#TaxChanges

Text

Self-employed?

Get ready for a tax game-changer! The House just approved a $78B bill boosting child tax credits, tweaking ERC, and supporting small businesses. Stay tuned for more! 💼🌟

0 notes

Text

Tax Return Amendment Time Limits: Your Financial Future Demystified

#TaxReturn#Amendment#FinancialFuture#TaxRefund#IRS#TaxTips#TaxPlanning#TaxFiling#FinanceAdvice#IncomeTax#TaxDeadline#TaxSeason#MoneyManagement#FinancialPlanning#TaxLaw#IRSUpdates#PersonalFinance#TaxChanges#Taxation#FinancialEducation

0 notes

Text

Tax Changes for Cryptocurrency Holders from FASB

Hi all!

Somehow, the news about the approval of new tax rules in the United States for the companies holding digital assets slipped past. Meanwhile, in my opinion, these changes catalyze the influx of investments into the crypto industry.

The point is that now companies owning cryptocurrencies evaluate them based on the value of the coin that was fixed upon purchase. And they are allowed to write off losses only if the price falls below the purchase price.

It turns out that, for example, a company bought 1000 BTC a year ago at a price of $16 thousand. And today, when its price is $26 thousand, it is still on the company’s balance sheet at a price of $16 thousand. That is, real capitalization has increased, but according to securities it has not.

Now, starting in 2025, companies in reporting periods will calculate the value of cryptocurrency based on the market value at the time of reporting. Consequently, they will be more transparent to investors.

An illustrative example is one of the largest BTC holders, MicroStrategy. As of the end of the second quarter of this year they had 152,300 BTC on their balance sheet; their reported dollar amount was $2.3 billion and the real price was almost 50% more.

The innovation will affect all companies that have crypto assets on their balance sheets. This will become mandatory from December 15 next year but if you wish you can switch to the new rules now.

At the FASB meeting, where it was decided (unanimously, by the way) to change tax rules, the issue regarding NFTs was separately considered. Everything here remains unchanged for now.

Why do I think this is good news? Well, imagine that you are an investor, you decided to invest in crypto, you come to a specialized company, they tell you: in three years we have earned millions on bitcoins. But the official reports show completely different figures - two or three years ago. Why do you need to delve into these tax jungles? You will find other investment projects in traditional markets where everything is clear. So I dare to assume that by the end of the year the number of investments in the crypto market will increase significantly.

0 notes

Text

🚀 Exciting Tax Updates for 2024! 🚀

Hello @lawyer2ca community! 🌐

Get ready for a transformative year ahead as we bring you the latest scoop on the 15 game-changing tax amendments for 2023 that are set to redefine your financial landscape in 2024! 💼💸

Here's a quick rundown:

1-New Tax Regime Slabs: Revamped to be more enticing, offering a boon to those unable to invest in tax-saving instruments previously.

2-Hike in Basic Exemption Limit: Save up to Rs 15,000 with the basic exemption limit under the new tax regime raised to Rs 3 lakh.

3-Default Tax Regime: The new tax regime becomes the default choice from April 1, 2023. Opt for the old regime if you seek common tax deductions.

4-Increased Rebate under Section 87A: Enjoy a higher rebate of Rs 25,000 under section 87A for taxable income up to Rs 7 lakh.

5-Standard Deduction in New Tax Regime: Salaried individuals with up to Rs 7.5 lakh taxable income benefit from a Rs 50,000 standard deduction.

6-No LTCG Benefit in Debt Mutual Funds: Post March 31, 2023, investments in debt mutual funds lose Long Term Capital Gains (LTCG) tax benefits.

7-Marginal Tax Relief for Small Taxpayers: A sigh of relief for individuals with slightly exceeding Rs 7 lakh taxable income.

8-Reduced Surcharge Rates: The highest surcharge rate for those earning over Rs 5 crore reduced from 37% to 25%.

9-Increased Tax Exemption on Leave Encashment: Non-government employees can now enjoy tax exemption on leave encashment up to Rs 25 lakh.

10-New Rules for Rent-Free House Salary: The CBDT introduces fresh rules for rent-free accommodations, potentially lowering TDS.

11-Tax on Maturity Amount from Non-ULIP Life Insurance Policies: Maturity amounts exceeding Rs 5 lakh are now taxable for non-ULIP life insurance policies issued after April 1, 2023.

12-Limit on Capital Gains Deductions from Property Sale: A cap of Rs 10 crore on maximum deductions from property sales.

13-Discard ITR Option: Introducing the Discard return option, allowing deletion of unverified ITR submissions.

14-TDS on Online Game Winnings: TDS on online game winnings is now applicable without any threshold, at a rate of 30%.

15-Relief on Higher TDS for Non-ITR Filers: Non-mandatory ITR filers won't face higher TDS on bank FDs, dividend income, and specified incomes.

Stay ahead of the curve and ensure your financial strategy aligns with these changes! 💡💼✨

For detailed insights, connect with our tax experts.

#Tax2024 #FinancialFreedom #TaxChanges #StayInformed #Lawyer2CA 📊🔍

1 note

·

View note

Text

Corporation tax for limited Company

A little reminder goes a long way, following the corporation tax changes that were effective from April 2023 find out more details about Corporation Tax and ensure your company's tax planning is on point!

🌐For More Details: https://www.dnsassociates.co.uk/blog/how-much-is-corporation-tax-for-a-limited-company

CorporationTax #TaxChanges #UKBusiness #TaxPlanning #topaccountingfirmsuk #personaltaxaccountantuk #taxadvisoruk #uktaxadvice #ukaccountingfirms #taxaccountantuk #ukpropertyaccountants #uktaxconsultant #ukpropertyaccountants

0 notes

Text

JR Cecil, Liberty Tax 04.19.21

0 notes

Text

Taxability of Dividends – NRIs

Taxability of Dividends in case of NRIs:

Further to the article on NRI residential status, there were a couple of queries raised by the readers on the taxability of dividends. Here are some of those queries and answers for the benefit of the readers.

Are dividends received by NRIs from Indian shares/mutual funds taxable in India?

Till 31 Mar 2020, dividend income from an Indian source was completely exempt in the hands of NRIs. However, from 01 April 2020, such dividends would be taxable in India and NRIs would need to pay tax at applicable rates. If there is a Double Taxation Avoidance Agreement (DTAA/tax treaty) between India and the country of residence, a beneficial rate as per the treaty could be applied. Taking the UK as an example, most dividends are taxed at 10% as per India-UK DTAA. This is subject to the availability of TRC from the country of residence.

What is TRC? Is it mandatory to avail treaty relief?

TRC stands for Tax Residency Certificate. This will be issued by the tax authorities of the respective country certifying that the individual NRI is a resident of such country. Most countries have a specific form prescribed for this purpose and an NRI who wishes to avail the treaty benefit would need to apply for the same to the respective country’s tax authorities. As per the Indian tax laws, TRC is a mandatory document required to avail any treaty relief by a non-resident.

Is withholding tax/Tax Deduction at Source (TDS) applicable in case of dividends paid to NRIs?

Yes, the dividends paid to NRIs would generally be subject to 20% withholding tax in India. However, the actual tax on dividends may vary depending on the total income of an individual and applicable slab rates. So, the differential taxes would get adjusted at the time of filing the tax return.

Can an NRI avail the beneficial rate as per the treaty at the time of tax withholding itself?

Yes. An NRI can avail of the beneficial rate on dividends at the time of tax withholding. In order to avail this, the individual needs to submit the TRC and other prescribed documents to the company. Some companies are contacting individual shareholders to confirm their residential status and other documentation to avail of the treaty benefit. Please ensure that this information is submitted to the companies so that the beneficial rate is availed at the time of withholding itself. In this way, refunds on the tax return could be avoided as well.

Can an NRI avail Foreign Tax Credit in his home country on taxes paid on dividends in India?

Generally, yes. However, this may also depend on any specific conditions/documentation requirement specified in the tax treaty or domestic tax laws of such resident country. It is advisable to go through the same and ensure that those requirements are met before availing the credit.

The write-up is for general understanding. We suggest the readers to discuss with their CAs before deciding on tax implications.

AUTHOR:

A S Amarnatha B.com, FCA, LLB

Amar is a practicing Chartered Accountant specializing in the field of NRI and expat taxation. His expertise includes various facets of global mobility like expatriate tax, DTAA, social security, ESOPs etc. He is also specialized in US individual taxation both from expat and foreign national tax compliances perspectives. He can be contacted at [email protected].

#nriresidentialstatus#dividend#tax#taxability#foreigntax#taxcredit#NRI#nritax#tds#trc#incometax#incometaxindia#finance#accounting#taxchanges#taxrates#dailyeconomics#asamarnatha

0 notes

Video

youtube

Stamp Duty in Property

Subscribe to our Youtube Channel: https://www.youtube.com/channel/UCDyqt_09GG8BsC7wtma_2FQ

‘The Property Coach’ Book for FREE! Click Here: https://arancurry.clickfunnels.com/opt-inrfyrdf8v

If you liked this video, you will love our video all about tax and the tax changes. Click here to watch now: http://arancurry.co.uk/taxweb

To find out more about Aran Curry and the brilliant education he has to offer, click here to visit our website: http://arancurry.co.uk/

Summary

In this video, Aran discusses the stamp duty changes for property investors that came into place in April 2016 and why this shouldn’t stop you investing!

Transcript

Hi and welcome to this short video where I’m going to talk to you about stamp Duty in property.

In April 2016 the stamp duty rules changed for property investors who were looking to buy what they defined as a second property or third property, or anything that was on top of your residential property. In very basic terms, how does stamp duty work? Well first of all, when you buy your first property, normally your residential property for most people. There’s a sliding scale that defines the amount of stamp duty that you should pay, for example, up to £125,000, you don’t pay any stamp duty. There’s 0 to pay. Between £125,000 and £250,000 you pay 2% of whatever value falls in there. For example, if the house is £130,000, that’s an extra £5,000 that’s in that bracket and you’d pay 2% of that, which would be £100, and so on up until £250. Then from £250,000 upwards there’s another bracket, and from £1 million upwards there’s another bracket and so etc. So, that’s how the stamp duty is worked out on a basic purchase. So, what’s the difference between investors? Basically, in April 2016 the government said ‘We want to raise more money and we’re going to raise some of it through landlords’ so they said that whenever you’re buying an investment property, or in effect it’s your name going on the deeds for a second property, whenever you’re doing that then we’ll charge you an extra 3% in stamp duty on whatever the purchase price is. So, basically the new way of working it out from April 2016 is you work it out the standard way and then you take 3% of the price and add it on. If it was a £100,000 house, the standard way is you’d have 0 to pay because anything up to £125,000 is 0, but now we add 3% of the £100,000 on which is £3,000 – that becomes the new bill. So, the new bill is £3,000 more than it would have been. If you’re buying a house, let’s say for £250,000 with the standard way, you will have paid 0 for the first £125,000 and 2% for the next £125,000 so your bill would have been £2,500 – your stamp duty tax bill. But with the new way, you pay 3% extra of that £250,000 which in this example is an extra £7,500 so your stamp duty bill is £10,000 instead of £2,500.

Now, that is not good news, no one likes paying extra taxes, I definitely don’t. We buy 50 properties a month for our clients and it affects all of them, it affects me, it’s not good news. However, what I want to be clear on, I think the government were quite cute with what they did. Although I don’t like it, here’s what they did. They went public and said ‘hey, we’re penalising the landlords’ which is always a vote winner. They also raised more money for the deficit, so they got more money coming in from these stamp duty bills. But, they knew underneath that landlords would keep buying.

What do I mean by that? Well I’m not going to not buy a house. Take that £250,000 house for example, what is that property going to be worth in 10-15 years from now? We know that property prices go up on average 7.9% a year. They have for the last 85 years. So, if I fast forward, normally properties double every 8 years, but let’s say it takes 10-15 years. So that £250,000 house is going to double. So, in 15 years from now it’s going to be worth an extra £250,000. I’d be pretty stupid to say I’m not going to buy it because of this increased stamp duty cost of £7,500 and miss out on £250,000 worth of growth. That would be a bad call! That is something you wouldn’t want to do in the long run logically. So, landlords are going to keep buying, they raise more money, and it was a vote winner for them.

So, bottom line, what’s my message? My message is don’t let the stamp duty changes stop you from buying property. On the continent, there are many countries where, on a purchase, you’ll pay anywhere between 8% and 11% in taxes on any purchase you make. Our stamp duty bills are a lot less than that. The UK property market, phenomenal market, makes great returns, great money for you in terms of cashflow and asset growth if you buy the right houses – you need to buy the right houses by the way and you can watch a few of my other videos to learn how to do that – but if you’re buying the right investment properties and you’re investing in the right place, phenomenal market place, do not let stamp duty get in the way. Go buy, go buy, go buy! But now at least you understand it and you know what you’re playing with.

We’re going to put a link just below this video if you want to see a lot more on taxes and you want to understand taxes in a lot more detail, then you can click on that link and see a whole hour and a quarter long webinar recording where I cover this in a lot more detail. (click here http://arancurry.co.uk/taxweb)

In the meantime invest with knowledge, invest with confidence, create financial freedom. I’ll speak to you soon. Thank you.

#property#propertyinvesting#investing#propertyinvestor#investor#stampduty#stampdutytax#tax#taxchanges#propertytax

1 note

·

View note

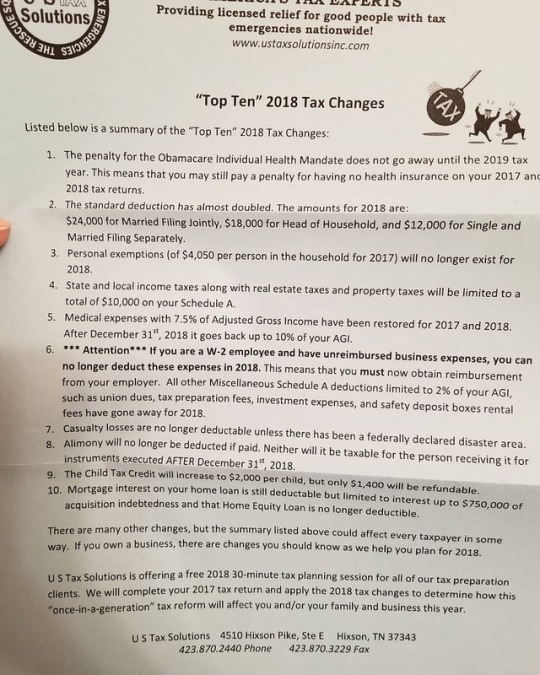

Photo

#FYI #taxreform #taxseason #tax #taxchanges

1 note

·

View note

Link

1 note

·

View note

Text

HSA Limits for 2022

The IRS recently released guidance providing the 2022 inflation-adjusted amounts for Health Savings Accounts (HSAs).

Fundamentals of HSAs

An HSA is a trust created or organized exclusively for the purpose of paying the “qualified medical expenses” of an “account beneficiary.” An HSA can only be established for the benefit of an “eligible individual” who is covered under a “high deductible health plan.” In addition, a participant can’t be enrolled in Medicare or have other health coverage (exceptions include dental, vision, long-term care, accident and specific disease insurance).

A high deductible health plan (HDHP) is generally a plan with an annual deductible that isn’t less than $1,000 for self-only coverage and $2,000 for family coverage. In addition, the sum of the annual deductible and other annual out-of-pocket expenses required to be paid under the plan for covered benefits (but not for premiums) can’t exceed $5,000 for self-only coverage, and $10,000 for family coverage.

Within specified dollar limits, an above-the-line tax deduction is allowed for an individual’s contribution to an HSA. This annual contribution limitation and the annual deductible and out-of-pocket expenses under the tax code are adjusted annually for inflation.

Inflation adjustments for next year

In Revenue Procedure 2021-25, the IRS released the 2022 inflation-adjusted figures for contributions to HSAs, which are as follows:

Annual contribution limitation. For calendar year 2022, the annual contribution limitation for an individual with self-only coverage under a HDHP will be $3,650. For an individual with family coverage, the amount will be $7,300. This is up from $3,600 and $7,200, respectively, for 2021.

High deductible health plan defined. For calendar year 2022, an HDHP will be a health plan with an annual deductible that isn’t less than $1,400 for self-only coverage or $2,800 for family coverage (these amounts are unchanged from 2021). In addition, annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) won’t be able to exceed $7,050 for self-only coverage or $14,100 for family coverage (up from $7,000 and $14,000, respectively, for 2021).

Many advantages

There are a variety of benefits to HSAs. Contributions to the accounts are made on a pre-tax basis. The money can accumulate tax free year after year and be can be withdrawn tax free to pay for a variety of medical expenses such as doctor visits, prescriptions, chiropractic care and premiums for long-term care insurance. In addition, an HSA is “portable.” It stays with an account holder if he or she changes employers or leaves the workforce. If you have questions about HSAs at your business, contact your employee benefits and tax advisors.

===

If you want to talk to us about your personal tax situation, please email us via our contact page and visit our website at www.ablonco.com.

© 2021, all rights reserved.

0 notes

Link

Ref Kare11 - http://ow.ly/FW4D30kNim9

0 notes

Video

Check out the new episode of #rethinkpolitics #obamacarerepeal #taxchanges #government #bougieblackbrothernetwork #ACA #taxreform https://buff.ly/2pIdQx0 (at Chill Room)

0 notes

Photo

Always follow the money trail. #smallbusinesstaxes #taxchanges #taxchanges2018 #smallbusinesstoronto #drwireless #drwirelessrepairs #quickfixtorontoplus

#drwirelessrepairs#drwireless#smallbusinesstaxes#taxchanges#quickfixtorontoplus#smallbusinesstoronto#taxchanges2018

0 notes

Photo

Texas Agriculture Tax Exemption Changes for 2012 ALERT! TEXAS AG TAX EXEMPTION CHANGES!... #surnativa #agriculture #farmtax #ranchtax #taxchanges #taxexemptions #taxexpert #texascomptroller Source: https://surnativa.com/texas-agriculture-tax-exemption-changes-for-2012/?feed_id=27808&_unique_id=5f54e396a43f7

0 notes

Last Seen Blogs

misternobody

Misternobody

suncity888vn

Untitled

moncler-soldes-femme-6-blog

moncler soldes femme - doudoune moncler femme sold

lunarimpact

If ᶦ ᶫᵒᵛᵉ ʸᵒᵘ was a promise

kinowa-wappa

みんなのカフェ