maloofinance

Maloo Investwise Pvt. Ltd.

The mutual fund advisor in jaipur helps evolve a comprehensive plan for all your

life events.

28 posts

Don't wanna be here? Send us removal request.

Last Seen Blogs

usmclpa-blog

USMC Lieutenants' Protection Association

ellie-lovett

ellie

zappner

LOST AND FOUND

livindeadr

PINKY!

daydreamingpastmidnight

Daydreams

Text

Maloo Investwise Pvt. Ltd

Mutual funds are investment vehicles that pool money from various investors to collectively invest in a diversified portfolio of stocks, bonds, or other securities. Managed by professional fund managers, mutual funds offer individual investors a way to access a broad range of financial instruments without the need for extensive knowledge or active management. Investors buy shares in the mutual fund, and their returns are based on the fund's overall performance.

One of the key advantages of mutual funds is diversification, as they spread investments across multiple assets, reducing risk compared to investing in a single security. Additionally, mutual funds provide liquidity, allowing investors to buy or sell shares on any business day at the fund's net asset value (NAV). There are various types of mutual funds, including equity funds, bond funds, and balanced funds, catering to different risk appetites and investment goals.

While mutual funds offer diversification and professional management, they come with fees, such as expense ratios, which cover the fund's operating costs. It's essential for investors to carefully consider their financial objectives, risk tolerance, and the fund's historical performance before choosing a mutual fund that aligns with their investment strategy.

1 note

·

View note

Text

Eight winning habits of successful investors

There is a big difference between knowledge and wisdom. Let us not waste time in differentiating them here, you can refer to a dictionary. One may have all the financial proficiency but still may make appalling decisions when it comes to investment planning. On the contrary, some people are almost zero when it comes to financial literacy, but they make huge profits out of their investments.

Wise investment decisions are habits or behavior. In other words, its wisdom! As per various studies, successful investors have a defined behavioral pattern. Here a few aspects that one can emulate from successful investors to make rich profits out of their investments.

They follow a Well-Defined investment strategy

Most successful investors have well thought of, researched and a clear investment strategy. They divide it based on period, allocation, and never put all eggs in one basket.

Smart strategy leads to investment discipline and long-term gains. Despite all the noises around, a successful investor follows a disciplined investment strategy. Investment strategy serves as their guiding light to traverse in uncertainties.

Emotional Discipline and Critical thinking

It should have been put it in the first place. Lacking emotional discipline means playing in the hands of rumours and tittle-tattle. This leads to wavering thoughts and action. This can stray you from following your investment strategy.

Therefore, successful investors do critical thinking before making any investment decision. For instance, smart investors do not stick to a loss-making investment. It is not like "It was my first house; how can I sell it on loss?'' If there is no long-term positive perspective, if it is bleeding then pull out the money and invest somewhere else.

They keep learning

Successful investors, financial planners are voracious readers. They make a point of learning a new financial aspect, emerging investment options. They do not wait for others to tell them. They keep themselves abreast of the latest.

Regular learning and knowledge upgrading keeps them ahead of others and makes smart profits before others. Learning enables them to avoid repeating a mistake. Remember a famous proverb that a wise man learns from others mistakes.

They are possessive of their assets & wealth

Successful investors know that Money is Power and they not only love to acquire it, they also fight hard to safeguard it. They know that it is their hard earn money. Therefore, they are protective of their wealth.

Now, what does it mean? Being protective does not imply that they pull out swords and guns to fight others. It means that they ensure that their wealth is not eroded due to inflation, market risk or unavoidable exigencies.

They are prepared for all emergencies and carry plan 'B' in case any investment decision goes haywire.

They make their path

Successful investors do not have sheep mentality. They are independent in their thinking and actions. They make their own path. During the first world war, Ghanshyam Das Birla invested heavily in jute capabilities as he figured out that it is the product of the future. Dhirubhai Ambani saw a fortune in petrochemicals. Dhirubhai's elder son Mr Mukesh Ambani found data as the new oil. Hence, when all the other telecom companies are bleeding, Reliance Jio is in profits.

They have the zeal to take the risk and flow against the tides. Shakespeare said that There are tides in the affairs of men when they take head-on, they rise.

They are there to stay

Successful investors think long term. They have a big picture in their mind and are not perturbed of short-term hick-ups. After all, they are they have to play longer innings.

Please remember winning in investments is all about staying for an extended period. They are not in a hurry to become rich overnight. More than making money, they think of creating wealth. Wealth creation leads to the overall development of society. Look at Warren Buffet, he creates wealth, and he does not think twice before doing charity. That is how they achieve their goals.

They are swift movers

Successful investors do not suffer of inertia. They are proactive and never believe in procrastination. They believe in the faster rotation of the money as they are aware that more the money rotates, more they earn. Moreover, they know the advantage of acting in time. For instance, mutual funds, SIP should be plan at an early stage of carrier.

Let's wait here for a bit long. Those who start investing in SIP at a young age, and continue doing for a long per; they have earned higher returns than any average investor.

The mantra is that they do not let their money take rest in the banks, lockers. They put deploy it to achieve their goals. And this makes all the difference in the game. They hate losing money in penalties, fines and unnecessary taxes.

They hate to overspend

They are wise in their spending habits; they hate to over-spend. They are tough negotiators and love drawing the maximum out of every deal. They hate to spend even a penny extra.

Narayan Murthy, the poster boy of that Indian software industry, is known to live his life in a very modest way. Robert Kiyosaki's famous book-Rich Dad, Poor Dad perfectly exemplifies this behaviour. He mentions that a big house, a big car is a liability.

Lesser wasteful expenditure results in higher savings and thus there are higher chances of earning higher returns on the money saved and invested.

Is not Warren Buffet right when he says that Expenses= Earning-Savings?

Though there are many other aspects too, I have tried to cover some of the behavioral patterns of successful investors and hope you will learn a bit from it. Remember to make your best moves when it comes to investment planning.

#Investment planning#mutual fund#investment financial advisor#financial planning#mutual funds#mutual funds in jaipur#investment advisor

2 notes

·

View notes

Text

low-income-financial-plan

Low income, unplanned decisions and unrealistic goals are relatively common among middle-class households. When SEBI registered fee-only financial advisor Preeti Zende discussed the budget for a few with kids, many readers were in disbelief – how can we invest such a lot for such financial goals?

Preeti Zende may be a SEBI Registered investment adviser (RIA) and Fee-only Financial Planner based in Navi Mumbai India. She is an Associate of Insurance Institute of India (AII) and features a post-graduate Diploma in Business Finance from ICFAI university. She also holds a Masters’s degree in Commerce from Pune University.

Preeti was related to the Insurance and Finance industry for long and having experience in both administration and marketing of monetary products. She had worked as a Medical and Nonmedical Underwriter and was heading a top quality check team in Reliance life assurance Company. She also worked with ICICI Prudential life assurance Company’s sales and marketing team. you'll contact her via her website, Apanadhan.

As financial planners, we encounter many sorts of clients. Some are earning well, and a few are from medium earning group, some are with double income, some are the sole earners in 6 relations , some are conservative investors, some are very aggressive investors, some are confused about life goals and a few are very focussed and well prepared. Some are very cooperative, and few are rigid.

Financial Planners in jaipur don't just plan your finances, but they work more on the client’s behavioural and psychological pattern towards Personal Finance and life too.

What are the priorities of a financial planner when a client approaches them? to form them understand the importance of identifying their life goals and plan their investments accordingly.

Sadly this process isn't straightforward. When clients pen down their life goals and aspirations, repeatedly , there's a mismatch. Therefore we'd like to priorities.

Some of you'll have seen the reactions to my previous article of designing education and marriage for youngsters . The case discussed of Ventakesh and Latha, got many comments about the high monthly investment required for teenagers education and marriage planning. therein case, that couple was earning well, and that they could afford to allocate that much amount for teenagers education and marriage planning as their other life goals were set.

This is not the case for several middle-class Indian families. Parents do want to offer best to their kids, but this relies on our income. If our finances permit, we will fulfill those and feel relaxed, but if not, then what can we do? What can a financial Advisor neutralize such a situation?

she can provide a rosy picture to the client and convey them that “All is Well “now and “All are going to be better tomorrow” or are often fair with them and make them understand the important situation and supply the answer accordingly.

The first way is quite easy. Everybody wants secure solutions and assurance that things will always be favorable. How can this picture be created?

Prioritize life goals: Give priority for retirement planning over the other goal. After retirement kid’s education and marriage planning goals, house purchase, car purchase goal, and dream vacations etc. are often accounted for.

Invest within the proportion of the priority and urgency

Study your spending pattern: once we can’t invest the specified amount to fulfill our goals what we will do? we've two options: spend less or earn more. we'd like to figure on both options. While studying our spending pattern we will put needs over wants. Pen down each expense or track the typical of six months expenses, etc.

Save first spend later: this may help to extend saving as you'll fix your monthly saving percentage and achieve it.

Make a monthly budget: Budgeting helps to be disciplined in spending and any impulsive spending are often curbed.

Be content and find real happiness in experiences instead of things: If we start moulding our mind towards happiness we are deriving from the experiences, our desire to spend on material happiness will go down. this may help in increasing our savings.

Focus on secondary/passive income: during this times , there are n numbers of excellent options available to earn a secondary income. Explore them. specialise in those during which you've got interest and knowledge. Use your overtime to earn this income which can assist you all achieve all those dreams and aspirations you've got in mind.

Upgrade your skills and knowledge for a far better prospect.

It was not hard to convince Prashant and Sneha to figure on these aspects. We mutually derived the subsequent points on which the budget was based.

Financial Planning in jaipur may be a lifelong dynamic process. we've to stay reviewing our financial situation periodically, make necessary changes in our corpus requirement from time to time consistent with the change in our income and expenditure, family responsibilities, market returns etc and see how we will achieve all our dreams in our lifetime.

mutual fund in jaipur, Tax planning in jaipur

#investment planning#investment advisor#mutual fund advisor#mutual fund advisor in jaipur#investment advisors#investment planner#mutual fund in jaipur

1 note

·

View note

Text

When it comes to investment, why do you need a financial planner?

Before we deep dive further to understand why do you need a financial planner, answer this question. While going on a flight or a train, did you ever go to the pilot or loco driver and said that you today you will be in the cockpit or run the train? It’s no point waiting for your answer. These are the specialist jobs & you aren’t trained for them. Similarly, when it comes to financial planning we all think that since we earn money, so we know how and where to park it for future use.

But, hold on, this is far from reality. Earning and managing money are two altogether different aspects. You need a specialist as it’s a complicated world and he is called a certified financial planner. Financial planning is not as simple as it seems. Sound financial planning and a certified financial planner are the same sides of a coin! So let’s understand how a financial advisor in jaipur helps you with financial planning?

Helps you in setting your financial goals

Depending on your financial income, age, and requirements; there are three types of financial goals-Short, Medium, and Long term. Similarly, the requirements can be of an individual or family. For instance, your vacation plan can be a short or medium-term goal, the education of your child is a long term plan. Financial Planner helps you in deciding your goals and also assist you in revising them according to your requirements.

Educate you on risks and rewards of various financial options

There are hosts of financial options available. To name a few are fixed deposits, stocks & bonds, Insurance products, and Mutual funds. For instance, a certified financial planner will always guide you to go for SIP as it is a wonderful tool for maximizing returns in the long term. He has read & analyzed the financial market and knows the importance of SIP and mutual funds.

A good financial advisor is well versed with all the options available. He understands that which financial products will suit your particular goal. With his knowledge, he does the financial planning and analysis of your portfolio

Helps you in selecting the right investment portfolio

The financial planner is adept in portfolio management service. In other words, he does asset allocation. Let’s understand this by an example. You have 10 years to get your daughter married & you are not clear whether to invest in equity or in debt. The intelligent financial advisor will always give you a solution that is in consonance with market conditions. He may advise you that up to 8 years, you park money in equity and for the next two years, in the debt.

Saves your time

This is the world of specialists and one becomes specialists with years of practicing. A financial planner saves a lot of your time. He has put her number of years in learning financial markets and products that can give you higher returns. He has developed financial wisdom to share with others. Therefore, be wise; leave it to the financial advisor to decide on your behalf.

Monitors portfolio and interprets the performance

Your portfolio typically consists of following investment options- Real Estate, Precious Metals, Stocks, Bonds, Fixed Deposits, and Mutual Funds. Since the market is dynamic, so are these options and as a result, the returns vary. Hence it becomes imperative that your portfolio is reviewed regularly. Financial Consultant’s prime objective is the portfolio management service in Jaipur. He keeps a tab on it and fiddles with it as per the need so that the risk is minimized, investment is diversified and returns are maximized.

Saves you from making emotional financial blunders

This can be understood from a very simple example. Let’s say you have invested through SIP an ‘X’ amount of money in the pension funds for your later years. After two years, you realize that the market behaved badly and your net fund value has become negative than what was invested. Out of desperation, you would withdraw the entire amount and hope for a fixed return, you park the same in fixed deposit.

The financial advisor would stop you from making this decision as he knows that in fixed deposits the rate of interest would slide further and insist you keep investing in a pension fund or opt for some other financial products. Thus, he saves you from making such blunders and your money too.

Summary

The financial planner is your friend in a true sense as she makes you financially sound by taking care of your finances and investment & help you realize your financial goals. Whilst, you leave at her discretion to make a financial investment decision, you also learn the basic nuances of financial planning.

Learn to have patience, be willing to take a calculated risk, and believe that in life the purpose of money is not just earning but investing wisely spending prudently and enjoying it fully. Therefore friends, enjoy the flight or train journey and leave it for the pilot or loco driver to take you to your destination.

Mutual fund advisor in jaipur

Original Source: https://www.mftoday.com/when-it-comes-to-investment-why-do-you-need-a-financial-planner/

#investment planning#best mutual funds financial planning investment cunsultant mutual fund advisor in jaipur Mutual Fund Consultants in Jaipur mutual fund inves#investment#mutual funds#financial planner#financial advisor#financial planning#mutual fund advisor

1 note

·

View note

Text

Catch The Falling Knife During Corona Crisis

Historically, the India SENSEX reached an all-time high of 42,273.87 in January 2020. However, it lost 16,292.63 points or 38.5% since then when it recorded it its lowest value of the quarter on 23 Mar at 25,981.24. In the month of March 20, it recorded its second double-digit fall of -13.15%, after it recorded the first double-digit fall of -10.96% on 24 Oct 08. On March 20, it also recorded the other two highest falls so far from -8.18% and -7.96%. Nevertheless, the question remains whether the investor wants to catch the falling knife? For an investor, a falling knife is a sharp drop in the market. However, the bottom and the duration of the drop is not known to him. Therefore, the investor uses the falling knife with caution and does not invest in the market during a drop.

A careful study of the 25 major Sensex drops since 2006 reveals a positive outlook for the investor to capitalize. He must carefully study the fall and not form a biased opinion due to the large points change in the value. Instead, he must focus on the percentage change from the fall. In the table below, it is evident that the largest points fall of March 20 was not the largest percentage fall. The fall of October 08 changed the market perceptibly and to date stays the largest percentage fall in history. The other aspect of relevance is that even after the 25 falls in 14 years since 2006, the Sensex has climbed almost 5½ times from its lowest value of 7,697.39 on October 08 to its highest value of 42,273.87 on January 20, i.e. 11¼ years. Next, is the point regarding the duration of the Sensex reclaiming and moving beyond its previous closing value in these falls. Table 2 below indicates 10 of the 25 major fall instances since 2006. The duration of these 10 falls subsumes the remaining 15 other instances of fall. A significant point that emerges from this table is that the duration of the Sensex reclaiming and moving beyond its previous closing value varies from 2 to 36 months. The average duration of these 10 major falls is 13.5 months or just above a year.

Table 1: Major Sensex Falls

Although the markets are volatile and unpredictable, yet one thing is clear and that is their recovery with time. If an investor has a long-term perspective, then he must try and catch the falling knife since most of the stocks are trading close to their historical/52-week lows. For mutual fund investors, fiscal prudence lies in topping up their existing schemes through top-up SIP/STP or investing additional lump sum amount so that they make the best of this market fall and its associated uncertainty.

able 2: Sensex Reclaiming Previous Closing Value

Financial planner in Jaipur, mutual fund company in Jaipur, Best Mutual Fund Advisors in Jaipur

Original Source: https://www.mftoday.com/catch-the-falling-knife-during-corona-crisis/

#financial planning companies in jaipur#financial planner in jaipur#certified financial planner in jaipur#Financial investment services in jaipur#mutual fund advisor in jaipur#Investment Consultant in jaipur#Investment Advisors in Jaipur#Finance and investment companies in jaipur#Mutual funds in jaipur#Financial Planning in Jaipur#mutual fund company in jaipur#Mutual Fund Consultants in Jaipur#Best Mutual Fund Advisors in Jaipur

1 note

·

View note

Text

Ten reasons why financial planning is vital

Financial planning helps you identify your short and long-term financial goals and make a balanced decide to meet those goals.

Here are ten powerful reasons why financial planning – with the assistance of an expert financial advisor – will get you where you would like to be.

Income: It's possible to manage income more effectively through planning. Managing income helps you understand what proportion money you will need for tax payments, other monthly expenditures and savings. We can invest our saving part of income in mutual funds through mutual fund advisor.

Cash Flow: Increase cash flows by carefully monitoring your spending patterns and expenses. Tax planning, prudent spending and careful budgeting will assist you keep more of your hard-earned cash.

Capital: a rise in income , can cause a rise in capital. Allowing you to think about investments to enhance your overall financial well-being.

Family Security: Providing for your family's financial security is a crucial a part of the financial planning process. Having the right coverage and policies in suit can provide peace of mind for you and your loved ones.

Investment: a correct budget considers your personal circumstances, objectives and risk tolerance. It acts as a guide in helping choose the proper sorts of investments to suit your needs, personality, and goals. an investment advisor can help you to planning your investments.

Standard of Living: The savings created from good planning can prove beneficial in difficult times. for instance , you'll confirm there's enough coverage to exchange any lost income should a family bread winner become unable to figure.

Financial Understanding: Better financial understanding are often achieved when measurable financial goals are set, the consequences of selections understood, and results reviewed. supplying you with an entire new approach to your budget and improving control over your financial lifestyle.

Assets: A pleasant 'cushion' within the sort of assets is desirable. But many assets accompany liabilities attached. So, it becomes important to work out the important value of an asset. The knowledge of settling or canceling the liabilities, comes with the understanding of your finances. the general process helps build assets that do not become a burden within the future. you can find best investment advisor company for your financial planning.

Savings: It wont to be called saving for a time period . But sudden financial changes can still throw you astray . it's good to possess some investments with high liquidity. These investments are often utilized in times of emergency or for educational purposes.

Ongoing Advice: Establishing a relationship with a financial advisor you'll trust is critical to achieving your goals. Your financial advisor in jaipur will meet with you to assess your current financial circumstances and develop a comprehensive plan customized for you.

The first step in developing your budget is to satisfy with an advisor. At Maloo Investwise pvt. Ltd., we use our unique discovery and assessment process called lifespring. This complimentary process begins with a review of your current Portfolio, anticipated changes, future goals, and leads to your customized plan. Call us today to book your assessment at 98290 40524, 8287 099 099

#financial planning companies in jaipur financial planner in jaipur certified financial planner in jaipur Investment Advisors Financial inves#financial planning companies in jaipur#financial planner in jaipur#Investment Advisors#Financial investment services in jaipur#mutual fund advisor in jaipur#Investment Consultant#Investment Consultant in jaipur#Investment Advisors in Jaipur#Finance and investment companies in jaipur#Financial investment services#Tax planning services in jaipur#Financial Planning in Jaipur

1 note

·

View note

Text

Investing For a Child Education is Better than Taking the Loan for the Same

Education is one of the best levers to make this world a better place. Famous entrepreneur and CEO of Apple Inc. Steve Jobs once said, “The best thing that could happen to me was that my parents had put me in a school.” From Thomas Elva Edison to Albert Einstein and from Mark Zuckerberg to Bill Gates, all of them had credited education for their success.

In India, primary education is a fundamental right. It implies that the Government is bound by the constitution of the country to provide free education for the children of the age group of 6 to 14 years. Before the other Indian States catch up with the standards of New Delhi’s Primary education, you have to rely on private education. Similar is the scenario in Graduation & Higher education.

No doubt, every parent wants the best education for their children, but the costs are a major concern. The best school in your city may remain a dream. The same can be true about the graduation college, maybe your child has a dream to be a graduate from a foreign university and he qualifies for that too. What if you don’t have enough money to fund his/her education? This can destroy the entire career of your loved one. These are several milestones that you have to cross to shape your child’s future, and planning for their education in the best possible way is the one among them.

Here are a few steps that you can follow to plan your child's Education and Future.

1. Remember the important milestone dates

2. Evaluate the current cost of education.

3. Decide the amount that you would like to spend.

4. Calculate the return you can get.

5. Calculate your monthly contribution.

Steps to Achieve Your Financial Goal

Buy an insurance policy

Only if you are healthy, you can work towards your child achieving her dreams. Therefore, first, think of yourself. You should buy a health insurance policy. There are two benefits of it; first, it keeps you fit for your family and second, it doesn't let you burn your savings. Health insurance policies are tax saving options too.

Start Saving Early

No one can beat the early birds. The sooner you start saving for your kid(s), the better it is. The whole idea is to create sizeable equity as per the requirement calculated. Make sure the savings amount is in direct proportion to salary. Factor-in the inflation. It will ensure that when your child enters college education, you have the requisite funds.

Choose the right investment portfolio

it's not about savings; it's also about the parking of funds in the right investment matrix plan. Here are a few options that you can think of while saving money for your kids' education.

Mutual Funds

They are one of the best instruments to see your money multiplying. Often the investors think that investing in mutual funds is short term investment plans. No, it isn't the case. Mutual funds are long term investment options. Often investors assume that mutual funds are short term investment plans. No, it isn't the case. They are long term investment options. Child Education Planning In Jaipur is a very important part of your Financial Planning.

ULIPs

Unit Linked Insurance Policies (ULIPs) provide security cover and offer the potential for wealth creation. In ULIPs, a part of the premium is parked towards your Life Cover and the rest is invested in various market-linked equity schemes. The returns on your investments depend upon the performance of the funds opted. Through ULIPs, you can save substantial money for your kids' education. One should plan it in a manner that on important milestones in your kids' life, you get payback from them.

Term Insurance

Imagine the plight of a family that loses its earning member before he/she could fulfill the responsibilities like kids education, marriage, or taking care of spouse in the old age. In such cases, Term Insurance provides the much-needed support to the family of the policyholder as it receives the entire sum assured as opted by the policyholder. Opting for the term insurance at an early age has many benefits. The entire family gets an umbrella of financial security, & the premium is less. Therefore, Term insurance is one of the most advised solutions in case of any eventuality.

PPF for Your Child

Public provident fund (PPF) It is one of the time tested instruments to save money for your kids' education. PPF has a 15-years lock-in-period. However, you can also withdraw partially the amount after the sixth year from this account. One more benefit of this plan is that when your child becomes adult they can also contribute to the same account. One can opt for it from a post office or any bank. It enables you to create tax-free savings for your kid’s future.

Summary

The part of life's uncertainty can be met with a solid action plan. Let money not pose any hindrance to your child's education. Whichever investment matrix you choose, just on having a regular look on it. Keep watching the fund’s performance; take the advice of your financial planner in Jaipur, he is the best guy suited for it. Often people advise taking bank loans for children's higher education. This can be another option. However, it should be the last resort. Plan to use your own funds & for that, save regularly. It is like seeing the seed turning into the tree.

For more Details: https://www.mftoday.com

Call Us At: 98290 40524, 8287 099 099

#inves#best mutual funds financial planning investment cunsultant mutual fund advisor in jaipur Mutual Fund Consultants in Jaipur mutual fund inves#mutual funds#financial planning#investment planning#financial advisor#financial planner#financial investment advisory

1 note

·

View note

Text

7 Steps in Financial Planning in life

Who hasn't heard of Gucci? The Italian Fashion Giant that revolutionized clothing concept in the world. Like any other family, Gucci's too had internal disputes & they were out in the street. Since it came from a reputed family, tabloids sneaked into the Gucci kids' lives. In one of the interviews, one of the daughters-in-law of Gucci's told that everybody in the family was fighting with others in the family. Sometimes I used to feel like crying while walking on the streets. I would fear that people walking would see me doing so. Thank God! I had a car to seek some privacy. She went on to say if at all you have to weep it's better to do so in the car then out in the street.

The whole objective of this story was not to tell you about Gucci's. But to make a point that money saves from embarrassments. For many centuries Indians learnt from mythologies that lots of money is taboo. As we Indians are gradually coming out of the concept of "money is bad', our thought processes have started to change. Now we not only earn, we like to flaunt.

Hold yourself; remember what Robert Kiyosaki mentions in 'Rich Dad Poor Dad'. He writes that income from investments should meet out the monthly expenditure & let monthly income be invested. The game is to have sound financial planning in Jaipur.

Here are a few simple steps that can be followed.

Make Saving a Habit

You do regular exercise to remain fit. Similarly, savings should be part of your daily curriculum. Is this weird? Yes, it is. Think of saving daily from what you earn daily. Cut down from daily expenses that are unworthy.

Take an example- Mr X smokes a particular brand of a cigarette priced @15 per piece. If he smokes 10 per day, monthly expenditure is INR 4500, yearly is 54000 and if he continues doing so for a decade, and even if we forget every year inflation, he would have spent 5,40,000.

Another way of looking at it. 150 rupees saved daily for 10 years could have given him 5,40,000 after a decade! Investments are like sowing a seed to have a tree in the future.

Start Investing Early

It matters. Warren Buffet, The Oracle of Omaha, proudly mentions that at 11 he purchased his first stock and he regrets that he started late! When you start doing something at an early stage, you have an ample amount of time to manoeuvre. However, that doesn't mean that you should not do in later stages if you haven't done early.

Invest for the long term

As much as this may sound clichéd; it’s a fact that is hard to ignore. Every damn financial advisor in jaipur cries out loud to his/her investors that come-on, save for the long term. But there are hardly a few that pay any heed to this advice.

Look how the Sensex has moved. From 5,491 on Jan 4, 2000, to 17,558 on Jan 4, 2010, and was 41,464 on Jan 4, 2020. Where it head? The obvious answer is North. Look how Rakesh Jhunjhunwala makes moolah out of the stock markets.

Never Put All Eggs in One Basket

In the gig economy, diversification of skills has become the norm of the day. Likewise, business cycles have shorter life spans. Investments have to spread out. Choose wisely from available options and park some amount in each. Trust, you will be benefited. To relate it to health. Spreading out investments are like having a balanced diet.

Plan for retirement

While one can achieve almost every life goal with the help of a loan; your retirement is something that you need to work on.

Look at the double whammy- Due to medical science, you will live longer. Corona Virus or other stupid viruses will not bring an end to this world but inflation will eat up your income.

Moreover, don't rely on kids to take care of you when you are old. Let's be honest. They will have priorities like their lives, their family and so on so forth.

Planning for retirement is not a mystery; You have to start saving now for your rainy days.

Post the retirement, when the regular income flow in the form of salary is stopped, one should have enough money to take care of self and Finfalso enjoy during that period. Make sure you start saving for retirement from the time you start earning.

Take an Insurance

The point is why do you need it? Medicare cost is increasing year on year. It rises the fastest in comparison to other items like food or clothing.

The problem of bearing the cost is more for someone who doesn't have a high income or who hasn't saved it for such exigencies. As the age progresses, the frequencies of paying visits to doctor or hospital increases. Moreover, old age is prone to critical illness- something that requires a lot of money to be parted away.

Hence, health insurance plans provide much-needed support during these times.

Need a good advisor

You are not a hero in any Bollywood film where you dance with your girlfriend, fly an airplane to take her to romantic locations, fight with 20 goons to save her, fire from Bofors to destroy terrorists’ launch pads. While you are doing all these you are a chairman of a big company and you are just 20!

The fact of the matter is in real life you don't take paracetamol without consulting a doctor. So you need a specialist.

But is being a specialist sufficient? Imagine, if you come to know that the airplane you've boarded to travel over the Atlantic Ocean will be flown by a solo pilot. And that too, he is a lad who's just passed out of flying college & this is his maiden flight. What would you do? Sure you will jump out of the plane before it takes off. Likewise, would anyone like to go under the blade of a fresh surgeon?

There comes the importance of experience. Therefore, leave your financial matters to be handled by a good investment advisor in Jaipur. He's been doing it for many others and he is been doing it for ages.

Select an advisor who has the experience and meets your needs. Word of mouth references are a good start, but you could also check their credentials to ensure you are engaging someone with training and experience.

In the end, life is simple and let it be run by simple rules. Don’t make it complicated, work hard, be honest to this world. And when you have earned and saved, think of giving back some part of it to the society.

#investment#investment advisor#investment consultant#investment advisors#investing#property investing#finan#financial planning#best financial planner#best financia

1 note

·

View note

Text

Why Insurance Is One Of The Most Critical Levers Of Financial Planning

When it comes to financial planning in Jaipur there are various options to choose from. There are a few who believe that investing in land or creating a fixed asset is the best option. Then there are a set of people who put money in buying precious metals and there are who believe in stocks and securities. Lastly, people even balance out between all the above options.

Insurance is also one of the ways to do Health Financial Planning. There are some critical aspects of it- Health insurance planning and Term insurance planning. Let’s understand all of them.

Health Insurance

Health insurance is an insurance product that covers medical and surgical expenses of an insured individual or the family. It reimburses the expenses incurred due to illness or injury or pays the care provider of the insured individual directly.

The point is why do you need it? Medicare cost is increasing year on year. It rises the fastest in comparison to other items like food or clothing.

The problem of bearing the cost is more for someone who doesn’t have a high income or who hasn’t saved it for such exigencies. As the age progresses, the frequencies of paying visits to doctor or hospital increases. Moreover, old age is prone to critical illness- something that requires a lot of money to be parted away.

Hence, health insurance plans provide much-needed support during these times. These days, health insurance plans offer considerable flexibility in terms of disease and ailment coverage.

One should choose the insurance plan that covers as many critical illnesses and surgeries. Also, one should choose to opt for the plan that offers the cashless hospitalization or medication. This largely depends on the premium paid per year. Otherwise, one can choose the fixed payment plan that is regardless of the actual cost borne during hospitalization. The good part of the health insurance policy is that it continues even after the benefit payment on selected illnesses.

Therefore, with health insurance, one is secured both health-wise and money-wise. In most of the families, the earning member takes health insurance policy. The ideal is that one should keep the entire family safe.

Term Insurance

To understand why we need to go for term insurance, let’s know what term insurance is? It is an insurance product, which offers financial coverage to the policyholder for a fixed time period. In other words, if a policyholder dies during the policy term, the nominee of the deceased is paid the sum assured amount. It’s imperative to know the key features of any term insurance policy, before buying it.

For most, term insurance is still something ‘not required’ types. Because most of us tend to believe that we will not get affected by any critical illness. But, one cannot be sure of anything in life. After all, the human body is just a machine only and at any point in time it can become faulty and some serious illness can claim life. God forbid it happens. But it can happen.

Imagine the plight of a family that lost its earning member before she or he could the basic responsibilities like education, the marriage of kids or taking care of the spouse in times to come! In such cases, Term Insurance provides the much-needed support to the family of the policyholder as the family receives the entire sum assured as opted by the policyholder.

Opting for the term insurance at an early age has many benefits. Most importantly, the family is provided with an umbrella to cover them and secondly, the premium is less. Some important key features in term plan can be larger life cover, riders, and enhanced coverage.

Original Source: https://www.mftoday.com/why-insurance-is-one-of-the-most-critical-levers-of-financial-planning

#investment#investment advisor#investment advisors#advisor'#Financial Advisor#mutual funds#mutual fund advisor#mutual fund advisor in jaipur#financial planner#financial planning

1 note

·

View note

Text

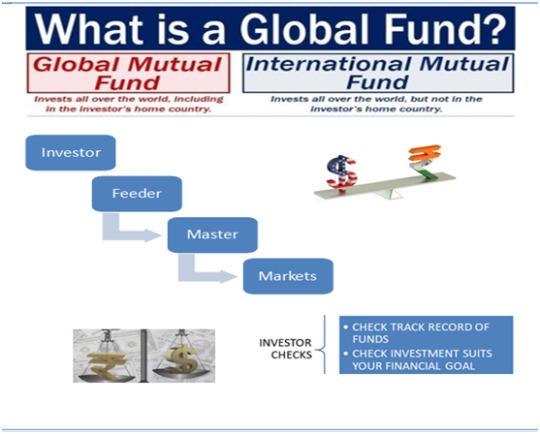

Go International in Your Mutual Fund Investment

A retail investor is bemused when he hears Dow Jones, NASDAQ or Nikkei. Dow Jones Industrial Average (DJIA) is an index that tracks 30-large, publicly-owned companies trading on the New York Stock Exchange (NYSE) and the NASDAQ. The DJIA, commonly referred to as Dow Jones, gets its name from Charles Dow, who created it in 1896, and his business partner, Edward Jones. Originally, NASDAQ was an acronym for the National Association of Securities Dealers Automated Quotations. It is now the second-largest stock exchange in the world by market capitalization, behind only NYSE. NASDAQ Composite is the stock market index of the common stocks and securities listed on the NASDAQ stock market. It is one of the three most-followed indices in US stock markets, the others being the Dow Jones Average and Standard &Poor (S&P) 500. Closer home in Asia, the SSE Composite Index is also known as SSE Index is a stock market index of all stocks that trade at the Shanghai Stock Exchange. Nikkei is short for Japan’s Nikkei 225 Stock Average, the leading and most-respected index of Japanese stocks. It is a price-weighted index composed of Japan’s top 225 blue-chip companies traded on the Tokyo Stock Exchange. The Nikkei is equivalent to the DJIA index in the United States. A latent ambition of any retail investor is to invest in markets abroad so that he can reap their benefits. However, it is not everybody’s cup of tea to track these markets or understand their investment nuances. An easier and simpler option available to investors is to take the mutual fund (MF)route, which professional fund managers maintain, but come with their own pros and cons. Nevertheless, on the part of the investors, this does not imply complacency and overreliance on the wisdom of the mutual fund advisor in jaipur or fund manager. An investor will do well to correctly formulate his financial goals before venturing towards foreign markets and thereafter continually track his investments.

An international MF helps the investor to invest in companies abroad and some people also refer to them as overseas or foreign funds. They help an investor to benefit from the growth stories of other developed or developing economies. These funds come with chances of higher returns; thus, they also carry the associated higher risk. Ipso facto, investors use them as an alternative investment with a long-term horizon and invest only 10 to 15% of their net worth in these funds. Over the medium and long-terms, an investor can also benefit from the depreciating value of rupee by putting some money in an international fund that further invests it in dollar-denominated assets. It also helps the investors to diversify their portfolios by spreading their risks while simultaneously taking advantage of the growth or earning potential of other markets. These funds can also help an investor to hedge against currency fluctuations if his financial goal is to teach his child or go for a vacation abroad. Investing in international funds is now more lucrative. Simply because the government treats all investments in international funds as debt investments and accordingly taxes them at 20% with indexation for LTCG and as per the investor’s income tax slab for STCG.The various types of funds that help you to invest in foreign markets are – international, global, regional, country, commodity, and global sector. Typically, international MFs invest in foreign markets except for the investor’s country of residence. On the other hand, global funds invest in foreign markets as well as the investor’s country of residence. We can further classify the international MFs into the emerging market or developed market funds. The emerging-market funds invest in emerging markets like India, China, Russia, Brazil etc and reap the benefits from the respective country’s growth story. On the other hand, developed market funds primarily invest in developed and mature economies and thus offer stability. The emerging-market funds are riskier than the developed market funds because of their inherently unstable economies, currency risks and in certain cases the prevalent internal political turmoil. Another point that comes to mind is that most of these funds have a small asset size of less than 100 crore and funds with low AUM may suffer from the pressure of large redemptions due to any of these risk factors. Wealth creation in Jaipur An investor will invest in a geographic region or specific country through regional or country funds respectively. The commodity and global sector funds help the investor to either invest in specific commodities like gold, precious metals, crude oil or specific themes like infrastructure, real estate, or pharmaceutical abroad. Some international funds follow the direct route of investment in foreign stocks, while some take the more diversified approach to invest in indices such as the S&P 500 or NASDAQ. The modus operandi of investment is that of a feeder and master, where the domestic fund acts as the feeder to its international master mutual fund.

A word of advice for the investors is to follow the basic investment rules that they follow while investing in domestic mutual funds. They must invest as per their quantified financial objective based on their risk profile and net worth. They need to track their investments and not leave it on autopilot with the financial planner in jaipur or fund manager. They should be pragmatic in their approach and not let their emotions rule their investment sense. The investor will do well to remember that time is his friend and impulse his enemy. The investor must seek sound financial advice and avoid self-investment that may prove perilous, much the same way as self-medication proves deadly.

A cumulative performance chart below, generated from our research software, shows that international funds category (S&P 500) has outperformed domestic funds category (S&P 500 BSE) through all time horizons. The table below also gives out the simple averages of various stock market categories.

Investment Advisors in Jaipur , Financial Planning Companies in jaipur

Original Source : https://www.mftoday.com/go-international-in-your-mf-investment/

#financial planning companies in jaipur#financial planner in jaipur#Investment Advisors#mutual fund advisor in jaipur#Investment Consultant in jaipur#Finance and investment companies in jaipur#Tax planning services in jaipur#Financial Planning in Jaipur#Wealth creation in Jaipur#mutual fund company in jaipur

1 note

·

View note

Text

FINANCIAL ADVISERS BRING A LOT TO THE TABLE

A person suffering from an ailment or involved in a legal wrangle seek a doctor or a lawyer for professional help. However, if he must invest his hard-earned money then he will shy away from seeking a financial adviser. A financial advisor in jaipur is a professional who provides financial guidance to clients based on their needs and goals and helps manage their money including investments and other accounts. There are two types of advisers: Fiduciaries are the ones who charge a fee for their advice and holds assets in trust for a client; the others are distributors who earn commissions from the products they sell to their clients. Then there are financial planners who are professionals helping companies and individuals create a program to meet long-term financial goals. In India, due to the proliferation of the financial industry, the same entity performs the dual task of planning and advising the clients. Financial Planner in Jaipur choose investments for a client by assessing the investor’s tolerance of and capacity for risk. Often, a person seeks a financial advisor after suffering a loss of investment, or due to a windfall of capital, or for his need to save for retirement. As per the third CFA institute investor trust study report, 70% of Indian investors hire professional advisers vis-à-vis 54% globally.Why does one require a financial advisor in today’s digital world? After all, so much information

is freely available on the net and number offer-based Robo-advisory services have also sprung up in the market. Nevertheless, self-investing is as harmful to your financial well-being, as for the health of the people indulging in self-medication after researching on the internet. Although there is a lot of data and information available in the public domain but is it enough for the investor to take prudent financial decisions? Data available on the internet is raw, unorganized facts. When somebody processes, organizes, structures, or presents this data with reference to a context, it becomes information. Both data and information are freely available and easily accessible on the internet. However, the retail investor lacks the experience and insight to combine with this information, which we term as knowledge. When the individual applies this knowledge to discern and makes good judgments about what is the right thing to do in a situation, he has then gained financial wisdom. The ancient Greeks called this ‘practical wisdom’ as Phronesis.Recently, I read an article by Radhika Gupta, CEO Edelweiss Asset Management Limited, where she imaginatively coined an acronym PEACE. She discusses that the financial adviser brings peace and comfort to the client. The acronym PEACE per se had the following important elements:

Trust and service are the two most important facets of any adviser-client relationship. It takes time for an mutual fund adviser in jaipur to reach the stage where his client starts trusting him. To do this, the adviser must provide detached and candid advice that is always and every time for the betterment of

the client. On the other hand, the client must learn to rely on his adviser through good and bad market times. In today’s time, service plays an equally important role in fostering the adviser-client relationship. ( Finance and investment companies in jaipur) To provide quality service, the adviser must use technology for the portfolio management of his clients, generating timely reminders to them about impending investments and withdrawals, initiate properly vetted periodic portfolio reviews to the clients, provide value-added services through online portals and mobile apps, enhance digital outreach through innovative and targeted use of social media. certified financial planner in jaipur

Original Source:

https://www.mftoday.com/financial-advisers-bring-a-lot-to-the-table/

#financial planning companies in jaipur#financial planner in jaipur#certified financial planner in jaipur#Investment Advisors#Financial investment services in jaipur#mutual fund advisor in jaipur#Investment Consultant#Investment Advisors in Jaipur#Finance and investment companies in jaipur#Financial investment services#Tax planning services in jaipur#Financial Planning in Jaipur#Wealth Creation companies in jaipur

1 note

·

View note

Text

Importance of side pocket in debt mutual funds

SEBI, the mutual fund regulator, tightened its mechanisms, since the global financial crisis of 2008, to ensure fair treatment to all unitholders in case of a credit event through various orders like modification of its valuation guidelines and restrictions on redemption in mutual funds (Redemption Gate). The recent defaults on debt obligations by a few entities particularly in September 2018 and subsequent volatility in the debt and money market instruments issued by NBFCs and HFCs resulted in redemption pressures in debt mutual fund schemes, more specifically in liquid schemes. An analysis of Asset under Management (AUM) of all debt-oriented schemes indicates that their AUM declined from ₹ 12.13 Cr to ₹9.9 Cr over a period of two months with effect from 31 Aug 2018 i.e. a decline of around 18%. The Indian bond market has relatively lesser depth and width than developed markets that permit side pockets of non-retail funds. More so, Indian mutual funds that invest in debt and money market instruments face liquidity constraints in case of credit events, since trading in those securities freezes, as seen recently. With this as the backdrop, the SEBI permitted side pocketing of debt mutual funds and money market instruments in all mutual fund schemes, at the discretion of the fund house, on the day of the downgrade of a debt instrument to below investment grade or on the day of each subsequent downgrade from below investment grade.

Side Pocketing is a mechanism to separate distressed, illiquid, and hard-to-value assets from other more liquid assets in a mutual fund portfolio. This prevents the distressed assets from damaging the returns generated by more liquid and better-performing assets. To side pocket, the fund house generally creates a separate portfolio of distressed, illiquid, and hard-to-value assets and declares separate NAVs for this portfolio. Each investor is allocated his/her pro-rata share of units in the side pocketed portfolio. The rules do not permit redemption or subscription in the bad asset portfolio. When the bad asset recovers, the side pocketed portfolio also recovers and the fund house distributes the profit amongst the investors on a pro-rata basis.

The distinct advantage of side pocketing is that it offers investors the benefit of selling liquid investment and staying invested in risky funds until they generate profitable returns. It also prevents a new investor from taking undue benefit from the investments of a previous investor. Further, it mitigates the risk accompanying the credit-risk investments. One big disadvantage is that the fund house may find it difficult to determine the NAV of the liquid or defaulted assets since their valuation remains contentious.

mutual fund advisor in jaipur

financial advisor in jaipur

original source: https://www.mftoday.com/importance-of-side-pocket-in-debt-mutual-funds/

#mutual funds#MutualFundInvestments#mutual fund advisor#mutual fund#mftoday#financial investment services#investing#investment advisors#planning#best financial planner#investmentplanning

1 note

·

View note

Text

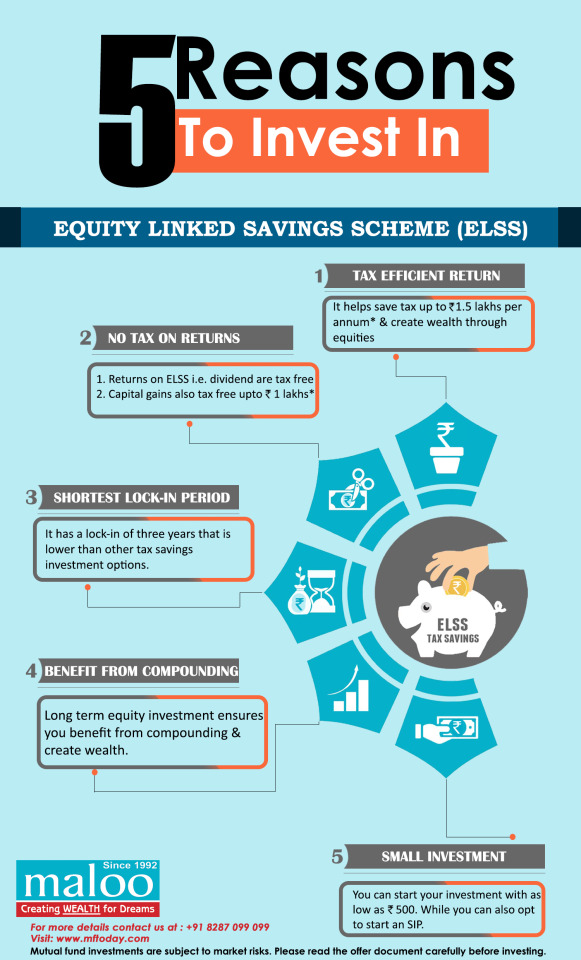

What are the advantages of investing in ELSS?

Financial planning is of utmost importance and has become a dire necessity in times. regardless of what proportion you earn, it’s important to save lots of and invest in order that you'll aim to realize your financial goals. Now, what if we tell you there’s an open-end fund scheme that saves tax & helps you create wealth too? Yes, you heard it right. Equity Linked Saving Scheme or ELSS is one among such scheme that helps a private to save lots of tax up to Rs. 46,800* u/s 80C of tax Act and also invest your money with a possible to get wealth. Here are 2 advantages of investing in an ELSS scheme:

1. Tax Exemption

The primary goal of ELSS Schemes is to assist taxpayers to save money. As stated earlier, with ELSS a private can claim tax benefits of Rs. 46, 800* with an annual investment of up to Rs. 1.5 lakh. albeit the Section 80C of tax Act only allows tax exemption worth Rs. 1.5 lakhs, there are no limitations of investing in an ELSS scheme.

2. Low Lock-in

ELSS features a lock-in period of three years. this is often one among the merchandise with the shortest lock-in period among all the tax-saving instruments.

Now that you simply are conscious of advantages of ELSS, allow us to introduce you Axis future Equity Fund (this is an open-ended equity-linked saving scheme with a statutory lock-in of three years and tax benefit) So if you would like to save lots of tax while getting to build wealth, invest in Axis future Equity Fund now.

*As per this tax laws, eligible investors (individual/HUF) are entitled to a deduction from their gross income of the quantity invested in Equity Linked Saving Scheme (ELSS) up to Rs.1.5 lakhs (along with other prescribed investments) under section 80C of the tax Act, 1961. Tax savings of Rs. 46,800 mentioned above is calculated for the very best tax slab. Investors are advised to consult his/her own Tax Consultant with reference to the precise amount of tax and other implications arising out of his/her participation in ELSS.

Investment advisor in Jaipur mutual fund investment in jaipur mutual fund advisor in Jaipur investment planning in jaipur

#taxsaving#mutalfunds#maloo#elss#taxsaving bonds#investmentplanning#investment advisor#financial planning#financial advisor

1 note

·

View note

Text

Best mutual funds to shop for in 2020

A mutual fund may be a sort of investment product where the funds of the many investors are pooled into an investment product. The fund then focuses on the utilization of these assets on investing during a group of assets to succeeding in the fund's investment goals. There are many various sorts of mutual funds available. for a few investors, this vast universe of obtainable products could seem overwhelming.

Identifying best schemes in mutual funds remains a really challenging exercise given there are quite 40 mutual fund houses in India with quite 10 different fund categories. the foremost important aspects in the selection of mutual schemes which many distributors/financial advisors in Jaipur overlook are the danger profile and time horizon of investors.

The systematic investments within the above themes/categories can help investors diversify their portfolios and may achieve handsome returns in 2020.

Identifying Goals and Risk Tolerance

Before investing in any fund, you want to first identify your goals for the investment. Are your objective long-term capital gains, or is current income more important? Will the cash be wont to buy college expenses, or to fund a retirement that's decades away? Identifying a goal is an important step in whittling down the universe of quite 8,000 mutual funds are available to investors.

History Often Doesn't Repeat

We’ve all heard that ubiquitous warning: “Past performance doesn't guarantee future results.” Yet looking at a menu of mutual funds for your 401(k) plans, it’s hard to ignore people who have crushed the competition in recent years.

A report by Standard & Poor’s showed that just 21.2% of domestic stocks within the top quartile of performers in 2011 stayed there in 2012. Furthermore, only about 7% remained within the top quartile two years later.

Selecting a mutual fund could seem sort of a daunting task, but doing touch research and understanding your objectives makes it easier. If you perform this due diligence before selecting a fund, you'll increase your chances of success.

mutual fund in Jaipur

financial planning in Jaipur

#mutualfunds#mutual funds#MutualFundInvestments#investment#pplanning#financial planning companies in jaipur#planning#financial advisor#investment advisor

1 note

·

View note

Text

Plan Your Travel and Next Big Holiday with SIP

Planning the finances for your holiday can be a headache but it doesn’t have to be if you plan in advance! Whether it’s an international trip or a local getaway, mutual funds investment can be your financial stress busters.

All you need to create a holiday plan with these eight simple steps:-

1

Figure out the prices

Find out what proportion of the varied holiday options cost. You would possibly not wish to draw a bead on Spain directly and might wish to transcend Kathmandu.

2

Find out ways of reducing costs

Thorough research will assist you to reduce costs and make your pennies travel the additional mile. for instance, you’ll save with air tickets cost with the grand sale, hotel deals, and discounts available on the internet.

3

Gain from others experience

Learn and gain from experiences of previous travelers. don’t forget to read travelers' reviews on popular blogs and comparison sites featuring their experiences. this may not only assist you to plan the trip better but also save costs.

4

Explore free homestays

Explore the choice of free homestays with locals abroad through various travel sites.

5

Slash local travel costs

There are many ride-sharing applications in many countries. They will assist you to bring down the local travel costs through carpool or hitchhikes.

6

Gain from off-season discounts

If you can, time your visit during the off-season, you’ll save to 50-60 percent. it’s better to sneak an excellent destination in your budget than head for help from dad. Besides, bragging about your travel budget will hardly impress anyone during a party.

7

Help your holiday plans get a leg up with mutual funds

Now, that you simply have a more manageable holiday expense target to save lots of for, choose a sensible investment to require you there. Mutual funds are often an excellent ally during this Endeavour. They permit fixed monthly investments through systematic investment plans (SIPs). Consider ultra short term funds that generally invest in highly rated debt securities. They assist your money to grow within the short term like one year approximately. If the vacation is three or more years away, you’ll choose other debt funds.

8

Set a practical date for your holiday

This will get to be taken in tandem with the previous. You would like to reach a vacation date. It is the time by which your money will really grow to the specified amount. For instance, if you would like to save Rs 1 lakh and may invest Rs 4,000 a month, you’ll need 25 months to succeed in near your savings target through your principal alone. You’ll make your trip happen sooner. For that, you simply might be got to spend a touch less on regular items, say, expenses on weekend unwinding, and invest a better amount monthly.

Similarly, you may have multiple dreams and each dream requires its own plan

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

financial advisor in Jaipur, mutual funds in Jaipur, Investment consultant

1 note

·

View note

Text

How to plan your visit dream destination through mutual funds

You can invest in several funds like Small Cap, Large Cap, Thematic funds etc to attenuate risk and maximize chances of earning returns at a rate above that of a recurring deposit. To play it safe, you'll prefer to invest in fixed-return debt funds.

Mutual fund investments held for quite one year are considered long-term capital assets as per the Indian law. For equity-oriented funds held for 3 years during this case, you would like not to pay any tax on dividend or capital gains after the liquidation of your investment. If you decide for low-risk debt funds, then you want to be prepared to pay a tax of 10%/20% on indexed/unindexed capital gains respectively.

Over a previous couple of years, for many Indians, annual vacations and experiencing new cultures became almost as important as saving for retirement or buying a house. However, the truth is that vacations cost an honest amount of cash and lack of designing for this goal means either you've got to require a loan or use your credit cards to fund them. But it doesn’t need to be this manner.

Start a SIP in Low-risk Debt Mutual Funds to save lots of For These Vacations

Though you've got the choice to go away the cash you're saving for a vacation in your checking account, it'd not be the simplest option. That’s because you've got instant access to the present money and there's a high probability that you simply will find yourself using it for a few other expenses.

So the best way is to place it aside monthly, at an area where it is often accessed at short notice and there's minimal risk. Although you've got RDs as an option, they are available with a hard and fast tenure and withdrawing it before the tenure ends means penalties.

Then there are mutual funds. However, the approach to save lots of for your travel has got to vary from what you would possibly be doing for your future investments. That’s because saving for a vacation may be a short to medium-term goal and you can’t take much risk with this amount.

The good part is that there are specific Debt mutual funds that are almost perfect for this type of need.

Although the first aim of those funds is to guard your capital, they still find yourself providing a minimum of 50% higher returns than your bank account. Plus there are not any tenure commitments or penalties for withdrawal, which suggests you get the pliability.

Travelling enriches our lives in multiple ways. You distress and spend time with yourself and your family, returning more energized. So you ought to travel, but if you actually want to form it stress-free, plan, and travel. the simplest part, it's really not complicated. All it takes is starting a SIP and you're set for all times.

Best sip plans, mutual funds in Jaipur, top mutual funds, a financial advisor in jaipur

#mutual funds#financial planning companies in jaipur#Investment Advisors in Jaipur#Finance and investment companies in jaipur#Mutual funds in jaipur#Tax planning services in jaipur#Financial Planning in Jaipur#Wealth Creation companies in jaipur#Wealth creation in Jaipur#mutual fund company in jaipur

1 note

·

View note

Text

When should I start investing in Mutual Funds?

There is no right time in and of it once it involves creating investments. Investments should be created at the earliest. Any day is that the best time to speculate in mutual funds. There is no minimum age when one can start investing.

Even a child can open their mutual fund investment account with the money once in a while in form of gifts during their birthdays or festivals. So, same as that, there is no age bar for start an investment with mutual funds. There is no age limit or restriction on the investment amount.

You can invest in mutual funds as soon as you start your professional career. You can start your investment as soon as your professional career. But best is that always buy fund at lower NAV rather than paying a higher price.

Mutual Fund may be a nice convenience for people who ought to invest their cash for future necessities. A team of professionals manages the money and therefore the investors will enjoy the fruits of this experience while not obtaining concerned within the mundane tasks.

The following are 3 situations that are appropriate to begin investment in mutual funds:

a. The market is rock-bottom

b. Bond yields are the highest, and/or

c. Real estate and infrastructure are at the lowest point.

The best time to invest in mutual funds is, therefore, now!

Factors Determine the Best Time to Invest?

If we are talking about the best time for investment, it is better start today. This depends on several factors, which include your personal goals as well. These are following:

Risk Appetite, Market Positioning, Return on Investment, Tax Saving Under Section 80C, Long-term or Short-term Horizon

There are many reasons to invest with mutual funds. You can achieve your financial goals with the help of mutual fund advisor.

How to find best Mutual fund Company In Jaipur?

Read our previous blog for this How to Select a Suitable Financial Advisor.

#mutual fund#mutual fund advisor#financial planning#best financial advisors in jaipur#best financial planner#best mutual fund advisor in Jaipur#financial planner in jaipur#Investment Advisors#Investment Consultant#mutual fund advisor in jaipur#Mutual Fund Agents In Jaipur#mutual fund company in jaipur#tax planning service in jaipur#The financial goal planner#Wealth Creation companies in jaipur#Wealth creation in Jaipur

1 note

·

View note