#myconcall

Text

Transform Your Financial Data Management with

Novel Patterns’ Account Aggregator Ecosystem — CART

Introduction to Account Aggregator

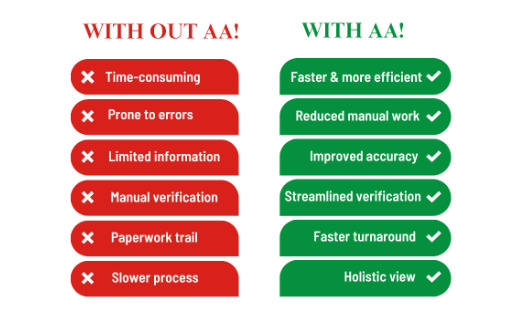

In today’s digital age, managing financial data across various platforms can be a daunting task. The emergence of the Account Aggregator (AA) ecosystem is set to revolutionize this space, offering a seamless, secure, and efficient way to share financial information across different institutions with user consent. This innovative system is regulated by the Reserve Bank of India (RBI), ensuring compliance and security.

Account Aggregators act as a bridge, facilitating the transfer of financial data from Financial Information Providers (FIPs) to Financial Information Users (FIUs) in a structured manner. This system empowers users by giving them control over their data, allowing for informed decision-making and improved financial planning. The AA ecosystem not only enhances user experience but also drives financial inclusion by making data accessible to various stakeholders in the financial sector.

The Role of Novel Patterns

At the forefront of this technological advancement is Novel Patterns, a leading Fintech solutions provider. Their CART platform is designed to streamline the integration of FIUs and FIPs into the AA ecosystem, providing a comprehensive solution for data sharing and management. The CART platform is built with advanced APIs, robust security measures, and compliance with regulatory standards, ensuring a smooth and secure data exchange process.

Key Features and Benefits

Seamless Integration — The CART platform is engineered for easy integration with existing financial systems, reducing the complexities associated with adopting new technologies. This seamless integration enhances operational efficiency and ensures minimal disruption to business processes.

Advanced Analytics — The CART platform offers advanced analytics capabilities, providing FIUs and FIPs with actionable insights. These insights help optimize AA integrations, uncover growth opportunities, and make data-driven decisions. By leveraging these analytics, financial institutions can improve their services and better meet customer needs.

Data Security — Security is paramount when dealing with financial data. Novel Patterns employs top-tier security measures to protect sensitive information throughout the integration process. Their platform adheres to stringent security protocols, ensuring that data is safeguarded against unauthorized access and breaches.

Compliance and Certification — Navigating the regulatory landscape can be challenging for financial institutions. The CART platform facilitates the necessary certifications and approvals, ensuring compliance with regulatory standards. This helps FIUs and FIPs stay ahead of regulatory requirements and avoid potential legal issues.

User-Centric Design — The CART platform is designed with the end-user in mind. Its intuitive design enhances user satisfaction and engagement, making it easy for users to navigate and manage their financial data. This user-centric approach ensures that the platform meets the needs of both FIUs and FIPs.

Scalability — As financial institutions grow, their data management needs evolve. The CART platform is built to scale, accommodating increasing data volumes and expanding with organizational growth. This scalability ensures that the platform can support the long-term needs of financial institutions.

Comprehensive Solutions for Financial Institutions

Novel Patterns’ CART platform offers a wide range of solutions tailored to the needs of financial institutions. These solutions are designed to streamline processes, enhance efficiency, and ensure compliance with regulatory standards.

Data and Consent Management — Efficient data and consent management is crucial for the success of the AA ecosystem. The CART platform simplifies consent processes, allowing users to easily grant or revoke access to their financial data. This ensures that data sharing is always done with user consent, promoting transparency and trust.

KYC/AML Compliance — Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are critical components of the financial industry. The CART platform helps financial institutions comply with these regulations by providing comprehensive tools for customer verification and monitoring. This ensures that institutions can prevent fraud and maintain the integrity of their operations.

Risk Assessment and Credit Scoring — Accurate risk assessment and credit scoring are essential for making informed lending decisions. The CART platform leverages comprehensive risk assessment tools and credit scoring algorithms to provide FIUs with the information they need to assess the creditworthiness of borrowers. This helps reduce the risk of default and improve lending outcomes.

Underwriting and Financial Analysis — Efficient underwriting processes are key to the success of financial institutions. The CART platform streamlines underwriting processes, allowing FIUs to quickly evaluate loan applications and make informed decisions. Additionally, the platform provides tools for detailed financial analysis, helping institutions better understand the financial health of their customers.

Why Choose Novel Patterns?

Choosing the right partner for integrating into the AA ecosystem is crucial for financial institutions. Novel Patterns stands out for several reasons:

Personalized Support — Novel Patterns offers personalized support to their clients, ensuring that they have the assistance they need throughout the integration process. Their team of experts is available to provide guidance and address any issues that may arise.

Transparent Pricing — Transparency in pricing is a key consideration for financial institutions. Novel Patterns offers transparent pricing models, allowing institutions to understand the costs involved and budget accordingly. This transparency helps build trust and ensures that there are no hidden fees.

Unified Platform — Novel Patterns’ CART platform provides a unified solution for managing invoices, support, and billing inquiries. This simplifies the management process and ensures that all aspects of the integration are handled efficiently.

Scalability and Growth — The CART platform is built to scale, ensuring that it can support the long-term growth of financial institutions. As data volumes increase and business needs evolve, the platform can adapt to meet these changing requirements.

Success Stories

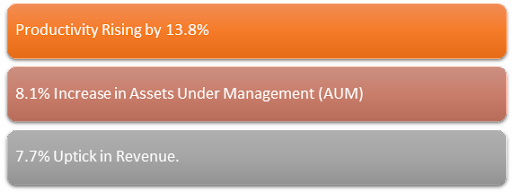

Novel Patterns has a proven track record of successfully integrating financial institutions into the AA ecosystem. Their clients have reported significant improvements in operational efficiency, data management, and customer satisfaction. By leveraging Novel Patterns’ solutions, these institutions have been able to enhance their services, expand their customer base, and achieve their business goals.

Future Prospects

The future of the AA ecosystem looks promising, with increasing adoption and continuous innovation. Novel Patterns is committed to staying at the forefront of this evolution, continually enhancing its CART platform to meet the growing needs of financial institutions. By investing in research and development, they aim to introduce new features and capabilities that will further streamline data management and enhance the user experience.

Get Started

To experience the transformative power of Novel Patterns’ AA solutions, connect with us today. Explore how their innovative Fintech SaaS offerings can elevate your business and drive success in the ever-evolving financial landscape.

#cart#fintech#novel patterns#myconcall#account aggregator#bfsi#credit underwriting#finance#Financial Institution

1 note

·

View note

Text

Ride the Wave: Embrace Wealth Management's Next Frontier with Genesis by Novel Patterns

In the swiftly evolving financial domain, sophisticated wealth management platforms are in soaring demand. Investors clamor for comprehensive solutions to adeptly manage their assets and investments, propelling the emergence of innovative technologies tailored to these dynamic needs.

Enter Genesis by Novel Patterns, a groundbreaking wealth management platform poised to redefine the industry standard. This article delves into the transformative features of Genesis and explores how it is revolutionizing wealth management. With its advanced algorithms and customizable features, Genesis offers a unique approach to portfolio management that maximizes returns and minimizes risks. By leveraging cutting-edge technology and data analytics, this platform provides investors with unparalleled insights and opportunities for growth in today's complex financial markets.

Understanding Wealth Management Platforms

Wealth management platforms serve as the backbone for financial institutions, offering a suite of tools and functionalities to effectively oversee clients' assets and investments. These platforms streamline processes, provide insightful analytics, and facilitate decision-making, empowering advisors and clients alike to navigate complex financial landscapes with confidence.

By leveraging cutting-edge technology and data analytics, wealth management platforms enable financial institutions to deliver personalized and efficient services to their clients. These platforms also help advisors stay informed about market trends and client preferences, ultimately leading to better investment decisions and increased client satisfaction. Overall, wealth management platforms have revolutionized the way financial advisors and clients interact, making it easier to manage portfolios and achieve financial goals. With the ability to access real-time data and customize investment strategies, these platforms have become essential tools in the modern financial industry.

Genesis: A Product by Novel Patterns: Pioneering Innovation in Wealth Management

Built upon years of industry expertise and cutting-edge technology, Genesis sets a new benchmark for wealth management solutions. With its intuitive interface, advanced analytics, and customizable features, Genesis empowers financial institutions to deliver unparalleled value to their clients.

Genesis emerges as a game-changer in the wealth management landscape, setting a new benchmark for excellence. With its intuitive interface, advanced analytics, and customizable features, Genesis empowers portfolio management service providers to deliver unparalleled value to their clients.

Key Features Tailored for Portfolio Management Service Providers

Comprehensive Portfolio Management: Genesis offers robust capabilities for constructing, analyzing, and rebalancing portfolios with ease. Through advanced algorithms and risk assessment tools, advisors can optimize asset allocation strategies tailored to each client's unique goals and risk tolerance.

Advanced Analytics: Leveraging big data and machine learning algorithms, Genesis provides actionable insights into market trends, investment opportunities, and risk factors. This empowers advisors to make informed decisions and seize opportunities for portfolio growth.

Integrated Compliance Solutions: Compliance is paramount in the financial industry, and Genesis includes built-in features to ensure adherence to regulatory standards and mitigate risk. From automated compliance checks to real-time monitoring, Genesis streamlines regulatory processes, enhancing efficiency and transparency.

Client-Centric Dashboard: Genesis prioritizes the client experience with its intuitive dashboard interface. Clients gain access to real-time portfolio performance, financial reports, and interactive tools to track their investments and monitor progress toward their financial goals. Personalized dashboards foster transparency and strengthen client-advisor relationships.

Robust Double-Entry Accounting Management: Genesis accounting system boasts robust double-entry management, ensuring accuracy and reliability in financial records. With a highly configurable chart of accounts, we tailor our system to suit the unique needs of your business. From tracking expenses to monitoring revenues, our platform provides comprehensive support for your accounting needs, empowering you to make informed financial decisions with confidence.

Scalable Architecture: Whether serving individual investors or large institutional clients, Genesis offers a scalable architecture to accommodate diverse business needs. With its cloud-based infrastructure and modular design, Genesis adapts to evolving market dynamics and scales seamlessly as client portfolios grow.

360-degree Reporting: Our reporting functionality offers a 360-degree view of your financial landscape, encompassing standard Arbor and Ibor reporting as well as global/local regulatory compliance. Whether you require standardized reports or bespoke client-specific insights, our platform delivers tailored solutions to meet your diverse reporting needs. With our comprehensive reporting capabilities, you gain unparalleled visibility into your financial performance, enabling strategic decision-making and regulatory compliance with ease.

Standard Arbor Reporting: Includes comprehensive reporting features tailored to Arbor standards, offering insights into various financial aspects such as assets, liabilities, income, and expenses.

Standard Ibor Reporting: Equipped with standard Ibor reporting capabilities, enabling detailed analysis and tracking of interest rate benchmarks, providing valuable insights for decision-making.

Global / Local Regulatory Reporting: Ensures compliance with regulatory requirements on both global and local levels, facilitating accurate and timely submission of financial reports to regulatory authorities.

Tailor-made client reporting: Offers customizable reporting options to meet specific client preferences and requirements, providing personalized insights and enhancing client satisfaction and engagement.

Navigating the Trade Lifecycle: A Journey through Genesis

In the realm of financial markets, the lifecycle of a trade encompasses various stages, each vital for ensuring smooth and efficient transactions. Within the sophisticated infrastructure of Genesis, a comprehensive platform for trade management, these stages are meticulously orchestrated to streamline processes and enhance operational efficacy. Let's delve into the intricacies of the trade lifecycle within Genesis: From trade initiation to settlement, Genesis provides real-time monitoring and reporting capabilities to optimize decision-making and risk management. By offering customizable workflows and automated processes, Genesis empowers users to navigate the complexities of the trade lifecycle with ease and confidence.

1. Trade Creation: Trades are initiated through diverse channels such as the Order Management Module, interfaces, APIs, or manual input via UI screens. This versatility ensures flexibility and convenience in trade initiation, catering to diverse user preferences and requirements.

2. Trade Processing: This phase involves intricate processes including LOT accounting, weighted average accounting, handling of multi-currency trades, and customizable transaction charges. Whether capitalizing or expensing transaction charges, Genesis offers adaptable solutions to suit varying business needs.

3. Transaction View: Providing transparency and clarity, Genesis allows users to view accounting entries, facilitating comprehensive oversight and auditability throughout the transaction lifecycle.

4. Corporate Actions: Genesis facilitates the seamless processing of security-based corporate actions, ensuring timely and accurate execution to reflect corporate events impacting securities held within portfolios.

5. Prices and FX Updates: Keeping pace with global market dynamics, Genesis integrates with service providers to deliver real-time pricing and foreign exchange updates. Whether at a global or security/fund-specific level, users benefit from access to multiple price and FX lists within a single schedule.

6. Valuation: From pre-valuation checks for accuracy to fund closing activities encompassing mark-to-market valuation, interest calculations, accruals amortization, and expense triggering, Genesis ensures precision and integrity in valuation processes.

7. Reporting: Genesis empowers users with a plethora of reporting options, ranging from canned reports to comprehensive 360-degree client reporting and regulatory reporting functionalities. These features enable stakeholders to extract valuable insights and meet compliance requirements effortlessly.

In essence, Genesis serves as a beacon of efficiency and reliability across the entire spectrum of trade lifecycle management. By seamlessly integrating diverse functionalities and providing customizable solutions, Genesis empowers users to navigate the complexities of financial markets with confidence and precision. Genesis's robust reporting capabilities ensure that users have access to the information they need to make informed decisions and stay ahead of industry trends. Additionally, its user-friendly interface makes it easy for stakeholders to quickly generate and analyze reports, saving time and streamlining operations.

The Impact of Novel Patterns Genesis on the Wealth Management Landscape

As financial institutions embrace digital transformation, the adoption of advanced wealth management platforms like Genesis becomes imperative for staying competitive. By harnessing the power of Novel Patterns Genesis, institutions can:

Enhance Client Engagement: One of the primary strengths of Genesis lies in its ability to facilitate meaningful client interactions. With its intuitive interface and personalized insights, Genesis empowers advisors to deliver actionable information to clients. This, in turn, fosters deeper engagement and trust, laying the foundation for long-term relationships that are essential in wealth management.

Drive Operational Efficiency: Genesis streamlines processes and automates workflows, allowing advisors to focus on high-value tasks such as financial planning and strategic advisory services. By eliminating the burden of routine administrative tasks, Genesis enables advisors to deliver superior service while optimizing resource allocation, ultimately enhancing operational efficiency.

Mitigate Risk: Compliance breaches and regulatory non-compliance pose significant risks to financial institutions. Genesis addresses these concerns by offering integrated compliance solutions that ensure adherence to regulatory standards. By safeguarding against legal implications, Genesis helps mitigate risks and reinforces the institution's credibility and reputation in the market.

Enhancing Cost Efficiency through Legacy System Optimization: Our strategic approach centers on enhancing cost efficiency by addressing the drain on operational costs associated with legacy systems. Legacy systems often incur substantial expenses due to the need for extensive maintenance and support. To combat this, we prioritize transitioning from outdated technologies to more efficient alternatives. By modernizing our systems, we not only streamline processes but also reduce ongoing maintenance costs and enhance overall productivity. This transition not only yields cost savings but also minimizes the risk of disruptions or downtime, ensuring a more efficient and sustainable operational environment.

API-Driven Platform: Genesis is built on an API-driven platform, which means it offers robust capabilities for seamless integration with existing systems and applications. This architecture allows for easy communication and data exchange between Genesis and other software solutions used within the financial institution. By leveraging APIs, institutions can customize and extend the functionality of Genesis to suit their specific needs, whether it involves integrating with internal databases, third-party services, or other software platforms. This flexibility enables financial institutions to create a cohesive ecosystem of tools and services, optimizing their operations and enhancing overall efficiency.

Cloud-Centric Application for Rapid Deployment: Genesis combines API-driven architecture with cloud-centric design for rapid deployment. Leveraging cloud technology offers scalability, accessibility, and agility, eliminating the need for complex infrastructure and reducing upfront costs. Cloud deployment allows quick scaling to meet evolving business needs, enhances mobility for advisors, and supports remote work capabilities. This setup ensures swift implementation and ongoing scalability, enabling financial institutions to stay agile and responsive in today's fast-paced environment.

Embracing the Future of Wealth Management with Novel Patterns Genesis

In conclusion, Genesis by Novel Patterns represents a paradigm shift in wealth management, empowering financial institutions to thrive in an increasingly digital world. With its innovative features, advanced analytics, and client-centric approach, Genesis equips advisors with the tools they need to deliver exceptional value and drive growth. As the industry evolves, Novel Patterns remains at the forefront of innovation, shaping the future of wealth management one client at a time.

In the competitive landscape of wealth management, embracing technological advancements is no longer optional—it's essential for success. With Novel Patterns Genesis, financial institutions can embark on a journey of transformation, unlocking new opportunities and staying ahead of the curve in an ever-changing market.

Through its powerful combination of cutting-edge technology and industry expertise, Novel Patterns Genesis is poised to revolutionize the way we think about wealth management. As institutions across the globe embrace this innovative platform, the future of wealth management has never looked brighter.

1 note

·

View note

Text

Recent IPOs to IPO History: A Comprehensive Exploration of Investor Fervor

Have you ever witnessed an IPO that sparked such a wildfire of investor enthusiasm, breaking records? Well, you would have braced yourself for the extraordinary tale of Tata Technologies' recent initial public offering (IPO), a spectacle that left the financial world buzzing with excitement.

In a remarkable display of investor confidence, Tata Technologies' initial public offering (IPO) shattered records, attracting an unprecedented 73.6 lakh applications, the highest ever for a private sector company in India. This overwhelming response underscored the company's robust financial performance, strong growth prospects, and its position as a leading global IT services provider.

Tata Technologies' IPO, which opened on November 22, 2023, and closed on November 24, 2023, saw an overwhelming surge in applications from retail investors, non-institutional investors, and qualified institutional buyers (QIBs). The retail investor segment oversubscribed by a staggering 36.2 times, while non-institutional investors oversubscribed by 12.1 times. QIBs, too, showed strong interest, with a subscription rate of 1.9 times.

This overwhelming response is attributed to several factors, including:

Stellar Financial Performance: Tata Technologies has demonstrated consistent growth and profitability over the past few years. In the financial year 2023, the company's revenue grew by 22% to ₹12,500 crore, while its net profit increased by 18% to ₹2,500 crore. This robust financial performance instilled confidence in investors, who saw Tata Technologies as a financially sound and stable company.

Promising Growth Prospects: The global IT services industry is expected to witness substantial growth in the coming years, driven by the increasing adoption of digital technologies and the growing demand for cloud computing, cybersecurity, and data analytics solutions. Tata Technologies is well-positioned to capitalize on this growth, given its strong expertise in these areas and its presence in key verticals such as automotive, aerospace, and manufacturing.

Reputed Brand and Strong Management: Tata Technologies is part of the Tata Group, one of India's most respected and well-established conglomerates. The Tata brand name carries significant weight in the Indian market, and investors were attracted to the company's association with the Tata Group. Additionally, Tata Technologies' management team is highly experienced and has a proven track record of success, further enhancing its appeal to investors.

Strategic Positioning: Tata Technologies has strategically positioned itself to cater to the evolving needs of its global clientele. The company has invested heavily in building its capabilities in emerging technologies such as artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT). This focus on innovation and technological advancement resonated with investors, who saw Tata Technologies as a company at the forefront of the IT industry.

Favorable Market Conditions: The Indian stock market has been on an upward trajectory in recent years, creating a favorable environment for IPOs. Investors were eager to participate in IPOs, and Tata Technologies' IPO offered an attractive opportunity to invest in a company with strong fundamentals and promising growth prospects.

Skilled Marketing Campaign: Tata Technologies' IPO was backed by a well-executed marketing campaign that effectively communicated the company's strengths and growth potential to investors. The company engaged with potential investors through various channels, including roadshows, investor conferences, and media outreach.

The overwhelming response to Tata Technologies' IPO is a testament to the company's strong fundamentals, its bright prospects, and the confidence that investors have placed in its management team. The company is poised to continue its growth trajectory and become a leading player in the global IT services industry.

Decoding the IPO Phenomenon: Understanding the Allure of Initial Public Offerings

In the dynamic world of finance, initial public offerings (IPOs) have emerged as a captivating spectacle, attracting both seasoned investors and curious onlookers alike. These events mark the momentous transition of a private company into a publicly traded entity, allowing its shares to be traded on stock exchanges.

An IPO represents a company's debut on the grand stage of public markets, granting access to a vast pool of capital and potentially propelling it to new heights of growth and success. For investors, IPOs offer a tantalizing opportunity to participate in the early stages of a company's journey, potentially reaping substantial rewards if the company's fortunes rise.

The allure of IPOs stems from several factors. Firstly, they present a chance to invest in companies with promising growth prospects. Private companies, often operating at the cutting edge of their respective industries, hold immense potential to disrupt traditional markets and capture significant market share.

Secondly, IPOs offer investors the opportunity to diversify their portfolios. By venturing into uncharted territories, investors can mitigate the risks associated with concentrated holdings in established companies.

Furthermore, IPOs can generate significant returns for investors who correctly identify the next big thing. The history of finance is replete with instances of companies that have skyrocketed in value following their IPOs, rewarding those who had the foresight to invest early on.

However, investing in IPOs is not without its risks. The inherent uncertainty associated with early-stage companies makes their future performance difficult to predict. Moreover, the initial pricing of IPO shares is often subject to speculation and may not accurately reflect the company's true value.

Despite these risks, IPOs continue to hold a magnetic appeal for investors, offering a chance to be part of a company's transformative journey and potentially reap substantial rewards.

A Deeper Dive into the History of Indian IPOs: From Humble Beginnings to Today's Mega Listings

The history of Initial Public Offerings (IPOs) in India is a fascinating journey that reflects the dynamic evolution of the country's economy and financial markets. From modest beginnings to today's mega listings, Indian IPOs have played a pivotal role in shaping the nation's corporate landscape. This article will take you on a comprehensive journey through the milestones, trends, and statistics that define the history of Indian IPOs.

I. Humble Beginnings (Late 19th Century - 1980s):

The concept of IPOs in India can be traced back to the late 19th century, with the establishment of the Bombay Stock Exchange (BSE) in 1875. However, the market for public offerings remained relatively subdued until the 1980s. During this period, companies seeking capital infusion predominantly relied on traditional debt financing.

The 1980s marked a significant turning point with the introduction of economic reforms, liberalization, and globalization. The era saw a gradual shift towards equity financing, and a few pioneering companies leaped to go public. The IPO landscape began to transform, laying the foundation for the vibrant market we witness today.

II. Regulatory Reforms and Milestones (1990s - Early 2000s):

The Securities and Exchange Board of India (SEBI) was established in 1988, and the subsequent years witnessed a series of regulatory reforms aimed at fostering transparency, investor protection, and market efficiency. The introduction of the SEBI (Disclosure and Investor Protection) Guidelines in 1992 was a landmark event that standardized disclosure norms for companies going public.

The mid-1990s to the early 2000s saw a surge in IPO activity. Companies from diverse sectors, including information technology, telecommunications, and pharmaceuticals, tapped into the capital market to fuel their growth ambitions. The IPO boom was fueled by robust economic growth, technological advancements, and a growing appetite for equity investments among retail and institutional investors.

III. Dotcom Boom and Bust (Late 1990s):

The late 1990s witnessed the global dotcom boom, and India was not immune to the fervor. Several technology and internet-based companies rushed to go public, leading to a frenzy of IPOs. The BSE Sensex soared to unprecedented levels, reflecting the exuberance in the market. However, the dot-com bubble eventually burst in the early 2000s, resulting in a sharp correction in stock prices and a cautious approach towards IPOs.

IV. Recovery and Resilience (Mid-2000s - 2010s):

Post the dot-com bust, the Indian IPO market displayed resilience and gradually recovered. The mid-2000s saw a resurgence of IPO activity, driven by a mix of domestic and global factors. Robust economic growth, a stable political environment, and increasing investor confidence contributed to the positive sentiment.

The introduction of Book Building as a price discovery mechanism in 2005 brought more efficiency to the IPO process. Companies increasingly adopted this method to determine the IPO price based on investor demand, contributing to more realistic valuations.

V. Regulatory Enhancements and Reforms (2010s):

The SEBI continued to play a proactive role in refining regulations to align with global best practices and address emerging challenges. The introduction of the SEBI (Issue of Capital and Disclosure Requirements) Regulations in 2009 streamlined the IPO process, emphasizing transparency, and investor protection.

The SEBI's efforts to curb fraudulent activities and market manipulation through enhanced surveillance mechanisms bolstered investor confidence. The introduction of the Institutional Trading Platform (ITP) in 2013 provided a dedicated exchange for startups to list and raise capital.

VI. Mega Listings and Market Dynamics (2010s - Present):

The last decade witnessed a surge in mega listings, with companies raising substantial capital through IPOs. The Indian stock market saw blockbuster listings in various sectors, including technology, finance, and consumer goods. The advent of unicorns – privately held startups valued at over a billion dollars – going public added to the excitement.

Technology companies, in particular, played a pivotal role in shaping the IPO landscape. The success of e-commerce giants, fintech firms, and software companies in the public markets showcased the maturity and potential of India's tech ecosystem.

Timeline Chart:

Let's delve into some key statistics and trends that highlight the evolution of Indian IPOs:

Number of IPOs:

1990s: Limited IPO activity, gradual increase.

2000s: Surge in IPOs, especially during the mid-2000s.

2010s: Robust IPO activity with a focus on quality issuances.

2020s: Record-breaking IPOs, with mega listings dominating.

Sectoral Distribution:

Early Years: Diversification across traditional industries.

2000s: Emergence of technology and IT-enabled services.

2010s: Dominance of technology, finance, and consumer sectors.

2020s: Continued tech dominance, with a rise in green and sustainable offerings.

Market Capitalization:

1990s-2000s: Gradual increase in overall market capitalization.

2010s-Present: Significant expansion, driven by mega listings and valuation surges.

Investor Participation:

1990s-2000s: Increasing interest from institutional investors.

2010s-Present: Growing retail investor participation, especially in high-profile IPOs.

Challenges and Opportunities:

Despite its remarkable progress, the Indian IPO market still faces certain challenges. Regulatory complexities, concerns about corporate governance, and market volatility are factors that can impede its growth. However, the future remains bright, fueled by several promising developments:

A Vibrant Startup Ecosystem: India's thriving startup scene presents a plethora of innovative companies poised to enter the market, offering attractive investment opportunities to both domestic and international investors.

Growing Investor Base: Increasing financial literacy and rising wealth within the domestic market are driving greater participation from individual investors, providing a strong foundation for long-term market stability.

Ongoing Reforms: The government's commitment to streamlining regulations and improving corporate governance is expected to further enhance investor confidence and attract more capital to the market.

Looking Ahead: A Promising Future

As India's economy continues its impressive growth trajectory and its corporate landscape undergoes further evolution, the IPO market is poised for further expansion and diversification. With a growing pool of potential investors and a vibrant startup ecosystem, the journey from nascent beginnings to global phenomenon is set to continue, solidifying India's position as a leading force in the global IPO market.

Re-Wind Up:

The history of Indian IPOs is a narrative of growth, resilience, and adaptation to changing economic landscapes. From the tentative steps in the late 19th century to the mega listings of the present day, Indian companies have embraced the capital markets to fuel their expansion and contribute to the nation's economic development. The regulatory reforms, market dynamics, and investor participation have collectively shaped the trajectory of IPOs in India, making it a compelling journey worth exploring. As we step into the future, the continued evolution of the IPO landscape promises to bring forth new milestones, challenges, and opportunities for companies and investors alike.

Additional Notes:

This article provides a high-level overview of the history of Indian IPOs and is not intended to be an exhaustive analysis. It may not encompass all relevant details or nuanced perspectives.

The information presented in this article is based on research from various reputable sources, including news articles, research reports, and industry publications. While every effort has been made to ensure accuracy, the provided information should not be considered definitive and may require further investigation.

#cart#fintech#myconcall#novel patterns#account aggregator#bfsi#wealth management#genesis#Tata#IPO#Tata IPO

1 note

·

View note

Text

Transforming Wealth Management: The Tech-Infused Evolution

In a time when innovation is primarily driven by digital change, the wealth management sector is leading the charge. It is more important than ever to have a simple, safe, and interesting solution for personalized portfolio management, client interaction, and client onboarding. As a means of achieving efficiency and personalization, technological improvements have become the primary driver behind the transformation of the wealth management industry. These advancements have allowed wealth managers to streamline processes, automate tasks, and provide clients with real-time access to their portfolios. Additionally, technology has enabled the development of sophisticated algorithms and data analytics tools that can analyze market trends and make informed investment decisions. As a result, wealth management firms are able to offer more tailored investment strategies and deliver a higher level of service to their clients.

Statistics of the Indian wealth management industry:

Assets under management (AUM): US$429.70 billion (2023).

Market size: US$390.00 billion (2023).

Number of high-net-worth individuals (HNIs): 3.5 lakhs (2020), expected to grow to 6.11 lakhs by 2025.

Number of ultra-high-net-worth individuals (UHNIs): 13,637 (2021), expected to grow to 19,006 by 2026.

70–80% of wealth management firms in India are using video KYC for onboarding new clients.

85–90% of wealth management firms in India are using technology to automate some of their wealth management processes.

The fintech market in India is expected to grow to US$2.1 trillion by 2030.

India has the highest fintech adoption rate globally, with 87% of Indians using fintech services.

Financial technology companies are at the forefront of India's wealth management sector's digital development. By automating and streamlining wealth management procedures, fintech is able to increase efficiency, lower costs, and make investing more accessible to a larger group of individuals.

Fintech is being applied in the Indian wealth management sector in the following significant ways:

Digital onboarding: To make the process of opening a wealth management account simpler and faster for investors, fintech businesses are utilizing digital onboarding solutions. This includes minimizing the need for paperwork and in-person meetings by utilizing Video KYC and other digital verification techniques.

Investment automation: Fintech firms are creating tools to assist wealth managers in automating processes including risk management, asset allocation, and portfolio rebalancing. This can free up wealth managers to concentrate on additional value-added tasks, including giving their clients individualized financial advice.

Data analytics: Wealth managers may gain a better understanding of their customer's financial needs and risk tolerance by working with fintech businesses to leverage data analytics. The creation of more individualized and successful wealth management plans may then be accomplished with the usage of this data.

Engagement with clients: Wealth managers may keep in touch with their customers and provide them with real-time information on their investments with the aid of client engagement platforms that fintech businesses are building. Stronger client-wealth manager connections and an enhanced customer experience can result from this.

Both investors and wealth managers are benefiting from the growing usage of fintech in the wealth management sector. Lower expenses, increased convenience, and more individualized investing advice are all advantages for investors. Increased productivity and efficiency assist wealth managers by enabling them to concentrate on giving their clients greater service.

All things considered, the adoption of fintech in India's wealth management sector is a trend that is anticipated to continue in the years to come.

The Wealth Management Tapestry

The financial dreams and objectives of people are intimately woven into the wealth management sector, creating a complicated tapestry. It has historically been associated with in-person meetings, voluminous documentation, and drawn-out procedures. But a new era has arrived with the development of technology, changing how wealth management firms carry out their fundamental duties.'

It is impossible to emphasize the importance of technology in asset management. The foundation of efficiency and innovation in this industry is technology, which offers real-time data analytics that yield actionable insights and complex algorithms that customize investment plans to the particular demands of customers. Technology integration creates new opportunities for customized customer experiences in addition to streamlining operational procedures. Furthermore, technology also plays a crucial role in risk management within asset management firms. By utilizing advanced risk assessment tools and predictive modeling, technology enables firms to identify and mitigate potential risks, ensuring the safety and security of clients' investments. Additionally, technology-driven automation processes help reduce human errors and increase overall operational efficiency, allowing firms to focus more on strategic decision-making and delivering superior financial outcomes for their clients.

Video KYC and Seamless Onboarding: Catalysts for Growth

As the wealth management industry embraces the digital age, the adoption of video KYC (Know Your Customer) and seamless onboarding processes emerges as a game-changer. These technological advancements not only simplify the onboarding journey for clients but also play a pivotal role in expanding the user base for management companies.

The Video KYC Advantage

Video KYC, a revolutionary approach to identity verification, allows wealth management firms to remotely and accurately authenticate their clients. This transformative process not only saves valuable time but also elevates the overall customer experience to unprecedented heights. The ability to fulfill KYC requirements online eliminates the need for clients to physically visit, bestowing convenience and enhanced security upon the process.

In an industry where trust is paramount, Video KYC adds an extra layer of credibility. The face-to-face interaction through secure video calls instills confidence in clients, assuring them that their sensitive information is handled with the utmost care. As a result, Video KYC not only expedites the onboarding process but also establishes a foundation of trust, crucial for long-lasting client relationships.

Seamless Onboarding: A Strategic Imperative

Seamless onboarding, facilitated by Video KYC, is a strategic imperative for wealth management companies looking to thrive in the digital era. Traditionally, client onboarding has been plagued by cumbersome paperwork and tedious procedures, often acting as a deterrent for potential clients. The marriage of Video KYC and seamless onboarding transforms this arduous process into a user-friendly, efficient journey.

Clients can now complete the required identity verification and documentation procedures from the comfort of their homes through secure video calls. This not only saves time but also enhances the overall client experience, making the onboarding process a crucial touchpoint for positive first impressions. The ease of onboarding becomes a catalyst for client retention and acquisition, as individuals are more likely to engage with a wealth management platform that respects their time and simplifies complex procedures.

Expanding the User Base

The marriage of Video KYC and seamless onboarding acts as a gateway for wealth management companies to expand their user base. In an era where individuals seek instant gratification and streamlined processes, a frictionless onboarding experience becomes a powerful differentiator. Wealth management firms that embrace these technological advancements position themselves as frontrunners in attracting a diverse clientele.

Research indicates that 60% of wealth management firms are planning to implement Video KYC in the next two years, underscoring the industry's recognition of the transformative potential of this technology.

As companies leverage Video KYC and seamless onboarding to create a more accessible and user-friendly environment, the barriers to entry for potential clients are significantly lowered. This not only broadens the reach of wealth management services but also democratizes access to financial planning and portfolio management.

Genesis and MyConCall by Novel Patterns: Crafting the Future of Wealth Management

Genesis: A Comprehensive Investment Solution

Genesis by Novel Patterns offers a holistic solution for investment management with support for multiple asset classes, multi-currency capabilities, configurable charts of accounts, dynamic fee set-up, user-defined fields, and an efficient multitab user interface.

Asset & Investment Management Platform by Novel Patterns

Revolutionising Wealth Management: MyConCall's Video KYC & Personal Discussion Integration

In the realm of wealth management, a transformative shift is underway with MyConCall's integration of video KYC and personal discussion features. Wealth management extends beyond mere financial planning; it embodies the creation of a personalized experience tailored to the distinct needs and aspirations of each client. Recognizing this paradigm, Genesis and MyConCall have embarked on a collaborative journey to pioneer a new era of customized wealth management.

The integration of video KYC enables wealth management firms to fulfill KYC requirements seamlessly online, eradicating the necessity for clients to make physical visits. This shift bestows both convenience and heightened security upon the onboarding process, aligning with the contemporary preferences of clients who seek streamlined and safeguarded interactions. The elimination of the physical presence requirement is a pivotal enhancement, epitomizing the commitment to client-centricity and reflecting the industry's dedication to embracing cutting-edge solutions for a more accessible and secure wealth management experience.

Video Engagement Platform by Novel Patterns for Video KYC & Personal Discussion Solution

Against this backdrop of technological transformation, the partnership between Genesis and MyConCall emerges as a beacon of innovation. Their collaboration seeks to redefine wealth management by combining cutting-edge technology with personalized service, addressing key pain points in the client onboarding process, portfolio management, and client engagement.

The Genesis and MyConCall alliance harnesses the power of video KYC to remotely verify the identity of clients, setting the stage for a seamless and secure onboarding process. This collaboration understands that wealth management is not a one-size-fits-all endeavor; it's about creating bespoke experiences for each client. Through personalized portfolio management and enhanced client engagement facilitated by MyConCall's unique features, the partnership aims to elevate the wealth management experience to new heights.

Genesis & MyConCall: Transforming Wealth Management

In a game-changing partnership, Genesis and MyConCall redefine wealth management through video KYC and personal discussions. This collaboration streamlines onboarding, personalizes portfolio management, and enhances client engagement.

Video KYC onboarding: Genesis and MyConCall simplify client onboarding with secure video calls, eliminating paperwork, and offering a seamless experience from home.

Personalized Portfolio Management: Cutting-edge algorithms tailor investment strategies to individual goals and risk tolerance, ensuring optimized and diversified portfolios.

Enhanced client engagement: The MyConCall platform facilitates one-on-one personal discussion sessions, fostering trust and satisfaction by addressing client concerns directly.

Robust security & compliance: Video KYC ensures secure identity verification, complies with regulatory requirements, and safeguards sensitive client information.

Geo-tagging for security: The geo-tagging feature verifies client location during video KYC, adding an extra layer of security and enabling personalized services based on geography.

Rewind-Up: A Future Defined by Innovation

In a nutshell, technology plays a revolutionary role in the wealth management business as it navigates the digital frontier. Specifically, video KYC and seamless onboarding stand out as particularly important examples. These developments serve as catalysts to increase wealth management businesses' user bases in addition to streamlining operational procedures. Genesis and MyConCall's collaboration is a prime example of the industry's dedication to innovation, ushering in a time where trust, efficiency, and customization will characterize wealth management. Those who take advantage of these technological advancements will be well-positioned to prosper in a cutthroat market and usher in a new era of wealth management characterized by accessibility, security, and client-centricity. These advancements in technology have the potential to revolutionize the way wealth management services are delivered, making them more accessible to a wider range of clients.

By leveraging technology, platforms like Genesis and MyConCall by Novel Patterns can provide personalized investment strategies and financial advice tailored to each individual's unique needs and goals. This level of customization not only enhances the client experience but also ensures that their investments are aligned with their long-term objectives, ultimately leading to greater success and satisfaction in the wealth management industry.

#cart#fintech#myconcall#novel patterns#account aggregator#bfsi#video kyc#financial accounting#genesis#wealth management

1 note

·

View note

Text

Unlock Unprecedented Financial Success: Genesis and the Double-Entry Accounting Revolution in Wealth Management

The selection of accounting procedures becomes crucial for operational efficiency in the dynamic world of wealth management, where accuracy and insight are important. It's unsettling to see that the majority of solutions now available on the market don't take a comprehensive approach and frequently exclude crucial elements like double-entry bookkeeping and a single window for Front, Middle, and Back office integration. Due to these flaws, wealth management companies struggle with fragmented systems that impede efficient financial operations. As a result, these companies often face challenges in maintaining accurate and up-to-date financial records, which can lead to errors and inefficiencies. Additionally, the lack of integration between different departments within the company hinders collaboration and slows down decision-making processes.

This article explains the dramatic differences between single-entry and double-entry systems, acting as a guide in navigating the complex world of accounting. Additionally, it highlights the ground-breaking value of Genesis by Novel Patterns, a comprehensive solution that effortlessly incorporates double-entry accounting.

Genesis by Novel Patterns streamlines the accounting process by automating data entry and reducing the risk of errors. This integrated system allows for seamless communication between departments, promoting collaboration and improving overall efficiency.

Many wealth management companies in India are not using double-entry accounting.

This is a significant disadvantage, as double-entry accounting provides a number of benefits, including improved financial visibility, better financial decision-making, reduced tax liability, and increased peace of mind for clients.

Genesis - A Wealth Management Platform by Novel Patterns, on the other hand, is committed to using double-entry accounting for all of its clients. This allows us to provide our clients with the highest level of service and help them to achieve their financial goals.

If you are looking for a wealth management firm that uses double-entry accounting, Genesis Wealth Management is the right choice for you. To learn more about our services, please read the full article or visit our website.

Double-Entry Accounting for Unparalleled Financial Success

Traditional wealth management practices have failed to keep up with the rapidly evolving financial landscape. Today's high-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNIs) face a complex and ever-changing set of financial challenges, from managing their global assets to navigating the latest tax laws.

To achieve unparalleled financial success, HNWIs and UHNWIs need a wealth management approach that is tailored to their specific needs and goals, and that leverages the latest technologies and best practices. Double-entry accounting is a basic requirement consistent with global/ local accounting standards that can be used to revolutionize wealth management by providing a holistic view of an individual's financial situation and empowering them to make informed financial decisions.

Some of the stats regarding double accounting entry:

According to a recent survey by Deloitte, 80% of HNWIs believe that double-entry accounting is essential for effective wealth management.

A study by PwC found that double-entry accounting can help to reduce tax liability by an average of 10%.

A study by the American Institute of CPAs found that businesses that use double-entry accounting are more likely to be successful than businesses that use single-entry accounting.

Single-entry accounting vs. double-entry accounting

Single-entry accounting is a system of bookkeeping that records each financial transaction in a single account. This type of accounting is relatively simple to implement and maintain, but it can be inaccurate and difficult to use for complex financial situations.

Double-entry accounting is a system of bookkeeping that records each financial transaction in two or more accounts. For each transaction, one account is debited and another account is credited. This ensures that the total debits are always equal to the total credits, which helps to maintain the accuracy of the financial records.

Here is a characteristic chart that compares benefits attributed to wealth management firms using single and double-entry accounting:

Other key differences:

Single-entry accounting firms typically have less sophisticated systems and processes in place.

Single-entry accounting firms may be less likely to have certified financial planners (CFPs) and other financial professionals on staff.

Single-entry accounting firms may be less likely to offer a full range of wealth management services, such as tax planning and estate planning.

Single-entry accounting firms may be more likely to charge fees based on a percentage of assets under management, while double-entry accounting firms may be more likely to charge fees based on a flat rate or hourly basis.

Overall, double-entry accounting firms are better equipped to help clients achieve their financial goals. They have the systems, processes, and expertise to provide clients with comprehensive financial advice and help them reduce their tax liability.

What is double-entry accounting?

Double-entry accounting is a system of bookkeeping that records every financial transaction in two or more accounts. For each transaction, one account is debited and another account is credited. This ensures that the total debits are always equal to the total credits, which helps to maintain the accuracy of the financial records.

Evolution of Double entry accounting:

The history of double-entry bookkeeping in Europe is indeed fascinating and has had a significant impact on the field of accounting. Here is a summary of the key developments and figures mentioned in the text:

In the late 13th century, Amatino Manucci, a Florentine merchant, introduced the modern double-entry system in Europe through his work with the Farolfi firm. Their ledger from 1299-1300 provides early evidence of double-entry bookkeeping.

Giovannino Farolfi & Company, a Florentine merchant firm headquartered in Nîmes, played a role in spreading the double-entry system, particularly as moneylenders to the Archbishop of Arles.

While some suggest that Giovanni di Bicci de' Medici may have introduced double-entry bookkeeping in the 14th century for the Medici bank, there is no concrete evidence to support this claim.

In the 16th century, Venice became a hub for the theoretical development of accounting science. Key figures such as Luca Pacioli, Domenico Manzoni, Bartolomeo Fontana, Alvise Casanova, and Giovanni Antonio Tagliente contributed to this advancement.

Luca Pacioli, often called the "father of accounting," published a detailed description of the double-entry system in his 1494 mathematics textbook, "Summa de arithmetica, geometria, proportioni et proportionalità," in Venice.

Benedetto Cotrugli, a Ragusan merchant and ambassador to Naples, described double-entry bookkeeping in his treatise "Della mercatura e del mercante perfetto," written in 1458 but not printed until 1573, with some alterations by the printer.

These developments in accounting laid the foundation for the modern accounting practices that are widely used today. Double-entry bookkeeping remains a fundamental and standardized method for recording financial transactions in businesses and organizations.

Double-entry accounting has been used by businesses for centuries to track their income and expenses, assets and liabilities. However, it has only recently begun to be adopted by wealth managers to help their clients manage their personal finances.

How can double-entry accounting revolutionize the wealth management industry?

Double-entry accounting can revolutionize wealth management in a number of ways. First, it can help individuals to gain a clearer understanding of their overall financial situation. By tracking all of their income and expenses, assets and liabilities in a single system, individuals can see exactly where their money is going and identify areas where they can make savings or reduce debt.

Second, double-entry accounting can help individuals to make better financial decisions. By understanding the impact of their financial decisions on their overall financial situation, individuals can make more informed choices about their investments, spending, and other financial matters.

Third, double-entry accounting can help individuals to reduce their tax liability. By carefully tracking their income and expenses, individuals can take advantage of all available tax deductions and credits. This can lead to significant tax savings, especially for HNWIs and UHNWIs.

Benefits of using double-entry accounting for wealth management

Indian wealth management firms like Genesis by Novel Patterns can enhance operations for their clients using double-entry accounting in a number of ways, including:

Improved financial visibility: Double-entry accounting provides a holistic view of a client's financial situation, making it easier to track income and expenses, assets and liabilities, and investments. This can help wealth managers to identify areas where they can help their clients to save money, reduce debt, and grow their wealth.

Better financial decision-making: By understanding the impact of their financial decisions on their overall financial situation, clients can make more informed choices about their investments, spending, and other financial matters. Wealth managers can use double-entry accounting to help their clients to model different financial scenarios and make the best decisions for their individual needs.

Reduced tax liability: By carefully tracking their income and expenses, clients can take advantage of all available tax deductions and credits. This can lead to significant tax savings, especially for high-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNIs). Wealth managers can use double-entry accounting to help their clients to develop tax-efficient strategies and reduce their tax liability.

Increased peace of mind: Having a clear understanding of one's financial situation and being confident in the accuracy of one's financial records can lead to increased peace of mind. Wealth managers can use double-entry accounting to provide their clients with accurate and up-to-date financial reports, giving them peace of mind knowing that their finances are in order.

In addition to these benefits, double-entry accounting can also help to:

Improve their efficiency and productivity: By automating many of the tasks involved in financial accounting, double-entry accounting can free up wealth managers to focus on providing their clients with value-added services.

Reduce the risk of errors and fraud: Double-entry accounting provides a built-in system of checks and balances, which can help to reduce the risk of errors and fraud. This is important for wealth management firms, which have a fiduciary responsibility to their clients.

Enhance their reputation: Wealth management firms that use double-entry accounting are demonstrating to their clients that they are committed to accuracy, transparency, and accountability. This can help to enhance their reputation and attract new clients.

How to implement double-entry accounting in an Indian wealth management firm

There are a number of ways to implement double-entry accounting in an Indian wealth management firm. One option is to use a traditional accounting software program. However, these programs are often designed for businesses and can be complex and difficult to use for wealth management firms.

Another option is to use a cloud-based wealth management platform that offers double-entry accounting capabilities. These platforms are typically more user-friendly and easier to set up and use.

Once you have chosen a software solution, you will need to gather all of your client's financial information and enter it into the system. This includes their income and expenses, assets and liabilities, and investments. Once you have entered all of the information, you will be able to generate reports that show your client's overall financial situation, including their net worth, cash flow, and investment performance.

Must Read - Unleashing Transformation with Genesis: Redefining Wealth Management for the Future

Genesis by Novel Patterns is not just a wealth management platform; it's a transformative force reshaping the narrative of financial success. Positioned as a catalyst for the future, Genesis stands at the forefront of the continuous transformation in the financial landscape.

Tailored for Asset Managers, Portfolio Management, FPI & AIF, Mutual Funds, and Family Offices, Genesis offers an unparalleled suite of features that redefine wealth management. With a commitment to accuracy, efficiency, and innovation, Genesis ensures a unified view of all investments, whether in traditional assets or alternative investments. The platform is both Cloud Ready and Enterprise Solution, offering a highly configurable system that adapts to the unique needs of each user.

The 360° Monthly Client Reporting feature provides comprehensive insights, while the integrated support for Front, Middle, and Back Office functions streamlines operations. With FoF & Asset Pooling Structure, automated workflow execution, and support for multi-assets and alternatives, Genesis paves the way for a user-friendly, efficient interface, making worries about wealth management a thing of the past. Say hello to streamlined financial success with Genesis!

Genesis Features and Advantages:

1: Comprehensive Accounting:

Genesis by Novel Patterns emerges as a game-changer by providing a one-stop solution for investment in accounting books of record preparation. Its integration of double-entry accounting principles ensures a more accurate and comprehensive financial representation.

2: Easy Error Rectification:

Genesis simplifies the rectification of errors and modifications, a critical feature for maintaining accurate financial records. This ease of correction minimizes the risk of discrepancies and ensures the integrity of financial data.

3: Accurate NAV Generation:

Net Asset Value (NAV) is a critical metric in assessing the performance of investment portfolios. Genesis ensures accurate NAV generation, providing a reliable basis for decision-making in wealth management.

4: Unitized and Non-Unitized Views:

Genesis offers the flexibility of both unitized and non-unitized views within double-entry accounting. This flexibility caters to diverse investment strategies, accommodating the unique needs of different portfolios.

Why Choose Genesis?

Genesis emerges as the preferred choice for discerning businesses seeking an advanced wealth management platform. Its appeal is rooted in its ability to facilitate seamless migration from legacy systems, providing a modernized financial infrastructure. The platform's cost efficiency is a standout feature, offering a streamlined solution without compromising on quality.

Genesis's cloud-agnostic nature adds a layer of adaptability, allowing businesses to tailor their financial operations to specific cloud environments. Notably, an explicit discount policy ensures transparency in pricing structures, fostering trust and confidence in the financial partnership. Time efficiency is a strategic advantage as Genesis streamlines processes, reducing manual interventions in a fast-paced financial landscape. The graphical representation of 360-degree client reporting enhances data visualization, offering stakeholders, including financial advisors and clients, a sophisticated and comprehensive view of financial information.

In choosing Genesis, businesses embrace not just a platform but a transformative force unlocking unparalleled financial efficiency:

1: Easy Migration:

Businesses often face challenges in migrating from legacy systems. Genesis streamlines this process, allowing for easy migration without disrupting ongoing operations. This is particularly advantageous for businesses looking to modernize their financial infrastructure.

2: Cost Efficiency:

In a landscape where operational costs can be a significant concern, Genesis stands out for its cost efficiency. It provides a streamlined solution without exorbitant expenses, making it an attractive choice for businesses aiming to optimize their financial operations.

3: Cloud Agnostic:

Genesis is a cloud-agnostic solution, offering flexibility and adaptability to various cloud environments. This ensures that businesses can choose the cloud service that aligns with their specific needs and preferences, adding a layer of customization to their financial operations.

4: Explicit Discount Policy:

Transparency in pricing structures is paramount in the financial sector. Genesis provides an explicit discount policy, ensuring businesses have a clear understanding of the costs associated with using the platform.

5: Time Efficiency:

Genesis is designed for time efficiency, streamlining processes and reducing the time spent on manual interventions. In a fast-paced financial landscape, where timely decisions are crucial, this feature becomes a strategic asset.

6: 360-Degree Client Reporting:

The graphical representation of 360-degree client reporting enhances data visualization. This feature makes it easier for stakeholders, including financial advisors and clients, to comprehend complex financial information. The ability to visualize data from multiple perspectives adds a layer of sophistication to client reporting.

The All-encompassing Solution: Unveiling the Versatility of Genesis in Modern Wealth Management

In the ever-evolving landscape of wealth management, Genesis emerges as a comprehensive and versatile solution, catering seamlessly to both conventional and non-conventional investment techniques. As a go-to platform for companies navigating the complexities of the contemporary financial landscape, Genesis showcases remarkable adaptability and agility. Its capacity to provide a uniform platform, whether dealing with traditional investment vehicles or delving into alternative options, positions it as an invaluable asset for businesses seeking a holistic view of their investment portfolio.

This holistic perspective empowers companies to make well-informed decisions by considering multiple angles and factors. With Genesis, clients gain the ability to effortlessly compare and analyze the performance of different investment strategies. This not only facilitates a deeper understanding of portfolio dynamics but also enables them to optimize returns and effectively mitigate risks. In essence, Genesis stands as more than just a platform; it is a dynamic and versatile tool empowering businesses to thrive in the intricate and ever-changing world of modern wealth management.

The Dance Continues: Unveiling the Dynamic Symphony of Debits and Credits within Genesis

Far from a static process, the dance of debits and credits within Genesis unfolds as a dynamic symphony, orchestrating the intricate movements of financial transactions. A profound understanding of how these debits and credits impact various accounts—ranging from assets, expenses, revenue, liabilities, and equity—becomes not only essential but a gateway to unlocking the full potential of Genesis.

The holistic integration of double-entry accounting principles within the Genesis framework transcends the conventional, providing a real-time and comprehensive understanding of financial movements. Here, assets ascend and descend with market fluctuations, expenses rise and fall with operational dynamics, revenue undergoes subtle shifts, liabilities ebb and flow in response to financial commitments, and equity experiences dynamic changes reflective of strategic financial decisions. This dance is not a mere choreography of numbers; it is the rhythmic heartbeat pulsating through the veins of financial operations.

Delving into this dynamic symphony, users of Genesis gain more than just a ledger of transactions; they acquire a real-time narrative of their financial landscape. It's a tool that not only captures financial data but transforms it into actionable insights, allowing businesses to navigate the complex rhythms of the financial world with precision and agility. In essence, the dance of debits and credits within Genesis is not just a feature; it's the artistry that shapes the very core of financial operations.

Rewind-Up:

In conclusion, the adoption of double-entry accounting principles and the comprehensive features of Genesis by Novel Patterns mark a transformative moment in wealth management. Businesses looking for accuracy, efficiency, and a unified solution for diverse investment strategies find their answer in Genesis. As the financial landscape continues to evolve, embracing innovative solutions becomes a strategic imperative.

Genesis, with its unique features and advantages, positions itself as a leader in reshaping the future of financial operations in wealth management. This holistic approach to wealth management, coupled with the precision of double-entry accounting, sets the stage for a new era of financial insight and operational excellence. The journey towards a more sophisticated, integrated, and streamlined wealth management process is underway, and Genesis stands at the forefront of this revolution.

This comprehensive integration of accounting principles and technology, along with Genesis's commitment to providing a single window for Front, Middle, and Back office solutions, marks the dawn of a new era in wealth management. The dance of numbers within Genesis is not just about financial transactions; it's about orchestrating a symphony of success for businesses navigating the complexities of the financial landscape. As businesses look to the future, the choice of a robust and adaptable solution becomes not just a necessity but a strategic advantage. In Genesis, the wealth management industry discovers not just a platform but a transformative force shaping the future of financial operations.

1 note

·

View note

Text

Revolutionizing Credit Assessment in India: Exploring the Role of Bank Statement Analyzers

The Bank Statement Analyser not only enhances the efficiency and precision of assessing a borrower’s financial status but also holds the potential to unveil hidden insights that might otherwise remain unnoticed. Through its capacity to scrutinize trends and patterns in a borrower’s financial conduct, the Bank Statement Analyzer identifies potential risks and opportunities. This empowers lenders to make well-informed decisions aligned with their institution’s risk management strategies. Additionally, by offering a more transparent and objective approach to credit assessments, the Bank Statement Analyser fosters trust between borrowers and lenders, cultivating stronger and more profitable relationships. Hence, the adoption of a Bank Statement Analyser proves to be a mutually beneficial strategy for all involved parties, rendering it an indispensable tool for banks and financial institutions navigating an ever-evolving industry.

While the utilization of Bank Statement Analyser (BSA) platforms for credit underwriting in India is a relatively recent development, it is rapidly gaining traction. These automated tools extract and analyze crucial financial data from bank statements, encompassing income, expenses, liabilities, and transaction patterns. Lenders employ this information to evaluate a borrower’s creditworthiness and make well-informed lending decisions.

Initially employed predominantly by large banks and financial institutions, BSAs are now more widely adopted, including by smaller banks, NBFCs, and fintech companies. The burgeoning popularity of BSAs in India can be ascribed to several factors:

Increasing Availability of Digital Bank Statements: The prevalence of digital bank statements in India has made it easier for lenders to collect and analyze relevant data.

Rising Demand for Digital Lending: The escalating demand for digital lending in India, driven by borrowers seeking convenient and streamlined access to credit, is a significant factor. Bank Statement Analysers facilitate lenders in automating and expediting their lending processes, thereby enhancing the accessibility of loans.

Growing Awareness of BSA Benefits: Lenders are becoming progressively cognizant of the advantages offered by Bank Statement Analysers, such as heightened accuracy, reduced risk, and expedited loan processing.

In the Indian lending landscape, Bank Statement Analysers are assuming an increasingly pivotal role. By automating the bank statement analysis, these tools enable lenders to make more informed credit underwriting decisions, thereby mitigating the risk of loan defaults. Ultimately, this benefits borrowers by making access to credit easier, more efficient, and affordable.

Decoding Bank Statement Analyzers: Practical Significance and Real-World Applications

A bank statement analyzer (BSA) is a sophisticated software tool designed to extract and scrutinize crucial financial data from bank statements. The applications of BSAs extend across various domains, providing utility for both businesses and individuals in the following areas:

Key Features of Bank Statement Analyzers: Illuminating the Landscape of Financial Wisdom

Analysis of Various Statement Types: Distinguishing itself, the Best Bank Statement Analyzer demonstrates versatility by scrutinizing not only eStatements but also electronic and scanned versions of bank statements, as well as passbooks. This expansive capability ensures that underwriters have access to a diverse array of financial documents, thereby facilitating more holistic and nuanced assessments.

Fraud Detection: In a lending industry fraught with the specter of fraud, Bank Statement Analyzers incorporate robust mechanisms for fraud detection. These mechanisms are designed to flag suspicious transactions and patterns, erecting an additional layer of security that shields lenders from potential risks.

Real-time Financial Worthiness Analysis: An exceptional facet of Bank Statement Analyzers is their adeptness in extracting and analyzing an applicant’s financial worthiness in real-time. This dynamic capability empowers underwriters with access to up-to-date information about an applicant’s financial situation, thereby facilitating expeditious and accurate assessments.

Elimination of Manual Verifications: The time-consuming nature of manual verification processes has long been a bane in the lending industry. Bank Statement Analyzers ingeniously automate these processes, effecting significant reductions in time and effort required for underwriting. This not only accelerates decision-making but also serves as a potent bulwark against human errors.

Optimization and Cost-effectiveness: The bedrock of the Bank Statement Analyzer lies in its commitment to efficiency and cost-effectiveness. By automating tasks that were hitherto performed manually, the Analyzer optimizes the lending process, culminating in cost savings for financial institutions. This efficiency cascades into faster loan approvals, thereby elevating the overall borrower experience.

Automatic Identification of Income/Expense Patterns: A profound understanding of an applicant’s income and expense patterns is pivotal for accurate lending decisions. Bank Statement Analyzers leverages advanced algorithms to automatically identify and analyze these patterns, presenting underwriters with invaluable insights into an applicant’s financial behavior.