#assessee

Photo

Many people are misinterpreting new regime in following two points: 1. 1st misinterpretation is #Standarddeduction is Rs. 52,500 2. 2nd misinterpretation is it is applicable for assessee having income of 15.50 lakhs and more. These above misinterpretations are because of FM’s following statement in budget speech: “Each #salaried person with an #income of Rs. 15.5 lakh or more will thus stand to #benefit by Rs. 52,500.” Clarification is as follows: 1. As per Finance bill, Standard deduction as per sec 16(i) is Rs. 50,000 and not Rs.52,500. 2. This standard deduction is currently available in old regime also. Govt has just extended the same to new regime without any modification. 3. In FM’s above statement, govt is trying to compare the benefit the assesses would get in case of ‘Current new regime’ vs ‘Proposed new regime’. FM has nowhere mentioned that standard deduction is applicable for people having income of Rs.15.50 or more. Hence, it is applicable to all assesses irrespective of their income. Hence, if an #assessee is having income of Rs. 15.50 lakhs then his #tax liability would reduce by Rs. 52,500 in Proposed new regime as compared to current new regime. https://www.instagram.com/p/CoX3C0ZtKDu/?igshid=NGJjMDIxMWI=

0 notes

Video

youtube

Income Tax Basics|Tax Slab FY 2023-24|115BAC New Slab|How to compute Total Income/Total Tax FY 23-24 Income Tax Basics: Understanding Charging Sections, Assessments, and Tax Slabs (FY 2023-24)" Description: 🔍 Unlock the complexities of Income Tax with our comprehensive guide! In this video, we delve into the fundamental concepts of Income Tax, covering crucial topics like Charging Sections, Assessments, and the latest Tax Slabs for the financial year 2023-2024, assessment year 2024-25. 👉 Charging Sections & Key Concepts: What is the Income Tax Charging Section? Who qualifies as an Assessee? Understanding the Assessment Year and its significance. Deciphering the concept of Previous Year. Unraveling the Rates and Slabs applicable to different entities. 💼 Income Tax Slabs for FY 2023-2024: (a) For Individuals, AOP, BOI, HUF (b) For Domestic and Foreign Companies (c) For Co-operative Societies, Firms, LLP, with insights into surcharge and cess. 📈 Explore 115BAC - New Rates from FY 2023-24 Onwards: Learn about the latest tax rates under Section 115BAC and understand how they impact your financial planning. 💡 How to Calculate Total Income: The 5 Heads of Income: Income From Salaries Income from House Property Income from PGBP (Profit and Gains from Business or Profession) Income from Capital Gain Income from Other Sources 🧮 Income Tax Calculation for FY 2023-24: (a) A step-by-step guide for Individuals (b) Special considerations for Senior Citizens and Super Senior Citizens 🚀 Whether you're an individual taxpayer, a business owner, or part of a company or co-operative society, this video equips you with the knowledge needed to navigate the intricate landscape of Income Tax. Stay informed, plan smartly, and make the most of your financial journey. 📌 Don't forget to like, share, and subscribe for more insightful content on financial literacy! Let's empower ourselves with tax wisdom. 💼💰 #incometax #incometaxreturn #incometaxreturnfiling2024 #itr #itr1 #incometaxbasics #incometaxslab #newtaxrates #newtaxregime #115bac #howtocomputetax #howtocomputetax Follow me on: Pinterest: https://in.pinterest.com/cadevesht LinkedIn: https://www.linkedin.com/in/cadeveshthakur/ Instagram: https://www.instagram.com/cadeveshthakur/ Twitter: https://twitter.com/cadeveshthakur Tumblr: https://www.tumblr.com/blog/cadeveshthakur Youtube Channel: https://www.youtube.com/c/cadeveshthakur Reddit: https://www.reddit.com/user/cadeveshthakur E-Commerce Accounting: https://www.facebook.com/groups/ecommerceaccountingsolutions #cadeveshthakur

#youtube#income tax#income tax basics#how to compute total income#how to compute total tax#income tax slab fy 2023-24#income tax slab ay 2024-25#income tax slab for individual#income tax slab for companies#income tax slab for foreign company#income tax slab for domestic company#ca inter#ca student#ca students#surcharge fy 2023-24#charging section#who is assessee#what is assessment year#what is previous year#who is person

0 notes

Text

How to link PAN with Aadhaar by May 31 to avoid Income Tax Notice?

Link PAN with Aadhaar: In cases where PANs of the deductees/ collectees have been inoperative, the TDS is deducted at higher rates. However, the income tax department has said that no action will be taken for a short deduction of TDS in case the assessee links his/her PAN with Aadhaar by May 31. Know how to link your PAN with Aadhaar. As per income tax rules, if a Permanent Account Number (PAN)…

View On WordPress

0 notes

Text

Section 33A of Income Tax Act 1961

Section 33A of Income Tax Act 1961-Development allowance

Section 33A(1) of Income Tax Act 1961

In respect of planting of tea bushes on any land in India owned by an assessee who carries on business of growing and manufacturing tea in India, a sum by way of development allowance equivalent to—

(i) where tea bushes have been planted on any land not planted at any time with tea bushes or on any…

View On WordPress

0 notes

Text

Show Cause Notice (SCN) issued by Customs Department is Void ab-initio where Pre-SCN consultation is not given to the assessee

Show Cause Notice (SCN) issued by Customs Department is Void ab-initio where Pre-SCN consultation is not given to the assessee

“Indirect Tax I Arbitration I Insolvency Advisory I Litigations”

Dated: 09.04.2024

Show Cause Notice (SCN) issued by Customs Department is void ab-initio where Pre-SCN consultation is not given to the assessee

The Jharkhand High Court has ruled that under the proviso to Section 28(1)(a) of the Customs Act, 1962, pre-SCN consultation is mandatory before issuing a show cause notice.

The…

View On WordPress

#AdvisoryServices#BiharFoundry#CBIC#CoalImport#CoalIndustry#Consulting#Facebook#India#IndirectTax#Instagram#Jharkhand#JharkhandHighCourt#Law#LawFirm#Lawyer#LegalUpdate#LitigationSupport#Meta#SCN#ShowCauseNotice#Telegram#Tumblr#Twitter#WhatsApp#YouTube#Google

0 notes

Photo

IT Dept Sends E-mail, SMS To Assessees For Mismatch In Tax Profile, Fin Transactions - News18

0 notes

Text

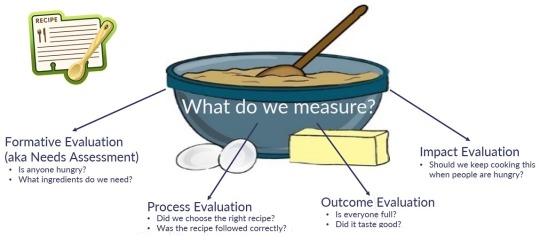

ASSESSMENT AND EVALUATION: UNRAVELING THE NUANCES

These two words have a special significant in the context of education and development, and although many people tend to use these terms interchangeably, there is a distinct difference between the two. Assessments and evaluations are two essential components in the process of teaching and learning. Although teaching, learning, and assessment have been there since forever, people still have dozens of misconceptions regarding them. An assessment is the process of investigating what and how participants are learning/ working, while evaluating involves making a judgment about the quality of participants’ learning/ work.

Assessment is a systematic process of collecting information from diverse sources about something or someone to gauge the skills, knowledge, and usage, whereas the meaning of evaluation is concerned about making a judgment about quality, skills, or importance or something or someone. The basic difference between assessment and evaluation lies in the orientation, i.e. while the assessment is process oriented, evaluation is product oriented.

Understanding the differences between assessment and evaluation is crucial for educators, researchers, and professionals involved in various assessment processes.

A Situation Narrative

Mrs Jayanthi Sharma eagerly anticipated the upcoming parent-teacher conferences of the day. She had studied hard as a Childhood Education major and had worked diligently in her first year as a 3rd Std teacher at XXX School. Jayanthi had planned interdisciplinary lessons, employed inquiry-based learning centers, and met regularly with individual students to ensure that they had mastered the skills as determined by the state standards.

Each student had a portfolio filled with dated representations of their work. Jayanthi understood the importance of specific and timely feedback and had painstakingly provided detailed written feedback on each work sample. She meticulously arranged the portfolios along with anecdotal notes and looked forward to sharing the accomplishments of the students with their family members. As last-minute jitters began to set in, Jayanthi realized that she had no grades for any of the students.

Jayanthi quickly realized she was not as prepared as she had anticipated.

What is Assessment

The word “assess” is derived from the Medieval Latin word “assessee” whose meaning is “fix a tax upon.” Assessment helps the educators to investigate what participants are learning and how well they are learning it, especially in relation to the expected learning outcomes of a lesson. The word assessment often is used to assess skills, abilities, aptitude, performance, and competence.

Thus, it helps the assessor to understand how the assesse understands the lesson, and to determine what changes need to be made to the teaching process. Thus it focuses on learning as well as teaching and can be termed as an interactive process. The purpose of conducting an assessment is to provide constructive feedback so that the assesse (the assessed person) can improve. Assessment is a continuous interactive process where two parties are involved.

What is Evaluation

The meaning of the word “evaluate” is to make a judgment about something or someone to learn about their abilities or skills or qualities. The word evaluate is derived from the Latin word “valere” whose meaning is to “too strong, be of value, be well, or be worth.”

Evaluation focuses on what has been learned by the participants. The evaluation process is used to make a judgment about the quality of participants’ learning/work. It usually involves assignment of grades/ ranks. Evaluation activities such as examples, papers, etc. are considered to be a formal way to assess the expected outcomes of a course. The evaluation may not only judge knowledge but may also include other components such as attendance, participation in activities, discussions, etc.

The evaluation process may be conducted to compare the skills and qualities of two or more individuals. The person being evaluated must fulfill the criteria set by the evaluator. Unlike assessment, the result of does not provide constructive feedback, but it passes the judgment.

Differences between Assessment & Evaluation

Characteristics of Assessment & Evaluation

One of the most important characteristics of an assessment is it is an ongoing process. This means at various points in the learning process, the instructor uses different tools to measure the individual’s abilities and level of knowledge. Also, assessments are collaborative, consistent, reliable, and tailored to a specific context.

A good evaluation process is valid, reliable, and practical. Validity means that the evaluation must measure the subject using well-defined criteria that are tailored to the subject. Reliability means that the process must be consistent while practicality suggests that every evaluation should be realistic and achievable within its context of usage.

Illustrations of Assessment & Evaluation

Assessment & Evaluation In Industry

To a large extent, both assessments and evaluations are used in similar industries. Like evaluations, assessments are very popular in educational research and human resources. They are used during employee engagement surveys to gather feedback from workers on how to improve the workplace. Different tools come in handy during assessments including concept maps, straw polls, surveys and questionnaires.

Evaluations are also used in the accounting/finance industries to determine the viability of a business. For example, before an investor gives money to an organization, they conduct a company evaluation to know if the business can provide returns on time. Common tools for evaluation include a rubric or some other standard grading criteria, focus groups, case studies, observation, and interviews.

Assessment & Evaluation in Survey Research

In survey research, assessments help the researcher to gather feedback on the quality of the systematic investigation. At the same time, assessments help to define and modify the research framework at different points in the process. Evaluations provide useful data for measuring the impact and success of the research. It helps you to determine how much progress has been made in the systematic investigation and if any changes need to be effected along the way.

Assessment vs Evaluation in Education

In educational contexts, assessments provide valuable information about a student’s knowledge, how much he has learned, the quality of this knowledge, and the different challenges faced during the learning process. Through assessments, teachers identify learning gaps and address them on time.

Evaluation provides useful data for building the core of the educational curriculum and improving it from time to time. For the learners, it validates their knowledge and determines how they progress from one level to the next. Data from an evaluation is a great way to show how successful a program is.

Benefits & Drawbacks of Assessment and Evaluation

Contrast Outline- Assessment & Evaluation

We measure distance, we assess learning, and we evaluate results in terms of some set of criteria. These three terms are certainly share some common attributes, but it is useful to think of them as separate but connected ideas and processes. Assessment and evaluation are integral processes used across diverse fields to measure performance, determine effectiveness, and guide decision-making. By understanding the key concepts, steps, and significance of assessment and evaluation, stakeholders can utilize these processes to improve outcomes, enhance quality, and drive progress. Assessment and evaluation are iterative processes, often involving multiple cycles of data collection, analysis, interpretation, and action. Continuous feedback and improvement are essential to maximize the value and effectiveness of these processes.

Content Curated By: Dr Shoury Kuttappa

#evaluation#decision#preformance#metrics#assessment#feedback#continuousimprovement#emotional intelligence#self leadership

0 notes

Text

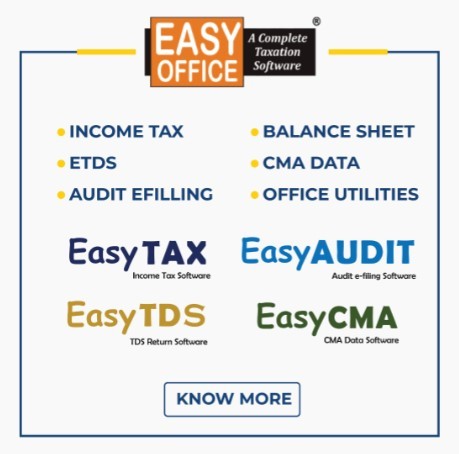

electrocom.in I Income tax software, best income tax software, income tax return filing software free download, income tax software free download

Income tax software,income tax computation software

.

EasyTAX

Income Tax Return Filing Software

File your Income-Tax Returns Quickly with Ease & Accuracy

It offers a range of features to help Tax Professionals to streamline tax preparation process and ensure accurate computation of income and taxes. Completely automate the process of return preparation and computation of tax.

.

best income tax software,income tax software price

Auto Selection of applicable ITR as per Income, generates ITR forms 1, 2, 3, 4, 5, 6, 7 and ITR U (updated Return) in both paper and electronic format, making filing of e-returns easier. The JSON / XML Import facility helps to import master and return data easily.

.

income tax return filing software free download,income tax software for a.y. 2024-25

Other key features include Computation of business income for multiple businesses, Presumptive income under sections 44AD, 44ADA, and 44AE, Calculation of allowable remuneration and interest to partners in a firm, Auto set off and carry forward of losses, Interest Calculation under sections 234A, 234B, 234C, 234F, Comparative income tax summary for multiple assessment years, Computation for both the old & new Tax regime under section 115BAC with a comparative income statement, Generate various Analysis reports such as Pending returns, Filed returns with dates, Refund status, Tax Register etc. EasyOffice Software demo can be downloaded free of cost.

.

EasyOFFICE’s Income Tax Module EasyTAX is the Best Income Tax Software for Tax Professionals. The software simplifies the tax preparation process, reduces errors, and provides a more efficient way to file taxes.

.

income tax software free download,it return software

Accurately Compute Income & Tax, Self-Assessment Tax, Advance Tax, Provision for set-off losses, clubbing of incomes, chapter VIA deductions, rebates, arrears, Interest Calculation, etc.

.

EasyOFFICE is a very popular software among Chartered Accountants and Tax professionals. Experience the ease of Tax Preparation with EasyTAX - The most effective & user-friendly Income Tax Software.

.

tax filing software , best income tax software in india

India’s Best Income Tax, TDS, GST Software

Electrocom’sEasyOffice and EasyGST Taxation software is specifically designed & developed to revolutionize the complete Taxation management of CA & Tax Professionals. Our Software has created a reputation in the PAN India market for user-friendly operations, Accuracy, Taxation process automation & excellent after-sales support.

best income tax software for chartered accountants,income tax software for ca

Show More

Simplifying Tax and Account Compliance

Easy, Effective & Efficient Software

Competitive Price

Fully Menu-Driven Solution for all Assessee status to prepare and file their income tax e-returns.

.

income tax software free for chartered accountants,Top 10 Income tax software in India free

Contact Us :

505, Sukhsagar Complex, Nr. Hotel Fortune Landmark, Usmanpura Cross Road, Ashram Road, Ahmedabad - 380013, Gujarat (INDIA),

Call us :079-27562400, 079-35014600

Website: https://easyofficesoftware.com/

Email us : [email protected]

Office Time : 10:15AM - 7PM (Mon-Fri), 10:30AM - 5PM (Sat)

0 notes

Video

youtube

Commissionerate issuing SCN to assessee with highest demand holds jurisdiction to adjudicate all connected SCNs - Delhi High Court

0 notes

Text

Legal Precision Unveiled: Unraveling the Intricacies of Input Tax Credit Quandaries

Delving deeper into the intricate tapestry of Goods and Services Tax (GST) implications, the saga of Input Tax Credit (ITC) assumes greater complexity, offering a nuanced perspective on the petitioner-assessee’s odyssey.

Embedded within the labyrinth of statutory constructs, the petitioner’s invocation of Input Tax Credit (ITC) rights under section 16 of the CGST Act unfolds against the backdrop…

View On WordPress

#assessing authority#Chartered Accountant#GST regulations#Ingram Micro India#Input Tax Credit#judicial scrutiny#judiciary#landmark case#legal documentation#legal intricacies#legal landscape#legal odyssey#legal recalibration#procedural norms#regulatory compliance#Show Cause Notice#State Tax Officer#statutory provisions#tax disputes

0 notes

Text

Section 234F of the Income Tax Act - Penalty for Late Filling

What is Section 234F of the Income Tax Act?

The Finance Act of 2017 introduced Section 234F of the Income Tax Act, which deals with the problem of late income tax return filing. Encouraging timely filing and streamlining the tax administration are the main goals. This section pertains to all individuals who must file income tax returns in India.

The Income Tax Act penalizes individuals for filing income tax returns (ITRs) after the deadline, as stated in Section 234F. This section came into effect for the 2018–19 assessment year.

Who is required to file an Income Tax Return?

Filing an Income Tax Return (ITR) is mandatory under the following circumstances:

1. Exceeding Basic Exemption Limit: Filing an ITR is required if an individual's total income exceeds the basic exemption limit.

2. Age-specific Income Criteria: When an individual's income surpasses Rs. 2.5 lakhs, they are required to file a return, regardless of age. The threshold is Rs. 3 lakhs for senior citizens (60 years or older) and Rs. 5 lakhs for super senior citizens (80 years or older). Notably, this cap was raised to Rs. 5,000,000 for extremely senior citizens and Rs. 3 lakhs for individuals under the new tax regime that was unveiled in the Budget 2023.

Under the old tax regime, the Basic exemption limit is calculated without considering any deductions from capital gains under sections 54, 54B, 54D, 54EC, 54F, 54G, 54GA, or 54GB, or deductions under Section 80C to 80U.

Important Note: Assessee Opting for the new tax regime will not be allowed to avail the above-mentioned deductions.

3. Assets Abroad and Foreign Accounts: If they have signing authority over foreign accounts or own assets or financial interests in entities outside of India, citizens and regular residents of India are required to file a return.

4. Bank Deposits: An ITR must be filed if you deposit Rs. 1 crore or more in one or more bank current accounts.

5. International Travel Expenses: Individuals spending more than Rs. 2 lakhs on international travel during the previous year are required to file a return.

6. Substantial Power Consumption: Filing an ITR becomes mandatory for those spending more than Rs. 1 lakh on power consumption in the preceding year.

7. Profession Gross Receipts: If the total gross receipts from a profession exceed Rs. 10 lakhs in the previous year, filing an ITR is necessary.

8. TDS and TCS Threshold: If the total TDS and TCS amount for the prior year was Rs. 25,000 or more, individuals under the age of 60 are required to file a return. The threshold is raised to Rs. 50,000 for senior citizens.

9. Business Turnover Requirement: Individuals with business turnovers exceeding Rs. 60 lakhs in the preceding year are required to file a tax return.

10. High Savings Bank Deposits: Filing an ITR is necessary if an individual's total deposit in one or more savings bank accounts during the previous year is Rs. 50 lakhs or more.

What is the last date to file ITR?

The due date for filing Income Tax Returns (ITR) in India can vary based on the type of taxpayer and the applicable audit provisions.

Individuals, Hindu Undivided Families (HUFs), and taxpayers whose accounts are not required to be audited: Usually, the deadline is July 31st of the assessment year. For the fiscal year 2021–2022, for instance, the deadline would be July 31, 2022.

Taxpayers whose accounts are required to be audited (including companies):

September 30th of the assessment year is the deadline. For instance, September 30, 2022 would be the deadline for the fiscal year 2021–2022.

Nonetheless, the deadline for filing an ITR is November 30 of the assessment year if the company has any foreign transactions or specified domestic transactions for which it must provide a report in Form No. 3CEB u/s section 92E.

How to file Challan No. 280 to pay the 234F Fees?

Challan No. 280 is the form for remitting penalties related to the non-filing or late filing of Income Tax Returns (ITR). To make a payment through Challan No. 280, the assessee must complete the following steps:

1. Assessment Year and Tax Type: Indicate the relevant Assessment Year and choose the applicable tax type, distinguishing between corporate tax and others.

2. PAN (Permanent Account Number): Enter the PAN or Permanent Account Number in the provided space on the challan.

3. Name and Residential Address: Provide the full name and complete residential address of the assessee.

4. Contact Details: State a phone number along with the STD code for communication purposes.

5. Select Tax Type: Choose the appropriate type of tax from the following options:

Advance Tax

Surcharge

Self-Assessment Tax

Tax on Regular Assessment

Tax on Distributed Profits of Domestic Companies

Tax on Distributed Income to Unit Holders

6. Payment Details: Fill in the payment details, ensuring accuracy in the entered information.

7. Bank Information: Specify the precise date of payment, the name of the bank, and the branch where the payment is being made.

8. Signature: Affix the signature of the individual making the payment.

9. Counterfoil Details: In the counterfoil section, provide the details as shown in the form, including PAN, name of the bank and branch, assessment year, etc.

Accurately completing these steps guarantees a seamless and error-free Challan No. 280 payment process. It's also advised to keep a copy of the counterfoil for documentation's sake. It is advisable to consult the most recent guidelines provided by the tax authorities or seek advice from a tax professional if any doubts or inquiries arise during the process.

Loss Carry Forward Restriction:

Failure to file by the deadline limits the amount of losses in your business or under the head capital gains that can be carried forward, which could have an impact on future tax benefits.

Delayed Refund Processing: In order to guarantee that people receive their overpaid taxes as soon as possible, timely filing is crucial to accelerating the processing of refunds.

How can you avoid giving the Income Tax Department the money due under section 234F?

It is imperative that you file your Income Tax Return (ITR) by the specified deadline in order to avoid having to pay the late filing penalties under Section 234F of the Income Tax Act. The following crucial actions can help you avoid paying late filing fees:

1. File Your ITR on Time: The most straightforward way to avoid late filing fees is to file your ITR on or before the specified due date. For individual taxpayers, the due date is typically July 31 of the assessment year.

2. Be Aware of Due Dates: Remain aware of the ITR filing deadlines. Depending on the type of taxpayer, audit requirements, and other variables, the deadline may change. Look for any updates or extensions from the Department of Income Taxation.

3. Keep Track of Changes in Regulations: Keep an eye out for updates to late filing penalties, deadlines, and other relevant provisions when it comes to tax regulations. You can prepare and file your returns on time if you keep yourself informed.

4. Use Electronic Filing (e-filing): Make use of the Income Tax Department's electronic filing (e-filing) option. E-filing typically saves time and improves convenience, so there's less chance that your ITR submission will be delayed.

5. Organize Your Financial Documents: Make sure you have all the required financial information and documentation well in advance. Maintaining organisation will make filing easier and ensure that your ITR is submitted on time.

6. Seek Professional Assistance: Seek advice from a tax expert if you find the tax filing process difficult or if your financial situation is more complicated. They can help you file on time and walk you through the procedure.

7. Make Use of Reminder Tools: Set up reminders on your calendar or use digital tools to receive notifications about upcoming tax deadlines. This will help you stay proactive and avoid unintentional delays.

8. Consider Advance Tax Payments: Consider paying your taxes in advance if you have a sizable income that isn't subject to tax deduction at source (TDS). By doing this, you can pay your taxes throughout the year rather than all at once when you file.

9. Plan for Contingencies: Be prepared for obstacles that might cause your filing to be delayed, such as unforeseen events or technical problems. Make the necessary plans to submit your ITR well in advance of the deadline.

By following these procedures, you can reduce the possibility that you won't make the filing deadline and, as a result, stay out of trouble with Section 234F's late filing fees. Maintaining awareness, organisation, and initiative in meeting your tax responsibilities is essential.

0 notes

Text

What is GSTR 10 and how to file GSTR 10?

Introduction

Goods and Services Tax (GST) has streamlined the tax structure in India. As a part of GST compliance process, taxpayers are required to file various returns including GSTR 10. In this article, we’ll discuss everything you need to know about filing GSTR 10, including what it means, who needs to file, the due date, and the penalty for non-compliance.

The meaning of GSTR 10

GSTR 10, also known as final return, is the return filed by a taxpayer whose GST registration has been canceled or surrendered. It is a statement which contains details of all supplies made and received during the period from the effective date of cancellation of registration to the date of cancellation or surrender.

Who is required to file GSTR 10?

Any taxpayer whose GST registration is canceled or surrendered is required to file a GSTR 10. It is important to note that GSTR 10 is a mandatory return and non-compliance may result in penalties and legal consequences.

GSTR 10 Filing Due Date

The due date for filing GSTR 10 is within three months from the date of cancellation of registration. For example, if a taxpayer surrenders his registration on 15th February 2023, the due date for filing GSTR 10 will be 15th May 2023.

Penalty for Non-Compliance GSTR 10

Non-compliance with GSTR 10 may result in penalties and legal consequences. If a taxpayer fails to file GSTR 10 on the due date, they will be liable to pay late fee of Rs. 100 per day of delay, subject to a maximum of 0.25% of the turnover of the assessee. In addition, the taxpayer’s registration may be deemed to be active, and they may be required to file all outstanding returns and pay any outstanding tax liability.

Details to be furnished in GSTR 10

GSTR 10 requires the taxpayers to furnish details of all supplies made and received during the period from the effective date of cancellation to the date of cancellation or surrender. The return should also contain information about the stock held on the date of cancellation or surrender and the tax liability arising out of such stock for availing and availing of input tax credit.

Procedure for filing GSTR 10

In order to file GSTR 10, taxpayers must first log in to the GST portal using their credentials.

Then they must navigate to the “Services” tab and select “Return” > “Final Return”.

After selecting the financial year and tax period, taxpayers must provide the necessary details and submit the return.

Once the return is submitted, an acknowledgment receipt will be generated with a unique reference number. Taxpayers should download and save this receipt for future reference.

GSTR 10 Consequences of non-filing or delayed filing

Failure to file GSTR 10 or late filing may result in penalties and legal consequences. In addition to the late fee Rs. 100 per day of delay, subject to a maximum of 0.25% of the taxpayer’s turnover, the taxpayer’s registration may be deemed to be active, and they may be required to file all due returns and pay any outstanding tax liability. The taxpayer may also be subject to interest and penalties on any tax liability arising out of the stock held on the date of cancellation or surrender.

Exceptions to Filing GSTR 10

There are some exceptions for filing GSTR 10. Taxpayers who have obtained registration under GST but have not supplied or received any goods or services during the period from the effective date of registration to the date of cancellation or surrender. File the GSTR 10. In addition, taxpayers who have obtained registration but have not started business and subsequently surrendered their registration are also exempted from filing GSTR 10.

Key takeaways

GSTR 10 is a return filed by a taxpayer whose GST registration has been canceled or surrendered.

GSTR 10 is a mandatory return, and non-compliance can lead to penalties and legal consequences.

The due date for filing GSTR 10 is within three months from the date of cancellation of registration.

Non-compliance with GSTR 10 may result in a late fee of Rs. 100 per day of delay, subject to a maximum of 0.25% of the turnover of the assessee.

If a taxpayer fails to file GSTR 10 by the due date, their registration may be deemed active, and they may be required to file all pending returns and pay any outstanding tax liability.

Conclusion

In conclusion, GSTR 10 is an important return which needs to be filed by taxpayers whose GST registration has been canceled or surrendered. Failure to comply with GSTR 10 filing requirements may result in fines and legal consequences. Taxpayers need to be aware of the due date for filing GSTR 10 and ensure that they file the return within the stipulated deadline. By doing so, taxpayers can avoid unnecessary fines and legal troubles.

0 notes

Video

youtube

TDS ki कक्षा|Part 3|Interest, Fees, Penalty, Prosecution, Expense Disallowance under TDS|Income Tax

TDS ki कक्षा TDS Knowledge series Part 3 @cadeveshthakur #tds #incometax #cadeveshthakur #trending #viral TDS compliance and the consequences associated with it. In this video, we’ll explore various sections of the Income Tax Act related to TDS (Tax Deducted at Source) and discuss the implications for defaulting taxpayers. Here’s the content breakdown: 📌 Timestamps 📌 00:00 to 00:56 Introduction 00:57 to 02:46 Content Part3 02:47 to 03:54 Example 03:55 to 08:48 Assessee in default 08:49 to 11:00 example 11:01 to 17:07 late fees 17:08 to 23:40 interest 23:41 to 31:51 how to calculate interest & fees 31:52 to 37:00 penalties 37:01 to 38:30 prosecution 38:31 to 39:43 disallowance 1. Section 201: Assessee in Default o Explanation of what constitutes an “assessee in default.” o Consequences for failure to deduct or pay TDS. o Key points: Interest (Section 201(1A)): When a deductor fails to deduct tax at source or doesn’t deposit it to the Government’s account, they are deemed an assessee in default. They become liable to pay simple interest: 1% per month (or part of a month) on the amount of tax from the date it was deductible to the date of deduction. 5% per month (or part of a month) on the amount of tax from the date of deduction to the date of actual payment. Interest as Business Expenditure: Clarification that interest paid under Section 201(1A) cannot be claimed as a deductible business expenditure. Penalty (Section 221): If a person is deemed an assessee in default under Section 201(1), they are liable to pay penalty under Section 221 in addition to tax and interest under Section 201(1A). The penalty amount cannot exceed the tax in arrears. Reasonable Opportunity: The assessee has the right to be heard and prove that the default was for good and sufficient reason. 2. Section 234E: Late Fee for TDS/TCS Returns o Explanation of late fees for non-filing or late filing of TDS/TCS returns. o Due dates for filing TDS/TCS returns. o Late fee calculation: INR 200 per day until the default continues (not exceeding the TDS/TCS amount). o FAQs on Section 234E. 3. Section 276B: Prosecution for Failure to Deduct TDS o Overview of prosecution provisions for non-compliance with TDS obligations. 4. Disallowance of Expenses (Section 40(a)(i)/(ii)) o Explanation of disallowance of expenses if TDS is not deducted or paid. #youtubevideos #youtube #youtubeviralvideos #tdsfreecourse #freecourse #taxdeductedatsource #TDSCompliance #IncomeTax #TaxDeduction #TCSReturns #LateFiling #Penalty #BusinessExpenditure #TaxLiabilities #FinancialCompliance #TaxPenalties #TaxationLaws #AssesseeInDefault #InterestPayment #TaxProcedures #LegalObligations #TaxAwareness #TaxEducation #FinancialLiteracy #TaxPlanning #TaxConsultancy #TaxAdvisory #TaxProfessionals #TaxUpdates #TaxGuidance #TaxTips #TaxAccounting #TaxFiling #TaxReturns #TaxPolicies #TaxChallenges #TaxSolutions #TaxExperts #TaxCompliance #TaxAware #TaxMistakes #TaxConsequences #TaxPenalties #TaxKnowledge #TaxRules #TaxRegulations #TaxBestPractices #TaxManagement #TaxUpdates #TaxNews #TaxInsights #TaxGuidelines #TaxCode #TaxEnforcement #TaxEnforcementActions #TaxPenaltyProvisions #TaxPenaltyLaws #TaxPenaltyGuidance #TaxPenaltyExplained #TaxPenaltyFAQs #TaxPenaltyCompliance #TaxPenaltyAvoidance #TaxPenaltyMitigation #TaxPenaltyResolution #TaxPenaltyAdvice #TaxPenaltyConsulting #TaxPenaltyExperts #TaxPenaltyHelp #TaxPenaltyTips #TaxPenaltyEducation #TaxPenaltyAwareness #TaxPenaltyPrevention #TaxPenaltyManagement #TaxPenaltyStrategies #TaxPenaltyUpdates #TaxPenaltyNews For more detailed videos, below is the link for TDS ki कक्षा TDS Knowledge series https://www.youtube.com/playlist?list=PL1o9nc8dxF1RqxMactdpX3oUU2bSw8-_R

#youtube#what is tds#tax deducted at source#how to file tds return#how to issue tds certificate#tds due dates fy 2024-25#tds due dates fy 2023-24#tds free course#cadeveshthakur

0 notes

Text

Gain/Loss On Futures And Options – Income Tax Treatment

Derivative trading, or the trading of futures and options, has increased dramatically in the last few years. Usually referred to as F&O. People who had previously been involved in it on a part-time basis are now pursuing it full-time. Along with their jobs, people are earning extra money through trading. Through F&O investment, investors can forecast the price of stocks or commodities and earn substantial returns. However, there is a significant risk involved.

Investors are talking a lot about trading futures and options, or F&O, on stocks, currencies, and commodities, but they need to know how this is taxed. Allow us to better understand how to handle your taxes.

What is F&O, or futures and options?

Financial derivatives instruments traded on stock exchanges are called futures and options, or F&O. These are contracts that let investors guess or hedge their bets on how the prices of underlying assets—like stocks, commodities, currencies, or indexes—will change in the future. This is a quick summary of options and futures:

Futures:

A standardised contract for the purchase or sale of an underlying asset at a fixed price and future date is known as a futures contract.

Regardless of the market price at the time the contract expires, it requires the seller to sell the asset at the agreed-upon price and the buyer to buy it.

Futures are highly standardised with respect to contract size, expiration date, and settlement method. They are traded on organised exchanges.

Options:

The buyer of an options contract is granted the right, but not the responsibility, to purchase (call option) or sell (put option) an underlying asset at a strike price on or before a specific date (expiry date) at a given price.

For the option, the buyer gives the seller a higher price.

If the buyer chooses to exercise the option, the seller is required to comply with the terms of the agreement.

Options come in a variety of forms, including index options, stock options, and commodity options, and are also traded on organised exchanges.

Future and Option Trading.

Options & Futures Trading is the act of exchanging derivatives for an underlying asset at a fixed price. A currency, equity shares, or a commodity could be this underlying asset.

With futures, a trader purchases or sells a contract at a fixed price and on a fixed future date.

Options provide the buyer the right, not the obligation, to purchase or sell, so he can terminate the agreement if he suffers any losses.

Treatment of Futures and Options in the ITR along with the adjustment of Losses?

Trades of futures and options are reported under Profit and Gains from Business or Profession. Net of all the trades whether positives or negatives are considered as Business Income. Whereby for reporting purposes Turnover is considered as Absolute amount of ( Selling Amount – Purchase Amount). While Profits are reported under Profit and Gains from Business and Profession and taxed as per the slab rate of the assessee.

Trading in futures and options is regarded as non-speculative activity under Section 43(5). This implies that the taxation of any income derived from F&O trading is comparable to that of business transactions.

Transactions can be offset against all other sources of income (salary excluded) in the event of a F&O loss. This is a main advantage. These sources of income could come from a business or occupation, real estate, or other sources. For instance, if you are paying Rs 100,000 in rent each month, you will receive Rs 12,00,000 a year. If you have any loss on F&O for the year, which let’s say is Rs. 200,000, you can deduct this loss from your rental income. Your taxable income will drop to Rs. ((1200000- (30%*1200000)- 200000)= 640,000 as a result.

In this instance, the loss may be carried forward over the following eight years if it could not be set off in the current year. But for the next eight years, nothing will change; but you can only deduct it from your business income.

When reporting F&O income, which ITR form should I file?

To file an ITR, there are various forms available. Given that F&O income and losses are regarded as typical business income and losses, selecting the appropriate option is crucial depending on the nature of your revenue. Therefore, the appropriate form to report this income is ITR-4. To guarantee accurate reporting of your income and prevent any discrepancies, it is imperative that you choose the appropriate ITR form.

What variables are considered and how is F&O turnover calculated?

Calculating trading turnover is crucial to determining whether or not the tax audit is relevant.

Total Profit (the absolute total of the gains and losses on all of the transactions that were made during the year) is the turnover for futures and options trading.

Here, the sum of the positive and negative differences equals the profit or loss.

Let’s use an example to better understand this:-

On 07/09/2023, Mr. X purchases 400 Nifty Futures contracts at a price of Rs. 50. On October 20, 2023, he sells these contracts for Rs. 30. Additionally, on October 5, 2022, Mr. X purchases 200 Sensex Futures contracts for Rs. 100. On December 9, 2023, he sells these contracts for Rs. 150.

Loss from Trade 1 = (30-50) * 400 = Rs. -8,000

Profit from Trade 2 = (150-100) * 200 = Rs. 10,000

Turnover = 8000+10,000=Rs.18,000

Profit/ Loss from Business and Profession = Rs. 2000

The Advantages of Reporting Your F&O Loss

There are various advantages Futures and Options (F&O) loss when submitting your income tax return. These advantages include:

Tax Deduction: One of the main advantages of proving the loss is that it can be deducted from any other money you have received. You can deduct a loss on a F&O trade from all sources of income other than your salary. This could come from a job work, a business, a house property, or any other source of income. It lowers your total amount of owed taxes. This may assist in reducing your tax obligation.

Carry Forward: You may carry forward unabsorbed losses to subsequent fiscal years if your F&O losses in a given year surpass your total income. Your tax obligation in later years can be decreased by deducting these losses from your F&O gains. Carry Forward of losses would only be available if the return is filed timely as per Section 139(1)

Documentation for Future Use: When you accurately report your F&O losses, you get a record of your financial transactions that you can use for future financial planning or loan applications.

Adjustment against F&O Gains: Declaring the losses enables you to offset them against the gains, lowering the total tax obligation on F&O transactions, if you have both F&O gains and losses in a financial year.

Preparation of Books of Accounts and Audit Requirements

It is significant to note that once your account is classified as a business, appropriate books of accounts must be kept if the income exceeds Rs 2,50,000 or the turnover exceeds Rs 25,00,000 in any of the preceding three years, or in the first year in the case of a new business. Individuals conducting business, such as F&O trading, are subject to the same rules. Under Section 44AA of the Income Tax Act, the trader would have to prepare regular books of accounts. However, a tax audit under Section 44AB will be carried out if the turnover surpasses Rs. 10 crore or the profit declared is less than 8%. This implies that you must have a Chartered Account audit your accounts, and you must file your tax return and the audit report by the deadline set by the act.

Under Section 271A, there is a penalty for failing to keep accounting records. The fine is Rs 25,000. Furthermore, failing to have books audited in accordance with Section 44AB may result in a fine under Section 271B equal to the lesser of Rs 1.5 lakhs or 0.5% of gross receipts or turnover.

In what situations and with whom is a F&O trading tax audit permissible?

Case 1: Up to $2 Cr in trading turnover.

Tax Audit is not applicable if the profit is greater than or equal to 6% of Trading Turnover and presumptive taxation has been chosen.

If the taxpayer’s income exceeds the exemption limit and they have lost money or made money that is less than 6% of trading turnover, a tax audit is necessary.

Case 2: Trading Turnover Exceeds $2Cr and May Reach $10Cr

A tax audit is necessary if the taxpayer has lost money or made a profit that is less than 6% of trading turnover.

The Tax Audit is relevant if the profit exceeds or equals 6% of Trading Turnover and presumptive tax has not been chosen.

The Tax Audit is not relevant if the profit is greater than or equal to 6% of Trading Turnover and presumptive tax has been chosen.

Case 3: The trading turnover exceeds $10 billion.

Tax Audit is relevant in every situation, regardless of trading volume.

0 notes

Text

Section 33 of Income Tax Act 1961

Section 33 of Income Tax Act 1961-Development rebate

Section 33(1) of Income Tax Act 1961

(a) In respect of a new ship or new machinery or plant (other than office appliances or road transport vehicles) which is owned by the assessee and is wholly used for the purposes of the business carried on by him, there shall, in accordance with and subject to the provisions of this section and of section…

View On WordPress

0 notes

Last Seen Blogs

loop-and-stitch

Loop & Stitch - handmade

smartass--opposum

◇.Alexavier.◇

cleodobelle

theory is like a forest full of giant spiders

lunas-fat-ass

Luna Creed And Her Shenanigans

moonunion

Chefboy RD