#REALISTICALLY i feel like net would be grossed out by a situation like this but i can draw what i want!!! heheheh

Text

self-indulgent fnin doodles cause existance is Not Fun right now:/

#my art#felix and nika bonding over having the worst organ in the human body(uterus)(i HATE that bitch)#sorry this is kinda dumb but. yeah..#REALISTICALLY i feel like net would be grossed out by a situation like this but i can draw what i want!!! heheheh#so hes cool and supportive. cause i think that would be neat#uhhhhh actually ive been thinkin about net recently..#okay so hear me out- transfem net.#like........ the casual misoginy and shit being a product of net's weird love-hate relationship with feminity???#they want and crave it but always saw being a girl as 'playing w/ barbie dolls' and 'not understanding technology' and they dont want THAT#but they want to be called pretty and wear a dress sometimes?#so he just kinda represses all those weird complicated feelings and tries his best to be manly and strong and#Not Like Those Stupid Girls who are beyond his comprehension#and then maybe felix comes out as a trans guy and net decides to do some research on trans ppl and#actually starts to realise they relate to these people??#and it takes a LOT of time and introspection but she figures it out. eventually.#and shes still Net! she still scoffs at romantic musicals and is terminally online and a teenage genius and a snarky bitch-#but she also doesnt have to prove her masculinity to anyone. she doesnt have to put girls down for being girls and she#starts to appriciate them as people and not prizes to be won by boys#i dont know if this makes any sense whatsoever but...... i like this idea! i like net realising casual sexism Is Not Funny Actually#i like nika helping her figure things out and try diffrent things and see feminity as something fun and exciting#like i dont think net would suddenly start wearing all pink or something! shes just. herself.#and that means watching horror movies and saving the world from an evil a.i. and movie nights at felixs and hating to admit when shes wrong#yeah. something to think about i guess.#fnin#felix net i nika#sorry this propably makes no sense lol

6 notes

·

View notes

Text

I want to preface this confession by saying that I have no stake in the discussion. I am not trans, I am not from the UK and I don't care about HP. I made business with V0lks in the past and will continue to do so and I know some people are calling for a complete boycott of V0lks, but I find that, quite frankly, unnecessary. Calling out and boycotting a compony for bad behavior is great, but I see no reason why supporting them for releasing good or 'unproblematic' products should be a bad thing. Anyhow..

The HP franchise or 'W1zarding W0rld' is listed on Wikipedia's 'List of highest-grossing media franchises' as spot Number 10, with a total revenue of $30.06 billion. Realistically speaking, boycotting a doll line will have very little effect on the franchise as a whole. It might stop V0lks from making more HP dolls, but that's about it. I get the argument, it's not just about the dolls, the franchise should be boycotted in all of it's forms. With how popular it is, however, I don't think that's really feasible.

It's hard to find numbers on this, but HP is fairly popular all around the world. One of their mobile games made a whole lot of money over in China last year for example. I think it's pretty reasonable to assume that most fans of HP are likely unaware of JKs harmful agenda and then there is also people who buy HP merch not for themselves, but for their loved ones or whatever and they most likely will have even less of a clue about the entire situation regarding the franchise.

So, what now? Educate people, I suppose.

Now, let's say we manage to tell the world all about JKs behavior, etc. and absolutely everyone stops buying into the franchise - or at least enough people stop for it to become unappealing to vendors.

Another quick google search revealed that JK is the seventh richest entrepreneur in the UK, with an estimated net worth of $1 billion. Of course, not all of that is actual money, but I have the strong feeling that she has at least enough cash in her pockets to do whatever the heck she wants for the rest of her life. Even if she didn't earn another penny from today on, she can continue to do what she does, influencing politics, going on cruises, whatever it is rich people do really.

If someone wants to knowingly support JK, that's a decision they have to make for themselves. The impact their decision will have is virtually non-existent, regardless of which choice they make. I don't think it's okay to attack people based on it though and I've seen a couple confessions/comments that got really aggressive and it just baffles me to be honest. I understand where the frustration is coming from, but if you want people to join your cause, don't antagonize them. It's just going to alienate people. I'm not very familiar with sculpts and stuff like that, but maybe someone could compile a list of dolls/sculpts that could work to customize and make 'homebrew' HP dolls. That would be more helpful than hurling insults at each other.

If you really want to do something about the situation go out and educate people within the UK. Voting with your wallet can be a powerful tool, but in this case voting with your, well, vote and getting people to do the same is probably the easier way - even if it's still incredibly hard.

~Anonymous

10 notes

·

View notes

Link

Garment Workers Who Lost Jobs in Pandemic Still Wait for Severance Pay Over a crackling phone line, Ashraf Ali, a 35-year-old father in Bangladesh, described feeling suicidal and desperate to feed his family. Sokunthea Yi, in Cambodia, said she spends sleepless nights worrying about how she will pay off loans she took out to build her house. And at only 23, Dina Arviah in Indonesia said she was hopeless about her future as there were no longer any jobs in her district. All once held jobs as garment workers in factories producing clothes and shoes for companies like Nike, Walmart and Benetton. But in the last 12 months those jobs have disappeared, as major brands in the United States and Europe canceled or refused to pay for orders in the wake of the pandemic and suppliers resorted to mass layoffs or closures. Most garment workers earn chronically low wages, and few have any savings. Which means the only thing standing between them and dire poverty are legally mandated severance benefits that most garment workers are owed upon termination, wherever they are in the world. According to a new report from the Worker Rights Consortium, however, garment workers like Mr. Ali, Ms. Yi and Ms. Dina Arviah are being denied some or all of these wages. The study identified 31 export garment factories in nine countries where, the authors concluded, a total of 37,637 fired workers were not paid the full severance pay they legally earned, a collective $39.8 million. According to Scott Nova, the group’s executive director, the report covers only about 10 percent of global garment factory closures with mass layoffs in the last year. The group is investigating another 210 factories in 18 countries, leading the authors to estimate that the final data set will detail 213 factories with severance pay violations affecting more than 160,000 workers owed $171.5 million. “Severance wage theft has been a longstanding problem in the garment industry, but the scope has dramatically increased in the last year,” Mr. Nova said. He added that the figures were likely to rise as economic aftershocks related to the pandemic continued to unfold across the retail industry. He believes the lost earnings could total between $500 million and $850 million. The report’s authors say the only realistic solution to the crisis would be the creation of a so-called severance guarantee fund. The initiative, devised in conjunction with 220 unions and other labor rights organizations, would be financed by mandatory payments from signatory brands that could then be leveraged in cases of large-scale nonpayment of severance by a factory or supplier. Several household names implicated in the report made money during the pandemic. Amazon, for example, reported an increase in net profit of 84 percent in 2020, while Inditex made 11.4 billion euros, about $13.4 billion, in gross profit. Nike, Next and Walmart all also had healthy earnings. Some industry experts believe the purchasing practices of the industry’s power players are a major contributor to the severance pay crisis. The overwhelming majority of fashion retailers do not own their own production facilities, instead contracting with factories in countries where labor is cheap. The brands dictate prices, often squeezing suppliers to offer more for less, and can shift sourcing locations at will. Factory owners in developing countries say they are forced to operate on minimal margins, with few able to afford better worker wages or investments in safety and severance. “The onus falls on the supplier,” said Genevieve LeBaron, a professor at the University of Sheffield in England who focuses on international labor standards. “But there is a reason the spotlight keeps falling on larger actors further up the supply chain. Their behavior can impact the ability of factories to deliver on their responsibilities.” “Historically, severance hasn’t received the same amount of attention as other types of compensation,” Ms. LeBaron added. “But it should. Often workers who lose their jobs are at their most vulnerable. When they aren’t paid what they are owed, many are forced into taking desperate or dangerous measures to survive.” All major fashion brands publish a labor rights code of conduct. Most say they guarantee that suppliers will pay workers their legally mandated benefits. But in some cases, factory owners can go into hiding or refuse to pay fired employees. In others, owners claim that exploitative contracts brought them to bankruptcy or made it impossible for them to reserve funds for severance. Caught in the middle are garment workers. In Bangladesh, Mr. Ali worked for 17 years as a knitting operator at the A-One factory in Dhaka before it closed in April 2020, laying off 1,400 workers. The factory, which Benetton and Next listed as a supplier, was late paying workers in its final months and has yet to offer any severance pay, which by Bangladeshi law equates to roughly one month of wages per year of service. Mr. Ali, who is owed 350,000 taka, about $4,130, has struggled to find anything other than casual construction work since. “So many people have lost their jobs, which makes the situation all the more desperate,” Mr. Ali said in Bengali. “I want to believe that the money will come, as it would change everything for me.” Updated April 5, 2021, 4:37 a.m. ET The former owner of A-One did not respond to emailed requests for comment. Benetton, in a statement over email, called the commercial value of its relationship with A-One “marginal” and did not respond to questions about severance payments. A spokesman for Next said that the factory had previously produced orders for a subsidiary brand, Lipsy, and that the brand’s code of conduct included checks to ensure workers received what was owed to them after factory closures or layoffs. The company did not respond to any questions about missing severance payments by A-One. When contacted by The New York Times about wage theft at factories, most brands downplayed their relationships, even though corporate codes of conduct do not specify that responsibilities to workers are proportionate to their order size. Ms. Yi was one of 774 workers who were laid off in June from Hana I, a factory in Cambodia that supplied Walmart and Zara. The workers are owed more than $1 million in severance, the report estimates. Although she received an initial $500, Ms. Yi, 33, was still owed $1,290 in severance and was still unemployed as of this month. Inditex, the parent company of Zara, said it had not worked with the factory for five years. Walmart said it believed the factory had paid all the severance it legally owed to workers in June. The factory owners did not respond to requests for comment via email. “We are saddened by the unfortunate financial hardship that has occurred for many businesses due to the pandemic and are particularly concerned about the impact it has on their employees,” a Walmart spokeswoman said. She noted that the company made efforts to “review and hold suppliers accountable for compliance” with its standards and local laws. Hulu Garment factory in Phnom Penh, a former supplier for Walmart, Amazon, Macy’s and Adidas, owes 1,000 former workers $3.63 million, according to the report. Adidas said it had used the company only for small orders. The owners of Hulu did not respond to a request for comment. Of all the companies approached by The Times, only Gap, which placed orders with factories cited in the report in Indonesia, Cambodia, India and Jordan, specifically said it had investigated allegations made in the report. “In all cases we either confirmed that severance had been provided or remediated any that were outstanding,” a Gap spokeswoman said, adding that the company would investigate any further evidence of severance not being paid out. As consumers put pressure on companies to make amends and clean up their supply chains, brands “are shrinking their supplier bases,” Ms. LeBaron said. “That could well produce long-term benefits, but it will mean further disruption, closures and layoffs,” she said. “And that means the severance dilemma is going to become even more common.” Source link Orbem News #Garment #jobs #Lost #Pandemic #pay #Severance #wait #Workers

0 notes

Text

Thoughts on 7.8 “Pretty in Blue”

I liked this one. Ella’s back story got a little more filled in, so we know what made her so jaded, and Alice and Hook were so good. I do like how Ella is not like Snow White: she’s not so filled with hope as Snow was. She’s kind of more realistic, but then she learns to have hope. I like that. Thoughts below.

Ella’s fear of taking a chance - as I said, I like Ella’s jadedness and how she changes. Her back story is more realistic. She’s coming more from a place of nothing ever working out, and promises being broken. But then she finds out the truth about her mother - that she did love them - and she decides to take a chance for herself. It’s nice. It’s grounded in the real world, where things don’t always work out, but sometimes you go for it anyway and take a chance that, this time, they will. I don’t know: there’s something very real about Ella, in a way the other princesses weren’t. She’s brought something new. I really liked her mother’s story, and the lockets, and her taking a chance with Henry. I loved the callback to Snowing and the net, and Ella saying she’d like Henry’s grandmother :)

Alice and her father - aw! I really like this relationship. I’m not even sorry. Wish Hook is so much better, and you can tell Colin is enjoying himself so much more. He’s really stepped the acting up, because he’s been given more to do, and he and Rose are heartbreaking together. I really believe that they’re father and daughter. Not being able to be together is horrible as well. I’m so rooting for this curse to be broken!

So is the portal to Wonderland always open? - It seemed to be open when Alice jumped through and remained open when Henry jumped through. So, maybe in EF2 there are portals between realms that stay open all the time. Or maybe it’s like the portal from the Underworld - it stays open for a certain length of time. Interesting anyway.

Drizella and Henry - ugh, Drizella go away! She’s obviously got a thing for him, which…ew. Didn’t like the ways she was touching him when she had frozen him, and then she said something about seeing what would happen when Ella was out of the way. Gross.

Is Rogers starting to think Weaver was right? - Weaver says he has no idea what he’s just blown open and then Rogers looked kind of unsure, so is he starting to question whether his partner was telling the truth, and there’s more to this than there appears? Is that why he fobs everyone off by saying he was just doing his job? Think maybe Rogers is coming around…

Eloise and the ‘cake’ - I’m sure there was poison in it! And when Rogers cut into it later, there was like a red smear from the knife, so… Yeah, pretty sure that would have killed him. Or, there was something in the cake that would have meant she could control him or something. She was trying to do magic right after Roni threw the cake in the trash. Just as well Roni knew to throw it away!

Lucy’s ‘dad’ - *sigh* I hate triangles. We don’t need another Kathryn Nolan situation, guys! Still, we saw Henry be the noble guy he is and step aside so that Jacinda could show a good front to get Lucy back. Of course, Dtizella wants to keep Ella and Henry apart, so the curse won’t break, so she’d definitely fix it so they all thought someone else was Lucy’s dad. Nick was ok, but I don’t like triangles. He’s obviously EF2’s version of Jack from the beanstalk story, right? Obviously giants are evil in this realm…

Why does Anastasia have Drizella’s magic? - There was no transfer of magic, was there? Drizella has her own magic, which Regina taught her how to use, so why is she saying Anastasia has her magic? Just jealousy, maybe? That would make sense.

Jacinda gave Lucy up - aw. That makes total sense. Of course she’d feel like she could never beat her stepmother, so she’d give her up to spare herself and Lucy heartbreak. I’m so glad she’s fighting for her now, and the way she’s remembering who she really is by saying they’ll always find each other :)

Rumple keeping his cover - I’m not really sure why he’s doing that. It could be any number of reasons. Maybe it is that he’s trying to lie low so that he can find the Guardian before someone else does. Maybe he’s trying to protect Regina somehow. Maybe he’s even angry with her for teaching Drizella magic, since that led to them all being cursed. Maybe he doesn’t want to get involved in stopping Drizella and Gothel because he’s an addict who’s trying to stay away from the source of his addiction: magic. I do think it’s interesting that he was looking right at Regina the whole time she was talking, as if he was saying ‘yes, I’m awake, but would you shut up?’ or something like that. He’s always pretty deep and always has more than one reason for why he does something. Is he being selfless or selfish? Or both? Maybe he wants Regina to go and find her sister… Maybe he doesn’t feel like he can or should help her because Dark One = dark magic = Darkness that he’s trying to control and keep from getting out of hand. I do think he does need to get involved in this fight at some stage, though. I think he does have to help Regina out, and his grandson. I can’t think that it was easy for him to deny Belle - it didn’t look easy. I think he must have his reasons, though, and I don’t think they’re necessarily bad, because he is a good man.

Roni and Henry on a road trip - :) this scene was funny. Drunk Henry. Scandalised Mama Regina! Obviously Zelena’s in San Francisco. Wonder what happened between the sisters this time to cause their feud.

Rogers and Tilly - aw, they’re each other’s tether to the world :) That was a lovely scene. Whoever wrote that one did a good job on it. But, Tilly, Weaver does care about you! And he is a good man! *Sigh* Rumple makes everyone hate him…

Where is Anastasia? - Ah, Lady Tremaine is one step ahead of her daughter. Interesting…

#ouat#scribbles-by-kate's episode reviews#7.8 pretty in blue#ouat cinderella 2#henry mills#alice jones#rumplestiltskin

1 note

·

View note

Text

Catering Company Business Plans - Why You Need One for Your Catering Startup

Why are You wondering if you actually require a business plan on the catering company? Maybe you're thinking that since you simply intend on beginning a rather modest company it will not really be required. Lots of men and women feel like that and, clearly, a lot of men and women wind up failing in their very first year of business.

We highly recommend that you prevent Getting still another company that computes costs or revealed that the market was not prepared for what they had to provide. Below we've summarized ten reasons why you have to prepare a catering firm business program. We explain how should you take some opportunity to prepare a strategy you'll be increasing your odds of being successful with your catering startup.

1) Start at the Right Direction

Many Entrepreneurs feel they can begin without doing a great deal of preparation and study. They believe they can always get a sense of the company as they proceed. But a number of those early selections that you make in the life span of your company can be hard to undo in a later date. You have to get a very clear route set out before you so you could make the correct decisions concerning how to establish the company right from the beginning.

2) Reinforce Your Ideas

As you gradually get Ideas concerning the catering business you need to begin you will realize that these ideas start floating around on your head. Everything you envision yourself performing is frequently quite different from what you can do so realistically. Nothing is hopeless but you simply have to work out how to get there.

By putting your thoughts down on paper You'll Be Clarifying them on mind. Since you write you will discover that you just do extra brainstorming. You might get new ideas about what you need to do along with your organization and you may decide that a number of the tips you had originally aren't really feasible.

3) Figure Out How To Do It

Each Entrepreneur has an extremely idealistic picture in their mind of the type of company they need. Getting to this point is a procedure though and you have to work out a route to get there.

1 Fantastic Way to figure Out how you'll move is to write down what you wish to do. Then write down as many queries as possible about how you're really going to get it done. These can contain questions such as'Will I do on-site or off-site catering?' , 'How will I get access to kitchen facilities?' Or'How many catering jobs will I need to land each month to break even?' . As you gradually work out the answers to the issues which you stumble around you can write them down at the right segments of your business strategy.

4) Know Your Startup Requirements

When you Prepare a business plan by a business plan consultant you'll find an accurate idea of just what's required before you start the provider. You'll have to take into account each the situations which you'll have to cover before starting like catering equipment, first advertising and so forth. When you have calculated that the entire price then you will know precisely how much cash you'll need and can examine where this financing will come out.

5) Increase Personal Productivity

You Must be organized when you begin a small business. As opposed to writing down things on loose bits of newspaper and hoping for the very best you want to have someplace to compile all the critical information you collect. A business strategy is excellent for this function. Should you store the company plan for a document in your PC that you can just add new info as you run across it. In case you've completed your research and have all you info stored in a convenient place you'll be organized during your small business launch and you'll avoid a great deal of unnecessary headaches.

6) Prove the Viability of Your Idea to Others

A Business program is a superb way to prove to yourself that your thoughts are workable and the catering firm which you're proposing can flourish and turn a profit. You'll also require a plan so as to prove to others the business model which you have in mind would be fiscally sound. Consider your business plan as being just like a resume you could hand out to folks who require information regarding your company. You may always exit sections which aren't pertinent to the reader in question.

There are a Lot of People who Might Wish to view Your Company Strategy and you ought to keep them in mind while you put it all together. If you're trying to find financing then you might need to demonstrate the strategy to potential lenders or equity investors. As a secretary you will definitely need to comply with local health and hygiene requirements and also these regional authorities might expect to observe a part on your strategy relating to those regions. You might even have to demonstrate your company plan to the proprietor of any kitchen assumptions that you aspire to rent till they agree to sign a deal with you.

7) Set Goals and Objectives

A Business strategy is like a road map to achievement. Your objectives are the destinations which you're planning to reach. They ought to be rather sensible and achievable but also needs to compel you to work hard to achieve them. You may establish financial goals that place out which type of gross or net monthly earnings you mean to be earning following your first season. Other targets can also refer to additional metrics like average food cost percentages on catering tasks such as.

8) Identify Weaknesses and Strengths

It Is important to evaluate your strengths and weaknesses and how they will affect you when it comes to competing with the established players on the regional catering market. You will bring competitive benefits of the company such as catering expertise or neighborhood hospitality and food business relations. You might also identify personal flaws which you are able to work on enhancing or flaws your company will confront in comparison to a established opponents.

9) Track Your Progress

A Business plan shouldn't be forgotten about when the catering company has established. Consult with the program regularly to see whether you're on track to reach the targets that you put out. Make modifications to the strategy as you proceed so you have a strategy in place to your company going forward at least 2 or three decades.

10) Make Selling Out a Breeze

Many Caterers wind up selling their companies when they retire or proceed to Additional jobs. A business plan That's up to date can really help if In regards to assessing your company for a possible sale. If your Small Business Provides a purchaser a blueprint for managing the company and it provides Strong evidence that the company is earning a profit then it may really Enable one to seal a bargain at a price that is favorable.

0 notes

Text

"How much house can I afford?"

How much house can I afford? Answering this question correctly is one of the keys to building a happy, wealthy life. Unfortunately, theres a vast housing industry in the U.S. thats geared toward providing the wrong answer.

You see, housing is by far the largest expense in most peoples budgets. According to the U.S. governments 2016 Consumer Expenditure Survey, the average American family spends $1573.83 on housing and related expenses every month. Thats more than they spend on food, clothing, healthcare, and entertainment put together!

Too many folks struggling to make ends meet focus their attention on fine-tuning their budget. They try to save big bucks by clipping coupons, growing their own food, and/or making their own clothes. While theres nothing wrong with frugal habits I applaud everyday thriftiness! all of these actions combined wont (and cant) have the same impact on your budget as keeping your housing payments affordable.

Part of the problem is what I call the Real-Estate Industrial Complex, each piece of which has a vested interest in convincing consumers that bigger, more expensive homes are better. Real-estate agents, mortgage brokers, home-shopping shows, and glossy magazines all encourage folks to buy at the top end of their budget. But buying at the top end of your housing budget is dangerous.

Buying a home is a huge decision, financially and otherwise. If youre going to purchase a place, its important to know how much house you can truly afford.

Debt-to-Income Ratio

Economists have used decades of financial stats to create computer models to predict how much people can afford to spend on housing and debt. Banks use these models to figure out how much they think you can afford to spend on housing.

Traditionally, lenders use whats called a debt-to-income ratio (or DTI ratio) a measure of how much of your income goes toward debt every month to estimate how much you can afford to pay for a home without risk of defaulting. This might sound complicated, but its not.

To find this ratio, divide your monthly debt payments by your gross (pre-tax) income. So, for example, if you pay $400 toward debt every month and you have an income of $4000, then your DTI ratio is 10%. If you pay $800 toward debt on a $4000 income, your DTI ratio is 20%. The lower your debt-to-income ratio, the better.

Banks and mortgage brokers look at two numbers when deciding how much to loan:

The front-end DTI ratio (sometimes called the housing expense ratio), which includes only your housing expenses: mortgage principle, interest, taxes, and insurance.The back-end DTI ratio (also known as the total expense ratio), which include all of the above plus other debt payments like auto loans, student loans, and credit cards.

The key thing to understand about debt-to-income ratios is that theyre used to estimate the lenders risk, not yours. That is, your mortgage company uses them to check whether they think youll be able to make the payments not whether you can comfortably make the payments.

If you want room in your budget for fun, you should opt for a lower debt-to-income ratio than your real-estate agent and mortgage broker say you can use.

If youre a money nerd, you can read more about debt-to-income ratios at Fannie Maes website.

How Much House Can You Afford?

During the 1970s (before credit-card debt was common), DTI wasnt split between front-end and back-end. There was only one ratio, and it was 25%. If your mortgage, taxes, and insurance costs were less than 25% of your income, people assumed you could make the payment.

This is still an excellent rule of thumb: Spend no more than 25% of your budget on housing. (In fact, this is the number that money guru Dave Ramsey advocates.)

That said, debt-to-income guidelines have relaxed over the years.

When my ex-wife and I bought our first home in 1993, our mortgage broker told us that our front-end DTI ratio had to be 28% or lower, meaning we couldnt pay any more than 28% of our gross income toward housing. The back-end DTI ratio was capped at 36%, which meant that our housing expenses and other debt payments combined couldnt be more than 36% of our income.When my ex-wife and I bought a new home in 2004, the accepted DTI ratios had grown by 5%. That 28% figure is outdated, we were told. Most people can go as high as 33%. The back-end ratio had been raised to 38%.According to the Fannie Mae website, in 2018 maximum back-end DTI ratios are up to 45% (and sometimes even 50%). These numbers are insane. Nobody should be spending half of their gross income on debt not even mortgage debt! Thats a recipe for financial disaster.

Heres a little table I whipped up to show what sort of housing payment youd be looking at based on your pre-tax income (the left-hand column) and various debt-to-income ratios (the header row):

A 5% increase in your debt-to-income ratio might not seem like a big deal. But when youre talking about a house payment, its huge.

In 2016, the average American household earned $74,664 before taxes. Using this, a 5% change would be $3733.20 per year or $311.10 per month. Many folks lost their homes during the housing crisis because they took on mortgage payments that were just $300 more than they could afford each month.

Real-Life Examples

When my ex-wife and I moved in 2004, our housing payments went from around $1200 per month to roughly $1600 per month. This $400 per month difference was enough to make me panicked about money.

Similarly, my youngest brother made the mistake of believing the banks when they told him he could afford a big housing payment. He could at first. But when the financial crisis hit in 2008 and 2009, he was screwed. Because hed bought at the top end of his budget, when his income faltered, so did his ability to pay his mortgage. He lost his home to foreclosure.

For the most part, banks are happy to lend you as much money as you want. (Within reason, of course, and if your credit is good.) Theyre not going to stop you from taking on more debt if their computer models say you can afford it. Its up to you to exercise caution.

In The Automatic Millionaire Homeowner, David Bach writes [emphasis is mine]:

You should generally assume that the amount the bank or mortgage company will loan you is more than you should borrowDont fool around with this. Do the math. Be realistic about your situation. Dont pretend youre in better shape than you are.

Remember: Nobody cares more about your money than you do. Your real-estate agent, mortgage broker, and bank all have a vested interest in encouraging you to buy as much house as possible their incomes depend on it. Listen to what they have to say, but make your decision based on whats best for you.

Playing House

If you think youre ready to buy a house, take a few months to do a trial run. In The Money Book for the Young, Fabulous, and Broke, Suze Orman says that you should play house before you buy a house. I like this idea. Heres how it works:

Figure out how much you think you can afford to pay for a home every month, including mortgage and maintenance. Lets use $1750 as an example.Subtract the amount youre currently paying for housing. If your rent (or current mortgage) is $1000 per month, youd subtract this from our hypothetical $1750 to get $750 per month.Open a new, separate savings account. On the first day of each of the next six months, stick $750 into this account.

This exercise lets you experience what its like to make a higher housing payment. If you cant make these numbers work, Orman says you need to wait:

If you miss one payment, or if you are consistently late in making the payments, you are not ready to buy a home. If you can handle the extra payments, then youve got the thumbs-up to start looking for a home to buy.

Generally speaking, once youve saved 20% for a down payment and you can afford monthly mortgage payments, youre ready to start looking for a home. Yes, you can buy a home with a smaller down payment I bought my first place with a 2% down payment! but itll cost you in the long run. Youll need to carry private mortgage insurance (PMI), youll pay more in interest, and you could put yourself in a position where you cant afford to keep your home.

The Bottom Line

Homebuyers are often told to buy as much house as you can afford. But the problem with this advice is that it leaves you without a buffer. What if you lose your job? What if youre forced to sell your home after housing prices have dropped?

Instead of buying as much house as you can afford, buy only as much house as you need. Think of conventional debt-to-income ratios as ceilings, not targets.

Give yourself margin for error. Instead of basing your home-buying budget on a 36% front-end DTI ratio, consider dropping that to 28%. Or, better yet, 25% (just like the olden days!).

If you have an average U.S. household income of around $75,000, a 36% DTI ratio would lead you to budget $2250 per month for housing (assuming you have no other debt). If you were to go with a more conservative 25% DTI ratio, that budget would be $1563 per month. Thats a savings of $687 per month over $8000 per year! Just think: What could you do with a chunk of change like that?

Another way to create a buffer is to base your budget on your net (take-home) pay instead of your gross pay. Or, if youre in a relationship where both partners work, run the numbers for only one of the two incomes.

No, you wont be able to afford a big mortgage if you do what Im recommending. But you know what? You wont feel pinched by your mortgage payments. And youll be at much less risk the next time the housing market implodes. Best of all, you can plow all of the money youve saved on housing into a building a ginormous wealth snowball!

https://www.getrichslowly.org/how-much-house/

0 notes

Text

“How much house can I afford?”

“How much house can I afford?” Answering this question correctly is one of the keys to building a happy, wealthy life. Unfortunately, there’s a vast housing industry in the U.S. that’s geared toward providing the wrong answer.

You see, housing is by far the largest expense in most people’s budgets. According to the U.S. government’s 2016 Consumer Expenditure Survey, the average American family spends $1573.83 on housing and related expenses every month. That’s more than they spend on food, clothing, healthcare, and entertainment put together!

Too many folks struggling to make ends meet focus their attention on fine-tuning their budget. They try to save big bucks by clipping coupons, growing their own food, and/or making their own clothes. While there’s nothing wrong with frugal habits — I applaud everyday thriftiness! — all of these actions combined won’t (and can’t) have the same impact on your budget as keeping your housing payments affordable.

Part of the problem is what I call the Real-Estate Industrial Complex, each piece of which has a vested interest in convincing consumers that bigger, more expensive homes are better. Real-estate agents, mortgage brokers, home-shopping shows, and glossy magazines all encourage folks to buy at the top end of their budget. But buying at the top end of your housing budget is dangerous.

Buying a home is a huge decision, financially and otherwise. If you’re going to purchase a place, it’s important to know how much house you can truly afford.

Debt-to-Income Ratio

Economists have used decades of financial stats to create computer models to predict how much people can afford to spend on housing and debt. Banks use these models to figure out how much they think you can afford to spend on housing.

Traditionally, lenders use what’s called a debt-to-income ratio (or DTI ratio) — a measure of how much of your income goes toward debt every month — to estimate how much you can afford to pay for a home without risk of defaulting. This might sound complicated, but it’s not.

To find this ratio, divide your monthly debt payments by your gross (pre-tax) income. So, for example, if you pay $400 toward debt every month and you have an income of $4000, then your DTI ratio is 10%. If you pay $800 toward debt on a $4000 income, your DTI ratio is 20%. The lower your debt-to-income ratio, the better.

Banks and mortgage brokers look at two numbers when deciding how much to loan:

The front-end DTI ratio (sometimes called the housing expense ratio), which includes only your housing expenses: mortgage principle, interest, taxes, and insurance.

The back-end DTI ratio (also known as the total expense ratio), which include all of the above plus other debt payments like auto loans, student loans, and credit cards.

The key thing to understand about debt-to-income ratios is that they’re used to estimate the lender’s risk, not yours. That is, your mortgage company uses them to check whether they think you’ll be able to make the payments — not whether you can comfortably make the payments.

If you want room in your budget for fun, you should opt for a lower debt-to-income ratio than your real-estate agent and mortgage broker say you can use.

If you’re a money nerd, you can read more about debt-to-income ratios at Fannie Mae’s website.

How Much House Can You Afford?

During the 1970s (before credit-card debt was common), DTI wasn’t split between front-end and back-end. There was only one ratio, and it was 25%. If your mortgage, taxes, and insurance costs were less than 25% of your income, people assumed you could make the payment.

This is still an excellent rule of thumb: Spend no more than 25% of your budget on housing. (In fact, this is the number that money guru Dave Ramsey advocates.)

That said, debt-to-income guidelines have relaxed over the years.

When my ex-wife and I bought our first home in 1993, our mortgage broker told us that our front-end DTI ratio had to be 28% or lower, meaning we couldn’t pay any more than 28% of our gross income toward housing. The back-end DTI ratio was capped at 36%, which meant that our housing expenses and other debt payments combined couldn’t be more than 36% of our income.

When my ex-wife and I bought a new home in 2004, the accepted DTI ratios had grown by 5%. “That 28% figure is outdated,” we were told. “Most people can go as high as 33%.” The back-end ratio had been raised to 38%.

According to the Fannie Mae website, in 2018 maximum back-end DTI ratios are up to 45% (and sometimes even 50%). These numbers are insane. Nobody should be spending half of their gross income on debt — not even mortgage debt! That’s a recipe for financial disaster.

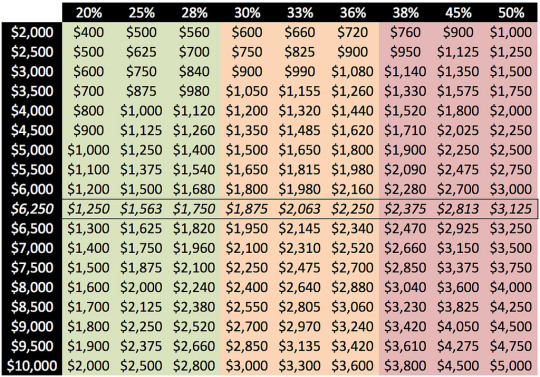

Here’s a little table I whipped up to show what sort of housing payment you’d be looking at based on your pre-tax income (the left-hand column) and various debt-to-income ratios (the header row):

A 5% increase in your debt-to-income ratio might not seem like a big deal. But when you’re talking about a house payment, it’s huge.

In 2016, the average American household earned $74,664 before taxes. Using this, a 5% change would be $3733.20 per year or $311.10 per month. Many folks lost their homes during the housing crisis because they took on mortgage payments that were just $300 more than they could afford each month.

Real-Life Examples

When my ex-wife and I moved in 2004, our housing payments went from around $1200 per month to roughly $1600 per month. This $400 per month difference was enough to make me panicked about money.

Similarly, my youngest brother made the mistake of believing the banks when they told him he could afford a big housing payment. He could at first. But when the financial crisis hit in 2008 and 2009, he was screwed. Because he’d bought at the top end of his budget, when his income faltered, so did his ability to pay his mortgage. He lost his home to foreclosure.

For the most part, banks are happy to lend you as much money as you want. (Within reason, of course, and if your credit is good.) They’re not going to stop you from taking on more debt if their computer models say you can afford it. It’s up to you to exercise caution.

In The Automatic Millionaire Homeowner, David Bach writes [emphasis is mine]:

You should generally assume that the amount the bank or mortgage company will loan you is more than you should borrow…Don’t fool around with this. Do the math. Be realistic about your situation. Don’t pretend you’re in better shape than you are.

Remember: Nobody cares more about your money than you do. Your real-estate agent, mortgage broker, and bank all have a vested interest in encouraging you to buy as much house as possible — their incomes depend on it. Listen to what they have to say, but make your decision based on what’s best for you.

Playing House

If you think you’re ready to buy a house, take a few months to do a trial run. In The Money Book for the Young, Fabulous, and Broke, Suze Orman says that you should “play house before you buy a house”. I like this idea. Here’s how it works:

Figure out how much you think you can afford to pay for a home every month, including mortgage and maintenance. Let’s use $1750 as an example.

Subtract the amount you’re currently paying for housing. If your rent (or current mortgage) is $1000 per month, you’d subtract this from our hypothetical $1750 to get $750 per month.

Open a new, separate savings account. On the first day of each of the next six months, stick $750 into this account.

This exercise lets you experience what it’s like to make a higher housing payment. If you can’t make these numbers work, Orman says you need to wait:

If you miss one payment, or if you are consistently late in making the payments, you are not ready to buy a home. If you can handle the extra payments, then you’ve got the thumbs-up to start looking for a home to buy.

Generally speaking, once you’ve saved 20% for a down payment and you can afford monthly mortgage payments, you’re ready to start looking for a home. Yes, you can buy a home with a smaller down payment — I bought my first place with a 2% down payment! — but it’ll cost you in the long run. You’ll need to carry private mortgage insurance (PMI), you’ll pay more in interest, and you could put yourself in a position where you can’t afford to keep your home.

The Bottom Line

Homebuyers are often told to “buy as much house as you can afford”. But the problem with this advice is that it leaves you without a buffer. What if you lose your job? What if you’re forced to sell your home after housing prices have dropped?

Instead of buying as much house as you can afford, buy only as much house as you need. Think of conventional debt-to-income ratios as ceilings, not targets.

Give yourself margin for error. Instead of basing your home-buying budget on a 36% front-end DTI ratio, consider dropping that to 28%. Or, better yet, 25% (just like the olden days!).

If you have an average U.S. household income of around $75,000, a 36% DTI ratio would lead you to budget $2250 per month for housing (assuming you have no other debt). If you were to go with a more conservative 25% DTI ratio, that budget would be $1563 per month. That’s a savings of $687 per month — over $8000 per year! Just think: What could you do with a chunk of change like that?

Another way to create a buffer is to base your budget on your net (take-home) pay instead of your gross pay. Or, if you’re in a relationship where both partners work, run the numbers for only one of the two incomes.

No, you won’t be able to afford a big mortgage if you do what I’m recommending. But you know what? You won’t feel pinched by your mortgage payments. And you’ll be at much less risk the next time the housing market implodes. Best of all, you can plow all of the money you’ve saved on housing into a building a ginormous wealth snowball!

The post “How much house can I afford?” appeared first on Get Rich Slowly.

from Finance https://www.getrichslowly.org/how-much-house/

via http://www.rssmix.com/

0 notes

Text

"How much house can I afford?"

How much house can I afford? Answering this question correctly is one of the keys to building a happy, wealthy life. Unfortunately, theres a vast housing industry in the U.S. thats geared toward providing the wrong answer.

You see, housing is by far the largest expense in most peoples budgets. According to the U.S. governments 2016 Consumer Expenditure Survey, the average American family spends $1573.83 on housing and related expenses every month. Thats more than they spend on food, clothing, healthcare, and entertainment put together!

Too many folks struggling to make ends meet focus their attention on fine-tuning their budget. They try to save big bucks by clipping coupons, growing their own food, and/or making their own clothes. While theres nothing wrong with frugal habits I applaud everyday thriftiness! all of these actions combined wont (and cant) have the same impact on your budget as keeping your housing payments affordable.

Part of the problem is what I call the Real-Estate Industrial Complex, each piece of which has a vested interest in convincing consumers that bigger, more expensive homes are better. Real-estate agents, mortgage brokers, home-shopping shows, and glossy magazines all encourage folks to buy at the top end of their budget. But buying at the top end of your housing budget is dangerous.

Buying a home is a huge decision, financially and otherwise. If youre going to purchase a place, its important to know how much house you can truly afford.

Debt-to-Income Ratio

Economists have used decades of financial stats to create computer models to predict how much people can afford to spend on housing and debt. Banks use these models to figure out how much they think you can afford to spend on housing.

Traditionally, lenders use whats called a debt-to-income ratio (or DTI ratio) a measure of how much of your income goes toward debt every month to estimate how much you can afford to pay for a home without risk of defaulting. This might sound complicated, but its not.

To find this ratio, divide your monthly debt payments by your gross (pre-tax) income. So, for example, if you pay $400 toward debt every month and you have an income of $4000, then your DTI ratio is 10%. If you pay $800 toward debt on a $4000 income, your DTI ratio is 20%. The lower your debt-to-income ratio, the better.

Banks and mortgage brokers look at two numbers when deciding how much to loan:

The front-end DTI ratio (sometimes called the housing expense ratio), which includes only your housing expenses: mortgage principle, interest, taxes, and insurance.The back-end DTI ratio (also known as the total expense ratio), which include all of the above plus other debt payments like auto loans, student loans, and credit cards.

The key thing to understand about debt-to-income ratios is that theyre used to estimate the lenders risk, not yours. That is, your mortgage company uses them to check whether they think youll be able to make the payments not whether you can comfortably make the payments.

If you want room in your budget for fun, you should opt for a lower debt-to-income ratio than your real-estate agent and mortgage broker say you can use.

If youre a money nerd, you can read more about debt-to-income ratios at Fannie Maes website.

How Much House Can You Afford?

During the 1970s (before credit-card debt was common), DTI wasnt split between front-end and back-end. There was only one ratio, and it was 25%. If your mortgage, taxes, and insurance costs were less than 25% of your income, people assumed you could make the payment.

This is still an excellent rule of thumb: Spend no more than 25% of your budget on housing. (In fact, this is the number that money guru Dave Ramsey advocates.)

That said, debt-to-income guidelines have relaxed over the years.

When my ex-wife and I bought our first home in 1993, our mortgage broker told us that our front-end DTI ratio had to be 28% or lower, meaning we couldnt pay any more than 28% of our gross income toward housing. The back-end DTI ratio was capped at 36%, which meant that our housing expenses and other debt payments combined couldnt be more than 36% of our income.When my ex-wife and I bought a new home in 2004, the accepted DTI ratios had grown by 5%. That 28% figure is outdated, we were told. Most people can go as high as 33%. The back-end ratio had been raised to 38%.According to the Fannie Mae website, in 2018 maximum back-end DTI ratios are up to 45% (and sometimes even 50%). These numbers are insane. Nobody should be spending half of their gross income on debt not even mortgage debt! Thats a recipe for financial disaster.

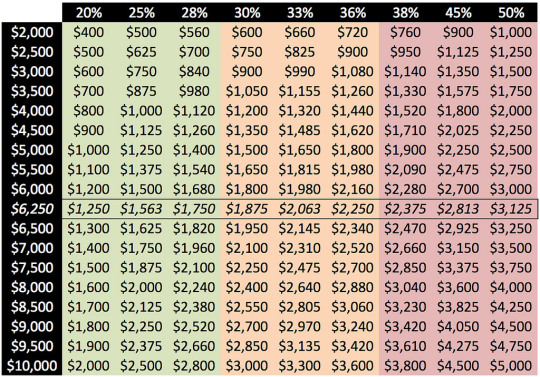

Heres a little table I whipped up to show what sort of housing payment youd be looking at based on your pre-tax income (the left-hand column) and various debt-to-income ratios (the header row):

A 5% increase in your debt-to-income ratio might not seem like a big deal. But when youre talking about a house payment, its huge.

In 2016, the average American household earned $74,664 before taxes. Using this, a 5% change would be $3733.20 per year or $311.10 per month. Many folks lost their homes during the housing crisis because they took on mortgage payments that were just $300 more than they could afford each month.

Real-Life Examples

When my ex-wife and I moved in 2004, our housing payments went from around $1200 per month to roughly $1600 per month. This $400 per month difference was enough to make me panicked about money.

Similarly, my youngest brother made the mistake of believing the banks when they told him he could afford a big housing payment. He could at first. But when the financial crisis hit in 2008 and 2009, he was screwed. Because hed bought at the top end of his budget, when his income faltered, so did his ability to pay his mortgage. He lost his home to foreclosure.

For the most part, banks are happy to lend you as much money as you want. (Within reason, of course, and if your credit is good.) Theyre not going to stop you from taking on more debt if their computer models say you can afford it. Its up to you to exercise caution.

In The Automatic Millionaire Homeowner, David Bach writes [emphasis is mine]:

You should generally assume that the amount the bank or mortgage company will loan you is more than you should borrowDont fool around with this. Do the math. Be realistic about your situation. Dont pretend youre in better shape than you are.

Remember: Nobody cares more about your money than you do. Your real-estate agent, mortgage broker, and bank all have a vested interest in encouraging you to buy as much house as possible their incomes depend on it. Listen to what they have to say, but make your decision based on whats best for you.

Playing House

If you think youre ready to buy a house, take a few months to do a trial run. In The Money Book for the Young, Fabulous, and Broke, Suze Orman says that you should play house before you buy a house. I like this idea. Heres how it works:

Figure out how much you think you can afford to pay for a home every month, including mortgage and maintenance. Lets use $1750 as an example.Subtract the amount youre currently paying for housing. If your rent (or current mortgage) is $1000 per month, youd subtract this from our hypothetical $1750 to get $750 per month.Open a new, separate savings account. On the first day of each of the next six months, stick $750 into this account.

This exercise lets you experience what its like to make a higher housing payment. If you cant make these numbers work, Orman says you need to wait:

If you miss one payment, or if you are consistently late in making the payments, you are not ready to buy a home. If you can handle the extra payments, then youve got the thumbs-up to start looking for a home to buy.

Generally speaking, once youve saved 20% for a down payment and you can afford monthly mortgage payments, youre ready to start looking for a home. Yes, you can buy a home with a smaller down payment I bought my first place with a 2% down payment! but itll cost you in the long run. Youll need to carry private mortgage insurance (PMI), youll pay more in interest, and you could put yourself in a position where you cant afford to keep your home.

The Bottom Line

Homebuyers are often told to buy as much house as you can afford. But the problem with this advice is that it leaves you without a buffer. What if you lose your job? What if youre forced to sell your home after housing prices have dropped?

Instead of buying as much house as you can afford, buy only as much house as you need. Think of conventional debt-to-income ratios as ceilings, not targets.

Give yourself margin for error. Instead of basing your home-buying budget on a 36% front-end DTI ratio, consider dropping that to 28%. Or, better yet, 25% (just like the olden days!).

If you have an average U.S. household income of around $75,000, a 36% DTI ratio would lead you to budget $2250 per month for housing (assuming you have no other debt). If you were to go with a more conservative 25% DTI ratio, that budget would be $1563 per month. Thats a savings of $687 per month over $8000 per year! Just think: What could you do with a chunk of change like that?

Another way to create a buffer is to base your budget on your net (take-home) pay instead of your gross pay. Or, if youre in a relationship where both partners work, run the numbers for only one of the two incomes.

No, you wont be able to afford a big mortgage if you do what Im recommending. But you know what? You wont feel pinched by your mortgage payments. And youll be at much less risk the next time the housing market implodes. Best of all, you can plow all of the money youve saved on housing into a building a ginormous wealth snowball!

https://www.getrichslowly.org/how-much-house/

0 notes

Last Seen Blogs

rokn5gar

İsimsiz

lazyotakuchan

𝒜𝓉𝒽𝒶𝓁𝒽𝒶𝒾𝒹

sonye4-ka

It's a me,Sonya !

story20883

Untitled

pengold

Pengold