#Competition | Increasingly | Consolidated World

Text

America Has a Resilience Problem

The Chair of the Federal Trade Commission Makes the Case for Competition in an Increasingly Consolidated World.

— March 20, 2024 | By Lina M. Khan | Foreign Policy

Aïda Amer Illustration For Foreign Policy

The Federal Trade Commission (FTC) enforces the nation’s antitrust and consumer protection laws. We focus primarily on domestic markets and the U.S. economy. Through this work, we get a ground-level view of how markets are structured in America—and of how the extent of competition or consolidation drives outcomes that affect us all.

Like many across government, the FTC is watching closely as the release of sophisticated AI tools creates both opportunities and risks. Our work is already tackling the day-to-day harms these tools can turbocharge, from voice-cloning scams to commercial surveillance.

But beyond these immediate challenges, we face a more fundamental question of power and governance. Will this be a moment of opening up markets to free and fair competition, unleashing the full potential of emerging technologies? Or will a handful of dominant firms concentrate control over key tools, locking us into a future of their choosing?

The stakes of how we answer this question are enormously high. Technological breakthroughs can disrupt markets, spur economic growth, and change the nature of war and geopolitics. Whether we opt for a national policy of consolidation or of competition will have huge consequences for decades to come.

As in prior moments of contestation, we are starting to hear the argument that America must protect its domestic monopolies to ensure we stay ahead on the global stage. Rather than double down on promoting free and fair competition, this “national champions” argument holds that coddling our dominant firms is the path to maintaining global dominance.

We should be extraordinarily skeptical of this argument and instead recognize that monopoly power in America today is a major threat to America’s national interests and global leadership. History and experience show that lumbering monopolies mired in red tape and bureaucratic inertia cannot deliver the breakthrough technological advancements that hungry start-ups tend to create. It is precisely these breakthroughs that have allowed America to harness cutting-edge technologies and have made our economy the envy of the world. To stay ahead globally, we don’t need to protect our monopolies from innovation—we need to protect innovation from our monopolies. And one of the clearest illustrations of how consolidation threatens our national interests is the risk monopolization poses to our common defense.

U.S. airmen load pallets with baby formula from Switzerland bound for the United States during a baby formula shortage in the U.S., at Ramstein Air Base in Germany on May 21, 2022. Thomas Lohnes/Getty Images

In 2021, an errant spark in an explosives factory in Louisiana destroyed the only plant in the United States that makes black powder, a highly combustible product that is used to make mortar shells, artillery rounds, and Tomahawk missiles. There is no substitute for black powder, and it has hundreds of military applications. So when that factory blew up, and we didn’t have any backup plants, it destroyed the only black powder production in all of North America. There’s a simple lesson here: Don’t put all your eggs in one basket.

This is but one of many examples of how consolidation threatens our national interests. We know that monopolies and consolidated markets can result in higher prices and lower output. But monopolies also foster systemic vulnerabilities, since concentrating production also concentrates risk. Someone could probably argue it was more efficient to put all black powder production in one plant in Louisiana. And maybe it was—until it wasn’t.

Defense officials now identify the problem of monopoly in our country as a strategic weakness. The Pentagon has been warning about vulnerabilities in our national security supply chain for years. One top official recently noted that our increased reliance on a small number of contractors for critical capabilities impacts our ability to ramp up production.

One early victory in my tenure as FTC chair was blocking the proposed merger between Lockheed and Aerojet. Aerojet is the last independent U.S. supplier of key missile inputs, and our investigation showed that the deal would have allowed Lockheed to cut off rivals’ access to this key input and jack up the price that our government, and ultimately the public, has to pay. It was the first time in decades that our government sued to halt consolidation in the defense industrial base.

It’s not just our defense industrial base where we have a problem. The pandemic exposed fragilities across our supply chains, with shortages in everything from semiconductors to personal protective equipment. And it’s not just a once-in-a-century pandemic. Even more routine disruptions like plant contaminations or hurricanes have revealed how, in a concentrated system, a single shock can have cascading effects, yielding shortages in products ranging from baby formula to IV bags.

Consolidation causes problems beyond supply chains. For years, successive administrations have sought to strengthen our cybersecurity defenses against a catastrophic attack. A few weeks ago, one of the main medical benefit claims networks in America, Change Healthcare, was taken down for weeks due to a cyberattack, depriving hospitals and medical providers of the ability to bill for their services—and wreaking havoc across our health care system. That network is owned by UnitedHealth Group, which was allowed to buy Change despite a Department of Justice lawsuit seeking to block the deal. Quite simply, we have a resiliency problem in America. Consolidation and monopolization have left us more vulnerable and less resilient in the face of shocks.

But what about AI and the innovation economy? Black powder and baby formula shortages are one thing, but the corporations that run big data centers and large language models are highly technical operations, with tens of billions of dollars of capital to deploy, trillions in market capitalization, and some of the most highly skilled professionals.

Again, we should be guided by history. In the 1970s, Walter Wriston, the CEO of Citibank and a key leader on Wall Street, asked why antitrust enforcers were filing suits against high-tech American darlings like IBM and AT&T: “What is the public good of knocking IBM off?” he said. “The conclusion to all this nonsense is that people cry, ‘Let’s break up the Yankees—because they are so successful.’” By contrast, Europe and Japan were protecting their national champions to win in the international arena.

We chose to promote competition, and that choice to bring antitrust lawsuits against IBM and AT&T ended up fostering waves of innovation—including the personal computer, the telecommunications revolution, and the logic chip. The national champions protected by Japan and Europe, meanwhile, fell behind and are long forgotten. In the United States, we bet on competition, and that made all the difference.

Imagine a different world, where today’s giants never had a chance to get their start and innovate, because policymakers decided that it was more important to protect IBM and AT&T from competition and allowed them to maintain their monopolies. Even when monopolies do innovate, they will often prioritize protecting their existing market position. Famously, an engineer at Kodak invented the first portable digital camera in the ’70s—but Kodak didn’t rush it to market in part because it didn’t want to cannibalize its existing sales. More generally, significant research shows that while monopolies may help deliver marginal innovations, breakthrough and paradigm-shifting innovations have historically come from disruptive outsiders. It is our commitment to free and fair competition that has allowed America to harness the talents of its citizens, reap breakthrough innovations, and lead as an economic powerhouse. But what about those times when we have accepted the national champions argument? One prominent example serves as a cautionary tale.

Boeing 727 and 737 airplanes are seen on the production line at a factory in Renton, Washington, in 1977. AFP Via Getty Images

In the 1990s, a White House advisor noted that there was one very high-tech firm that was “de facto national champion,” so important that “you can be an out-and-out advocate for it” in government. And we did support it, provide it with government contracts, and allow it to consolidate the industry. That national champion was Boeing, whose trajectory illustrates why this strategy can be catastrophic.

In 1997, Boeing became the only commercial aerospace maker in the United States. It came to enjoy this status after buying up McDonnell Douglas, the only other domestic producer of commercial airplanes—a merger reviewed by the FTC. Boeing is the clearest example of a purposeful decision to bet on national champions on behalf of American interests. Policymakers wanted a national champion, and they got it.

Three things happened after Boeing eliminated its domestic competition. First, according to commenters such as United Airlines CEO Scott Kirby, the merger allowed Boeing to slow innovation and to reduce product quality. Boeing’s R&D budget is consistently lower than that of its only rival, Airbus. Worse quality is one of the harms that most economists expect from monopolization, because firms that face little competition have limited incentive to improve their products.

Second, reporting suggests that Boeing executives began to view their knowledgeable workforce as a cost, not an asset, with tragic outcomes. As one consultant put it in 2000, “Boeing has always been less a business than an association of engineers devoted to building amazing flying machines.” This corporation’s engineers designed the B-52 in a single weekend. But the new post-merger Boeing decimated its workforce, offshored production, and demanded wage concessions.

Third is the risk that Boeing effectively became too big to fail and a point of leverage for countries seeking to influence U.S. policymaking.

Relying on a national champion creates supply chain weaknesses and taxpayer liabilities, but it also creates geopolitical vulnerabilities that can be exploited both by global partners and rivals. As it was buying McDonnell Douglas, Boeing held a board meeting in Beijing and lobbied Congress to end the annual review of China’s trading rights so that it could sell more planes. The Chinese government would order Boeing planes contingent upon certain U.S. policies, like whether the U.S. held off on sending warships into the Strait of Taiwan, or whether the U.S. lifted bans on the export of certain technologies.

National champions are still corporations first. They have earnings calls, shareholders, and quarterly profit targets. When policymakers in Washington decide to back a single monopoly, their objectives are but one concern among many for that corporation’s senior executives. As then-Exxon CEO Lee Raymond said, “I’m not a U.S. company and I don’t make decisions based on what’s good for the U.S.”

These days, the national champions argument often gets made in the context of our dominant tech firms. We often hear that pursuing antitrust cases against or regulating these firms will weaken American innovation and cede the global stage to China. These conversations often assume a Cold War-like arms race, with each country’s firms in a zero-sum quest for dominance.

The reality today is that some of these same tech firms are fairly integrated in China and are seeking greater access to the Chinese market. While there is nothing intrinsically improper about these ties, we should be clear-eyed about how they shape business incentives. Various incidents in recent years have highlighted how when U.S. corporations are economically dependent on China, it can spur them to act in ways that are contrary to our national interests.

Even if America’s dominant firms are not prioritizing America’s national interests, what should we make of the idea that they can keep America in the lead, if only they are left alone? This, too, is an argument we should treat with great skepticism.

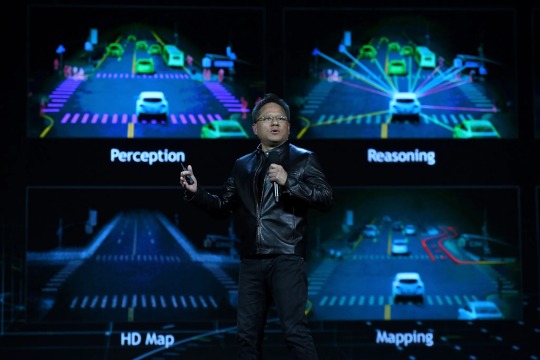

Nvidia President Jen-Hsun Huang delivers a keynote address at CES 2017 in Las Vegas on January 4, 2017. Ethan Miller/Getty Images

In 2021, the FTC sued to block Nvidia’s $40 billion acquisition of Arm, what would have been the largest semiconductor chip merger in history. Our investigation found that the merger would’ve allowed a major chip provider to control key computing technologies that rival firms depend on to develop their own competing chips. Our lawsuit alleged the deal would have risked stifling the innovation pipeline for next-generation technologies, affecting everything from data centers to self-driving cars. Two years on, Nvidia has continued to provide innovative products at a lower cost than we estimated they would have charged businesses after completing the acquisition of Arm. Arm itself is thriving, with its stock price doubling since it went public last year.

This is but the latest example of antitrust laws in action. The FTC was created in part to protect the innovative boons of open markets by ensuring that market outcomes—who wins and who loses—are determined by fair competition rather than by private gatekeepers. Protecting open and competitive markets means that the best ideas win. It means that businesses get ahead by competing on the merits of their skill, not by exploiting special privileges or bowing down to incumbent monopolists.

One final argument against protecting monopolies over competition is that it can leave our democracy more brittle.

Over the last couple of years, I’ve had the chance to hear from thousands of people across America—from nurses, farmers, and grocery store workers to tech founders, hotel franchisees, and writers in Hollywood. A recurring theme across their stories is a sense of fear, anxiety, and powerlessness. People from strikingly different walks of life have shared accounts of how markets monopolized by dominant middlemen enable coercive tactics—of how they feel their ability to make a decent living or thrive in their craft is, too often, not a function of their talents or diligence but instead is dictated by the arbitrary whims of distant giants.

A basic tenet of the American experiment is that real liberty means freedom from economic coercion and from the arbitrary, unaccountable power that comes with economic domination. Our antitrust laws were passed as a way to safeguard against undue concentration of power in our economic sphere, just as the Constitution creates checks and balances to safeguard against concentrated power in our political sphere.

Recommitting to robust antitrust enforcement and competition policy is good for America because it will make us safer, our technologies more innovative, and our economy more prosperous—but also because it is essential for safeguarding real opportunity for Americans and for ensuring that people in their day-to-day dealings experience liberty rather than coercion. When people believe that government has stopped fighting on their behalf, it can become a strategic weakness that outsiders are only too happy to exploit.

Thankfully, over the last few years we have seen significant progress across government in ensuring that we are centering everyday Americans in our policy decisions. From trade to industrial policy to competition, this administration has learned from past experiences and adopted new paradigms. A common throughline across these approaches is a commitment to revisiting old assumptions and updating our thinking in light of real-life experience and evidence.

Fighting back against the challenges we face is about more than enforcing the antitrust laws. But by promoting fair competition, by showing the American people that we will fight for their right to enjoy free, meaningful lives outside the grip of monopolists, we can help rebuild not just people’s confidence in the economy, but also a belief in American government, and its leadership both at home and abroad.

This article is adapted from a speech Lina Khan gave to the Carnegie Endowment for International Peace on March 13.

— Lina M. Khan is the Chair of the Federal Trade Commission.

#America 🇺🇸#USA 🇺🇸 | Resilience#Problem#Competition | Increasingly | Consolidated World#Foreign Policy#Lina M. Khan#The Federal Trade Commission (FTC)#Images: Getty Images#Boeing#Nvidia

0 notes

Text

The Federal Trade Commission (FTC) enforces the nation’s antitrust and consumer protection laws. We focus primarily on domestic markets and the U.S. economy. Through this work, we get a ground-level view of how markets are structured in America—and of how the extent of competition or consolidation drives outcomes that affect us all.

Like many across government, the FTC is watching closely as the release of sophisticated AI tools creates both opportunities and risks. Our work is already tackling the day-to-day harms these tools can turbocharge, from voice-cloning scams to commercial surveillance.

But beyond these immediate challenges, we face a more fundamental question of power and governance. Will this be a moment of opening up markets to free and fair competition, unleashing the full potential of emerging technologies? Or will a handful of dominant firms concentrate control over key tools, locking us into a future of their choosing?

The stakes of how we answer this question are enormously high. Technological breakthroughs can disrupt markets, spur economic growth, and change the nature of war and geopolitics. Whether we opt for a national policy of consolidation or of competition will have huge consequences for decades to come.

As in prior moments of contestation, we are starting to hear the argument that America must protect its domestic monopolies to ensure we stay ahead on the global stage. Rather than double down on promoting free and fair competition, this “national champions” argument holds that coddling our dominant firms is the path to maintaining global dominance.

We should be extraordinarily skeptical of this argument and instead recognize that monopoly power in America today is a major threat to America’s national interests and global leadership. History and experience show that lumbering monopolies mired in red tape and bureaucratic inertia cannot deliver the breakthrough technological advancements that hungry start-ups tend to create. It is precisely these breakthroughs that have allowed America to harness cutting-edge technologies and have made our economy the envy of the world. To stay ahead globally, we don’t need to protect our monopolies from innovation—we need to protect innovation from our monopolies. And one of the clearest illustrations of how consolidation threatens our national interests is the risk monopolization poses to our common defense.

In 2021, an errant spark in an explosives factory in Louisiana destroyed the only plant in the United States that makes black powder, a highly combustible product that is used to make mortar shells, artillery rounds, and Tomahawk missiles. There is no substitute for black powder, and it has hundreds of military applications. So when that factory blew up, and we didn’t have any backup plants, it destroyed the only black powder production in all of North America. There’s a simple lesson here: Don’t put all your eggs in one basket.

This is but one of many examples of how consolidation threatens our national interests. We know that monopolies and consolidated markets can result in higher prices and lower output. But monopolies also foster systemic vulnerabilities, since concentrating production also concentrates risk. Someone could probably argue it was more efficient to put all black powder production in one plant in Louisiana. And maybe it was—until it wasn’t.

Defense officials now identify the problem of monopoly in our country as a strategic weakness. The Pentagon has been warning about vulnerabilities in our national security supply chain for years. One top official recently noted that our increased reliance on a small number of contractors for critical capabilities impacts our ability to ramp up production.

One early victory in my tenure as FTC chair was blocking the proposed merger between Lockheed and Aerojet. Aerojet is the last independent U.S. supplier of key missile inputs, and our investigation showed that the deal would have allowed Lockheed to cut off rivals’ access to this key input and jack up the price that our government, and ultimately the public, has to pay. It was the first time in decades that our government sued to halt consolidation in the defense industrial base.

It’s not just our defense industrial base where we have a problem. The pandemic exposed fragilities across our supply chains, with shortages in everything from semiconductors to personal protective equipment. And it’s not just a once-in-a-century pandemic. Even more routine disruptions like plant contaminations or hurricanes have revealed how, in a concentrated system, a single shock can have cascading effects, yielding shortages in products ranging from baby formula to IV bags.

Consolidation causes problems beyond supply chains. For years, successive administrations have sought to strengthen our cybersecurity defenses against a catastrophic attack. A few weeks ago, one of the main medical benefit claims networks in America, Change Healthcare, was taken down for weeks due to a cyberattack, depriving hospitals and medical providers of the ability to bill for their services—and wreaking havoc across our health care system. That network is owned by UnitedHealth Group, which was allowed to buy Change despite a Department of Justice lawsuit seeking to block the deal. Quite simply, we have a resiliency problem in America. Consolidation and monopolization have left us more vulnerable and less resilient in the face of shocks.

But what about AI and the innovation economy? Black powder and baby formula shortages are one thing, but the corporations that run big data centers and large language models are highly technical operations, with tens of billions of dollars of capital to deploy, trillions in market capitalization, and some of the most highly skilled professionals.

Again, we should be guided by history. In the 1970s, Walter Wriston, the CEO of Citibank and a key leader on Wall Street, asked why antitrust enforcers were filing suits against high-tech American darlings like IBM and AT&T: “What is the public good of knocking IBM off?” he said. “The conclusion to all this nonsense is that people cry, ‘Let’s break up the Yankees—because they are so successful.’” By contrast, Europe and Japan were protecting their national champions to win in the international arena.

We chose to promote competition, and that choice to bring antitrust lawsuits against IBM and AT&T ended up fostering waves of innovation—including the personal computer, the telecommunications revolution, and the logic chip. The national champions protected by Japan and Europe, meanwhile, fell behind and are long forgotten. In the United States, we bet on competition, and that made all the difference.

Imagine a different world, where today’s giants never had a chance to get their start and innovate, because policymakers decided that it was more important to protect IBM and AT&T from competition and allowed them to maintain their monopolies. Even when monopolies do innovate, they will often prioritize protecting their existing market position. Famously, an engineer at Kodak invented the first portable digital camera in the ’70s—but Kodak didn’t rush it to market in part because it didn’t want to cannibalize its existing sales. More generally, significant research shows that while monopolies may help deliver marginal innovations, breakthrough and paradigm-shifting innovations have historically come from disruptive outsiders. It is our commitment to free and fair competition that has allowed America to harness the talents of its citizens, reap breakthrough innovations, and lead as an economic powerhouse. But what about those times when we have accepted the national champions argument? One prominent example serves as a cautionary tale.

In the 1990s, a White House advisor noted that there was one very high-tech firm that was “de facto national champion,” so important that “you can be an out-and-out advocate for it” in government. And we did support it, provide it with government contracts, and allow it to consolidate the industry. That national champion was Boeing, whose trajectory illustrates why this strategy can be catastrophic.

In 1997, Boeing became the only commercial aerospace maker in the United States. It came to enjoy this status after buying up McDonnell Douglas, the only other domestic producer of commercial airplanes—a merger reviewed by the FTC. Boeing is the clearest example of a purposeful decision to bet on national champions on behalf of American interests. Policymakers wanted a national champion, and they got it.

Three things happened after Boeing eliminated its domestic competition. First, according to commenters such as United Airlines CEO Scott Kirby, the merger allowed Boeing to slow innovation and to reduce product quality. Boeing’s R&D budget is consistently lower than that of its only rival, Airbus. Worse quality is one of the harms that most economists expect from monopolization, because firms that face little competition have limited incentive to improve their products.

Second, reporting suggests that Boeing executives began to view their knowledgeable workforce as a cost, not an asset, with tragic outcomes. As one consultant put it in 2000, “Boeing has always been less a business than an association of engineers devoted to building amazing flying machines.” This corporation’s engineers designed the B-52 in a single weekend. But the new post-merger Boeing decimated its workforce, offshored production, and demanded wage concessions.

Third is the risk that Boeing effectively became too big to fail and a point of leverage for countries seeking to influence U.S. policymaking.

Relying on a national champion creates supply chain weaknesses and taxpayer liabilities, but it also creates geopolitical vulnerabilities that can be exploited both by global partners and rivals. As it was buying McDonnell Douglas, Boeing held a board meeting in Beijing and lobbied Congress to end the annual review of China’s trading rights so that it could sell more planes. The Chinese government would order Boeing planes contingent upon certain U.S. policies, like whether the U.S. held off on sending warships into the Strait of Taiwan, or whether the U.S. lifted bans on the export of certain technologies.

National champions are still corporations first. They have earnings calls, shareholders, and quarterly profit targets. When policymakers in Washington decide to back a single monopoly, their objectives are but one concern among many for that corporation’s senior executives. As then-Exxon CEO Lee Raymond said, “I’m not a U.S. company and I don’t make decisions based on what’s good for the U.S.”

These days, the national champions argument often gets made in the context of our dominant tech firms. We often hear that pursuing antitrust cases against or regulating these firms will weaken American innovation and cede the global stage to China. These conversations often assume a Cold War-like arms race, with each country’s firms in a zero-sum quest for dominance.

The reality today is that some of these same tech firms are fairly integrated in China and are seeking greater access to the Chinese market. While there is nothing intrinsically improper about these ties, we should be clear-eyed about how they shape business incentives. Various incidents in recent years have highlighted how when U.S. corporations are economically dependent on China, it can spur them to act in ways that are contrary to our national interests.

Even if America’s dominant firms are not prioritizing America’s national interests, what should we make of the idea that they can keep America in the lead, if only they are left alone? This, too, is an argument we should treat with great skepticism.

We need to choose competition over national champions, and there are steps we are taking to put that into practice.

In 2021, the FTC sued to block Nvidia’s $40 billion acquisition of Arm, what would have been the largest semiconductor chip merger in history. Our investigation found that the merger would’ve allowed a major chip provider to control key computing technologies that rival firms depend on to develop their own competing chips. Our lawsuit alleged the deal would have risked stifling the innovation pipeline for next-generation technologies, affecting everything from data centers to self-driving cars. Two years on, Nvidia has continued to provide innovative products at a lower cost than we estimated they would have charged businesses after completing the acquisition of Arm. Arm itself is thriving, with its stock price doubling since it went public last year.

This is but the latest example of antitrust laws in action. The FTC was created in part to protect the innovative boons of open markets by ensuring that market outcomes—who wins and who loses—are determined by fair competition rather than by private gatekeepers. Protecting open and competitive markets means that the best ideas win. It means that businesses get ahead by competing on the merits of their skill, not by exploiting special privileges or bowing down to incumbent monopolists.

One final argument against protecting monopolies over competition is that it can leave our democracy more brittle.

Over the last couple of years, I’ve had the chance to hear from thousands of people across America—from nurses, farmers, and grocery store workers to tech founders, hotel franchisees, and writers in Hollywood. A recurring theme across their stories is a sense of fear, anxiety, and powerlessness. People from strikingly different walks of life have shared accounts of how markets monopolized by dominant middlemen enable coercive tactics—of how they feel their ability to make a decent living or thrive in their craft is, too often, not a function of their talents or diligence but instead is dictated by the arbitrary whims of distant giants.

A basic tenet of the American experiment is that real liberty means freedom from economic coercion and from the arbitrary, unaccountable power that comes with economic domination. Our antitrust laws were passed as a way to safeguard against undue concentration of power in our economic sphere, just as the Constitution creates checks and balances to safeguard against concentrated power in our political sphere.

Recommitting to robust antitrust enforcement and competition policy is good for America because it will make us safer, our technologies more innovative, and our economy more prosperous—but also because it is essential for safeguarding real opportunity for Americans and for ensuring that people in their day-to-day dealings experience liberty rather than coercion. When people believe that government has stopped fighting on their behalf, it can become a strategic weakness that outsiders are only too happy to exploit.

Thankfully, over the last few years we have seen significant progress across government in ensuring that we are centering everyday Americans in our policy decisions. From trade to industrial policy to competition, this administration has learned from past experiences and adopted new paradigms. A common throughline across these approaches is a commitment to revisiting old assumptions and updating our thinking in light of real-life experience and evidence.

Fighting back against the challenges we face is about more than enforcing the antitrust laws. But by promoting fair competition, by showing the American people that we will fight for their right to enjoy free, meaningful lives outside the grip of monopolists, we can help rebuild not just people’s confidence in the economy, but also a belief in American government, and its leadership both at home and abroad.

11 notes

·

View notes

Text

[The Daily Don]

* * * *

LETTERS FROM AN AMERICAN

September 26, 2023

HEATHER COX RICHARDSON

Today, on the anniversary of the creation of the Federal Trade Commission (FTC) in 1914, the FTC and 17 state attorneys general sued Amazon for using “a set of interlocking anticompetitive and unfair strategies to maintain its monopoly power.” The FTC and the suing states say “Amazon’s actions allow it to stop rivals and sellers from lowering prices, degrade quality for shoppers, overcharge sellers, stifle innovation, and prevent rivals from fairly competing against Amazon.”

The states suing are Connecticut, Delaware, Maine, Maryland, Massachusetts, Michigan, Minnesota, New Hampshire, New Jersey, New Mexico, Nevada, New York, Oklahoma, Oregon, Pennsylvania, Rhode Island, and Wisconsin. The lawsuit was filed in U.S. District Court for the Western District of Washington.

While estimates of Amazon’s control of the online commerce market vary, they center around about 40%, and Amazon charges third-party merchants for using the company’s services to store and ship items. Last quarter, Amazon reported more than $32 billion in revenues from these services. The suit claims that Amazon illegally overcharges third-party sellers and inflates prices.

This lawsuit is about more than Amazon: it marks a return to traditional forms of government antitrust action that were abandoned in the 1980s. Traditionally, officials interpreted antitrust laws to mean the government should prevent large entities from swallowing up markets and consolidating their power in order to raise prices and undercut workers’ rights. They wanted to protect economic competition, believing that such competition would promote innovation, protect workers, and keep consumer prices down.

In the 1980s, government officials replaced that understanding with an idea advanced by former solicitor general of the United States Robert Bork—the man whom the Senate later rejected for a seat on the Supreme Court because of his extremism—who claimed that traditional antimonopoly enforcement was economically inefficient because it restricted the ways businesses could operate. Instead, he said, consolidation of industries was fine so long as it promoted economic efficiencies that, at least in the short term, cut costs for consumers. While antitrust legislation remained on the books, the understanding of what it meant changed dramatically.

Reagan and his people advanced Bork’s position, abandoning the idea that capitalism fundamentally depends on competition. Industries consolidated, and by the time Biden took office, his people estimated the lack of competition was costing a median U.S. household as much as $5,000 a year.

On July 9, 2021, Biden called the turn toward Bork’s ideas “the wrong path” and vowed to restore competition in an increasingly consolidated marketplace. In an executive order, he established a White House Competition Council to direct a whole-of-government approach to promoting competition in the economy.

“[C]ompetition keeps the economy moving and keeps it growing,” Biden said. “Fair competition is why capitalism has been the world’s greatest force for prosperity and growth…. But what we’ve seen over the past few decades is less competition and more concentration that holds our economy back.”

In that speech, Biden deliberately positioned himself in our country’s long history of opposing economic consolidation. Calling out both Roosevelt presidents—Republican Theodore Roosevelt, who oversaw part of the Progressive Era, and Democrat Franklin Delano Roosevelt, who oversaw the New Deal—Biden celebrated their attempt to rein in the power of big business, first by focusing on the abuses of those businesses, and then by championing competition.

While still a student at Yale Law School, FTC chair Lina Khan published an essay examining the anticompetitive nature of modern businesses like Amazon, arguing that focusing on consumer prices alone does not address the problems of consolidation and monopoly. With today’s action, the FTC is restoring the traditional vision of antitrust action.

President Biden demonstrated his support for ordinary Americans in another historic way today when he became the first sitting president to join a picket line of striking workers. In Wayne County, Michigan, he joined a UAW strike, telling the striking autoworkers, “Wall Street didn’t build the country, the middle class built the country. Unions built the middle class. That’s a fact. Let’s keep going, you deserve what you’ve earned. And you’ve earned a hell of a lot more than you’re getting paid now."

Even as Biden was standing on the picket line, House speaker Kevin McCarthy (R-CA) released a new budget plan that moves even farther to the right. Yesterday, former president Trump backed the far-right extremists threatening to shut down the government, insisting that holding the government hostage is the best way to get everything they want, including, he wrote, an end to the criminal cases against him.

“The Republicans lost big on Debt Ceiling, got NOTHING, and now are worried that they will be BLAMED for the Budget Shutdown. Wrong!!! Whoever is President will be blamed,” Trump wrote on social media. “UNLESS YOU GET EVERYTHING, SHUT IT DOWN! Close the Border, stop the Weaponization of ‘Justice,’ and End Election Interference.”

McCarthy is reneging on the agreement he made with Biden in the spring as conditions for raising the debt ceiling, and instead is calling for dramatic cuts to the nation’s social safety net, as well as restarting construction of a border wall between the U.S. and Mexico, as starting points for funding the government. Cuts of more than $150 billion in his new proposal would mean cutting housing subsidies for the poor by 33%, fuel subsidies for low-income families by more than 70%, and funding for low-income schools by nearly 80% and would force more than 1 million women and children off of nutritional assistance.

The “bottom line is we’re singularly focused right now on achieving our conservative objectives,” Representative Garret Graves (R-LA) told Jeff Stein, Marianna Sotomayor, and Moriah Balingit of the Washington Post. The Republicans plan to preserve the tax cuts of the Trump years, which primarily benefited the wealthy and corporations.

At any point, McCarthy could return to the deal he cut with Biden, pass the appropriations bills with Democratic support, and fund the government. But if he does that, he is almost certain to face a challenge to his speakership from the extremists who currently are holding the country hostage.

This evening, the Senate reached a bipartisan deal to fund the government through November 17 and to provide additional funding for Ukraine (although less than the White House wants), passing it by a vote of 77–19. Senate minority leader Mitch McConnell (R-KY) urged the House Republicans to agree to the measure, warning them that shutdowns “don’t work as bargaining chips.” Nevertheless, McCarthy would not say he would take up the bill, and appears to feel the need to give in to the extremists’ demands. Moreover, he has suddenly said he thinks a meeting with Biden could avert the crisis, suggesting he is desperate for someone else to find a solution.

Former president Trump has his own problems this evening stemming from the civil case against him, his older sons, and other officers and parts of the Trump Organization in New York, where Attorney General Letitia James has charged him with committing fraud by inflating the value of his assets. Today New York judge Arthur Engoron ruled that Trump and his company deceived banks and insurers by massively overvaluing his real estate holdings in order to obtain loans and better terms for deals. The Palm Beach County assessor valued Mar-a-Lago, for example, at $18 million, while Trump valued it at between $426 million and $612 million, an overvaluation of 2,300% (not a typo).

Engoron canceled the organization’s New York business licenses, arranged for an independent receiver to dissolve those businesses, and placed a retired judge into the position of independent monitor to oversee the Trump Organization.

This decision will crush the heart of Trump’s businesses, and he issued a long statement attacking it, using all the usual words: “witch hunt,” “Communist,” “Political Lawfare” (ok, I don’t get that one), and “If they can do this to me, they can do this to YOU!” Law professor Jen Taub commented, “It reads better in the original ketchup.” Trump’s lawyers say they are considering an appeal. The rest of the case is due to go to trial early next month.

Finally, today, the Supreme Court rejected Alabama’s request to let it ignore the court’s order that it redraw its congressional district maps to create a second majority-Black district. Alabama will have to comply with the court’s order.

LETTERS FROM AN AMERICAN

HEATHER COX RICHARDSON

#Letters from an American#Heather Cox Richardson#political#big money#corruption#anti-trust#the Public Good#TFG#FTC#government shutdown#Daily Don

12 notes

·

View notes

Text

Welcome to BIG, a newsletter on the politics of monopoly power. If you’re already signed up, great! If you’d like to sign up and receive issues over email, you can do so here.

Today, as the U.S. is drawn into wars in Israel and Ukraine, as well as the defense of now-peaceful Taiwan, I’m writing about war. Not the policy choices, or whether U.S. military power is a net force for good or ill, but the actual practical machinery behind the American defense base that produces the weaponry necessary to sustain the military.

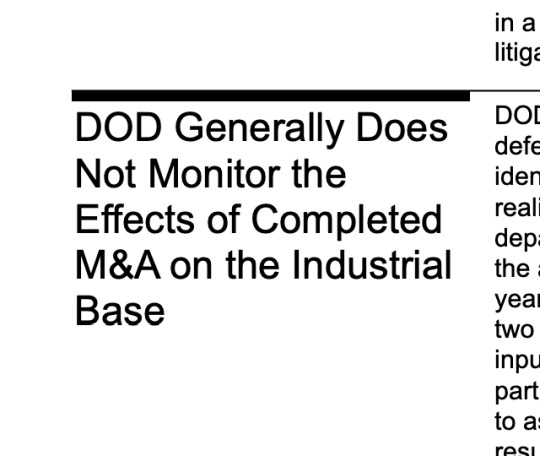

As stockpiles dwindle, there is now widespread agreement among policymakers that America must rebuild its capacity to arm itself and its allies. But according to a new scorching government report released this week, that’s mostly just talk. The Pentagon doesn’t bother tracking the guts of defense contracting, which is who owns the mighty firms that build weaponry.

But first, I have a personal announcement. I am going on leave this week, and I’ve hired a colleague named Lee Hepner to take over for BIG while I am out. You are in for a treat. Hepner works with me at the American Economic Liberties Project. He’s a lawyer with over a decade's worth of policy and political experience at the state and local level, and when I have a question on the law or procedure, Hepner’s one of my go-to people. He’s drafted important legislation, and has recently been focusing on the airline industry, labor issues, and a lot of the major antitrust litigation I've written about here, including the trials of the Meta-Within merger, the Microsoft-Activision acquisition and the Google monopolization case. You're in good hands.

And now, let’s talk the defense base. Here’s an exceptionally boring chart that involves all the money in the world. Welcome to the Pentagon.

One of the more important side stories to the recent wars in Ukraine and Israel, and competition with China over Taiwan, is that the U.S. defense industrial base, composed of 200k plus corporations, is being forced to actually build weapons again. Defense is big business, and since the end of the Cold War, the government has allowed Wall Street to determine who owns, builds, and profits from defense spending.

The consequences, as with much of our economic machinery, are predictable. Higher prices, worse quality, lower output. Wall Street and private equity firms prioritize cash out first, and that means a once functioning and nimble industrial base now produces more grift than anything else. As Lucas Kunce and I wrote for the American Conservative in 2019, the U.S. simply can’t build or get the equipment it needs. There are at this point a bevy of interesting reports coming out of the Pentagon. The last one I wrote up earlier this year showed that unlike the mid-20th century defense-industrial base, today government cash goes increasingly to stock buybacks rather than actual armaments. And now, with a dramatic upsurge in need for everything from missiles to artillery shells to bullets, we’re starting to see cracks in the vaunted U.S. military.

The signs are unmistakable. In Ukraine, fighters are rationing shells. Taiwan can’t get weapons it ordered years ago. The Pentagon has put together a secret team to scour stockpiles to find high-precision armaments in demand on every battlefield and potential battlefield. But the problem goes beyond national defense. In Lake City, Missouri, the largest small arms ammunition plant in the world has decided all ammo production is going to the military, meaning that there is going to be a domestic shortage for hunters, sportsmen, and maybe even police. This shortage may look like a story of a sudden surge in demand, but it’s actually, as Elle Ekman wrote in the Prospect in 2021, a story of consolidation and de-industrialization.

Surges due to wars aren’t new, and there’s always some time lag between the build-up and the delivery. But today, the lengths of time are weirdly long. For instance, the Army is awarding contracts to RTX and Lockheed Martin to build new Stinger missiles, which makes sense. But the process will take.. five years. Why? What is new is Wall Street’s role in weaponry. We used to have slack, and productive capacity, but then came private equity and mergers. And now we don’t. The government can’t actually solicit bids from multiple players for most major weapons systems, because there’s just one or two possible bidders. So that means there’s little incentive for firms to expand output, even if there’s more spending. Why not just raise price?

But don’t take my word for it, take that of the Pentagon. In 2022, the DOD reported that “that consolidation of the industrial base reduces competition for DOD contracts and leads DOD to rely on a more limited number of suppliers. This lack of competition may in turn increase the risk of supply chain gaps, price increases, reduced innovation, and other adverse effects.” And that’s why, more than a year into the Ukraine conflict, the ramp-up is still not where it needs to be.

This week, the Government Accountability Office (GAO), which is a Congressional office charged with investigating problems in government and business, explained why. The GAO came out with a report on how the Pentagon is doing essentially zero oversight of Wall Street’s acquisitions of defense contractors. The title is as boring as you’d expect, designed to have few people pay attention, but offering a red-alert to procurement officials.

The report is simply jaw-dropping. Despite all the chatter about consolidation at high levels within the Pentagon, and in Congress, the bureaucracy has made essentially no progress whatsoever. For instance, we have a trillion dollar defense budget, but there are just two people in the Department of Defense who look at mergers in the defense base. You couldn’t staff the morning shift of a small coffee shop with that, and yet two people are supposed to look at the estimated four hundred mergers plus going on every year among defense contractors and subcontractors.

Four hundred mergers every year is a lot, but of course, that’s just an estimate. Why don’t we know how many acquisitions happen in the defense base? As it turns out, it’s an estimate because the Pentagon isn’t tracking defense mergers anymore. To put it in boring GAO-speak, Pentagon“officials could not say with certainty how many defense-related M&A now occur annually because they no longer track or maintain data on all M&A in the defense industrial base.” So the DOD is almost totally blind to the corporate owners of contractors and subcontractors, which might be one reason that, say, Chinese alloys are being discovered in sensitive weapons systems like the state of the art F-35.

It gets worse. There’s no policy or guidance on mergers, and DOD doesn’t even require contractors or subcontractors to tell them that there is new ownership when an acquisition occurs. In fact, the Pentagon relies on public news to learn of mergers. They often do not know that the mergers are going on, or that the Federal Trade Commission is reviewing them. When big mergers happen, even if the Pentagon is concerned, no one tracks what happens after it closes. They do no analysis of industry sectors, as their “M&A office is not collecting robust data or conducting recurring trend analyses that could help them identify M&A in risky areas of consolidation among defense suppliers.”

The Pentagon’s head-in-the-sand approach is why Lockheed now has a chokehold on nuclear missile modernization, since it bought the key supplier of rocket engines and denies those engines to rivals bidding for the contract to upgrade what is known as the nuclear triad.

So how does the U.S. government manage defense base mergers? Well, the Pentagon defers to the antitrust agencies to look solely at competition. “While DOD policy directs Industrial Base Policy and DOD stakeholders to assess other types of risks, such as national security and innovation risks,” wrote the GAO, “they have not routinely done so.” Basically, dealing with their own defense base is someone else’s job.

What I found most useful about the GAO report is the Pentagon’s response, a classic bureaucratic hand wave. The DOD agreed with all the conclusions of the GAO. It should track mergers and what happens afterwards, it should have more personnel doing so, it should consider national security aspects of corporate combinations, and it should have clear policy on mergers. But it doesn’t. The DOD says it will have a better strategy to deal with mergers… by 2024. Basically, you’re right, but it’s not our problem.

Every day, it seems like political leaders and consultants are saying it’s time to really get that arsenal of democracy going, and to re-industrialize for real. It’s quite possible to get a lot done. The FTC and DOJ now have significant amounts of national security-related information on mergers due to a Congressional change in pre-merger notification laws in 2022, so the DOD could easily do a better job of tracking what’s happening in the defense base.

More to the point, the Pentagon is very powerful. The Deputy Secretary of Defense, Kathleen Hicks could simply start smashing heads on competition and begin telling contractors that if they don’t shape up, she will start an internal war against them. Or the head of the Armed Services Committees could threaten the cushy cash flow that leads to record stock buybacks among contractors, if the ramp-up doesn’t start. Or they could grant antitrust authority for the DOD straight-up, which would rely on a national security standard that allows widespread corporate restructuring without the long slog of a court case. There are many paths.

But if you actually look at the guts of the bureaucracy, nothing is happening, because doing something about our industrial base means thwarting Wall Street, and that’s generally not something that’s considered on the table among normie policymakers. Giant bureaucracies are hard to change, but they are not immovable. One of the ways that you know a previously non-functional bureaucracy is on the right track is, ironically, if there is bitter infighting and anger among staff, who are being tasked to do things differently. But as the GAO showed this week, that’s just not happening in the Pentagon, or at least, not happening nearly fast enough.

And that’s why America is increasingly out of ammunition.

#military industrial complex#us military#nato#ukraine#israel#capitalism#economics#wall street#finance capitalism#finance capital#lockheed martin

7 notes

·

View notes

Text

Nintendo vs. Sega: The Console Wars of the '90s

In the world of '90s gaming, two names ruled the roost: Nintendo and Sega. This was an era of fierce competition, iconic games, and significant financial ups and downs for both companies. Let’s dive into how these gaming giants fared in terms of hardware and software sales, IP franchises, and overall financial status during this pivotal decade.

Nintendo: The Reigning Champ

Nintendo, already a dominant force in the video game industry, reached its pinnacle in the mid-90s. They were the top seller and producer of video games and game units worldwide. In 1997, Nintendo's net income peaked at $528 million, marking its zenith in profitability. This success was fueled by the widespread popularity of their gaming consoles and the billionth game sale achieved in 1995.

The strategy was simple but effective: affordable consoles like the NES at $100, coupled with a steady stream of high-priced game cartridges ranging from $25 to $45 each. The sales figures were staggering - 7 million N64 machines, 46 million Super Nintendos, 60 million Game Boys, and 62 million NES consoles, with hundreds of millions of games sold for these platforms.

Sega: A Challenger’s Turmoil

Sega, meanwhile, experienced a rollercoaster ride through the 90s. They saw rapid growth early in the decade, with revenue reaching ¥347 billion in FY1993, thanks in part to the success of titles like Sonic the Hedgehog on the Genesis platform. However, by the second half of 1993, Sega faced a sharp revenue decline in key markets like North America and Europe.

The Sega Saturn, launched to compete with Nintendo's offerings, failed to capture the market. It sold 9.26 million units globally but was considered a commercial failure, especially in the U.S., where it was discontinued in 1998. Sega's financial situation worsened by the end of the decade, with a net loss of ¥43.3 billion in the fiscal year ending March 1998, and a further consolidated net loss of ¥35.6 billion.

The IP Franchise Battle

Both companies had strong IP franchises. Nintendo’s Mario Brothers and Donkey Kong were pivotal to its success, consistently driving high sales. Sega, while also relying on its own software, increasingly turned to third-party titles on its Genesis platform. By 1994, Sega was earning around $90 million in royalties annually from these third-party games. However, these royalties were less profitable than sales from their own titles, indicating a different strategic approach compared to Nintendo.

Final Financial Showdown

The financial state of both companies in the 90s can be summarized as a tale of two strategies. Nintendo maintained steady profitability and market dominance, while Sega experienced initial growth followed by a significant decline. In terms of net income, Nintendo’s peak at $528 million in 1997 starkly contrasts with Sega’s loss of over $327.8 million in the fiscal year ending March 1998.

In conclusion, the 90s were a period of significant achievements and challenges for both Nintendo and Sega. While Nintendo maintained a strong financial and market position throughout the decade, Sega, despite its initial success, faced financial troubles and declining market share, especially in the face of competition from not only Nintendo but emerging players like Sony. This era of console wars left an indelible mark on the gaming industry and shaped the future of both companies in profound ways.

- Raz

4 notes

·

View notes

Text

Master Your Finances: Netsuite Accounting Services

In the fast-paced world of business, effective financial management is paramount to success. Whether you're a small startup or a large corporation, mastering your finances is essential for sustainable growth and profitability. With the advent of technology, businesses now have access to advanced accounting solutions that can revolutionize their financial operations. One such solution is Netsuite Accounting Services, a comprehensive platform designed to streamline financial processes and empower businesses to take control of their finances like never before.

The Power of Netsuite Accounting Services

Netsuite Accounting Services is a cloud-based financial management solution that provides businesses with a wide range of tools and capabilities to manage their finances efficiently and effectively. From general ledger and accounts payable to budgeting and financial reporting, Netsuite offers a complete suite of features designed to meet the diverse needs of modern businesses.

One of the key advantages of Netsuite Accounting Services is its integration capabilities. By consolidating financial data from various sources into a single, centralized platform, Netsuite enables businesses to gain real-time visibility into their financial performance. This holistic view allows businesses to make informed decisions, identify trends, and proactively address potential challenges.

Streamlined Financial Processes

One of the hallmarks of Netsuite Accounting Services is its ability to streamline financial processes and automate repetitive tasks. With features such as automated invoice generation, expense tracking, and bank reconciliation, Netsuite helps businesses reduce manual errors, improve efficiency, and free up valuable time and resources.

Moreover, Netsuite's cloud-based architecture ensures that financial data is always up-to-date and accessible from anywhere, at any time. This flexibility enables businesses to stay agile and responsive in today's dynamic business environment, whether they're in the office or on the go.

Advanced Reporting and Analytics

In addition to streamlining day-to-day financial operations, Netsuite Accounting Services offers advanced reporting and analytics capabilities that empower businesses to gain deeper insights into their financial performance. With customizable dashboards, real-time reporting, and predictive analytics, Netsuite enables businesses to track key metrics, monitor KPIs, and make data-driven decisions with confidence.

Furthermore, Netsuite's robust reporting tools allow businesses to generate a wide range of financial reports, from balance sheets and income statements to cash flow forecasts and profitability analysis. This comprehensive reporting functionality provides businesses with the visibility and transparency they need to effectively manage their finances and drive growth.

Scalability and Flexibility

Whether you're a small startup or a multinational corporation, Netsuite Accounting Services offers scalability and flexibility to meet your evolving needs. With customizable workflows, configurable dashboards, and a modular architecture, Netsuite can be tailored to fit the unique requirements of businesses across industries and geographies.

Moreover, Netsuite's cloud-based platform ensures that businesses can easily scale up or down as needed, without the need for costly infrastructure investments or IT overhead. This scalability and flexibility make Netsuite Accounting Services an ideal solution for businesses of all sizes, from startups looking to streamline their financial operations to established enterprises seeking to drive innovation and growth.

Conclusion

In today's increasingly competitive business landscape, mastering your finances is essential for success. Netsuite Accounting Services offers businesses a comprehensive suite of tools and capabilities to streamline financial processes, gain deeper insights, and drive growth. From automated invoicing and expense tracking to advanced reporting and analytics, Netsuite empowers businesses to take control of their finances and achieve their goals with confidence. Whether you're a small startup or a large corporation, Netsuite Accounting Services can help you master your finances and unlock your full potential.

0 notes

Text

Maximizing Efficiency: The Benefits of Shopify ERP Integration Services

In the bustling world of e-commerce, efficiency is key to maintaining a competitive edge. Online businesses, particularly those using Shopify, often find themselves juggling various processes and systems to keep everything running smoothly. This is where integrating Enterprise Resource Planning (ERP) systems with Shopify can make a significant impact. By unifying different business operations under one system, companies can achieve greater efficiency, improved data accuracy, and enhanced overall performance. In this blog, we'll delve into the benefits of Shopify ERP integration services and highlight why Oyecommerz is an excellent choice for facilitating this integration.

What is Shopify ERP Integration?

Shopify is a popular e-commerce platform known for its ease of use, powerful features, and extensive app ecosystem. However, as businesses scale, managing multiple aspects of operations manually can become overwhelming and prone to errors. Enterprise Resource Planning (ERP) systems come to the rescue by consolidating various functions such as inventory management, order processing, customer relationship management (CRM), and accounting into a single, integrated system.

Integrating Shopify with an ERP system allows for seamless data flow between your online store and backend operations. This means real-time updates, automated processes, and a holistic view of your business operations, which are crucial for making informed decisions and optimizing performance.

The Benefits of Integrating Shopify with ERP

Centralized Data Management: One of the primary advantages of integrating Shopify with an ERP system is centralized data management. All your business data—from sales and inventory to customer information and financial records—is stored in one place. This centralization eliminates data silos, ensuring consistency and accuracy across all departments.

Enhanced Inventory Management: With ERP integration, you gain real-time visibility into your inventory levels. This helps prevent overstocking or stockouts, ensuring that you always have the right amount of stock on hand. Improved inventory management leads to better customer satisfaction and optimized storage costs.

Streamlined Order Processing: ERP integration automates the order processing workflow. Orders placed on your Shopify store are automatically synced with the ERP system, reducing the need for manual data entry and minimizing the risk of errors. This automation speeds up order fulfillment, enhancing efficiency and customer satisfaction.

Accurate Financial Management: ERP systems come with robust financial management tools. Integrating these tools with Shopify ensures that all sales, expenses, and financial transactions are accurately recorded and easily accessible. This integration simplifies accounting processes, improves financial reporting, and aids in better financial planning and analysis.

Improved Customer Relationship Management: ERP systems often include CRM functionalities. By integrating Shopify with an ERP system, you can manage customer information, track interactions, and analyze customer behavior more effectively. This data can be used to personalize marketing strategies, improve customer service, and foster stronger customer relationships.

Scalability and Flexibility: As your business grows, handling operations manually can become increasingly challenging. ERP systems are designed to scale with your business, managing increased data volume and complexity without compromising efficiency. Integrating Shopify with an ERP system ensures that your operations remain smooth and efficient, even as your business expands.

How Oyecommerz Facilitates Seamless Shopify ERP Integration ?

Integrating Shopify with an ERP system can be a complex task, especially for businesses with extensive product catalogs and unique operational requirements. This is where Oyecommerz excels. As a leading provider of e-commerce solutions, Oyecommerz specializes in migration and integration development services, ensuring a seamless and efficient integration process.

Here’s why Oyecommerz stands out as the ideal partner for your Shopify ERP integration:

Expertise and Experience: Oyecommerz boasts a team of seasoned professionals with deep expertise in e-commerce platform integrations. Their experience with both Shopify and various ERP systems ensures that every aspect of the integration is handled with precision and expertise.

Customized Integration Solutions: Recognizing that each business has unique needs, Oyecommerz offers tailored integration solutions. They work closely with clients to understand their specific requirements and develop customized strategies that align with their business goals. This personalized approach ensures that the integration process addresses all of your operational needs.

Efficient and Accurate Integration: Minimizing downtime during integration is crucial to maintaining business operations. Oyecommerz prioritizes efficiency and accuracy, ensuring that your store’s data—including products, customer information, and order history—is seamlessly integrated with your ERP system with minimal disruption.

Comprehensive Support and Maintenance: Oyecommerz’s commitment doesn’t end with the integration process. They provide ongoing support and maintenance services to help you optimize your Shopify-ERP integration for long-term success. Whether it's troubleshooting issues or implementing new features, Oyecommerz is dedicated to your store’s continuous improvement.

Post-Integration Optimization: Beyond the initial integration, Oyecommerz offers continuous optimization services. They monitor the performance of your integration, provide insights, and recommend strategies to maximize your sales and operational efficiency. This proactive approach ensures that your business can adapt and thrive in a constantly changing e-commerce landscape.

Conclusion: Unlocking Efficiency with Shopify ERP Integration

In the competitive world of e-commerce, efficiency is a crucial factor for success. Integrating Shopify with an ERP system provides numerous benefits, from centralized data management and enhanced inventory control to streamlined order processing and accurate financial management. This integration not only boosts operational efficiency but also equips you with valuable insights to drive business growth.

Choosing Oyecommerz for your Shopify ERP integration ensures that the process is smooth, efficient, and tailored to your specific needs. Their expertise, personalized solutions, and comprehensive support make them the perfect partner for businesses looking to enhance their e-commerce operations through ERP integration.

Integrating an ERP system with your Shopify store can significantly improve how you manage your business. At Oyecommerz, we provide seamless Shopify ERP integration services, Magento to Shopify Migration Services, bringing together various business operations like inventory management and financial accounting into one unified system. Our team of seasoned experts collaborates with you to understand your unique requirements and develop customized integration strategies that enhance efficiency and ensure accurate data management. With Oyecommerz, you can streamline your Shopify operations, achieve real-time data synchronization, and minimize disruptions, turning your online store into an efficient business tool.

Embrace the opportunity to maximize your business efficiency with Shopify ERP integration, and let Oyecommerz be your trusted partner throughout the journey. Together, you can unlock new possibilities for your business and secure long-term success in the ever-evolving e-commerce landscape.

#ecommerce#erp#enterprise resource planning#oyecommerz#shopify#integration#migration#online store#development

0 notes

Text

Current Landscape of Resist Salt Manufacturers in India

The chemical manufacturing sector in India is a pivotal part of the country's industrial framework, with resist salt playing a significant role in the textile and dyeing industries. Resist salt, a critical component used in the dyeing process to produce specific patterns and resist dyeing effects on fabrics, has seen substantial growth in demand both domestically and internationally. This article delves into the current landscape of resist salt manufacturers in India, exploring the industry's dynamics, challenges, and the competitive environment.

Industry Overview

India stands as one of the leading producers of resist salt, thanks to its robust textile industry, which is one of the largest in the world. The resist salt manufacturers of India cater not only to the local market but also export to countries in Europe, Asia, and the Americas. The industry's growth is fueled by the expansion of textile manufacturing and the increasing demand for high-quality and diverse fabric patterns which require specialized chemical treatments.

Major Players and Market Structure

The market for resist salt in India is moderately consolidated with a few key players dominating the industry. These companies are equipped with advanced manufacturing facilities and have extensive distribution networks both within and outside India. Companies like Bodal Chemicals, Colourtex, and Atul Ltd are some of the prominent names in this sector. These manufacturers have established a strong foothold in the market by continuously investing in research and development to improve product quality and by adapting to the latest environmental regulations.

Technological Advancements

Technological innovation is a significant driver in the resist salt market. Indian manufacturers are increasingly adopting advanced technologies to enhance the efficiency of their production processes and to reduce waste. Automation and data analytics are becoming integral parts of manufacturing operations, enabling companies to optimize their production lines and improve quality control. Moreover, there is a growing focus on developing eco-friendly manufacturing processes that minimize the environmental impact of production, responding to global demands for sustainable practices.

Challenges Facing the Industry

Despite the growth prospects, resist salt manufacturers in India face several challenges. One of the primary concerns is the fluctuation in raw material prices, which can significantly impact production costs and profit margins. Additionally, environmental regulations are becoming stricter, requiring manufacturers to invest more in pollution control technologies and waste management systems, further increasing operational costs.

Competition from other low-cost producing countries also poses a significant challenge, as these competitors can undercut prices, making market conditions more intense. Indian manufacturers need to continually innovate and improve their efficiency to maintain their competitive edge in the global market.

Regulatory Environment

The Indian government has implemented several regulations that impact the chemical manufacturing sector, including those specific to the production of resist salt. Compliance with these regulations is crucial for manufacturers to ensure continued operations. These regulations are designed to ensure safe production practices, reduce environmental impact, and protect worker health and safety.

Future Outlook

Looking ahead, the future of resist salt manufacturers in India appears promising, driven by the growth of the textile industry and increasing exports. However, success will depend on the ability of these manufacturers to adapt to changing market dynamics, embrace technological advancements, and meet regulatory requirements. Investing in sustainable practices will also be crucial, as global markets increasingly favor environmentally friendly products.

In conclusion, the landscape of resist salt manufacturers in India is characterized by both opportunities and challenges. With strategic planning, continuous innovation, and adherence to regulatory standards, Indian manufacturers can not only sustain but also potentially expand their market share both domestically and internationally. As the industry moves forward, it will be interesting to see how the leading players navigate these complexities and capitalize on the emerging opportunities in the global textile chemical market.

0 notes

Text

Unveiling Success: Case Studies in SAP Decommissioning

Introduction:

In the realm of enterprise IT, SAP systems are often regarded as the backbone of operations, facilitating critical business processes and data management. However, as organizations evolve and modernize, the need to decommission outdated SAP systems becomes increasingly apparent. In this blog, we delve into real-world case studies of SAP decommissioning initiatives, highlighting the lessons learned, challenges overcome, and the success stories that emerged.

Streamlining Operations Through SAP Decommissioning

Company XYZ, a global manufacturing conglomerate, embarked on a journey to streamline its IT infrastructure and reduce operational costs. With a multitude of legacy SAP systems running on outdated hardware, the company faced inefficiencies and maintenance challenges. By leveraging SAP decommissioning services, Company XYZ successfully retired redundant systems, consolidated data, and migrated critical functions to modern platforms. As a result, the organization streamlined operations, enhanced agility, and realized significant cost savings.

Key Lessons Learned:

Thorough planning is essential: Company XYZ invested time and resources in conducting a comprehensive assessment of its SAP landscape, identifying redundant systems, and prioritizing decommissioning efforts.

Stakeholder alignment is critical: Engaging key stakeholders, including business users, IT teams, and executive leadership, ensured buy-in and support for the decommissioning initiative.

Data migration requires meticulous attention: Careful planning and execution of data migration activities ensured data integrity, security, and accessibility throughout the decommissioning process.

Enabling Digital Transformation Through SAP Decommissioning

Company ABC, a leading financial services provider, recognized the need to modernize its IT infrastructure to support digital transformation initiatives. With multiple legacy SAP systems hindering agility and innovation, the organization embarked on a comprehensive SAP decommissioning project. By retiring outdated systems, migrating data to modern platforms, and embracing cloud-based solutions, Company ABC enabled digital innovation, enhanced customer experiences, and gained a competitive edge in the market.

Key Lessons Learned:

Embrace innovation opportunities: SAP decommissioning presents an opportunity to modernize IT infrastructure, embrace emerging technologies, and drive digital transformation initiatives.

Collaboration is key: Cross-functional collaboration between IT, business, and external partners facilitated the successful execution of SAP decommissioning activities.

Measure success and iterate: Continuous monitoring and evaluation of decommissioning efforts enabled Company ABC to measure success, identify areas for improvement, and iterate on its digital transformation strategy.

Success Stories:

Both Company XYZ and Company ABC achieved remarkable success through their SAP decommissioning initiatives. By retiring legacy SAP systems, streamlining operations, and embracing digital transformation, these organizations unlocked new opportunities for growth, innovation, and competitiveness in today's dynamic business landscape.

Conclusion:

The case studies of Company XYZ and Company ABC serve as compelling examples of the transformative power of SAP decommissioning. By learning from their experiences, organizations can glean valuable insights, overcome challenges, and chart a course towards successful legacy system retirement. With careful planning, stakeholder engagement, and a commitment to innovation, organizations can unlock the full potential of SAP decommissioning and pave the way for a brighter, more agile future.

1 note

·

View note

Text

Navigating Global Trade: The Vital Role of Freight Forwarders

In the complex ecosystem of global trade, freight forwarders emerge as indispensable orchestrators, seamlessly connecting businesses with markets around the world. With expertise in logistics, customs regulations, and supply chain management, these unsung heroes play a crucial role in facilitating the movement of goods across borders. Let's explore the multifaceted world of freight forwarders and their pivotal contributions to international commerce.

The Backbone of Global Trade

At the heart of international commerce, freight forwarders serve as the backbone of supply chains, ensuring the efficient and timely transportation of goods from origin to destination. Whether it's shipping raw materials for manufacturing, distributing finished products to retailers, or delivering goods to consumers' doorsteps, freight forwarders manage the intricate logistics involved in moving cargo across air, sea, and land.

Expertise in Logistics and Supply Chain Management

Freight forwarders possess specialized knowledge and expertise in logistics and supply chain management, enabling them to navigate the complexities of global transportation networks with precision and efficiency. From selecting the optimal mode of transport to coordinating warehousing, packaging, and distribution, these professionals orchestrate end-to-end solutions tailored to the unique needs of each shipment.

Customized Solutions for Diverse Industries

One of the key strengths of freight forwarders lies in their ability to provide customized solutions for diverse industries and market sectors. Whether it's automotive, pharmaceuticals, electronics, or perishable goods, freight forwarders leverage their industry-specific knowledge and resources to design tailored logistics solutions that meet the unique requirements of each client.

Managing Regulatory Compliance

Navigating the labyrinth of customs regulations and international trade laws can be daunting for businesses engaged in cross-border trade. Freight forwarders serve as trusted advisors, guiding clients through the intricacies of regulatory compliance and documentation requirements. By staying abreast of changing regulations and maintaining strong relationships with customs authorities, freight forwarders help businesses avoid costly delays and penalties.

Enhancing Efficiency and Cost Savings