#ynab

Text

ADHD money/budgeting system I'm currently using for my benefit is going well (I've been using it for like half a year now?), and I wanna recommend it.

You Need a Budget is EXCELLENT. 10/10 do recommend. Uhhh rambling about it and my generic disclaimers + gushing extensively under the cut but TL;DR I think it's great for ADHD ppl, I've used it for 6+ months now and I find it super SUPER helpful. also weirdly fun.

DISCLAIMERS:

Budgeting helps you understand/know your money, it can't make money appear where there is none.

Everyone should learn to budget even if you don't have much money (especially then)

This is NOT a magic trick solution. Just like everything else, it is an assistive tool. This is one of those adult things we can't simply opt out of without negative consequences, though.

My advice is based on something I am currently able to do. That is, I can spend an amount of money on this specific thing that works well for me. If you have no extra money to spend then previously I was tracking things in a notebook. So you can still do this.

I believe Dave Ramsey is a fundie fraud/hack and no one should listen to him about money.

DID YOU KNOW THEY CANCELLED MINT???

Okay? OKAY.

Ahem.

You Need a Budget is EXCELLENT.

It is called YNAB for short. The first 34 days are your free trial, and that is my referral link. If anyone uses it and then signs up for a subscription, we both get a month free. Also you can share a subscription with up to six people (account owner can see everything but individuals can pick and choose what they share amongst each other) so like...idk your whole polycule can be on one account. Or your kids. Whatever.

If you are a student, it's free for a year. If you aren't, a subscription is $99 for a year (paid all at once) or $14.99 monthly, which is equivalent to paying Amazon prime. Go cancel Prime and get this instead tbh.

They got a whole article just on ynab and ADHD. They also have like...a big variety of ways to access their info? They have a book, podcast episodes, YouTube videos, blog posts, q&A's, free live workshops you can join (you can request live captioning), emails they can send (if you want) a wiki, and so on. They got workshops on all kinds of topics!!

So whatever ends up working for your brain. It also has a matching app.

If you lost Mint this year they have a gajillion things for moving from Mint.

Also they have a "got five minutes?" Page which has a slider so you can decide how much attention/time you have before going on lol:

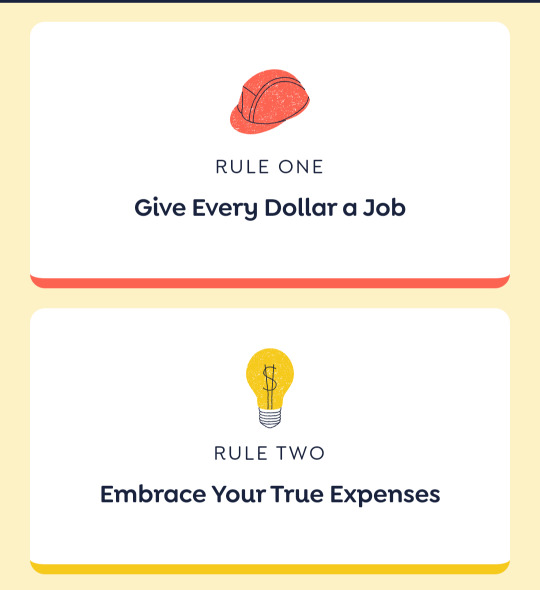

They only have 4 rules of the budget, they're simple and practical, and it doesn't get judgey or like...mean about your spending.

1. Give every dollar a job 2. Embrace your true expenses 3. Roll with the punches 4. Age your money.

THEN THEY BREAK THESE DOWN INTO SMALL STEPS FOR YOU! They even have a printable! Also these rules are great because there's built in expectations that things WILL HAPPEN and it's NOT all or nothing with a fear of total collapse into failure. Reality and The Plan don't always align, especially if you have ADHD. So it's directing our energy towards the true expenses and not clinging to The Plan!! over reality.

You can automate a lot of shit (you can sync with your bank accounts just like mint, but also automate tagging the categories of regular expenses/transactions). And if for whatever reason you accidentally do something that makes the budget look weird or wrong:

A) you can usually fix it somehow OR b) they have like, a button you can press that gives you a clean slate and archives the previous version of the budget for you.

So if you forget for a few weeks or months, or accidentally input something wildly wrong, or just don't want to look at a really terrible month anymore and feel like you need a fresh start you can usually either fix it or start fresh which is really nice.

The app also (for whatever reason) scratches my itch to have things like...have incentives or little game-like goals in a way mint never did? I don't know why. Filling up the bars or putting money into the categories to cover my expenses is satisfying lmao. You can also make a big wish expense category for all the fun shit you want, and fund it whenever you can and then you can see the little bar go up and that's fun.

Anyways I've been using it for like 6+ months now and I think it's really helped me when I use it.

610 notes

·

View notes

Note

Just saw your post about Mint, Credit Karma, and YNAB and would like to toss my two cents in. I found out about Mint late in 2023 and really liked it, but then they shut down. Looked far and wide for another free budgeting app and tbh they all kinda… sucked. Which led me to the unfortunate conclusion that if you want something decent you’re gonna have to pay for it. The three apps that have come out on top in my opinion are YNAB, Copilot, and Monarch Money. YNAB is zero based budgeting, the other two aren’t, and none of them do *everything* I want in a budgeting/personal finance app but all of them are damn good. I personally am a major proponent of Copilot, I check it daily, I adore it, I’ve been telling all my friends about it. Unfortunately it’s only available for iPhone/Mac rn but it is my absolute favorite. The other two are definitely great too. 12/10 recommend

Thanks babycakes!!! This is a great endorsement for all of us Mint refugees.

Do you guys want more content on budgeting? Traditionally we haven't been ANTI-budget, but we both use slightly different systems so we haven't written about them from personal experience. But if that's what our babies want, that's what our babies get!

Budgets Don’t Work for Everyone—Try the Spending Tracker System Instead

Season 1, Episode 7: "I'm Terrible at Budgeting. Do I Suck It Up---Or Is There Another Way?"

Did we just help you out? Tip us!

25 notes

·

View notes

Text

I haven't fully reconciled my budget and spending in YNAB for like 18 months because ~that's the magic of ADHD and depression~ but I'm mostly functional rn so I'm trying to get caught up before the end of the year (mostly so I can start January first with a comprehensive debt payment plan) and oh wow yeah that's right my cat got progressively sicker and died last Christmas and I've been mostly in a fog since. like, good work, brain, deciding to do this when you have to look at all these vet bills and food orders and increasingly desperate attempts to keep her healthy and comfortable and myself distracted as the anniversary looms 👍🏻👍🏻👍🏻

#oblig if anyone wants to try ynab i can share my trial link#cw: pet death#cw: depression#adhd#budgeting#ynab

9 notes

·

View notes

Link

Get a handle on your finances with the best Android apps for budgeting and saving money. Compare Mint, PocketGuard, YNAB, Digit, Qapital, and Acorns to find the right app for your needs. Start saving and investing for your future today! https://howtological.com/best-6-apps-for-budgeting-and-saving-money/?feed_id=1991&_unique_id=65fefde2ecf35

#Acorns#budgetingapps#Digit#financemanagement#financialgoals#financialliteracy#financialplanning#investing#Mint#moneymanagement#moneytips#personalfinance#PocketGuard#Qapital#savingmoney#YNAB

0 notes

Text

Welcome to YNAB: You're Right on Time

Screeeeeech! There it was: the trash truck just one house away, interrupting my morning coffee. Another shirt stain as I shot up to make it to the curb in time. Clad in my rattiest pajamas and house slippers, unacceptable by any social standard, I couldn’t miss pick-up for a third week in a row. With a furrowed brow and sheer determination, I got as close to sprinting as I have in my adult life.…

View On WordPress

0 notes

Text

How Apps Can Help You Manage Your Personal Finances

Personal Finances

Managing personal finances can be a daunting task, especially if you have multiple streams of income, debts to pay, and several expenses to track.

Fortunately, technology has made it easier for people to manage their finances efficiently.

Apps are now available to enable you to track your expenses, manage debt, budget, and invest your money.

With the right app, you can stay on…

View On WordPress

0 notes

Text

I don't know why I find this so funny

#decided to throw my change into month ahead and uhhh I guess I'll reach that goal in the year 2 455#better get immortal ASAP#ynab

1 note

·

View note

Text

Summary of "You Need a Budget" by Jesse Mecham

“You Need a Budget” by Jesse Mecham is a personal finance book that introduces a practical budgeting system aimed at helping individuals take control of their money and achieve financial peace. Mecham’s approach emphasizes the importance of proactive budgeting, assigning every dollar a job, and embracing a mindset of intentionality. This summary provides an overview of the key concepts and…

View On WordPress

#Budgeting#FinancialFreedom#FinancialPlanning#JesseMecham#MoneyGoals#MoneyManagement#WealthBuilding#YNAB#YouNeedABudget

0 notes

Note

I don't own any boots or high heels yet. What the fuck are you trying to do to my wallet

i'm priming my followers for when i share my ynab referral link because we all need adult supervision

#original#(i figure i'll wait until my finances are actually fixed for real before endorsing ynab lmao)#i'm doing better but the credit card situation is not yet fixed

49 notes

·

View notes

Text

the government like crying like "we're running out of money in the social security fund 😭😭😭" okay. put more money in it dumb ass bitch

3 notes

·

View notes

Link

Get a handle on your finances with the best Android apps for budgeting and saving money. Compare Mint, PocketGuard, YNAB, Digit, Qapital, and Acorns to find the right app for your needs. Start saving and investing for your future today! https://howtological.com/best-6-apps-for-budgeting-and-saving-money/?feed_id=1931&_unique_id=65efcef707782

#Acorns#budgetingapps#Digit#financemanagement#financialgoals#financialliteracy#financialplanning#investing#Mint#moneymanagement#moneytips#personalfinance#PocketGuard#Qapital#savingmoney#YNAB

0 notes

Text

A Decade Into YNAB: Here's Why My Wife and I Are Still Thankful

When my wife and I first started using YNAB in 2013, our finances were a) a mess, and b) something we didn’t know how to talk about. I was barely employed, dealing with a serious health crisis, and we were spending more than we were earning (pretty easy to do in Brooklyn). We had very different views on money, and eventually realized that we needed a new way to think about money beyond “saving =…

View On WordPress

0 notes

Text

Finding the Perfect Quicken Replacement: Top Alternatives Reviewed

Are you currently tired of managing your finances manually or using outdated software? Nowadays, there are many of personal finance software options that will make you stay along with your finances. While Quicken is a well-known name in this space, it is not the sole player. In this information, we shall explore some of the greatest quicken alternatives available today.

Money Patrol is designed with simplicity at heart, allowing users to quickly and easily set up their accounts and start tracking their finances. Its intuitive graphical user interface allows you to navigate the dashboard, view reports, analyze data, and take action on their financial decisions. MoneyPatrol also offers excellent customer support, providing users with help and advice regarding financial management and budgeting.

Here are some best Quicken alternatives available today:-

1. Mint – Mint is a popular personal finance software that is liberated to use. It syncs with your bank accounts and credit cards to keep an eye on your spending and income. Mint also offers you a complete breakdown of your finances by categorizing your spending and providing you insights into your financial health. Mint makes it easy to create budgets and track your progress throughout the month. Additionally, you are able to pay bills directly from the software and create alerts to notify you about upcoming bills or low balances.

2. Personal Capital – Personal Capital is another great personal finance software option that's free to use. Among the unique options that come with Personal Capital is its investment tracking capabilities. You are able to link your investment accounts and get reveal breakdown of your portfolio, including asset allocation, fees, and performance. Additionally, Personal Capital gives you a whole view of one's financial picture by including your cash, charge cards, and loans. You can even access a range of planning tools, including retirement planning and college savings calculators.

3. YNAB – YNAB, short for You Need A Budget, is just a personal finance software that is targeted on budgeting. It works on the unique approach called the YNAB Method, which involves giving every dollar employment and living on last month's income. YNAB also helps you place up and track your budget through the entire month, with real-time syncing across devices. Additionally, YNAB provides you with a selection of reports and insights to help you understand your spending habits and make informed decisions.

4. Moneydance – Moneydance is just a personal finance software that is similar to Quicken, but with increased modern features and design. It may sync with your bank accounts, charge cards, and investment accounts to provide you with an entire financial picture. Moneydance also supports budgeting and bill management, with customizable reports and reminders. Additionally, Moneydance provides an array of personal finance tools, including check printing and investment tracking.

5. Tiller Money – Tiller Money is really a personal finance software that helps automate your finances by importing your transaction data into a Google Sheets template. It offers you complete control over your finances, with customizable budgeting, expense tracking, and debt management tools. Additionally, Tiller Money supports real-time syncing and provides you with a variety of reports and insights to assist you make informed decisions.

Conclusion:

There are lots of Quicken alternatives available today, each having its own unique features and benefits. If you are searching for free or paid software, budgeting or investment tracking, there's a personal finance software out there for you. Consider giving one of these top picks a take to and see how it can help you gain control over your finances.

1 note

·

View note

Text

The one thing I dislike about YNAB (other than how expensive it is) is that it's now become an annoyance to me to transfer money between my accounts but I don't want to keep 500 Euro in my primary account so I kind of have to

#but what I love about YNAB is that it does work very well for me#what student has fucking 550 euro in their bank#yes all of it is intended to get spent eventually#but that is in a way the wonder of YNAB#bc I want to save the money because I want to buy that thing

0 notes

Text

Ynab budgeting how to video

Variable expenses are things you have more control over, such as groceries, travel, dining out, shopping, and charitable donations. In general, your budget should be divided into three categories of expenses: fixed, discretionary, and savings.įixed expenses are things you can’t avoid paying, such as rent or a mortgage, utilities, and loans. You can make a budget for a specific time frame (monthly or annual are the most common). Take how much you expect to earn next month and use the expenditure percentages from step three to estimate what you can spend. You can now set up next month’s budget.For instance, maybe your typical $500 grocery bill jumps to $700 in November and December, or you pay your homeowners insurance premium at the beginning of each year. Estimate how much you’ll spend in different categories each month over the next year.Use last year’s pay stubs as a reference point and adjust as needed (perhaps you recently got a raise or finalized a new business deal). Estimate how much you’ll earn each month over the next year.Variable/discretionary ordinary living expenses (such as food, clothing, household expenses, medical payments, and other items for which your monthly spending tends to fluctuate).Fixed costs (such as housing payments, utility bills, charitable contributions, insurance premiums, and loan payments).Separate your spending categories into main buckets.(This is an especially useful exercise if you have uneven income.) For instance, let’s say you spent $500 in January on groceries, which was 12% of your household earnings. Note how much you spent in each category every month, as well as what percentage of your monthly income that spending represented. Categorize all of your expenses over the past year.Add up your take-home pay over the past year.Most institutions let you export your transactions as a CSV file that you can open in Google Sheets, Excel, or Numbers. A year’s worth can give you a good sense of how much you tend to spend over a given period of time. Collect all of your bank and credit card statements over the past year.(Ever get hit with a large bill, such as for an auto repair or emergency dental treatment? Those kinds of things can throw your budget off track.) Spreadsheet-based budgets (and some other budgeting tools) prompt you to create a myriad of categories and assign a dollar amount to each one, which is not only overwhelming but also likely to fail. It tracks your spending, revolving bills, savings goals, and earnings history to estimate how much you have left to spend in a given month in any category you want. We recommend Simplifi for most people because it’s a happy medium between the two. Conversely, zero-balance apps encourage a more hands-on approach, forcing you to account for every dollar you bring in (X amount for savings, Y amount for rent, and so on), but they tend to be idiosyncratic and costly. Tracking apps offer a 30,000-foot view of your finances, display your transactions in real time, and require very little effort to set up. When you roll your own spreadsheet, it’s surprisingly complex to allow for cleared and uncleared transactions.There are two basic types of budget apps: trackers ( à la Mint) and zero-balancers. YNAB walks you through the process of reconciling your account. Reviewing Your (shared) transactions and resolving any discrepancies, aka budget reconciliation, is also very simple. You might actually keep a true budget instead of a ledger. If that happens it’s much easier to help them be engaged from the beginning thanks to a dedicated budgeting tool. Think about the following: your partner might want to pitch in from time to time, or sooner or later the person managing the budget will change. It provides a better, more efficient interface than Excel. It’s a system that doesn’t need maintenance and it’s constantly improving. It takes most of the work of your hands allowing you to purely focus on budgeting. When talking about limitations it can be good to compare to YNAB. These accounts can be investment accounts but also a mortgage. This an overview of my tracking accounts.

0 notes

Last Seen Blogs

bioresilient

THE ONE AND ONLY.

cryptopressreleasefirm

Untitled

dilkizeenat

~hello frens~

mathandnumberystuff

math discoveries