#but yeah if I ever read it I will not be financially supporting mr card

Note

heartily unrecommend ender's game. the author is like smeyer but ten times worse.

funny you should mention that because I happen to know from my podcast research that smeyer loves ender's game. which, like, her book taste ranges all over the place, from "this book fucks" to "this book is fine" to "this is the worst drivel imaginable" so that doesn't actually tell us much but quelle coincidence you should bring her up in the same breath

unrecommend me books

#I've actually heard ender's game is really great#but yeah if I ever read it I will not be financially supporting mr card#asks#anonymous#unrecommend me books asks

3 notes

·

View notes

Video

youtube

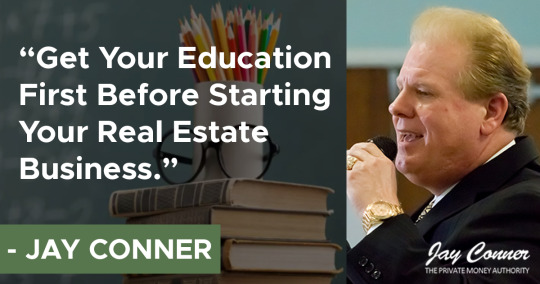

The Reality of Real Estate Investing with Dave Seymour & Jay Conner, The Private Money Authority

https://www.jayconner.com/the-reality-of-real-estate-investing-with-dave-seymour-jay-conner-the-private-money-authority/

Jay Conner, The Private Money Authority has a very special guest, Dave Seymour.

They discuss the reality of real estate investing. The nit and grit of the business. The struggles and lessons that need to be learned in order to achieve success in the real estate business.

Plus, Jay and Dave also talk about the best way how to grow capital!

All these and more in Real Estate Investing with Jay Conner.

After 16 years as a firefighter and paramedic, Dave Seymour launched his career, rapidly becoming one of the Nation’s top real estate investors. Within his first few years, Dave had transacted millions of dollars of real estate and had become one of the Nation’s leading experts in both residential and commercial transactions.

His unabridged passion for business and real estate put him on the radar of the A&E Television network as well as multiple television organizations like CBS, ABC, CNBC, Fox News, and CNN. New York Times reported that Dave Seymour’s series “Flipping Boston” posted the highest ratings ever for the A &E Network at the time of airing.

Dave has been sought after as a “tell like it is” mentor and motivator in the real estate world with a track record of unmatched success everywhere he reaches. Dave is well-known for doing business alongside investors on their very first real estate deal as well as guided some of the largest investment firms in the nation through complex transactions.

Timestamps:

0:01 – Get Ready To Be Plugged Into The Money

1:06 – Jay’s New Book: “Where To Get The Money Now” –https://www.JayConner.com/Book

2:16 – Today’s guest: Dave Seymour

4:27 – The Secret Origin of Dave Seymour

8:10 – Dave talks about when he started his real estate business.

10:10 – Early struggles and best lesson learned by Dave Seymour.

14:18 – What niche in the real estate business that you focused on?

16:49 – The best way to grow capital.

21:07 – Dave talks about his reality tv show “Flipping Boston”

24:06 – What does the law of reciprocity means to Dave Seymour?

26:54 – How does the law of reciprocity apply in real estate investing?

28:22 – Books recommended by Dave

29:04 – Dave’s parting comments: “ You don’t have to know everything. Educate don’t speculate”

30:39 – Connect with Dave Seymour – https://www.FreedomVenture.com

Private Money Academy Conference:

https://jaysliveevent.com/live/?oprid=&ref=42135

Have you read Jay’s new book: Where to Get The Money Now? It is available FREE (all you pay is the shipping and handling) at https://www.JayConner.com/Book

Free Webinar: http://bit.ly/jaymoneypodcast

Jay Conner is a proven real estate investment leader. Without using his own money or credit, Jay maximizes creative methods to buy and sell properties with profits averaging $64,000 per deal.

What is Real Estate Investing? Live Private Money Academy Conference

https://youtu.be/QyeBbDOF4wo

YouTube Channel

https://www.youtube.com/c/RealEstateInvestingWithJayConner

iTunes:

https://podcasts.apple.com/ca/podcast/private-money-academy-real-estate-investing-jay-conner/id1377723034

Listen to our Podcast:

https://realestateinvestingdeals.mypodcastworld.com/11213/the-reality-of-real-estate-investing-with-dave-seymour-jay-conner-the-private-money-authority

The Reality of Real Estate Investing with Dave Seymour & Jay Conner

Jay Conner (01:44):

After 16 years as a firefighter and a paramedic, my special guest launched his career, rapidly becoming one of the nation’s top real estate investors himself. So within his first few years as a real estate investor, he had transacted millions of dollars of real estate and had become one of the nation’s leading experts in both residential and commercial transactions.

Well, his unabridged passion for business and real estate put him on the radar very, very quickly in the A&E television network, and other multiple television stations and organizations like CBS, ABC, CNBC, Fox News, and CNN. Well, the New York Times reported that my guest’s series titled, “Flipping Boston,” posted the highest ratings ever for the A&E Network at the time of airing. Well, my guest has been sought after as the tell-it-like-it-is motivator. Well folks, my guest, friend, and fellow mastermind member is Mr. Dave Seymour. So welcome to the Private Money Academy Podcast, Dave!

Dave Seymour (03:39):

My Lord, I was looking around to find the guy that you were just describing.

And then I have one of those moments, “Oh, it’s me.” Yeah. I’ve kicked some butt and taken some names in my career. God bless you, man. It’s a pleasure to be with you, dude. It really is. Thanks for having me on.

Jay Conner (03:59):

Well, I’m excited to have you on Dave. I mean, you have got quite the story. I mean, there’s not many of us guys and gals out here that have had the trip and the journey that you had. So, yes, we want to hear all about “Flipping Boston” and being on the A&E Network. But before we get to that, you got your seatbelt on? You ready to go?

Dave Seymour (04:22):

I’m ready to rock and roll, brother. I’m ready. Let’s rock and roll. You got it.

Jay Conner (04:26):

Well, tell us, how did you get started in real estate?

Dave Seymour (04:29):

Yeah. Great question. It’s always a good opener. It’s like you said, I was a firefighter and a paramedic for many years. I’m actually an immigrant to the United States of America. Don’t tell anybody. It’s a secret. I came from London, England back in 1986. I became a naturalized citizen. Absolutely loved what I was doing, but the challenge was, I wasn’t very financially literate back then, Jay, and I suffered the consequences of financial illiteracy and I got hurt pretty badly during the crash of 2008-09. I was a firefighter paramedic. I was working construction. I was working retail security. I was working about 120 hours a week and I couldn’t make ends meet. And I very quickly realized that what I was doing wasn’t working. I was following the herd as I call it, 401-Ks, et cetera, et cetera. Debt was bad.

Saved money. I mean, all of the misnomers that I was given from years of education. But anyway, I found myself in 2008 losing my primary residence, a pre-foreclosure scenario cost me a marriage, Jay, and it was a serious side to all of this stuff, relationship-wise. It wasn’t easy to be a father to my son or a husband to my wife when I was working that many hours, I was out of the house. And it’s funny, man. I look back at it today and I have a bright smile. At my lowest, lowest point, I always kind of looked north for some help and guidance and I’m screaming and shouting at my God. And I’m like, “What did I do wrong?!” I didn’t lie. I didn’t cheat. Didn’t steal.

I worked hard. I was a man among men. Worker among workers, and yet everything had turned to crap. And I’m shouting at my God and I’m like, “Help, help!” Those that seek shall find, right? And in that moment of clarity or insanity, depending on how you want to look at it, a commercial came on the radio and it was, “Teach me foreclosure.” I was in my pickup truck. “Teach me foreclosure. Free one and a half hour seminar coming to your neck of the woods. Do you want to be a real estate investor? Do you want to learn how to do transactional deals with no money down, no credit?” And I’m like, well, I got no credit. My credit score is like 2. I’ve got no money. I’m losing my house. But I believe that it worked, Jay.

That was what was important. Like I had faith that real estate was a vehicle to wealth because I’d seen it, working on the construction sites, the investors showed up. They didn’t have any dirt on their boots. They were driving nicer cars. They got shiny white teeth. They were smiling. I wasn’t. So that was how it started, man. I went to a seminar. I’m a product of real estate education and training. And I took to it like a duck to water. I had no way to go but up really, was the answer to it. And I put one foot in front of the other. Worked with my now-wife, Mary Beth, for the 3-day class, and invested $27,000 on her credit cards. She was my first private lender, go figure, right? My wife. It’s the truth. I looked at her and I said, “What do you think?” It was $27,000 for like 5 classes.

I said, “What do you think, baby?” Then she goes, “I don’t know, what do you think?” I said, “I can’t keep doing what I’ve been doing. You know, the cost just keeps going up. The emotional costs, the physical costs.” She said, “Go get ’em!” She said, “I’m proud of you. I love you. I support you in anything you want to do.” And I looked at her, I said, “I’m so glad you said that. We’ve got to use your credit cards, mine are maxed out.” That was the truth and that’s how it all began. So yeah, kind of a long story, short, short story long, however you want to put it, but that was it.

Jay Conner (08:09):

So what year did you start your education and when did you go full-time real estate investing?

Dave Seymour (08:19):

Yeah, I started my first classes in late 2007 and 2008. Like the foreclosure crisis was just beginning to ramp up. And I started learning how to do short sales and distressed assets. And 18 months later, I quit the fire department and I say, “I quit.” I didn’t really quit. I retired. And the reason I retired was it got to a point where it cost me way too much money to go to work. It is as simple as that. I had made enough noise and grabbed enough attention in those 18 months that I was in the process of doing the TV show, “Flipping Boston.” I had surrounded myself with different people. I learned about internet marketers and the different ways of lead generation and attraction and execution and contracts and money. And I was like, all in man. I was like, where am I? Where has this been my whole life? You know, I’m like, I’m alive!

And that was it. That was how it started.

Jay Conner (09:22):

I experienced the same exact thing when I got into real estate investing. It was like, “My lands, where has this been all my life?” And my very first real estate investing seminar that I went to, I had already been doing this business for 6 years. My lands, don’t start out that way, get your education first. But I was cut off and lost my lines of credit in January of 2009. And that’s what triggered me to go to my first educational seminar to learn about private money. And that’s what got me going, this world of private money. So you got in there 18 months after getting your education. You retired from the firefighting and paramedic world. What were some of your early struggles when you started out and what are the lessons you learned from them?

Dave Seymour (10:18):

Yeah, that’s a great question. The biggest struggle I ever had was with my own head. Growing up a blue-collar guy now moving into a white-collar world. It was very hard for me to believe early in my career that people would sell assets to me for a discount. It was about self-worth, like I did a ton of personal development as part of my business development. Believing that I was worthy, believing that I had something of value, which was my education, which was the way that I looked at a real estate transaction. And as you do it, here’s the key. I think Jay, and I don’t know if you agree with this, I anticipate that you do, but as long as I was always in motion, in forward motion, as long as I was putting, honestly, my very best effort with one foot in front of the other.

If I was removing the negativity around me, the people who said, “You can’t.” I loved it when somebody said I can’t because I’d immediately turn it to, “I can.” And I just execute. And I just somehow succeeded. So it was about working on my mind first. A guy said to me, “Dave, there’s 6 inches of detrimental thinking that lives between your ears.” He said, “Only you can control that. Only you can. Are you wealth? Are you confidence? Are you joy? Are you value?” He said, “Because if you believe you are, then that will resonate to the people around you.” And I started looking at opportunities where I could bring massive value. And it wasn’t money-driven, Jay. It wasn’t money. Money was the by-product of service first. Helping a distressed homeowner. Looking after your contractors and treating them like equals, not like they were lesser citizens or whatever. Leaving my pride and my ego and pocket it to one side. Stepping into every relationship with everybody being at a hundred. And losing points rather be at zero.

I’d always have to gain points. You know what I mean? I bought an attitude of gratitude to everything that I did. And I just kept going, man. There’s a book out there. It says, “Six inches short of gold, or six feet short of gold.” And the idea is, is it just that one more phone call? Is it just that one more author? Is it just that one more relationship? Are you gonna quit before it’s time to succeed? And what happens is, 90% of our competition, if not higher, quit. And that’s why guys like us succeed because we stay the course. We have the tenacity, we have the drive, we have the faith, the belief. And again, surrounding myself with like-minded people who wanted to do what I was doing and that overcame any hurdle. There aren’t any hurdles. They’re just little blips along the radar. It’s as simple as that.

Jay Conner (13:13):

Well, what you just said, Dave, is one of the reasons that you and I resonate so well with each other and that is, it’s never about the money for the long-term. Making a lot of money can be a motivation for somebody in their short term. But you know, it’s been my experience over all the years of being in business. Whenever I got involved in an activity or an opportunity, and the only interest that I had in that opportunity was to make money, I never succeeded. I never succeeded. And it all comes down to what you just said, having a servant’s heart. I know you gotta love Zig Ziglar like I love Zig Ziglar, right?

Dave Seymour (13:54):

Right on my wall, right there. “You can have everything in life you want, if you will just help enough other people get what they want.” Zig Ziglar, it’s right there on my wall, brother.

Jay Conner (14:07):

That’s it, that’s it.

Dave Seymour (14:13):

Look at that, I’m getting goosebumps on my arms.

Jay Conner (14:13):

Mine are standing up on my neck. So, as far as your real estate investing journey, what have you focused on? Fix and flips? Wholesaling? What niches of real estate have you really been involved in and like, just knocked it out of the park?

Dave Seymour (14:34):

“Yes” is the answer to all of them. Yeah. Look, here’s the thing. As you become more intelligent in your industry, you see more opportunities. So, the TV show, “Flipping Boston,” pigeon-holed me as the grumpy construction guy who just got it done, which is all BS, it’s reality TV, right? But the reality of it was, I really did buy houses with my partner, we really did renovate them, fix them, sell them, and make a profit. Wholesaling is easier money. It’s just great negotiation skills, understanding the mechanics. I think the biggest disservice in the education space is that people say, if you just learn how to be a wholesaler, then you’ll make quick money. Well, that’s garbage. You gotta know how to be a rehabber so that you can be a great wholesaler, right?

If you don’t understand the mechanics, the numbers, the time, the ARVs, et cetera, et cetera. So I’ve always been in that field. Always, always will be in that field. Although it’s not my focus so much today. Along the way, buy and hold, get some cash flow coming in, get some appreciation, let the tenant go to work and pay down your debt service for you, thank you very much. Treat them like the gold that they are. Don’t be a slum landlord, give them clean, decent, affordable housing, give them a response immediately when they need you, if you can, to make sure that you build that relationship with them. They’re the most valuable asset that you have as a real estate investor, is your tenant base. And then today, we level up. It’s always a case of levelling up. I can’t sit still. It’s my A.D.D. DNA. And today we’re in the commercial real estate space. I run a $100 million private equity fund that invests in multi-family assets in the Sunbelt. And we just started our build-for-rent strategies where we’ve got 6-acreage plots in Florida, another 8-acreage plots in South Carolina and Atlanta. And now we’re going to be building houses for the folks who want to rent and not own. So there’s a trajectory, Jay, which part of that do you want to address for us?

Jay Conner (16:44):

Well, you’ve done it all and it’s just part of ascending up the ladder. Now you just mentioned that you’ve got a pretty large fund for the commercial projects. So like myself, you know a whole lot about growing capital, attracting capital. I mean, both you and I could talk a long time about that, but let’s just stop here for a moment. Tell us from your experience, what’s the best way to grow capital?

Dave Seymour (17:14):

So look, there is an absolute learning curve, right? So when I was doing single-family buy fix and flip, attracting an investor, first of all, who understood the business, was critically important. So you could do that through show and tell. This is what we paid for it. This is what we did to it. This is how much we made. And this is what our private lender made on it. Protected, secured, and insured. 8% interest. Interest only, blah, blah, blah. You know the pitch, right? And that becomes word of mouth. So, my portfolio attracted that retail investor. I’m not going to lie, Jay. I’m going to be truly transparent. It can be hard work. It could be heavy lifting sometimes with the retail investor. We use the term, “If it feels like I’m pushing a donkey up a hill, then I got to stop doing it.”

Right? So how do I get attraction? How do I get motion? Repetitive actions? It’s by being successful. The very first private loan I took was $35,000 from a lieutenant at the fire department. And I said, “So, Mike, could you give me $35,000? I’m going to put you in a third lien position on this property. But I’m going to give you your $35,000 back in 3 weeks plus an additional $5,000.” I knew I could do it because the property was on the contract. We just needed this money to squeeze roots at the finish line. So I give him his money back in 2 weeks and he’s ecstatic. And he said to me that day, “Dude, that was a great deal!” I said, “Thanks, Lt. I appreciate it.” He said, “If you ever,” magic words, “if you ever need money again, you come to me first.”

“And if I don’t have it, I know somebody who does.” And what he was referring to was his father because his father was a retired chief. So, the first one is always the toughest one. But once you’ve got traction underneath that, it becomes a system. It becomes repetitive and it creates its own motion. Today, I’m in a different sandbox altogether. Today, I attract capital through the portfolio. I attract capital through family offices, institutional capital. How would you like this for a problem, Jay? You ready? I have 18 months to put together a half a billion dollar portfolio because I’ve got an arbitrage trust company that’s ready to take it out at a full cap on the buy-side and an 8.5, 9% cash on cash return. So, there’s a guy waving a half a billion dollar check in my face and he’s like, “Go find me the real estate. Let’s go!” So, it’s interesting because the first guy that I learned commercial from was a very, very cool gentleman. His name’s Dave Lindahl. He’s in Massachusetts.

Jay Conner (20:12):

Yeah, Dave’s a good friend of mine.

Dave Seymour (20:14):

Okay. So DL said to me, “Dave, it’s just zeroes. More zeroes on the way in, more zeros on the way out. Just run the deal the same way.” And I never forgot that. So yeah, that’s how we raise money today, man.

Jay Conner (20:30):

That’s awesome. Before I get to my next question, let me ask you this first. So everybody’s dying to hear the short story summary of your television stardom of the A&E show “Flipping Boston.” So take a moment and tell us about that. Well, before you tell us about reality TV, I tell people whenever the ask me, “Jay, tell me about all these flipping shows.” And I’ll say, “The only thing real about reality TV is none of it’s real, except Dave Seymour’s Flipping Boston because he actually did have to do all that.” But anyway, take a moment and tell me and the audience about that reality TV experience.

Dave Seymour (21:12):

Look, it’s a blessing and a curse, depending on how you want to look at it. The blessing was the national exposure. I don’t know about anybody else. I didn’t get rich off of a TV show. I think it was $15,000 an episode at the end of our career there. Here’s what the benefits are. The exposure. It put me on the Today Show multiple times. It put me on the Rachel Ray show multiple times. It allowed me to be recognized as a national expert and a pundit on CNBC and CBS and other networks. So that was the caveat to it. The nitty gritty of a real estate transaction being filmed for a TV show. If it’s a half an hour TV show like these fix and flippers, these shows on HGTV, you know what I mean?

If it’s a half hour show, look, man. Paint and carpet, paint and carpet. You’re not making 40, 50, 60, 70, 80, 90, a hundred thousand dollars on paint and carpet, okay? So stop it. Be serious. They’re creating a TV show. You know, with us up here in New England, my inventory’s some old, old ladies, man. I mean, 1890, you know, 1880. The oldest lady I ever loved was 1892, I think she was born. And she was an old school in Newburyport that we turned into a couple of high-end condominiums. But we really did rip the houses apart and put them back together again. And the thing is, I will always give kudos to my ex-partner, Pete, on this, was he ran the numbers as if there was nothing special about the exposure or anything else. Like the numbers were real. The real numbers in, the real numbers out. The profit, whether it was a skinny margin or a better margin, he stayed true to the numbers.

Look, can you flip a house in 3 weeks and make 40, 50 grand? Maybe. You can flip a contract and make 40 grand. And you can do that in 24 hours if you know what I know, right? So, reality TV had to create a story, had to create a show. And I allowed a goofball like me to have some fun. I’d break the fourth wall all the time. The fourth wall is the camera. I got to break it all the time, just not talking to the camera. You know what I mean? They’re like, “You can’t do that.” And I’d say, “Keep it in there. It’s good.” So yeah, if you’re watching those shows, watch them for the show value, do not watch them for educational value because if you’re watching for educational value, you’re going to get your butt handed to you. We’ll watch them for show value and I’ll enjoy the pretty ladies. Enjoy the drama. Oh my God, the pipes burst! Let’s go to commercials. Right? You can play all of that as silly games if you’re hunting. It’s a show, come on now.

Jay Conner (23:58):

I love it. Thanks for telling it like it is, Dave. After all, you are known as the “tell it like it is guy.” So both you and I, Dave, are big believers in the law of reciprocity. So 2 questions. Tell everybody, what’s your definition of the law of reciprocity? And how does it apply to real estate investing?

Dave Seymour (24:20):

Yeah, that’s such a good question. Look, man reciprocity, they actually did, like the intelligence psychoanalyst kind of guys and girls looked at reciprocity, and it’s part of our DNA. And our DNA says as homo sapiens, that if I do something for you that is perceived to be valuable, you in return will do something back for me. But don’t bring value to someone with an expectation of value. Just give because giving is good, right? Start there. Our rewards are coming from high up above. They’re not always coming in the paycheck. You know what I mean? So reciprocity is just going out and being of service, I believe. I know a guy, who I see as the ultimate in reciprocity. I know a guy who’s financially stable. This guy has a couple of boys. They’re now 11 and 9 years old.

And what this man does is he takes his children to Walmart the last 2 weeks before Christmas every year. And he will put down $5,000 at the layaway counter and tell the lady behind the counter, “Pay down $5,000 worth of layaways, whatever comes up on your screen until those layaways are all paid off.” And he just shows his sons that. That’s reciprocity, this man. And I’ve had many, many, many conversations with him. And he says, “Reciprocity has put me in a position to be financially free.” And the Law of Reciprocity says if I want to keep something, I have to give it away. Say that again. If you have something of value, if you’re going to keep it, then you have to give it away. Pass it on, is what we use for terminology. So that’s my definition of reciprocity. And here’s the other thing, man, when it comes to charity and giving them philanthropy, don’t do it to get recognized, do something good for somebody else and then keep your mouth shut. Because that I believe is the definition of humility, which works side by side with reciprocity. So that’s just my own philosophy on it. And it’s served me pretty well.

Jay Conner (26:37):

It reminds me of what Jesus told the Pharisees when they’re out there praying in the public square, their arms lifted up and leg Jesus said, “Go pray in your closet and shut the door,” right? I love it. How does the law of reciprocity apply in real estate investing?

Dave Seymour (27:00):

Look, through coaching. Through passing it on. Through being humble. Okay? There’s a lot of ego in our industry, Jay. Let’s just be honest about it, right? “Look at me, I’m the best. I’ve got a private jet. I’ve got a big house,” you know, all of that stuff. I don’t believe that encompasses reciprocity. Reciprocity is an opportunity to give somebody a hand up, not give somebody a handout, right? When you’re in a position to share knowledge, knowledge is only powerful if implemented, right? So that’s what I like about real estate reciprocity. And then we get to pass that along to our clients. To a homeowner in distress with whatever that situation is and the reciprocity in there works along the way of, “You know what, that person knows somebody else.” And my reputation will always walk before me. Unfortunately, bad news travels faster than good news. We all know that. And if you make loud, good news with clients and let them speak your words afterwards, then reciprocity and momentum follows afterwards. So that’s how I look at it, brother, right or wrong. It’s certainly good.

Jay Conner (28:21):

I love it. Dave, what book have you gifted to other people more than any other book?

Dave Seymour (28:28):

It’s “The Secret” by Rhonda Byrne. Law of attraction. And then my good friend, Jack Canfield’s “Secrets of Success.”

Jay Conner (28:38):

Oh yes. My wife, Carol Joy, and I went to see him. I’m looking at the certificate up here. We went to Jack Canfield’s first event of his, that was The Breakthrough to Success. And I got so excited. I went back and paid the big bucks and got certified to teach Jack Canfield stuff because I just love it. Dave, I have just loved having you here on the podcast as we wind down. Do you have any parting comments or final advice that you would like to share with the audience and then be sure to tell the folks how they can get hold of you.

Dave Seymour (29:13):

Yeah, for sure. It’s always interesting how you wrap up a conversation. For me, I think about the people who listened to us, Jay. What do they want? What are their needs? How can we serve them best? And I know it sounds kind of kitschy, but I always say, “To thine own self, be true.” Is what you’ve been doing working? Be honest with yourself. And if it hasn’t, it’s okay to do something different. You don’t have to know everything before you do anything. Take the first step. Educate, don’t speculate. And find the people that are doing what you want to do at the highest level possible. Do your due diligence and then step into action. A lot of fantastic people sitting on couches, wishing and wanting and dreaming. But then there’s a smaller population of guys like us who are out there actually doing it, right?

Not just teaching it, but we’re actually out there doing it as well. So step into your own greatness. And if you want to connect with us, if you want to learn anything about what we do at Freedom Venture Investments, I know Jay’s got a website that he can send you to there. I’m old school, brother. You could pick up the phone and call us at (781) 922-4418. One of my team members will pick up the phone and connect to me if that’s possible. I try to be as available as I can. So I just want to keep it moving forward, brother. I’m the opposite of stale.

#Jay Conner#Private Money Lender#Real Estate Business#Real Estate#Real Estate Investing#Real Estate Investor#Real Estate Profit#The Private Money Authority#Flip Your House

18 notes

·

View notes

Text

Believe Me - Yolanda Hadid

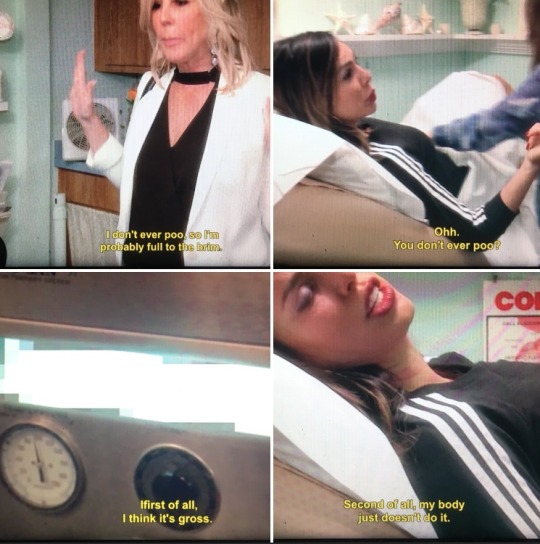

Have you ever wanted to see pictures of a housewife’s shits? I mean, not Vicki Gunvalson’s, of course, as she does not shit. As a side note, I don’t understand why this isn’t talked about more. It’s literally my favourite thing that has ever happened on any RH episode since the beginning of time. Vicki Gunvalson does not shit. First of all, she thinks it’s gross. Second of all, her body just doesn’t do it.

The fact that Vicki Gunvalson does not ever shit is the most incredible fact I have ever learned in my life, and honestly, I think about it like at least once a week. When Vicki Gunvalson dies, her body ought to be preserved, cross-sectioned, and displayed in science museums forever. The woman who just decided it was too messy to like, get rid of the calcifying waste inside her body???? Honestly, find me a better metaphor for how Vicki lives her life.

Aaaaaaaanyways. You know who does shit? Yolanda Hadid. I know this as a full-colour, high resolution fact because Yolanda Hadid felt the need to take photos of her deformed shits in order to prove to the world that she has Lyme.

This is what we have brought upon ourselves. Or, rather, this is the price we must all pay for the sheer blessing of Lisa Rinna’s existence. That bitch came in hot, found a first season storyline and fucking ran with it (which is why she’s still around and miss Eileen Davidson is not, thank you). Yes, in order to gain Mama Rinna, we had to all experience the Munchausen arc, and now we have to look at Yolanda Hadid’s shits.

Yet somehow, in a book filled with diarrhea and ass worms (worms that lived in Yolanda’s ass, of course), the biggest piece of shit around was David Foster.

Here is a (stool) sampling of Mr. Foster’s offences:

Required Yolanda, a beautiful nymph who made him dinner every day and packed curated outfits in labeled ziplocs for his every trip, to be financially independent throughout their marriage. Just trash. If I had a wife like Yolanda, bringing me goddamn picnic baskets of lunch at work, gifting me glossy books of her bangin’ nude bod, and making me fresh lemonade from her ORCHARD, I think I’d fucking share my excessive wealth with her. The list of garbage ass husbands who encourage their wives to do the show as an exit strategy is a guest list for the seventh circle of hell.

Refused to support Yolanda’s kids from her previous marriage (you may have heard of Gigi, Bella, and Anwar?). Such fucking barf. You have a $27m house and you’re gonna be such a scrooge that you can’t support your stepchildren??????? Absolute trash of the highest order.

Got his balls in a knot when Yolanda removed her implants because they were like, idk...LEAKING INTO HER CHEST CAVITY?????

Ended his marriage ON THE PHONE like the way you break up with your grade seven boyfriend when summer comes cause you wanna be a ho at summer camp

Told Yolanda her SICK CARD was up. Because as we all know, marriage consists of counting the other person’s hardships, and tapping out at the designated threshold.

Honestly, there are more, but I cannot talk about David Foster for another second, other than to say that as a citizen of British Columbia, I rebuke thee and hereby excommunicate your trash ass from our beautiful province you horrible shit monster.

K. That’s done. Let’s talk about the ass worms.

The whole crux of the book is that this poor woman felt compelled to prove to the world that she was sick. This is a legit problem. Women are so often misdiagnosed or placated when reporting pain and chronic symptoms to doctors. It’s a thing, and it’s awful. There are so many instances throughout this book where men tell Yolanda that she’s making herself sick by working too hard, or assume that Bella is lazy because chronic fatigue isn’t real. it’s garbage, and it sucks.

Now, I get that neurological Lyme is like, a controversial diagnosis and whatever. But you know what:

What I do know is that this woman shit out a series of long worms, ass worms, worms from her ass. And I know this because she took pictures of them. So, like, yeah, she’s sick. I don’t think you can give yourself ass worms by “working too hard for your little woman body”. So, I believe you, Yolanda.

THAT BEING SAID. These rich white women have GOT to stop promoting “alternative” treatments for serious illnesses. Rinna had a point in all the Munchausen mess, which was that Yolanda was trying every possible treatment under sun all at once. Overlapping antibiotic rounds with detox centres, sketch as hell blood oxidizing in questionable Mexican alleys. And like, whatever. If no one is taking you seriously, and all you can do is get colonics and stand in industrial freezers, then sure. What else have you got?

But you know what’s not cool? Referring everyone you fucking meet to the same Lyme doctor, who diagnoses literally every person alive with Lyme, and then sends them through a suite of expensive alternative treatments by the same doctors. This is a goddamn racket, and these doctors are making a killing off all these gullible patients who think getting their dental fillings removed is gonna cure them. A lot of this gets uncomfortably close to Jenny McCarthy, anti-vax territory.

Please do not tell normal, middle class, suffering people that the answers lie in essential oils, illegal stem cell procedures, starving yourself with lemonade, and doing ayahuasca and mushrooms in Bali. This is bad advice.

Overall, this book was gross as hell and I did not enjoy reading it. It made me sad that women’s pain is so diminished that books like this exist. It made me mad that David Foster exists. It honestly made me not want to be a millionaire if it turns people into the kind of lunatics who bottle and preserve their own bodily disgustingments for research because when you’re rich, people tell you that’s acceptable behaviour. If a poor person did that, she’d be on several TLC shows and none of them good.

I truly hope that there is less diarrhea in the next book I read. Like, what an effort to get me to a point where looking at Simon Van Kempen in leather pants would be a reprieve.

Quick Stats:

Pages: 312

Did it need to be that many pages?: NOOOOOOOOO so much diarrhea.

Did it change my mind about the housewife?: Ugh. Like, not really? Who could ever dislike Yolanda?

Real-ass book rating: 📖📖/5 (It’s like, heartfelt and genuine, and kudos to Yolanda for writing through impaired brain functioning, and for being so candid, but it just kinda reads like a series of sad blog posts cobbled together with instagram screenshots.)

Junk food book rating: 💎💎/5 (like yeah, there’s some shade thrown at Kyle Richards, which I’m like, all about. But a good beach read has more shade than diarrhea.)

5 notes

·

View notes

Text

The Trapped Class, the Treadmill Class, and the Freedom Class

The way we think about economic class in America doesn’t make any sense.

In the past, there was the “poor,” the “middle class,” and the “rich.”

But there’s just one problem:

EVERYONE THINKS THEY’RE MIDDLE CLASS!

Look at this comment from an investment forum:

“We’re 62 and 59, Semi-Retired…at around $4.5M… (Note: We most definitely don’t consider ourselves wealthy, but just moderately affluent, and we still live the same as we did when we had $10K)…”

Allow me to translate: “We have 4.5 MILLION FUCKING DOLLARS but we ‘definitely’ don’t consider ourselves wealthy.”

I know, I know. “Ramit! That sounds like a lot of money…but when you live in San Francisco with 2 kids, and private scho—” Ugh, you already know the rest of this. I’m not even going to get into Mr. and Mrs. 4.5M Who Think They’re Middle Class.

Then you have the opposite side. My friend gave a eulogy for one of his relatives, who grew up poor (“I’m talking we-moved-13-times-as-kids poor”). Within hours, he was getting Facebook messages from his family, criticizing him for calling them poor. “We weren’t poor. Our neighbors — they were poor.”

Do you see how ridiculous this is? A multimillionaire couple refuses to believe they’re rich…and a family who had their electricity repeatedly shut off refuses to believe they’re poor.

IWT Philosophy on Economic Class

In America, the almighty dollar rules, but don’t you dare talk about class.

Buy a Tesla, walk around with your LV bag, renovate your kitchen, take lots of vacations…and post it on Instagram, please. But don’t ever say you’re rich. You’re just “moderately affluent.”

I see it myself. I get lots of people who teasingly ask me, “So are YOU rich?” Even though I’ve spent 15+ years talking about how money is just one part of a Rich Life, most people wink and nod and smile, like deep down they know I’m just playing a trick and they’re in on it.

“Yeah yeah, I know…life isn’t just about money. [Now that we got that out of the way…] So are you rich?”

Once, just to see what would happen, I replied, “Yes.” No caveats, no clarification, just yes.

Try to imagine the pin drop silence you’d hear in outer space. That was their response — an awkward, stunned silence. They were completely unsure how to respond. Would you? Have you ever heard someone openly acknowledge they were rich?

Not in this country. Because we worship the almighty dollar, but you can’t talk about it.

I now soften my answer to say, “Well, I was rich before I had money and I live a Rich Life now.”

A Rich Life is about more than money. Especially when everyone lies about it.

A Rich Life is about FREEDOM and FLEXIBILITY. You can be rich on $50K/year if you’ve created a life where you can do the things you love — whether it’s traveling, eating sushi every week, or teaching drawing. You can also live that Rich Life on $500,000 or $5 million. And of course, more money makes it easier.

You can also have a lot of money and be drowning. For example, over the weekend, I had coffee with a friend who used to work in investment banking. He and his coworkers would get together and compare notes about their boss, who’d randomly share tiny bits of his life. One person overheard him talking about his lake house. Another heard him say his 3 kids go to private school.

For a bunch of young bankers stuck at the office for 14+ hours/day, they built a model incorporating all the “clues” they heard from his expenses. At a certain point, they looked at each other and realized that this guy — who was making $2.5 million/year — might actually be LOSING money.

That’s why I think we need a new framework to use.

A new framework for class in America

The old framework — poor, middle class, and rich — is reductive. It’s incomplete.

How many of us know someone who’s technically rich…but when they factor in the costs of housing, student loan debt, day care, and basic expenses, they don’t “feel” rich? You can have someone making $500K who feels trapped (or our banker friend who obviously is living beyond his means)…but someone making $40K who feels free.

That’s why a new framework should focus less on net worth and more on lifestyle, which you can intentionally design for yourself.

(Note: These classes don’t justify massive inequality and systemic problems, which are genuine problems. They simply provide a “lens” through which to view your financial state.)

Read below and see if you can spot yourself.

1. The “Trapped” Class

In The Trapped Class, you’re stuck working paycheck to paycheck, one accident away from financial disaster. There is no “buffer,” no time to think ahead and plan for the long term.

Key phrases used by people in The Trapped Class:

“I’ll never be able to afford that”

“Once I do XYZ, I’ll be rich”

“I need money now so I can buy XYZ”

“I’ll be working for the rest of my life, so I might as well buy X”

“Don’t raise my taxes!!!”

“Things will never change”

“It just doesn’t matter what I do”

“That’s not for people like you and me”

“Money is the root of all evil”

Remember, you can be trapped at $30,000/year or $300,000/year depending on your lifestyle!

If you’re living in The Trapped Class, you have very few options and fewer resources or free time to improve your situation. This is a scary place to be and a very hard cycle to break out of.

2. The “Treadmill” Class

People on the treadmill have a decent job and a small bit of savings. If you live in America, the treadmill is a relatively good quality of life — The Treadmill Class has a roof, a car, internet, pizza delivery any time they want, and they can take a vacation once a year.

But they’re stuck — and getting off the treadmill is more of a dream, not a plan. They usually have some credit card debt. They aren’t saving enough for retirement. They’re likely to spend most of their lives working their job just to stay afloat.

Key phrases used by people in The Treadmill Class:

“If I just keep going, one day I’ll be able to do that…one day I’ll be able to afford that…one day I’ll be happy”

“I’ve got some $ saved but I’ll never be rich enough to actually quit my job to do what I want”

“That’s for rich people”

“I wish I could do X, but I need to keep saving money in case I lose my job”

“I really want X but I can’t afford it right now”

“Don’t raise my taxes!!”

“I feel stuck”

“Everyone thinks I should be happy making this much…but they don’t understand my expenses”

“My job pays the bills”

“I work hard. I deserve this”

I remember my first time in NYC as an adult, when I met a friend for lunch near Grand Central. I loved seeing all the people casually eating $30 salads in their beautiful suits — it was like I was sitting in a glamorous TV show. Only later did I understand that the fancy suit and salad belied the 2-hour commute, the multiple mortgages, the $50,000+/year private school tuition (per kid), and the thankless jobs with a capricious boss.

Day to day, the treadmill can be “fine,” even nice. But 30+ years of running will drain you.

3. The “Freedom” Class

These are the people who have the ability to do what they want, when they want. Money is no longer a major constraint in their lives. In fact, cost is rarely the first thing they consider. More often, it’s time, quality, experience, relationships, or simply “I want it.”

I’m not just talking about billionaires and trust fund babies, even though they get all the spotlight. There’s actually a growing wave of people who are living this life by building small, automated businesses that support their lives.

The key insight here: It’s not simply about how much money you have. It’s how much FLEXIBILITY and FREEDOM you have.

Key phrases used by people in The Freedom Class:

“My money works for me. I don’t work for it”

“So what if I pay a little more? It makes my life easier”

“I can afford to be generous”

“I can afford to make investments for the future”

“I want something created especially for me, not cookie-cutter for everyone else”

“I work hard and I want the best”

“Yes, I can do that”

“I trust the people around me”

“If I invest now, think how much I’ll gain later”

“My business operates without me day to day”

We almost always fixate on the money required to be in The Freedom Class. Sure, more money helps. But I recently spoke to a retired couple and asked them, “What would you tell yourselves back in your 20s?” They looked at each other and said, “Save more.” I pressed them: “Why? You’re retired and you have good money now. What would you have used the extra money for?”

They just stared at me. They had no answer. In America, we believe that “more” is the answer — but in reality, you can reach The Freedom Class by creating a life of flexibility and purpose.

* *

Which one of these classes do you fit into? What are your thoughts on my framework?

The Trapped Class, the Treadmill Class, and the Freedom Class is a post from: I Will Teach You To Be Rich.

The Trapped Class, the Treadmill Class, and the Freedom Class published first on https://justinbetreviews.tumblr.com/

0 notes

Text

The Trapped Class, the Treadmill Class, and the Freedom Class

The way we think about economic class in America doesn’t make any sense.

In the past, there was the “poor,” the “middle class,” and the “rich.”

But there’s just one problem:

EVERYONE THINKS THEY’RE MIDDLE CLASS!

Look at this comment from an investment forum:

“We’re 62 and 59, Semi-Retired…at around $4.5M… (Note: We most definitely don’t consider ourselves wealthy, but just moderately affluent, and we still live the same as we did when we had $10K)…”

Allow me to translate: “We have 4.5 MILLION FUCKING DOLLARS but we ‘definitely’ don’t consider ourselves wealthy.”

I know, I know. “Ramit! That sounds like a lot of money…but when you live in San Francisco with 2 kids, and private scho—” Ugh, you already know the rest of this. I’m not even going to get into Mr. and Mrs. 4.5M Who Think They’re Middle Class.

Then you have the opposite side. My friend gave a eulogy for one of his relatives, who grew up poor (“I’m talking we-moved-13-times-as-kids poor”). Within hours, he was getting Facebook messages from his family, criticizing him for calling them poor. “We weren’t poor. Our neighbors — they were poor.”

Do you see how ridiculous this is? A multimillionaire couple refuses to believe they’re rich…and a family who had their electricity repeatedly shut off refuses to believe they’re poor.

IWT Philosophy on Economic Class

In America, the almighty dollar rules, but don’t you dare talk about class.

Buy a Tesla, walk around with your LV bag, renovate your kitchen, take lots of vacations…and post it on Instagram, please. But don’t ever say you’re rich. You’re just “moderately affluent.”

I see it myself. I get lots of people who teasingly ask me, “So are YOU rich?” Even though I’ve spent 15+ years talking about how money is just one part of a Rich Life, most people wink and nod and smile, like deep down they know I’m just playing a trick and they’re in on it.

“Yeah yeah, I know…life isn’t just about money. [Now that we got that out of the way…] So are you rich?”

Once, just to see what would happen, I replied, “Yes.” No caveats, no clarification, just yes.

Try to imagine the pin drop silence you’d hear in outer space. That was their response — an awkward, stunned silence. They were completely unsure how to respond. Would you? Have you ever heard someone openly acknowledge they were rich?

Not in this country. Because we worship the almighty dollar, but you can’t talk about it.

I now soften my answer to say, “Well, I was rich before I had money and I live a Rich Life now.”

A Rich Life is about more than money. Especially when everyone lies about it.

A Rich Life is about FREEDOM and FLEXIBILITY. You can be rich on $50K/year if you’ve created a life where you can do the things you love — whether it’s traveling, eating sushi every week, or teaching drawing. You can also live that Rich Life on $500,000 or $5 million. And of course, more money makes it easier.

You can also have a lot of money and be drowning. For example, over the weekend, I had coffee with a friend who used to work in investment banking. He and his coworkers would get together and compare notes about their boss, who’d randomly share tiny bits of his life. One person overheard him talking about his lake house. Another heard him say his 3 kids go to private school.

For a bunch of young bankers stuck at the office for 14+ hours/day, they built a model incorporating all the “clues” they heard from his expenses. At a certain point, they looked at each other and realized that this guy — who was making $2.5 million/year — might actually be LOSING money.

That’s why I think we need a new framework to use.

A new framework for class in America

The old framework — poor, middle class, and rich — is reductive. It’s incomplete.

How many of us know someone who’s technically rich…but when they factor in the costs of housing, student loan debt, day care, and basic expenses, they don’t “feel” rich? You can have someone making $500K who feels trapped (or our banker friend who obviously is living beyond his means)…but someone making $40K who feels free.

That’s why a new framework should focus less on net worth and more on lifestyle, which you can intentionally design for yourself.

(Note: These classes don’t justify massive inequality and systemic problems, which are genuine problems. They simply provide a “lens” through which to view your financial state.)

Read below and see if you can spot yourself.

1. The “Trapped” Class

In The Trapped Class, you’re stuck working paycheck to paycheck, one accident away from financial disaster. There is no “buffer,” no time to think ahead and plan for the long term.

Key phrases used by people in The Trapped Class:

“I’ll never be able to afford that”

“Once I do XYZ, I’ll be rich”

“I need money now so I can buy XYZ”

“I’ll be working for the rest of my life, so I might as well buy X”

“Don’t raise my taxes!!!”

“Things will never change”

“It just doesn’t matter what I do”

“That’s not for people like you and me”

“Money is the root of all evil”

Remember, you can be trapped at $30,000/year or $300,000/year depending on your lifestyle!

If you’re living in The Trapped Class, you have very few options and fewer resources or free time to improve your situation. This is a scary place to be and a very hard cycle to break out of.

2. The “Treadmill” Class

People on the treadmill have a decent job and a small bit of savings. If you live in America, the treadmill is a relatively good quality of life — The Treadmill Class has a roof, a car, internet, pizza delivery any time they want, and they can take a vacation once a year.

But they’re stuck — and getting off the treadmill is more of a dream, not a plan. They usually have some credit card debt. They aren’t saving enough for retirement. They’re likely to spend most of their lives working their job just to stay afloat.

Key phrases used by people in The Treadmill Class:

“If I just keep going, one day I’ll be able to do that…one day I’ll be able to afford that…one day I’ll be happy”

“I’ve got some $ saved but I’ll never be rich enough to actually quit my job to do what I want”

“That’s for rich people”

“I wish I could do X, but I need to keep saving money in case I lose my job”

“I really want X but I can’t afford it right now”

“Don’t raise my taxes!!”

“I feel stuck”

“Everyone thinks I should be happy making this much…but they don’t understand my expenses”

“My job pays the bills”

“I work hard. I deserve this”

I remember my first time in NYC as an adult, when I met a friend for lunch near Grand Central. I loved seeing all the people casually eating $30 salads in their beautiful suits — it was like I was sitting in a glamorous TV show. Only later did I understand that the fancy suit and salad belied the 2-hour commute, the multiple mortgages, the $50,000+/year private school tuition (per kid), and the thankless jobs with a capricious boss.

Day to day, the treadmill can be “fine,” even nice. But 30+ years of running will drain you.

3. The “Freedom” Class

These are the people who have the ability to do what they want, when they want. Money is no longer a major constraint in their lives. In fact, cost is rarely the first thing they consider. More often, it’s time, quality, experience, relationships, or simply “I want it.”

I’m not just talking about billionaires and trust fund babies, even though they get all the spotlight. There’s actually a growing wave of people who are living this life by building small, automated businesses that support their lives.

The key insight here: It’s not simply about how much money you have. It’s how much FLEXIBILITY and FREEDOM you have.

Key phrases used by people in The Freedom Class:

“My money works for me. I don’t work for it”

“So what if I pay a little more? It makes my life easier”

“I can afford to be generous”

“I can afford to make investments for the future”

“I want something created especially for me, not cookie-cutter for everyone else”

“I work hard and I want the best”

“Yes, I can do that”

“I trust the people around me”

“If I invest now, think how much I’ll gain later”

“My business operates without me day to day”

We almost always fixate on the money required to be in The Freedom Class. Sure, more money helps. But I recently spoke to a retired couple and asked them, “What would you tell yourselves back in your 20s?” They looked at each other and said, “Save more.” I pressed them: “Why? You’re retired and you have good money now. What would you have used the extra money for?”

They just stared at me. They had no answer. In America, we believe that “more” is the answer — but in reality, you can reach The Freedom Class by creating a life of flexibility and purpose.

* *

Which one of these classes do you fit into? What are your thoughts on my framework?

The Trapped Class, the Treadmill Class, and the Freedom Class is a post from: I Will Teach You To Be Rich.

from Finance https://www.iwillteachyoutoberich.com/blog/class-in-america/

via http://www.rssmix.com/

0 notes

Text

The Trapped Class, the Treadmill Class, and the Freedom Class

The way we think about economic class in America doesn’t make any sense.

In the past, there was the “poor,” the “middle class,” and the “rich.”

But there’s just one problem:

EVERYONE THINKS THEY’RE MIDDLE CLASS!

Look at this comment from an investment forum:

“We’re 62 and 59, Semi-Retired…at around $4.5M… (Note: We most definitely don’t consider ourselves wealthy, but just moderately affluent, and we still live the same as we did when we had $10K)…”

Allow me to translate: “We have 4.5 MILLION FUCKING DOLLARS but we ‘definitely’ don’t consider ourselves wealthy.”

I know, I know. “Ramit! That sounds like a lot of money…but when you live in San Francisco with 2 kids, and private scho—” Ugh, you already know the rest of this. I’m not even going to get into Mr. and Mrs. 4.5M Who Think They’re Middle Class.

Then you have the opposite side. My friend gave a eulogy for one of his relatives, who grew up poor (“I’m talking we-moved-13-times-as-kids poor”). Within hours, he was getting Facebook messages from his family, criticizing him for calling them poor. “We weren’t poor. Our neighbors — they were poor.”

Do you see how ridiculous this is? A multimillionaire couple refuses to believe they’re rich…and a family who had their electricity repeatedly shut off refuses to believe they’re poor.

IWT Philosophy on Economic Class

In America, the almighty dollar rules, but don’t you dare talk about class.

Buy a Tesla, walk around with your LV bag, renovate your kitchen, take lots of vacations…and post it on Instagram, please. But don’t ever say you’re rich. You’re just “moderately affluent.”

I see it myself. I get lots of people who teasingly ask me, “So are YOU rich?” Even though I’ve spent 15+ years talking about how money is just one part of a Rich Life, most people wink and nod and smile, like deep down they know I’m just playing a trick and they’re in on it.

“Yeah yeah, I know…life isn’t just about money. [Now that we got that out of the way…] So are you rich?”

Once, just to see what would happen, I replied, “Yes.” No caveats, no clarification, just yes.

Try to imagine the pin drop silence you’d hear in outer space. That was their response — an awkward, stunned silence. They were completely unsure how to respond. Would you? Have you ever heard someone openly acknowledge they were rich?

Not in this country. Because we worship the almighty dollar, but you can’t talk about it.

I now soften my answer to say, “Well, I was rich before I had money and I live a Rich Life now.”

A Rich Life is about more than money. Especially when everyone lies about it.

A Rich Life is about FREEDOM and FLEXIBILITY. You can be rich on $50K/year if you’ve created a life where you can do the things you love — whether it’s traveling, eating sushi every week, or teaching drawing. You can also live that Rich Life on $500,000 or $5 million. And of course, more money makes it easier.

You can also have a lot of money and be drowning. For example, over the weekend, I had coffee with a friend who used to work in investment banking. He and his coworkers would get together and compare notes about their boss, who’d randomly share tiny bits of his life. One person overheard him talking about his lake house. Another heard him say his 3 kids go to private school.

For a bunch of young bankers stuck at the office for 14+ hours/day, they built a model incorporating all the “clues” they heard from his expenses. At a certain point, they looked at each other and realized that this guy — who was making $2.5 million/year — might actually be LOSING money.

That’s why I think we need a new framework to use.

A new framework for class in America

The old framework — poor, middle class, and rich — is reductive. It’s incomplete.

How many of us know someone who’s technically rich…but when they factor in the costs of housing, student loan debt, day care, and basic expenses, they don’t “feel” rich? You can have someone making $500K who feels trapped (or our banker friend who obviously is living beyond his means)…but someone making $40K who feels free.

That’s why a new framework should focus less on net worth and more on lifestyle, which you can intentionally design for yourself.

(Note: These classes don’t justify massive inequality and systemic problems, which are genuine problems. They simply provide a “lens” through which to view your financial state.)

Read below and see if you can spot yourself.

1. The “Trapped” Class

In The Trapped Class, you’re stuck working paycheck to paycheck, one accident away from financial disaster. There is no “buffer,” no time to think ahead and plan for the long term.

Key phrases used by people in The Trapped Class:

“I’ll never be able to afford that”

“Once I do XYZ, I’ll be rich”

“I need money now so I can buy XYZ”

“I’ll be working for the rest of my life, so I might as well buy X”

“Don’t raise my taxes!!!”

“Things will never change”

“It just doesn’t matter what I do”

“That’s not for people like you and me”

“Money is the root of all evil”

Remember, you can be trapped at $30,000/year or $300,000/year depending on your lifestyle!

If you’re living in The Trapped Class, you have very few options and fewer resources or free time to improve your situation. This is a scary place to be and a very hard cycle to break out of.

2. The “Treadmill” Class

People on the treadmill have a decent job and a small bit of savings. If you live in America, the treadmill is a relatively good quality of life — The Treadmill Class has a roof, a car, internet, pizza delivery any time they want, and they can take a vacation once a year.

But they’re stuck — and getting off the treadmill is more of a dream, not a plan. They usually have some credit card debt. They aren’t saving enough for retirement. They’re likely to spend most of their lives working their job just to stay afloat.

Key phrases used by people in The Treadmill Class:

“If I just keep going, one day I’ll be able to do that…one day I’ll be able to afford that…one day I’ll be happy”

“I’ve got some $ saved but I’ll never be rich enough to actually quit my job to do what I want”

“That’s for rich people”

“I wish I could do X, but I need to keep saving money in case I lose my job”

“I really want X but I can’t afford it right now”

“Don’t raise my taxes!!”

“I feel stuck”

“Everyone thinks I should be happy making this much…but they don’t understand my expenses”

“My job pays the bills”

“I work hard. I deserve this”

I remember my first time in NYC as an adult, when I met a friend for lunch near Grand Central. I loved seeing all the people casually eating $30 salads in their beautiful suits — it was like I was sitting in a glamorous TV show. Only later did I understand that the fancy suit and salad belied the 2-hour commute, the multiple mortgages, the $50,000+/year private school tuition (per kid), and the thankless jobs with a capricious boss.

Day to day, the treadmill can be “fine,” even nice. But 30+ years of running will drain you.

3. The “Freedom” Class

These are the people who have the ability to do what they want, when they want. Money is no longer a major constraint in their lives. In fact, cost is rarely the first thing they consider. More often, it’s time, quality, experience, relationships, or simply “I want it.”

I’m not just talking about billionaires and trust fund babies, even though they get all the spotlight. There’s actually a growing wave of people who are living this life by building small, automated businesses that support their lives.

The key insight here: It’s not simply about how much money you have. It’s how much FLEXIBILITY and FREEDOM you have.

Key phrases used by people in The Freedom Class:

“My money works for me. I don’t work for it”

“So what if I pay a little more? It makes my life easier”

“I can afford to be generous”

“I can afford to make investments for the future”

“I want something created especially for me, not cookie-cutter for everyone else”

“I work hard and I want the best”

“Yes, I can do that”

“I trust the people around me”

“If I invest now, think how much I’ll gain later”

“My business operates without me day to day”

We almost always fixate on the money required to be in The Freedom Class. Sure, more money helps. But I recently spoke to a retired couple and asked them, “What would you tell yourselves back in your 20s?” They looked at each other and said, “Save more.” I pressed them: “Why? You’re retired and you have good money now. What would you have used the extra money for?”

They just stared at me. They had no answer. In America, we believe that “more” is the answer — but in reality, you can reach The Freedom Class by creating a life of flexibility and purpose.

* *

Which one of these classes do you fit into? What are your thoughts on my framework?

The Trapped Class, the Treadmill Class, and the Freedom Class is a post from: I Will Teach You To Be Rich.

from Finance https://www.iwillteachyoutoberich.com/blog/class-in-america/

via http://www.rssmix.com/

0 notes

Text

The Trapped Class, the Treadmill Class, and the Freedom Class

The way we think about economic class in America doesn’t make any sense.

In the past, there was the “poor,” the “middle class,” and the “rich.”

But there’s just one problem:

EVERYONE THINKS THEY’RE MIDDLE CLASS!

Look at this comment from an investment forum:

“We’re 62 and 59, Semi-Retired…at around $4.5M… (Note: We most definitely don’t consider ourselves wealthy, but just moderately affluent, and we still live the same as we did when we had $10K)…”

Allow me to translate: “We have 4.5 MILLION FUCKING DOLLARS but we ‘definitely’ don’t consider ourselves wealthy.”

I know, I know. “Ramit! That sounds like a lot of money…but when you live in San Francisco with 2 kids, and private scho—” Ugh, you already know the rest of this. I’m not even going to get into Mr. and Mrs. 4.5M Who Think They’re Middle Class.

Then you have the opposite side. My friend gave a eulogy for one of his relatives, who grew up poor (“I’m talking we-moved-13-times-as-kids poor”). Within hours, he was getting Facebook messages from his family, criticizing him for calling them poor. “We weren’t poor. Our neighbors — they were poor.”

Do you see how ridiculous this is? A multimillionaire couple refuses to believe they’re rich…and a family who had their electricity repeatedly shut off refuses to believe they’re poor.

IWT Philosophy on Economic Class

In America, the almighty dollar rules, but don’t you dare talk about class.

Buy a Tesla, walk around with your LV bag, renovate your kitchen, take lots of vacations…and post it on Instagram, please. But don’t ever say you’re rich. You’re just “moderately affluent.”

I see it myself. I get lots of people who teasingly ask me, “So are YOU rich?” Even though I’ve spent 15+ years talking about how money is just one part of a Rich Life, most people wink and nod and smile, like deep down they know I’m just playing a trick and they’re in on it.

“Yeah yeah, I know…life isn’t just about money. [Now that we got that out of the way…] So are you rich?”

Once, just to see what would happen, I replied, “Yes.” No caveats, no clarification, just yes.

Try to imagine the pin drop silence you’d hear in outer space. That was their response — an awkward, stunned silence. They were completely unsure how to respond. Would you? Have you ever heard someone openly acknowledge they were rich?

Not in this country. Because we worship the almighty dollar, but you can’t talk about it.

I now soften my answer to say, “Well, I was rich before I had money and I live a Rich Life now.”

A Rich Life is about more than money. Especially when everyone lies about it.

A Rich Life is about FREEDOM and FLEXIBILITY. You can be rich on $50K/year if you’ve created a life where you can do the things you love — whether it’s traveling, eating sushi every week, or teaching drawing. You can also live that Rich Life on $500,000 or $5 million. And of course, more money makes it easier.

You can also have a lot of money and be drowning. For example, over the weekend, I had coffee with a friend who used to work in investment banking. He and his coworkers would get together and compare notes about their boss, who’d randomly share tiny bits of his life. One person overheard him talking about his lake house. Another heard him say his 3 kids go to private school.

For a bunch of young bankers stuck at the office for 14+ hours/day, they built a model incorporating all the “clues” they heard from his expenses. At a certain point, they looked at each other and realized that this guy — who was making $2.5 million/year — might actually be LOSING money.

That’s why I think we need a new framework to use.

A new framework for class in America

The old framework — poor, middle class, and rich — is reductive. It’s incomplete.

How many of us know someone who’s technically rich…but when they factor in the costs of housing, student loan debt, day care, and basic expenses, they don’t “feel” rich? You can have someone making $500K who feels trapped (or our banker friend who obviously is living beyond his means)…but someone making $40K who feels free.

That’s why a new framework should focus less on net worth and more on lifestyle, which you can intentionally design for yourself.

(Note: These classes don’t justify massive inequality and systemic problems, which are genuine problems. They simply provide a “lens” through which to view your financial state.)

Read below and see if you can spot yourself.

1. The “Trapped” Class

In The Trapped Class, you’re stuck working paycheck to paycheck, one accident away from financial disaster. There is no “buffer,” no time to think ahead and plan for the long term.

Key phrases used by people in The Trapped Class:

“I’ll never be able to afford that”

“Once I do XYZ, I’ll be rich”

“I need money now so I can buy XYZ”

“I’ll be working for the rest of my life, so I might as well buy X”

“Don’t raise my taxes!!!”

“Things will never change”

“It just doesn’t matter what I do”

“That’s not for people like you and me”

“Money is the root of all evil”

Remember, you can be trapped at $30,000/year or $300,000/year depending on your lifestyle!

If you’re living in The Trapped Class, you have very few options and fewer resources or free time to improve your situation. This is a scary place to be and a very hard cycle to break out of.

2. The “Treadmill” Class

People on the treadmill have a decent job and a small bit of savings. If you live in America, the treadmill is a relatively good quality of life — The Treadmill Class has a roof, a car, internet, pizza delivery any time they want, and they can take a vacation once a year.

But they’re stuck — and getting off the treadmill is more of a dream, not a plan. They usually have some credit card debt. They aren’t saving enough for retirement. They’re likely to spend most of their lives working their job just to stay afloat.

Key phrases used by people in The Treadmill Class:

“If I just keep going, one day I’ll be able to do that…one day I’ll be able to afford that…one day I’ll be happy”

“I’ve got some $ saved but I’ll never be rich enough to actually quit my job to do what I want”

“That’s for rich people”

“I wish I could do X, but I need to keep saving money in case I lose my job”

“I really want X but I can’t afford it right now”

“Don’t raise my taxes!!”

“I feel stuck”

“Everyone thinks I should be happy making this much…but they don’t understand my expenses”

“My job pays the bills”

“I work hard. I deserve this”

I remember my first time in NYC as an adult, when I met a friend for lunch near Grand Central. I loved seeing all the people casually eating $30 salads in their beautiful suits — it was like I was sitting in a glamorous TV show. Only later did I understand that the fancy suit and salad belied the 2-hour commute, the multiple mortgages, the $50,000+/year private school tuition (per kid), and the thankless jobs with a capricious boss.

Day to day, the treadmill can be “fine,” even nice. But 30+ years of running will drain you.

3. The “Freedom” Class

These are the people who have the ability to do what they want, when they want. Money is no longer a major constraint in their lives. In fact, cost is rarely the first thing they consider. More often, it’s time, quality, experience, relationships, or simply “I want it.”

I’m not just talking about billionaires and trust fund babies, even though they get all the spotlight. There’s actually a growing wave of people who are living this life by building small, automated businesses that support their lives.

The key insight here: It’s not simply about how much money you have. It’s how much FLEXIBILITY and FREEDOM you have.

Key phrases used by people in The Freedom Class:

“My money works for me. I don’t work for it”

“So what if I pay a little more? It makes my life easier”

“I can afford to be generous”

“I can afford to make investments for the future”

“I want something created especially for me, not cookie-cutter for everyone else”

“I work hard and I want the best”

“Yes, I can do that”

“I trust the people around me”

“If I invest now, think how much I’ll gain later”

“My business operates without me day to day”

We almost always fixate on the money required to be in The Freedom Class. Sure, more money helps. But I recently spoke to a retired couple and asked them, “What would you tell yourselves back in your 20s?” They looked at each other and said, “Save more.” I pressed them: “Why? You’re retired and you have good money now. What would you have used the extra money for?”

They just stared at me. They had no answer. In America, we believe that “more” is the answer — but in reality, you can reach The Freedom Class by creating a life of flexibility and purpose.

* *

Which one of these classes do you fit into? What are your thoughts on my framework?

The Trapped Class, the Treadmill Class, and the Freedom Class is a post from: I Will Teach You To Be Rich.

from Surety Bond Brokers? Business https://www.iwillteachyoutoberich.com/blog/class-in-america/

0 notes

Text

The Trapped Class, the Treadmill Class, and the Freedom Class

The way we think about economic class in America doesn’t make any sense.

In the past, there was the “poor,” the “middle class,” and the “rich.”

But there’s just one problem:

EVERYONE THINKS THEY’RE MIDDLE CLASS!

Look at this comment from an investment forum:

“We’re 62 and 59, Semi-Retired…at around $4.5M… (Note: We most definitely don’t consider ourselves wealthy, but just moderately affluent, and we still live the same as we did when we had $10K)…”

Allow me to translate: “We have 4.5 MILLION FUCKING DOLLARS but we ‘definitely’ don’t consider ourselves wealthy.”

I know, I know. “Ramit! That sounds like a lot of money…but when you live in San Francisco with 2 kids, and private scho—” Ugh, you already know the rest of this. I’m not even going to get into Mr. and Mrs. 4.5M Who Think They’re Middle Class.

Then you have the opposite side. My friend gave a eulogy for one of his relatives, who grew up poor (“I’m talking we-moved-13-times-as-kids poor”). Within hours, he was getting Facebook messages from his family, criticizing him for calling them poor. “We weren’t poor. Our neighbors — they were poor.”

Do you see how ridiculous this is? A multimillionaire couple refuses to believe they’re rich…and a family who had their electricity repeatedly shut off refuses to believe they’re poor.

IWT Philosophy on Economic Class

In America, the almighty dollar rules, but don’t you dare talk about class.

Buy a Tesla, walk around with your LV bag, renovate your kitchen, take lots of vacations…and post it on Instagram, please. But don’t ever say you’re rich. You’re just “moderately affluent.”

I see it myself. I get lots of people who teasingly ask me, “So are YOU rich?” Even though I’ve spent 15+ years talking about how money is just one part of a Rich Life, most people wink and nod and smile, like deep down they know I’m just playing a trick and they’re in on it.

“Yeah yeah, I know…life isn’t just about money. [Now that we got that out of the way…] So are you rich?”

Once, just to see what would happen, I replied, “Yes.” No caveats, no clarification, just yes.

Try to imagine the pin drop silence you’d hear in outer space. That was their response — an awkward, stunned silence. They were completely unsure how to respond. Would you? Have you ever heard someone openly acknowledge they were rich?

Not in this country. Because we worship the almighty dollar, but you can’t talk about it.

I now soften my answer to say, “Well, I was rich before I had money and I live a Rich Life now.”

A Rich Life is about more than money. Especially when everyone lies about it.

A Rich Life is about FREEDOM and FLEXIBILITY. You can be rich on $50K/year if you’ve created a life where you can do the things you love — whether it’s traveling, eating sushi every week, or teaching drawing. You can also live that Rich Life on $500,000 or $5 million. And of course, more money makes it easier.

You can also have a lot of money and be drowning. For example, over the weekend, I had coffee with a friend who used to work in investment banking. He and his coworkers would get together and compare notes about their boss, who’d randomly share tiny bits of his life. One person overheard him talking about his lake house. Another heard him say his 3 kids go to private school.

For a bunch of young bankers stuck at the office for 14+ hours/day, they built a model incorporating all the “clues” they heard from his expenses. At a certain point, they looked at each other and realized that this guy — who was making $2.5 million/year — might actually be LOSING money.

That’s why I think we need a new framework to use.

A new framework for class in America

The old framework — poor, middle class, and rich — is reductive. It’s incomplete.

How many of us know someone who’s technically rich…but when they factor in the costs of housing, student loan debt, day care, and basic expenses, they don’t “feel” rich? You can have someone making $500K who feels trapped (or our banker friend who obviously is living beyond his means)…but someone making $40K who feels free.