#employer fsa contributions

Text

4 Benefits of Group Health Insurance

When you get employer-sponsored healthcare through your job, you're likely signing up for group insurance. These plans provide coverage to several members of an organization. Typically, 70 percent of a company's workforce must participate for the group plan to remain valid.

Fortunately, getting 70 percent of employees to opt-in isn't a problem for most organizations. Around 50 percent of all Americans are part of a group health insurance plan. When you look at the benefits this type of insurance provides, it's not hard to see why.

Lower Premiums

The biggest perk of having group insurance is that you can enjoy lower premiums. Health insurance is one of the most significant employer perks available. With healthcare costs increasing, many people turn to employer-sponsored plans to reduce costs.

Typically, beneficiaries split premium costs with employers. Companies offering group insurance plans get favorable tax benefits, incentivizing them to provide great plan options. Therefore, the arrangement is mutually beneficial, making healthcare coverage far more affordable for employees than individual plans.

Extended Coverage for Family

Group insurance doesn't just apply to the employee. Many plans provide the option to extend coverage to dependents. That means employees and their entire families get affordable healthcare coverage.

Broader Networks

One lesser-known benefit of group insurance is broader coverage. When you get individual insurance, you may have a small network of providers to choose from when getting medical care. That's not the case with group plans.

The networks are large, giving you more options and possibly providing coverage when traveling to other states.

Reduced Overall Costs

We already know that group insurance results in lower premiums. However, it doesn't stop there. The entire insurance package tends to be more affordable when it applies to a larger group of individuals versus one person.

From an insurer's perspective, group plans are better for risk management. The risks spread across a pool of insured employees. Insurance companies know more about who they're covering, making assessing risk and controlling costs easier. The result is more affordable coverage without sacrificing network size or quality of benefits.

Read a similar article about HDHP here at this page.

#consolidated omnibus budget reconciliation act#how to reduce employer healthcare costs#integrated hra#group health insurance#dependent care fsa#hsa contribution limit#hsa savings account

0 notes

Text

Tax Strategy: Maximizing Savings and Minimizing Liability

Developing a solid tax strategy is critical for individuals and businesses alike. It involves analyzing and planning various financial decisions to optimize tax savings while ensuring compliance with tax laws. A well-designed tax strategy not only minimizes tax liability but also allows individuals and businesses to allocate resources more efficiently. In this article here, we will explore some essential elements of an effective tax strategy.

Understand the Tax Code

One of the first steps in formulating a tax strategy is to gain a comprehensive understanding of the tax code. Tax laws are complex and subject to constant updates and changes. Staying well-informed about current regulations and potential tax deductions or credits is crucial. This knowledge enables individuals and businesses to identify opportunities for tax savings and optimize their financial decisions accordingly.

Keep Well-documented Records

Maintaining accurate and organized financial records is essential for effective tax planning. Documenting expenses, income, investments, and other financial transactions provides the necessary evidence to claim deductions and credits. Good record-keeping also helps in the case of an audit. By establishing a robust record-keeping system, individuals and businesses can ensure they are claiming all eligible tax breaks and avoid any penalties for non-compliance.

Utilize Tax Advantaged Accounts

Maximizing the use of tax-advantaged accounts is a smart strategy to reduce tax liability. For individuals, contributing to retirement accounts such as 401(k)s or IRAs can reduce taxable income and provide long-term tax savings. Similarly, businesses can take advantage of various tax-advantaged accounts like Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), or Dependent Care FSAs to lower their taxable income and provide benefits to their employees. Please discover more about this post here.

Explore Deductions, Credits, and Incentives

The tax code includes numerous deductions, credits, and incentives that can significantly reduce tax liability. Understanding and utilizing these tax breaks is a fundamental part of an effective tax strategy. Deductions such as mortgage interest, student loan interest, medical expenses, or business expenses can lower taxable income. Tax credits, like the Child Tax Credit, Earned Income Tax Credit, or energy-related credits, offer a dollar-for-dollar reduction in tax liability. Additionally, businesses can benefit from various incentives like research and development credits, investment credits, or employment-related credits.

Conclusion

A well-executed tax strategy can provide substantial benefits by minimizing tax liability and maximizing savings. By understanding the tax code, keeping meticulous records, utilizing tax-advantaged accounts, and exploring deductions, credits, and incentives, individuals and businesses can make informed financial decisions and ensure compliance while optimizing tax savings. Remember, it is always a good idea to consult a tax professional or accountant to help develop and implement a tax strategy tailored to your specific situation. If you probably want to get more info about the post then, click here: https://en.wikipedia.org/wiki/Tax.

2 notes

·

View notes

Note

What’s your advice for girls in their twenties? What do you wish somebody told you?//

Adding on to health insurance: know how your insurance works. Learn about your copay, your deductible, your percentage of coinsurance after meeting your deductible. Learn about HSA and FSA plans and employer contributions.

Don’t pick the cheapest insurance. Usually employers offer a very cheap option with limited benefits. And you’ll be tempted because you’ll tell yourself you aren’t sick ever or rarely see your doctor. But if something major does happen, you’re stuck with that bill. Insurance means the difference between a 3,000 bill vs a 30,000 bill. I wish I was exaggerating.

Don’t skip your annuals. Cervical and ovarian cancer are the leading cause of death in women but are so treatable if detected early enough. This I cannot stress enough because I started needing paps every 3 months for years and have had more biopsies than anyone ever should. But I stopped the cancer.

Last: be your own advocate. Doctors will gloss over your health stating that it’s a comorbidity due to obesity, etc. You know your body. If something isn’t right, you keep going to doctors until you find one that listens. That could be the difference between life and death.

And yet more great advice!

13 notes

·

View notes

Text

Maximizing Tax Deductions: Strategies for Individuals and Small Businesses

In the realm of taxes, deductions serve as potent tools for individuals and small businesses alike to reduce their taxable income, ultimately lowering their tax liabilities. Whether you're a freelancer navigating the gig economy or a small business owner striving for fiscal efficiency, understanding and leveraging tax deductions can significantly impact your bottom line. In this comprehensive guide, we'll delve into the strategies and tactics for maximizing tax deductions, empowering you to optimize your tax planning and minimize your tax burden.

Understanding Tax Deductions

Before delving into strategies, it's essential to grasp the concept of tax deductions. Tax deductions are expenses that can be subtracted from your gross income, thereby lowering your taxable income and potentially decreasing the amount of tax you owe. Deductions can encompass a wide range of expenses, from business-related costs to medical expenses and charitable contributions. By strategically leveraging deductions, individuals and businesses can retain more of their hard-earned money and reinvest it in their growth and prosperity.

1. Keep Detailed Records

The foundation of maximizing tax deductions lies in meticulous record-keeping. Whether you're a freelancer, a sole proprietor, or a small business owner, maintaining accurate records of all expenses is paramount. This includes receipts, invoices, mileage logs, and any other documentation related to deductible expenses. By diligently documenting your expenditures throughout the year, you'll be better equipped to identify eligible deductions come tax time and avoid overlooking valuable opportunities for tax savings.

2. Know Your Eligible Deductions

To maximize deductions, it's crucial to be well-versed in the deductions available to you. For individuals, common deductions include mortgage interest, property taxes, medical expenses, charitable contributions, and certain education expenses. Small businesses, on the other hand, may be eligible for deductions such as business-related travel, office supplies, equipment purchases, utilities, insurance premiums, and professional services.

3. Leverage Retirement Contributions

Contributing to retirement accounts not only secures your financial future but also offers valuable tax benefits. Contributions to traditional Individual Retirement Accounts (IRAs) and employer-sponsored retirement plans such as 401(k)s are typically tax-deductible, reducing your taxable income for the year. By maximizing your contributions to retirement accounts, you not only build a nest egg for retirement but also capitalize on immediate tax savings.

4. Optimize Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

Health-related expenses can constitute a significant portion of your annual expenditures. By contributing to Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), you can allocate pre-tax dollars toward qualified medical expenses, thereby reducing your taxable income. HSAs, in particular, offer triple tax benefits: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. Maximizing contributions to these accounts can yield substantial tax savings while providing a financial safety net for healthcare expenses.

5. Deduct Business Expenses

For small business owners and self-employed individuals, deducting business expenses is a crucial strategy for minimizing tax liability. Business-related expenses such as advertising, office rent, utilities, professional fees, and equipment purchases are typically deductible. Additionally, expenses incurred for business travel, meals, entertainment, and vehicle usage may also be eligible for deduction, provided they are documented and meet IRS guidelines.

6. Take Advantage of Home Office Deductions

With the rise of remote work and home-based businesses, the home office deduction has become increasingly relevant for many taxpayers. If you use a portion of your home exclusively for business purposes, you may be eligible to deduct related expenses such as utilities, insurance, and maintenance. The IRS offers two methods for calculating the home office deduction: the simplified method, which provides a flat rate deduction based on square footage, and the regular method, which involves calculating actual expenses. Evaluating both options can help you determine the most advantageous approach for your situation.

7. Explore Tax Credits

In addition to deductions, tax credits offer another avenue for reducing tax liability. Unlike deductions, which lower taxable income, tax credits directly reduce the amount of tax owed, dollar for dollar. For individuals, tax credits such as the Earned Income Tax Credit (EITC), Child Tax Credit, and Lifetime Learning Credit can result in significant tax savings. Small businesses may also qualify for various tax credits, including the Small Business Health Care Tax Credit, Research and Development (R&D) Tax Credit, and Work Opportunity Tax Credit (WOTC). Exploring available tax credits and ensuring eligibility criteria are met can further enhance tax planning efforts.

8. Seek Professional Guidance

Navigating the complexities of tax deductions can be daunting, particularly for small business owners with limited resources and expertise. Seeking professional guidance from qualified tax professionals, accountants, or financial advisors can provide invaluable support in identifying eligible deductions, optimizing tax strategies, and ensuring compliance with tax laws and regulations. While professional assistance may entail upfront costs, the potential tax savings and peace of mind gained from expert advice can far outweigh the investment.

Conclusion

Maximizing tax deductions is not merely a matter of minimizing tax liability; it's a strategic approach to optimizing financial efficiency and fostering long-term prosperity. By understanding the array of deductions available, maintaining meticulous records, and leveraging tax-advantaged accounts and strategies, individuals and small businesses can harness the power of deductions to retain more of their earnings and fuel their growth and success. With careful planning, informed decision-making, and perhaps a little professional guidance, you can navigate the complexities of tax deductions with confidence and emerge financially stronger.

0 notes

Text

Lasik Eye Surgery Cost With Insurance

The cost of LASIK eye surgery can vary depending on several factors, including the surgeon’s experience, the technology used, and the geographical location. While many insurance plans do not cover LASIK surgery because it is considered an elective procedure for vision correction, some vision insurance plans or flexible spending accounts (FSAs) may offer partial coverage or reimbursement for LASIK surgery.

It’s essential to check with your insurance provider to determine if LASIK surgery is covered under your plan and to understand any coverage limitations, such as specific providers or facilities. Some insurance plans may offer discounts or negotiated rates for LASIK surgery through participating providers.

If LASIK surgery is not covered by insurance, patients may explore other options to help manage the cost, such as:

Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): These accounts allow individuals to set aside pre-tax dollars to pay for qualified medical expenses, including LASIK surgery. Contributions to FSAs or HSAs can help reduce out-of-pocket costs for LASIK surgery.

Financing Options: Many LASIK providers offer financing plans or payment options to help patients manage the cost of surgery. These plans may include low-interest loans, payment plans, or promotional offers with deferred interest.

Employee Benefits: Some employers offer vision benefits or discount programs that provide savings on LASIK surgery as part of their employee benefits package. Employees should check with their human resources department to explore available benefits.

Special Offers or Discounts: LASIK providers may offer special promotions, discounts, or package deals on LASIK surgery, particularly during certain times of the year. Patients can inquire about any available offers when researching LASIK providers.

Before undergoing LASIK surgery, it’s crucial to schedule a consultation with a qualified ophthalmologist to assess candidacy for the procedure, discuss treatment options, and obtain a personalized cost estimate. Additionally, patients should thoroughly review their insurance coverage, FSA/HSA eligibility, and financing options to make an informed decision about LASIK surgery and its associated costs.

0 notes

Text

You can use Good RX with your flexible spending account as well as your health savings account.

You should talk to your insurance company. Because anything you pay should be included as an out-of-pocket expense toward the deductible. It is lowering the cost of operations for an insurance company so it would make sense for them to encourage the use. The more you use it, the less the insurance company has to pay out-of-pocket So if I was running an insurance company, I would encourage you to use this program every time it offered a better deal. Is there anything you paid out-of-pocket I would include torture deductible. So mean as a financial adviser for all my group insurance plans or individual health plans. I would encourage them to do comparison shopping each time to make sure they're getting the best deal. As it said, it also could beat medicaid and medicare prescription cost. So again. It would lower the government's out-of-pocket expenditures.

By the way, if you're still working, you can contribute to your health savings account. And if you're getting medicare, you can use it towards the cost of atop pocket expenses plus any flexible spending account or if you're on medicaid. Since both of these further reduce your taxable income, it will lower your income tax and increase your ability for credits.

GoodRx

https://www.goodrx.com › business

How to Use GoodRx With Your High-Deductible Health Plan and HSA

May 28, 2019 — No. Even if your insurance plan doesn't cover a drug you need, you can always use a GoodRx discount and your HSA, as long as it's for qualified ...

Missing: group | Show results with: group

Cypress Benefit Solutions

https://cypressbenefitsolutions.com › ...

GoodRx vs. Insurance: Which Should My Employees Use?

According to the company, “Paying with a GoodRx coupon is considered an 'out-of-network' purchase, and it's up to the insurance company

Aetna

https://www.aetna.com › hsa-vs-fsa

FSA, HSA & HRA: What's the difference?

Learned the basics of tax-advantaged Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs). The see how different life

Medical News Today

https://www.medicalnewstoday.com › ...

HSA vs. FSA: Differences and more

Jan 4, 2023 — FSAs and HSAs are medical savings accounts, but they differ in that FSAs can provide funds more quickly, whereas HSAs are more flexible.

FSA overview

HSA overview

Differences

Which is better?

Can a person have both?

CMS National Training Program (.gov)

https://cmsnationaltrainingprogram.cms.gov › ...PDF

FAQ: Medicare & Tax-Favored Programs

The U.S. Internal Revenue Service (IRS) creates the rules for how most tax-favored health programs operate, like Flexible Spending

Yes. Even if enrolled in Medicare, you may keep an HSA if it was in existence prior to Medicare enrollment. You can spend from your HSA to help pay for medical expenses, such as deductibles, premiums, copayments, and coinsurances. If you use the account for qualified medical expenses, it will continue to be tax-free.

https://offices.depaul.edu › H...

PDF

Medicare and Your HSA FAQs

So Enroll in these two programs , and if you're working for an employer that has greater than Twenty employees then medicare is not mandatory to Enroll into at age 65. So you can continue on without medicare. And if you do so, you're allowed to contribute to a health savings account past age 65. Also, you delay your social security that age 70. This allows you to contribute to a health savings account. But you must not enroll in medicare and you must delay social security to age 70. 😉

However, people who continue working beyond age 65 (or whose spouse does so) and have access to an employer-provided HDHP can continue making HSA contributions as long as they don't enroll in Medicare or apply for Social Security benefits.Dec 13, 2023

https://www.kitces.com › blog › hs...

Preserving HSA Eligibility & Maximizing Contributions After 65

You can choose to never enroll in medicare as long as you continue to work it is not mandatory. Even at age seventy or eighty if you're still working then you don't have to enroll in Medicare but if you stop working it becomes mandatory to enroll into or you will be penalized. It's also if you start working, you may be able to pause medicare after the age 65 if you go back to work.

And yes, returning to work.You must return to work for a company that has greater than twenty employees for you to be able to pause medicare. But if it has greater than 20 employees, then you can or should be able to pause medicare after the age of 65. If you start it medicare and then return to work, you can pause medicare. The government should encourage this the use of private health care.....

AARP

https://www.aarp.org › health › ca...

What Happens to Medicare if I Start Working Again?

Jun 27, 2022 — For most employers with fewer than 20 employees, Medicare becomes your primary coverage at age 65 and the employer plan

As it says here if you're going back to work after age sixty-five and you can get a good medical plan And if the employer is greater than twenty people then you can pause Medicare you can drop Medicare.... This also means the government can divert funds to address any government debt... They can lower the budget for Medicare. And hopefully for Medicaid and redirect those funds to cover any government debt the federal government can give loans to the state county and local governments that are 0 interest rates loans to address any debt of the state county or local government. 🤔 So the state would have to pay back the principal or the county would have to pay back the principal or the local government would have to pay back the principal, but there would be no interest..... So this is like giving them a zero coupon bond.... They would receive a chunk of money upfront and then they would pay it back over a period of time the principal only... So it is A reverse 0 coupon bond. 🤔 So the federal government can help shut up the state county and local government. This would also help them to offer municipal bobans with higher ratings and lower interest payments at the state government level county government and local level because they will have lower debt service payments...... So the federal government can go around strengthening up the economies around the United States by strengthening the state government's county governments and local governments through 0 interest loan. If need be the federal government can actually forgive the debt as well. But all of this Is created by people working.... And also the government starts collecting more income tax and other related taxes.... So, it increases the flow of cash into the federal and the states and even if the state doesn't have an income tax the federal government should be giving a more back from the federal income tax states that have no income tax.... Because the federal government will be receiving more money from the individuals working in those states......

Can you pause Medicare if you go back to work?

Do I need to keep Medicare if returning to work? Well it depends. If you're going back to work and can get employer health coverage that is considered acceptable as primary coverage, you are allowed to drop Medicare and re-enroll again without penalties.

https://www.uhc.com › news-articles

Does Medicare coverage change if you return to work?

1 note

·

View note

Text

Payroll Deductions: What You Need To Know

Are you a small business owner navigating the complex world of payroll deductions? Understanding payroll deductions is crucial for ensuring accurate payroll processing and compliance with legal requirements. In this guide, we'll break down everything you need to know about payroll deductions in simple terms, empowering you to manage your payroll with confidence.

What Are Payroll Deductions?

Payroll deductions refer to the amounts withheld from an employee's paycheck to cover various expenses. These deductions can include taxes, contributions to retirement plans, insurance premiums, and other benefits offered by the employer.

Types of Payroll Deductions

1. Taxes: Federal, state, and local income taxes are typically withheld from employees' paychecks based on their earnings and withholding allowances. Additionally, Social Security and Medicare taxes, known as FICA taxes, are withheld to fund these government programs.

2. Retirement Contributions: Many employers offer retirement plans such as 401(k) or IRA options, allowing employees to contribute a portion of their earnings towards retirement savings. These contributions are deducted from employees' paychecks on a pre-tax or post-tax basis, depending on the plan.

3. Health Insurance Premiums: Employers may offer health insurance coverage to their employees, with premiums deducted from employees' paychecks to cover the cost of insurance.

4. Other Benefits: Payroll deductions may also include contributions to other employee benefits such as dental insurance, vision coverage, flexible spending accounts (FSAs), and commuter benefits.

Understanding Legal Requirements

As a small business owner, it's essential to comply with federal, state, and local laws governing payroll deductions. Failure to do so can result in penalties and legal consequences. Here are some key considerations:

1. Tax Withholding Requirements: Employers must calculate and withhold the correct amount of taxes from employees' paychecks based on applicable tax rates and withholding allowances.

2. Employee Consent: In most cases, employers must obtain written consent from employees before deducting certain expenses from their paychecks, such as insurance premiums or retirement contributions.

3. Wage Garnishments: Employers may be required to withhold a portion of an employee's wages to satisfy a court-ordered wage garnishment, such as child support or unpaid debts.

4. Record-Keeping: Employers must maintain accurate records of payroll deductions, including the amounts withheld from each employee's paycheck and the purpose of each deduction.

Tips for Managing Payroll Deductions

1. Stay Updated on Tax Laws: Tax laws and regulations are subject to change, so it's essential to stay informed about any updates that may affect payroll deductions.

2. Use Reliable Payroll Software: Invest in payroll software that automates the calculation and deduction of payroll taxes and other deductions, reducing the risk of errors and ensuring compliance.

3. Communicate with Employees: Clearly communicate with employees about their payroll deductions, including the purpose of each deduction and how it impacts their take-home pay.

4. Seek Professional Assistance: If you're unsure about payroll deductions or need help navigating complex tax laws, consider seeking assistance from a qualified accountant or payroll service provider offering payroll services for small businesses in Oklahoma City, OK.

0 notes

Text

Health Savings Accounts (HSAs): Maximizing Benefits

Health Savings Accounts (HSAs) are powerful financial tools that offer individuals and families tax advantages for saving and paying for qualified medical expenses. When used effectively, HSAs can help maximize savings and provide financial security for healthcare needs. Here's how to make the most of your health insurance plan in PA:

Understand HSA Basics: Before diving into maximizing HSA benefits, it's essential to understand how they work. An HSA is a tax-advantaged savings account available to individuals enrolled in a High Deductible Health Plan (HDHP). Contributions to an HSA are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

Contribute Regularly: Maximize the benefits of your HSA by contributing to it regularly. The IRS sets annual contribution limits, which may vary based on whether you have individual or family coverage. For 2024, individuals can contribute up to $3,650, while families can contribute up to $7,300, with an additional $1,000 catch-up contribution allowed for those aged 55 or older.

Take Advantage of Employer Contributions: Many employers offer contributions to employees' HSAs as part of their benefits package. If your employer provides this benefit, take full advantage of it. Employer contributions are typically considered tax-free income and can significantly boost your HSA balance.

Use HSA Funds Wisely: HSAs can be used to pay for a wide range of qualified medical expenses, including deductibles, copayments, prescription medications, dental care, vision expenses, and certain over-the-counter items. By using HSA funds to cover these expenses, you can effectively reduce your out-of-pocket healthcare costs while enjoying tax savings.

Save for Future Healthcare Expenses: In addition to using HSA funds for current medical expenses, consider using your HSA as a long-term savings vehicle for future healthcare needs. Unlike flexible spending accounts (FSAs), HSAs have no "use it or lose it" provision, meaning any unused funds roll over from year to year and continue to grow tax-free. Building a substantial HSA balance can provide financial security for unexpected medical costs in the future, including retirement healthcare expenses.

Invest HSA Funds: Many HSA providers offer the option to invest HSA funds in various investment options, such as mutual funds, stocks, and bonds. Investing in HSA funds can potentially generate higher returns than leaving them in a standard savings account, allowing your savings to grow more quickly over time. However, it's essential to consider your risk tolerance and investment objectives when choosing investment options for your HSA.

Keep Records of Medical Expenses: To ensure compliance with IRS regulations and maximize tax benefits, keep accurate records of all qualified medical expenses paid for with HSA funds. This includes receipts, invoices, and explanations of benefits (EOBs) from your healthcare providers. Maintaining organized records will make it easier to substantiate HSA withdrawals and claim tax deductions if necessary.

Consider HSA as a Retirement Tool: HSAs offer unique advantages for retirement planning. Once you turn 65, you can withdraw HSA funds for non-medical expenses without penalty, although withdrawals for non-qualified expenses are subject to income tax. This makes HSAs a valuable supplement to other retirement accounts, as funds can be used tax-free for healthcare expenses in retirement or as taxable income for other purposes.

Review Investment Performance Regularly: If you choose to invest HSA funds, monitor the performance of your investments regularly and adjust your investment strategy as needed. Rebalancing your investment portfolio periodically can help manage risk and ensure that your HSA funds continue to grow effectively over time.

Educate Yourself: Stay informed about HSA rules, regulations, and best practices to maximize your benefits. The IRS regularly updates guidelines related to HSAs, so it's essential to stay current with any changes that may affect your account.

In conclusion, Health Savings Accounts offer numerous benefits for individuals and families seeking to save money on healthcare expenses while enjoying tax advantages. By contributing regularly, using HSA funds wisely, investing strategically, and staying informed about HSA rules and regulations, you can maximize the benefits of your HSA and achieve greater financial security for healthcare needs now and in the future.

0 notes

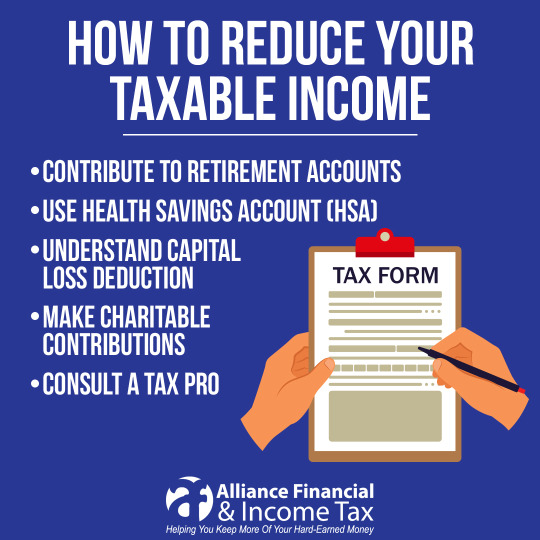

Photo

Here are some legal strategies to help reduce your taxable income: Contribute to a Retirement Account: Maximize contributions to traditional 401(k)s and IRAs. These contributions are tax-deductible and can significantly lower your taxable income. Roth IRAs, funded with after-tax dollars, allow tax-free growth and withdrawals in retirement. Open a Health Savings Account (HSA): If you have a high-deductible medical plan, contribute to an HSA. The money you put in is tax-free when used for medical expenses. Invest in Tax-Exempt Bonds: Consider municipal bonds, which provide tax-free interest income at the federal level. These bonds are issued by state or local governments. Utilize Flexible Spending Plans (FSAs): If your employer offers FSAs, take advantage of them. FSAs allow you to set aside pre-tax dollars for qualified medical or dependent care expenses. Claim Business Deductions: If you’re self-employed, explore deductions related to your business. Examples include home office expenses, business travel, and equipment purchases. Make Charitable Contributions: Donating to qualified charities can reduce your taxable income. Keep records of your contributions for tax purposes. Remember to consult a tax professional to tailor these strategies to your specific situation. 🌟

0 notes

Text

U.S. Healthcare Account

Health Savings Account (HSA): This is a type of savings account that allows individuals to save money for medical expenses on a tax-advantaged basis. To be eligible to contribute to an HSA, individuals must be enrolled in a high-deductible health plan (HDHP). Contributions to an HSA are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

Flexible Spending Account (FSA): A flexible spending account is another type of tax-advantaged savings account available in the United States that allows employees to set aside a portion of their earnings to pay for qualified medical expenses. Unlike HSAs, FSAs are typically funded through pre-tax payroll deductions and are subject to a "use it or lose it" rule, meaning funds not used by the end of the plan year may be forfeited.

Health Reimbursement Arrangement (HRA): An HRA is an employer-funded benefit plan that reimburses employees for out-of-pocket medical expenses and, in some cases, health insurance premiums. Unlike HSAs and FSAs, HRAs are funded solely by the employer and may have different rules regarding rollover of funds and eligibility.

Medical Savings Account (MSA): MSAs are a type of tax-advantaged savings account that was available prior to the introduction of HSAs. They functioned similarly to HSAs but had some key differences in terms of eligibility requirements and contribution limits.

Healthcare Spending Account: Some employers may offer their own customized healthcare spending accounts or reimbursement programs to help employees cover medical expenses not covered by their health insurance plans. These accounts could have varying rules and structures depending on the employer.

0 notes

Text

Tax-Saving Strategies for Surgeons_ Maximizing Deductions and Credits with John Moakler

John Moakler

Tax-Saving Strategies for Surgeons: Maximizing Deductions and Credits with John Moakler

As a surgeon, navigating the complexities of tax laws can be as intricate as performing a delicate procedure. However, understanding and implementing tax-saving strategies can significantly alleviate financial burdens and maximize your earnings. In this guide, we delve into effective methods with the help of experts like John Moakler tailored specifically for surgeons to optimize deductions and credits, ensuring a robust financial outlook.

Utilize Medical Expense Deductions

One of the primary avenues for tax savings for surgeons is through medical expense deductions. Beyond the obvious benefit of reducing taxable income, this deduction encompasses a wide range of expenses, including equipment, supplies, and even travel costs related to medical conferences or seminars. Ensure meticulous record-keeping to substantiate these expenses. Additionally, consider establishing a Health Savings Account (HSA) or Flexible Spending Account (FSA) to further capitalize on pre-tax dollars for medical expenses.

Maximizing deductions under this category involves strategic planning and foresight. For instance, timing elective medical procedures towards the end of the year can concentrate expenses within a single tax year, potentially surpassing the threshold for deductibility. Collaborate with a qualified tax professional to optimize these deductions within legal bounds, minimizing tax liabilities while adhering to regulatory guidelines.

Leverage Retirement Contributions

Surgeons can significantly reduce taxable income by maximizing contributions to retirement accounts such as 401(k) or Individual Retirement Accounts (IRAs). Not only do these contributions secure financial stability in the long term, but they also offer immediate tax advantages. Contributions to traditional retirement accounts are typically tax-deductible, lowering the current tax burden while allowing investments to grow tax-deferred until withdrawal during retirement.

A strategic approach involves contributing the maximum allowable amount to retirement accounts annually, taking advantage of employer matching programs whenever available. Additionally, surgeons nearing retirement age can explore catch-up contributions, allowing for increased contributions beyond standard limits. By prioritizing retirement savings with the help of experts like John Moakler, surgeons not only secure their financial future but also capitalize on immediate tax benefits, bolstering their overall financial health.

Optimize Business Expenses

Surgeons operating private practices or working as independent contractors can optimize tax savings by meticulously tracking and categorizing business expenses. This encompasses a broad spectrum, including equipment purchases, office rent, utilities, insurance premiums, and professional development costs. Leverage technology such as accounting software to streamline expense tracking and ensure compliance with tax regulations.

Moreover, consider structuring business expenses to maximize tax deductions. For instance, leasing equipment rather than purchasing outright can spread costs over time while retaining deductibility. Collaborate with a knowledgeable tax advisor to explore nuances specific to your practice and identify opportunities for tax optimization. By diligently managing business expenses with the help of experts like John Moakler, surgeons can not only reduce tax liabilities but also enhance profitability and sustainability in the long run.

Explore Home Office Deductions

In the wake of the COVID-19 pandemic, many surgeons have transitioned to telemedicine or remote administrative work, necessitating a home office setup. Leveraging home office deductions can yield substantial tax savings by allocating a portion of household expenses, such as rent, utilities, and internet bills, towards business use. However, adherence to stringent IRS guidelines is paramount to avoid triggering audits or penalties.

Establish a dedicated workspace within your home exclusively for business activities, ensuring it meets IRS criteria for eligibility. Document expenses meticulously and calculate deductions accurately based on the proportion of space utilized for business purposes. While home office deductions offer significant tax advantages, exercise prudence to remain compliant with regulatory requirements, safeguarding against potential audit risks.

Investigate Tax Credits

Beyond deductions, surgeons can harness various tax credits to further reduce tax liabilities. Explore credits such as the Research and Development Tax Credit or the Health Coverage Tax Credit, which offer incentives for specific activities or expenditures. Research eligibility criteria and collaborate with tax professionals to ascertain qualification and maximize utilization of available credits.

While tax credits provide direct reductions in tax liabilities, navigating eligibility criteria and application processes can be complex. Conduct thorough due diligence to identify applicable credits and leverage expert guidance to optimize tax-saving opportunities effectively. By capitalizing on available tax credits with the help of experts like John Moakler, surgeons can augment overall tax savings and enhance financial resilience in an ever-evolving tax landscape.

Consider Entity Structure Optimization

The choice of business entity structure can profoundly impact tax liabilities for surgeons. Evaluate options such as sole proprietorship, partnership, S corporation, or Limited Liability Company (LLC) to determine the most advantageous structure based on your practice's size, scope, and long-term objectives. Each entity type offers unique tax implications, ranging from pass-through taxation to corporate tax rates.

Consult with tax advisors and legal professionals to assess the tax implications of each entity structure comprehensively. Consider factors such as liability protection, administrative requirements, and potential tax-saving opportunities associated with each option. By aligning entity structure with tax planning strategies, surgeons can optimize tax efficiency, minimize compliance burdens, and position their practices for sustainable growth and success.

Navigating the intricate terrain of tax-saving strategies for surgeons demands meticulous planning, strategic foresight, and expert guidance. By optimizing deductions and credits tailored to their profession with the help of experts like John Moakler, surgeons can minimize tax liabilities, maximize earnings, and fortify their financial well-being. Embrace proactive tax planning, leverage available resources, and collaborate with knowledgeable professionals to navigate the complexities of tax laws effectively. By implementing these strategies diligently, surgeons can achieve financial empowerment and thrive in their professional endeavors.

0 notes

Text

Tips on How to Spend Your FSA So You Don't Lose It

If you have a flexible spending account, you only have a finite amount of time to use the funds you contribute. While employers can provide grace periods and rollover options, these accounts are often "use it or lose it."

Fortunately, there are many ways to spend your FSA before that expiration date hits! But how do FSAs work, and what can you use your funds on?

How Do FSAs Work?

An FSA is an employer-sponsored benefit allowing employees to contribute pre-tax dollars with every paycheck for qualified medical expenses. There's an annual limit to how much money you can put into your account, and you can only use the funds to pay for costs outlined by the IRS.

Furthermore, those funds typically expire at the end of the year. If you don't spend them, they go back to your employer.

Spending Your FSA Funds

Spending your FSA is usually easy if you have doctor appointments, prescription medications, dental care and other services throughout the year. But if you rarely use it, you might scramble at the end of the year to avoid losing your contributions.

Here are a few ideas on what you can use leftover FSA funds for at the end of the year.

Stock Up on Essentials

Did you know you can use your FSA to buy over-the-counter products? Headache medicine, pain relievers, decongestants, antacids, menstrual products and more all count as qualified medical expenses.

Why not stock up? You can spend that last bit on products you'll likely use next year, ensuring you never run out.

Buy New Sunglasses

You can also use your FSA to pay for optometry services and products. If you have prescription lenses, consider buying a new pair of sunglasses. Pick up a new stylish pair you can use when summer rolls around!

Try a New Service

FSAs cover all your typical healthcare services like doctor's visits and specialist care. However, you can also use those funds on less traditional services like acupuncture or chiropractic services.

Try those services if you have aches and pains. It's a great way to use up your FSA funds while seeing if you like the experience.

Read a similar article about is an FSA worth it here at this page.

#what is an fsa#hdhp#2024 contribution limits for fsa#health savings account companies#hsa qualification#top rated hsa#how do fsas work

0 notes

Text

How FSAs Can Complement Group Health Insurance For Employees?

Flexible Spending Accounts (FSAs) can complement group health insurance for employees by providing additional financial flexibility and tax advantages. FSAs are employer-sponsored benefit programs that allow employees to set aside pre-tax dollars to cover qualified medical expenses.

When integrated with group health insurance, FSAs offer several advantages that enhance the overall healthcare benefits package for employees.

Tax Savings: One of the primary benefits of FSAs is the tax advantage they provide. Contributions to an FSA are made with pre-tax dollars, meaning that the money is deducted from employees' paychecks before taxes are applied. This reduces employees' taxable income, resulting in lower income tax liabilities. The tax savings extend to both employees and employers, making FSAs a valuable component of a comprehensive benefits package.

Supplemental Coverage for Out-of-Pocket Costs: Group insurance plans often come with deductibles, copayments, and other out-of-pocket expenses that employees are required to cover. FSAs offer employees the opportunity to set aside funds specifically for these costs. Whether it's copayments for doctor visits, prescription medications, or other qualified medical expenses, employees can use FSA funds to supplement their group health insurance coverage.

Broader Coverage of Health-Related Expenses: FSAs cover a wide range of qualified medical expenses that may not be fully covered by group health insurance. This includes expenses such as over-the-counter medications, certain medical supplies, and preventive care costs. By having an FSA, employees can address various health-related needs beyond what their insurance plan may cover, providing a more comprehensive approach to healthcare financing.

Flexibility in Spending: FSAs provide employees with flexibility in how they use the allocated funds. Unlike Health Savings Accounts (HSAs), which require a high-deductible health plan, FSAs can be used in conjunction with various types of health insurance plans, including traditional group health insurance. This flexibility allows employees to tailor their healthcare spending to their specific needs and circumstances.

Year-to-Year Contribution Options: Employees have the flexibility to decide how much money to contribute to their FSA each year. While there is an annual contribution limit set by the Internal Revenue Service (IRS), employees can choose an amount that aligns with their expected healthcare expenses. This control over contributions allows employees to budget for their healthcare needs effectively.

Ease of Access to Funds: Accessing funds in an FSA is typically straightforward. Employees can use a dedicated debit card linked to their FSA or submit reimbursement requests for qualified expenses. This ease of access ensures that employees can readily use their FSA funds when needed, streamlining the process of managing out-of-pocket healthcare costs.

Enhanced Employee Satisfaction: Offering FSAs as part of the benefits package enhances employee satisfaction. Employees appreciate the financial flexibility and tax savings provided by FSAs, as well as the opportunity to have more control over their healthcare spending. This can contribute to a positive workplace culture and increased employee loyalty.

Encouragement of Preventive Care: FSAs support preventive care by covering expenses such as screenings, vaccinations, and certain wellness programs. Encouraging employees to prioritize preventive care aligns with the broader goal of maintaining a healthy workforce. Preventive measures supported by FSAs can contribute to lower overall healthcare costs and improved employee well-being.

Complementary to High-Deductible Health Plans: While FSAs can complement traditional group health insurance plans, they are also compatible with high-deductible health plans (HDHPs). This versatility makes FSAs suitable for employers offering a range of health insurance options, ensuring that employees can benefit from pre-tax contributions regardless of their chosen plan.

In conclusion, Flexible Spending Accounts offer valuable advantages that complement group health insurance for employees. From tax savings and supplemental coverage for out-of-pocket costs to flexibility in spending and encouragement of preventive care, FSAs enhance the overall healthcare benefits package.

Employers that incorporate FSAs into their benefits offerings provide employees with a more comprehensive and flexible approach to managing healthcare expenses, contributing to employee satisfaction and well-being.

0 notes

Text

Maximizing Deductions: Strategies for Optimizing Your Tax Return

Introduction:

Tax season can be a stressful time for many individuals and businesses alike. However, understanding how to maximize deductions can significantly impact your tax return, potentially saving you money and reducing your taxable income. In this blog post, we will explore various strategies for optimizing your tax return by maximizing deductions. From common deductions to lesser-known opportunities, we'll cover everything you need to know to make the most of tax season.

Understanding Deductions:

Deductions are expenses that you can subtract from your taxable income, reducing the amount of income that is subject to taxation.

Common deductions include:

Mortgage interest

Property taxes

Medical expenses

Charitable contributions

State and local taxes

It's essential to keep accurate records of your deductible expenses throughout the year to ensure you can claim them come tax time.

Keeping Track of Expenses:

Maintaining detailed records of your deductible expenses is crucial for maximizing your deductions.

Utilize software or apps to track expenses, organize receipts, and categorize deductions efficiently.

Be diligent about documenting all potential deductions, including business expenses, unreimbursed work-related costs, and any other eligible expenses.

Leveraging Retirement Contributions:

Contributing to retirement accounts such as a 401(k) or IRA not only helps you save for the future but can also provide immediate tax benefits.

Contributions to traditional retirement accounts are typically tax-deductible, reducing your taxable income for the year.

Take advantage of employer-sponsored retirement plans and consider maximizing contributions to reap the full tax benefits available.

Exploring Education Credits and Deductions:

Education-related expenses can also qualify for tax deductions or credits.

The American Opportunity Tax Credit and the Lifetime Learning Credit are two common credits available to taxpayers who incur higher education expenses.

Additionally, student loan interest may be deductible, providing further opportunities to reduce taxable income.

Maximizing Business Deductions:

If you are a business owner or self-employed individual, there are numerous deductions available to you.

Deductible business expenses may include office supplies, equipment purchases, travel expenses, professional services, and more.

Keep detailed records of all business-related expenses and consult with a tax professional to ensure you are maximizing your deductions while remaining compliant with tax laws.

Taking Advantage of Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs):

Contributions to HSAs and FSAs can provide tax advantages for medical expenses.

Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

FSAs allow you to set aside pre-tax dollars for eligible medical expenses, reducing your taxable income.

Timing Deductions Strategically:

Consider timing your deductions strategically to maximize their impact on your tax return.

For example, if you anticipate significant medical expenses, it may be beneficial to schedule elective medical procedures before the end of the tax year to maximize your deduction.

Similarly, accelerating charitable contributions or prepaying deductible expenses can help boost your deductions in a particular tax year.

Seeking Professional Advice:

Tax laws and deductions can be complex and subject to change, making it essential to seek professional advice.

Consult with a qualified tax professional or accountant to ensure you are taking advantage of all available deductions and credits while minimizing your tax liability.

A tax professional can provide personalized guidance based on your individual financial situation and help you navigate the complexities of the tax code.

Conclusion:

Maximizing deductions is a key strategy for optimizing your tax return and reducing your tax liability. By understanding the various deductions available, keeping detailed records of expenses, and leveraging tax-advantaged accounts and credits, you can make the most of tax season. Whether you're a business owner, individual taxpayer, or somewhere in between, implementing these strategies can help you maximize your deductions and achieve greater financial flexibility. Remember to consult with a tax professional for personalized advice tailored to your specific circumstances. With careful planning and attention to detail, you can take control of your tax return and make tax season a little less daunting.

0 notes

Text

The ABCs of Dental Insurance: Navigating Coverage with Ease

Having dental insurance can assure you that you are covered for various dental procedures when it comes to your oral health. However, it can occasionally be daunting to comprehend all the details of dental insurance. We have put together a thorough tutorial on the fundamentals of dental insurance to assist you in navigating the complicated world of dental coverage.

A - Annual Maximum

The maximum amount that your dental insurance plan will cover for your dental care in a given calendar year is known as the annual maximum. It's critical to understand your plan's yearly maximum so you can plan your dental spending. Should you surpass the yearly cap, you have the financial responsibility for any extra expenses incurred.

B - Benefits

The coverage that is provided by your insurance plan is outlined in the dental insurance benefits. This covers restorative operations like fillings, crowns, and root canals and preventative services like routine checkups, cleanings, and x-rays. Gaining knowledge about your benefits will enable you to maximize the value of your insurance coverage and make well-informed decisions regarding your dental treatment.

C - Co-Payments

Co-payments, often called co-pays, are the set sum of money you must have on hand for every dental appointment or treatment. Depending on the kind of service you receive, this sum could change. A standard cleaning, for instance, can need less co-payment than a more involved treatment like a dental implant. You can better budget your out-of-pocket costs if you know your co-payment levels.

D - Deductible

The amount of money you have to fork out before your dental insurance coverage begins is known as your deductible. Usually, there is an annual maximum that you must reach before your insurance provider begins to pay for your dental care. Depending on your insurance plan, deductibles may differ, so be sure to review the specifics of your policy to find out how much you must pay out of pocket before your coverage starts.

E - Exclusions

Exclusions are specified dental services or procedures not covered by dental insurance policies. These are common in the plans. Plan exclusions might differ, so it's essential to read your policy to find out which services are thoroughly and aren't covered. Orthodontic treatments like adult braces or cosmetic dental procedures like tooth whitening are standard exclusions.

F - Flexible Spending Account (FSA)

You can utilize a tax-advantaged account called a Flexible Spending Account (FSA) to set aside money for dental and medical costs. Pre-tax money is used to fund contributions to an FSA, which can reduce your taxable income. Your FSA money can be used to pay your deductible and co-payments and for dental procedures and treatments not covered by your insurance plan.

G - Group Plans

Employers frequently provide group dental insurance as a part of their benefits package for workers. These policies cover a set of people, including employees and their families. Compared to individual policies, group plans often feature cheaper rates and more extensive coverage. Dental insurance through a group plan could be more affordable if you can participate in one.

H - HMO and PPO

Two popular forms of dental insurance policies are HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization). Selecting a primary care dentist to handle all your dental needs is a requirement of HMO insurance. PPO plans, on the other hand, often have higher premiums but provide you greater freedom to choose your dentist. If you are aware of their distinctions, it will be easier for you to choose the PPO or HMO plan that best meets your needs.

I - In-Network and Out-of-Network Providers

Dental insurance policies frequently include a network of dentists who have agreed to provide treatments at subsidized prices. We refer to these dentists as "in-network providers." Your insurance coverage is usually higher, and your out-of-pocket costs may be cheaper when you see an in-network dentist. Your coverage may be lowered if you decide to see a dentist not part of your plan's network; these providers are known as out-of-network providers.

J - Justification of Benefits (EOB)

Following your dental care, you will get a paper from your insurance company called an Explanation of Benefits (EOB). It lists the treatments rendered, the dentist's fee, the insurance company's reimbursement, and any potential outstanding balance you may be liable for. It's crucial to check your EOBs to make sure your insurance provider has handled your claims fairly and that you aren't being overcharged.

Making sense of dental insurance can be challenging, but knowing its fundamentals can enable you to make well-informed choices regarding your oral health. Remember to go over the specifics of your insurance, comprehend your advantages, and keep yourself updated on any modifications to your coverage. By doing this, you can keep your smile healthy and avoid any costly shocks while maximizing the benefits of your dental insurance.

In conclusion, dental insurance is essential for guaranteeing that people have access to high-quality dental treatment. You can optimize the advantages offered by your insurance plan, make educated decisions about your dental treatment, and navigate coverage easily if you are familiar with the fundamentals of dental insurance.

Remember that sustaining good oral health requires routine dental checkups and preventative treatment. Thus, use your dental insurance well, be knowledgeable, and keep grinning!

Author Bio: Dr. Ty King, DDS, is a highly skilled dentist in Rogers, Arkansas. With years of experience in the dental field, Dr. King is passionate about providing top-quality dental care to his patients. His expertise and commitment to oral health make him a trusted name in the community.

0 notes

Text

Mastering Your Paycheck: A Step-by-Step Guide to Understanding Paycheck Taxes and Maximizing Your Take-Home Pay

Understanding your paycheck can sometimes feel like deciphering a complex puzzle. From taxes to deductions, it can be overwhelming to navigate the various components that affect your take-home pay. However, with a little knowledge and careful planning, you can master your paycheck and maximize your earnings. In this step-by-step guide, we will walk you through the process of understanding paycheck taxes and show you how to make the most of your hard-earned money.

Step 1: Know Your Income

The first step in mastering your paycheck is understanding your income. This includes your salary, wages, tips, and any other forms of compensation. It's important to know the exact amount you earn before any deductions or taxes are taken out.

Step 2: Understand Tax Withholdings

Taxes are a necessary part of every paycheck, but understanding how they are calculated can help you plan your finances more effectively. The two main types of taxes that are typically withheld from your paycheck are federal income tax and Social Security tax.

Federal income tax is based on your income level and filing status. The higher your income, the higher the percentage of tax you will owe. Your employer will calculate the amount of federal income tax to withhold based on the information you provide on your W-4 form.

Social Security tax is a flat percentage of your income, up to a certain limit. As of 2021, the Social Security tax rate is 6.2% of your earnings, up to a maximum taxable limit of $142,800. This tax goes towards funding the Social Security program.

Step 3: Determine Other Deductions

In addition to taxes, there may be other deductions taken from your paycheck. These can include contributions to retirement plans, health insurance premiums, and any other voluntary deductions you have elected to take. It's important to review your paycheck stub or online portal to understand all the deductions that are being taken out.

Step 4: Calculate Your Take-Home Pay

Now that you understand the various deductions from your paycheck, you can calculate your take-home pay. This is the amount of money you actually receive after all taxes and deductions have been taken out. It's important to have a clear understanding of your take-home pay so that you can budget and plan accordingly.

Step 5: Maximize Your Take-Home Pay

Once you have a clear picture of your take-home pay, you can take steps to maximize it. Here are a few strategies to consider:

- Adjust Your Tax Withholdings: If you consistently receive a large tax refund, you may be having too much tax withheld from your paycheck. By adjusting your W-4 form, you can increase your take-home pay throughout the year.

- Take Advantage of Pre-Tax Benefits: Many employers offer pre-tax benefits such as flexible spending accounts (FSAs) or health savings accounts (HSAs). These allow you to set aside pre-tax dollars for eligible expenses, reducing your taxable income and increasing your take-home pay.

- Contribute to Retirement Plans: Contributing to a retirement plan, such as a 401(k), can not only help you save for the future but also reduce your taxable income in the present. By lowering your taxable income, you can increase your take-home pay.

- Review Your Deductions: Periodically review the deductions being taken from your paycheck to ensure they are accurate and necessary. If you no longer need a particular deduction, such as additional life insurance coverage, you can adjust or remove it to increase your take-home pay.

As an employee, it's essential to have a clear understanding of the various components that make up your paycheck. One crucial aspect is paycheck taxes. Understanding paycheck taxes is vital because it allows you to make informed financial decisions and ensures that you're maximizing your take-home pay. In this comprehensive guide, we will take you through the step-by-step process of understanding paycheck taxes and provide valuable insights on how to optimize your earnings.

Understanding the components of your paycheck

Before diving into the intricacies of paycheck taxes, let's first take a closer look at the different elements that make up your paycheck. When you receive your paycheck, it typically includes your gross income, which is the total amount you earned before any deductions. From your gross income, various deductions are made, such as taxes and other withholdings, resulting in your net income or take-home pay.

Types of paycheck taxes

Paycheck taxes can be categorized into different types, each serving a specific purpose. By understanding these tax types, you will gain a clearer picture of how they impact your overall earnings.

Federal income tax

One of the most significant paycheck taxes is the federal income tax. This tax is imposed by the federal government on individuals' earnings and is calculated based on a progressive tax system. The federal income tax is deducted from your paycheck based on the information you provide on your W-4 form, which determines your tax withholding.

State income tax

In addition to federal income tax, many states also impose their own income tax. The state income tax rate and regulations vary from state to state, so it's crucial to familiarize yourself with the specific laws of your state. The state income tax is typically calculated as a percentage of your taxable income, which can differ from your federal taxable income.

Social Security tax

The Social Security tax is a federal tax that funds the Social Security program, which provides benefits to retirees, disabled individuals, and survivors of deceased workers. The Social Security tax is levied on both employees and employers, with each contributing a specific percentage of the employee's earnings. This tax is subject to an income limit, beyond which no further Social Security tax is deducted from your paycheck.

Medicare tax

Similar to the Social Security tax, the Medicare tax is a federal tax that funds the Medicare program, which provides healthcare benefits for individuals over the age of 65 and certain disabled individuals. The Medicare tax is also levied on both employees and employers, and the rates are fixed percentages of the employee's earnings. Unlike the Social Security tax, there is no income limit for Medicare tax deductions.

Other paycheck deductions

Apart from paycheck taxes, there are various other deductions that can impact your take-home pay. These deductions can include contributions to retirement plans, health insurance premiums, and other benefits offered by your employer. It's essential to review these deductions carefully to ensure accuracy and understand how they affect your overall compensation.

Maximizing your take-home pay

Now that you have a solid understanding of paycheck taxes and deductions, let's explore strategies to maximize your take-home pay. Here are some effective tips to help you optimize your earnings:

Paycheck tax planning strategies

One way to maximize your take-home pay is through effective paycheck tax planning. This involves reviewing and adjusting your tax withholdings to ensure that you're neither overpaying nor underpaying your taxes. By accurately completing your W-4 form and considering any life changes or tax credits, you can align your tax withholdings more closely with your actual tax liability, resulting in a more favorable paycheck.

Utilize tax-advantaged accounts

Another strategy to boost your take-home pay is to take advantage of tax-advantaged accounts offered by your employer, such as a 401(k) or a Health Savings Account (HSA). By contributing to these accounts, you can reduce your taxable income and potentially lower your overall tax liability. Additionally, some employers may offer matching contributions to your retirement account, which is essentially free money that can significantly enhance your long-term financial security.

Review your paycheck regularly

It's crucial to review your paycheck regularly to ensure that there are no errors or discrepancies. Mistakes can happen, and it's essential to catch them early to avoid any financial setbacks. Take the time to carefully examine the breakdown of your paycheck, including taxes, deductions, and contributions, and compare them to your expectations and any relevant documentation.

Resources for further understanding paycheck taxes

Understanding paycheck taxes can be complex, but fortunately, there are numerous resources available to help you navigate this subject. The Internal Revenue Service (IRS) website is an excellent starting point, providing detailed information on federal tax regulations and resources. Additionally, many state government websites offer resources and guides specific to state income taxes. If you prefer more personalized assistance, consider consulting with a tax professional who can provide expert advice tailored to your specific circumstances.

Conclusion

Mastering your paycheck and understanding paycheck taxes is an essential aspect of managing your finances effectively. By having a comprehensive understanding of the various components that make up your paycheck, including paycheck taxes and deductions, you can make informed decisions to maximize your take-home pay. Remember to utilize paycheck tax planning strategies, explore tax-advantaged accounts, and review your paycheck regularly to ensure accuracy. By implementing these practices, you can optimize your earnings and achieve greater financial stability.

By following these steps and implementing these strategies, you can master your paycheck and make the most of your hard-earned money. Understanding paycheck taxes and maximizing your take-home pay is an essential part of financial success. Take the time to review your paycheck and make any necessary adjustments to ensure you are optimizing your earnings.

Remember, if you have any specific questions about your paycheck or taxes, it's always a good idea to consult with a tax professional or financial advisor. They can provide personalized guidance based on your unique situation and help you make informed decisions.

Read the full article

0 notes

Last Seen Blogs

spunangel34

SpunGirl

mytwdblog

Untitled

masonmount

magiskt men tragiskt

phalle

i do not get bitches

mmoutfitters

MMOutfitters