#new Mortgage Calculators

Text

Unlock the Power of Your Mortgage: Use a Calculator to See the Benefits of Extra Payments

and subheadings in the word count

Unlock the Power of Your Mortgage: Use a Calculator to See the Benefits of Extra Payments

Making extra payments on your mortgage can be a great way to save money and pay off your loan faster. By making extra payments, you can reduce the amount of interest you pay over the life of the loan and potentially save thousands of dollars. But how do you know if making…

View On WordPress

#best Mortgage Calculators#mortgage calculator amortization#Mortgage Calculators#mortgage calculators australia#mortgage calculators canada#mortgage calculators nationwide#mortgage calculators uk#mortgage calculators with extra payments#new Mortgage Calculators

0 notes

Text

#me this fine thursday morning 🤠#honestly I’ve been really enjoying my new job because I get to specialise in what I want and my boss is a literal angel#like i would do anything for her bcs she is such a kind soul who is constantly looking out for the people under her charge#and she’s so down to earth and easy to work with#BUT. my mom has been throwing all kinds of shade and subtext at me#and I keep telling myself it’s a small thing I’m used to it it shouldn’t grate on my nerves so much#but it does??? and I can’t keep gaslighting myself???#tldr she lowkey thinks I got ‘let off’ my previous job bcs I was lazy and left a bad impression due to my coming in late#but what about all the 3am nights?????? girl’s gotta sleep????#also I literally told my previous job ‘give me disputes or nothing’ and they couldn’t give me what I wanted bcs it was a bad time#and just recession vibes#so they offered for me to go to Dubai instead#which my mom just INSISTS was a dumping ground bcs I wasn’t good enough or smt wtf#meanwhile she gets so defensive of my sister who hasn’t worked for nearly 4 years#I tried to tell her FACTS and she literally told me not to accuse my sister and that she’s working part time and I’m like??? she’s not???#and my sister is being so miserly and insufferably calculative over every penny#while JETTING OFF EVERYWHERE ON BUSINESS CLASS. I JUST. ?!?-&:&/!:!:!:$:#anyway the subtext is just that my mom is concerned her only source of income aka me will be cut off lol#but I was still??? giving her an allowance while travelling??? meanwhile my sister is just asking us to cough up $$ for her share of the#mortgage?????!????!!!!?#what a morning. I’m so mad I could punch a wall lol#Spotify

1 note

·

View note

Text

Calculating Your New Home Budget: How Much Can You Afford to Spend?

The dream of homeownership is a beacon of hope, a testament to your aspirations and hard work. It’s the vision of your sanctuary, where the morning sun filters through the curtains and the laughter of loved ones fills the air. But before you get lost in the reverie of choosing paint colours and arranging furniture, there’s a practical question that requires your attention: How much can you…

View On WordPress

#Budgeting#debt-to-income ratio#down payment impact#Financial planning#future financial goals#home purchase finances#homeownership decision#mortgage calculations#new home affordability#PITI expenses#pre-approval process#real estate budgeting#real estate budgetingbudgeting

0 notes

Text

Mortgage payment calculator- How much can you borrow?

Mortgage payment calculator- How much can you borrow?

FIRST-TIME buyers may find they’re offered smaller mortgages as interest rates rise after record lows during the pandemic. There are mortgage calculators available that can help yo

Read Full Text

View On WordPress

0 notes

Text

#National commercial banks #Regional and community banks #Asset-based lenders #Non-bank lenders #Mezzanine fund #PO Factors and Lenders #SBIC and BDC #Equipment Finance Lenders #Family Offices #Private Debt Funds #student loan #Risk debt #Business loans for bad credit #Business line of credit #Business loans for women #Business Term Loans #Equipment financing #Financing of invoices/receivables #Merchant Cash Advance #Revenue Based Business Loan #SBA Business Loan #Working capital loan #TERM LOANS #CREDIT LINE #ASB LOANS #ASSET-BASED FINANCING #LOANS-BRIDGE #ALTERNATIVE LOANS #MERCHANT MONEY ADVANCE #EQUIPMENT FINANCING #FINANCING OF INVOICES #USDA BUSINESS

# STOCK LOAN # securities-based lending # share-secured loan # leveraged buyout # Growth capital # merchant banking

Best Advisor : [email protected]

#finance#business#how to earn money#money slave#investment#invoice#investors#debt help#get out of debt guy new articles#mortgage calculator#marchés#capital risk#central banking#buyout#shareholders#stock news#trends#merchantservices#merchant cash movies#rates#instant loan#payday loan#loans#credit types#sbahj#sbi cap#asset management#asset finance#asset class#commercial real estate

1 note

·

View note

Text

ULTIMATE Realistic Money overhaul | Roleplay Guide | The sims 3

TYSM for 600+ subscribers on Youtube!

youtube

Introduction:

Hello everyone and welcome back to my channel! In today's video I'm going to show you how to overhaul the sims 3 economy, how to have complete control over your billing system, and how to have a more realistic money exchange mechanic! We will also be exploring how to go about a much more realistic renting/mortgage system. This guide has been a long time coming, it's very simple and beginner friendly, but to find all the mods it would take to set this up would be a pain for anyone trying to revamp their sims economy. I've playtested this mod setup for a couple of years, and I can never go back to the original EA economy and billing system. All of these mods work with each other in a synergy circle, they compliment, play off of, and enhance one another. All links will be included in my tumblr guide, and the comment leading to my tumblr guide will be pinned in the comments below. I recommend following alongside the guide and the video, especially if you do not speak english, so you can translate the guide to your native language, while still being able to follow along the video! If I am talking too slowly for you I highly recommend everyone to increase the video speed to x2, and slow it down at certain parts you need extra focus on. Don't worry, I won't be offended at all by this, I do it myself for tutorial videos.

First - Overhaul the sims economy.

No bills

First we need to get rid of the EA billing system. This is because we are going to add new mods that introduce much more realistic billing and rental mechanics. This also eliminates some core issues with the EA billing system. Such as having a large piece of land, but a tiny house, and your bills being upwards of 40k every couple of days. Utilities not being calculated properly. And being billed more because of your more expensive items on your lot. Since we are also overhauling the sims economy, the original EA calculations wouldn't make any sense anymore.

EVM Career Wages

This mod adds a much more realistic financial wage system. Since we have now removed EA bills, our sims wages need to be able to reflect the more realistic economy we are going for. Gone are the days of every Sim earning a fortune with a mere $45 per hour entry-level job. This mod adjusts the wages across all career levels to align with real-world standards, creating a more immersive gameplay experience.

With EVM Career Wages, climbing the career ladder feels genuinely rewarding as higher pay accompanies each promotion. This encourages players to strive for advancement and invest in their Sims' professional growth. Additionally, when paired with the UC mod, promotions become more challenging to attain, placing greater emphasis on the player's decisions and strategic gameplay.

Camo fairer priced groceries and books

Camo tweaked goods

Revamped Economy Essentials:

With Camo's Fairer Priced Groceries and Books alongside Camo's Tweaked Goods, the Sims 3 economy undergoes a significant transformation. These combined mods slash the prices of commonly purchased items, bringing a newfound sense of realism to the game. No longer will a single egg set you back $11; now, it's a mere $2, making grocery shopping a more authentic experience. The same principle applies to book prices, ensuring that essential items are now more affordable for Sims across the board.

This overhaul becomes even more impactful when paired with the Savvier Seller mod, which ensures that prices are not only reasonable for your household but also for the entire neighborhood. This adds a more balanced and lifelike economy, where every Sim can afford the necessities without breaking the bank.

taxi charge

simsmathew subway charger

Realistic Transportation Fees:

Combining the Taxi Charge and Simsmathew Subway Charger mods introduces a new level of realism to transportation in The Sims 3. Each time your Sims opt for a taxi ride or subway journey, they'll incur a small fee. This adds a layer of financial consideration, prompting players to rethink their Sims' commuting habits.

Immersive roleplaying opportunities emerge as players strategize the best way to navigate their Sims from point A to point B. Whether it's opting for eco-friendly methods like walking or biking, or planning a journey that involves a mix of walking and subway rides, every choice impacts your Sims' budget and experience.

This deeper level of engagement allows players to connect with their Sims on a more personal level, experiencing the journey alongside them and enjoying the rich scenery and interactions along the way. Now you'll be pushed to experience y

Ani tax collector

New Billing System:

The tax collector mod essentially allows you to create your own billing and taxing system. This mod introduces a scripted computer interface with customizable settings, allowing players to seamlessly implement various taxes and fees. From water and electricity bills to health insurance premiums and car payments, Sims will autonomously be directed to settle these financial obligations once the tax settings are activated.

For an added layer of realism and roleplay, consider situating these computers at opened rabbithole like the city hall. This not only streamlines your Sim's outing tasks but also enriches the gameplay experience, allowing players to engage in more dynamic and immersive storytelling.

I'm going to go in game and show you how I achieve this effect for a very quick and easy tutorial.

So because we turned off the EA billing system, we need to create our own bills, to still simulate having to lose money through our gameplay. You can place these new tax computers on an opened city hall rh lot (if you don't care for aesthetic then I recommend placing these in the basement), or another community lot altogether. Please note that if you place these computers on a cityhall RH lot, and you enable UC mod on that lot, you should lock the doors leading to the tax computers. This is because with SonyaJu's UC version, the sims working on the lot will be pushed to use the computers which will result in all of your sims being sent to pay their taxes throughout the day. You can lock community doors using Nraas Go Here, or nona lock community doors mod as an alternative.

Now that we have set up our computers, you click the settings and rename the computer. Rename this to any bill you want to pay. Here I am setting up a, Water, Electric, Phone bill, Car note, and Car insurance computer. Now I can click on tax collector > settings > edit multiplier.

Water = 0.8

Electric = 0.4

Phone - 0.2

Car note = 0.5

Car insurance = 0.6

these multipliers automatically calculate what you currently have available in your sims household funds, and deducts the "tax" based off of the multiplier. This adds a more logical calculations to what each individual household could actually afford, without being too overbearing on your funds loss. This make a much more realistic and immersive billing system actually possible in the game, that fixes a lot of the issues with EA billing system, and matches the new sims economy we have created with this combination of mods.

Which leads me to my next part. I pay all of these bills monthly in my game. This adds a much more immersive and realistic experience, and I even have to keep an eye on my sims budget throughout the month, like in real life. Sometimes, I may have to sell things or find any way to make extra money to pay my new bills, or pick which bill I have to pay if I can't afford them all. I give myself consequences if I can't afford certain things. When I show you how to use the new renting system, I'll even roleplay getting evicted as a consequence if I can't afford my rent.

Enhancement Miscellaneous Mods:

The collection of these next mods serve to either rectify the Sims economy hiccups or introduce a fresh layer of roleplay, prompting players to reassess their spending habits and EP career choices.

Some of these mods make purchasing certain items actually reusable like bubble bath products and painting supplies. While others make certain careers have higher payouts which makes the wages for that career make more sense and become more satisfying so you'd actually want to work at it. This also enhances rags-to-riches playthroughs, rendering them more intricate and gratifying.

For instance, with these mods combined, the necessity for pets to rely on manually refilled food bowls instead of random props elevates pet care to a level akin to caring for a toddler. This makes having a pet a lot more impactful in your household, as well as financially.

In general, all of these mods balance back out certain EA default settings, which slowly begins to push together a more and more realistic economy.

I will place the mods you want to add on the screen, and all the links will be provided in the tumblr guide.

speedo higher concert payouts

picnicbasketpricechange

bubble bath runs out

pet bowl needs food

Nona always more gigs 3 times money

wildflowernerf per value

Double money highchancs faster mooch skill

painting needs supplies

painting costs money

government benefits and service

This mod is tailored to amplify the immersive experience of playing as lower-income households in The Sims 3. This mod introduces a plethora of meticulously scripted game mechanics designed to add depth and realism to the struggles and triumphs of impoverished Sims.

One standout feature is the ability to establish child support payments, calculated with precision based on the target parent's income. This introduces a compelling dynamic for players who wish to roleplay scenarios involving relationships with wealthier partners, where child support checks become a lifeline for sustaining the family's livelihood, as an example.

Furthermore, Sims can now apply for various forms of assistance such as health insurance and Electronic Benefit Transfer (EBT), opening up new avenues for navigating the challenges of financial hardship within the game. These additions inject a newfound sense of complexity and realism into rags-to-riches playthroughs, providing players with additional gameplay mechanics to consider and explore. You'll find yourself embarking on a journey of resilience and resourcefulness as you guide your Sims through the highs and lows of economic adversity in the game.

If you are following my guide step by step consider applying these tweaks to the xml's.

As an added note, I no longer add a health insurance tax collector computer, as with MonocoDoll's new GA mod poorer sims can get affordable health care, and sims who do not qualify for this have a good job where I imagine the job offers it's own health insurance instead. So because of this new mod addition, this eliminates the need to set up health insurance payments for my households.

Second - Career's addon's

Gamefreak's check for work

job overhaul

lemonaise 50 jobs offer

These mods revolutionizes the Sims' job acquisition process, enhancing realism and depth. This also enhances the effectiveness of attending university. Without a degree, Sims may struggle to secure certain jobs and will always start at entry level.

The mod introduces a comprehensive interview and application process, typically lasting about an hour in-game, during which Sims disappear into the rabbit hole. Sims can attend resume building and interview classes to improve their chances of employment, mimicking real-life strategies. Uploading a resume, particularly a University Life degree, significantly boosts job prospects.

Maintaining cleanliness, hunger, and a positive mood is crucial as neglecting these factors decreases the likelihood of job offers. The "check for work" option allows Sims to scout for job openings beyond the replaced job hunting UI.

Lemonaise's 50 Jobs Offer expands job opportunities, reflecting the realistic scenario where obtaining desired employment may require starting elsewhere. Just as in real life, a degree does not guarantee the desired job immediately, necessitating patience and flexibility in career pursuits.

This mod combination adds layers of realism and challenges, making Sims' lives more expansive and rewarding. Achieving dream jobs becomes a testament to perseverance and hard work, enhancing the sense of accomplishment for players.

Ani's job board

Ani's Job Board introduces a WA-inspired board object that fills the gap left by missing opportunities in UC mod. With UC's scripted behaviors for work, some autonomous opportunities were removed. However, this mod remedies the situation by providing Sims with a platform to browse and undertake additional work and school opportunities. Now, players have the autonomy to choose whether to pursue these extra projects, adding depth and flexibility to their Sims' lives.

Nraas Careers

Nraas Careers is a mod that expands the possibilities for Sims by enabling custom careers and establishing a homeworld university. While the details of setting up a homeworld university can be explored in another video, this guide focuses on how this mod integrates custom career opportunities with UC. With Nraas Careers, players can seamlessly bind custom careers to EA careers, unlocking a wealth of new professional paths for their Sims within the game. What this means in basic terms, is that UC works by adding a number of objects sims use on a lot, to increase their work/school performance. If you are playing as a custom career, UC won't know which objects can increase that careers performance if the career hasn't been bonded to an EA career.

Sonja's UC

Sonja's UC is an enhanced iteration of Zerbu's UC mod, designed to optimize the original mod's scripting for improved performance and stability. While still a work in progress and subject to occasional issues, this update enhances the main features of the mod, resulting in faster and smoother gameplay. Sims now spend less time deliberating their actions, experience reduced lag before heading to work, and are not as rigidly constrained to complete tasks. Instead, they are encouraged to take breaks and socialize, mirroring real workplace dynamics.

Although ongoing testing is underway, I recommend trying out this version as it also introduces additional modded script objects to careers. Setting up the mod in-game is straightforward and can be easily demonstrated.

zoeoe flower arranging

knitting

pheobejaysims take sims to court

pheobejaysims betting

On the Screen, will be a selection of miscellaneous mods that enrich your gameplay experience by introducing custom playable careers and intricately scripted mechanics.

With these mods, you can immerse yourself in diverse professions such as modeling, flower arranging, or managing a home-based Etsy-style knitting business. Additionally, you have the opportunity to delve into the legal world as an attorney or explore the unique avenue of earning money through litigation against other Sims and establishments.

For those inclined towards risk and excitement, Phoebejaysims' Betting mod allows for a full-time gambling lifestyle, leveraging specific store objects to enhance the thrill of the game.

These mods significantly expand the scope of gameplay possibilities, offering players a plethora of new career paths and immersive money mechanics to explore and enjoy.

Third - Biggest gameplay changes and fixes

Bank mod

Otherwise known as the non-core global banking mod, this mod is a game-changer in how you manage money in The Sims. This mod allows you to establish a bank account for your Sims, complete with essential banking functionalities like deposits, withdrawals, and money transfers.

I'll guide you through setting up a new renting and mortgage system in-game, offering alternative perspectives on cash handling, including household funds versus bank account funds. Additionally, I'll show you how to separate all Sims' incomes and present an edited version where the bank account resembles a debit card in your Sims' inventory.

Let's dive into these transformative features that will revolutionize your Sims' financial management experience.

How to make a bank account.

Simply click on a computer, whether on your home lot or community lot. Navigate to online banking interaction > Open Account. $25 will be deducated automatically, and you will have a new bank account in your sims inventory.

How to create a landlord.

Simply select any sim you would like to be your new landlord. Using Nraas MC > Make Active, you can then open a bank account for the selected sim you've chosen to be your landlord.

How to pay rent.

Once the bank account has been sucessfully opened you can go back to your original active household. Then select the bank account in your sims inventory > Transfers, if you are friends with the landlord then select "Sims you know", if you are not friends with them then select "in your neighborhood". Navigate the list to find your new landlord, then send them your rent or mortgage for the month.

How to separate income.

Using this banking system I separate my sims money by having their bank account as their debit card and their household funds as their cash on hand. I typically, split up the funds reasonably between everyone's bank account in the household. This leaves $0 in the household funds. Once a sim is done with their work day, the exact amount of money they made for the day will go straight into your household funds. From there, I deposit that money into their bank account. It only takes a couple of seconds and is very simple.

As an added note, when sending the sims out and about in the world, I'll need the money from their account in the household funds so that they are able to spend money. So I quickly withdraw a random amount of money I think they will need for the outing, allowing them to actually buy what they want from the community lots. For extra immersion, consider adding a deco ATM machine, to simulate where your sims would be withdrawing their money from.

Just as promised, I told you how I would roleplay an eviction process, using this new renting system. If my sims cannot pay the rent, and they ask their landlord to an outing, if the landlord does not have a good time then I only get 1 sim month to leave the home or pay rent for both months. If the landlord does have a good time, then I imagine they allowed me to skip my rent payment for that month. If I still don't have rent money by the end of the month, I move my sim to a 10x10 empty lot somewhere in the world, and have my sim live out of a tent, or shady motel (set as a base camp), until I can afford to move into another home. If I choose to live in a motel, while the base camps are free to stay in, I create a custom role titled "Motel front desk", open that sim a bank account, and then pay them $100 weekly, while this is still a payment it is much cheaper than my sims rent that we couldn't afford, and still allows me to roleplay money being lost. If I don't have to be completely homeless then I won't, if I have $0, then I will.

nraas consigner

nraas register

Nraas Consigner and Nraas Register are essential mods that address the shortcomings of the register systems in the base game. Consigner enhances gameplay by introducing the option to make all items consignable, simulating a realistic thrift store or pawn shop experience. Meanwhile, Register adds extra checks to ensure Sims are correctly assigned, along with providing additional population controls beyond the capabilities of Story Progression. Whether or not you utilize other mods, these fixes are indispensable for enhancing your gameplay experience.

Exciting Update Alert!

@olomaya on Tumblr is currently developing an innovative new renting system for the game, which promises to offer Simmers a wide array of options for money roleplaying. This upcoming system represents a significant evolution in gameplay mechanics, potentially replacing older systems and providing fresh opportunities for immersive financial management.

Stay tuned for a comprehensive guide on this mod, which will delve into its functionalities, compatibility considerations, and potential replacements for older mechanics. Until this mod is developed, playtested, and released, I'll be using this system that I have set up and just showed you guys in this video!

So this concludes everything that I wanted to show you guys! You now know how to set up a more realistic billing system. Renting/mortgage system. You've learned how to add and roleplay more complex money gaming mechanics. You've overhauled your wage system, as well as your cost of living economy in the world. And none of these are too overbearing, with just a little bit of set up, you'll have an ultimate realistic economy and money system in your sims 3 from now on! Thank you all for joining me, thank you for 600 subscribers, and thank you for your love and support! I'll see you all in the next video!

91 notes

·

View notes

Text

Mortgage Calculator Service in California:

Use the free California Mortgage Calculator to estimate your monthly payment, including taxes, mortgage insurance, principal, and interest.

A mortgage calculator helps in calculating things in a few minutes.

Buying a new home is a time of dreams and opportunity, but navigating the mortgage process can also make it stressful and confusing. Different interest rates and repayment terms can make it difficult to compare mortgage loan offers.

Our mortgage calculator should help you understand everything. This helpful tool makes it easy to find mortgage loans and choose the best deal for you.

How to Use This Calculator:

Our mortgage calculator can help you understand how differences in interest rates and repayment terms affect the size of your monthly payment and the total cost of a home over time. Little information is required to get started. Adding a few more details using the calculator's optional advanced options can give you an even clearer idea of what your monthly mortgage payment might look like for different loans.

- House Price: This is the amount you pay the house seller. If you are in the early stages of home shopping, use the seller's asking price for comparison, but remember that this number is negotiable. If you are shopping in a highly competitive market and expect to be one of several bidders, you may want to bid above the asking price. In slower markets or for properties that have been on the market for a longer period of time, a bid below the asking price could be successful. Work with a real estate professional/ Mortgage Advisor to set your bidding strategy.

- Down Payment: When you enter the house price, the calculator automatically fills in the Down Payment field to reflect 20% of the house price. This is the standard down payment required for most traditional mortgages. Many mortgage lenders, including those who make government-backed loans, will accept lower down payments, usually in exchange for higher interest rates and/or fees - and with the stipulation that you pay for mortgage insurance, which you can factor into the calculator's advanced features.

- Term (in years): Enter the number of years required for the mortgage to be repaid. By default, this calculator assumes a 30-year mortgage, as this is the most common home loan term in America. Other standard mortgage terms include 15 years, 20 years, and 40 years. Adjust this number according to the offer you are evaluating. All things being equal, longer mortgage terms mean lower monthly payments, but also significantly higher interest costs over the life of the loan.

- Interest Rate: Enter the interest rate for the loan you are considering. Be sure to enter the interest rate, not the APR (annual percentage rate). These numbers may be similar, but the APR reflects interest costs plus additional financing costs like fees and mortgage insurance.

#mortgage#term#payments#downpayment#downpay#insurance#usa#united states#canada#advisor#mortgage adviser#financial advisers#calculator#calculations#california#year#loan#house#sale#service

186 notes

·

View notes

Text

Sorry, parents: The American dream is only for DINKS

Homebuyers with kids will likely spend 66% of their income on a mortgage and childcare this year.

Parents in Los Angeles and San Diego can expect to spend as much as 121% and 113%, respectively.

Some Californians have moved across the country to afford to buy a home.

Thinking about buying a home this year with kids already in the picture? Get ready to dig deep.

A recent study from Zillow found that potential homebuyers with children are likely to spend 66% of their income on mortgage payments and childcare expenses — an increase of nearly 50% from 2019.

The real-estate company estimated city- and state-level childcare costs from 2009 to 2022 for the typical American family with 1.94 children by analyzing data from the Women’s Bureau of the US Department of Labor and advocacy group Child Care Aware.

According to Zillow’s analysis, in 31 of the largest 50 US metropolitan areas with available childcare cost data, families looking to buy a home can expect to spend more than 60% of their income on mortgage and childcare costs.

Some areas are even costlier, with parents in cities like Los Angeles and San Diego needing to dedicate as much as 121% and 113%, respectively. (In those areas, the cost of buying a typical home and childcare is so big relative to the median income that Zillow's calculation results in figures over 100%.)

Zillow determined that a family earning a median household income of $6,640 per month can expect to allocate $1,984 of that to childcare. If the family purchased a house at a 6.61% interest rate — the rate in early January, when the US Department of Labor released its latest data on childcare costs — and made a 10% down payment, their monthly mortgage would amount to $1,973.

That leaves just $2,683 for additional expenses like food, transportation, and healthcare. This means many households with kids are financially strained; they're likely spending more than 30% of their income on housing, well above what experts recommend.

It all adds up to a costly reality that's making the American dream of homeownership seem farther out of reach for parents than ever before.

Parents can blame a yearslong battle with inflation, as well as stubbornly high home prices and mortgage rates, for contributing to their predicament.

Based on the study, a new buyer household in the United States, making the median income, would spend 30% of it on housing. It's paying for childcare, then, that adds so much on top of the housing budget.

The upshot: Another group, less encumbered financially, appears better poised to realize the dream of homeownership: "DINKS," an acronym that stands for "dual income, no kids."

Some child-free DINKS — who boast a median net worth above $200,000 according to the Federal Reserve's Survey of Consumer Finances — devote their disposable income to luxuries like boats and expensive cars.

Without the financial obligations of raising children, such as covering medical expenses or enrolling them in daycare or private school, DINKS can save thousands of dollars a year and build greater long-term wealth.

Some DINKS use their savings to finance vacations and travel the world, like Elizabeth Johnson and her husband, who, over the past couple of years, have hiked in the Swiss Alps, snorkeled in Hawaii, and enjoyed leaf peeping in Canada.

"We hang out with other people's kids every once in a while," Johnson previously told Business Insider's Bartie Scott and Juliana Kaplan, "but then we happily just give them back to their parents."

Some Americans with kids move to places where their money goes further

One solution to the high cost of both buying a home and raising a family?

Move.

In recent years, young Americans in higher-cost states have decided to move to places that offer them a cheaper cost of living.

Janelle Crossan moved to New Braunfels, Texas, from Costa Mesa, California, in 2020 following a divorce.

She was able to become a first-time homebuyer and found a safe community to raise her son.

"I paid $1,750 for rent in a crappy little apartment in California," Crossan told BI earlier this year. "Now, three years later, my whole payment, including mortgage and property taxes, is $1,800 a month for my three-bedroom house."

Pengyu Cheng, a program manager for a tech company, told BI in 2023 that moving from California to Texas allowed him and his wife to afford their first home, giving them the confidence and security to have their first child.

"Living in California has always been expensive," Cheng said. "I knew that when my wife and I eventually expanded our family, we wouldn't be able to afford San Francisco or the Bay Area in general — even though we both earn good salaries."

7 notes

·

View notes

Text

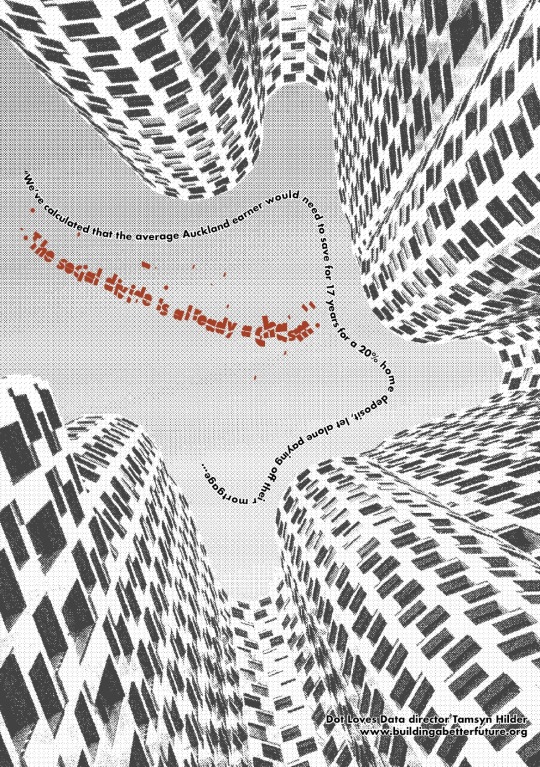

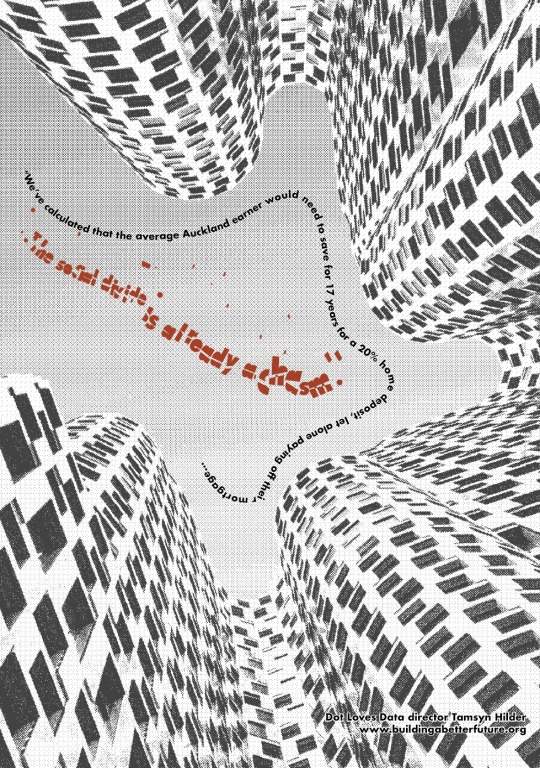

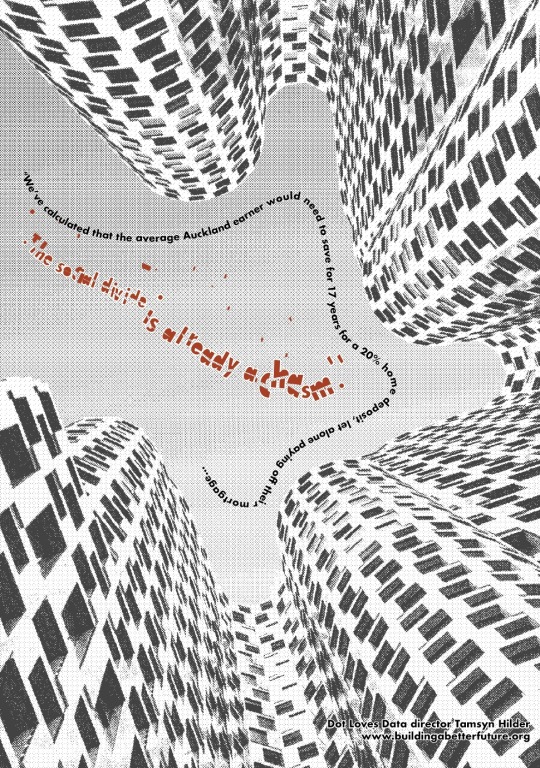

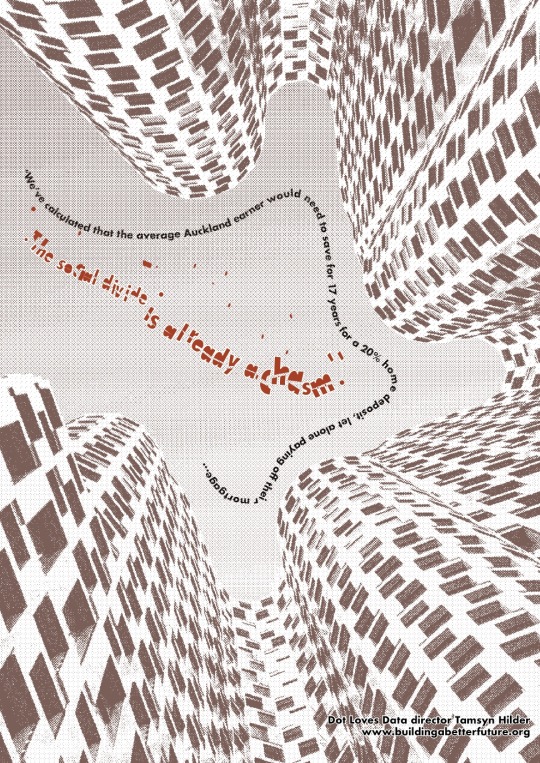

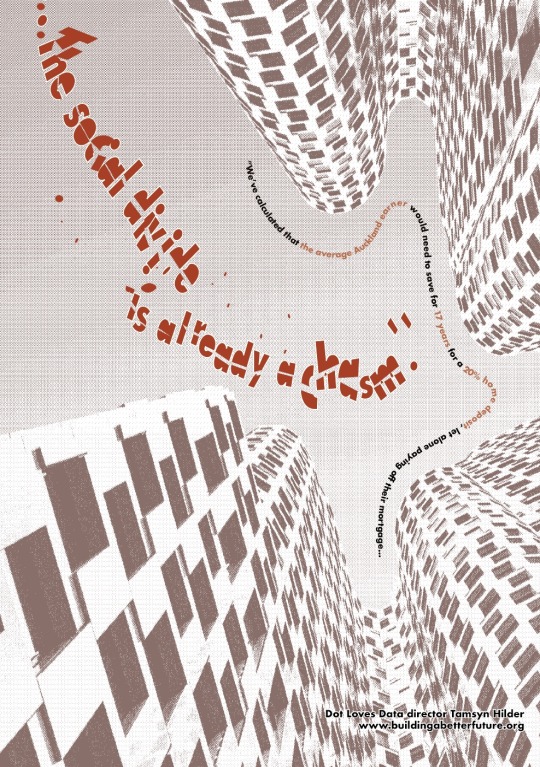

Political Statement Poster Experiments Continued:

I worked with creating a different version of my initial minimal styled political poster design.

For these experiments I worked with changing the scale of background to text, shifted the layout and placement of the text, and colour of the background and the text. I really like where it ended up creatively (the last image). It's not as clean, and is jarring, but still modern which is a statement about the issue being a modern problem.

The main text is centred, though it's broken up and non linear, to create a vibe of something jolting, and unexpected, and mimicking the social 'chasm' that we are discussing as the central theme of the poster. The text is falling, in bold red, to project the the alarm and tension of the statement, and broken system/political processes that are currently in place. The idea is to pull the eye to the focus of the statement "...The social divide is already a chasm." and then the eye flows to the context/details/explanation of the statement in the smaller font. I've tinted the most important words to help create a subtle emphasis that doesn't conflict with the main headline or focal point. It is in the same tone and colour family as the composition, but you'll only read it second, if that makes sense.

The background gives us a sense of scale, to make us feel small by the sheer height of the building towering above. Also, the tone & texture of the background is meant to remind us of something from a black & white newspaper clipping, so that it implies that the topic is both old news (from an old newspaper), while also being a current news headline too.

Typeface: Futura Bold : I've kept the typeface the same throughout so that the design isn't messy, especially since I've got lots of flowy lines and cut up text going on.

I picked Futura bold, because it is clean, simple, clear, and geometric, which flows well with the abstract forms in the poster. This typeface is determined, striking, timeless, ambitious and respectful while also representing the eras of Modernism & Industrialisation, which speaks to the current Auckland housing crisis that I'm looking to highlight here.

The name of the typeface itself is important as well "FUTURA" which speaks to 'hope for the future'.

***

Here is the original quote for your reference:

We’ve calculated that the average Auckland earner would need to save for 17 years for a 20% home deposit, let alone paying off their mortgage. The social divide is already a chasm.”

Dot Loves Data director Tamsyn Hilder

from: buildingabetterfuture.org.nz/delivering_adequate_housing_and_our_infrastructure_needs_for_the_21st_century

3 notes

·

View notes

Text

ELI5: The Silicon Valley Bank Collapse

TL:DR SVB made a somewhat risky investment which went poorly in changing market conditions, and didn’t have the money to pay back their depositors. The FDIC has decided to fund the remaining bank accounts, but shareholders will realize a total loss on their stock.

If you haven’t been following the news, the second biggest bank collapse in American history just happened. But you probably have no idea what that means, so I’m going to explain it all in simple terms, with no frills, no biases, and no opinions.

Please let me know if I get anything wrong here. While I do work in finance, I’ve heard conflicting sources on some of the events.

The Basics of How Banks Work

Left to their own devices, people ordinarily wouldn’t just give their wealth to someone else for safekeeping. But these days there are many incentives for the average person to lend their money to a bank. Yes, there’s the matter of security (robbers can steal physical tender, such as physical bills and valuables), but there is also interest. By lending your money to a bank (like a loan!), the bank then uses your balance to invest in the stock market or major projects such as other peoples’ mortgages, with the promise that all of the money you’ve placed with them will be returned to you when you ask... with a little bit extra as interest. That’s your incentive for placing your money with them.

The point is, you placed your money with a bank, and in exchange for you lending them your money, they’ve promised to give it back to you when you ask, with a little bit extra. That’s important to understanding the next topic.

Investments, Reserves, and Insolvency

Okay, but how do banks generate the “little bit extra” that they promised to give you in exchange for borrowing your money? Through investments!

Investments can be a lot of things. Mortgages are investments- a bank can lend someone a big chunk of money, and in exchange the bank receives cash monthly that ends up being worth more than they loaned out. They can be investments into the stock market- buying stocks at low price, watching the price rise, and selling them high is a way to net profit. There are other types of investments too, like bonds (mini loans), CDs (low risk, long-term investments that guarantee profits that bank customers can take out), and options (very complicated). What they have in common is that you lend your money, and hopefully get more back (though there’s some risk of loss).

As an example, let’s pretend you’ve put $20,000 in a bank account. The bank could then take $10,000 and put it into a risk-free investment that returns at 2%. One year later, the return is $10,200, at least $10,000 of which must return to you. The bank may take $100 of that as their own profit and return the remaining $10,100 to your account- the remaining $100 is your interest. (This is a theoretical example. My own bank account hasn’t generated nearly that much in interest.)

But let’s say the investment isn’t risk-free. They’ve taken $10,000 of your money, invested in that 2% return project, and it flopped. Ouch. Now they’re out $10,000- of your money! That doesn’t seem fair!

That’s why banks have reserves. It’s a buffer/stockpile of cash or liquid assets (things that can be converted to cash really quickly) that covers a depositor’s finances should the bank’s own investments go south, OR if people need to pull out their money. Banks usually have a dedicated team of analysts that calculate the amount of reserves a bank can safely set aside to cover these sorts of events. This covers souring investments as well as times when a big customer is planning to pull out a ton of savings. That $10,000 is a drop in the bucket for them, but something like $1 million is more concerning.

So, even if the investment goes south, at least you’ve still got that guaranteed $20,000 on demand in case of, say, a medical emergency.

... At least, that’s how it should work.

If a bank doesn’t have enough reserves/quick money to fulfill its obligations of money on demand to everyone who lent it to them, it becomes insolvent- basically bankrupt unless they do a lot of stuff to get money fast really quickly. This can involve pulling money out of investments (which costs money to do, and is not something any investor would want to do unless they need a lot of money really really fast). This is the worst case scenario for any financial institution and one they want to prevent at all costs.

Understandably, the insolvency of the bank you’re keeping your money at is a terrifying situation for people who really need that money. And it was a common situation up until the 1930′s.

Bank Runs

You probably know someone who lived through the Great Depression who has a large stockpile of cash and refuses to use credit cards or banks. Some people probably even call them stupid for doing so. I’m not going to call your money hoarding grandparents stupid, since they’re operating off a very real fear- the fear that a bank won’t have the legal tender to give them their money when they ask. That situation was VERY COMMON before the FDIC was created in 1933 to insure the deposits of its member banks.

What would happen is that you’d hear that some news about how a certain bank was having financial trouble, and might close very, very soon. You freak out and realize that if they close, you’ve given your money to them, and now you’re not going to get it back! You go to a branch of the bank to withdraw all of your money, only to find that everyone else had the same thoughts as you, and the branch is already out of physical tender. As more and more people realize they’re about to lose all of their savings, the bank is drained at an exponentially increasing rate- and soon, the bank has become insolvent.

Banks have defenses for this- suspending withdrawals, limiting withdrawals, and asking their central bank for more liquid funds. But in the case of a bank run, or a bank panic, which is a bunch of banks experiencing bank runs at once, those defenses might fail entirely.

The FDIC, an American Government Corporation, was created as an insurance company for banks. Basically, banks pay dues to the FDIC, and in the case of the bank’s insolvency, the FDIC guarantees deposits up to about $250,000. It was created partially as a way to avoid future bank runs and protect consumers in the case of a bank collapse.

Interest Rates and Inflation

You’ve probably heard about the Federal Reserve hiking interest rates or keeping them low throughout the recent pandemic, but what does that actually mean, and why is it relevant here?

The Federal Reserve sets target interest rates- basically, setting the price at which major banks can borrow from the government. This ends up forming the basis for other types of loans you can get from banks- mortgages, car loans, etc.. Periodically these are revised with regards to economic conditions.

Basically, raising interest rates is used to encourage people to STOP borrowing money and START lending money- the return for lending is higher, and the price of borrowing is higher. Lowering interest rates is used to encourage people to START borrowing money and STOP lending money- the return for lending is lower, and the price of borrowing is lower.

(This is why you always want a loan with a low interest rate, btw!)

(And keep in mind that these are with regards to major economic decisions, and not necessarily the types of loans an ordinary person would get.)

Now, why is inflation relevant? Yes, it’s really high right now, and that means that the prices of everything are increasing a lot! The Federal Reserve’s answer to that is to increase interest rates- by making it more costly to borrow money, they’re hoping to stop an unsustainable level of price increases in everything else.

I think I get it. Now what’s going on?

Silicon Valley Bank was a fast-growing bank that, in recent years, held a lot of funds for entrepreneurs and tech startups- about 50% of all venture capital money in the US! What this means is a. a lot of large accounts in b. mainly one sector of the economy (technology).

That being said, the bank would most certainly not outpace inflation if they didn’t invest it. However, at the time, they couldn’t find any places they could loan money to.

Furthermore, the tech/crypto/startup sector of the economy has been going through hard times for a while. Many needed to slowly pull out funds from the bank, further straining the amount of liquid cash on hand.

In 2021, SVB instead decided to invest in mortgage-backed securities with the deposits placed with them. Mortgages are basically very long loans, but they can also be very risky. Mortgage-backed securities are based on mortgages. (The risk surrounding mortgage-backed securities is one reason for the housing crisis of 2008.) It should also be noted that they’re very susceptible to changes in interest rates- if interest rates increase, mortgage-backed securities lose their value.

In 2022, we got severe inflation.

And then, the Federal Reserve’s answer to severe inflation: raising interest rates.

And the mortgage-backed securities that SVB took out became unprofitable!

Now remember how I said that banks need to be able to not only provide customers their deposits on demand, but also give it back with interest? Because the investment in mortgage-backed securities failed, SVB didn’t have money for interest OR deposits, and not enough in reserves to fill the gap. They would be insolvent, if they didn’t come up with a lot of money really, really fast.

Word spread fast- depositors had already realized that the bank had become insolvent, and they demanded their deposits back. In other words, SVB went through a bank run, losing their money over the course of three days.

The FDIC then stepped in. Now this is a bit of an unusual case, because the FDIC only insures accounts up to $250,000. Most venture capital startups have accounts that are many times that. However, the FDIC has decided (with their own member deposits, not taxpayer money) that all of the venture capital money will be paid. All of the bankers will get their deposits back.

SVB is still closing, however, and shareholders and stockholders will not be compensated for the stock loss.

So while shareholders lose out, every creditor/depositor who invested will be getting their money back. As for Silicon Valley Bank, it’s being administered by the FDIC up until it’s time for it to close down.

#silicon valley bank#eli5#economics#finance#the more you know!#life as an aj#okay what other tags should i put in here#please reblog if you found this informative i worked VERY hard on it!#this is 1.8k words

10 notes

·

View notes

Photo

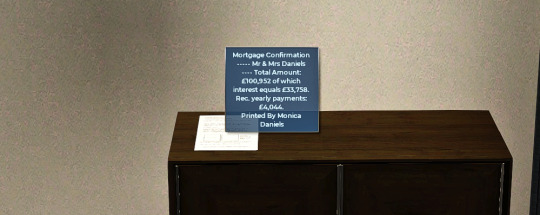

Daniels Family - Round 4

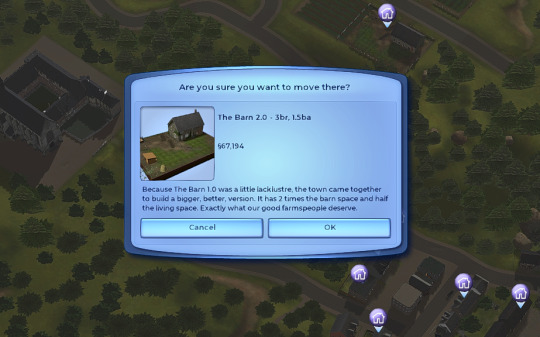

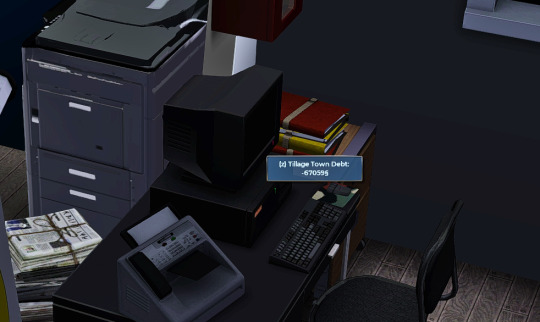

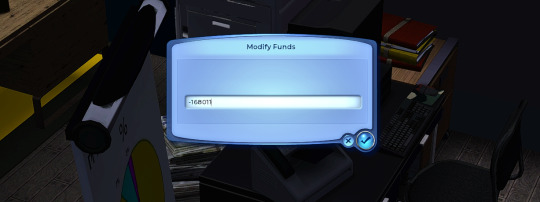

Not too far away from their current house, the city had just finished developing a new farming space. It seemed the council had come to a unanimous decision to relegate all the farmland to the same street and so The Barn 2.0 was built across the road from our Supermarket owners, the Cleggs.

Because I suddenly couldn’t use a calculator properly, the Daniel’s took out a mortgage, sold their old house and closed the deal on the property right away.

The fun financial stuff:

Since all the money my sims receive for loans must come from the town fund, and there wasn’t enough money in the town fund for their mortgage, the loaned money was added to the Tillage Town Debt. Of course, once the Daniels pay back their mortgage, with interest, the town will recover the money.

Hopefully I’ll be able to make things even more convoluted in the future once I have sims working in the lawyer and banking careers :)

#ts3#queued#sims 3#tillage#daniels family#sims 3 gameplay#sims 3 screenshots#sims 3 rotational play#sims 3 legacy#sims 3 family#ts3 simblr#simblr

44 notes

·

View notes

Text

Empowering Financial Decisions with Modern Calculators: Your Key to Financial Success

In an era where information is readily available, financial empowerment is key to making informed decisions. Thanks to the digital age, we have access to an impressive array of calculators that can simplify complex financial tasks. Let's explore the world of Modern Calculators and discover how these tools can empower you in various aspects of your financial journey.

1. Rectangle Body Shape Calculator

Your body shape plays a significant role in fashion choices. The Rectangle Body Shape Calculator not only identifies your body shape but also offers tailored fashion advice to help you look and feel your best.

2. Pear Body Shape Calculator

Enhance your style by understanding your body shape. The Pear Body Shape Calculator provides insights and fashion tips specifically designed for pear-shaped individuals.

3. Triangle Body Shape Calculator

Confidence in your wardrobe starts with knowing your body shape. The Triangle Body Shape Calculator identifies your body type and offers fashion recommendations to elevate your style.

4. Car Payment Calculator GA

Planning to buy a car in Georgia? The Car Payment Calculator GA simplifies the process by helping you estimate your monthly car payments, ensuring they fit comfortably within your budget.

5. Mobile Home Mortgage Calculator

Homeownership is a dream for many, and mobile homes provide an affordable path. The Mobile Home Mortgage Calculator assists in estimating your monthly mortgage payments, making homeownership more achievable.

6. Car Payment Calculator Illinois, Colorado, Virginia

If you're relocating to Illinois, Colorado, or Virginia, this calculator helps you estimate car payments in different states, ensuring your budget aligns with your new location.

7. Car Payment Calculator AZ

Considering a vehicle purchase in Arizona? The Car Payment Calculator AZ enables you to calculate potential car payments, allowing you to budget effectively.

8. FintechZoom Mortgage Calculator

Mortgages can be complex, but the FintechZoom Mortgage Calculator simplifies the process. Calculate mortgage payments, explore interest rates, and understand your amortization schedule with ease.

9. Construction Loan Calculator

Building your dream home? The Construction Loan Calculator estimates your construction loan requirements and monthly payments, ensuring a smooth building process.

10. Aerobic Capacity Calculator

Your fitness journey starts with understanding your aerobic capacity. Calculate your fitness level and tailor your workouts for optimal results using this essential tool.

11. Aircraft Loan Calculator - Airplane Loan Calculator

For aviation enthusiasts, owning an aircraft is a dream come true. The Aircraft Loan Calculator simplifies the financial side of aviation, helping you understand loan terms and payments.

12. Manufactured Home Loan Calculator

Thinking about a manufactured home? This calculator provides invaluable insights into potential loan payments, making homeownership in a manufactured home more achievable.

13. Classic Car Loan Calculator

Passionate about classic cars? The Classic Car Loan Calculator helps estimate classic car loan payments, bringing you closer to your dream vehicle.

14. FintechZoom Loan Calculator

Whether you need a personal or business loan, the FintechZoom Loan Calculator equips you to estimate monthly payments and assess the financial impact of borrowing.

15. ATV Loan Calculator

Ready for off-road adventures? The ATV Loan Calculator calculates potential ATV loan payments, ensuring your outdoor escapades are within reach.

16. Farm Loan Calculator

Aspiring farmers can benefit from the Farm Loan Calculator. It simplifies estimating loan payments and planning expenses for a successful agricultural venture.

17. Pool Loan Calculator

Turn your backyard into a paradise with a pool. The Pool Loan Calculator helps you understand the cost of financing your dream pool, making planning easy.

18. Solar Loan Calculator

Considering solar energy? Calculate the financial impact of a solar energy system on your budget and savings with the Solar Loan Calculator, helping you make eco-friendly choices.

19. Mobile Home Loan Calculator

Contemplating a mobile home purchase? Estimate potential mobile home loan payments to make an informed decision about your future home.

20. Bridge Loan Calculator - Bridging Loan Calculator

Real estate investors often use bridge loans for flexibility. The Bridge Loan Calculator simplifies the process of evaluating your bridge loan requirements, facilitating smarter investment decisions.

21. Hard Money Loan Calculator

Hard money lending can be a viable financing option. Use this calculator to assess potential hard money loan terms and payments, ensuring you make sound financial choices.

22. HDFC SIP Calculator

Systematic Investment Plans (SIPs) are an excellent way to grow your wealth. The HDFC SIP Calculator helps plan your investments and understand potential returns on your SIP portfolio.

23. Step Up SIP Calculator

Planning to increase your SIP investments gradually? The Step Up SIP Calculator allows you to calculate the benefits of incremental investment increases on your wealth accumulation.

24. What Calculators Are Allowed on The ACT

For students preparing for the ACT, understanding which calculators are permitted during the exam is crucial. This article provides valuable insights into the types of calculators allowed, ensuring you're well-prepared for test day.

In conclusion, Modern Calculators offers a wide range of calculators that simplify complex tasks and empower you to make informed decisions in various aspects of your life. These calculators are your tools for financial empowerment, helping you achieve your goals and secure your financial future. Explore them today and embark on your journey to financial success!

#Rectangle Body Shape#Pear Body shape#Triangle Body Shape#Car Payment Calculator GA#Mobile Home Mortgage Calculator#Car Payment Calculator Illinois#Colorado#Virginia#Car Payment Calculator AZ#FintechZoom Mortgage Calculator#Construction Loan Calculator#Aerobic Capacity Calculator#Aircraft Loan Calculator - Airplane Loan Calculator#Manufactured Home Loan Calculator#Classic Car Loan Calculator#FintechZoom Loan Calculator#ATV Loan Calculator#Farm Loan Calculator#Pool Loan Calculator#Solar Loan Calculator#Mobile Home Loan Calculator#Bridge Loan Calculator - Bridging Loan Calculator#Hard Money Loan Calculator#HDFC SIP Calculator#Step Up SIP Calculator

2 notes

·

View notes

Text

The queue forms early outside Norwich’s Citizens Advice. Right next door another other long line waits for the library to open. Queueing for books? Maybe, but mainly for a warm place to spend the day, a member of Citizens Advice staff tells me. They aren’t street homeless but neatly dressed people from cold homes.

This branch of Citizens Advice is only open for two hours on weekday mornings, as it can’t cope with any more clients for its volunteers to triage. Appointments are fully booked for the next two weeks and sometimes desperation explodes. On this day, the advice coordinator, Trudie Gibbons, has to ask a man to leave. He had been yelling, “You’re not giving me any advice!” but she talks him down with what she calls “zero tolerance but great understanding” from her 20 years’ experience. One man arrived with a sharpened stake the other day.

“We are just about the only face-to-face service left,” she says. “Everything else is online, or a phone line that never answers, no humans to talk to.” And so some vent their frustration here. Most people arriving are awkward, never having needed help before; they never expected this devastation of unpayable bills, soaring debt, bare cupboards. Gibbons gives out six food bank vouchers in the first hour to deeply embarrassed clients. “They don’t quite know how to phrase asking for food,” she says.

Staff who have worked here for years, alongside admirable volunteers, say that they have never seen anything like this. They are well accustomed to advising people in trouble, but it’s hard to capture their sense of shock at what’s happening now. People I meet on the frontline in all kinds of services are lost for new ways to describe the scale of this tsunami crashing in not just on the already poor, but on middling households impoverished overnight. “Cost of living crisis” sounds too tame, too polite to capture the brutal fear of losing homes and everything. Martin Lewis, the wise money-saving expert, saw this arriving early on, admitting earlier this year that he was “virtually out of tools” to help people now. Are Tory MPs hearing all this in their surgeries? Perhaps few still expect any help from them.

It’s no wonder that specialist debt adviser Marcel Cheek echoes Lewis’s words to me. After 22 years, he is used to getting people’s debts delayed or cancelled, maybe with a debt relief order. He makes personal “better off” calculations that tot up outgoings and incomings to get people back on their feet. Cancel that Sky subscription, but not the pet food or wifi. Apply for that benefit they never knew was there. “But this is quite different,” he says, this sudden rise in energy bills, food costs and rent or mortgage payments. “When I’ve done all that,” he says, “people in ordinary jobs find they have a deficit budget I can’t fix. I’ve never seen that before.”

How many people is he talking about? He keeps figures carefully: he finds 48% of those they see here now have less coming in than they can live on – so debts will start mounting again as soon as they’re cleared. What will happen, I ask. “I don’t know,” he says. “I really don’t know.” His father was a debt adviser for 30 years before him; there has never been a surge like this. At Citizens Advice’s head office, Morgan Wild, the head of policy, confirms the unprecedented nature of the problem: “Debts I’ve never seen before. We’re handing out more food vouchers in a couple of months than in the last five years combined.” The Trussell Trust, the food bank charity, warns of emptying crates and low supplies. This emergency is what the rising groundswell of strikes is about.

As they help to navigate the nightmare maze of benefits, advisers tell working clients to claim even if they’re only entitled to £5 in universal credit, as at least that then qualifies them for other benefits: a cost of living bonus, housing benefit, council tax reduction and others. Absurdly, it can be worth earning £5 less to qualify, which is why, I’m told, the Department for Work and Pensions (DWP) work coaches are increasingly told to pressure claimants to earn more – although they will then lose 55p in universal credit for every extra pound they earn. It’s effectively a 55% tax rate on extra earnings: if that’s OK for them, why not for the richest in society?

As for personal independence payments for disability, almost half are refused at first; yet the benefit is so badly administered that 70% of those who appeal to a tribunal are successful. But the backlog of claims means waiting, in dire hardship, for six months for your appeal to go through. I speak to a woman whose payments had been cut when she went into hospital for a cancer operation, but she couldn’t get them restored when she came out. “They were so rude on the phone. I’m treated like crap!” she explodes.

A man comes in to Citizens Advice whose payments were stopped when he was “sanctioned” by the DWP. He says he has no food, no phone and no electricity from his prepay meter, and is left in the cold and dark. All benefits were stopped when his online claim asked him to “verify his identity”, but he couldn’t as his phone had run out of credit. All claims are made online, and many claimants have no means of getting online besides their phone. He’d waited days, cold and hungry and in the dark, before summoning the courage to come here.

Every week, another avalanche of reports tells this story: the Office for National Statistics last week showed that 58% of people in England’s most deprived districts were spending less on food and essentials (in the least deprived areas, it’s a third). With the worst wage growth in 200 years, one in five children in key worker households are brought up below the poverty line. In a country growing rapidly poorer, its services logjammed by austerity and staff pay cuts, child poverty gallops ahead, with reports of low-paid school support staff paying from their own pockets for hungry children’s food and uniforms. The Financial Times calls this “the steepest fall in living standards on record”, with the UK the worst performer in the G20 (bar Russia). The former prime minister Gordon Brown, who did much in power to ease poverty, produces new figures showing millions are spending a third of their income on energy bills. That’s unaffordable. Lewis confirms what Citizens Advice sees: “You could put me into one of those households and do every trick in the book and I wouldn’t even get close to scratching the sides of what is needed.”

Ministers tour TV studios to say that raising strikers’ pay is “unaffordable”. But a country affords what it prioritises. George Osborne deceitfully spoke of us all being “all in it together”, but it’s a civic sentiment still to be called on in a national emergency. After remarkable passivity over years of falling wages, strikes are inevitable to reverse decades of money draining from pay packets up into grossly accumulating capital wealth. The Citizens Advice Bureau in Norwich, and branches everywhere else, can do little to resolve a nationwide crisis of working people earning less than they can survive on.

10 notes

·

View notes

Text

A perfect storm for evictions is forming all around us. A new report reveals that rents are rising four times faster than incomes in the United States. In recent years, the rate of rent price growth has tripled, making housing increasingly unaffordable for millions of Americans. For some households, it now takes more than three full-time workers to afford the typical two-bedroom rental.

Researchers found that in many areas, rent prices shot up over 200%, and are likely to continue to rise in 2023. This means that many struggling U.S. families are about to lose their homes as they fall behind payments, and evictions start to pile up all across the country. That’s what we’re going to break to you in today’s video.

Over the past three years, home prices jumped by almost 47%, and today, they remain about 38% more expensive than they were in 2019. Higher mortgages are also pricing many would-be homeowners out of the market. As a result, demand for rents is soaring, and a shortage of affordable rental units is creating a perfect storm for evictions, experts say.

Right now, rental vacancy rates are at the lowest level since 1984, which is giving landlords, especially corporate landlords, much more power to mark up prices for a limited number of available units. On the other hand, we all know by now that wages aren’t keeping pace with rising rents in the U.S.

In point of fact, wages aren’t keeping pace with anything these days, and 58% of renters are currently living paycheck to paycheck. About the same rate, or 57% to be precise, are now paying more than 30% of their income on rent.

In cities with minimum wages above $7.25, it takes an average of 2.5 full-time minimum wage workers to make the typical two-bedroom rental affordable, meaning renters would spend no more than a third of their income on rent. In cities with a $7.25 minimum wage, it takes an average of 3.5 full-time workers to meet this threshold. “Income disparity does really play a big role and impact the affordability outlook for a lot of renters,” Chen added.

With 90% of ingredients in pharmaceuticals coming from Communist China, the risk of a medical supply chain crisis has never been greater. Secure five types of antibiotics to have ready when you need. Use promo code “Rucker10” for $10 off.

From 1985 to 2022, the national median rent price rose 151%, while overall income grew just 35%. That’s to say, the average rent rose over 4 times faster than wages. Overall, the cost of living in the U.S. increased by 89% since the mid-1980s, according to the firm’s calculations. In other words, Americans have experienced a steep decline in their purchasing power across the last four decades, and they have been forced to move to cheaper, subpar units or spend significantly more of their earnings on rent.

We’re going to see cases of evictions reaching crisis levels in the months ahead, especially as big companies start to layoff their workers en masse. Many renters are hanging by a thread at this point, and as the economic downturn that is now unfolding all around us accelerates, millions of U.S. households will be pushed over the edge.

3 notes

·

View notes

Text

FinThink - Financial Technology

FinThink Research will Launch by covering 20 Crypto Projects, 20 NFT Reports, and 30 Equity Reports. Covering a total of 70 profiles and updating them every quarter.

Surveillance reports will be released throughout the quarter covering news releases to keep members up to date on relevant macro events.

FinThink AI is a suite of Machine Learning Applications that will:

Forecast Stock Prices.

Provide market sentiment per individual stock or the overall stock market.

Provide Search Trends Corellated with price movements.

Risk Management forecasting Maximum Loss at a 95% and 99% probability level.

Trading Entry and Exit Points using our Trading Algorithm.

FinThink is a Financial Technology Company Headquartered in New York City.

Finthink AI is a Financial Technology Product

FinThink Finance Tools will consist of a Mortgage Calculator, a Car Buying Calculator, and a Real Estate Portfolio Building Calculator. Close every Mortgage confidently and never leave the car dealership feeling that you were taken advantage of. Learn how to build a Real Estate portfolio and build financial freedom.

FinThink Members can achieve Financial Freedom for $50 a month.

FinThink is Financial Technology.

Financial Technology is the Future of Finance.

Check out the Future of Finance at:

www.finthink.com

2 notes

·

View notes

Text

First Time Home Buyer Pros

At First Time Home Buyer Pros, we understand how daunting it can be to take the first step towards buying a home. As experts in providing Home Loans, Mortgages and assisting with FHA Loans for FTHBs in Temecula, CA, our team of Loan Officers and Real Estate Agents are here to help guide you through the process. Our mission is to make your journey as smooth as possible by offering tailored advice based on your situation and needs. We pride ourselves on our deep knowledge of the market in Temecula, CA, enabling us to guide you on what type of loan would best suit you while also helping negotiate the best price for your new home purchase. With years of experience under our belts and a passion for helping people achieve their homeownership goals, trust us to be there every step, from finding that perfect property until signing those final papers.

At First Time Home Buyer Pros, we pride ourselves on being a trusted resource for individuals in the Temecula, CA area interested in purchasing their first home. Buying a home can be an overwhelming and confusing process, especially for those who have never gone through it before. That's where we come in - our team of Loan Officers and Real Estate Agents is dedicated to providing personalized guidance to help you find your dream home.

We offer services tailored specifically to our client's needs as FTHBs in Temecula, including assistance finding suitable loan options, such as FHA loans or other mortgages that fit individual situations. Our experts are here to walk each step of the journey with you, from calculating what type of costs will be involved upfront (down payment, etc.) to all necessary paperwork submissions like getting pre-qualified for financing to negotiating better homes they desire.

We believe everyone deserves the chance to own their real estate and build wealth over time through homeownership. With free service consultations at every appointment provided by expert agents that also specialize solely towards serving people looking into buying homes using different forms, which include FHA Loans or traditional mortgages, we're able to share relevant information about neighborhoods within this community so prospective buyers feel confident enough not just when making offers but negotiations too!

Contact Us:

First Time Home Buyer Pros

32209 Camino Herencia Temecula CA 92592

+1 949-357-5029

[email protected]

http://fthbpros.com/

2 notes

·

View notes

Last Seen Blogs

siehen

A scientist in the fandom

noelssluttt

Yapper

poisonpearls

$lackin

lemon-squeeze

Sometimes Brutal,

Always the Truth

plasticwebs

Plastic Webs