#federal debt

Text

Imagine you and your Republican coworkers went out to a restaurant for lunch, ordered from the menu (you had the soup dejour, they had the most expensive lobster on the menu), and ate your meals

When the check comes, Republicans say they refuse to pay (for the meals they’ve already eaten!), UNLESS everyone agrees to starve the homeless and rob the poor the next time you eat here

That’s what is happening

I know that the hypocrisy and the cruelty is the point with Republicans, but it needs to be noted that they never had a problem with raising the debt limit when Trump was in the White House and blowing holes in the deficit to give tax cuts to billionaires

241 notes

·

View notes

Text

So, what do you think will happen if our federal government keeps borrowing and spending?

(and borrowing and spending)

(and borrowing and spending)

(and borrowing and spending)

(and borrowing and spending)

#leadership#government#save america#government spending#government waste#federal spending#federal debt#borrow and spend#debt crisis#national debt#debt bomb#Debt apocalypse

4 notes

·

View notes

Text

A feud over spending cuts between hardline and centrist Republicans in the U.S. House of Representatives raises the risk that the federal government will suffer its fourth shutdown in a decade this fall.

Members of the hardline House Freedom Caucus are pushing to cut spending to a fiscal 2022 level of $1.47 trillion, $120 billion less than President Joe Biden and House Speaker Kevin McCarthy agreed to in their May debt ceiling compromise.

With Republicans also seeking higher spending on defense, veterans benefits and border security, analysts say the hardline target would mean cuts of up to 25% in areas such as agriculture, infrastructure, science, commerce, water and energy, and healthcare.

Centrists, who call themselves "governing" Republicans, say their hardline colleagues are ignoring the fact that their priorities are rejected by Democrats who control the Senate and White House, and that spending will wind up near the level agreed by McCarthy and Biden anyway.

The result is a major headache for centrist Republicans from swing districts that Biden won in 2020 and others with constituents in the firing line of hardline spending targets.

"The reductions are so deep," said Representative Don Bacon, a centrist Republican from Nebraska. "They want to make everything a root canal."

Hardliners view the 2024 fiscal year that begins on Oct. 1 as a test of Republican resolve to reduce the federal debt and move on to reform social programs including Medicare and Social Security.

"I don't fault any individual member for raising concerns and wanting to make sure that the bill is right for them and for their district," said Representative Ben Cline, who belongs to the Freedom Caucus, the conservative Republican Study Committee and the bipartisan Problem Solvers Caucus.

"What there has to be is an understanding that for there to be 218 Republican votes, the spending needs to be in line with pre-COVID levels rather than the debt-limit agreement."

One significant source of frustration is hardline demands for cuts to bills that have already been vetted by the 61-member House Appropriations Committee.

"We're not, willy-nilly, just trying to give money away. We're trying to focus and prioritize," said Representative David Joyce, a member of the appropriations committee who heads the 42-member centrist Republican Governance Group.

With Democrats opposed to hardline proposals, McCarthy can afford to lose no more than four Republican votes if he hopes to pass all 12 appropriations bills before funding expires on Sept. 30.

"I do not know how they get themselves out of this jam," said William Hoagland, a former Senate Republican budget director now at the Bipartisan Policy Center think tank.

TRICKY PATH

When the House returns from summer recess on Sept. 12, lawmakers will have 12 days to complete their bills and hammer out compromise legislation with the Senate or risk a partial government shutdown.

McCarthy acknowledged last week they may have to resort to a stopgap funding bill, known as a "continuing resolution," or CR, to keep federal agencies open.

That option could be complicated by hardline demands that it include some of former President Donald Trump's border policies, which Democrats reject.

Some House Republicans say the challenges are similar to disagreements McCarthy has overcome on other major legislation, including an April Republican debt ceiling bill that cemented his negotiating position in talks with Biden.

"The more appropriations bills we can get across the finish line, the more we'll have the leverage we need to negotiate a good deal with the Senate," said Representative Dusty Johnson, who chairs the Main Street Caucus, whose members describe themselves as "pragmatic conservatives".

Failure would mean another costly government shutdown starting in October, which would be the fourth in a decade.

SHUTDOWN RISK

House Freedom Caucus members say a shutdown could be necessary to achieve their objectives.

"It's not something that the members of the Freedom Caucus generally wish for," said Representative Scott Perry, who chairs the group of roughly three dozen conservatives.

"But we also understand that very little happens in Washington that's difficult, without someone or something forcing it to happen," he told Reuters.

Senate Majority Leader Chuck Schumer, the top Democrat in Congress, said last week that Republicans will be to blame for any new shutdown "if the House decides to go in a partisan direction."

Disputes over funding and policy have shut down the federal government three times in the past decade: once in 2013 over healthcare spending and twice in 2018 over immigration. A 35-day shutdown that began in December 2018 and ran into January 2019 cost the economy 0.02% of GDP, according to the nonpartisan Congressional Budget Office.

This time, the slim 222-212 House Republican majority could pay a political price. A shutdown would disrupt the lives of Americans barely a year before the 2024 election, when Republicans must defend 18 House seats in districts that Biden won in 2020.

McCarthy could face the prospect of having to resort to a CR that requires bipartisan support to pass, neutralizing the hardliners, analysts said.

That could endanger McCarthy's speakership under a deal he struck allowing a single lawmaker to move for his dismissal.

Would the House Freedom Caucus end McCarthy's reign over a CR?

"I wouldn't go that far," Perry said. "That's a final option. We want to work with the leadership. We want to work with Kevin, and we think that we can."

#us politics#news#reuters#republicans#conservatives#2023#us house of representatives#government shutdown#House Freedom Caucus#rep. Kevin McCarthy#biden administration#president joe biden#rep. Don Bacon#federal debt#rep. Ben Cline#rep. David Joyce#William Hoagland#continuing resolution#stopgap funding bill#rep. Dusty Johnson#sen. Chuck Schumer

12 notes

·

View notes

Text

Point The Finger In The RIGHT Direction ➡️

Given free rein, I think hardcore Republicans, those I refer to as the ‘radical right wing’ of the GOP, would gladly shut down all humanitarian programs such as food stamps, housing assistance, Social Security, Medicare/Medicaid, not to mention aid to other nations such as Ukraine, environmental programs, infrastructure, education, healthcare and more. They claim to be oh-so-concerned about the…

View On WordPress

#Donald Trump#Federal debt#George W. Bush#humanitarian programs#Robert Reich#tax cuts for the wealthy

0 notes

Text

The single most misunderstood and misused word in economics

The word is “debt.”

Virtually everyone believes they know what it means—I assume you do—but virtually everyone, including economists, is confused by the term.

Here is a dictionary definition:

Debt is an obligation that requires one party, the debtor, to pay money or otherwise withheld from another party, the creditor. Debt may be owed by a sovereign state , country, local government, company,…

View On WordPress

#Bernanke#federal debt#federal deficit#federal taxes don&039;t fund spending#Greenspan#monetary sovereignty#ticking time bomb

0 notes

Photo

Federal Spending and The $31 Trillion Debt Crisis in The United States

It is important that we realize we have over $31 Trillion of U.S. Federal Debt. A budget cut of $130 Billion in discretionary spending has NO impact on a $1.4 Trillion U.S Deficit. If the US Government was run like a business, then it would be bankrupt and closed for business. Less government and less spending is required. How can we pay down $31 Trillion of Debt? While there is no intention to ever pay this down, the U.S. National Debt is expected to reach $89 Trillion by the end of this decade. We need to have spending cuts, and not budget cuts. I believe in deadlines, objectives and ownership, and we need to institute deep federal spending cuts to reduce our budget deficit to zero within 3 years.

Another way of looking at the Debt Ceiling: You come home from work and find there has been a sewer backup in your home and the sewage is all the way up to your ceilings. Do you “raise the ceiling” or remove the waste?

Gerard Rotonda

$31.4 Trillion Debt Ceiling currently.

$31.8 Trillion is US National Debt as of today

https://www.usdebtclock.org

As of 2022 Year End:

(in $ Trillions) = 13 digits!!!

$ 4,900,000,000,000 U.S Tax Revenue

$ 6,270,000,000,000 Fed Spending

----------------------------------------------------------

$ 1,370,000,000,000 Deficit, New Debt

$30,930,000,000,000 National Debt

-------------------------------------------------

$ 130,000,000,000 Budget cut in Discretionary Spending

Simplified example - remove 8 zero’s

$ 49,000 Annual Family income

$ 62,700 The money the family spent

-------------------------------

$ 13,700 New debt on the credit card

$ 309,300 Outstanding balance on the credit card

-----------------------------

$ 1,300 Total budget cuts so far

While there is no intention to ever pay this debt down, the U.S. National Debt is expected to reach $89 Trillion by the end of this decade. We need spending cuts, and not budget cuts, to reduce our budget deficit to zero within 3 years.

1 note

·

View note

Text

Biden’s Cancellation of Billions in Debt Won’t Solve the Larger Problem

Biden’s Cancellation of Billions in Debt Won’t Solve the Larger Problem

For years, American lawmakers have chipped away at the fringes of reforming the student-loan system. They’ve flirted with it in doomed bills that would have reauthorized the Higher Education Act—which is typically renewed every five to 10 years but has not received an update since 2008. Meanwhile, the U.S. government’s student-debt portfolio has steadily grown to more than $1.5 trillion.

Today,…

View On WordPress

#Administration#American lawmakers#basic problem#Benjamin Rush#Biden’s debt relief#college#college degree#college education#college enrollment#college students#current loan-repayment pause#December 31.The debt relief#Democrats#early proponent of the idea of a national university#entire generation#federal debt#federal government#George Washington#GI Bill#good future#higher education#James Madison#lack of better words#largest federal investments#massive benefit#national identity#pandemic-relief measure#past half century#Pell Grant recipients#Pell Grants

0 notes

Text

Canada’s debt level is sustainable over long term, parliamentary budget officer says - National

Canada’s debt level is sustainable over long term, parliamentary budget officer says – National

The parliamentary budget officer says Canada’s current fiscal policy is sustainable over the long term.

The PBO’s latest fiscal sustainability report, released Thursday, finds that Canada’s overall debt level is projected to decline steadily over time.

At the federal level, the report says, the government could permanently increase spending or reduce taxes by 1.8 per cent of GDP and remain…

View On WordPress

#Budget#budget 2022#Canada#Canada Budget#Canada budget 2022#Canada debt#canada debt levels#Canada economy#Canada News#debt canada#debt levels canada#Economy#Featured#federal debt#Fiscal policy

0 notes

Text

Why the Fed wants to crush workers

The US Federal Reserve has two imperatives: keeping employment high and inflation low. But when these come into conflict — when unemployment falls to near-zero — the Fed forgets all about full employment and cranks up interest rates to “cool the economy” (that is, “to destroy jobs and increase unemployment”).

An economy “cools down” when workers have less money, which means that the prices offered for goods and services go down, as fewer workers have less money to spend. As with every macroeconomic policy, raising interest rates has “distributional effects,” which is economist-speak for “winners and losers.”

Predicting who wins and who loses when interest rates go up requires that we understand the economic relations between different kinds of rich people, as well as relations between rich people and working people. Writing today for The American Prospect’s superb Great Inflation Myths series, Gerald Epstein and Aaron Medlin break it down:

https://prospect.org/economy/2023-01-19-inflation-federal-reserve-protects-one-percent/

Recall that the Fed has two priorities: full employment and low interest rates. But when it weighs these priorities, it does so through “finance colored” glasses: as an institution, the Fed requires help from banks to carry out its policies, while Fed employees rely on those banks for cushy, high-paid jobs when they rotate out of public service.

Inflation is bad for banks, whose fortunes rise and fall based on the value of the interest payments they collect from debtors. When the value of the dollar declines, lenders lose and borrowers win. Think of it this way: say you borrow $10,000 to buy a car, at a moment when $10k is two months’ wages for the average US worker. Then inflation hits: prices go up, workers demand higher pay to keep pace, and a couple years later, $10k is one month’s wages.

If your wages kept pace with inflation, you’re now getting twice as many dollars as you were when you took out the loan. Don’t get too excited: these dollars buy the same quantity of goods as your pre-inflation salary. However, the share of your income that’s eaten by that monthly car-loan payment has been cut in half. You just got a real-terms 50% discount on your car loan!

Inflation is great news for borrowers, bad news for lenders, and any given financial institution is more likely to be a lender than a borrower. The finance sector is the creditor sector, and the Fed is institutionally and personally loyal to the finance sector. When creditors and debtors have opposing interests, the Fed helps creditors win.

The US is a debtor nation. Not the national debt — federal debt and deficits are just scorekeeping. The US government spends money into existence and taxes it out of existence, every single day. If the USG has a deficit, that means it spent more than than it taxed, which is another way of saying that it left more dollars in the economy this year than it took out of it. If the US runs a “balanced budget,” then every dollar that was created this year was matched by another dollar that was annihilated. If the US runs a “surplus,” then there are fewer dollars left for us to use than there were at the start of the year.

The US debt that matters isn’t the federal debt, it’s the private sector’s debt. Your debt and mine. We are a debtor nation. Half of Americans have less than $400 in the bank.

https://www.fool.com/the-ascent/personal-finance/articles/49-of-americans-couldnt-cover-a-400-emergency-expense-today-up-from-32-in-november/

Most Americans have little to no retirement savings. Decades of wage stagnation has left Americans with less buying power, and the economy has been running on consumer debt for a generation. Meanwhile, working Americans have been burdened with forms of inflation the Fed doesn’t give a shit about, like skyrocketing costs for housing and higher education.

When politicians jawbone about “inflation,” they’re talking about the inflation that matters to creditors. Debtors — the bottom 90% — have been burdened with three decades’ worth of steadily mounting inflation that no one talks about. Yesterday, the Prospect ran Nancy Folbre’s outstanding piece on “care inflation” — the skyrocketing costs of day-care, nursing homes, eldercare, etc:

https://prospect.org/economy/2023-01-18-inflation-unfair-costs-of-care/

As Folbre wrote, these costs are doubly burdensome, because they fall on family members (almost entirely women), who have to sacrifice their own earning potential to care for children, or aging people, or disabled family members. The cost of care has increased every year since 1997:

https://pluralistic.net/2023/01/18/wages-for-housework/#low-wage-workers-vs-poor-consumers

So while politicians and economists talk about rescuing “savers” from having their nest-eggs whittled away by inflation, these savers represent a minuscule and dwindling proportion of the public. The real beneficiaries of interest rate hikes isn’t savers, it’s lenders.

Full employment is bad for the wealthy. When everyone has a job, wages go up, because bosses can’t threaten workers with “exile to the reserve army of the unemployed.” If workers are afraid of ending up jobless and homeless, then executives seeking to increase their own firms’ profits can shift money from workers to shareholders without their workers quitting (and if the workers do quit, there are plenty more desperate for their jobs).

What’s more, those same executives own huge portfolios of “financialized” assets — that is, they own claims on the interest payments that borrowers in the economy pay to creditors.

The purpose of raising interest rates is to “cool the economy,” a euphemism for increasing unemployment and reducing wages. Fighting inflation helps creditors and hurts debtors. The same people who benefit from increased unemployment also benefit from low inflation.

Thus: “the current Fed policy of rapidly raising interest rates to fight inflation by throwing people out of work serves as a wealth protection device for the top one percent.”

Now, it’s also true that high interest rates tend to tank the stock market, and rich people also own a lot of stock. This is where it’s important to draw distinctions within the capital class: the merely rich do things for a living (and thus care about companies’ productive capacity), while the super-rich own things for a living, and care about debt service.

Epstein and Medlin are economists at UMass Amherst, and they built a model that looks at the distributional outcomes (that is, the winners and losers) from interest rate hikes, using data from 40 years’ worth of Fed rate hikes:

https://peri.umass.edu/images/Medlin_Epstein_PERI_inflation_conf_WP.pdf

They concluded that “The net impact of the Fed’s restrictive monetary policy on the wealth of the top one percent depends on the timing and balance of [lower inflation and higher interest]. It turns out that in recent decades the outcome has, on balance, worked out quite well for the wealthy.”

How well? “Without intervention by the Fed, a 6 percent acceleration of inflation would erode their wealth by around 30 percent in real terms after three years…when the Fed intervenes with an aggressive tightening, the 1%’s wealth only declines about 16 percent after three years. That is a 14 percent net gain in real terms.”

This is why you see a split between the one-percenters and the ten-percenters in whether the Fed should continue to jack interest rates up. For the 1%, inflation hikes produce massive, long term gains. For the 10%, those gains are smaller and take longer to materialize.

Meanwhile, when there is mass unemployment, both groups benefit from lower wages and are happy to keep interest rates at zero, a rate that (in the absence of a wealth tax) creates massive asset bubbles that drive up the value of houses, stocks and other things that rich people own lots more of than everyone else.

This explains a lot about the current enthusiasm for high interest rates, despite high interest rates’ ability to cause inflation, as Joseph Stiglitz and Ira Regmi wrote in their recent Roosevelt Institute paper:

https://rooseveltinstitute.org/wp-content/uploads/2022/12/RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

The two esteemed economists compared interest rate hikes to medieval bloodletting, where “doctors” did “more of the same when their therapy failed until the patient either had a miraculous recovery (for which the bloodletters took credit) or died (which was more likely).”

As they document, workers today aren’t recreating the dread “wage-price spiral” of the 1970s: despite low levels of unemployment, workers wages still aren’t keeping up with inflation. Inflation itself is falling, for the fairly obvious reason that covid supply-chain shocks are dwindling and substitutes for Russian gas are coming online.

Economic activity is “largely below trend,” and with healthy levels of sales in “non-traded goods” (imports), meaning that the stuff that American workers are consuming isn’t coming out of America’s pool of resources or manufactured goods, and that spending is leaving the US economy, rather than contributing to an American firm’s buying power.

Despite this, the Fed has a substantial cheering section for continued interest rates, composed of the ultra-rich and their lickspittle Renfields. While the specifics are quite modern, the underlying dynamic is as old as civilization itself.

Historian Michael Hudson specializes in the role that debt and credit played in different societies. As he’s written, ancient civilizations long ago discovered that without periodic debt cancellation, an ever larger share of a societies’ productive capacity gets diverted to the whims of a small elite of lenders, until civilization itself collapses:

https://www.nakedcapitalism.com/2022/07/michael-hudson-from-junk-economics-to-a-false-view-of-history-where-western-civilization-took-a-wrong-turn.html

Here’s how that dynamic goes: to produce things, you need inputs. Farmers need seed, fertilizer, and farm-hands to produce crops. Crucially, you need to acquire these inputs before the crops come in — which means you need to be able to buy inputs before you sell the crops. You have to borrow.

In good years, this works out fine. You borrow money, buy your inputs, produce and sell your goods, and repay the debt. But even the best-prepared producer can get a bad beat: floods, droughts, blights, pandemics…Play the game long enough and eventually you’ll find yourself unable to repay the debt.

In the next round, you go into things owing more money than you can cover, even if you have a bumper crop. You sell your crop, pay as much of the debt as you can, and go into the next season having to borrow more on top of the overhang from the last crisis. This continues over time, until you get another crisis, which you have no reserves to cover because they’ve all been eaten up paying off the last crisis. You go further into debt.

Over the long run, this dynamic produces a society of creditors whose wealth increases every year, who can make coercive claims on the productive labor of everyone else, who not only owes them money, but will owe even more as a result of doing the work that is demanded of them.

Successful ancient civilizations fought this with Jubilee: periodic festivals of debt-forgiveness, which were announced when new monarchs assumed their thrones, or after successful wars, or just whenever the creditor class was getting too powerful and threatened the crown.

Of course, creditors hated this and fought it bitterly, just as our modern one-percenters do. When rulers managed to hold them at bay, their nations prospered. But when creditors captured the state and abolished Jubilee, as happened in ancient Rome, the state collapsed:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Are we speedrunning the collapse of Rome? It’s not for me to say, but I strongly recommend reading Margaret Coker’s in-depth Propublica investigation on how title lenders (loansharks that hit desperate, low-income borrowers with triple-digit interest loans) fired any employee who explained to a borrower that they needed to make more than the minimum payment, or they’d never pay off their debts:

https://www.propublica.org/article/inside-sales-practices-of-biggest-title-lender-in-us

[Image ID: A vintage postcard illustration of the Federal Reserve building in Washington, DC. The building is spattered with blood. In the foreground is a medieval woodcut of a physician bleeding a woman into a bowl while another woman holds a bowl to catch the blood. The physician's head has been replaced with that of Federal Reserve Chairman Jerome Powell.]

#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters

465 notes

·

View notes

Text

In October, tens of millions of borrowers will be required to pay their monthly federal student loan bills for the first time since March 2020, the Department of Education clarified Monday.

The pandemic-related pause on both payments and interest accumulation has been set to end later this summer, though the exact date payments would be due was a little fuzzy.

The Biden administration had previously said that the pause would end either 60 days after June 30 or 60 days after the Supreme Court rules on the separate student loan forgiveness program – whichever comes first.

A law passed in early June to address the debt ceiling officially prevented the pandemic-related pause from being extended again. The repayment date has been extended a total of eight times under both the Biden and Trump administrations.

“Student loan interest will resume starting on September 1, 2023, and payments will be due starting in October. We will notify borrowers well before payments restart,” the Department of Education said in a statement sent to CNN Monday.

The update was first reported by Politico.

Borrowers typically receive their bill statements from their loan servicer a few weeks before they are due. Not every borrower’s bill is due at the same time of the month.

The Department of Education has said that it will be in direct communication with borrowers and ramp up its communication with student loan servicers before repayment resumes.

Student loan experts recommend that borrowers reach out to their student loan servicer with any questions about their loans as soon as possible, especially if they are interested in enrolling in an income-driven repayment plan. Those plans, which set payments based on income and family size, can lower monthly payments but require borrowers to submit some paperwork.

Federal student loan borrowers can check the Federal Student Aid website for updates on resuming payments.

SOME BORROWERS COULD BE AT RISK OF DEFAULT

Some borrowers may struggle to resume paying their monthly student loan bills.

More student loan borrowers are currently behind on other kinds of bills than they were before the COVID-19 pandemic, according to a recent study by the Consumer Financial Protection Bureau.

The report also said that about 1 in 5 student loan borrowers have risk factors that suggest they could struggle when scheduled payments resume, like being delinquent on student loan payments before the pandemic or having multiple student loan servicers.

When payments restart, many people might be confused about how much they owe, when to pay and how. Millions of borrowers will have a different servicer handling their student loans since the last time they made a payment.

Originally, the pause on federal student loan payments was put in place to help borrowers struggling financially due to the pandemic.

From a jobs perspective, the economy has largely recovered from the pandemic-related disruptions. In May, 3.7 million more people were working than in February 2020.

But there are some soft spots. Major layoffs have recently been announced at big companies like Disney and Amazon. Earlier this year, a regional banking crisis was set off by the collapse of Silicon Valley Bank, the largest bank to fail since the 2008 financial crisis. And inflation remains high but is cooling after reaching a 40-year peak last year.

STUDENT LOAN FORGIVENESS STILL ON THE TABLE

Meanwhile, all eyes are on the Supreme Court as borrowers wait to see if the Biden administration will be allowed to move forward with its student loan forgiveness program. A decision is expected in late June or early July.

Under the proposal, individual borrowers who made less than $125,000 in either 2020 or 2021 and married couples or heads of households who made less than $250,000 a year could see up to $10,000 of their federal student loan debt forgiven.

If a qualifying borrower also received a federal Pell grant while enrolled in college, the individual is eligible for up to $20,000 of debt forgiveness.

But several lawsuits argue that the Biden administration is abusing its power and using the pandemic as a pretext for fulfilling the president’s campaign pledge to cancel student debt.

No debt has been canceled yet. But if the Supreme Court allows the program to take effect, it’s possible the government moves quickly to forgive the debts of 16 million borrowers who the administration already approved for relief.

If the Justices strike down Biden’s student loan forgiveness program, it could be possible for the administration to make some modifications to the policy and try again – though that process could take months.

#us politics#news#cnn politics#president joe biden#biden administration#student loan forgiveness#cancel student loans#federal student loans#student debt forgiveness#student loan debt#us supreme court#scotus#2023#Department of Education#politico#Consumer Financial Protection Bureau

172 notes

·

View notes

Text

THE STUDENT LOAN FORGIVENESS APPLICATION... IS LIVE!!!

IT’S HAPPENINGGGGGGG

Ok that’s too much capslock. Go here to fill out the application, babies:

Student loan forgiveness application

It takes about 30 seconds to fill out with your basic info. And while the site is in beta mode (or so it says) it seems... extremely well-designed and user friendly for a government site? Where was this level of web design when the ACA was passed?

If you have student loans we IMPLORE YOU to fill it out and see if you qualify. If you have questions (and who don't?), see our FAQ on student loan forgiveness here:

The 2022 Student Loan Forgiveness FAQ You've Been Waiting For

#student loan forgiveness#student loans#student debt#debt relief#federal student loans#Joe Biden#student loan debt relief#debt forgiveness#student loan forgiveness application#government

356 notes

·

View notes

Text

Fact Vs Fiction

There are so many misconceptions and falsehoods swirling around the upcoming debt ceiling debate that people don’t know what to think. Today’s newsletter from Robert Reich pushes aside the lies and cuts to the core of things, including why the nation needs to keep borrowing more to pay its bills.

The biggest story you’ve never heard about today’s federal debt

America’s wealthy used to pay taxes…

View On WordPress

#Debt ceiling#Federal debt#income disparity#Lies lies and more lies#Robert Reich#tax cuts for the wealthy#U.S. Congress

0 notes

Text

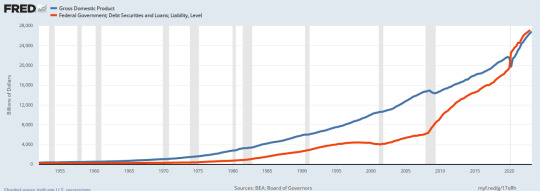

A child's picture book for those who tell you the federal debt is too high

Page 1.

As federal debt (red) has risen, so has the economy (blue — GDP). Higher federal debt leads to higher GDP growth. The reason: GDP=Federal Spending +Non-federal Spending + Net Exports.

Page 2. The reason:

Economic growth and federal debt growth have been extraordinarily high since the end of the COVID recession. Despite efforts to reduce Federal Debt growth — efforts that, if successful,…

View On WordPress

0 notes

Last Seen Blogs

ignatiius-archived

c'est le malheur qui a fait de moi un monstre

firmbutfairmatureman

spanking service for women

yee-yee-babes

I Want A Cowboy Hat

lipsuponmyfingertips

Lips Upon My Fingertips.

semimero

Une Goutte de Nuage.