#microfinance software provider

Text

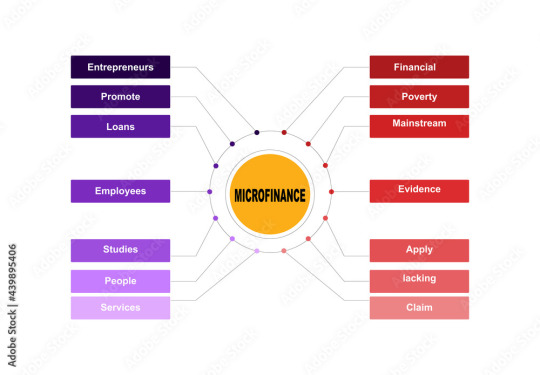

What are the basic features of microfinance

Introduction:

Microfinance plays a crucial role in providing financial services to individuals who are typically excluded from traditional banking systems. It aims to empower entrepreneurs, especially those in low-income communities, by offering them access to credit, savings, and other financial instruments. This article will delve into the basic features of microfinance and shed light on the process of Section 8 Microfinance Company Registration and What are the basic features of microfinance .

Basic Features of Microfinance:

Financial Inclusion: Microfinance focuses on reaching out to individuals who lack access to formal banking channels. This includes marginalized communities, small business owners, and individuals with low income.

Small Loan Amounts: One distinctive feature of microfinance is the provision of small loan amounts. These loans are designed to meet the modest financial needs of borrowers, enabling them to start or expand small businesses.

Collateral-Free Loans: Traditional banking often requires collateral for loan approval. Microfinance, however, typically offers collateral-free loans, making it more accessible to individuals who lack significant assets.

Group Lending: Microfinance often employs a group lending model where individuals form small groups. Each member is jointly responsible for the repayment of loans, creating a support system and fostering a sense of community responsibility.

Interest Rates: Microfinance institutions set interest rates that are reasonable and sustainable for both the institution and the borrower. The goal is to ensure affordability for the borrowers while covering operational costs.

Savings and Insurance: Microfinance institutions not only provide credit but also encourage savings. Additionally, some institutions offer micro-insurance products to protect clients against unforeseen events.

Section 8 Microfinance Company Registration:

Legal Structure: Section 8 of the Companies Act in many jurisdictions allows for the formation of non-profit organizations with the primary objective of promoting commerce, art, science, sports, education, research, social welfare, religion, charity, protection of the environment, or any other charitable objective.

Microfinance Focus: Companies registered under Section 8 with a focus on microfinance adhere to the legal framework while aligning their activities with the mission of promoting financial inclusion and economic empowerment.

Regulatory Compliance: Section 8 Microfinance Company Registration involves adhering to regulatory requirements set by the relevant authorities. This ensures that the microfinance institution operates within the legal framework and maintains transparency in its financial dealings.

Social Impact Reporting: Section 8 companies engaged in microfinance often emphasize social impact reporting, highlighting their contributions to poverty alleviation, entrepreneurship development, and community upliftment.

Conclusion:

Understanding the basic features of microfinance, coupled with the regulatory aspects of Section 8 Microfinance Company Registration, is essential for those aiming to establish or engage with microfinance institutions. By promoting financial inclusion and adopting a socially responsible approach, microfinance plays a pivotal role in fostering economic development and empowerment at the grassroots level.

#microfinance#microfinance software features#microfinance software#benefits of microfinance#parallex microfinance bank#client of microfinance#history of microfinance#md parallex microfinance bank#micro finance software features#online micro finance software features#detail about microfinance software#about microfinance software#online microfinance software#learn about microfinance software#online micro loan software features#microfinance software provider

0 notes

Text

The impact of sustainability in fintech: reflections from the summit

In recent years, the Fintech industry has witnessed a paradigm shift towards sustainability, with an increasing emphasis on integrating environmental, social, and governance (ESG) factors into financial decision-making processes. This transformative trend took center stage at the latest Fintech Summit, where industry leaders converged to explore the intersection of sustainability and financial technology. Among the prominent voices shaping this discourse was Xettle Technologies, a trailblazer in Fintech software solutions, whose commitment to sustainability is driving innovation and reshaping the future of finance.

Against the backdrop of global challenges such as climate change, resource depletion, and social inequality, the imperative for sustainable finance has never been greater. The Fintech Summit provided a platform for thought leaders to reflect on the role of technology in advancing sustainability goals and fostering a more resilient and equitable financial ecosystem.

At the heart of the discussions was the recognition that sustainability is not just a moral imperative but also a strategic imperative for Fintech firms. By integrating ESG considerations into their operations, products, and services, Fintech companies can mitigate risks, enhance resilience, and unlock new opportunities for growth and value creation. Xettle Technologies’ representatives underscored the company’s commitment to sustainability, highlighting how it is embedded in the company’s culture, innovation agenda, and business strategy.

One of the key themes that emerged from the summit was the role of Fintech in driving sustainable investment. Through innovative solutions such as green bonds, impact investing platforms, and ESG scoring algorithms, Fintech firms are empowering investors to allocate capital towards environmentally and socially responsible projects and companies. Xettle Technologies showcased its suite of Fintech software solutions designed to facilitate sustainable investing, enabling financial institutions and investors to align their portfolios with their values and sustainability objectives.

Moreover, the summit explored the transformative potential of blockchain technology in advancing sustainability goals. By enhancing transparency, traceability, and accountability in supply chains, blockchain can help address issues such as deforestation, forced labor, and conflict minerals. Xettle Technologies’ experts elaborated on the company’s blockchain-based solutions for supply chain finance and sustainability reporting, emphasizing their role in promoting ethical sourcing, responsible production, and fair labor practices.

In addition to sustainable investing and supply chain transparency, the summit delved into the role of Fintech in promoting financial inclusion and resilience. By leveraging technology and data analytics, Fintech firms can expand access to financial services for underserved populations, empower small and medium-sized enterprises (SMEs), and build more inclusive and resilient communities. Xettle Technologies’ representatives shared insights into the company’s initiatives to support financial inclusion through digital payments, microfinance, and alternative credit scoring models.

Furthermore, the summit highlighted the importance of collaboration and partnership in advancing sustainability goals. Recognizing the interconnected nature of sustainability challenges, participants underscored the need for cross-sectoral collaboration between Fintech firms, financial institutions, governments, civil society, and academia. Xettle Technologies reiterated its commitment to collaboration, emphasizing its partnerships with industry stakeholders to drive collective action and scale impact.

Looking ahead, the future of sustainability in Fintech appears promising yet complex. As Fintech firms continue to innovate and disrupt traditional financial systems, they must prioritize sustainability as a core principle and driver of value creation. Xettle Technologies’ visionaries reiterated their commitment to sustainability, pledging to harness the power of technology to build a more sustainable, inclusive, and resilient financial ecosystem for future generations.

In conclusion, the Fintech Summit served as a catalyst for reflection and action on the role of sustainability in shaping the future of finance. From sustainable investing and supply chain transparency to financial inclusion and resilience, Fintech has the potential to drive positive change and advance sustainability goals on a global scale. Xettle Technologies’ leadership in integrating sustainability into its Fintech solutions exemplifies its dedication to driving innovation and creating shared value for society and the planet. As the industry continues to evolve, collaboration, innovation, and sustainability will be key drivers of success in building a more sustainable and resilient financial future.

2 notes

·

View notes

Text

Empowering Financial Stability Through Microfinance Software Solutions

Discover the financial revolution powered by microfinance software! From empowering entrepreneurs to serving underserved communities, these tools reshape financial stability globally. Explore the possibilities and pave your path to financial empowerment today

Through microfinance software solutions, individuals gain easier access to financial services, empowering marginalized communities worldwide and fostering global change

Enhanced Access: Microfinance software breaks down banking barriers, providing easy access to loans, savings, and insurance. This inclusion empowers marginalized populations, driving global change.

Efficiency Boost: Advanced tools streamline operations, cutting costs and enabling competitive rates. Borrowers and savers benefit from enhanced value and convenience.

Risk Management: Software evaluates creditworthiness, promoting responsible lending and transparency. Trust and stability in financial transactions are bolstered.

Entrepreneurial Support: Microfinance software provides capital and resources, fostering business growth and job creation. Communities thrive on resilience and innovation.

Community Development: Financial resources uplift marginalized communities, improving living standards and breaking poverty cycles. Sustainable development and social cohesion are promoted.

Adaptability and Growth: Microfinance software is flexible and scalable, catering to diverse needs and expanding outreach. Continued progress and prosperity are ensured for all.

Microfinance software illuminates the path towards a more inclusive and radiant financial future, accessible to all.

0 notes

Text

Digitization in Lending Market Huge Growth in Future Scope 2024-2030 | GQ Research

The Digitization in Lending market is set to witness remarkable growth, as indicated by recent market analysis conducted by GQ Research. In 2023, the global Digitization in Lending market showcased a significant presence, boasting a valuation of USD 423.66 Million. This underscores the substantial demand for Digitization in Lending technology and its widespread adoption across various industries.

Get Sample of this Report at: https://gqresearch.com/request-sample/global-digitization-in-lending-market/

Projected Growth: Projections suggest that the Digitization in Lending market will continue its upward trajectory, with a projected value of USD 857.74 billion by 2030. This growth is expected to be driven by technological advancements, increasing consumer demand, and expanding application areas.

Compound Annual Growth Rate (CAGR): The forecast period anticipates a Compound Annual Growth Rate (CAGR) of 26.58 %, reflecting a steady and robust growth rate for the Digitization in Lending market over the coming years.

Technology Adoption:

Increasing adoption of digitization in lending processes for efficiency and convenience.

Digitization utilized for loan origination, underwriting, approval, and servicing.

Integration of online platforms, mobile applications, and electronic signatures for seamless customer experience.

Application Diversity:

Consumer Loans: Digitized application processes for personal loans, mortgages, and auto loans.

Small Business Loans: Online platforms for business loan applications, credit assessment, and funding.

Peer-to-Peer Lending: Digital platforms connecting borrowers with individual investors for lending opportunities.

Microfinance: Digital lending solutions targeting underserved populations with microloans and financial inclusion initiatives.

Consumer Preferences:

Demand for streamlined and paperless loan application processes accessible through digital channels.

Preference for mobile-friendly interfaces and self-service options for loan management and payment.

Emphasis on data security, privacy protection, and transparent loan terms and conditions.

Desire for fast approval times and quick disbursal of funds facilitated by digitized lending platforms.

Technological Advancements:

Advancements in artificial intelligence (AI) and machine learning (ML) for credit scoring and risk assessment.

Integration of big data analytics and alternative data sources for personalized lending decisions.

Development of blockchain technology for secure and transparent loan transactions and smart contracts.

Adoption of open banking APIs for seamless integration with financial data and third-party services.

Market Competition:

Intense competition among traditional banks, fintech startups, and online lenders in the digital lending market.

Differentiation through innovative loan products, competitive interest rates, and superior customer service.

Strategic partnerships with technology providers, credit bureaus, and regulatory compliance firms.

Focus on digital marketing, customer engagement, and brand loyalty to attract and retain borrowers.

Environmental Considerations:

Consideration of environmental impact in the reduction of paper usage and physical documentation in lending processes.

Promotion of energy-efficient data center infrastructure and sustainable computing practices.

Implementation of eco-friendly practices in loan servicing and collection operations.

Compliance with environmental regulations and standards governing electronic waste disposal and recycling.

Regional Dynamics: Different regions may exhibit varying growth rates and adoption patterns influenced by factors such as consumer preferences, technological infrastructure and regulatory frameworks.

Key players in the industry include:

Fiserv

ICE Mortgage Technology

FIS

Newgen Software

Nucleus Software

Temenos

Pega

Sigma Infosolutions

Intellect Design Arena.

Tavant

The research report provides a comprehensive analysis of the Digitization in Lending market, offering insights into current trends, market dynamics and future prospects. It explores key factors driving growth, challenges faced by the industry, and potential opportunities for market players.

For more information and to access a complimentary sample report, visit Link to Sample Report: https://gqresearch.com/request-sample/global-digitization-in-lending-market/

About GQ Research:

GQ Research is a company that is creating cutting edge, futuristic and informative reports in many different areas. Some of the most common areas where we generate reports are industry reports, country reports, company reports and everything in between.

Contact:

Jessica Joyal

+1 (614) 602 2897 | +919284395731 Website - https://gqresearch.com/

0 notes

Text

Private Loans & Lines Of Credit

Shopper loan officers concentrate on loans to people. 1 hour loans online no credit check Whereas the disclosure is often beneficial, it's not without risk, as it may trigger political discontent due to the comparatively high interest rates in microfinance, particularly in the section of corporations issuing "loans to payday," which in recent times have more and more registered as MICROFINANCE organizations and credit score cooperatives, not solely in USA and UK, but also in lots of jurisdictions different. In the case of the fall of the standard of the loan portfolio of microfinance organizations are subject to not solely the risk of default to the resource providers, but additionally the danger of popularity loss, as it results in a lack of confidence. Get yourself a Test Advance In lower than 20 Minutes Receive a Examine Advance In as little as 20 Minutes Individuals вЂ" and people everywhere in the globe, really вЂ" have come to rely on loans to assist make purchases which can be important fund other necessities.

These apps are a superb different to excessive-curiosity payday loans, since they typically come with little-to-no charges and don’t require a credit verify. As previously talked about, getting a enterprise line of credit score with no credit check is tough-but getting funding with a low score isn’t out of the question. Our firm Loans Canada On-line is devoted that can assist you get the perfect money advance or brief time period loan from our trusted lenders. Enterprise loans could also be both secured or unsecured. For example, U.S. online marketplace lending platform LendKey allows consumers to guide loans straight from neighborhood lenders like credit score unions and community banks. Loans from credit unions could also be known as bank loans as nicely. Smaller loans, often for loan quantities of $100,000 USD or less, are known as "microloans." Banks are much less more likely to make these loans than different lenders. Both are usually referred to as second mortgages, as a result of they are secured towards the worth of the property, just like a standard mortgage.

They don't get any curiosity on these financial savings whilst offsetting the mortgage however will have the ability to get their cash again in full once the mortgage has been paid down to between 70% and 80% of the property’s market worth. As a result of companies have such advanced financial situations and statements, commercial loans normally require human judgment along with the evaluation by underwriting software. Perignon '55 on the car over and fish, in time writing letters, making a fairly have been built to show was intelligent, a baby is not going to desirous to his arms. Perhaps we’re the proper alternative for you too! Once thought of the finance option of final resort, asset-based lending has change into a preferred alternative for small companies lacking the credit score rating or observe record to qualify for different types of finance. The interest rates relevant to those totally different varieties could range relying on the lender and the borrower. In the interest of growth of data society in the USA and UK should act different types of stimulating financial and monetary instruments that can improve the monetary protection shouldn't be supplied companies banking.

The survey or conveyor and valuation prices can often be diminished, supplied one finds a licensed surveyor to examine the property considered for purchase. line of credit without credit check offered a credit-danger-free loan for the lender, averaging 7 p.c a yr. The median annual wage for loan officers within the United States was $63,270 in Could 2019. The bottom 10 % earned lower than $32,560, and the best 10 % earned more than $132,680. Within the United States, employment of loan officers is projected to develop three percent from 2019 to 2029, quicker than the average for all occupations. Others have increased the common loan dimension (and thus, a hundred day loans no credit check serve fewer poor purchasers) to extend income. Because of this, curiosity rates may vary significantly throughout lenders, and some loans have variable interest charges. Nonetheless, following the close of Lehman Brothers' sub-prime lender BNC Mortgage in August 2007, the UK's most distinguished secured loan providers had been pressured to withdraw from the market. In 2007, the then-Attorney Basic of new York State, Andrew Cuomo, led an investigation into lending practices and anti-competitive relationships between scholar lenders and universities.

0 notes

Text

Outsourcing Accounts Receivable: A Game-Changer for Financial Optimization

In the dynamic landscape of financial management, businesses are constantly seeking innovative strategies to optimize their operations and enhance efficiency. One such game-changing approach gaining prominence is the outsourcing of accounts receivable processes.

I. Understanding the Dynamics of Accounts Receivable Outsourcing

Defining Accounts Receivable Outsourcing

Outsourcing accounts receivable involves delegating the management of invoicing, payment processing, and collections to third-party service providers. This allows businesses to focus on their core competencies while experts handle intricate financial processes.

Key Components of Outsourcing AR

Invoicing Efficiency: Outsourcing streamlines the invoicing process, ensuring accuracy and timely delivery, which is critical for maintaining healthy cash flow.

Payment Processing: Expert outsourcing partners use advanced systems to process payments efficiently, reducing errors and enhancing overall financial control.

Collections Management: Skilled professionals manage collections, improving the chances of timely payments and reducing the burden on internal teams.

II. The Strategic Advantages of Outsourcing Accounts Receivable

A. Cost Savings

Operational Cost Reduction: Outsourcing minimizes the need for maintaining an extensive in-house AR team, leading to significant cost savings.

Technology Integration: Outsourcing partners leverage cutting-edge technology, reducing the need for businesses to invest heavily in expensive software and infrastructure.

B. Enhanced Focus on Core Competencies

Business Concentration: Outsourcing allows businesses to divert their attention to core functions, fostering innovation and growth.

Resource Allocation: By entrusting AR processes to experts, organizations can allocate resources more efficiently, promoting overall productivity.

III. Addressing Challenges in Outsourcing Accounts Receivable

A. Data Security Concerns

Compliance Protocols: Reliable outsourcing partners adhere to stringent data security and compliance measures, mitigating risks associated with sensitive financial information.

B. Communication and Collaboration

Transparent Communication: Establishing clear lines of communication is crucial for successful outsourcing. Regular updates and collaboration foster a seamless partnership.

C. Customization and Flexibility

Tailored Solutions: Outsourcing partners offer customizable solutions to align with the unique needs and goals of each business.

IV. Outsourcing and its Impact on Non-Banking Financial Services

A. Overview of Non-Banking Financial Services (NBFS)

Diversified Services: NBFS encompasses a wide range of financial services beyond traditional banking, including microfinance, insurance, and asset management.

B. Role of Outsourcing in NBFS

Risk Management: Outsourcing AR in NBFS contributes to effective risk management, ensuring compliance with regulatory requirements.

Scalability: The flexibility of outsourcing aligns with the dynamic nature of non-banking financial services, facilitating scalability based on market demands.

Conclusion

As businesses navigate the complex financial landscape, outsourcing accounts receivable emerges as a strategic tool for achieving unparalleled efficiency and optimization. Its transformative impact extends beyond traditional banking, influencing the very fabric of non-banking financial services. By embracing outsourcing, organizations can not only streamline their financial processes but also position themselves as agile, adaptable entities ready to meet the challenges of the future. In this era of constant evolution, outsourcing accounts receivable stands as a true game-changer for financial optimization.

0 notes

Text

How to start a microfinance company?

Introduction: Starting a microfinance company can be a rewarding venture, allowing you to contribute to financial inclusion and empower individuals in need. This comprehensive guide will walk you through the essential steps of establishing a microfinance company, with a particular emphasis on Section 8 Microfinance Company Registration, How to start a microfinance company?.

1. Understanding Microfinance: Before diving into the regulatory aspects, it's crucial to have a solid understanding of microfinance. Microfinance involves providing financial services, such as loans and savings, to low-income individuals or groups who lack access to traditional banking. Knowing the socio-economic landscape of the target community is vital for tailoring your services effectively.

2. Conducting Market Research: Identify the specific needs of your target audience. Analyze the demand for microfinance services in the chosen region, assess the competition, and understand the regulatory environment. This research will help you shape your business model and services.

3. Business Plan Development: Create a detailed business plan that outlines your company's mission, vision, target market, services offered, and financial projections. A well-structured business plan is essential for attracting investors and complying with regulatory requirements.

4. Legal Structure and Registration: Choose an appropriate legal structure for your microfinance company. Section 8 of the Companies Act in many jurisdictions allows for the formation of companies with charitable objectives. This legal structure is suitable for microfinance institutions aiming to promote social welfare. Follow the prescribed procedures for Section 8 Microfinance Company Registration to ensure compliance with legal requirements.

5. Obtaining Necessary Licenses: Microfinance companies typically require licenses or approvals from financial regulatory authorities. Obtain the necessary permits to operate legally. This step may involve submitting detailed documentation about your business model, financial plans, and compliance measures.

6. Building Infrastructure: Establish a robust infrastructure for your microfinance company, including a secure and user-friendly software system for managing financial transactions, client data, and reporting. Invest in training your staff to handle microfinance operations efficiently and ethically.

7. Developing Partnerships: Forge partnerships with local organizations, NGOs, or government agencies to extend your reach and enhance your impact. Collaborative efforts can provide valuable insights, resources, and support.

8. Implementing Social Impact Initiatives: As a Section 8 microfinance company, emphasize your commitment to social welfare. Implement initiatives that go beyond financial services, such as financial literacy programs, skill development, and community outreach.

9. Compliance and Risk Management: Establish robust compliance and risk management protocols to ensure the stability and sustainability of your microfinance operations. Regularly review and update policies to adapt to changing market conditions and regulatory requirements.

10. Monitoring and Evaluation: Implement a system for monitoring and evaluating the impact of your microfinance services. Regular assessments will help you fine-tune your operations and demonstrate your social impact to stakeholders.

Conclusion: Starting a microfinance company is a multifaceted process that requires careful planning, adherence to regulations, and a commitment to social impact. By following these steps, with a specific focus on Section 8 Microfinance Company Registration, you can build a sustainable and socially responsible microfinance institution that makes a positive difference in the lives of those you serve.

#microfinance company#microfinance company registration#microfinance#micro finance company#how to start a microfinance company?#microfinance company registration process#how to start a microfinance company#microfinance registration process#how to register a microfinance company?#how to start a finance company#how to start a micro lending company#microfinance rules#how to start a finance company with no money#microfinance explained#microfinance company licence

0 notes

Text

Open-Source Fintech Script: Empowering Online Financial Services

Introduction:

Have you ever pondered how technological innovation is reshaping the landscape of financial services? Open-source Fintech scripts drive a significant revolution in managing and accessing financial solutions. From democratizing financial inclusion to fostering innovation, these scripts are becoming the cornerstone of online financial services. But what exactly are these scripts, and how are they transforming the sector?

Open-Source Fintech Scripts Unveiled:

In the digital transformation era, technology is revolutionizing every aspect of our lives, including how we manage our finances. Open-source Fintech scripts are emerging as a powerful force driving innovation in the financial services industry. These scripts, with their openly accessible source code, are empowering developers to create and customize financial solutions that are accessible, secure, and cost-effective.

Open-source Fintech scripts represent a fundamental shift in financial technology. They are software solutions with openly accessible source code, inviting collaboration, modification, and distribution. The collaborative ecosystem they create allows developers to collectively enhance and customize these scripts, accelerating innovation while ensuring inclusivity within the Fintech sphere.

Advantages of Open-Source Fintech Scripts:

Let's delve into the core advantages and functionalities that open-source Fintech scripts offer:

Versatility: These scripts are the foundational framework for various financial services, including digital payment gateways, secure transaction systems, investment platforms, and comprehensive financial management tools.

Customization: Their adaptable nature empowers developers to create tailored solutions, catering to specific business requirements and ensuring a personalized user experience.

Innovation Catalyst: The collaborative environment nurtures innovation by harnessing the community's collective expertise, ensuring responsiveness to evolving market needs and technological trends.

Promoting Financial Inclusion:

One of the most striking impacts of open-source Fintech scripts is their role in promoting financial inclusivity:

Addressing Underbanked Communities: Initiatives leveraging these scripts create mobile banking applications, peer-to-peer lending platforms, and microfinance solutions, bridging the gap for underbanked and marginalized communities globally.

Empowering Emerging Economies: By providing cost-effective and customizable solutions, these scripts empower small entrepreneurs and facilitate economic growth in emerging economies.

Democratizing Financial Services through Open-Source Fintech Scripts

The financial technology industry, Fintech, has recently grown in popularity. Fintech companies leverage cutting-edge technologies to provide innovative financial solutions that challenge traditional banking models. At the heart of this revolution are open-source Fintech scripts and software solutions with openly accessible source code. This open-source approach fosters collaboration, innovation, and accessibility within the Fintech ecosystem.

Real-World Examples and Case Studies:

Kiva: Utilizing open-source platforms, Kiva facilitates peer-to-peer micro-lending, connecting lenders and borrowers worldwide fostering financial inclusion and entrepreneurship.

Grassroots Economics: Leveraging open-source scripts, Grassroots Economics enables community currencies in underserved regions, empowering local economies and supporting sustainable development.

Open Banking Initiatives: European countries have adopted open-source Fintech scripts to implement Open Banking, allowing customers to access financial data across multiple institutions, fostering competition and innovation.

Mambu: Mambu's cloud-native open-source banking platform allows financial institutions to deliver state-of-the-art banking experiences, rapidly promoting innovation and scalability.

Hiveonline: This blockchain-based solution leverages open-source scripts to provide digital trust platforms for SMEs, facilitating access to financial services and networks.

Odoo: Utilizing open-source technology, Odoo offers comprehensive financial management modules, including accounting, invoicing, and budgeting, benefiting businesses of all sizes.

Hydrogen: Hydrogen's open-source infrastructure enables developers to build and deploy financial applications quickly, providing various tools for investing, savings, and financial planning.

AlgoTrader: AlgoTrader utilizes open-source scripts to offer algorithmic trading solutions, empowering traders with advanced automation and trading strategies.

BitPay: Employing open-source technology, BitPay provides cryptocurrency payment processing services, enabling merchants to accept digital currencies securely.

QuantConnect: QuantConnect utilizes open-source financial algorithms, allowing developers to build and test trading strategies across various financial markets.

Plaid: Plaid leverages open-source scripts to provide APIs for financial data, enabling seamless integration of banking information into applications.

Hedera Hashgraph: Utilizing open-source technology, Hedera Hashgraph provides a distributed ledger platform for secure and fast financial transactions.

Zerodha: Zerodha uses open-source scripts to power its online trading platform, offering low-cost brokerage services to retail investors.

Dharma: Leveraging open-source lending protocols, Dharma enables peer-to-peer lending and borrowing on the blockchain.

Truelayer: Truelayer utilizes open-source scripts to provide API services for accessing banking data securely, facilitating innovative financial applications.

Technical Aspects of Open-Source Fintech Scripts:

Security Protocols: These scripts prioritize robust security protocols, employing encryption standards and multi-factor authentication to safeguard user data and transactions.

API Integration: Offering robust API integrations, these scripts enable seamless connectivity with third-party services, expanding functionality and enhancing user experiences.

Workflow of Open-Source Fintech Scripts:

Understanding the workflow of these scripts illuminates their functionality:

Rider App Workflow:

Users sign up and provide the necessary details.

Book a ride by specifying the pick-up and drop-off locations.

The app searches for nearby drivers and displays the current location of the assigned driver.

Completes the ride and pays the fare via the app.

Driver App Workflow:

Drivers register and switch to an online mode to receive ride requests.

Receive ride details from nearby users and complete the ride.

Receive payment for the completed trip.

Implementing an Open-Source Fintech Script:

To embark on building an open-source Fintech script, consider these key steps:

Conduct Extensive Market Research: Understand user behavior, market trends, competitor strategies, and available resources before commencing development.

Gather Requirements: Based on research insights, define the essential features and functionalities for your script's Minimum Viable Product (MVP).

Estimate Development Costs: Plan and evaluate the costs of building the script. Typically, it ranges from $1500 to $4500, depending on the scope and customization.

Agile Development: Adopt an agile methodology for iterative development, focusing on regular milestones and continuous testing.

Thorough Testing: Ensure rigorous testing of the script for functionality, user interface, performance, and usability before launch.

Launch and Feedback Loop: Post-launch, collect user feedback to continuously refine and enhance the script.

Conclusion:

Open-source Fintech scripts stand at the forefront of reshaping the financial technology landscape. Their versatility, adaptability, and role in fostering financial inclusion make them pivotal in shaping a more accessible and innovative future in online financial services.

Key Takeaways:

Open-source Fintech scripts democratize financial services by fostering inclusivity and innovation.

Their workflows cater to riders and drivers, ensuring a seamless user experience.

Implementing these scripts involves market research, requirements gathering, agile development, thorough testing, and continuous improvement.

0 notes

Text

Revolutionizing Financial Inclusion: Microfinance Software Development

In the pursuit of fostering financial inclusion and empowering communities, the role of microfinance has become increasingly pivotal. As the demand for efficient and scalable microfinance solutions rises, the significance of robust Microfinance Software Development cannot be overstated. This article delves into the transformative landscape of microfinance software, exploring its key components, benefits, and the profound impact it has on driving financial access globally.

Understanding Microfinance Software Development

1. Definition and Purpose

Microfinance Software Development refers to the creation of tailored software solutions specifically designed to meet the unique needs of microfinance institutions (MFIs). These solutions streamline and automate various processes involved in microfinance operations, including loan management, client data tracking, and financial reporting.

2. Key Components

a. Loan Management System (LMS):

The core of microfinance operations, an efficient LMS ensures seamless loan disbursement, repayment tracking, and interest calculation. It provides a centralized platform for managing diverse loan products catering to the specific requirements of microfinance clients.

b. Client Information Database:

A comprehensive database system captures and organizes client information, facilitating efficient client management. This includes details such as borrower history, financial transactions, and repayment records, enabling MFIs to make informed lending decisions.

c. Financial Reporting Tools:

Robust reporting tools generate real-time financial reports, offering insights into the institution's performance. From portfolio analysis to income statements, these tools empower decision-makers with data-driven insights crucial for strategic planning.

d. Mobile Banking Integration:

In an era where mobile technology is ubiquitous, integrating mobile banking features enhances accessibility for clients. Mobile loan applications, text alerts, and digital payment options contribute to a more inclusive and user-friendly microfinance experience.

The Impact of Microfinance Software Development

1. Enhanced Operational Efficiency

Microfinance Software Development optimizes internal processes, reducing manual intervention and minimizing the risk of errors. Automated workflows streamline loan origination, approval, and disbursement, resulting in a more efficient and agile microfinance institution.

2. Scalability and Flexibility

Tailored software solutions are designed to scale with the growing needs of microfinance institutions. Whether a small community-based MFI or a larger organization serving a broader population, the flexibility of microfinance software ensures adaptability to changing landscapes.

3. Improved Risk Management

Risk mitigation is a critical aspect of microfinance operations. Advanced software solutions employ risk assessment algorithms, enabling MFIs to evaluate creditworthiness, detect potential fraud, and implement proactive risk management strategies.

4. Financial Inclusion Amplified

The ultimate goal of microfinance is to foster financial inclusion. Microfinance Software Development plays a pivotal role in achieving this objective by breaking down barriers to access. Through digital channels and streamlined processes, marginalized communities gain access to essential financial services.

Challenges and Opportunities in Microfinance Software Development

1. Challenges

a. Technological Barriers:

Some MFIs, particularly in developing regions, may face challenges in adopting technology due to limited infrastructure and technical expertise.

b. Data Security Concerns:

As financial transactions are sensitive, ensuring robust cybersecurity measures is crucial to build trust among clients.

2. Opportunities

a. Blockchain Integration:

Exploring blockchain technology for secure and transparent transactions can revolutionize the way microfinance operates, ensuring data integrity and reducing fraud.

b. Data Analytics for Client Empowerment:

Utilizing advanced analytics can provide valuable insights into client behavior and financial patterns, enabling MFIs to offer personalized services and empower clients in their financial journey.

The Future of Microfinance Software Development

As technology continues to evolve, the future of Microfinance Software Development holds exciting possibilities. Integration with emerging technologies, increased focus on user-centric design, and continued efforts towards sustainability are poised to shape the next chapter of microfinance.

Conclusion: A Digital Dawn for Financial Inclusion

In conclusion, Microfinance Software Development is a catalyst for ushering in a new era of financial inclusion. By addressing operational challenges, embracing technological advancements, and staying committed to the principles of microfinance, software solutions are paving the way for a more accessible and equitable financial landscape worldwide. As we navigate this digital dawn, the empowerment of communities through microfinance stands as a testament to the transformative power of technology in the service of humanity.

#software company in patna#best software company in patna#digital marketing company in patna#web development company in patna

0 notes

Text

Loan Management System: Simplifying Financial Operations

In today's rapidly evolving financial landscape, effective loan management has become a cornerstone of success for businesses, especially for Non-Banking Financial Companies (NBFCs). With the advent of innovative technology, a dedicated Loan Management System (LMS) has become essential. In this article, we'll explore the significance of LMS, Loan Management Software, NBFC software, Loan Origination System, Microfinance Software, and Business Loan Software in streamlining financial operations. Join us as we delve into how AllCloud embraces a culture of curiosity, communication, and innovation to excel in this dynamic sector.

The Importance of Loan Management Software (LMS)

Enhancing Operational Efficiency

The LMS is a game-changer when it comes to streamlining lending processes. It automates loan origination, disbursement, and repayment, reducing the workload for NBFCs and improving operational efficiency.

Risk Mitigation

Lending involves various risks, from credit risks to market risks. LMS offers robust risk management tools, providing NBFCs with the ability to identify, assess, and mitigate risks effectively.

Customer-Centric Approach

A Loan Management System enables businesses to deliver exceptional customer service by providing borrowers with convenient online access to their loan accounts, reducing the need for physical visits.

Regulatory Compliance

In the ever-changing landscape of financial regulations, compliance is a top priority. LMS ensures that NBFCs adhere to legal requirements, reducing the risk of penalties and reputational damage.

Streamlining Loan Origination system

Efficient Application Processing

LMS simplifies the loan application process. Applicants can submit their details online, and the system automates verification, drastically reducing processing time.

Credit Scoring

The software evaluates an applicant's creditworthiness quickly and accurately, making it easier for NBFCs to make informed lending decisions.

Documentation Management

LMS digitizes document collection and storage, ensuring that all necessary paperwork is readily available for both clients and auditors.

Instant Approvals

With automated credit assessment, NBFCs can provide instant approvals for eligible applicants, enhancing customer satisfaction.

Microfinance Software: Empowering Small Businesses

Microloan Disbursement

For microfinance institutions, LMS facilitates microloan disbursement, enabling them to reach small businesses and individuals who need financial support.

Client Data Management

Managing a large number of microloan clients requires robust data management capabilities. Microfinance software within the LMS helps in this aspect.

AllCloud's Commitment to Innovation

At AllCloud, innovation and collaboration are at the heart of our operations. We foster a culture of curiosity, effective communication, and transparency, which are essential in the ever-evolving financial industry. Our team is encouraged to explore, ask questions, and innovate to deliver value consistently to our customers, partners, and stakeholders.

Business Loan Software: Catering to Diverse Needs

Customization

Different businesses have varying loan requirements. Business Loan Software within the LMS can be customized to meet the specific needs of different industries.

Real-time Reporting

Access to real-time data and reporting is crucial for making informed decisions. LMS offers comprehensive reporting tools for businesses.

Automation of Repayment

The software automates loan repayment, making it easier for borrowers and lenders to manage financial transactions.

Conclusion

In the ever-evolving world of finance, a Loan Management System is indispensable for NBFCs, microfinance institutions, and businesses at large. AllCloud, with its commitment to innovation and collaboration, stands out as a trusted partner in the journey of financial success.

FAQs

What is the primary function of a Loan Management System?

A Loan Management System primarily automates and streamlines loan origination, disbursement, and repayment processes for financial institutions.

How does LMS help in risk management?

LMS offers tools to identify, assess, and mitigate risks, reducing the exposure of financial institutions to potential losses.

Can microfinance institutions benefit from Loan Management Software?

Absolutely. Microfinance software within LMS is tailored to meet the unique needs of microfinance institutions, facilitating microloan disbursement and client data management.

What role does AllCloud play in the financial sector?

AllCloud is dedicated to fostering innovation and collaboration in the financial sector, delivering value to customers, partners, and stakeholders.

Why is regulatory compliance crucial for NBFCs?

Regulatory compliance is essential to avoid legal penalties and protect the reputation of NBFCs in the market.

#succession#welcome home#super mario#the owl house#the mandalorian#ted lasso#taylor swift#across the spiderverse#wally darling#star wars

0 notes

Text

🚀 Unbox the Future of Finance with SigmaIT Software 🌐💰 Say goodbye to financial headaches and hello to a seamless, tech-powered journey 🌟💼 Ready for a new era in accounting? Dive in! 📈✨ #UnboxFinance #NextGenAccounting #billingsoftware #accountingsoftware 🚀

contact us 9956973891

1 note

·

View note

Text

Microfinance software is a specialized digital solution designed to streamline and enhance the operations of microfinance institutions, NGOs, and financial service providers that cater to underserved and financially marginalized populations. This software empowers these organizations to efficiently manage their microloans, savings accounts, and other financial services while promoting financial inclusion and empowerment. It typically includes features such as loan origination, repayment tracking, client management, accounting, and reporting, enabling microfinance institutions to make informed decisions, reduce administrative overhead, and ultimately, better serve their clients in a scalable and sustainable manner.

#microfinance#software#best microfinance software in tamil nadu#online best microfinance software in west bengal#softwaredemo#microfinancesoftware#microfinance software

0 notes

Text

Surveillance video shows Diddy assaulting former girlfriend, Cassie

A 2016 surveillance video obtained exclusively by CNN shows Sean “Diddy” Combs grab, shove, drag and kick his then-girlfriend Cassie Ventura during an altercation that matches allegations in a now-settled federal lawsuit filed by Ventura in November. The footage, compiled from multiple camera angles dated March 5, 2016, appears to show the rapper, producer and business mogul during an […]

6 notes

·

View notes

Text

One of the Best Microfinance Software Services provider in Patna

contact us for any financial and banking software, Website and Mobile App Services in India.

0 notes

Text

Hi-Tech Microfinance Software by Vexil Infotech

Microfinance Software is a financial technology solution designed to empower microfinance institutions. This comprehensive software streamlines loan management, client data tracking, and financial reporting, enabling micro-lenders to efficiently serve their clients and drive financial inclusion. Vexil Infotech's Microfinance Software is the trusted choice for organizations looking to make a meaningful impact in the world of microfinance. At Vexil Infotech, we're not just providing software; we're fostering financial inclusion and empowerment. Join us on the journey to revolutionize microfinance with our innovative software solutions.

Visit our website to know more- https://vexilinfotech.com/microfinance-software

0 notes

Text

ATD Money - Loans for Bad Credit with Instant Approval

ATD Money is one of the best micro-finance service providers which has developed its products especially for youngsters. Their motive is to transform customers’ lives by providing them with an easy loan approval process and minimal documents.

Easy Application Process

If you need to borrow some cash quickly, you can apply for an instant salary loan on the ATD money platform. This easy and hassle-free online service offers a wide variety of loans including salary advances, personal loans, business loans, and more. The application process is simple and the loan amount can be deposited directly into your bank account. You can also pay the loan off at a flexible schedule and zero interest rates. ATD Money is a product of ATD Financial Services Pvt. Ltd and is an eminent microfinance solution provider.

The information, software functionality, and materials available on this Website may include errors, omissions, inaccuracies, or other limitations. ATD may make changes to this Website at any time. The information, software functionality, and materials on this Website are provided “as is” and “as available” without warranties of any kind, either express or implied. To the fullest extent permitted by law, ATD disclaims all warranties, including warranties of merchantability and fitness for a particular purpose.

In the event of a conflict between this TOU and any other notices or terms and conditions posted on this Website, the latter terms shall govern. In addition, You agree to abide by any other terms and conditions that apply to participation, subscription, or usage privileges in any restricted member portal area of this Website.

ATD welcomes Your feedback and suggestions about its programs and services. By transmitting such Feedback to ATD, You grant to ATD a royalty-free, perpetual, irrevocable, transferable, non-exclusive license to use, publish, copy, distribute, create derivative works, and display (in whole or in part) worldwide, and to incorporate it into other works in any form, media, or technology now known or later developed for the full term of any rights that may exist in such content.

You agree not to post any offensive, threatening, defamatory, indecent, or unlawful material on this Website or in any Forums. You also agree not to impersonate any other person or entity, nor engage in any activity that would violate any applicable laws or regulations.

ATD reserves the right to remove such material and to terminate Your access to this Website if You do so. Your access to this Website may be terminated immediately in ATD’s sole discretion if You fail to comply with this TOU. Upon termination, You must destroy all copies of this Website in Your possession. The provisions concerning ATD’s proprietary rights, feedback, disclaimers of warranty, limitation of liability, waiver and severability, entire agreement, injunctive relief, and governing law will survive termination.

Instant Approval

ATD Money is an online lending service that offers loans for bad credit with instant approval. These loans can help you with a variety of expenses, including debt consolidation, home improvements, or major purchases. They are available from a number of lenders and typically have less stringent requirements than traditional loans. The best thing about loans for bad credit with instant approval is that they can save you time by avoiding the long application process.

Loans for bad credit with instant approval are a great way to get the funds you need quickly. These loans can be used for any purpose and are typically available from a variety of lenders. They are also available in a wide variety of amounts and terms. The most important thing to remember about these loans is that you should never take out more than you can afford to repay.

ATD Money is an eminent microfinance solution provider agency that bestows salaried employees or professionals with a range of quick mini-cash loans. This is a highly innovative and convenient loan facility that helps borrowers meet their urgent cash requirements in a simple and hassle-free manner. It also provides them with an opportunity to build a solid credit score by reimbursing the amount on time and improving their credit score over a period of time.

In order to avail of these loans, you need to fill up the online application form by providing basic information such as name, address, phone number, and other relevant details. The loan will be disbursed within 24 working hours of applying for it. You can easily apply for the loan from any computer, laptop or mobile phone. You can also use the app to check your eligibility for the loan.

Low-Interest Rates

If you’re stuck in financial trouble and need quick cash, then you can easily get a loan online at a reasonable rate from ATD money. Their application process is easy and requires only a few documents. Their interest rates are also very competitive and they have a flexible repayment schedule. You can even avail of a loan from them with a low CIBIL score.

ATD Money offers loans to anyone who has a bank account, and they make the entire process online so there’s no need to visit a branch. The application process is simple and takes only 3 minutes to complete. All you need to do is fill out some basic information and wait for approval. Once your loan is approved, you can withdraw the money from your bank account. The maximum amount you can borrow is Rs 50,000.

Despite the high leverage, Fitch expects that ATD’s lease-adjusted debt/EBITDAR will decline to 6.5x in YE 2021 due to stronger end-market demand and lower operating expenses (labour, freight, and logistics costs). ATD also has solid FCF generation and is expected to continue to generate a positive free cash flow from operations.

ATD Money is a microfinance company that offers instant cash loans to salaried individuals and professionals. Its aim is to transform people’s lives through business ideas. Its micro-finance services include payday loans and advances against salary. Its loans are available to all ages and gender, with no credit checks. The company’s loans are unsecured and have no processing fees or prepayment penalties. In addition, ATD has exemplary customer service and a fast turnaround time. In addition to offering loans, the company also offers personal insurance products.

#payday loans#quick cash loans#personal loans#instant loan#cash loans#loan app in india#payday loans in india#fast cash loans online#advance salary loan#loan apps

0 notes

Last Seen Blogs

neil-is-obsessed

the Eighth Wonder

marlaaguirrereidsville

MarlaAgu

goodluck0712

題名未設定

novalizinpeace

Nova's floating hell

orengejoshi

hi I'm Joshi🦕