileged, smart young people with a great education, a supportive family, and before they accumulate responsibilities like childcare or a mortgage. If you spend a year or two running a startup and it fails, it's not a big deal - the job at Google or McKinsey is still there at the end of it anyway. The potential upside is that you create a product that millions of people use and earn enough money that you never have to work again if you don't want to.

This view is obviously elitist - I'm aware it's not attainable for everyone. But, as a country, we should absolutely want our smartest and hardest working people building very successful companies - these companies are the engines of economic growth. They will employ thousands of people and generate billions in tax revenues. The prosperity that they create will make the entire country wealthier. We need to make our pie bigger, not fight over the economic leftovers of the US. Imagine how different the UK would feel if Google, Microsoft and Facebook were all founded here.

___

When I was talking with many of these smart students this week, many asked me how these American founders get away with all their wild claims. They seem to have limitless ambition and make outlandish claims about their goals - how can they be so sure it will pan out like that? There's always so much uncertainty, especially in scientific research. Aren't they all just bullshitters? Founders in the UK often tell me "I just want to be more realistic," and they pitch their business describing the median expected outcome, which for most startups is failure.

The difference is simple - startup founders in the US imagine the range of possible scenarios and pitch the top one percent outcome. When we were starting Monzo, I said we wanted to build a bank for a billion people around the world. That's a bold ambition, and one it's perhaps unlikely Monzo will meet. Even if we miss that goal, we've still succeeded in building a profitable bank from scratch that has almost 10 million customers.

And it turns out that this approach matches exactly what venture capitalists are looking for. It is an industry based on outlier returns, especially at the earliest stages. Perhaps 70% of investments will fail completely, and another 29% might make a modest return - 1x to 3x the capital invested. But 1% of investments will be worth 1000x what was initially paid. Those 1% of successes easily pay for all the other failures.

On the contrary, many UK investors take an extremely risk-averse view to new business - I lost count of the times that a British investor would ask for me a 3 year cash-flow forecast, and expect the company to break even within that time. UK investors spend too much time trying to mitigate downside risk with all sorts of protective provisions. US venture capital investors are more likely to ask "if this is wildly successful, how big could it be?". The downside of early-stage investing is that you lose 1x your money - it's genuinely not worth worrying much about. The upside is that you make 1000x. This is where you should focus your attention.

___

A thriving tech ecosystem is a virtuous cycle - there's a flywheel effect that takes several revolutions to get up-to-speed. Early pioneers start companies, raise a little money and employ some people. The most successful of these might get acquired or even IPO. The founders get rich and become venture capital investors. The early employees start their own companies or become angel investors. Later employees learn how to scale up these businesses and use their expertise to become the executives of the next wave of successful growth-stage startups.

Skype was a great early example of this - Niklas Zenstrom, the co-founder, launched the VC Atomico. Early employees of Skype started Transferwise or became seed investors at funds like Passion Capital, which invested in both GoCardless and Monzo. Alumni of those two companies have created more than 30 startups between them. Matt Robinson, my cofounder at GoCardless, was one of the UK's most prolific angel investors, before recently becoming a Partner at Accel, one of the top VCs in the world. Relative to 15 or 20 years ago, the UK tech ecosystem is flourishing - our flywheel is starting to accelerate. Silicon Valley has just had a 50 year head start.

There is no longer a shortage of capital for great founders in the UK (although most of the capital still comes from overseas investors). I just believe that people with the highest potential aren't choosing to launch companies, and I want that to change.

___

I don’t think the world is prepared for the tidal wave of technological change that’s about to hit over the next handful of years. Primarily because of the advances in AI, companies are being started this year that are going to transform entire industries over the next decade.

It doesn't seem hyperbolic to say that we should expect to see very significant breakthroughs in quantum computers, nuclear fusion, self-driving vehicles, space exploration and drug discovery in the next 10 or 20 years. I think we are about to enter the biggest period of transformation humanity has ever seen.

Instead of taking safe, well-paying jobs at Goldman Sachs or McKinsey, our young people should take the lead as the world is being rebuilt around us.

6 notes

·

View notes

Text

Monzo growth

I've been asked a few times recently how we got customers to sign up to Monzo in the early years and I haven't been able to give a satisfactory answer in a sufficiently short space of time. I thought I'd write out my thoughts in a longer piece so I can feel less bad about giving an incomplete answer - anyone who wants to know the details can read this instead.

Let's start with a rough timeline, which I'll then flesh out below.

2015

Started the company in February 2015.

We had a big, ambitious goal - to start a bank - and worked hard to get press coverage before publicly launching.

Ended the year with 3k "Alpha" cardholders and a waitlist of 20k.

2016

We launched an early prototype and continuously improved it.

Scarcity (waitlist) seemed to drive more signups - there was a standard "invite a friends and we'll bump you up the queue" mechanic.

A lot of hustle and hard work (100+ in-person events).

Community + Mission + Transparency - lots of blogging and social media. Crowdfunding.

Ended the year with about 70k "Beta" cardholders.

2017

Genuinely great product.

Market-leading customer service.

Hot coral card!

We consciously worked on viral product features & referral mechanics for the first time.

Ended the year with about 600k "Beta" customers.

2018

Full banking licence.

Hit 1m customers in September!

---

First, a note about the context. We started the company in the UK in February 2015, when "digital banks" weren't yet a popular idea. BankSimple had launched in 2012 with some big plans, but sold to BBVA in early 2014 with about 100,000 accounts, having struggled to raise sufficient funding to continue. N26 started development in late 2013, initially as a card for kids, while Revolut was founded a few months after Monzo, in April 2015. At around the same time, the UK regulator had announced plans to make it easier to start new banks, following the "too-big-to-fail" mess of the financial crisis, and it was on the back of this initiative that Monzo was born.

We spent the first couple of months of the company’s life furiously writing a banking licence application, believing that the licence might be granted within 12 months. In fact, it took 3 years before we were able to open full bank accounts for the bulk of our customers. Even 12 months felt slow; it had only been a handful of years since I'd gone through Y Combinator with my previous startup, GoCardless, and I was terrified of spending too much time building something without a real indication that customers wanted what we were building. Going back through my notes from the time, I found I'd peppered them with YC mantras like "Do things that don't scale", "Launch early and talk to users" and "Make something people want". So we looked for ways to get a product into users’ hands as soon as possible.

Pretty quickly we figured out that we could use prepaid debit cards as a sort of hacky prototype for a full bank. Before that point, prepaid cards had only really been used for kids' accounts (Osper and GoHenry had both been founded in 2012) and the financially excluded - people who couldn't get full bank accounts. These prepaid cards were horribly loss-making, and lacked about 60% of the functionality of a full bank account, so we budgeted for 10,000 cards. At the time, we couldn’t imagine more than 10,000 people would be willing to test out an incomplete bank account. In fact, we had almost 600,000 active prepaid cards by the time we transferred all customers to the full bank almost 3 years later. Despite the cost, these prepaid cards let us get a product into the hands of real users, who could help us figure out what product features to focus on.

---

So, about 3 months after the company was formed, we had a couple of dozen live prepaid cards linked to our backend systems and a very, very basic iOS app. We gave Eileen Burbidge, our first investor, one of the very earliest prototype cards and she was so excited about the payment push notifications that she immediately tweeted about it, which led to a Techcrunch article in May (and a reply from the N26 founder saying that it was nothing special 😆)

I don't think we were really ready for the press - we quickly scrambled to get a waitlist up on the website and launched our blog a few days later.

In any case, we got so much interest following the Techcrunch article that we doubled down on PR as a strategy. One of my notes at the time said we were aiming to get "Press at fever-pitch". Eileen seemed to know everyone in the UK press, and I worked really hard to meet journalists and explain what we were trying to build. More press followed over the next few months:

We were covered in the Guardian, The Memo, Bloomberg (complete with weird sci-fi photoshoot), Business Insider, Techcrunch again, plus a bunch more. It's important to note that we had zero real customers at this stage. Just two dozen internal test prepaid cards, a very basic iOS app and a lot of storytelling.

I spoke to Kiki recently (now the Director Of Communications at Monzo) about a conversation we had at the time. “I remember you turning up to my office when I was at the Sunday Times, signing me up with a Monzo account and telling me all about your plans to grow the business (and deep fry your Christmas turkey that year!)

You invested in forging relationships with the press and that paid dividends for you and Monzo. You were never too important to pick up the phone and explain simple stuff or go for a coffee with a journalist. Something many start-up founders don't do because they think it's all about finding angles and firing out press releases.”

PR is not a strategy that works for all early stage startups. I've been thinking a little about how it worked so well for Monzo in 2015 and 2016. Timing and context were important - the UK press was getting interested in startups (the Social Network movie honestly felt like a tipping point), but there weren't actually that many successful startups to write about in the UK in 2015. I had started another startup previously, and Eileen, our first investor, was very well known in the tech press, so I guess journalists were interested in covering us.

Probably more importantly, it seemed like we were embarking on a bold, ambitious project - to build a new bank from scratch - and we felt like underdogs in the way that the British press loves. So we got a lot of press, and I was the very visible figurehead. I'm pretty sure all that press was the reason for the hype and user signups we got by the end of 2015 - we didn't have a product live with users, nor did we really have any other meaningful marketing activity that year.

Looking back, I'm not sure how I feel about it. At the start, it was exciting to see my face in newspapers and it felt good when my friends and family told me that they'd seen me in an article or on TV. I guess I felt important, and it seemed to drive user signups. It was also a Faustian bargain. When we became a national brand name 4 years later, we were no longer the underdog - we were a big bank that the press could criticise.

I'm also not sure it was great for my relationship with my cofounders - we had 5 cofounders at the start, but it was often just my face in the picture. It was impractical to interview or photograph 5 people. They were busy working. Or at least that's what I told myself.

---

"Is it a bit early to hire a Head of Marketing?" - conversation with Eileen in June 2015, four months into the life of the company. Throughout June, July and August 2015 we were interviewing marketing candidates.

Although the hiring process was slow and frustrating, we learned a lot. We wanted to assess the paid social media ad skills of one candidate, so we had him set up and run 4 small Facebook campaigns. The first three were focussed on product benefits - "Here's a card that has no FX fees", "Turn off your overdraft", "Instant notifications". They all performed fine. But the fourth campaign outperformed the others by almost 300% - "Help us build a bank you'd be proud to call your own". This was to become a core part of our marketing over the next couple of years.

I eventually interviewed about 10 or 15 candidates, finally picking a woman who had decades of experience at a very large tech company and a UK media company. We hired her as a CMO. Looking back on my notes, all our conversations were about picking the right agency to run PR and another agency to run our paid social campaigns. She was used to running teams that were bigger than the entire headcount of the company at the time. I think she lasted less than 4 months.

At the same time, we interviewed and hired a young guy called Tristan as a community manager - he was in his early twenties, he'd graduated in Economics and spent the previous year in Egypt working with a local startup, where he'd picked up Arabic. He'd taught himself web development as a young teenager, and seemed to be extremely hands-on and impact-focussed.

Looking back, I think I would have counselled myself to think about what we wanted this person to do for the next ~12 months or so. If you hire a big-name CMO from a large, international brand, they are going to naturally assume there's a budget to spend on agencies and a marketing team. Even if they talk about being "hands-on" and "scrappy", that's probably only true relative to their previous work. For the first 12 months, what we really wanted was someone to write blog posts, respond to social media and edit the copy for our app and website. Tristan was perfect for us because he was representative of our customer base. Young, cosmopolitan lifestyle, socially conscious. He had never employed a marketing agency or really hired anyone at all, so it just didn't really occur to him to do that stuff. It was just obvious to him that he should write our Twitter posts himself.

We made another Head of Marketing hire later in 2016 who also didn't work out, and from that point onwards Tristan was put in charge of all marketing at Monzo.

---

Before talking about the launch of the product - the Alpha and then Beta programmes, I want to touch on a couple of things that didn't work.

First, we repeatedly thought about trying to pitch a TV production company to make a fly-on-the-wall documentary about Monzo in the early days. I still think that this might have been a great marketing idea to propel the brand onto a national stage (although may have made the eventual press backlash even harsher), but we just never followed through on it. Maybe it was just a vanity project!

We spent more time on a second idea - hackathons and developer relations. A lot of the early team (including me) were software developers and we were really excited about the idea of a bank account with an API. We ran 3 or 4 hackathons early on (even before we had live prepaid cards) and folks came up with a handful of interesting ideas, but we realised pretty quickly that this wasn't going to be a big growth mechanic. We only got 300 extra users, but it definitely helped hire several early engineers.

---

We finally got the "Alpha" prepaid debit card programme live to the public by November 2015 - it was a chance for people to get a card, try out the app and give us feedback to help improve the product. We capped the number of customers at 3000 because I think that was the limit for Testflight. There wasn't even a public release of the app you could download from the App Store.

What was the rationale here? The product wasn't even nearly "complete" - the list of things that were missing before you could call it a full bank account spanned several pages. Customers had to come to an event at our office to pick up the card because we hadn't yet built the functionality to collect customers’ postal addresses or post out cards. As a consequence, I met all 3000 of these users face-to-face - many of them would turn up to company events for the next 6 years and greet me with a smile.

Even though the app wasn't polished, exclusivity & scarcity was a big part of the strategy early on (drawing on early Gmail launch tactics). I read somewhere that human brains are basically wired to seek out scarce resources and perceive them as more valuable than those that are abundant. Being "in the know" - the first amongst your peers to get access to some new product or service - is a badge of honour amongst early adopters, and we harnessed that. Even the physical cards had "Alpha" printed on them - people would brag years later how early they'd signed up to Monzo. For these people, finding a bug wasn't an annoyance - it was proof that they were experiencing something at the bleeding edge of development, and they were excited to help improve the product. So we ran with that.

This is the first archived version of our website I can find - "We’ve only got 3000 invites for our Alpha Preview. Sign up now to be in with a chance"

It turns out this strategy also works on tech journalists. The early preview accounts we gave to Techcrunch and Business Insider journalists led to great coverage.

This strategy also let us organise events at a number of London's top companies. We would promise to come along with 50 or 100 Monzo cards, give a 20 minute presentation during the lunch break, and enable attendees to skip the waiting list. This proved irresistible - I got into companies like Transferwise, McKinsey and the BBC. Much like the hackathons, it didn’t actually turn out to be a very effective way to sign up users, but it was an incredibly strong recruiting strategy. We'd get a flood of inbound CVs a week or two after each talk.

Looking back, it’s quite surprising how many major pieces of functionality were missing from the app. You couldn’t make bank transfers or pay bills, for example, because we didn’t yet have access to the payments infrastructure we needed. Instead, we obsessed over the tiny details that we could control - accurate merchant logos that represented your spending, rather than the cryptic data you normally find on bank statements. Jonas (one of our cofounders) first came up with the idea to add emojis to the push notification customers received to alert them about spending. Plane tickets might show 🛫, while spend at a coffee shop would show ☕. I have so many notes from that first year about improving the logos - I even wrote some of the early code to put the right emojis onto transactions. We really cared about making it a delightful experience.

Even before we'd opened up the product to the full waitlist, we decided to run a £1m crowdfunding campaign early in 2016. Again, we ran the "scarcity" and "exclusivity" playbooks. We anticipated the round would sell out, so we set up a pre-registration system so that our customers could invest before the general public, and we capped individual investment at £1000 to maximise the number of people who could invest. Along with owning shares in the company, investors would get "Investor" printed on their debit card (and this is still honoured to this day). Investors would also be able to skip the main queue and get access to a Monzo card if they didn't already have one.

The campaign turned out to be a huge PR coup, but mainly for reasons we had not anticipated. Approaching the launch date, we told our crowdfunding partner to expect larger than normal volumes of people looking to invest, as we already had 6500 pre registrations. For whatever reason, they did not take this warning very seriously, and their servers buckled under the load just seconds after the round opened on Monday. This was very annoying and stressful at the time, especially since 6500 simultaneous visitors is not a huge amount of load. We quickly decided we'd rebuild the investment registration page ourselves, and planned to relaunch the campaign a few days later.

While our engineers rebuilt the site, we thought about how to communicate this to the press and our customers. It was an absolute gift of a PR story - we had so much demand to invest that the crowdfunding site had crashed. This story ran continually over the next couple of days. By Thursday, the campaign relaunched and sold out in 96 seconds, making it the fastest crowdfunding in history, and the press attention was intense.

We ultimately raised £1m from 1861 investors, out of the 6500 people who had pre-registered. In comparison, we only had 3000 cardholders who up to that point had only spent £1m in total on our cards. I'm not sure how repeatable this lesson is - lots of companies have tried crowdfunding since, and it's no longer newsworthy. I think we had an incredible amount of hype at the time, and we played the scarcity/exclusivity angles well. It also helped that we already had 45,000 customers on a waitlist, and £5m investment committed from Passion Capital - this was an extra £1m investment that normal people could get access to on the same terms as a VC.

---

Soon after the crowdfunding completed, we announced a public Beta in March 2016, the Alpha having capped out at 3000 users (the Testflight limit). This was 13 months after the company was founded.

Anyone (as long as they were an iOS user) could download the Monzo app and see their place in the queue. People could improve their place in the queue by inviting friends to join and a certain number of people at the top of the queue every week would have a card sent out. In the spirit of “doing things that don’t scale”, we figured out a basic system for collecting addresses in the app and posting cards directly from our office. When we had a particularly big week of signups, the whole team would have to stop their regular work to help stuff all the prepaid cards into envelopes to catch the last post. I vividly remember stuffing envelopes at the time, thinking “each of these cards is another person who wants to use our product”. It really felt like customers were signing up faster than we could ship out cards - one of the first indications that we had “product-market fit”. It seemed like we were on the verge of something huge.

I think there are a couple of interesting things worth mentioning in 2016 - both related to company values. The first is our name-change. We had been threatened with a trademark lawsuit from a German fintech company which had a similar brand name (we were "Mondo" at the time) and considerably more funding than us. I fought this for several months (against the counsel of my board and investors), before accepting we had to change our name. To make the most of a bad situation, we decided we'd ask our community members - our customers - to suggest new names. The only constraint was that it had to begin with "M" because we had recently designed a great new logo that we didn't want to give up. Incredibly, bearing in mind we only had around 20,000 customers at the time, we received 12,000 suggestions in about two weeks. 6 people suggested the name we chose - Matt from Bristol had studied a rock called "Monzonite" and another customer, Ashley, told us it was slang for money when he was a kid in Scotland. We hosted a big party and live-streamed the announcement of the new name - Monzo.

Predictably, our power-users overwhelmingly hated it, suggesting it sounded too much like "gonzo" (a form of first-person journalism and, later, pornography). It took a little while to stick, but I like it - it sounds much more dynamic and active than "Mondo", which now feels quite staid to me.

The second was our transparent Product Roadmap. In a world where the big banks had huge head offices and enormous marketing budgets, but very little personal trust, we wanted to come across as different. Where big banks were faceless and corporate, we would be human and personal. Where they were impenetrable and secretive, we would be transparent and approachable. So, in May 2016, we announced we'd publish the plans for our product, and take input from our community. In other situations, when things went wrong, we'd proactively tell our users about it and explain what we were doing to fix the situation. Invariably, this transparency generated more customer goodwill and positive PR.

These two core values - Community and Transparency - permeated almost everything we did throughout the life of the company. They became a fundamental part of our brand. Prior to Monzo, I didn’t really believe in the concept of “brand” - I thought it was a made-up thing that marketing agencies tried to sell you. And that “brand” didn’t really extend beyond a company’s name and logo. I now believe it can be a superpower for any company - and particularly consumer-facing businesses.

There’s been good stuff written about brand-building elsewhere, so I won’t try to recreate it all - I’ll offer just a handful of thoughts. A great brand is like a promise you make to your customers. It’s a shared set of beliefs, or the “why” behind the company. Building your brand is not a one-off thing; you build (or damage) your brand with every decision you make. Events like crowdfunding and the company rename were perfect examples to reinforce the brand. It has to be authentic - a lot of big banks’ marketing towards younger customers felt really painful. Monzo, in contrast, felt human and relatable.

And when a brand really resonates with a customer, it becomes an extension of their identity. I wear Patagonia. I drive a Tesla. I use an iPhone. I bank with Monzo. I think a lot of customers were proud to pull out their Monzo card and feel like they were part of something.

In the UK, at least, Monzo has become a verb.

---

We grew from about 3,000 users at the start of 2016 to 70,000 by year-end, which seemed pretty good, but I think we realised in the summer of 2016 that our strategies so far weren't going to scale to drive the kind of continued growth we ultimately needed. So, towards the end of the year we really started to think about product features with network effects, and referral mechanics. Pretty quickly, this became "Monzo with Friends" - we aimed to build a product that worked better and better as more of your friends joined. We started working on ideas, but nothing really launched until early 2017, so I'll talk about this more in the next section.

Before that though, here are two things that failed in 2016. First was the idea of "Campus Insiders" - university students that we employed to represent the Monzo brand and sign up new customers. They required a lot of babysitting and delivered no measurable impact, as far as I can tell. One of our early ideas was to have a custom Monzo card for each university - similar to how we had "Alpha" and "Beta" subtly printed on the corner of the card. Students might get Monzo "Oxford" or Monzo "Birmingham" if they signed up with a student email address. This could have maybe extended into discounts at local shops, but it seemed like too much work and we never followed through with it.

The second was a campaign to work with local businesses in the Old Street area of London in the run up to Christmas. I think we had folks out flyering and offering discounts in local shops, but again it was a lot of manual work with no discernible impact.

---

2017 was the year of product-driven growth. We had a slide in several of our early investor presentations that said "Viral mechanics will get us to the first million customers", but investors overwhelmingly didn't believe it. We set out to prove them wrong.

I'll make a distinction between two related ideas - viral mechanics and network effects. A "viral mechanic" normally uses the existing customer base to spread the product to friends. It’s sometimes called "member-get-member", and it can be incentivised or free. An example is the way Wordle allowed you to post your "score" to social media. Other people see it and sign up for Wordle themselves. The game isn't really improved in any way by having your friends join - they're just curious to check it out. Gmail used a viral waitlist + invitation mechanic in the early days - again, your experience of Gmail wasn't really improved if you convinced your friends to switch from Outlook.

A network effect is different - the product itself actually improves as more of your network joins. Whatsapp and Skype are great examples. The more of your friends who join, the more people you can communicate with for free. That was a big hook at a time when people paid for SMS and international phone calls.

Great products have both network effects and viral mechanics. Facebook's early photo tagging is an example. "You've been tagged in a photo" email - prompts you to sign up for Facebook, see the photos you're in, upload your own photos, tag more friends, repeat. The network gets more valuable and drives more growth as more users join.

At Monzo we had both of these, and 2017 was the year they really took off.

I'll talk about "Golden Tickets" first - a silly allusion to the Willy Wonka story. We had a pretty big waiting list at this point, but the "Invite friends to get bumped up the queue" felt a little old and ineffective. People who wanted an account enough would just create a bunch of throwaway email addresses. We figured that the best people to be making referrals were those who were already actively using the product. Presumably they liked it enough because they kept using it, and they'd all had the experience of having to wait in the queue, so they perceived a Monzo account to be both scarce and valuable.

Rather than paying our users to refer friends like most apps did, we decided that once you'd used the account for about two weeks, we'd send you a single "Golden Ticket". This was a one-time-use invitation that you could send to one friend to enable them to skip the queue entirely and get a Monzo account straight away. You can think about the psychology by analogy - you've queued all afternoon to attend a cool new event in your city, you’ve just managed to get in the door, and you've been able to talk the bouncer into getting your friend a queue-jump ticket. You get the early-adopter social credibility of having known about the event before your friends, plus you’ve done your friend a favour by getting them access. It just worked incredibly well - about 40% of our signups in 2017 came from Golden Tickets, and it cost us nothing.

Second, "Monzo with friends" was our drive to make Monzo work better if you invited your friends to use it. This might sound obvious now, but I can't really think of any other bank that had previously done this, beyond suggesting you get a joint account with your spouse. If you used Barclays and your friends used Natwest, there was no change in how useful the account was, right? We wanted to change that.

We started with peer-to-peer payments, based on the contact-list of your mobile phone. For US audiences, this was Venmo, but inside your bank account. UK banks already allowed you to pay any other UK account holder instantly, for free, but you needed to know their account number and sort-code, and the interface was really clunky. It basically worked, but it wasn't a delightful experience. We asked people to share their phone contact lists (using some clever encryption so that we'd never actually saw your friends' mobile phone numbers), and then allowed you to pay your friends on Monzo with just a couple of taps. For contacts who weren't on Monzo, that's where Golden Tickets came in! It was a really slick interface, and we allowed you to include longer-than-normal messages with the payment, including emoji. Later that year, we added "Reactions" - if you'd received money from a friend, you could send a quick response - just a single emoji. This was just a quick way of saying "thanks, payment received". And we let people quickly upload profile pictures to make it feel more personal.

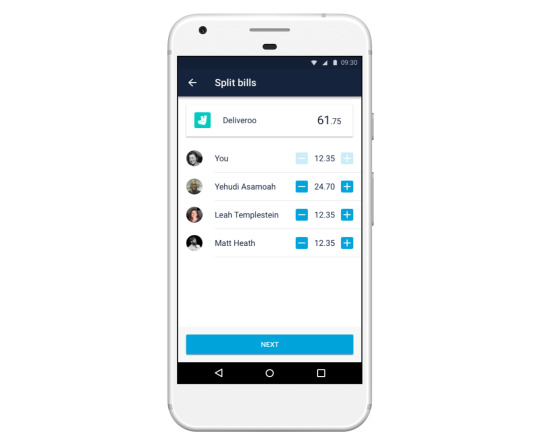

We then added "Split the bill" functionality for a single payment, plus a more general "Request money" feature, and finally more complex "Shared Tabs" for multi-day trips away with friends and family that might include dividing several payments. If your friends weren't on Monzo, you could still request money with your personal Monzo.me link, which would allow folks to pay you using another bank card or Apple/Google Pay (and Monzo covered the transaction fees), and included a little upsell for Monzo at the end. Mine is https://monzo.me/tomblomfield. If you clicked on this link with a Monzo app installed, it would just deep-link straight into the Monzo account with all the payment information pre-populated.

Alternatively, if you went for dinner or drinks and wanted to split a bill with someone who already had Monzo, but who wasn’t in your phone’s contact list, you could securely broadcast your account details by bluetooth, so you could pay each other without having to type in any account information. It's an incredibly slick experience that I am proud of to this day.

Peer-to-peer payments drove massive adoption - time and time again we saw Monzo take hold in a new group of friends and then quickly spread to the entire group. At the start of 2017, only 5% of our users had 10 or more friends on Monzo. By the end of 2017, more than 40% of our users had 10+ friends on Monzo. Today, the average Monzo user has more than 100 friends on Monzo. This is network effect in full force.

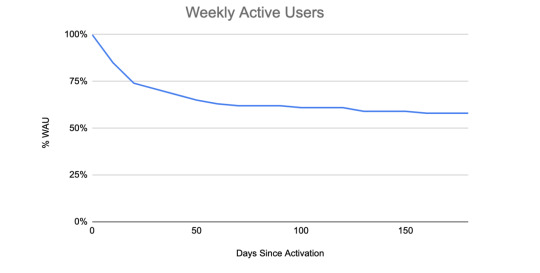

2017 was also the year that we really got a handle on our metrics - particularly retention. There are much more complete retention guides out there, but I'll give a quick summary here. Say 100 users sign up for Monzo, complete KYC, register a card and load money into the account. That's the denominator - 100 funded accounts. Fast forward say three months - how many are still using the account? Maybe 60? That's the numerator. So we have 60% (60/100) retention at Month 3 (or day 90). You can draw a curve to show how quickly retention falls off day by day since signup.

What does "still using the account" actually mean? We decided to count "at least one financial transaction in the 7 days" would make you a Weekly Active User (WAU). "At least one financial transaction in the preceding 30 days" would make you a Monthly Active User (MAU). Clearly, a WAU was more engaged than a MAU. I dug out our stats for 2017 - about 60% of our signups were WAU on day 90.

These retention rates still strike me as surprisingly high, especially considering that every user had to proactively add money to the account every time they ran low on funds. This wasn't (yet) a bank account where you sort of "defaulted" into retention once a customer set up the account - users could not deposit their salary into the account until 2018, and there was no auto-top up functionality.

Monzo started 2017 on 70k users and ended the year on around 650k - averaging just under 5% compounding weekly growth for 52 weeks of the year.

So why did it grow organically and retain so well? First of all, I think the day-to-day product experience (for all its functional limitations) was world-class - it was a delight to use, especially compared to the clunky old banking apps in the market. Without that, basically nothing else would have mattered. The customer service was also exceptional - this was often mentioned in our NPS surveys (NPS was around +70 at the time).

Secondly, I think the brand we had started to build really resonated with people. Our mission and values (mainly transparency and community) seemed to strike a chord with customers. Even the card itself was visibly different to traditional banks. The Monzo card was "hot coral" (aka bright pink) - the colour alone often started a conversation when customers pulled it out of their wallets to pay. Our tone of voice was youthful, direct and extremely personal. By 2019, Monzo was the single most recommended brand in the UK.

And third, the network effect really started to kick in - if you had 3+ friends on Monzo when you joined, you had a 70% chance of being a WAU by day 90, versus only a 50% chance if you didn't have any friends on the platform.

As a result of these things, Monzo hit 1 million customers in September 2018, without having spent any significant money on marketing.

---

This feels like a good place to draw this chapter of a story to a close. There are other topics I’d like to write about - getting a full UK banking licence, fixing unit economics, and spending money on paid advertising to catapult the bank from 1m to 4m customers - but they will have to wait for another time.

7 notes

·

View notes

Text

How to raise investment

Update: I am no longer personally angel investing - I'm focussed on other things at the moment. Please don't ask me to invest in your company! 🙂

I started angel-investing in 2021, and a large proportion of the companies I put money into asked for help raising an investment round. So I wrote up my standard advice as a guide here.

This guide is based on my experience raising about $400m at Monzo over the last 6 years and investing in about 75 seed deals as an angel in 2021.

It will be most relevant for founders who are raising a Seed or Series A round, with some amount of product development and early customer traction.

I believe the following advice is mostly correct as of September 2021. The market is changing so quickly that it may not stay correct for long. I plan to update it periodically.

General Approach

First, a couple of warnings.

If you build a strong business, fundraising will normally be easy. If you're too focussed on fundraising, you may never actually build a strong business.

It's very easy to get sucked into the competition of raising at the highest valuation of all your peers. This may feel like winning, but it is not. Seed-stage valuations don’t correlate well with success. Success to me means building a sustainable, profitable company that makes something people love. Investment is just a tool to help you do this.

Airbnb raised its first round out of YC at a $1.8m valuation. They've done pretty well. An extra 3-5% dilution isn't going to matter if you build a very successful company.

Conventional wisdom says you should aim to raise enough money to fund your business for the next 18 to 24 months, or until you hit a major milestone that's going to create a step-change in the valuation of the business. If that next milestone is "reaching breakeven", you will have a dramatically easier time fundraising in future - you can decide whether to raise more to grow faster, or run the business for profit. You have all the power.

I have always spent approximately double what I've forecast (oops), so I'd advise doubling whatever you estimate.

Fundraising is extremely distracting. If you have multiple founders, nominate one to run the fundraising process. He or she should be the primary point of contact for investors. VCs may want to meet all the founders once or twice, but all founders don't need to be in every meeting. As an angel investor now, it’s normally a red flag if there are 2 or more founders on the initial phone call. It typically makes the conversation more awkward as the founders talk over each other, or one person sits silently in the background.

If you have a CEO, this is the obvious person to run the fundraising. If you don't have a CEO, you're in for a potentially awkward discussion about who runs fundraising. This is one of many reasons I recommend deciding on a CEO earlier rather than later. We did not do this at GoCardless and it was painful.

Fundraising will become all-consuming, so you need to ensure your day to day job is covered by others for the duration of the process. If you are responsible for sales, for example, expect sales to dramatically slow during fundraising unless someone else covers it.

The VC Business Model

Before diving into the details of fundraising, it’s worth briefly understanding how the venture capital model works.

VC returns are extremely skewed by a tiny number of outsized successes. a16z's shareholding in Coinbase at IPO was worth about $10bn - roughly equivalent to all the funds a16z raised during their first 10 years of existence. Passion Capital's Monzo shareholding is worth about 5x the size of all their raised funds combined. The initial investment in Monzo has currently increased in value by approximately 100x, even after dilution - and I believe that will continue to increase (I may be biased).

VC returns are driven by outlier companies.

So VC investment decision-making is driven by fairly straightforward psychology. It's the fear of missing out on one of these apparently "hot" deals. This can then create a very aggressive bidding war. A hot round may get done in a handful of days.

Conversely, a VC doesn't really want to look stupid in front of all their buddies by investing in a crazy idea that comes to nothing. However, economically, it's much better for a VC to invest in a few extra "duds" than to risk missing out on the single hot deal of the year.

There's a second factor here - a massive global over-supply of capital. Recently, late-stage investing has been dramatically shaken up by investors like Softbank and Tiger Global deploying astonishing amounts of money into growth-stage companies in just a handful of days. Traditional growth stage investors are finding that they're too slow, or being consistently outbid on price. Their response has been to invest more money, faster, and into earlier-stage companies. This then squeezes the Series A investors who are now doing more and more seed deals.

The combination of these factors has lead to a massive rise in "pre-emptive" termsheets. VCs will try to offer termsheets to founders before they've had the chance to talk to a wide range of VCs in the market, with the aim of avoiding an expensive bidding war. Predictably, this just further increases valuations.

Raising with just an idea

This is this biggest mistake I see first-time founders make. Especially non-technical founders without a very strong CV. Trying to raise money from VCs with just an idea and a pitch deck is extraordinarily difficult unless you've successfully started a company in the past (or maybe been an early employee at a successful startup).

Instead, you should spend your time developing a prototype of your product and testing it out with customers. If you can't build it yourself, you should learn to code or recruit a technical cofounder. If you can't successfully do either these, you're probably not going to persuade investors to give you money yet. You could think about applying to an incubator like Entrepreneur First.

As an investor, it's basically the first filter I apply to exclude people who can't get stuff done. Of 50 investments I've made this year, 45 had a working product and active customers. Of the remaining 5, 3 had a working prototype and launched to customers within weeks of my investment. Only two raised on the strength of the founders and the idea alone - and in each case the founders had previously started businesses worth more than $100m.

Even the most minimal prototype and customer usage is better than nothing. I'll write a separate guide to building and launching a prototype at some point in the next few months.

So, as well as a great idea and impressive founders, you ideally need....

Traction

Traction is a phrase that investors seem to love. It reminds me of a medieval torture device, but perhaps that's because I have spent too much of the last 10 years fundraising.

You want to show investors some early metrics that can be extrapolated to show that you're going to build a very big business very quickly. This is "traction".

The best kind of metric is profit. This is very uncommon for early stage startups. The next best kind of metric is revenue - especially recurring revenue (if it's recurring, you don't have to keep acquiring users to simply maintain stable revenue levels). If you can't show revenue, try to show active users plus a coherent plan of how you're going to make revenue in the future. Total signups, app downloads or waiting-list signups are the next best metrics in order, but they're much less compelling than revenue or active users. Waiting list signups are widely ignored unless they're absolutely explosive. Monzo had a peak waiting list of about 300,000 people in the UK.

Letters of Intent for B2B companies are a bit like waiting list signups. Mostly useless.

The absolute value of your metrics is less important than the rate of growth. Hitting £100k monthly revenue after three years is much less impressive than £10k monthly revenue that's doubling every month.

"A good growth rate [at seed stage] is 5-7% a week. If you can hit 10% a week you're doing exceptionally well. If you can only manage 1%, it's a sign you haven't yet figured out what you're doing."

Tactics

With this in mind, you want to think about how to create a sense of scarcity and urgency about your round. You should aim to appear to be the hot deal of the year.

I would start by developing close relationships with perhaps 5 of your top target VCs. You might meet them for coffee every 2-3 months and share your plans, but say "We're not raising yet - maybe in 6 months". Share awesome product demos, social media buzz and impressive new customers. You can include them in your monthly shareholder update emails, and (hopefully) show metrics going up month after month, along with any major milestones you’ve hit. This is evidence of your "traction". I find this much more compelling than a polished pitch deck.

If you already have angel investors, use them to backchannel into VCs. They'll say "this is going to be an exceptionally hot round, you need to get in before they run a full process."

You want to project quiet confidence, huge ambition and relentless determination. UK founders often come across as extremely understated when compared to US counterparts. The front page of Monzo's first pitch deck said "We're building a powerful financial control centre for a billion people around the world".

You will know if you have succeeded in creating this buzz because you will have 5 new best friends. You’ll get phone calls every day and they will reply to your emails in seconds. I have had VCs show up at my house to try to get into deals. They’ll take you to fancy restaurants and buy you drinks.

Some of these VCs might try to “pre-empt” your round by offering you a termsheet before other VCs have had a chance to learn about your business. In general, companies that run a process with multiple competing VCs tend to get better terms than companies that accept a pre-emptive termsheet. But you may still consider accepting the pre-emptive offer if it is ridiculously good. I have done both in the past.

Running a Process

As you’re raising a seed round or Series A, this process can be pretty lightweight. As you get into Series B and onwards, it may get more complicated.

First, start with a list of perhaps 8-10 relevant VCs. These should be funds who you know will invest in your industry, geography and company stage. It’s pointless pitching a sovereign wealth fund for a seed stage investment, or a B2B SaaS fund if you’re a consumer-focused company. This is one of the most common mistakes I see new founders making. You’re wasting your time.

Pre-seed and Seed investors tend to focus on one geography, while later-stage investors are often more global. Having said that, funds are investing earlier and more globally than ever before. I’ve seen Index and Sequoia recently making a bunch of seed-stage investments in Africa, for example. This would not have happened even 3 years ago.

Next, put together a deck. YC has a great Series A pitch deck guide here. I think that advice still applies for seed rounds.

I would practice your pitch on 2-3 friendlier (or lower value) VCs first and ask for their feedback. Make a note of the common questions they ask, and make sure you have good answers to these. If you want to tweak your deck, do it now. This should take 2-3 days max.

Then, without too much delay, get introduced to the remaining VCs on your list. This is where early angel investors can be extremely useful. You want to avoid cold emails if at all possible.

Your aim is to schedule as many of your first meetings in parallel - perhaps the same week or two-week period. This creates a competitive dynamic that works in your favour.

If your round is dragging out over several months, you'll lose this advantage. It's still entirely possible to get the round done, but it will be harder work and your valuation will be lower. Probably 30% of the rounds I’ve raised have been “hot” - and very fast. 70% have been hard work, slow and stressful. This latter kind is normal. But we generally only read about the hot rounds in the press, so popular opinion is skewed towards thinking most companies raise money in 1 or 2 weeks.

Initial Call / Pitch Meetings

You generally want to be pitching the most relevant General Partner at the fund. That’s the most senior partner who covers your area. Larger funds will have pretty rigid specialisations, so a certain person does all the fintech deals. That’s fine - just figure out who that is.

Associates, analysts, “venture partners”, or EIRs (entrepreneurs in residence) will almost always carry less weight. Try to get introduced to a full partner if possible. Some funds have tried to combat this tactic by calling almost everyone a “partner”

It can be useful to build relationships with associates before raising, especially if you can’t get to a partner directly. Our first VC investment at GoCardless happened because I was introduced to an associate at Accel called Tyler several months earlier.

Since the Covid pandemic, almost all initial meetings are conducted on video conference. I would recommend that everyone spends ~$200 on an external camera, mic and lighting. Make sure you have somewhere quiet to take the call and a good internet connection. It makes a massive difference and it's surprising how many founder neglect this.

The best pitches start with an element of story-telling (perhaps 2-3 minutes) and then develop into a great conversation. If you are delivering a monologue for 30 minutes, you’re doing it wrong. Engage the investor in the conversation by asking them questions - how would they think about a potential challenge you’re facing, for example. Try to figure out what gets them excited, and double down on that. Don’t feel like you need to cover your whole pitch-deck in the intro meeting.

Follow-Ups and Monday Partner Meetings

If your meeting goes well, the investor will ask you follow-up questions (perhaps for some additional data) and may ask to meet you again, or have you meet with another (or several) of their partners. These are all good signs, and will usually happen rapidly.

If the investor doesn’t get back to you pretty quickly (within a couple of days), it’s normally a bad sign. You can send one polite follow-up email, but it’s usually pointless after that. If you’ve not heard from the investor in weeks, I wouldn’t bother chasing. They’re a) not interested (fine) and b) disrespectful of your time (not fine). The best investors always reply promptly (whether it's positive or negative).

Conversely, you should make sure to reply promptly to any follow-up requests they have. If you promise to send something by a certain day/time, make sure it happens. It’s the investor’s first impression of how you do business. Keep all your contacts in a spreadsheet (or lightweight CRM) and track what you've promised to each investor and by when.

Investment rounds are getting done faster and faster - it may only take a couple of partner meetings over a handful of days to get a termsheet for a seed round.

How you get to a “yes” decision - an offer to invest - varies from fund to fund.

Some funds will let any single partner make an investment if they have conviction. For solo-GP funds this is always the case!

Other funds will require a majority vote or (near) unanimous consent from amongst the partner group. This is quite common.

The worst funds have a strict hierarchy - the deal won’t get done unless the top guy (sadly it is almost always a man) says “yes”. I’d avoid working with these funds if you have a choice.

The fund may ask you to present to their whole partnership at a Monday Partner meeting. I have no idea why these are always on Mondays. I’ve done one of these Monday Partner meetings perhaps 4 times ever in my life, and I’ve raised probably 10 rounds of investment across various companies. It feels like they’re getting rarer.

If you get a “no” from the investor, it can be emotionally tough. But I’m afraid that’s part of the process. A normal company might get 20 “no” responses before they get a “yes”.

Unfortunately, many investors will send quite a lot of bullshit reasons for a “no”, rather than reveal their true rationale - which is normally that you did not sufficiently impress them, or your traction is too far behind comparable peers. Unless you really trust and respect the VC, take the “no” part onboard and discard the rest. I found Michael Abramson at Sequoia and Angela Strange at a16z both exceptional for writing really thoughtful rejection emails.

If you've been fundraising for 3-6 months and you’ve had 30-40 “no”s from decent VCs, then you’re in a tough spot. What you are doing isn’t working, and so you probably need to change your approach. There’s a point past which perseverance becomes destructive.

At this point, you need to become a cockroach - impossible to kill. Reduce costs, seek out revenue and keep burn to an absolute minimum. At this stage, it’s worth looking for the 1-2 common rejection themes from the VCs and working to fix them. For early-stage companies, this is generally that you don’t have enough traction with customers - people don’t seem to care about what you’re building. You need to find product-market fit, possibly by changing your core product. This is a subject that deserves more time in another post.

Termsheets and Legals

If a VC wants to invest in your company, they'll issue a termsheet to be the lead investor.

It will contain the main terms of the investment - pre-money valuation, investment amount, board seat, and perhaps 2-3 other key terms. You should have talked about the approximate amount you're looking to raise before a VC issues a termsheet, but I would suggest letting the lead VC suggest the price first.

The exception might be an ultra-early pre-emptive offer, when you really don't need the money yet. You might say "we don't need money for the next 12-18 months, and at that point we will be targeting a £1bn valuation, because we will have hit all these milestones. So for me to accept money now, that's the valuation I'd be looking for. Otherwise, it makes sense for me to wait". In this case, just think of the most outrageous price you can say with a straight face.

The termsheet will often leave room to bring in additional investors. Eg, the VC might offer to invest £1m in a round of up to £1.5m total, at a pre-money valuation of £4.5m. You can work with the lead VC to bring in other angels or VCs for the remaining £500k.

A termsheet is not binding on the VC (they can still technically back out), but prohibits you from soliciting investment from other VCs after you've signed it, usually for a period of 30 or 45 days.

Personally, I have only experienced investors reneging on signed termsheets once - as COVID took the world into lockdown. It's very, very rare for a top-quality VC to pull a termsheet. Shitty VCs may pull termsheets more often, but they quickly develop a bad reputation for doing so.

You will usually be given a few days or perhaps a week to sign the termsheet, or decline it. It is considered bad form to share the contents of a termsheet with other investors, but it is pretty standard practice to let any other firms in the running know that you've received a termsheet. Doing this with some level of deniability (eg, get an angel to do it for you) is sometimes useful. This will spur other VCs to make a faster decision, and potentially trigger a bidding process. It's a very useful forcing function.

You do not want to be seen "shopping around" your unsigned termsheet, but you can say something like:

There are two other interested firms, and they've already put in a lot of work with us, so I want to respect that work and give them a chance to get to the end of their process. They'll need another 5 days. Is that ok?

This is why it's important to keep a small number of VCs regularly updated. If you get a very early pre-emptive termsheet, other firms may be too far behind to get up to speed in 5 days from a standing start. This is less of a problem at seed stage - since it's more of a gut judgement about the quality of the founders, rather than any detailed analysis of business metrics, it can be done in a few hours.

You generally want to avoid naming the other VCs who are in the running, because it can encourage collusion. The VCs may just get on the phone to each other and agree to split the round at the already-agreed price. Instead, you ideally want them bidding each other up.

Only bad VCs will ask who else is looking at the deal, and you can just reply with something like “the usual folks you’d expect at this stage”. If they insist, you can simply refuse to answer. Treat this as a big red flag.

Picking a VC

If you’re in the fortunate position of having multiple, competing termsheets, you need to think about how to pick.

Along with the money, you should pay attention to the individual leading the investment from the VC firm. Arguably, choosing the right person is more important than the choice of the VC firm itself. You will be spending a lot of time with this person over the next 5-10 years, and it's almost impossible to get rid of them if you don't get on.

A fair valuation with clean terms and a VC you like is much better than a market-leading valuation with horrible terms, or a VC who behaves badly.

The first data point is the way the investor has behaved during the pitch process (and previous interactions). Did they show up on time? Did they follow-up promptly? Were they inquisitive and courteous during your pitches, or distracted and disrespectful?

I've worked with some fabulous investors over the years - Eileen and her partners at Passion, Anu at Y Combinator, Sonali at Accel, Adam Valkin at General Catalyst, Ed (now at Alpine) and Chi-Hua at Goodwater, Miles at Thrive (now Benchmark), Michael Moritz, the Stripe team and many more. I recommend them all to the entrepreneurs I speak to.

I've honestly also encountered some shitty ones. There are VCs who've verbally offered me terms and then tried to back out weeks later. I won't ever work with these folks again.

One particular example of bad behaviour that I will name is Softbank (at least the London team). Like most growth-stage founders, I've pitched them for investment multiple times. They passed - no hard feelings. But it seemed like standard practice during my visits to the London office to make me wait in the lobby, often for an hour or more after the meeting was supposed to start. I heard of one founder who'd flown in from another country and was made to wait for the entire day in their lobby.

Their behaviour during pitches was worse. The lead partner took meetings barefoot, and would pick his feet incessantly. During one meeting, he lit a cigarette and smoked it in his office, windows closed. He finally put it down in his lunch plate, and poured his coffee over the cigarette to extinguish it. I didn't know if it was some weird power play, or if he just lacked any kind of manners. Looking back, I wish I had the guts to ask him to stop, or to simply get up and walk out of his office. But my company really needed the investment and I didn't want to blow my chance.

Blind reference calls are also crucial here. The founder calls that the VC offers are less likely to give you a fully rounded view of the firm. They’ll pick their winners. But, especially for portfolio companies that have failed or are doing poorly, you want to know how the VC behaved. It's easy for everyone to be founder-friendly when times are good. During a crisis, behaviours sometimes diverge....

Example questions for founders:

Tell me about a time when you were really struggling to raise money to keep the company going.

Did the VC offer to participate in the round? Or even lead the round if you couldn't find new money? Were they helpful finding new investors? Did they push for a valuation cut, or attempt to introduce onerous terms? Have they tried to sell or transfer their stake in the company before you were ready? What was their language and behaviour during the tough period? Did they roll their sleeves up and help out, or did they ghost you?

What's their behaviour during board meetings? Do they add useful insight, or just like the sound of their own voice?

What are their regular information requirements? Do they bombard your finance team with constant ad-hoc queries?

Have they ever gone above-and-beyond what you expected to put in work for the company? (I had an investor who interviewed a bunch of ex-execs from all our competitors to gather intelligence)

If you don't have the good fortune to have multiple, competing termsheets, I think it's still worth doing the reference calls - you need to know what you're about to get into.

It's really tempting to skip the reference calls and just celebrate your termsheet. Don't do this.

Legals and Diligence

Once you sign a termsheet, the lead VC will do some basic “due diligence” (this will be less onerous in seed/series A compared to later rounds). This will involve reference calls to previous employers or colleagues, and checking your company documents, employment contracts, IP assignments etc. Any other (non-lead) investors should be able to piggy-back on the lead investor's diligence, rather than doing their own.

It's worth getting your corporate paperwork in order & up-to-date in a single Google Drive folder before you start fundraising, so that you can share with investors when they ask. This speeds things up a lot.

You'll need to appoint a lawyer - you can ask other founders or angels for recommendations. Your prospective investors will often ask you to cover their legal costs (the money just gets subtracted from the investment amount). This is annoying, but seems to be standard practice. For Seed or Series A, maybe try to keep it to $15,000-$25,000.

The VC's lawyers will put together an Investment Agreement, and modify your Company's Articles of Association (or create them from scratch if they don't exist). Your lawyers will review the documents, and raise any points with you that they think are contentious or non-standard. Good VCs will make this process very simple. Shitty VCs will try to sneak in all sorts of garbage.

One term that sometimes gets left until late in the process is the option pool top-up. Ideally, this should be covered in the termsheet. It's standard for investors to require the unallocated option pool to be topped up to a level that will equal 10% (sometimes less) of the post-investment shares, but for this to happen immediately before the new investor puts money in. Essentially, existing shareholders get diluted by the top-up, but the new investor does not get diluted. Again, it's a little annoying, but seems to be market standard.

This whole process might take 2-6 weeks, depending on how efficient the VC is, and how quickly you reply with the requested information.

The investment is only final when the money hits your bank account.

Congratulations. You now need to get back to building a successful business!

Angel Investors

“Angel investors” are rich individuals who invest small(-ish) amounts of their personal money into early stage technology companies. They have often (but not always) been founders or early employees of successful startups. A small angel cheque might be £5,000 or £10,000, but some “super-angels” make investments in the millions.

People take different views on how useful angels are. I’ve seen a seed round recently consisting of 56 separate angel investors. Other founders almost never take money from angels.

People talk about several different advantages that angels can bring.

If you get a number of angel investments early in your fundraising process, they can help by making warm introductions to VCs.

If you’re a B2B company, the founders of potential customers can help with product feedback and sales.

You can sometimes get other, more general business advice from angels who’ve been operators or founders themselves, but the quality of this advice is extremely variable.

Some founders seem to collect angel investors for their “brand name” or PR value. This is mostly bullshit, unless the angel is Jay Z. Journalists honestly don’t care that I’m investing in your company.

Very active angel investors may make 50+ investments a year, so realistically it’s hard for them to be super involved in your company.

The downside of taking angel money is that managing a group of angels can be like herding cats. You will need their signature on every official corporate action for the future of your company (ie future fundraising). If one angel has decided to go on a month-long ayahuasca retreat in the Peruvian mountains, it can be very inconvenient. If you really want to include angels, I would stick to the 5 or 6 highest value people, and enforce a reasonably high minimum cheque size.

You may also come across angel syndicates - this is generally for groups of angels who want to invest less money - perhaps £1k - £5k per deal - and as such find it hard to get individual allocation. So they all club together and offer to invest £50-100k as a syndicate. This is good for the entrepreneur because you only need the signature of the syndicate lead in future, but the value-add of each of the individual investors tends to be even lower. There are exceptions.

You can either try to pitch angel investors early - before you start talking to VCs - and aim to get a handful onboard who will help to make introductions. Or you can carve out a proportion of the round for angels after you have a termsheet, and then go and select angels you think will be most valuable.

Personally, I always steered away from taking money from angel investors. They are usually not as valuable as you think. And I say this as an angel investor myself!

Crowdfunding

I was involved in raising about £35m (?) in crowdfunding at Monzo, across 3 or 4 rounds. It is probably the slowest, hardest and most expensive way to raise money.

If you’re struggling to raise VC funding, it’s almost never a good fallback option.

But it is useful, I think, for deepening the engagement you have with your early customer base or community, especially where you want to get them involved in product or brand development.

Whether it’s a Kickstarter campaign, Steam Early Access or an equity platform like Crowdcube or Seedrs, it’s a great way to set expectations that this is a prototype product and invite customers to engage with a constructive and forgiving mindset. If you are open and communicative with these early supporters, they’ll turn into your most loyal customers and vocal advocates.

I would keep it as an option and discuss it with your lead VC - perhaps reserve £1m of a Series A round for crowdfunding if you think you have a product that’s suitable; normally something consumer-facing. It usually makes less sense to crowdfund for a B2B product.

I’ll repeat this - crowdfunding is generally a very tough way to raise funding if your other options aren’t working.

Investment Advisors

You may think about paying an Investment Bank or some other kind of advisor to run your investment process. They'll offer to help you put together a pitch deck, introduce you to relevant investors and negotiate key terms.

In general, you should not do this. Especially for a Seed or Series A.

Generally, only the weaker companies need to use advisors. By using an advisor, you are signalling to investors that you are one of these weaker company.

Instead, you should be able to get useful introductions and advice on your pitch deck from your existing VC investors or angels. If you don't already have useful investors, programmes like Y Combinator can be really useful for getting in front of VCs at Demo Day.

You might reasonably consider using advisors if you're raising a $500m pre-IPO growth round. But even at this stage, many of the best companies raise without advisors.

Secondaries

A VC investment in your company is sometimes called a “Primary” investment. It involves the creation of new shares in your company, diluting all existing shareholders, and the investor pays the investment money directly to the company. You can then spend that investment growing the company to hopefully make it more valuable. That’s how investment normally works.

“Secondary Share Sales” or “secondaries” are slightly different. It’s when founders, early employees or angels sell some of their existing shares directly to new investors. It doesn’t dilute existing investors - no new shares are created - and the money goes to the person selling the shares, not to the company.

It can be useful in a few different scenarios, but it should always come after you’ve raised enough primary investment to comfortably run the company comfortably for the next 18-24 months. You should normally only do secondaries when there’s excess demand from investors for more shares in your company, and your existing shareholders don’t want to dilute any further.

The first situation in which secondaries are useful is to quietly remove an angel investor, early employee or even cofounder who’s leaving the business. Allowing someone in this position to sell some proportion (or all) of their shareholding can make tricky conversations go a lot more smoothly. There are situations where you might want to do this at Seed or Series A.

The second situation is where founders or early employees have been working for several years on the company with relatively low salaries, and the business is starting to see some real success. You want to keep these people motivated to work hard - an exit might still be 5+ years away. In such situations, it can be incredibly stressful to know that approximately 99.9% of your total net worth is tied up in the business.