#COVID 19 Impact on UAE Loan Industry

Text

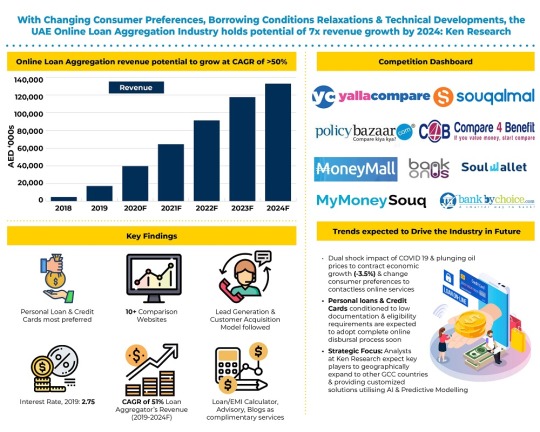

UAE Online Loan Aggregation Industry Holds Potential 7x Revenue Growth By 2024. Will UAE Online Loan Aggregation Industry Stand On This Projected Figure? Ken Research

REQUEST FOR SAMPLE REPORT

Buy Now

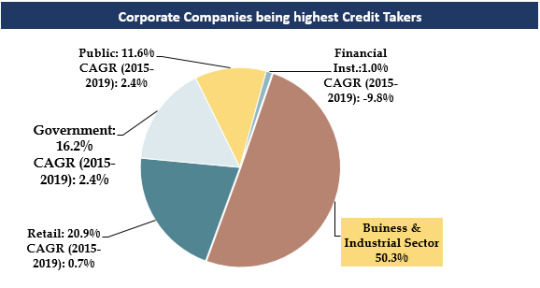

1. With rich, diverse & unparalleled infrastructure, the UAE Loan Industry driven by high corporate loan demand.

Trends and Developments in UAE Online Loan Aggregator Industry

Lending majorly dominated by national banks with wide distribution network, occupying >90% of all banks credit disbursal.

With major investment in hydrocarbon projects & other infrastructure projects, credit demand by government has been rising & expected to further rise in future as well.

Traditional methods of lending (Friends/family) are still preferred choice for availing loans by people with below avg credit history.

Banks are undertaking consolidation activities thereby reducing number of branches, cash offices & promoting digital banking services.

2. Technological Evolution in UAE Banking Services.

To Know More about this report, download a Free Sample Report

Adoption of Blockchain technology in enhancing “Know- Your-Customer” processes, useful in client onboarding, cross border transfers, payments & compliance reporting.

Tasharuk Platform: Launched by UBF to fight against cyber-attacks on banks. Platform enables cyber threat information sharing, identify threats & enhance defense systems.

Incorporating Artificial Intelligence in data analytics, combatting fraudulent activities & compliance improvement, further increasing focus on customer dealing & decision-making processes.

Increased penetration of virtual banking channels including Mobile (>85%), Online Banking (>90%), Branch/Call center (>90%) and ATMs (~100%).

Noticeable shift among customers to online medium for undertaking non-cash transactions of balance enquiries, fund transfers etc.

3. Housing Loan, one of the fastest growing retail loan segments.

Visit This link:- Request for Custom Report

In 2019, average house price in Dubai decreased by ~12% reaching to ~AED 2.58 Mn, thereby, shifting from investor led market to owner-occupied market.

While borrower’s previously preferred fixed interest rates but with Fed Reserve Predictions (2019), noticeable trend was observed for variable rate schemes.

Customers rising preferences for loan providers/aggregators offering other benefits like property management services & post-handover assistance services.

Dubai is dominated by expat population (11 times of Emirati population), who are observed to be preferring indirect channels due to high documentation & eligibility requirements.

Current lending process in The UAE is partially offline; however; with advancements & relaxations in regulations could help in making the process online.

For more insights on the market intelligence, refer to the link below:-

UAE Online Loan Aggregator Market

#BankOnUs Credit Cards Online Market Revenue#Car Loan Market UAE#Commercial Loan Market UAE#Commission Rate Online Aggregators UAE#COVID 19 Impact on UAE Loan Industry#Credit Cards Market UAE#Credit Outstanding in the UAE#Fee rate Loan disbursement UAE#Investments UAE Online Loan Aggregator Startups#Leading players of Loan Aggregator Market#Major Companies Loan Aggregator Market#Major Loan Providers in UAE#Number of Car Loans UAE#Number of Credit Card Users UAE#Number of House Loans UAE#Number of Loans Disbursed UAE#Number of Online Loan Market End Users#Number of Online Loans Disbursed UAE#Online Broker vs Online Aggregators UAE#Online Brokers in UAE#Online Distribution Loan UAE#Online Loan Aggregator Industry UAE#Outstanding Loans UAE#Personal Loan Market UAE#PolicyBazaar UAE Credit Cards Revenue#PolicyBazaar UAE Online Loan Market Share#Souqalmal UAE Personal Loan Revenue#Top 5 Online Loan Aggregator Startups UAE Top companies UAE Car Rental Market#Top Players Loan Aggregator Market#UAE Cash Loans Online Loan Market

0 notes

Photo

Future of UAE Online Loan Aggregator Market: Ken Research Buy Now COVID 19 Crisis Creating Opportunity in Credit Market As Coronavirus hit the world in 2020, whilst some countries took a slow approach to comprehend & dealing with the situation, UAE was one of the very few countries taking pivotal steps to minimize both health & economic risks in the country.

#BankOnUs Credit Cards Online Market Revenue#Commission Rate Online Aggregators UAE#COVID 19 Impact on UAE Loan Industry#Credit Outstanding in the UAE in AED#Fee rate Loan disbursement UAE#Future of UAE Online Loan Aggregator Market#Future Outlook of Retail Lending & Online Loan Aggregators#Impact of COVID 19 on UAE Loan Industry#Major Loan Providers in UAE#Online Brokers in UAE#Online Brokers vs Online Aggregators UAE#Online Loan Aggregator Industry UAE#Online Loan Aggregator Market UAE#Online Loans Industry in UAE#Online Loans Market in UAE#PolicyBazaar UAE Credit Cards Revenue#PolicyBazaar UAE Online Loan Market Share#PolicyBazaar UAE Personal Loan Revenue#Revenue Loan Aggregators UAE#Souqalmal UAE Personal Loan Revenue#UAE Cash Loans Online Loan Market#UAE Credit Cards Online Market#UAE Fintech Market#UAE Online Aggregator Services Market#UAE Online Car Loan Market#UAE Online Distribution Loan UAE#UAE Online Loan Aggregator Industry#UAE Online Loan Aggregator Industry Research Report#UAE Online Loan Aggregator Market#UAE Online Loan Aggregator Market Analysis

0 notes

Text

Working Capital Loan Market 2022-2028 Size, Share, Trend, Key Palyers with Products

Working Capital Loan Market 2022-2028

A New Market Study, Titled “Working Capital Loan Market Upcoming Trends, Growth Drivers and Challenges” has been featured on fusionmarketresearch.

Description

This global study of the Working Capital Loan market offers an overview of the existing market trends, drivers, restrictions, and metrics and also offers a viewpoint for important segments. The report also tracks product and services demand growth forecasts for the market. There is also to the study approach a detailed segmental review. A regional study of the global Working Capital Loan industry is also carried out in North America, Latin America, Asia-Pacific, Europe, and the Near East & Africa. The report mentions growth parameters in the regional markets along with major players dominating the regional growth.

Request Free Sample Report @ https://www.fusionmarketresearch.com/sample_request/2021-2030-Report-on-Global-Working-Capital-Loan-Market/69533

This research covers COVID-19 impacts on the upstream, midstream and downstream industries. Moreover, this research provides an in-depth market evaluation by highlighting information on various aspects covering market dynamics like drivers, barriers, opportunities, threats, and industry news & trends. In the end, this report also provides in-depth analysis and professional advices on how to face the post COIVD-19 period.

The research methodology used to estimate and forecast this market begins by capturing the revenues of the key players and their shares in the market. Various secondary sources such as press releases, annual reports, non-profit organizations, industry associations, governmental agencies and customs data, have been used to identify and collect information useful for this extensive commercial study of the market. Calculations based on this led to the overall market size. After arriving at the overall market size, the total market has been split into several segments and subsegments, which have then been verified through primary research by conducting extensive interviews with industry experts such as CEOs, VPs, directors, and executives. The data triangulation and market breakdown procedures have been employed to complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments.

Leading players of Working Capital Loan including:

Agricultural Bank of China Limited

Banco Santander SA

Bank of America Corporation

Bank of China Limited

Bank of Communications Co Ltd

Barclays Bank PLC

BB&T

BNP Paribas SA

BPCE

China Construction Bank Corporation

China Development Bank

China Merchants Bank Co Ltd

Citibank

Deutsche Bank AG

Industrial & Commercial Bank of China Limited

Industrial Bank Co Ltd

JAPAN POST BANK Co Ltd

JPMorgan Chase & Co.

Mizuho Bank Ltd

MUFG Bank Ltd.

PNC Financial Services Group Inc

Postal Savings Bank of China Co Ltd

Regions Financial Corporation

Royal Bank of Canada

Societe Generale

Sumitomo Mitsui Banking Corporation

The Norinchukin Bank

U.S. Bancorp

UBS AG

Wells Fargo & Company

Market split by Type, can be divided into:

Banking Loan

Non-Banking Institutions Loan

Market split by Application, can be divided into:

SMEs

Large Enterprises

Individuals

Market split by Sales Channel, can be divided into:

Direct Channel

Distribution Channel

Market segment by Region/Country including:

North America (United States, Canada and Mexico)

Europe (Germany, UK, France, Italy, Russia and Spain etc.)

Asia-Pacific (China, Japan, Korea, India, Australia and Southeast Asia etc.)

South America (Brazil, Argentina and Colombia etc.)

Middle East & Africa (South Africa, UAE and Saudi Arabia etc.)

Ask Queries @ https://www.fusionmarketresearch.com/enquiry.php/2021-2030-Report-on-Global-Working-Capital-Loan-Market/69533

Table of Contents

Chapter 1 Working Capital Loan Market Overview

1.1 Working Capital Loan Definition

1.2 Global Working Capital Loan Market Size Status and Outlook (2015-2030)

1.3 Global Working Capital Loan Market Size Comparison by Region (2015-2030)

1.4 Global Working Capital Loan Market Size Comparison by Type (2015-2030)

1.5 Global Working Capital Loan Market Size Comparison by Application (2015-2030)

1.6 Global Working Capital Loan Market Size Comparison by Sales Channel (2015-2030)

1.7 Working Capital Loan Market Dynamics (COVID-19 Impacts)

1.7.1 Market Drivers/Opportunities

1.7.2 Market Challenges/Risks

1.7.3 Market News (Mergers/Acquisitions/Expansion)

1.7.4 COVID-19 Impacts on Current Market

1.7.5 Post-Strategies of COVID-19 Outbreak

Chapter 2 Working Capital Loan Market Segment Analysis by Player

2.1 Global Working Capital Loan Sales and Market Share by Player (2018-2020)

2.2 Global Working Capital Loan Revenue and Market Share by Player (2018-2020)

2.3 Global Working Capital Loan Average Price by Player (2018-2020)

2.4 Players Competition Situation & Trends

2.5 Conclusion of Segment by Player

Chapter 3 Working Capital Loan Market Segment Analysis by Type

3.1 Global Working Capital Loan Market by Type

3.1.1 Banking Loan

3.1.2 Non-Banking Institutions Loan

3.2 Global Working Capital Loan Sales and Market Share by Type (2015-2020)

3.3 Global Working Capital Loan Revenue and Market Share by Type (2015-2020)

3.4 Global Working Capital Loan Average Price by Type (2015-2020)

3.5 Leading Players of Working Capital Loan by Type in 2020

3.6 Conclusion of Segment by Type

Chapter 4 Working Capital Loan Market Segment Analysis by Application

4.1 Global Working Capital Loan Market by Application

4.1.1 SMEs

4.1.2 Large Enterprises

4.1.3 Individuals

4.2 Global Working Capital Loan Revenue and Market Share by Application (2015-2020)

4.3 Leading Consumers of Working Capital Loan by Application in 2020

4.4 Conclusion of Segment by Application

Chapter 5 Working Capital Loan Market Segment Analysis by Sales Channel

5.1 Global Working Capital Loan Market by Sales Channel

5.1.1 Direct Channel

5.1.2 Distribution Channel

5.2 Global Working Capital Loan Revenue and Market Share by Sales Channel (2015-2020)

5.3 Leading Distributors/Dealers of Working Capital Loan by Sales Channel in 2020

5.4 Conclusion of Segment by Sales Channel

Continue…

ABOUT US:

Fusion Market Research is one of the largest collections of market research reports from numerous publishers. We have a team of industry specialists providing unbiased insights on reports to best meet the requirements of our clients. We offer a comprehensive collection of competitive market research reports from a number of global leaders across industry segments.

CONTACT US

Phone:

+ (210) 775-2636 (USA)

+ (91) 853 060 7487

0 notes

Text

Payday Loans Service Market Research Report 2021 - Industry Size, Share, Demands, Regional Analysis & Estimations Till 2027

The Payday Loans Service Market Report, in its latest update, highlights the significant impacts and the recent strategical changes under the present socio-economic scenario. The Payday Loans Service industry growth avenues are deeply supported by exhaustive research by the top analysts of the industry. The report starts with the executive summary, followed by a value chain and marketing channels study. The report then estimates the CAGR and market revenue of the global and regional segments.

Base Year: 2020

Estimated Year: 2021

Forecast Till: 2027

The report classifies the market into different segments based on type and product. These segments are studied in detail, incorporating the market estimates and forecasts at regional and country levels. The segment analysis is helpful in understanding the growth areas and potential opportunities of the market.

Get | Download FREE Sample Report of Global Payday Loans Service Market @ https://www.decisiondatabases.com/contact/download-sample-7877

A special section is dedicated to the analysis of the impact of the COVID-19 pandemic on the growth of the Payday Loans Service market. The impact is closely studied in terms of production, import, export, and supply.

The report covers the complete competitive landscape of the Worldwide Payday Loans Service market with company profiles of key players such as:

Wonga

Cash America International

Wage Day Advance

DFC Global Corp

Instant Cash Loans

MEM Consumer Finance

Speedy Cash

TitleMax

LoanMart

Check `n Go

Finova Financial

TMG Loan Processing

Just Military Loans

MoneyMutual

Allied Cash Advance

Same Day Payday

LendUp Loans

Want to add more Company Profiles to the Report? Write your Customized Requirements to us @ https://www.decisiondatabases.com/contact/get-custom-research-7877

Payday Loans Service Market Analysis by Type:

Platform Financial Support

Non-platform Financial Support

Payday Loans Service Market Analysis by Application:

Staff

Retired People

Others

Payday Loans Service Market Analysis by Geography:

North America (USA, Canada, and Mexico)

Europe (Germany, UK, France, Italy, Russia, Spain, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South-East Asia, Rest of Asia-Pacific)

Latin America (Brazil, Argentina, Peru, Chile, Rest of Latin America)

The Middle East and Africa (Saudi Arabia, UAE, Israel, South Africa, Rest of the Middle East and Africa)

Key questions answered in the report:

What is the expected growth of the Payday Loans Service market between 2022 to 2027?

Which application and type segment holds the maximum share in the Global Payday Loans Service market?

Which regional Payday Loans Service market shows the highest growth CAGR between 2022 to 2027?

What are the opportunities and challenges currently faced by the Payday Loans Service market?

Who are the leading market players and what are their Strengths, Weakness, Opportunities, and Threats (SWOT)?

What business strategies are the competitors considering to stay in the Payday Loans Service market?

Purchase the Complete Global Payday Loans Service Market Research Report @ https://www.decisiondatabases.com/contact/buy-now-7877

About Us:

DecisionDatabases.com is a global business research report provider, enriching decision-makers, and strategists with qualitative statistics. DecisionDatabases.com is proficient in providing syndicated research reports, customized research reports, company profiles, and industry databases across multiple domains. Our expert research analysts have been trained to map client’s research requirements to the correct research resource leading to a distinctive edge over its competitors. We provide intellectual, precise, and meaningful data at a lightning speed.

For more details:

DecisionDatabases.com

E-Mail: [email protected]

Phone: +91 90 28 057900

Web: https://www.decisiondatabases.com/

0 notes

Text

Hotel Financing Advisors in Berlin, Germany, Europe – Agilis Advisors

We are providing the financial Advisory service would help you to channelize your investments correctly but will also bring out strategies through which you can recover the old investments made. for more info:- +49 (0) 176 36395599.

Reinstating hospitality industry with pristine financial assistance from Agilis advisors

No doubt covid-19 pandemic has caused more disaster than one could manage. The hospitality industry is no exception and has been left with meager survival strategies. There are pending hospitality loans and the acute shortage of cash flow has literally drowned in the Vintage hotels. Agilis Advisors can introduce you with some great financial management strategies that can put an end to the Deep Impact of covid-19 pandemic. Hotel financing in Germany

Lower down business complexities with the laudable financial management system

The customised approaches and documentation can help your business to cover-up warranties for the loans. Everything is expertly tailored so that no financial shortage occurs and you invest in the correct place. The experts from Agilis Advisors are completely aware about the Global scenarios and for that's how they structure your financial Investments to give you maximized returns. They develop solutions that can be employed to overcome the debt constraints. You can discuss the financial complexities with them so as to clarify things better. A piece of advice from them can help you to overcome an ongoing series of issues in almost no time. The pandemic is not over yet and substantial regulatory movements have to be taken to mitigate the effects. It is only through export tips from agilis Advisors that there would be a possibility of quick Revival in your business. Measures regarding cash control and security can be left upon the experts who have a distinctive and knowledgeable approach of managing things. They Understand the way hotel business is run at global level and that's the reason why strategies applied by them are never a failure. Hotel financing in Berlin

Get distinctive Hospitality Management Services under one roof

Not only the financial Advisors would help you to channelise your investments correctly but will also bring out strategies through which you can recover the old investments made. The hotel management that are run under a brand name need more diligent financial management that we deliver. We understand that whatever financial management steps are taken by the franchise holders must not result in defying of certain rules. We undertake the Required refurbishing facilities and confirmation of financial resources to meet the future capital expenditures. We shoulder critical financial situations in a way that nothing attracts penalty but pure rewards. Unlike other businesses, Hotel Management requires expertise in a variety of tasks. Agilis Advisors undertake steps to make sure that the required services are delegated while keeping the short term and long term needs in mind.

Maintain your accounts and always remain confident

It goes without saying that the sound financial management system is the backbone of a successful business. Apart from taking a couple of personal decisions to run your business, it is also important to choose a good financial advisor that can give you a promising future . Naturally a single entity cannot focus on annual budget, financial reporting, accountability and adapting to change all alone. There has to be a helping hand that can cover up the services of maintenance, energy and revenue . The financial managers from Agilis aptly identify the sources of revenues and Threads. They also maintain proper accounts and reconcile the difference so that you always have everything written.

Track market changes single handedly

Not everybody can track the changing market scenarios while looking after the routine business chores. If you run a hotel, it is absolutely necessary to look after the changing market conditions. Agilis Advisors can help you to track those changes so that you can integrate them in your own business. The experts keep on exploring better opportunities and help your business to embrace them for a powerful Hotel financial management system.

https://www.agilisadvisors.com/

Germany (Headquarters) - Lindenstraße 74, 10969 Berlin

UAE - Sheikh Mohammed Bin Zayed Rd, 111123 Dubai

Mauritius - Royal Road, 71366, Rose Hill

Netherlands - 5612 LW, Eindhoven

+49(0)30 25293151 +49 17636395599, +971 552879830, +230 54988787, +31 682978092

#Hotel financing in Berlin#hotel financing in Germany#hotel financing in Europe#hotel financing advisors in Berlin#hotel financing advisors in Germany#hotel financing advisors in Europe

0 notes

Text

Student Loan CAGR, Volume and Value 2026

This report elaborates the market size, market characteristics, and market growth of the Student Loan Servicing industry, and breaks down according to the type, application, and consumption area of Student Loan Servicing. The report also conducted a PESTEL analysis of the industry to study the main influencing factors and entry barriers of the industry.

In Chapter 3.4 of the report, the impact of the COVID-19 outbreak on the industry was fully assessed. Fully risk assessment and industry recommendations were made for Student Loan Servicing in a special period. This chapter also compares the markets of Pre COVID-19 and Post COVID-19.

In addition, chapters 8-12 consider the impact of COVID-19 on the regional economy.

ALSO READ : http://www.marketwatch.com/story/global-electrical-fittings-market-size-share-value-and-competitive-landscape-2024-2021-05-19

Key players in the global Student Loan Servicing market covered in Chapter 13:

FedLoan Servicing

College Ave

Credible

MEFA

Custom Choice

Lendkey

Federal Government

Sallie Mae

Earnest

SoFi

Nelnet

In Chapter 6, on the basis of types, the Student Loan Servicing market from 2015 to 2025 is primarily split into:

Federal Loan

Private Loan

ALSO READ : http://www.marketwatch.com/story/global-fashion-apparel-plm-software-market-statistics-cagr-outlook-and-covid-19-impact-2021---2023-2021-05-10

In Chapter 7, on the basis of applications, the Student Loan Servicing market from 2015 to 2025 covers:

College Students

High School Student

Other

Geographically, the detailed analysis of production, trade of the following countries is covered in Chapter 4.2, 5:

United States

Europe

China

Japan

India

ALSO READ : http://www.marketwatch.com/story/global-fruit-punnet-market-by-type-by-application-by-segmentation-by-region-and-by-country-2020-2021-05-08

Geographically, the detailed analysis of consumption, revenue, market share and growth rate of the following regions are covered in Chapter 8, 9, 10, 11, 12:

North America (Covered in Chapter 8)

United States

Canada

Mexico

Europe (Covered in Chapter 9)

Germany

UK

France

Italy

Spain

Others

Asia-Pacific (Covered in Chapter 10)

China

Japan

India

South Korea

Southeast Asia

Others

Middle East and Africa (Covered in Chapter 11)

Saudi Arabia

UAE

South Africa

Others

ALSO READ : http://www.marketwatch.com/story/global-hazardous-location-led-lights-market-size-share-value-and-competitive-landscape-2024-2021-05-10

South America (Covered in Chapter 12)

Brazil

Others

Years considered for this report:

Historical Years: 2015-2019

Base Year: 2019

Estimated Year: 2020

Forecast Period: 2020-2025

Table of Contents

1 Student Loan Servicing Market - Research Scope

1.1 Study Goals

1.2 Market Definition and Scope

1.3 Key Market Segments

1.4 Study and Forecasting Years

2 Student Loan Servicing Market - Research Methodology

2.1 Methodology

2.2 Research Data Source

2.2.1 Secondary Data

2.2.2 Primary Data

2.2.3 Market Size Estimation

2.2.4 Legal Disclaimer

ALSO READ : http://www.marketwatch.com/story/student-loan-market-research-report-with-size-share-value-cagr-outlook-analysis-latest-updates-data-and-news-2020-2025-2021-06-22

3 Student Loan Servicing Market Forces

3.1 Global Student Loan Servicing Market Size

3.2 Top Impacting Factors (PESTEL Analysis)

3.2.1 Political Factors

3.2.2 Economic Factors

3.2.3 Social Factors

3.2.4 Technological Factors

3.2.5 Environmental Factors

3.2.6 Legal Factors

3.3 Industry Trend Analysis

3.4 Industry Trends Under COVID-19

3.4.1 Risk Assessment on COVID-19

3.4.2 Assessment of the Overall Impact of COVID-19 on the Industry

3.4.3 Pre COVID-19 and Post COVID-19 Market Scenario

3.5 Industry Risk Assessment

4 Student Loan Servicing Market - By Geography

4.1 Global Student Loan Servicing Market Value and Market Share by Regions

4.1.1 Global Student Loan Servicing Value ($) by Region (2015-2020)

4.1.2 Global Student Loan Servicing Value Market Share by Regions (2015-2020)

4.2 Global Student Loan Servicing Market Production and Market Share by Major Countries

4.2.1 Global Student Loan Servicing Production by Major Countries (2015-2020)

4.2.2 Global Student Loan Servicing Production Market Share by Major Countries (2015-2020)

4.3 Global Student Loan Servicing Market Consumption and Market Share by Regions

4.3.1 Global Student Loan Servicing Consumption by Regions (2015-2020)

4.3.2 Global Student Loan Servicing Consumption Market Share by Regions (2015-2020)

5 Student Loan Servicing Market - By Trade Statistics

5.1 Global Student Loan Servicing Export and Import

……continued

CONTACT DETAILS :

+44 203 500 2763

+1 62 825 80070

971 0503084105

0 notes

Photo

How are Online Aggregators gaining momentum in UAE? – Ken Research Buy Now Traditionally banks provided limited transparency on loan pricing & charges, making customers call up/visit bank branches just to attain basic loan pricing information.

#BankOnUs Credit Cards Online Market Revenue#Commission Rate Online Aggregators UAE#COVID 19 Impact on UAE Loan Industry#Credit Outstanding in the UAE in AED#Fee rate Loan disbursement UAE#Future of UAE Online Loan Aggregator Market#Future Outlook of Retail Lending & Online Loan Aggregators#Impact of COVID 19 on UAE Loan Industry#Major Loan Providers in UAE#Online Broker vs Online Aggregators UAE#Online Loan Aggregator Industry UAE#Online Loan Aggregator Market UAE#Online Loan Industry in UAE#Online Loans Market in UAE#PolicyBazaar UAE Credit Cards Revenue#PolicyBazaar UAE Online Loan Market Share#PolicyBazaar UAE Personal Loan Revenue#Revenue Loan Aggregators UAE#Souqalmal UAE Personal Loan Revenue#UAE Cash Loans Online Loan Market#UAE Credit Cards Online Market#UAE Fintech Market#UAE Online Aggregator Services Market#UAE Online Car Loan Market#UAE Online Distribution Loan UAE#UAE Online Loan Aggregator Industry#UAE Online Loan Aggregator Industry Research Report#UAE Online Loan Aggregator Market#UAE Online Loan Aggregator Market Analysis#UAE Online Loan Aggregator Market Forecast

0 notes

Link

Overview for “Mortgage Outsourcing Market” Helps in providing scope and definitions, Key Findings, Growth Drivers, and Various Dynamics.

The global Mortgage Outsourcing market focuses on encompassing major statistical evidence for the Mortgage Outsourcing industry as it offers our readers a value addition on guiding them in encountering the obstacles surrounding the market. A comprehensive addition of several factors such as global distribution, manufacturers, market size, and market factors that affect the global contributions are reported in the study. In addition the Mortgage Outsourcing study also shifts its attention with an in-depth competitive landscape, defined growth opportunities, market share coupled with product type and applications, key companies responsible for the production, and utilized strategies are also marked.

This intelligence and 2026 forecasts Mortgage Outsourcing industry report further exhibits a pattern of analyzing previous data sources gathered from reliable sources and sets a precedented growth trajectory for the Mortgage Outsourcing market. The report also focuses on a comprehensive market revenue streams along with growth patterns, analytics focused on market trends, and the overall volume of the market.

Moreover, the Mortgage Outsourcing report describes the market division based on various parameters and attributes that are based on geographical distribution, product types, applications, etc. The market segmentation clarifies further regional distribution for the Mortgage Outsourcing market, business trends, potential revenue sources, and upcoming market opportunities.

Download PDF Sample of Mortgage Outsourcing Market report @https://www.arcognizance.com/enquiry-sample/1586883

Key players in the global Mortgage Outsourcing market covered in Chapter 12:

Outsource2india

Mphasis

SLK Global Solutions

Sutherland Global Services Inc.

Verity Global Solutions

Invensis

WNS

AT Kearney

In Chapter 4 and 14.1, on the basis of types, the Mortgage Outsourcing market from 2015 to 2025 is primarily split into:

On-line

Offline

In Chapter 5 and 14.2, on the basis of applications, the Mortgage Outsourcing market from 2015 to 2025 covers:

Bank

Loan company

Other

Brief about Mortgage Outsourcing Market Report with TOC@https://www.arcognizance.com/report/covid-19-outbreak-global-mortgage-outsourcing-industry-market-report-development-trends-threats-opportunities-and-competitive-landscape-in-2020

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historic and forecast (2015-2025) of the following regions are covered in Chapter 6, 7, 8, 9, 10, 11, 14:

North America (Covered in Chapter 7 and 14)

United States

Canada

Mexico

Europe (Covered in Chapter 8 and 14)

Germany

UK

France

Italy

Spain

Russia

Others

Asia-Pacific (Covered in Chapter 9 and 14)

China

Japan

South Korea

Australia

India

Southeast Asia

Others

Middle East and Africa (Covered in Chapter 10 and 14)

Saudi Arabia

UAE

Egypt

Nigeria

South Africa

Others

South America (Covered in Chapter 11 and 14)

Brazil

Argentina

Columbia

Chile

Others

Regional scope can be customized

Get 20% complementary customization along with purchase of Mortgage Outsourcing Industry report@https://www.arcognizance.com/purchase/1586883

Some Point of Table of Content:

Chapter One: Mortgage Outsourcing Introduction and Market Overview

Chapter Two: Executive Summary

Chapter Three: Industry Chain Analysis

Chapter Four: Global Mortgage Outsourcing Market, by Type

Chapter Five: Mortgage Outsourcing Market, by Application

Chapter Six: Global Mortgage Outsourcing Market Analysis by Regions

Chapter Seven: North America Mortgage Outsourcing Market Analysis by Countries

Chapter Eight: Europe Mortgage Outsourcing Market Analysis by Countries

Chapter Nine: Asia Pacific Mortgage Outsourcing Market Analysis by Countries

Chapter Ten: Middle East and Africa Mortgage Outsourcing Market Analysis by Countries

Chapter Eleven: South America Mortgage Outsourcing Market Analysis by Countries

Chapter Twelve: Competitive Landscape

12.1 Outsource2india

12.1.1 Outsource2india Basic Information

12.1.2 Mortgage Outsourcing Product Introduction

12.1.3 Outsource2india Production, Value, Price, Gross Margin 2015-2020

12.2 Mphasis

12.2.1 Mphasis Basic Information

12.2.2 Mortgage Outsourcing Product Introduction

12.2.3 Mphasis Production, Value, Price, Gross Margin 2015-2020

12.3 SLK Global Solutions

12.3.1 SLK Global Solutions Basic Information

12.3.2 Mortgage Outsourcing Product Introduction

12.3.3 SLK Global Solutions Production, Value, Price, Gross Margin 2015-2020

12.4 Sutherland Global Services Inc.

12.4.1 Sutherland Global Services Inc. Basic Information

12.4.2 Mortgage Outsourcing Product Introduction

12.4.3 Sutherland Global Services Inc. Production, Value, Price, Gross Margin 2015-2020

12.5 Verity Global Solutions

12.5.1 Verity Global Solutions Basic Information

12.5.2 Mortgage Outsourcing Product Introduction

12.5.3 Verity Global Solutions Production, Value, Price, Gross Margin 2015-2020

12.6 Invensis

12.6.1 Invensis Basic Information

12.6.2 Mortgage Outsourcing Product Introduction

12.6.3 Invensis Production, Value, Price, Gross Margin 2015-2020

12.7 WNS

12.7.1 WNS Basic Information

12.7.2 Mortgage Outsourcing Product Introduction

12.7.3 WNS Production, Value, Price, Gross Margin 2015-2020

12.8 AT Kearney

12.8.1 AT Kearney Basic Information

12.8.2 Mortgage Outsourcing Product Introduction

12.8.3 AT Kearney Production, Value, Price, Gross Margin 2015-2020

Chapter Thirteen: Industry Outlook continue…

List of tables

List of Tables and Figures

Figure Product Picture of Mortgage Outsourcing

Table Product Specification of Mortgage Outsourcing

Table Mortgage Outsourcing Key Market Segments

Table Key Players Mortgage Outsourcing Covered

Figure Global Mortgage Outsourcing Market Size, 2015 – 2025

Table Different Types of Mortgage Outsourcing

Figure Global Mortgage Outsourcing Value ($) Segment by Type from 2015-2020

Figure Global Mortgage Outsourcing Market Share by Types in 2019

Table Different Applications of Mortgage Outsourcing

Figure Global Mortgage Outsourcing Value ($) Segment by Applications from 2015-2020

Figure Global Mortgage Outsourcing Market Share by Applications in 2019

Figure Global Mortgage Outsourcing Market Share by Regions in 2019

Figure North America Mortgage Outsourcing Production Value ($) and Growth Rate (2015-2020)

Figure Europe Mortgage Outsourcing Production Value ($) and Growth Rate (2015-2020)

Figure Asia Pacific Mortgage Outsourcing Production Value ($) and Growth Rate (2015-2020)

Figure Middle East and Africa Mortgage Outsourcing Production Value ($) and Growth Rate (2015-2020)

Figure South America Mortgage Outsourcing Production Value ($) and Growth Rate (2015-2020)

Table Global COVID-19 Status and Economic Overview

Figure Global COVID-19 Status

Figure COVID-19 Comparison of Major Countries

Figure Industry Chain Analysis of Mortgage Outsourcing

Table Upstream Raw Material Suppliers of Mortgage Outsourcing with Contact Information

Table Major Players Headquarters, and Service Area of Mortgage Outsourcing

Figure Major Players Production Value Market Share of Mortgage Outsourcing in 2019

Table Major Players Mortgage Outsourcing Product Types in 2019

Figure Production Process of Mortgage Outsourcing

Figure Manufacturing Cost Structure of Mortgage Outsourcing

Figure Channel Status of Mortgage Outsourcing

Table Major Distributors of Mortgage Outsourcing with Contact Information

Table Major Downstream Buyers of Mortgage Outsourcing with Contact Information

Table Global Mortgage Outsourcing Value ($) by Type (2015-2020)

Table Global Mortgage Outsourcing Value Share by Type (2015-2020)

Figure Global Mortgage Outsourcing Value Share by Type (2015-2020)

Table Global Mortgage Outsourcing Production by Type (2015-2020)

Table Global Mortgage Outsourcing Production Share by Type (2015-2020)

Figure Global Mortgage Outsourcing Production Share by Type (2015-2020)

Figure Global Mortgage Outsourcing Value ($) and Growth Rate of On-line (2015-2020)

Figure Global Mortgage Outsourcing Value ($) and Growth Rate of Offline (2015-2020)

Figure Global Mortgage Outsourcing Price by Type (2015-2020)

Figure Downstream Market Overview

Table Global Mortgage Outsourcing Consumption by Application (2015-2020)

Table Global Mortgage Outsourcing Consumption Market Share by Application (2015-2020)

Figure Global Mortgage Outsourcing Consumption Market Share by Application (2015-2020)

Figure Global Mortgage Outsourcing Consumption and Growth Rate of Bank (2015-2020)

Figure Global Mortgage Outsourcing Consumption and Growth Rate of Loan company (2015-2020)

Figure Global Mortgage Outsourcing Consumption and Growth Rate of Other (2015-2020)

Figure Global Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Global Mortgage Outsourcing Revenue (M USD) and Growth (2015-2020)

Table Global Mortgage Outsourcing Sales by Regions (2015-2020)

Table Global Mortgage Outsourcing Sales Market Share by Regions (2015-2020)

Table Global Mortgage Outsourcing Revenue (M USD) by Regions (2015-2020)

Table Global Mortgage Outsourcing Revenue Market Share by Regions (2015-2020)

Table Global Mortgage Outsourcing Revenue Market Share by Regions in 2015

Table Global Mortgage Outsourcing Revenue Market Share by Regions in 2019

Figure North America Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Europe Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Asia-Pacific Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Middle East and Africa Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure South America Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure North America COVID-19 Status

Figure North America COVID-19 Confirmed Cases Major Distribution

Figure North America Mortgage Outsourcing Revenue (M USD) and Growth (2015-2020)

Table North America Mortgage Outsourcing Sales by Countries (2015-2020)

Table North America Mortgage Outsourcing Sales Market Share by Countries (2015-2020)

Table North America Mortgage Outsourcing Revenue (M USD) by Countries (2015-2020)

Table North America Mortgage Outsourcing Revenue Market Share by Countries (2015-2020)

Figure United States Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Canada Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Mexico Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Europe COVID-19 Status

Figure Europe COVID-19 Confirmed Cases Major Distribution

Figure Europe Mortgage Outsourcing Revenue (M USD) and Growth (2015-2020)

Table Europe Mortgage Outsourcing Sales by Countries (2015-2020)

Table Europe Mortgage Outsourcing Sales Market Share by Countries (2015-2020)

Table Europe Mortgage Outsourcing Revenue (M USD) by Countries (2015-2020)

Table Europe Mortgage Outsourcing Revenue Market Share by Countries (2015-2020)

Figure Germany Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure UK Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure France Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Italy Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Spain Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Russia Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Asia Pacific COVID-19 Status

Figure Asia Pacific Mortgage Outsourcing Revenue (M USD) and Growth (2015-2020)

Table Asia Pacific Mortgage Outsourcing Sales by Countries (2015-2020)

Table Asia Pacific Mortgage Outsourcing Sales Market Share by Countries (2015-2020)

Table Asia Pacific Mortgage Outsourcing Revenue (M USD) by Countries (2015-2020)

Table Asia Pacific Mortgage Outsourcing Revenue Market Share by Countries (2015-2020)

Figure China Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure Japan Mortgage Outsourcing Sales and Growth Rate (2015-2020)

Figure South Korea Mortgage Outsourcing Sales and Growth (2015-2020)

Figure India Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Southeast Asia Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Australia Mortgage Outsourcing Sales and Growth (2015-2020)

Figure Middle East Mortgage Outsourcing Revenue (M USD) and Growth (2015-2020)continue…

If you have any special requirements, please let us know and we will offer you the report as you want.

About Us:

Analytical Research Cognizance (ARC) is a trusted hub for research reports that critically renders accurate and statistical data for your business growth. Our extensive database of examined market reports places us amongst the best industry report firms. Our professionally equipped team further strengthens ARC’s potential.

ARC works with the mission of creating a platform where marketers can have access to informative, latest and well researched reports. To achieve this aim our experts tactically scrutinize every report that comes under their eye.

Contact Us:

Ranjeet Dengale

Director Sales

Analytical Research Cognizance

+1 (646) 403-4695, +91 90967 44448

Email: [email protected]

0 notes

Text

Global Peer to Peer (P2P) Lending Market Audience, Geographies and Key Players 2026

Summary

A new market study, titled “Global Peer to Peer (P2P) Lending Market Report 2020 by Key Players, Types, Applications, Countries, Market Size, Forecast to 2026 (Based on 2020 COVID-19 Worldwide Spread) ” has been featured on WiseGuyReports.

The Peer to Peer (P2P) Lending market is expected to grow from USD X.X million in 2020 to USD X.X million by 2026, at a CAGR of X.X% during the forecast period. The global Peer to Peer (P2P) Lending market report is a comprehensive research that focuses on the overall consumption structure, development trends, sales models and sales of top countries in the global Peer to Peer (P2P) Lending market. The report focuses on well-known providers in the global Peer to Peer (P2P) Lending industry, market segments, competition, and the macro environment.

Under COVID-19 Outbreak, how the Peer to Peer (P2P) Lending Industry will develop is also analyzed in detail in Chapter 1.7 of the report.

In Chapter 2.4, we analyzed industry trends in the context of COVID-19.

In Chapter 3.5, we analyzed the impact of COVID-19 on the product industry chain based on the upstream and downstream markets.

In Chapters 6 to 10 of the report, we analyze the impact of COVID-19 on various regions and major countries.

In chapter 13.5, the impact of COVID-19 on the future development of the industry is pointed out.

ALSO READ: https://industrytoday.co.uk/finance/peer-to-peer--p2p--lending-2020-global-market-key-players---funding-circle-limited--lendup--auxmoney-gmbh--peerform--ondeck-capital--inc----analysis-and-forecast-to-2026-

A holistic study of the market is made by considering a variety of factors, from demographics conditions and business cycles in a particular country to market-specific microeconomic impacts. The study found the shift in market paradigms in terms of regional competitive advantage and the competitive landscape of major players.

Key players in the global Peer to Peer (P2P) Lending market covered in Chapter 4:

Funding Circle Limited

LendUp

Auxmoney GmbH

Peerform

onDeck Capital, Inc.

Social Finance, Inc.

Daric

Circleback Lending, LLC.

RateSetter

Avant, Inc.

Prosper Marketplace, Inc.

Isepankur

Zopa Limited

Kabbage, Inc.

LendingClub Corporation

In Chapter 11 and 13.3, on the basis of types, the Peer to Peer (P2P) Lending market from 2015 to 2026 is primarily split into:

Consumer Lending

Business Lending

In Chapter 12 and 13.4, on the basis of applications, the Peer to Peer (P2P) Lending market from 2015 to 2026 covers:

Consumer Credit Loans

Small Business Loans

Student Loans

Real Estate Loans

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historic and forecast (2015-2026) of the following regions are covered in Chapter 5, 6, 7, 8, 9, 10, 13:

North America (Covered in Chapter 6 and 13)

United States

Canada

Mexico

Europe (Covered in Chapter 7 and 13)

Germany

UK

France

Italy

Spain

Russia

Others

Asia-Pacific (Covered in Chapter 8 and 13)

China

Japan

South Korea

Australia

India

Southeast Asia

Others

Middle East and Africa (Covered in Chapter 9 and 13)

Saudi Arabia

UAE

Egypt

Nigeria

South Africa

Others

South America (Covered in Chapter 10 and 13)

Brazil

Argentina

Columbia

Chile

Others

Years considered for this report:

Historical Years: 2015-2019

Base Year: 2019

Estimated Year: 2020

Forecast Period: 2020-2026

FOR MORE DETAILS – https://www.wiseguyreports.com/reports/5824836-global-peer-to-peer-p2p-lending-market-report

About Us:

Wise Guy Reports is part of the Wise Guy Research Consultants Pvt. Ltd. and offers premium progressive statistical surveying, market research reports, analysis & forecast data for industries and governments around the globe.

Contact Us:

NORAH TRENT

Ph: +162-825-80070 (US)

Ph: +44 203 500 2763 (UK)

0 notes

Text

GlobalOutbreak-Global Bitcoin Bank Industry Market Size, Share, Value, and Competitive Landscape 2025

The concept of Bitcoin was originally proposed by Nakamoto in 2009. According to the idea of Nakamoto, the open source software was released and the P2P network was constructed. Bitcoin is a digital currency in the form of P2P. Peer-to-peer transmission means a decentralized payment system.

The Bitcoin Bank market revenue was xx.xx Million USD in 2019, and will reach xx.xx Million USD in 2025, with a CAGR of x.x% during 2020-2025.

GET FREE SAMPLE REPORT : https://www.wiseguyreports.com/sample-request/6124105-covid-19-outbreak-global-bitcoin-bank-industry-market

Under COVID-19 outbreak globally, this report provides 360 degrees of analysis from supply chain, import and export control to regional government policy and future influence on the industry. Detailed analysis about market status (2015-2020), enterprise competition pattern, advantages and disadvantages of enterprise products, industry development trends (2020-2025), regional industrial layout characteristics and macroeconomic policies, industrial policy has also been included. From raw materials to end users of this industry are analyzed scientifically, the trends of product circulation and sales channel will be presented as well. Considering COVID-19, this report provides comprehensive and in-depth analysis on how the epidemic push this industry transformation and reform.

ALSO READ : https://icrowdnewswire.com/2021/01/15/global-bitcoin-bank-industry-analysis-2021-market-growth-trends-opportunities-and-forecast-to-2026/

In COVID-19 outbreak, Chapter 2.2 of this report provides an analysis of the impact of COVID-19 on the global economy and the Bitcoin Bank industry.

Chapter 3.7 covers the analysis of the impact of COVID-19 from the perspective of the industry chain.

In addition, chapters 7-11 consider the impact of COVID-19 on the regional economy.

The Bitcoin Bank market can be split based on product types, major applications, and important countries as follows:

Key players in the global Bitcoin Bank market covered in Chapter 12:

Mizuho

Coinbase

E-Btcbank

Circle

Elliptic Vault

Robinhood

NextBank

Bitbank

ALSO READ : https://www.einpresswire.com/article/451372393/mobile-gaming-market-2018-global-key-players-trends-share-industry-size-segmentation-opportunities-forecast-2025

In Chapter 4 and 14.1, on the basis of types, the Bitcoin Bank market from 2015 to 2025 is primarily split into:

Commercial Bank

Tech Company

In Chapter 5 and 14.2, on the basis of applications, the Bitcoin Bank market from 2015 to 2025 covers:

Depository

Loan

Others

ALSO READ : http://www.marketwatch.com/story/global-electronic-manufacturing-software-industry-analysis-2021-market-growth-trends-opportunities-and-forecast-to-2027-2021-01-11

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historic and forecast (2015-2025) of the following regions are covered in Chapter 6, 7, 8, 9, 10, 11, 14:

North America (Covered in Chapter 7 and 14)

United States

Canada

Mexico

Europe (Covered in Chapter 8 and 14)

Germany

UK

France

Italy

Spain

Russia

Others

Asia-Pacific (Covered in Chapter 9 and 14)

China

Japan

South Korea

Australia

India

Southeast Asia

Others

Middle East and Africa (Covered in Chapter 10 and 14)

Saudi Arabia

UAE

Egypt

Nigeria

South Africa

Others

South America (Covered in Chapter 11 and 14)

Brazil

Argentina

Columbia

Chile

Others

ALSO READ : https://www.einpresswire.com/article/532807771/full-face-cpap-masks-market-global-demand-growth-opportunities-and-analysis-of-top-key-player-forecast-to-2025

Years considered for this report:

Historical Years: 2015-2019

Base Year: 2019

Estimated Year: 2020

Forecast Period: 2020-2025

0 notes

Text

How has Covid-19 Affected Real Estate Sectors Around the World?

The Covid-19 virus has made this year very unpredictable for everyone, whether it be economists, real estate agents or the general public. Since the past 3 months, the epidemic has affected various countries throughout the world and still continues to wreak havoc. With businesses around the world having to close their doors or adjust to a virtual workplace, the global economy looks unrecognizable.

Real estate is one of the industries that has borne great losses due to the pandemic. However, different countries have their ways of dealing with the issue at hand. This article will discuss how the Covid-19 has affected and continues to affect the real estate sector throughout the world.

UNITED ARAB EMIRATES

With jobs and incomes at risk, many tenants are having trouble paying their rent. To ease their troubles, Al Husn Properties exempted rent for 3 months. Dubai Holding and Meraas announced an economic relief package worth more than AED 1 billion to partially alleviate the burdens of businesses and individuals within the company’s ecosystem. Private real estate companies such as Majid Al Futtaim and Emaar Malls might also have to freeze rents to allow tenants to manage their businesses, as is the case in other regions.

Similar measures may also be extended by office real estate landlords, such as DIFC Investments, to support businesses that aren’t operating at their usual capacities.

According to recent data, up to 50% of homebuyers up to date are not residents of UAE. Which goes to show that a large proportion of the UAE’s residential community has not yet directly invested in the property market.

A massive chunk of the investment coming in to UAE properties, comes from China. As the virus spread in China and disrupted their economy, a lot of that foreign investment stopped coming into UAE properties.

Property developers are now looking towards buyers with strong purchasing power to offset the lack of investment coming in from China. With China out of the picture, there is an increased interest from Africa, Russia, India, and UK.

The property developers and dealers have also shifted their target to the local market, where young Emiratis are buying property at the low current prices with the hopes that the property’s value will rise in the future.

Many people do recognise the long-term benefits of investing in property and while people are working from home, there has been an upward shift in online traffic, as people are researching the property market that much more.

The market and consumer confidence are generally on an upward swing, the long-term economic indicators are positive and the global property guide is showing that the price fall in UAE has slowed down which means it is going to plateau very soon before recovering.

INDIA

The economic growth in India was already at an 11-year-low before the covid-19 pandemic halted economic activity in the country. According to data, house sales in nine major cities of India declined by 30% from October-December 2019 where the festive season failed to revive consumer confidence, which has been down due to large-scale delays in housing projects and increasing cases of builder insolvency.

The pandemic has further dampened the situation. Due to reduced manufacturing and strict restrictions, the supply of construction materials has been delayed, which could push the delivery timelines of many ongoing projects even further.

With business closures and salary cuts, job security is the first priority for many Indians at the moment. These homebuyers are likely to postpone their property decisions until they know which direction the economy is heading, and they have clarity on their job security.

However, like every other country, the government of India is trying to get a grasp on the economy before the situation gets worse. The Reserve Bank of India has injected Rs. 3.74 lakh crore and postponed all term loans by financial institutions, which will help homebuyers and developers by alleviating some of the short-term liquidity pressure.

The Real Estate Regulatory Authority in Maharashtra has announced a 3-month extension in project completion times, to facilitate the developers who are having trouble meeting their timelines due to the current pandemic.

The National Real Estate Council of India has estimated a 10-15% drop in prices of houses in the market. This could be a blessing in disguise for a country where the government was already focusing on lose cost housing. For homebuyers with an adequate cash flow and job security, this would be an excellent opportunity to invest in real estate.

UNITED STATE OF AMERICA

Real estate developers and agents need to understand that things will be weaker this year. Those would-be sellers who have flexibility will be able to defer, the turnover will decline, but there will still be properties coming into the market.

2020 will be a hard year for the economy. Talk of a recession is growing and a lot of small businesses are facing the prospect of low to no revenue. Which could and is leading to mass layoffs and downsizing.

In the housing market, there is to be an expected pullback from the buyers. As the worst hit country in the world by the epidemic, the incomes of Americans are at risk. Due to the reductions in income and closure of businesses, the real estate sector is expected to see price falls.

For a lot of people with wealth tied up in the share market, their wealth has been diminished. This further reduces the capacity for many people to use that wealth to buy into the housing market.

USA has an open house culture in the real estate sector, which requires the buyer’s physical presence at the location. Open houses are normally a crowded event, where all potential buyers come to the location to inspect it and ask questions about it.

These open houses are looking much different now, due to social distancing. With a lot of restrictions and total bans in some areas, selling houses is becoming very difficult. However, people are finding ways to go around the problem.

Pre-registration with a limited number of visitors is being used to ensure that a crowd does not gather at an open house. Some agents are conducting virtual open houses, where they give the potential buyers a virtual tour of the house and answer any questions the buyers may have.

Condition of the American real estate looks grim, but we must also consider that this is the worst hit country in the world. It is bound to have problems above all others. Although, all is not bad.

With dropping interest rates in the country, borrowing rates for developers have dropped. Some say there has been an increase in sellers due to the low interest rate, they want to quickly sell their property and take advantage of the favourable borrowing rates.

There has been an increased in the demand side as well. Some people in densely populated cities like New York are looking for short term rentals in the suburbs which has slightly increased the demand for rented houses.

The Federal Reserve has offered $3 trillion dollars in loans and asset purchases to prevent the economy from seizing up. Along with that, a stimulus package of $2.2 trillion has been introduced to make sure that the poorest of the country are taken care of.

ITALY

2019 was a great year for real estate in Milan, the economic engine of Italy. With record office leasing of 5.2 million square feet and an all-time high office investment of 3.6 billion euros.

Milan was the only Italian city which was looking at rising home prices due to a wave of new luxury development. However, the Covid-19 pandemic changed the face of the Italian economy within just two months.

Everyone has heard about Italy in the news since this virus was declared a pandemic. The country was in a complete shut down and its death toll was sky rocketing. However, the situation has started getting better, the peak of the problem has been crossed.

Italy has moved towards partially loosening its lockdown to jump start the economy again, businesses in some regions have opened up. During the past 2-3 months, Italy’s real estate sector was affected by the lockdown the same way it has affected other countries.

A lack of job security had reduced demand along with a lack of construction materials and labour had slowed down supply.

Over a month ago the Italian government, introduced a moratorium on mortgage and other debt payments during the emergency, to help consumers and businesses cope. During the first week of April, deals had been stopped, with investors becoming more cautious, mainly for value-add deals.

Corporate occupiers have started considering different office layouts to allow employees to come back to the office and still maintain a safe social distance. It may still be too early to assess long-term space requirements but it can be assumed that offices, in the future, would require a greater area per square feet for the same number of employees.

Market sentiment has become more stable compared to the previous week but the ‘wait and see’ approach is common among investors, landlords, corporates and, in general, real estate players.

Some investors, mainly opportunistic, started to ask for new opportunities with higher returns. On the other hand, vendors are still reluctant to put new assets on the market before understanding how tenants’ requests will impact prices and yields.

As mentioned in the discussion above, it seems that the overall trend around the world is towards sustainability and adaptability. Whether it be through deferred rent payments, virtual open houses, or changing marketing strategies.

It is a widely accepted reality that economies are struggling and the real sector has taken a big hit. However, as discussed above, all countries are trying their best to handle the situation in whatever way they see fit, to ensure the least amount of damage to the economy. All predictions from various countries suggest that the worst is now over.

It will get better.

The economy will recover. People will go back to offices. People will go back to open houses. Prices will go back to normal. Things will eventually bounce back – but there will be some business casualties along the way.

Read the full article

0 notes

Text

The global Commercial Banking Market is expected to register a considerable growth by 2027: AMR

Commercial banking system is one of the most important aspect for financial inclusion. Amid COVID 19, the commercial banking sector is expected to gain the market, because the citizens would like to earn interest on the idle amount rather than keeping the amount at home.

Allied Market Research published a new report, titled, " Commercial Banking Market By Products (Industrial Loans, Project Finance, Syndicated Loans, Leasing, Foreign Trade Financing, and Bills of Exchange), and Functions (Accepting Deposits, Advancing Loans, Credit Creation, Financing Foreign Trade, Agency Services and Others): Global Opportunity Analysis and Industry Forecast, 2020-2027." The report offers an extensive analysis of key growth strategies, drivers, opportunities, key segment, Porter’s Five Forces analysis, and competitive landscape. This study is a helpful source of information for market players, investors, VPs, stakeholders, and new entrants to gain thorough understanding of the industry and determine steps to be taken to gain competitive advantage.

The report offers key drivers that propel the growth in the global commercial banking market. These insights help market players in devising strategies to gain market presence. The research also outlined restraints of the market. Insights on opportunities are mentioned to assist market players in taking further steps by determining potential in untapped regions.

Request Sample Report at: https://www.alliedmarketresearch.com/request-toc-and-sample/2450?utm_source=google&utm_medium=Blog&utm_campaign=Aayushi_Aggarwal

The research offers a detailed segmentation of the global commercial banking market. Key segments analyzed in the research include products, functions and region. Extensive analysis of sales, revenue, growth rate, and market share of each segment for the historic period and the forecast period is offered with the help of tables.

The market is analyzed based on regions and competitive landscape in each region is mentioned. Regions discussed in the study include North America (United States, Canada and Mexico), Europe (Germany, France, UK, Russia and Italy), Asia-Pacific (China, Japan, Korea, India and Southeast Asia), South America (Brazil, Argentina, Colombia), Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria and South Africa). These insights help to devise strategies and create new opportunities to achieve exceptional results.

The research offers an extensive analysis of key players active in the global commercial banking industry. Detailed analysis on operating business segments, product portfolio, business performance, and key strategic developments is offered in the research. Leading market players analyzed in the report include Industrial and Commercial Bank of China, China Construction Bank Corporation, Agriculture Bank of China, J.P. Morgan Chase, HSBC Holdings PLC, Bank of America, Wells Fargo, BNP Paribas, Mitsubishi UFJ Financial Group, and Bank of China. These players have adopted various strategies including expansions, mergers & acquisitions, joint ventures, new product launches, and collaborations to gain a strong position in the industry.

For Purchase Enquiry at: https://www.alliedmarketresearch.com/request-toc-and-sample/2450?utm_source=google&utm_medium=Blog&utm_campaign=Aayushi_Aggarwal

Key Benefits:

· The report provides a qualitative and quantitative analysis of the current commercial banking market trends, forecasts, and market size from 2020 to 2027 to determine new opportunities.

· Porter’s Five Forces analysis highlights the potency of buyers and suppliers to enable stakeholders to make strategic business decisions and determine the level of competition in the industry.

· Top impacting factors & major investment pockets are highlighted in the research.

· The major countries in each region are analyzed and their revenue contribution is mentioned.

· The market player positioning segment provides an understanding of the current position of the market players active in the commercial banking industry.

Key offerings of the report:

· Key drivers & Opportunities: Detailed analysis on driving factors and opportunities in different segments for strategizing.

· Current trends & forecasts: Comprehensive analysis on latest trends, development, and forecasts for next few years to take next steps.

· Segmental analysis: Each segment analysis and driving factors along with revenue forecasts and growth rate analysis.

· Regional Analysis: Thorough analysis of each region help market players devise expansion strategies and take a leap.

· Competitive Landscape: Extensive insights on each of the leading market players for outlining competitive scenario and take steps accordingly.

About Us

Allied Market Research (AMR) is a market research and business-consulting firm of Allied Analytics LLP, based in Portland, Oregon. AMR offers market research reports, business solutions, consulting services, and insights on markets across 11 industry verticals. Adopting extensive research methodologies, AMR is instrumental in helping its clients to make strategic business decisions and achieve sustainable growth in their market domains. We are equipped with skilled analysts and experts, and have a wide experience of working with many Fortune 500 companies and small & medium enterprises.

Contact:

David Correa

Portland, OR, United States

USA/Canada (Toll Free): +1-800-792-5285, +1-503-894-6022, +1-503-446-1141

UK: +44-845-528-1300

Hong Kong: +852-301-84916

India (Pune): +91-20-66346060

Fax: +1(855)550-5975

Web: https://www.alliedmarketresearch.com

Follow Us on LinkedIn: https://www.linkedin.com/company/allied-market-research

0 notes

Text

GCC News Roundup: Saudi Arabia, UAE, Qatar, Kuwait implement new economic measures (April 1-30)

Register at https://mignation.com . The Only Social Network for Migrants. ---

New Post has been published on http://khalilhumam.com/gcc-news-roundup-saudi-arabia-uae-qatar-kuwait-implement-new-economic-measures-april-1-30/

GCC News Roundup: Saudi Arabia, UAE, Qatar, Kuwait implement new economic measures (April 1-30)

By Sumaya Attia Gulf economies struggle as crude futures collapse

Gulf debt and equity markets fell on April 21 and the Saudi currency dropped in the forward market, after U.S. crude oil futures collapsed below $0 on a coronavirus-induced supply glut. Saudi Arabia’s central bank foreign reserves fell in March at their fastest rate in at least 20 years and to their lowest since 2011, while the kingdom slipped into a $9 billion budget deficit in the first quarter. GCC countries cut oil production following OPEC+ deal OPEC, Russia and other oil-producing nations on April 12 finalized an unprecedented production cut of nearly 10 million barrels, or a tenth of global supply, in hopes of boosting crashing prices amid the coronavirus pandemic and a price war, officials said. Following the deal, Saudi Arabia announced its official crude pricing (OSP) for May, selling oil more cheaply to Asia while keeping prices flat for Europe and raising them for the United States. Oman has told its oil producing companies to cut 200,000 barrels per day (bpd) starting from May 1 until the end of June in line with OPEC+ crude supply reduction pact and will inform its customers of the same plan, its oil ministry said. The United Arab Emirates (UAE) is committed to reducing oil production from its current level of 4.1 million bpd, energy minister Suhail Al Mazrouei said in a tweet on April 12. Kuwait’s oil minister said on April 12 that his country would be cutting more than 1 million bpd in actual oil supply, taking into consideration its current April production of around 3.25 million bpd. Gulf states adjust curfews, airport restrictions Saudi Arabia eased curfews on April 26 across the country but kept 24-hour lockdowns in place in the city of Mecca and neighborhoods previously put in isolation to curb the spread of the new coronavirus, state news agency SPA said. The country also said it would allow entry into and exit from Qatif province starting April 30. Meanwhile, the emirate of Dubai said on April 26 it had lifted its full lockdown on two commercial districts that have a large population of low-income migrant workers, after the UAE eased nationwide coronavirus curfews the previous weekend Kuwait decided to extend the suspension of work in the public sector including at government ministries until May 31 and expand a nationwide curfew to 16 hours as part of efforts to combat the coronavirus, a government spokesman said on April 20. Bahrain reopened the Bahrain International Airport for transit passengers, Manama-based Gulf Air said on April 4, though entry to the country remains limited to Bahraini nationals and residents. Saudi Arabia, UAE, Qatar, Kuwait implement new economic measures Saudi Arabia was set to raise $7 billion with a three-tranche bond deal on April 15, a document showed, as the world’s biggest oil exporter seeks to replenish state coffers battered by low oil prices and expectations of lower output. King Salman has also ordered up to 9 billion riyals ($2.4 billion) to be disbursed to pay part of the wages of private-sector workers to deter companies from laying off staff, the state-run Saudi Press Agency reported on April 3. The UAE central bank has urged commercial lenders to use the $70 billion-worth of capital and liquidity measures launched by the regulator to support the economy during the coronavirus outbreak, reported Reuters on April 13. Dubai’s department of finance has told all government agencies to slash capital spending by at least half and halt new hiring until further notice, in response to the coronavirus outbreak, reported Reuters on April 9. Qatar’s ruler has asked the government to postpone $8.2 billion in unawarded contracts on capital expenditure projects due to the coronavirus outbreak, according to a bond prospectus dated April 7. Kuwait announced measures early on April 1 aimed at shoring up its economy against the coronavirus pandemic, including soft long-term loans from local banks. The country’s central bank asked banks to ease loan repayments for companies affected. Gulf states deport and repatriate migrant workers due to coronavirus The UAE and Pakistan are working to add more flights to repatriate Pakistani citizens, a Dubai government source said on April 22. More than 20,000 Pakistani workers stuck in the UAE have registered since April 3 with the consulate to go home, as the Gulf Arab state tightens restrictions due to the coronavirus outbreak. Qatar detained dozens of migrant workers and expelled them in March after telling them they were being taken to be tested for the new coronavirus, human rights group Amnesty International said on April 15. Saudi Arabia has deported 2,870 Ethiopian migrants to Addis Ababa since the start of the coronavirus pandemic, the U.N. migration agency said on April 13, urging Riyadh to suspend the practice for the time being. Saudi Arabia ends flogging, death sentences for minors Saudi Arabia said on April 26 that it would no longer impose the death sentence on individuals who committed crimes while still minors, according to a statement from the state-backed Human Rights Commission (HRC), which cited a royal decree by King Salman. The country also said that it is ending flogging as a form of punishment, according to a document from the kingdom’s top court seen by Reuters on April 24. GCC monarchies to establish food supply safety network The Gulf Cooperation Council’s (GCC) six Arab monarchies have approved Kuwait’s proposal for a common network for food supply safety, the state-run Kuwait News Agency reported on April 16. The decision was taken after a virtual meeting of GCC trade and industry ministers to discuss the COVID-19 outbreak’s impact on food supply safety. Qatar pushes back against US accusations of World Cup bribery The organizers of the 2022 World Cup in Qatar have strongly denied allegations from the U.S. Department of Justice that bribes were paid to secure votes for the hosting rights to the tournament. On April 6, for the first time, prosecutors set direct, formal allegations regarding the 2018 and 2022 World Cups down in an indictment.

0 notes

Text

UAE banking sector better prepared to withstand COVID-19 impact

A futuristic Emirates NBD department in Dubai. Monetary establishments that leverage expertise and information to ship could also be in a better place to drive enterprise progress and overcome disruption attributable to the worldwide COVID-19 pandemic, in accordance to KPMG’s newest UAE Banking Views report.

Picture Credit score: DailyKhaleej Archives

Dubai: Monetary establishments that leverage expertise and information to ship could also be in a better place to drive enterprise progress and overcome disruption attributable to the worldwide COVID-19 pandemic, in accordance to KPMG’s UAE Banking Views report.

In accordance to KPMG examine the UAE banks can have to intently study their enterprise continuity plans, in gentle of the present Covid-19 risk.

“Banks and other financial institutions are faced with tough times ahead, but technology can help mitigate negative effects for customers and business,” stated Abbas Basrai, Companion and Head of Monetary Companies, KPMG Decrease Gulf.

“Banks that effectively leverage their digital assets, bolster cyber resilience and manage third-party risks will likely reap the benefits of increased revenue streams, regulatory compliance and enhanced operational efficiency.”

Stimulus assist

The Central Financial institution of the UAE (CBUAE) has been proactive in rolling out stimulus packages and has introduced a complete Dh256 billion ‘Targeted Economic Support Scheme’ to comprise the repercussions of the pandemic.

Banks and different monetary establishments are confronted with robust occasions forward, however expertise might help mitigate detrimental results for purchasers and enterprise.

– Abbas Basrai, Companion and Head of Monetary Companies, KPMG Decrease Gulf

The CBUAE is permitting banks to free-up their regulatory capital buffers to increase lending capability and assist the UAE financial system; all banks working within the UAE can have entry to loans and advances prolonged at zero price in opposition to collateral by the CBUAE.

All banks will likely be allowed to faucet right into a most of 60 per cent of their capital conservation buffer, and people designated as systemically essential will likely be ready to use 100 per cent of their extra capital buffer for issues of systemic significance.

The CBUAE can also be lowering the quantity of capital banks have to maintain for his or her loans to SMEs by 15 to 25 per cent. This transformation, which is broadly in step with the minimal requirements set by the Basel Committee, will facilitate additional entry of SMEs to financing, and the CBUAE may even revise the prevailing restrict which units the utmost publicity that banks can have to the actual property sector. Banks will likely be allowed to improve it to 30 per cent, however will then be required to maintain extra capital.

“Major banks in the UAE have been proactive in providing financial relief to customers, in line with the CBUAE’s Dh256 billion economic stimulus package,” stated Emilio Pera, Companion, Head of Audit KPMG Decrease Gulf.

Authorities assist

The Dubai and Abu Dhabi governments are additionally being proactive in rolling out stimulus packages with the intention of optimizing prices and supporting companies.

The packages embrace a variety of initiatives geared toward lowering the price of doing enterprise and simplifying enterprise procedures, particularly within the industrial, retail, exterior commerce, tourism, and power sectors.

Digital future

The KPMG report confirmed that banks are more and more exploring the idea of ‘banking the ecosystem’, which is an interconnected set of companies, the place clients can fulfill a wide range of wants in a single built-in expertise. This integration of companies might characterize the cornerstone of digital banking within the years to come, making a differentiated expertise that may enhance buyer satisfaction, improve loyalty and generate extra income streams.

In accordance to KPMG examine, the banking trade within the nation the quickly evolving buyer expectations and rising regulatory scrutiny are placing stress on UAE banks to modernize each side of their operations. Many are structuring their companies in new and thrilling methods and are recognizing buyer expertise as a supply of economic worth quite than as a differentiator versus their competitors.

The report additionally noticed a wholesome pattern of accelerating banking profitability over the previous three years, with whole progress of 13.9 per cent in internet revenue among the many prime ten UAE banks in 2019. The first cause seems to be stronger non-interest revenue efficiency and sure one-off occasions, with revenues flowing in from price revenue and decrease credit score provisioning.

A comparability of key indicators corresponding to loans to deposit ratio (LDR), capital adequacy ratio (CAR) and liquidity ratios of prime 10 UAE banks.

Picture Credit score: KPMG