Last Seen Blogs

ishine-trade-uk

iShine Trade

skytheninja

~🫧🌊''Sky-Blue Ninja Chronicles''🌊🫧~

grn-fog

Side Blog

m-b-y-l

MBYL

kalasenjaproject90-blog

KalaSenja Project

Text

Fauji Wealth: Premium Partner for Defence Personnel for Financial Planning

Fauji Wealth offers specialized financial planning tailored exclusively for defense personnel, ensuring their unique needs and goals are met with precision.

#defence mutual funds#fauji wealth#mutual funds#financial planning#financial strategies#technology funds

0 notes

Text

Technology Mutual Funds for Defence Personnel By Fauji Wealth

Fauji Wealth's Technology Mutual Funds cater to the distinct financial planning needs of defense personnel, offering a tailored investment avenue to capitalize on the dynamic tech sector.

With a focus on empowering armed forces members with sound financial strategies, these funds align seamlessly with the unique challenges and goals of military life.

Designed by experts in both finance and defense, these mutual funds provide an opportunity for defense personnel to invest in a diversified portfolio of technology-oriented assets.

Fauji Wealth recognizes the ever-evolving nature of the tech industry and ensures that its Technology Mutual Funds remain well-positioned to capture potential growth and innovation.

By combining financial expertise with a deep understanding of defense personnel's aspirations, Fauji Wealth paves the way for military personnel to participate confidently in the technology sector's advancements, aiming for both financial security and future prosperity.

#defence mutual funds#fauji wealth#mutual funds#financial planning#technology mutual funds#financial startegies

0 notes

Text

Fauji Wealth: Meticulously Crafting Financial Strategies for Defence Personnel

"Fauji Wealth" is a specialized financial planning service exclusively designed for individuals serving or retired from the defense sector. With a deep understanding of the unique financial needs and challenges faced by defense personnel, Fauji Wealth offers tailored financial solutions to help them achieve their long-term goals and secure their financial future.

0 notes

Text

Quality Consultation for Technology Mutual Funds by Fauji Wealth

Technology Mutual Funds by Fauji Wealth offer a strategic investment opportunity for individuals, with a focus on serving defence personnel. As experts in financial planning and consultation, Fauji Wealth aims to empower members of the armed forces with tailored investment solutions in the dynamic technology sector. These mutual funds provide a diversified portfolio of technology-related assets, allowing investors to benefit from the potential growth and innovation in the technology industry. With Fauji Wealth's specialized expertise, defence personnel can confidently navigate the complexities of the financial world and work towards achieving their long-term financial goals.

0 notes

Text

Get to know Technology Funds with Fauji Wealth

Discover the power of Technology Funds with Fauji Wealth! As expert Financial Planners for Fauji's, we offer a reliable and value-adding investment opportunity. Technology Funds allow you to invest in cutting-edge companies at the forefront of innovation, providing impressive growth potential.

#defence mutual funds#fauji wealth#mutual funds#technology funds#financial planning#financial planners

0 notes

Text

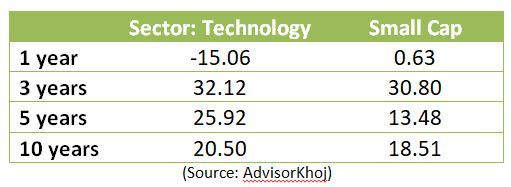

WHY SHOULD YOU NOT GIVE UP ON TECHNOLOGY FUNDS JUST YET

Up until 2021, Technology Funds gave investors astounding returns, some even receiving >90-100% returns. Even though 2021 saw a long bull run, wherein all funds, even the poorest performing funds in their respective categories, gave fantastic returns to investors, making everyone happy and drawing in many first-time investors also to dip their toes into the equity market pool. But come 2022, when the bull run ended, even the best funds in their respective categories failed to give returns, and first-time and short-term investors saw their savings plummet.

Technology mutual fund as a sector is one that everyone can bet on, given the evergreen nature of the type of companies these funds invest in. Technology funds invest in stocks belonging to IT, Technology, and related industries. Since the pandemic hit us, even the most archaic companies had to modernize and come to terms with new technology and had to adapt to stay afloat.

Many new companies using technology to make the lives of consumers comfortable were also born during this time and grew exponentially. So given the nature of these funds, why has the sector not given any returns, let alone negative returns in the past months? Why shouldn’t the investors stop investing in these and run away with whatever is left of their investments?

The answer lies in numerous factors, like exposure to foreign equity holdings for starters. Many global tech companies have seen a general correction after a higher-than-usual growth spurt driven by the pandemic, and lower-than-expected results of Infosys have added salt to the injuries. Also, as high inflation persists globally, many global tech firms have cut their advertising spending in order to save costs, and hence their profits are impacted as most of these tech giants run on advertisement fuelled growth.

The point is, there are many factors that have impacted the short-term performance of technology funds, but the market sentiment has been that the technology sector returns will start improving sooner if not later. And investors willing to take risks and add some diversity to their portfolios should capitalize on this correction. Small Cap funds have been the driving force for many investors’ portfolios, but in the long haul, technology funds seem to have outperformed them, making technology funds a must-have (but not the only thing) in one’s portfolio.

But what should the investors do?

1. Never concentrate all your investments in one very good category or fund, the mistake many new investors make upon seeing outstanding short-term returns from a fund

2. If an investor is risk-averse, investing in flexi-cap funds instead of sector funds is a better method to diversify investments, as flexi-cap funds invest in a multitude of sectors and track the market situation better than a part-time investor

3. Do not stop investing in technology funds or book your losses just yet because the sector is not doing well. Be patient, and once the market recovers like it always does, you will start seeing returns as you would have purchased more units for a cheaper price. Continue your SIPs and hold onto your old investments.

These suggestions are not some sort of ground-breaking mantras, but something every advisor guides their investors with. It is the job of an advisor to guide their investors, help them manage their emotions, and be patient when the investing market waters are turbulent. So hold on and tighten your seatbelts, as every phase in this market is temporary.

Reach out to Fauji Wealth if you have any suggestions or feedback on our article or wish to discuss it further.

View Source: - https://faujiwealth.in/f/why-should-you-not-give-up-on-technology-funds-just-yet

0 notes

Text

ELSS FUNDS: SIP OR LUMPSUM?

With the New Year comes a fleeting realization of the financial year wrapping up soon, putting the salaried and business folks alike into a frenzy of sorts to get their financial affairs in order. With the majority of the population sticking to the old tax regime to save whatever taxes they can, we get thousands of last-minute calls, “Sir, please quickly deposit INR 1.5 Lakh in any ELSS funds. Today is the last day and I don’t want to pay any tax which I can save”

This is one of the most common requests we get, in multitude, especially during the last week of March. Even the most risk-averse and learned investors don’t mind a lump sum transaction, with the market being wherever it is, as long as they can save a quick buck on taxes.

So the question arises, “should one start a SIP in ELSS funds (Equity Linked Savings Scheme a.k.a. Tax Saving Mutual Funds) or deposit a lump sum amount?”, and how much should one invest in the same annually?

Some features and benefits of Equity Linked Savings Scheme (ELSS) Funds are:

ELSS funds invest a major portion (minimum 80%) of their corpus into equity or equity-related instruments

Also known as Tax Saving Schemes as they offer an individual tax exemption of up to INR 1,50,000 from their taxable income under Section 80C of the income tax act (old tax regime).

Amount invested mandatorily gets locked in for 3 years from the investment date.

Income earned under this scheme if redeemed after completion of lock-in is considered as Long Term Capital Gain (LTCG)

Gains taxed at 10% (if LTCG from all investments exceed INR 1 Lakh)

No maximum tenure of investments

Investment can be made in either SIP or lump-sum mode

The dual benefit of saving tax and building wealth

A quick comparison between lump sum and SIP might help resolve many investors’ woes about how one should invest and treat ELSS funds.

Studying the aforementioned comparison between SIP and the lump-sum method explains how SIP can offer a better comprehensive solution to the tax-saving woe of many investors. For young investors, it also serves as a method to inculcate a habit of regular investing and managing expenses. A good rule of thumb for investors following the SIP method is to set the date of SIP very close to the date one receives a salary or business income. Investing before one gets the option to spend everything as avoidable expenses help establish saving habits in the young ones, all while helping them watch their money grow through the magic of compounding.

ELSS funds are one of the only tax-saving investment options with the potential to offer inflation-beating returns.

Now that we have established that ELSS is good, what stops one from investing in the same? And when SIP offers so many advantages over lump sum investment in ELSS funds, then why wait till the last minute to invest?

Reach out to Fauji Wealth to learn more and find which is the best ELSS Fund suited for your specific needs.

View Source:- https://faujiwealth.in/f/elss-funds-sip-or-lumpsum

0 notes

Text

DOES PASSIVE INVOLVEMENT IN YOUR INVESTMENTS HIT THE JACKPOT?

Being in the financial advisory industry for 6 years now, we have observed that there are 2 broad categories of investors:

Wholeheartedly and very actively involved in their portfolio.

Want to make money, but are unable to actually be involved in the process. They mostly outsource the job and are barely able to take out time for their investment-related tasks.

Don’t get us wrong, the 2nd category of investors does want to make money and are wiser than the majority who are not willing to move beyond FDs, but are unable or unwilling to take out time and be sincerely involved in their investments.

So what is the harm right? If one is investing through an advisor, then it is the advisor’s job to do this work. If investors had the time, they could also invest directly, right? So why pay any brokerage? This is where most investors go wrong. Outsourcing the job means it is your advisor’s job to manage your portfolio for you, but holding your advisor accountable for managing your money well is your job. Meaning, creating wealth requires involvement and is not a passive job.

‘Mutual Fund advisory is a parasite business.’

We being in this industry don’t shy away from admitting this. All an advisor needs to do is onboard investors and start their investments, and they start getting the brokerage without having to do anything post that, whether or not the investor makes money. If the investor gets perturbed, they simply say Mutual Funds are for the long term, relax! But in long term, even the worst fund in its category will give investors 12% when the best fund might be giving 30%!

Hence, it is the investor’s job to ask their advisor for:

1. Annual reviews of their investments

2. Annual profit bookings

3. Reason why they are invested in a particular fund over other funds

4. A comparison of different funds in a category

5. Method of selecting funds

We are not saying that one should go overboard with the process. Micromanaging your investments when an advisor is handling them can also become overbearing and intimidating for your advisor, becoming a hurdle in the way of the advisor doing the job right. But not knowing the basics as to why your investor suggests something means your advisor can take you for a ride and make decisions that put the advisor’s interests over the investors’.

Hence, we urge our readers to go on, open their portfolios, have a look at their investments and ask questions from their advisors and check when was the last time their advisor reviewed their portfolio to see if investors' funds were doing well. It is always a good idea to seek a second unbiased opinion to find out how good or bad your portfolio is and compare your funds with their category average since the time you started investing in it. There are multiple websites and advisors offering these services like Advisor Khoj, Money Control, Value Research, etc. Fauji Wealth also offers this service to offer an unbiased evaluation of one’s portfolio. Fauji Wealth has also been able to devise a method that can help investors ensure they stay invested in the best funds, in turn getting the best returns the category has to offer. Stay tuned for further details about the method. Till then, go on and get invested in your portfolio!

View Source:- https://faujiwealth.in/f/does-passive-involvement-in-your-investments-hit-the-jackpot

0 notes

Text

Defence Mutual Funds by Fauji Wealth

Fauji Wealth's Defence Mutual Funds offer a strategically designed investment solution that caters specifically to the needs of defense personnel and their families. With a focus on insightful investment strategies, impressive returns, and meticulous risk management, Fauji Wealth ensures that your hard-earned money is invested competently and securely. Invest in our Defence Mutual Funds to benefit from our specialized expertise and experience in the defense sector, providing you with a reliable and trusted avenue to grow your wealth.

1 note

·

View note