#consolidation

Text

Rural towns and poor urban neighborhoods are being devoured by dollar stores

Across America, rural communities and big cities alike are passing ordinances limiting the expansion of dollar stores, which use a mix of illegal predatory tactics, labor abuse, and monopoly consolidation to destroy the few community grocery stores that survived the Walmart plague and turn poor places into food deserts.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/03/27/walmarts-jackals/#cheater-sizes

"The Dollar Store Invasion," is a new Institute For Local Self Reliance (ILSR) report by Stacy Mitchell, Kennedy Smith and Susan Holmberg. It paints a detailed, infuriating portrait of the dollar store playback, and sets out a roadmap of tactics that work and have been proven in dozens of places, rural and urban:

https://cdn.ilsr.org/wp-content/uploads/2023/01/ILSR-Report-The-Dollar-Store-Invasion-2023.pdf

The impact of dollar stores is plainly stated in the introduction: "dollar stores drive grocery stores and other retailers out of business, leave more people without access to fresh food, extract wealth from local economies, sow crime and violence, and further erode the prospects of the communities they target."

This new report builds on ILSR's longstanding and excellent case-studies, augmenting them with the work of academic geographers who are just starting to literally map out the dollar store playbook, identifying the way that a dollar stores will target, say, the last grocery store in a Black neighborhood and literally surround it, like hyenas cornering weakened prey. This tactic is repeated whenever a new grocer opens in the neighborhood: dollar stores "carpet bomb" the surrounding blocks, ensuring that the new store closes as quickly as it opens.

One important observation is the relationship between these precarious neighborhood grocers and Walmart and its other big-box competitors. Deregulation allowed Walmart to ring cities with giant stores that relied on "predatory buying" (wholesale terms that allowed Walmart to sell goods more cheaply than its competitors bought them, and also rendered its suppliers brittle and sickly, and forced down the wages of those suppliers' workers). This was the high cost of low prices: neighborhoods lost their local grocers, and community dollars ceased to circulate in the community, flowing to Walmart and its billionaire owners, who spent it on union busting and political campaigns for far-right causes, including the defunding of public schools.

This is the landscape where the dollar stores took root: a nation already sickened by an apex predator, which left a productive niche for jackals to pick off the weakened survivors. Wall Street loved the look of this: the Private equity giant KKR took over Dollar General in 2007 and went on a acquisition and expansion bonanza. Even after KKR formally divested itself of Dollar General, the company's hit-man Michael M Calbert stayed on the board, rising to chairman.

The dollar store market is a duopoly. Dollar General's rival is Dollar Tree, another gelatinous cube of a company that grew by absorbing many of its competitors, using Wall Street's money. These acquisitions are now notorious for the weaknesses they exposed in antitrust practice. For example, when Dollar Tree bought Family Dollar, growing to 14,000 stores, the FTC waved the merger through on condition that the new business sell off 330 of them. These ineffectual and pointless merger conditions are emblematic of the inadequacy of antitrust as it was practiced from the Reagan administration until the sea-change under Biden, and Dollar Tree/Family Dollar is the poster child for more muscular enforcement.

The duopoly has only grown since then. Today, Dollar General and Dollar Tree have more than 34,000 US outlets - more than Starbucks, #Walmart, McDonalds and Target - combined.

Destroying a community's grocery store rips out its heart. Neighborhoods without decent access to groceries impose a tax on their already-struggling residents, forcing them to spend hours traveling to more affluent places, or living off the highly processed, deceptively priced (more on this later) goods for sale on the dollar store shelves.

Take Cleveland, once served by a small family chain called Dave's Market that had served its communities since the 1920s. Dave's store in the Collinwood neighborhood was targeted by Family Dollar and Dollar General, which opened seven stores within two miles of the Dave's outlet. The dollar stores targeted the only profitable part of Dave's business - the packaged goods (fresh produce is a money-loser, subsidized by packaged good).

The dollar stores used a mix of predatory buying and "cheater sizes" (packaged goods that are 10-20% smaller than those sold in regular outlets, which are not available to other retailers) to sell goods at prices that Dave's couldn't match, driving Dave's out of business.

Typical dollar stores stock no fresh produce or meat. If your only grocer is a dollar store, your only groceries are highly processed, packaged foods, often sold in deceptive single-serving sizes that actually cost more per ounce than the products that the defunct neighborhood grocer once sold.

Dollar stores don't just target existing food deserts - they create them. Dollar stores preferentially target Black and brown neighborhoods with just a single grocer and then they use predatory pricing (subsidizing the cost of goods and selling them at a loss) and predatory buying to force that grocery store under and tip the neighborhood into food desert status.

Dollar stores don't just target Black and brown urban centers; they also go after rural communities. The commonality here is that both places are likely to be served by independent grocers, not chains, and these indies can't afford a pricing war with the Wall Street-backed dollar store duopoly.

As mentioned, the "predatory buying" of dollar stores is illegal - it was outlawed in 1936 under the Robinson-Patman Act, which required wholesalers to offer goods to all merchants on the same terms. 40 years ago, we stopped enforcing those laws, leading the rise and rise of big box stores and the destruction of the American Main Street.

The lawmakers who passed Robinson-Patman knew what they were doing. They were aware of what contemporary economists call "the waterbed effect," where wholesalers cover the losses from their massive discounts to major retailers by hiking prices on smaller stores, making them even less competitive and driving more market consolidation.

When dollar stores invade your town or neighborhood, they don't just destroy the food choices, they also come for neighborhood jobs. Where a community grocer typically employs 12 or more people, Dollar General employs about 8 per store. Those workers are paid less, too: 92% of Dollar General's workers earn less than $15/h, making Dollar General the worst employer of the 66 large service-sector firms.

Dollar stores also lean heavily into the tactic of turning nearly every role at its store into a "management" job, because managers aren't entitled to overtime pay. That's how you can be the "manger" of a dollar store and take home $40,000 a year while working more than 40 hours every single week.

Understaffing stores turns them into crime magnets. Shootings at dollar stores are routine. Between 2014-21, 485 people were shot at dollar stores - 156 of them died. Understaffed warehouses are vermin magnets. In the Eastern District of Arkansas, Family Dollar was subpoenaed after a rat infestation at its distribution centers that contaminated the food, medicines and cosmetics at 400 stores.

The ILSR doesn't just document the collapse of American communities - it fights back, so this report ends with a lengthy section on proven tactics and future directions for repelling the dollar store invasion. Since 2019, 75 communities have blocked proposals for new dollar stores - more than 50 of those cases happened in 2021/22.

54 towns, from Birmingham, AB to Fort Worth, TX to Kansas City, KS, have passed laws to "sharply restrict new dollar stores, typically by barring them from opening within one to two miles of an existing dollar store."

To build on this momentum, the authors call for a "reinvigoration of antitrust laws," especially the Robinson-Patman Act. Banning predatory buying would go far to creating a level playing field for independent grocers hoping to fight off a dollar store infestation.

Further, we need the FTC and Department of Justice Antitrust Divition to block mergers between dollar-store chains and unwind the anticompetitve mergers that were negligently waved through under previous administrations (thankfully, top enforcers like Jonathan Kantor and Lina Khan are on top of this!).

We need to free up capital for community banks that will back community grocers. That means rolling back the bank deregulation of the 1980s/90s that allowed for bank consolidation and preferential treatment for large corporations, while reducing lending to small businesses and destroying regional banks. Congress should cap the market share any bank can hold, break up the biggest banks, and require banks to preference loans for community businesses. We also need to end private equity and Wall Street's rollup bonanza.

All of that sounds like a tall order - and it is! But the good news is that it's not just groceries at stake here. Every kind of community business, from pet groomers to hairdressers to funeral homes, falls into the antitrust "Twilight Zone," of acquisitions under $101m. With 60% of Boomer-owned businesses expected to sell in the coming decade, 2.9m businesses employing 32m American workers are slated to be gobbled up by private equity:

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

Whether you're burying a loved one, getting dialysis, getting your cat fixed or having your dog's nails trimmed, you are already likely to be patronizing a business that has been captured by private equity, where the service is worse, the prices are higher and the workers earn less for harder jobs. Everyone has a stake in financial regulation. We are all in this fight, except for the eminently guillotineable PE barons, and you know, fuck those guys

At the state level, the authors propose new muscular enforcement regimes and new laws to protect small businesses from unfair competition. They also call on states to increase the power of local governments to reject new dollar store applications, amending land use guidelines to require "cultivating net economic growth, ensuring that everyone has access to healthy food, and protecting environmental resources.

If all of this has you as fired up as it got me this morning, check out ILSR's "How to Stop Dollar Stores in Your Community" resources:

http://ilsr.org/dollar-stores

I’m kickstarting the audiobook for my next novel, a post-cyberpunk anti-finance finance thriller about Silicon Valley scams called Red Team Blues. Amazon’s Audible refuses to carry my audiobooks because they’re DRM free, but crowdfunding makes them possible.

Image:

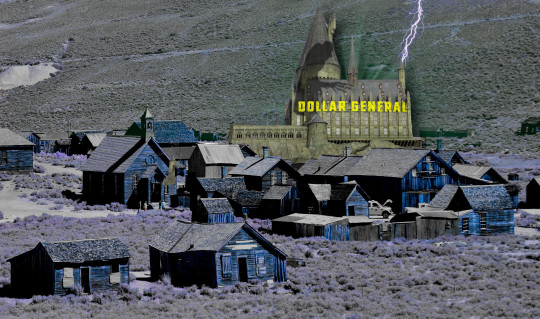

Mike McBey (modified)

https://www.flickr.com/photos/158652122@N02/38893547595/

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/

[Image ID: A ghost town; it is towered over by a haunted castle with a Dollar General sign on it, with the shadow of Count Orlock cast over its tower. One of its turrets is being struck by lightning.]

#pluralistic#shrinkflation#institute for local self reliance#ilsr#dollar tree#dollar general#dollar stores#groceries#food deserts#kkr#pe#private equity#predatory buying#predatory pricing#Robinson-Patman Act#consolidation#monopoly#monopsony#care labor

184 notes

·

View notes

Text

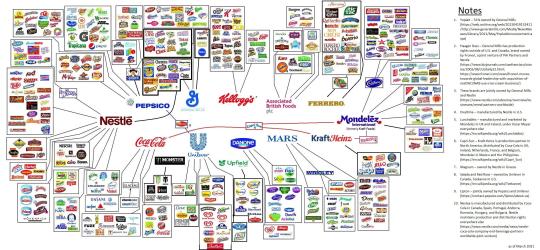

"My attempt at a Brand Map"

posted on Reddit r/coolguides

#brands#chart#categories#corporations#food companies#consolidation#Kellogg's#Mondelez#Coca-Cola#Pepsi#Nestle#Mars#Unilever#Ferrero#Kraft Heinz#General Mills#Dannon#Associated British Foods#Lipton#Wrigley#global conglomerates

25 notes

·

View notes

Text

This merging and consolidation of fur is a work of art 🖼️ 😋🤗

147 notes

·

View notes

Text

If you didn't, do so..

18 notes

·

View notes

Note

can i hold hands with phongraph and consolidation. if self shipping is ok

you have two paws, don't you

10 notes

·

View notes

Text

Marriages of propertied families were mostly arranged with a view to consolidating fortunes and providing a reliable wife and mother for the family and their business.

"Normal Women: 900 Years of Making History" - Philippa Gregory

#book quotes#normal women#philippa gregory#nonfiction#marriage#consolidation#fortunes#reliable#wife#mother#matriarch#arranged marriage

2 notes

·

View notes

Text

4 ways to advance your global security operations center - CyberTalk

New Post has been published on https://thedigitalinsider.com/4-ways-to-advance-your-global-security-operations-center-cybertalk/

4 ways to advance your global security operations center - CyberTalk

EXECUTIVE SUMMARY:

If your organization maintains a Global Security Operations Center (GSOC), ensure that you’re not heavily reliant on legacy systems and processes. In this article, find out about how to strategically advance your operations, enabling you to effectively prevent threats and drive more sustainable business outcomes.

What is a global security operations center?

In the early days of computing, a Security Operations Center (SOC) functioned as a physical ‘command center’ for security analysts. SOCs were comprised of rooms where staff sat shoulder-to-shoulder, looking at screens showing details from dozens of different security tools.

Large organizations with multiple Security Operations Centers (SOCs) began to consolidate them into Regional Security Operations Centers (RSOC) or a Global Security Operations Center, leading to faster remediation, reduced risk and a stronger cyber security posture overall.

In terms of function, a global security operations center monitors security, addresses threats before they become disruptive issues, responds to incidents, and liaise with stakeholders.

What are the benefits of a global security operations center?

A global security operations center allows an organization to contend with diverse security threats at-scale. Specific benefits include continuous monitoring, centralized visibility, increased efficiency and reduced costs. A global security operations center can also oversee and coordinate regional SOCs, network operations centers (NOCs) and operational teams.

What makes a good global security operations center?

For any global security operations center, access to timely and relevant threat intelligence is critical. GSOC staff need to remain updated on emerging cyber and physical security threats, as to stay ahead of potential risks.

Highly trained staff who can collaborate effectively with all stakeholders are also invaluable assets for a global security operations center.

Top-tier GSOCs have built-in redundancies of all kinds; from communication to data backups.

All GSOCs need to ensure that their organization adheres to industry regulations and compliance standards.

4 ways to advance your global security operations center

1. Ensure that the cyber security strategy aligns with business objectives. GSOCs need to know what the business aims to achieve, and must understand the corresponding threats and vulnerabilities that could hamper progress. Risk assessments should include both cyber security and business stakeholders, who can assist with the identification of resources that require protection.

Security policies and standards should also meet customer expectations. To gain insight around this, cyber security leaders may wish to join business planning meetings. Attendance can also assist with awareness around any upcoming business changes and implementation of appropriate, corresponding security measures.

2. Global security operations centers should shift towards the zero trust model. Zero trust is designed to reduce cyber security risk by eliminating implicit trust within an organization’s IT infrastructure. It states that a user should only have access and permissions required to fulfill their role.

Implementation of zero trust can be tough, especially if an organization has numerous interconnected and distributed systems. Organizations can simplify zero trust implementation through vendor-based solutions.

Tools like Quantum SASE Private Access allow teams to quickly connect users, sites, clouds and resources with a zero trust network access policy. In under an hour, security teams can apply least privilege to any enterprise resource.

Security gateways also enable organizations to create network segmentation. With detailed visibility into users, groups, applications, machines and connection types, gateways allow security professionals to easily set and enforce a ‘least privileged’ access policy.

3. Advance your global security operations center by mapping to industry standards and detection frameworks. Explore the MITRE ATT&CK framework. Standards like NIST and ISO27001 can also assist with identifying and reconciling gaps in an organization’s existing security systems.

4. Consider deploying a tool like Horizon SOC, which allows organizations to utilize the exact same tools that are used by Check Point Security Research, a leading provider of cyber threat intelligence globally.

Horizon SOC offers 99.9% precision across network, cloud, endpoint, mobile and IoT. Easily deployed as a unified cloud-based platform, it has powerful AI-based features designed to increase security operations efficiency.

Further thoughts

Strategic updates to global security operations centers not only enhance cyber security, they also enrich overarching business resilience – an increasingly common point of discussion among C-level stakeholders and the board.

By implementing the suggestions outlined above, organizations will maximize their opportunities for business longevity and continued business success.

Related resources

#ai#amp#applications#Article#assets#awareness#backups#board#Business#business resilience#c-level#Check Point#Cloud#clouds#collaborate#command#communication#compliance#computing#consolidation#continuous#cyber#cyber security#cyber security strategy#cyber threat#data#details#detection#efficiency#endpoint

2 notes

·

View notes

Text

Futility. Futility shapes the world. History is a story of futilities, progress is a sequence of futilities. “Development!” says the futurist. “Loss,” says the rebel. “Hangover!” shouts the moralist from the back row. “Failure,” says the angry rebel. “Time is grey,” he says. The Creator’s failure is an introduction to the era. Kras Mazov shoots himself in the head and Abadanaiz takes poison with Dobrev on the Ozonne islands. The wind blows sand over their bones under the palm trees. Who was supposed to know? Good people from all over the world came together. Teachers, writers, and migrant workers huddle in trenches... young soldiers desert their units. What beautiful songs they sing! Brave children are history’s favourites, so it seems to them, and they wave white flags with silver horned crowns.

And they lose.

Coups are crushed. Anarchists are piled into mass graves on the Great Blue. Communists, beaten back from the isola of Graad, retreat to Samara and become a degenerate worker’s state ruled by bureaucrats. The disappearance of revolutionary lovers is resolved thirty-five years later when the hugging skeletons of Abadanaiz and Dobrev are found on the shore of an unnamed Ozonne island by Riche LePomme’s eight-year-old son Eugene during a Saturday evening outing. Wearing shorts and a butterfly net, he stands and looks perplexedly at the bones of his past as they cling together. Faded and smooth. Where does one begin and the other end? Time has mixed them up like a deck of cards. Afterwards, Riche erects a hotel there along with a now world-famous health centre.

But the greatest failure is not how Mazov’s global revolution ended in bloodshed and then defeat, nor is it how the bones of revolutionary lovers are now displayed in an aromatherapy waiting room. With internal unrest suppressed, Graad becomes a world power, a giant nation, its cities thriving and the light of this growth shining like a sparkling network from orbit. Whole nations disappear from the map of the world. Nations where Mazov once had many supporters. Nations like Zsiemsk. Nations whose peoples are derogatorily referred to as “kojkos”. And this goes on for so long that eventually they even begin to call themselves that.

#quotes#fiction#sacred and terrible air#disco elysium#worldbuilding#history#capitalism#communism#anarchism#revolution#progress#development#futility#failure#racism#consolidation#homogenization

9 notes

·

View notes

Text

A bit of owed art for @ladyteelia!

Consolidation is thinking of her favorite spooky man!

2 notes

·

View notes

Text

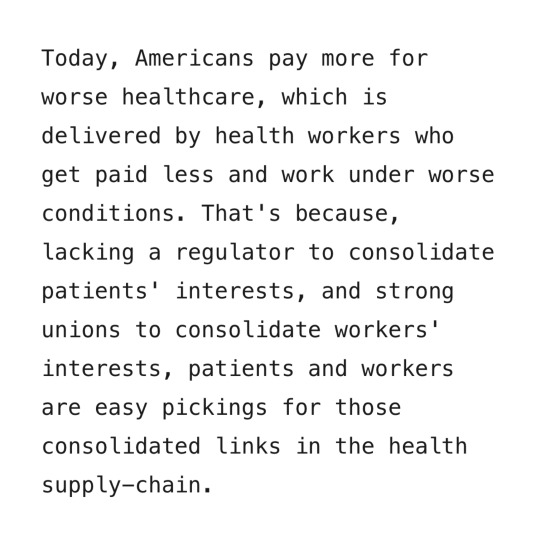

The antitrust Twilight Zone

Funeral homes were once dominated by local, family owned businesses. Today, odds are, your neighborhood funeral home is owned by Service Corporation International, which has bought hundreds of funeral homes (keeping the proprietor’s name over the door), jacking up prices and reaping vast profits.

Funeral homes are now one of America’s most predatory, vicious industries, and SCI uses the profits it gouges out of bereaved, reeling families to fuel more acquisitions — 121 more in 2021. SCI gets some economies of scale out of this consolidation, but that’s passed onto shareholders, not consumers. SCI charges 42% more than independent funeral homes.

https://pluralistic.net/2022/09/09/high-cost-of-dying/#memento-mori

SCI boasts about its pricing power to its investors, how it exploits people’s unwillingness to venture far from home to buy funeral services. If you buy all the funeral homes in a neighborhood, you have near-total control over the market. Despite these obvious problems, none of SCI’s acquisitions face any merger scrutiny, thanks to loopholes in antitrust law.

These loopholes have allowed the entire US productive economy to undergo mass consolidation, flying under regulatory radar. This affects industries as diverse as “hospital beds, magic mushrooms, youth addiction treatment centers, mobile home parks, nursing homes, physicians’ practices, local newspapers, or e-commerce sellers,” but it’s at its worst when it comes to services associated with trauma, where you don’t shop around.

Think of how Envision, a healthcare rollup, used the capital reserves of KKR, its private equity owner, to buy emergency rooms and ambulance services, elevating surprise billing to a grotesque art form. Their depravity knows no bounds: an unconscious, intubated woman with covid was needlessly flown 20 miles to another hospital, generating a $52k bill.

https://pluralistic.net/2022/03/14/unhealthy-finances/#steins-law

This is “the health equivalent of a carjacking,” and rollups spread surprise billing beyond emergency rooms to

anesthesiologists, radiologists, family practice, dermatology and others. In the late 80s, 70% of MDs owned their practices. Today, 70% of docs work for a hospital or corporation.

How the actual fuck did this happen? Rollups take place in “antitrust’s Twilight Zone,” where a perfect storm of regulatory blindspots, demographic factors, macroeconomics, and remorseless cheating by the ultra-wealthy has laid waste to the American economy, torching much of the US’s productive capacity in an orgy of predatory, extractive, enshittifying mergers.

The processes that underpin this transformation aren’t actually very complicated, but they are closely interwoven and can be hard to wrap your head around. “The Roll-Up Economy: The Business of Consolidating Industries with Serial Acquisitions,” a new paper from The American Economic Liberties Project by Denise Hearn, Krista Brown, Taylor Sekhon and Erik Peinert does a superb job of breaking it down:

http://www.economicliberties.us/wp-content/uploads/2022/12/Serial-Acquisitions-Working-Paper-R4-2.pdf

The most obvious problem here is with the MergerScrutiny process, which is when competition regulators must be notified of proposed mergers and must give their approval before they can proceed. Under the Hart-Scott-Rodino Act (HSR) merger scrutiny kicks in for mergers when the purchase price is $101m or more. A company that builds up a monopoly by acquiring hundreds of small businesses need never face merger scrutiny.

The high merger scrutiny threshold means that only a very few mergers are regulated: in 2021, out of 21,994 mergers, only 4,130 (<20%) were reported to the FTC. 2020 saw 16,723 mergers, with only 1.637 (>10%) being reported to the FTC.

Serial acquirers claim that the massive profits they extract by buying up and merging hundreds of businesses are the result of “efficiency” but a closer look at their marketplace conduct shows that most of those profits come from market power. Where efficiences are realized, they benefit shareholders, and are not shared with customers, who face higher prices as competition dwindles.

The serial acquisition bonanza is bad news for supply chains, wages, the small business ecosystem, inequality, and competition itself. Wherever we find concentrated industires, we find these under-the-radar rollups: out of 616 Big Tech acquisitions from 2010 to 2019, 94 (15%) of them came in for merger scrutiny.

The report’s authors quote FTC Commissioner Rebecca Slaughter: “I think of serial acquisitions as a Pac-Man strategy. Each individual merger viewed independently may not seem to have significant impact. But the collective impact of hundreds of smaller acquisitions, can lead to a monopolistic behavior.”

It’s not just the FTC that recognizes the risks from rollups. Jonathan Kanter, the DoJ’s top antitrust enforcer has raised alarms about private equity strategies that are “designed to hollow out or roll-up an industry and essentially cash out. That business model is often very much at odds with the law and very much at odds with the competition we’re trying to protect.”

The DoJ’s interest is important. As with so many antitrust failures, the problem isn’t in the law, but in its enforcement. Section 7 of the Clayton Act prohibits serial acquisitions under its “incipient monopolization” standard. Acquisitions are banned “where the effect of such acquisition may be to substantially lessen competition between the corporation whose stock is so acquired and the corporation making the acquisition.” This incipiency standard was strengthened by the 1950 Celler-Kefauver Amendment.

The lawmakers who passed both acts were clear about their legislative intention — to block this kind of stealth monopoly formation. For decades, that’s how the law was enforced. For example, in 1966, the DoJ blocked Von’s from acquiring another grocer because the resulting merger would give Von’s 7.5% of the regional market. While Von’s is cited by pro-monopoly extremists as an example of how the old antitrust system was broken and petty, the DoJ’s logic was impeccable and sorely missed today: they were trying to prevent a rollup of the sort that plagues our modern economy.

As the Supremes wrote in 1963: “A fundamental purpose of [stronger incipiency standards was] to arrest the trend toward concentration, the tendency of monopoly, before the consumer’s alternatives disappeared through merger, and that purpose would be ill-served if the law stayed its hand until 10, or 20, or 30 [more firms were absorbed].”

But even though the incipiency standard remains on the books, its enforcement dwindled away to nothing, starting in the Reagan era, thanks to the Chicago School’s influence. The neoliberal economists of Chicago, led by the Nixonite criminal Robert Bork, counseled that most monopolies were “efficient” and the inefficient ones would self-correct when new businesses challenged them, and demanded a halt to antitrust enforcement.

In 1982, the DoJ’s merger guidelines were gutted, made toothless through the addition of a “safe harbor” rule. So long as a merger stayed below a certain threshold of market concentration, the DoJ promised not to look into it. In 2000, Clinton signed an amendment to the HSR Act that exempted transactions below $50m. In 2010, Obama’s DoJ expanded the safe harbor to exclude “[mergers that] are unlikely to have adverse competitive effects and ordinarily require no further analysis.”

These constitute a “blank check” for serial acquirers. Any investor who found a profitable strategy for serial acquisition could now operate with impunity, free from government interference, no matter how devastating these acquisitions were to the real economy.

Unfortunately for us, serial acquisitions are profitable. As an EY study put it: “the more acquisitive the company… the greater the value created…there is a strong pattern of shareholder value growth, correlating with frequent acquisitions.” Where does this value come from? “Efficiencies” are part of the story, but it’s a sideshow. The real action is in the power that consolidation gives over workers, suppliers and customers, as well as vast, irresistable gains from financial engineering.

In all, the authors identify five ways that rollups enrich investors:

I. low-risk expansion;

II. efficiencies of scale;

III. pricing power;

IV. buyer power;

V. valuation arbitrage.

The efficiency gains that rolled up firms enjoy often come at the expense of workers — these companies shed jobs and depress wages, and the savings aren’t passed on to customers, but rather returned to the business, which reinvests it in gobbling up more companies, firing more workers, and slashing survivors’ wages. Anything left over is passed on to the investors.

Consolidated sectors are hotbeds of fraud: take Heartland, which has rolled up small dental practices across America. Heartland promised dentists that it would free them from the drudgery of billing and administration but instead embarked on a campaign of phony Medicare billing, wage theft, and forcing unnecessary, painful procedures on children.

Heartland is no anomaly: dental rollups have actually killed children by subjecting them to multiple, unnecessary root-canals. These predatory businesses rely on Medicaid paying for these procedures, meaning that it’s only the poorest children who face these abuses:

https://pluralistic.net/2022/11/17/the-doctor-will-fleece-you-now/#pe-in-full-effect

A consolidated sector has lots of ways to rip off the public: they can “directly raise prices, bundle different products or services together, or attach new fees to existing products.” The epidemic of junk fees can be traced to consolidation.

Consolidators aren’t shy about this, either. The pitch-decks they send to investors and board members openly brag about “pricing power, gained through acquisitions and high switching costs, as a key strategy.”

Unsurprisingly, investors love consolidators. Not only can they gouge customers and cheat workers, but they also enjoy an incredible, obscure benefit in the form of “valuation arbitrage.”

When a business goes up for sale, its valuation (price) is calculated by multiplying its annual cashflow. For small businesses, the usual multiplier is 3–5x. For large businesses, it’s 10–20x or more. That means that the mere act of merging a small business with a large business can increase its valuation sevenfold or more!

Let’s break that down. A dental practice that grosses $1m/year is generally sold for $3–5m. But if Heartland buys the practice and merges it with its chain of baby-torturing, Medicaid-defrauding dental practices, the chain’s valuation goes up by $10–20m. That higher valuation means that Heartland can borrow more money at more favorable rates, and it means that when it flips the husks of these dental practices, it expects a 700% return.

This is why your local veterinarian has been enshittified. “A typical vet practice sells for 5–8x cashflow…American Veterinary Group [is] valued at as much as 21x cashflow…When a large consolidator buys a $1M cashflow clinic, it may cost them as little as $5M, while increasing the value of the consolidator by $21M. This has created a goldrush for veterinary consolidators.”

This free money for large consolidators means that even when there are better buyers — investors who want to maintain the quality and service the business offers — they can’t outbid the consolidators. The consolidators, expecting a 700% profit triggered by the mere act of changing the business’s ownership papers, can always afford to pay more than someone who merely wants to provide a good business at a fair price to their community.

To make this worse, an unprecedented number of small businesses are all up for sale at once. Half of US businesses are owned by Boomers who are ready to retire and exhausted by two major financial crises within a decade. 60% of Boomer-owned businesses — 2.9m businesses of 11 or so employees each, employing 32m people in all — are expected to sell in the coming decade.

If nothing changes, these businesses are likely to end up in the hands of consolidators. Since the Great Financial Crisis of 2008, private equity firms and other looters have been awash in free money, courtesy of the Federal Reserve and Congress, who chose to bail out irresponsible and deceptive lenders, not the borrowers they preyed upon.

A decade of zero interest rate policy (ZIRP) helped PE grow to “staggering” size. Over that period, America’s 2,000 private equity firms raised buyout warchests totaling $2t. Today, private equity owned companies outnumber publicly traded firms by more than two to one.

Private equity is patient zero in the serial acquisition epidemic. The list of private equity rollup plays includes “comedy clubs, ad agencies, water bottles, local newspapers, and healthcare providers like hospitals, ERs, and nursing homes.”

Meanwhile, ZIRP left the nation’s pension funds desperate for returns on their investments, and these funds handed $480b to the private equity sector. If you have a pension, your retirement is being funded by investments that are destroying your industry, raising your rent, and turning the nursing home you’re doomed to into a charnel house.

The good news is that enforcers like Kanter have called time on the longstanding, bipartisan failure to use antitrust laws to block consolidation. Kanter told the NY Bar Association: “We have an obligation to enforce the antitrust laws as written by Congress, and we will challenge any merger where the effect ‘may be substantially to lessen competition, or to tend to create a monopoly.’”

The FTC and the DOJ already have many tools they can use to end this epidemic.

They can revive the incipiency standard from Sec 7 of the Clayton Act, which bans mergers where “the effect of such acquisition may be substantially to lessen competition, or to tend to create a monopoly.”

This allows regulators to “consider a broad range of price and non-price effects relevant to serial acquisitions, including the long-term business strategy of the acquirer, the current trend or prevalence of concentration or acquisitions in the industry, and the investment structure of the transactions”;

The FTC and DOJ can strengthen this by revising their merger guidelines to “incorporate a new section for industries or markets where there is a trend towards concentration.” They can get rid of Reagan’s 1982 safe harbor, and tear up the blank check for merger approval;

The FTC could institute a policy of immediately publishing merger filings, “the moment they are filed.”

Beyond this, the authors identify some key areas for legislative reform:

Exempt the FTC from the Paperwork Reduction Act (PRA) of 1995, which currently blocks the FTC from requesting documents from “10 or more people” when it investigates a merger;

Subject any company “making more than 6 acquisitions per year valued at $70 million total or more” to “extra scrutiny under revised merger guidelines, regardless of the total size of the firm or the individual acquisitions”;

Treat all the companies owned by a PE fund as having the same owner, rather than allowing the fiction that a holding company is the owner of a business;

Force businesses seeking merger approval to provide “any investment materials, such as Private Placement Memorandums, Management or Lender Presentations, or any documents prepared for the purposes of soliciting investment. Such documents often plainly describe the anticompetitive roll-up or consolidation strategy of the acquiring firm”;

Also force them to provide “loan documentation to understand the acquisition plans of a company and its financing strategy;”

When companies are found to have violated antitrust, ban them from acquiring any other company for 3–5 years, and/or force them to get FTC pre-approval for all future acquisitions;

Reinvigorate enforcement of rules requiring that some categories of business (especially healthcare) be owned by licensed professionals;

Lower the threshold for notification of mergers;

Add a new notification requirement based on the number of transactions;

Fed agencies should automatically share merger documents with state attorneys general;

Extend civil and criminal antitrust penalties to “investment bankers, attorneys, consultants who usher through anticompetitive mergers.”

#pluralistic#american economic liberties project#jonathan kantor#doj#clayton act#hart-scott-rodino act#zirp#financial engineering#monopoly#consolidation#rollups#debt financing#private equity#hedge funds#serial acquirers#antitrust#incipiency standard#Celler-Kefauver Act#vons#brown shoe#boomers#silver wave#labor#monopsony#pricing power#kkr#envision#funeral homes#surprise billing#sci

103 notes

·

View notes

Text

Stocks Seeking Their Daily Cycle Low

Stocks broke bearishly out of consolidation on Wednesday, closing below the 10 day MA. Stocks went on to deliver bearish follow through on Thursday.

Thursday was day 28, placing stocks in the early part of its timing band for a DCL. Stocks formed a swing high on Thursday to signal the daily cycle decline. We will be watching the rising 50 day MA for possible support for the DCL to form. Stocks…

View On WordPress

0 notes

Text

Not great.

#private equity#monopoly#monopsony#consolidation#anti-competitive#economy#economics#us politics#us police#politics

1 note

·

View note

Text

The USD/JPY returns to consolidation and I want to see the price taking buystop and high quality OB to short.

0 notes

Text

How platformization is transforming cyber security - CyberTalk

New Post has been published on https://thedigitalinsider.com/how-platformization-is-transforming-cyber-security-cybertalk/

How platformization is transforming cyber security - CyberTalk

With more than 15 years of experience in cyber security, Manuel Rodriguez is currently the Security Engineering Manager for the North of Latin America at Check Point Software Technologies, where he leads a team of high-level professionals whose objective is to help organizations and businesses meet their cyber security needs. Manuel joined Check Point in 2015 and initially worked as a Security Engineer, covering Central America, where he participated in the development of important projects for multiple clients in the region. He had previously served in leadership roles for various cyber security solution providers in Colombia.

In this insightful Cyber Talk interview, Check Point expert Manuel Rodriguez discusses “Platformization”, why cyber security consolidation matters, how platformization advances your security architecture and more. Don’t miss this!

The word “platformization” has been thrown around a lot recently. Can you define the term for our readers?

Initially, a similar term was used in the Fintech industry. Ron Shevlin defined it as a plug and play business model that allows multiple participants to connect to it, interact with each other and exchange value.

Now, this model aligns with the needs of organizations in terms of having a cyber security platform that can offer the most comprehensive protection, with a consolidated operation and easy enablement of collaboration between different security controls in a plug and play model.

In summary, platformization can be defined as the moving from a product-based approach to a platform-based approach in cyber security.

How does platformization differ from the traditional way in which tech companies develop and sell products and services?

In 2001, in a Defense in Depth SANS whitepaper, Todd McGuiness said, “No single security measure can adequately protect a network; there are simply too many methods available to an attacker for this to work.”

This is still true and demonstrates the need to have multiple security solutions for proper protection of different attack vectors.

The problem with this approach is that companies ended up with several technologies from different vendors, all of which work in silos. Although it might seem that these protections are aligned with the security strategy of the company, it generates a very complex environment. It’s very difficult to operate and monitor when lacking collaboration and automation between the different controls.

SIEM and similar products arrived to try to solve the problem of centralized visibility, but in most cases, added a new operative burden because they needed a lot of configurations and lacked automation and intelligence.

The solution to this is a unified platform, where users can add different capabilities, controls and even services, according to their specific needs, making it easy to implement, operate and monitor in a consolidated and collaborative way and in a way that leverages intelligence and automation.

My prediction is that organizations will start to change from a best-of-breed approach to a platform approach, where the selection factors will be more focused on the consolidation, collaboration, and automation aspects of security controls, rather than the specific characteristics of each of the individual controls.

From a B2B consumer perspective, what are the potential benefits of platformization (ex. Easier integration, access to a wider range of services…)?

For consumers, the main benefits of a cyber security platform will be a higher security posture and reduced TCO for cyber security. By reducing complexity and adding automation and collaboration, organizations will increase their abilities to prevent, detect, contain, and respond to cyber security incidents.

The platform also gives flexibility by allowing admins to easily add new security protections that are automatically integrated in the environment.

Are there any potential drawbacks for B2B consumers when companies move towards platform models?

I have heard concerns from some CISOs about putting all or most of their trust in a single security vendor. They have in-mind the recent critical vulnerabilities that affected some of the important players in the industry.

This is why platforms should also be capable of integration through open APIs, permitting organizations to be flexible in their journey to consolidation.

How might platformization change the way that B2B consumers interact with tech companies and their products (ex. Self-service options, subscription models)? What will the impact be like?

Organizations are also looking for new consumption models that are simple and predictable and that will deliver cost-savings. They are looking to be able to pay for what they use and for flexibility if they need to include or change products/services according to specific needs.

What are some of main features of a cyber security platform?

Some of the main features are consolidation, being able to integrate security monitoring and management into a single central solution; automation based on APIs, playbooks and scripts according to best practices; threat prevention, being able to identify and block or automatically contain attacks before they pose a significant risk for an organization…

A key component of consolidation is the use of AI and machine learning, which can process the data, identify the threats and generate the appropriate responses.

In terms of collaboration, the platform should facilitate collaboration between different elements; for example sharing threat intelligence or triggering automatic responses in the different regions of the platform.

In looking at platformization from a cyber security perspective, how can Check Point’s Infinity Platform benefit B2B consumers through platformization principles (ex. Easier integration with existing tools, all tools under one umbrella…etc)?

The Check Point Infinity platform is a comprehensive, consolidated, and collaborative cyber security platform that provides enterprise-grade security across several vectors as data centers, networks, clouds, branch offices, and remote users with unified management.

It is AI-powered, offering a 99.8% catch rate for zero day attacks. It offers consolidated security operations; this means lowering the TCO and increasing security operational efficiency. It offers collaborative security that automatically responds to threats using AI-powered engines, real-time threat intelligence, anomaly detection, automated response and orchestration, and API-based third-party integration. Further, it permits organizations to scale cyber security according to their needs anywhere across hybrid networks, workforces, and clouds.

Consolidation will also improve the security posture through a consistent policy that’s aligned with zero trust principles. Finally, there is also a flexible and predictable ELA model that can simplify the procurement process.

How does the Check Point Infinity Platform integrate with existing security tools and platforms that CISOs might already be using?

Check Point offers a variety of APIs that make it easy to integrate in any orchestration and automation ecosystem. There are also several native integrations with different security products. For example, the XDR/XPR component can integrate with different products, such as firewalls or endpoint solutions from other vendors.

To what extent can CISOs customize and configure the Check Point Infinity Platform to meet their organization’s specific security posture and compliance requirements?

Given the modular plug and play model, CISOs can define what products and services make sense for their specific requirements. If these requirements change over time, then different products can easily be included. The ELA consumption model gives even more flexibility to CISOs, as they can add or remove products and services as needed.

How can platformization (whether through Infinity or other platforms) help businesses achieve long-term goals? Does it provide a competitive advantage in terms of agility, innovation and cost-efficiency?

A proper cyber security platform will improve the security posture of the business, increasing the ability to prevent, detect, contain and respond to cyber security incidents in an effective manner. This means lower TCO with increased protection. It will also allow businesses to quickly adapt to new needs, giving them agility to develop and release new products and services.

Is there anything else that you would like to share with Check Point’s thought leadership audience?

Collaboration between security products and proper intelligence sharing and analysis are fundamental in responding to cyber threats. We’ve seen several security integration projects through platforms, such as SIEMs or SOARs, fail because of the added complexity of generating and configuring the different use cases.

A security platform should solve this complexity problem. It is also important to note that a security platform does not mean buying all products from a single vendor. If it is not solving the consolidation, collaboration problem, it will generate the same siloed effect as previously described.

#ai#AI-powered#America#Analysis#API#APIs#approach#architecture#automation#B2B#Business#business model#change#Check Point#Check Point Infinity Platform#Check Point Software#CISOs#Cloud Security#cloud-delivered#clouds#Collaboration#collaborative#Companies#complexity#compliance#comprehensive#consolidated#consolidation#consumers#cyber

0 notes

Text

Moving from Mimicry to Meaningful Learning

Ever been in a classroom that feels more like a sleep-inducing seminar? I can see you raising your hand. You know the scene: students zoning out, fidgeting like they’re auditioning for a tap dance, begging for bathroom breaks like they’re fleeing a sinking ship. As both a former student and now a teacher, I’ve danced this engagement tango more times than I care to count.

But here’s the kicker…

View On WordPress

0 notes

Text

Timeline of The End (from 9/8/2023)

We were already in a bad place by Summer of 2020. Pandemic and COVID stuff; political divisions; daily stresses of simply being humans with 2 small kids and another on the way…

I was depleted and finding no validation or understanding from Evan. I was seriously considering divorce, and then my hands went numb and I was totally handicapped when Rosie was born, and I was terrified.

I was depressed, isolated, and helpless, and I was NOT pleasant. I became extremely critical of Evan, and angry. He grew frustrated with my moods and resentful of me for being critical AND for being depressed. Every depressed thought I shared was not only invalidated, but served him as evidence of how horrible I was.

Looking back on it now, I see how much I hurt him and damaged our relationship. I was oppositional and unaware of how determined I was to be miserable. I was the epitome of a one-woman pity party — and it made sense that he didn’t want to come. Still, I wanted something from him, but neither of us knew what that was.

It was Love and Care. I see how he did try to give me love and care in the ways he knows, and I see how I refused to accept any of it. I had my reasons, at the time; it was reactionary, it was superficial, it was the wrong way/time, etc. But he did try, and I wouldn’t trust his efforts to be honest. I didn’t trust him.

Maybe I never trusted him. Not the way a spouse should trust their partner if they truly want a healthy, loving marriage. Perhaps I self-sabotaged. Perhaps he wasn’t equipped, and demonstrated a constant resistance to accepting that possibility.

0 notes

Last Seen Blogs

peterb-rundekunst

RundeKunst

faith-unadulterated-blog

Faith Unadulterated

simspopfinds

Sims Pop Culture Finds

sage1x1s-blog

BLACK MAGIC ☾☼

mccormicx-archived

which may eternal lie.