#Fed Interest Rate Hike Mean

Link

Even in July-2022, FED may increase interest rate by 50 bps or 75 bps and recession either in 2022 or 2023 is inevitable in 2022 or 2023.

To control high inflation in USA, FED is increasing interest rates aggressively.

So companies who wants to expand their businesses by depending upon debt will try to control the spend and even cut down their existing businesses if it is not profitable.

So even unemployment rate will increase a bit.

In June-2022, FED increased interest rate by 75 bps and it is highest since 1994. FED is very aggressive to control inflation.

There is high possibility that recession will occur either in 2022 or 2023 in USA.

Recession means if there negative GDP growth for 2 quarters then we will be calling it as recession.

FED aggressive interest rates will lead to recession in USA.

However long term investors can invest in index stocks who can invest till end of 2024.

Bull market may be back either in second half of 2023 or first half of 2024 where FED will start to reduce interest rates.

Interest Rate hikes increase and Interest Rates decrease

and

Economic GDP growth and Economic GDP shrinkage

are cycles that will be repeated.

0 notes

Note

Why do you think tumblr will die in only a few years?

Answer with jargon: a strong correlation between recent economic shifts and chaotic choices by major tech companies is most easily explained if the 'traditional' social media platforms of 2005-2020 are mostly a zero-interest rate phenomenon.

Longer answer, with less jargon: Even though Musk's takeover is making all the headlines recently, the last year has in fact seen major shakeups at many social media platforms, so Twitter is actually part of a trend. Almost inevitably, these are cases of social media companies trying to find a way to squeeze more money out of their userbase (Reddit), cut costs dramatically (Twitter), or both. This marks a sudden departure from a much more relaxed attitude towards revenue in the Pictures Of Cats industry, where the focus was historically more on expanding the userbase to a global scale and then counting on world domination to sort of <????> and then the company would become profitable eventually.

We joke, correctly, that Tumblr has never been profitable. But the entire structure of ad-supported content curation between human users is deeply suspect as a business model; IIRC Twitter was never profitable either, and Facebook has been juicing its numbers in very shenanigany ways. Discord was actually making money on net last I checked, at least a bit, so they're not all completely in the hole. But even if you take the accounting figures at face value, none of these companies has anything like the amount of money that their cultural prominence would suggest. Instead, they're heavily fueled by investment dollars, money given by super-rich people and institutions in the expectation that fueling the growth of the company now will pay off with interest later.

So what changed?

I'm not an expert here, but I'll do my best to muddle through. The American Federal Reserve has one mandate that dominates all others (sometimes called the 'dual mandate'), and one primary tool that it uses to enforce that mandate. The goal is to maintain low (but nonzero) rates of inflation and unemployment, which in their models are deeply interlinked phenomena. The tool is 'rate hikes', or more specifically, tweaking the mandatory rate of interest that banks charge one another when making loans.

As a particular consequence of this, hiking the rate also means that bonds start paying out much better. When the rate hike goes through, that affects people who let the government borrow their personal cash- that is, people who buy bonds- as well as institutions like banks that lend to one another. A rate hike means that you, personally, can make a little extra money by letting the government borrow it for a while. The federal government of the US is a rock-solid low-risk choice for this kind of moneymaking scheme, so the federal interest rate sort of defines the 'number to beat'; to attract investors, a company has to give those investors money at a better percentage than whatever the feds are offering. Particularly since a company is a lot more likely to go out of business than the state!

To wrap this back around to the Pictures Of Cats industry: the higher the rate hike, the better your company needs to be doing (or the less risky it needs to be as an option) to attract big investment dollars. Very high rates make it very hard to convince people to invest in business activity rather than the government itself, and very low rates put moonshots and big dreams on the table, investment-wise, in a way that wouldn't otherwise be possible. Social media companies were one of these big dreams.

In the great financial crisis of 2008, the Fed took the dramatic step of reducing their rate to zero, trying to juice the economy back to life. And ever since then, they've kept it there. This has produced an unprecedented amount of funding for very crazy stuff; it's part of what has allowed so many weird new tech companies (Uber, streaming services, etc.) to get so much money, so quickly, and use that to grow to massive size without a clear model of how they're ever going to make money. This state of affairs kept going for quite a while, with no clear stopping point; that zero-interest environment has been one of the shadowy forces in the background that shaped fundamental contours and limits in how our Very Online World has grown and developed. Until COVID.

Or rather, the bounce back from COVID: we suddenly saw a massive spike in inflation and an incredibly strong labor market, as employees quit in record numbers, negotiated higher salaries, and found better work, and at the same time supply chain issues and other economy stuff caused prices to climb dramatically. Recall the Fed's 'dual mandate', to control the employment rate and inflation. This was, basically, kicking them right in the jooblies. They responded in kind, finally finally raising their rates for the first time in 15 years. For some of the people reading this, it'll be the first significant shift in their entire adult lives.

The goal, as I understand it, is to fight inflation by reducing the amount of outside investment into private companies, forcing them to hire fewer people and pay smaller salaries, ultimately drawing money out of the working economy and driving prices back down by lowering demand for everything. You get paid less, so you eat out less, and buy at cheaper restaurants when you do, so restaurants have to compete harder by lowering their prices; seems pretty dodgy to me as a theory, but it's the theory. And the first part will almost certainly work- companies are going to see less investment.

For social media companies that are still paying most of their salaries with investor dollars instead of revenues, this is especially catastrophic. Without outside investment, they're just a massive pile of expenses waiting to happen, huge yearly costs in developer salaries and server fees. This is why, all of a sudden, every social media company is suddenly making bonkers decisions. They're noticing that nobody wants to give them any more money! So they're trying to figure out how to live a lot more cheaply, to actually somehow for reals turn their giant userbases in to some kind of actual revenue stream, or both.

Tumblr is kind of the ur-example of this kind of thing, supporting a very large userbase with no coherent plan whatsoever to start paying its staff with our dollars instead of investors' dollars. When interest rates were low and Scrooge McDuck had nowhere else to hide his pile of gold coins, a crazy kid with a dream was the best alternative available to him. But now, unless something changes, he's going to notice he can just buy bonds instead, and that crazy kid can go take a hike.

That's why I think Tumblr is living on borrowed time, though I don't know how much. Like all cartoons, the economy doesn't really fall off a cliff until somebody looks down and notices they've been standing on thin air this whole time. But they always fall eventually; that's the gag.

#I am not an economics#so if somebody wants to grade my accuracy here#that would be welcome#this is the situation as I understand it but my models are hazy

2K notes

·

View notes

Text

Oh while I'm on U.S. economics, I have another thing that bugs the hell out of me: the hiking of mortgage interest rates.

For those who don't know, mortgage interest rates dropped low during the pandemic. Which is not all sunshine since it resulted in many bidding wars and a ton of way-over-asking offers in competitive areas, but it put home-ownership way more within reach for a lot of people.

Then the fed started to pee their pants over inflation, and hiked their rates up, prompting mortgage companies to follow.

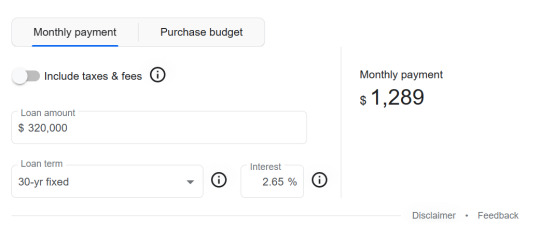

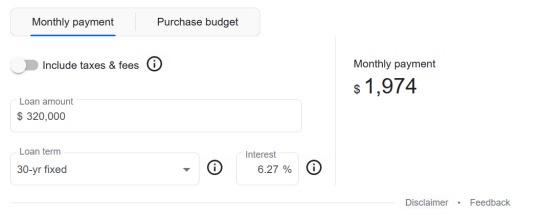

Here's a chart of mortgage interest rates over the last 4 years

It hit a trough at 2.65% on average in early January 2021, and then you see it hiked itself way back up, now chilling at 6.27%

For context on how different these are: let's use an example of a $400,000 home - someone pays 20% down ($80,000) in cash, and finances the remaining 80% ($320,000).

Monthly payments at 2.65%:

This results in paying back, in total, $464,040. You'll notice that's well over the initial $320,000, and that's because of the interest paid over those 30 years.

Now, monthly payments at 6.27%:

This results in paying back, in total, $710,640. That's more than twice the initial loan of $320,000.

And, of course, it means the same exact property which could be paid for with a monthly budget of ~$1,300 in early 2021 now requires a monthly budget of ~$2,000 in 2023.

Also, those pandemic lows were an anomaly... Historically, mortgage interest rates were on average HIGHER than 6.27% - but also, historically, wages were much better relative to the prices of homes and people could afford the high interest rates (with the exception of the people who got screwed over in the 2008 housing market meltdown... There's a really good Cold Fusion video on that.)

And because these low interest rates were an anomaly, they may never come back...

So with mortgage interest rates going up, home-buying becomes harder. When home-buying becomes harder, rents increase (because renters have no alternative).

So who DOESN'T get affected?

ENTITIES THAT CAN PAY IN ALL CASH.

They need no mortgage. They pay the sticker price on-spot with no interest applying to them. And I say ENTITIES because, sure, some people can buy their home in all-cash. But a huge number of the entities that can buy in all cash are BIG investment companies--the Blackrocks and the Mega-landlords who scoop up properties to sit on, rent out, and turn for a profit later like it's a piece of stock, and not a habitable property...

Anyway I don't have a conclusion for this. Fix wages, or bring interest rates back down, or kill Blackrock. Preferably all 3.

#Federal Reserve shivering quaking 'but if poor people have disposable income then companies will have no CHOICE but to price-gouge and#turn record profits and fuel inflation... theres no helping it... we have to make#everything harder for poor people...'#gonna start a bingo card if this breaches containment and sparks an argument on libertarian tumblr

279 notes

·

View notes

Text

Rent control works

This Saturday (May 20), I’ll be at the GAITHERSBURG Book Festival with my novel Red Team Blues; then on May 22, I’m keynoting Public Knowledge’s Emerging Tech conference in DC.

On May 23, I’ll be in TORONTO for a book launch that’s part of WEPFest, a benefit for the West End Phoenix, onstage with Dave Bidini (The Rheostatics), Ron Diebert (Citizen Lab) and the whistleblower Dr Nancy Olivieri.

David Roth memorably described the job of neoliberal economists as finding “new ways to say ‘actually, your boss is right.’” Not just your boss: for decades, economists have formed a bulwark against seemingly obvious responses to the most painful parts of our daily lives, from wages to education to health to shelter:

https://popula.com/2023/04/30/yakkin-about-chatgpt-with-david-roth/

How can we solve the student debt crisis? Well, we could cancel student debt and regulate the price of education, either directly or through free state college.

How can we solve America’s heath-debt crisis? We could cancel health debt and create Medicare For All.

How can we solve America’s homelessness crisis? We could build houses and let homeless people live in them.

How can we solve America’s wage-stagnation crisis? We could raise the minimum wage and/or create a federal jobs guarantee.

How can we solve America’s workplace abuse crisis? We could allow workers to unionize.

How can we solve America’s price-gouging greedflation crisis? With price controls and/or windfall taxes.

How can we solve America’s inequality crisis? We could tax billionaires.

How can we solve America’s monopoly crisis? We could break up monopolies.

How can we solve America’s traffic crisis? We could build public transit.

How can we solve America’s carbon crisis? We can regulate carbon emissions.

These answers make sense to everyone except neoliberal economists and people in their thrall. Rather than doing the thing we want, neoliberal economists insist we must unleash “markets” to solve the problems, by “creating incentives.” That may sound like a recipe for a small state, but in practice, “creating incentives” often involves building huge bureaucracies to “keep the incentives aligned” (that is, to prevent private firms from ripping off public agencies).

This is how we get “solutions” that fail catastrophically, like:

Public Service Loan Forgiveness instead of debt cancellation and free college:

https://studentloansherpa.com/likely-ineligible/

The gig economy instead of unions and minimum wages:

https://www.newswise.com/articles/research-reveals-majority-of-gig-economy-workers-are-earning-below-minimum-wage

Interest rate hikes instead of price caps and windfall taxes:

https://www.npr.org/2023/05/03/1173371788/the-fed-raises-interest-rates-again-in-what-could-be-its-final-attack-on-inflati

Tax breaks for billionaire philanthropists instead of taxing billionaires:

https://memex.craphound.com/2018/11/10/winners-take-all-modern-philanthropy-means-that-giving-some-away-is-more-important-than-how-you-got-it/

Subsidizing Uber instead of building mass transit:

https://prospect.org/infrastructure/cities-turn-uber-instead-buses-trains/

Fraud-riddled carbon trading instead of emissions limits:

https://pluralistic.net/2022/05/27/voluntary-carbon-market/#trust-me

As infuriating as all of this “actually, your boss is right” nonsense is, the most immediate and continuously frustrating aspect of it is the housing crisis, which has engulfed cities all over the world, to the detriment of nearly everyone.

America led the way on screwing up housing. There were two major New Deal/post-war policies that created broad (but imperfect and racially biased) prosperity in America: housing subsidies and labor unions. Of the two, labor unions were the most broadly inclusive, most available across racial and gender lines, and most engaged with civil rights struggles and other progressive causes.

So America declared war on labor unions and told working people that their only path to intergenerational wealth was to buy a home, wait for it to “appreciate,” and sell it on for a profit. This is a disaster. Without unions to provide countervailing force, every part of American life has worsened, with stagnating wages lagging behind skyrocketing expenses for education, health, retirement, and long-term care. For nearly every homeowner, this means that their “most valuable asset” — the roof over their head — must be liquidated to cover debts. Meanwhile, their kids, burdened with six-figure student debt — will have little or nothing left from the sale of the family home with which to cover a downpayment in a hyperinflated market:

https://gen.medium.com/the-rents-too-damned-high-520f958d5ec5

Meanwhile, rent inflation is screaming ahead of other forms of inflation, burdening working people beyond any ability to pay. Giant Wall Street firms have bought up huge swathes of the country’s housing stock, transforming it into overpriced, undermaintained slums that you can be evicted from at the drop of a hat:

https://pluralistic.net/2022/02/08/wall-street-landlords/#the-new-slumlords

Transforming housing from a human right to an “asset” was always going to end in a failure to build new housing stock and regulate the rental market. It’s reaching a breaking point. “Superstar cities” like New York and San Francisco have long been priced out of the reach of working people, but now they’re becoming unattainable for double-income, childless, college-educated adults in their prime working years:

https://www.nytimes.com/interactive/2023/05/15/upshot/migrations-college-super-cities.html

A city that you can’t live in is a failure. A system that can’t provide decent housing is a failure. The “your boss is right, actually” crowd won: we don’t build public housing, we don’t regulate rents, and it suuuuuuuuuuuuuuucks.

Maybe we could try doing things instead of “aligning incentives?”

Like, how about rent control.

God, you can already hear them squealing! “Price controls artificially distort well-functioning markets, resulting in a mismatch between supply and demand and the creation of the dreaded deadweight loss triangle!”

Rent control “causes widespread shortages, leaving would-be renters high and dry while screwing landlords (the road to hell, so says the orthodox economist, is paved with good intentions).”

That’s been the received wisdom for decades, fed to us by Chicago School economists who are so besotted with their own mathematical models that any mismatch between the models’ predictions and the real world is chalked up to errors in the real world, not the models. It’s pure economism: “If economists wished to study the horse, they wouldn’t go and look at horses. They’d sit in their studies and say to themselves, ‘What would I do if I were a horse?’”

https://pluralistic.net/2022/10/27/economism/#what-would-i-do-if-i-were-a-horse

But, as Mark Paul writes for The American Prospect, rent control works:

https://prospect.org/infrastructure/housing/2023-05-16-economists-hate-rent-control/

Rent control doesn’t constrain housing supply:

https://dornsife.usc.edu/pere/rent-matters

At least some of the time, rent control expands housing supply:

https://onlinelibrary.wiley.com/doi/full/10.1111/j.1467-9906.2007.00334.x

The real risk of rent control is landlords exploiting badly written laws to kick out tenants and convert their units to condos — that’s not a problem with rent control, it’s a problem with eviction law:

https://web.stanford.edu/~diamondr/DMQ.pdf

Meanwhile, removing rent control doesn’t trigger the predicted increases in housing supply:

https://www.sciencedirect.com/science/article/pii/S0094119006000635

Rent control might create winners (tenants) and losers (landlords), but it certainly doesn’t make everyone worse off — as the neoliberal doctrine insists it must. Instead, tenants who benefit from rent control have extra money in their pockets to spend on groceries, debt service, vacations, and child-care.

Those happier, more prosperous people, in turn, increase the value of their landlords’ properties, by creating happy, prosperous neighborhoods. Rent control means that when people in a neighborhood increase its value, their landlords can’t kick them out and rent to richer people, capturing all the value the old tenants created.

What is life like under rent control? It’s great. You and your family get to stay put until you’re ready to move on, as do your neighbors. Your kids don’t have to change schools and find new friends. Old people aren’t torn away from communities who care for them:

https://ideas.repec.org/a/uwp/landec/v58y1982i1p109-117.html

In Massachusetts, tenants with rent control pay half the rent that their non-rent-controlled neighbors pay:

https://economics.mit.edu/sites/default/files/publications/housing%20market%202014.pdf

Rent control doesn’t just make tenants better off, it makes society better off. Rather than money flowing from a neighborhood to landlords, rent control allows the people in a community to invest it there: opening and patronizing businesses.

Anything that can’t go on forever will eventually stop. As the housing crisis worsens, states are finally bringing back rent control. New York has strengthened rent control for the first time in 40 years:

https://www.nytimes.com/2019/06/12/nyregion/rent-regulation-laws-new-york.html

California has a new statewide rent control law:

https://www.nytimes.com/2019/09/11/business/economy/california-rent-control.html

They’re battling against anti-rent-control state laws pushed by ALEC, the right-wing architects of model legislation banning action on climate change, broadband access, and abortion:

https://www.nmhc.org/research-insight/analysis-and-guidance/rent-control-laws-by-state/

But rent control has broad, democratic support. Strong majorities of likely voters support rent control:

https://www.bostonglobe.com/2023/03/07/metro/new-statewide-poll-shows-strong-support-rent-control/

And there’s a kind of rent control that has near unanimous support: the 30-year fixed mortgage. For the 67% of Americans who live in owner-occupied homes, the existence of the federally-backed (and thus federally subsidized) fixed mortgage means that your monthly shelter costs are fixed for life. What’s more, these costs go down the longer you pay them, as mortgage borrowers refinance when interest rates dip.

We have a two-tier system: if you own a home, then the longer you stay put, the cheaper your “rent” gets. If you rent a home, the longer you stay put, the more expensive your home gets over time.

America needs a shit-ton more housing — regular housing for working people. Mr Market doesn’t want to build it, no matter how many “incentives” we dangle. Maybe it’s time we just did stuff instead of building elaborate Rube Goldberg machines in the hopes of luring the market’s animal sentiments into doing it for us.

Catch me on tour with Red Team Blues in Toronto, DC, Gaithersburg, Oxford, Hay, Manchester, Nottingham, London, and Berlin!

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/05/16/mortgages-are-rent-control/#housing-is-a-human-right-not-an-asset

[Image ID: A beautifully laid dining room table in a luxury flat. Outside of the windows looms a rotting shanty town with storm-clouds overhead.]

Image:

ozz13x (modified)

https://commons.wikimedia.org/wiki/File:Shanty_Town_Hong_Kong_China_March_2013.jpg

Matt Brown (modified)

https://commons.wikimedia.org/wiki/File:Dining_room_in_Centre_Point_penthouse.jpg

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/deed.en

#pluralistic#urbanism#weaponized shelter#housing#the rent's too damned high#rent control#economism#neoliberalism#monetarism#mr market#landlord brain#speculation

118 notes

·

View notes

Text

Biden offers assurances after major US banks collapse | Business and Economy News | Al Jazeera

What can even be said at this point?

Both the second and third largest bank failures in the history of the United States occurred over the weekend.

This really shouldn't be surprising. Thanks largely to the sanctions regimes placed on Russia and China over the last year have caused stubbornly high inflation across the West.

The US banker-run Fed has responded to the inflation with ever increasing interest rates, raising borrowing costs for Banks that have, once again, been mainly focused on short-term profit seeking over stable investments.

Unlike the banking regulations put into effect after the Great Depression, Dodd-Frank, enacted shortly after 2008 bank failures, was purposely over-complicated, full of loopholes, and only partially enacted and enforced.

It should come as no surprise then that banks like SVB and Signature Bank held an inordinate amount of risky investments that lost value since the Feds interest rate hikes, and because of obvious loopholes in the Law, these banks didn't have to report the degradation in value of these investments until they went to sell them, when suddenly their customers realized just how much money their bank had lost, leading to a traditional bank-run.

And of course, the Biden Administration runs to the rescue, securing depositors of ALL amounts at these banks, once again making it crystal clear to the rich that there will be no consequences to any of their actions EVER.

The point is, the Capitalist Class at the helm can't even make decisions based on their own long-term stability, let alone for the economic stability of the people.

From idiotic sanctions, pointless wars, endless aid to Ukraine, bailouts of rich depositors, endless increases in the Defense Budget, these people can't even defend their own interests because they're so hyperfocused on short-term political and economic gain.

I mean do people even realize this inflation is basically the result of just two things, sanctions and endless war spending???

#bank failures#socialist news#socialist politics#socialism#communism#marxism leninism#socialist#communist#marxism#marxist leninist#progressive politics#politics

29 notes

·

View notes

Note

What happened with this bank crash? Everyone says something different, could you make sense of it all?

The Silicon Valley Bank Crash was a result of primarily three things - low interest rates and a flush of deposits, a subsequent hike due to the expansionary monetary policy and high inflation, and poor risk decisions on the part of the bank. The 2018-2019 Dodd-Frank rollback did not contribute given the size of the bank run in relation to the fractional reserve; anyone that tells you that is either a salesman, an ideologue, or both (Elizabeth Warren is as terrible in interpreting financial policy as she is on the post-Soviet collapse history of Eastern Europe).

A decade of low-interest has made borrowing very easy for start-ups, and the pandemic brought SVB flush with new investments and startup cash. SVB grew extraordinarily rapidly, which would be some cause for alarm that no one seemed to take seriously. SVB took the cash and primarily invested it in Treasury bonds, which are safe, low yield investments that are wise to invest in when the interest rate is low. As inflation spiraled due to the expansionary monetary policy of the pandemic, the Fed raised interest rates to help cool it off, which meant that the bonds that SVB bought lost value. No one wants to buy a bond with a low interest rate when higher bonds exist, so usually that means that if you want to liquidate the bonds, you sell them at a loss. Now, this wasn't a problem on its own, but the higher interest rates made borrowing tougher and so companies tried to withdraw funds to cover payroll and other expenditures, which meant SVB had to sell assets. This panicked depositers since a lot of their accounts were uninsured/underinsured, triggering a bank run.

A lot of blame for this has to fall on SVB management. Investing so much into Treasury bonds during the pandemic is anything a halfway decent economic forecaster or risk management analyst would say was a bad idea. Everyone knew interest rate hikes were coming, the fact that no one said that was a bad idea is baffling.

Thanks for the question, Anon.

SomethingLikeALawyer, Hand of the King

16 notes

·

View notes

Photo

David Horsey

* * * * *

What Robert Hockett writes here comes pretty close to a consensus view among constitutional scholars I've read on the subject. An important read.

"The deadline for a debt ceiling hike is only weeks away, with Treasury Secretary Janet Yellen saying the U.S. could run out of money to pay its debts by June 1. Some Republicans, whether serious or bluffing, seem ready to go to the brink of default — if not actually default on the U.S. national debt. Debate has intensified over whether President Biden might sidestep the debt ceiling so the nation can keep paying what it owes. There are powerful legal reasons and arguments for him to do so.

These include the 14th Amendment, which prohibits questioning what we already owe, and the so-called later-in-time rule of statutory construction, which basically means that Congress’s most recent budget legislation trumps any earlier legislated ceiling.

Given the stakes, it’s important to explore the likely consequences if Mr. Biden ignores the debt ceiling — how doing so would affect our economy and the markets, our retirement savings and even our constitutional system. There is encouraging news for the president and those who follow our first Treasury secretary, Alexander Hamilton, in believing we must pay our legally incurred debts. We are far better off doing so, even if it means short-term chaos should Mr. Biden allow the June 1 deadline to come and go.

First, consider the consequences if the United States stopped paying its debts and defaulted on June 1. This would undo what Hamilton and his successors sought to ensure: a national credit rating beyond cavil or reproach. We would see a great tottering — if not worse — of U.S. banking, U.S. financial markets and the world’s capital markets. For one thing, U.S. Treasury securities, valued at over $24 trillion (by far, the largest asset market in the world), are the primary safe asset held in banking, pension fund, mutual fund and other business portfolios. Our present regional bank crisis involving Silicon Valley Bank and others is occurring in response to a relatively slight, temporary drop in the value of low-yield Treasuries largely because of the Fed’s interest rate hikes. An outright default would leave us nostalgic for the comparable placidity of this troubled moment.We would also probably see a rapid plunge in the value of the dollar worldwide as a global reserve asset.

Our currency’s value in relation to others’ is rooted primarily in global demand for dollar-denominated financial assets, since we have relinquished our primacy as a goods exporter to China. Since Treasury securities are by far the most voluminous asset, their slide would be the dollar’s slide. This would quickly render imports, on which we continue to rely, far more expensive. Inflation could look more like that of Argentina or Russia 20 years ago than that of the present or even the 1970s.This is to say nothing of our subsequent incapacity to maintain our military bases and other assets abroad and to pay thousands of U.S. military personnel. Only China would be a world-bestriding global superpower, abetting the moves it is already making with Russia, Brazil and other nations to displace the dollar as what Valéry Giscard d’Estaing once called the United States’ global “exorbitant privilege.”

Finally, even the serious prospect of U.S. default would quickly raise debt-servicing costs, rendering our deficit larger than it currently is — a consequence dramatically at odds with Republicans’ professed concerns about tying the debt ceiling hike to massive budget cuts."

It almost makes you think that fiscal responsibility isn’t what House Speaker Kevin McCarthy’s caucus really wants.

[New York Times :: This Is What Would Happen if Biden Ignores the Debt Ceiling and Calls McCarthy’s Bluff]

8 notes

·

View notes

Text

Fauxflation

On the back of my previous posts on bonds and the housing bubble and/or crisis, I'd like to describe a form of inflation happening that isn't direct inflation.

I've talked before about loan caps, and how bank debt (not to be confused with the country debt of 30trillion+ which is how we determine how much money the fed injects into the economy.) Can be used to inflate the country's debt outside of the control of the government (and thus outside the federal reserve's control).

Banks use debt as assets, they trade them like they would money, because they expect the money to be paid back. However, they are also allowed to give out loans based on the debt they control, and thus expect to be paid back. (This is part of the problem with bonds in 2008).

Banks loans money to Steve, and based on how Steve pays that loan back, the bank is then allowed to loan money to Geoff. Sometimes at the expected interest they expect to make from Steve. And if Geoff is paying back the bank regularly, the bank is able to make another loan out to a third person: Jenny.

If you're tracking; that means the bank has given out three loans based on one pool of money. Effectively tripling that original pool, until those loans are paid back. Which would both cause inflation while the loans are in circulation, and deflation should they be paid back, or even forgiven.

This should be controlled by the digital debt ceiling that the fed allows banks to loan against. *Should* being the operative word.

That's only part of the fauxflation equation.

The next part is companies, who have taken these loans, and are selling goods to end users. They borrow against interest rates and if the interest rates are high, that also compounds inflation. (More money is expected to pay back that initial loan. Thus creating an drain on the revenue of those companies.)

How do those companies make money? They charge the end user more and more. As much money as they are willing to pay. Companies have said as much: "They are willing to charge as much as the customers can afford".

The U.S. subsidizes certain products in order to keep prices down, and to account for increased demand. So that parents can feed their children. It's funny that even those products are starting to see insane price hikes. From $1.50 for a quart of milk to nearly $5 over the course of the past few years.

That's with the subsidies that they get to sell those products.

Simultaneously, corporate profits are at a record high.

Now, I'm going to take this time to explain why record profits might not *actually* be profit. Please bear with me it's stupid. I know.

Many loans have increased, or lowered fees after a certain time period of one-time payments. If companies have taken a loan out like you would on a credit card: "0% APR for 12 months, and then 30% annual after that". That means their payment of their loan is included on their revenue sheet

Some loans, like a car or house loan have a maximum interest based on the term of the loan. And your credit score is based on paying that interest back on time, not early, not late. If you have a six year loan, it's in your best interest to pay it back in six years. So that you have good credit for a better loan after that.

Any Earlier and the banks know that you won't be making them enough money to bother.

But if the company is making record profits, it might behoove them to include that in their future projections. If that APR kicks in at a higher % like on your credit card, then they have to hang onto that profit, possibly invest it (to try to keep up with the APR) because they know they'll be paying back that interest at a later date, since they won't be paying the whole thing off this year.

Basically: what happens if you only make minimum payments on your credit card?

With wage hikes, and with high interest, and with both of those causing fauxflation: you can see where the problem point in this chain is:

Whatever money is owed back to the banks

Now, why do the banks include things like APR increases in some products and not others? They believe it's an effective stick to the loan's carrot. They believe that you'll be encouraged to pay it back at that point, and they have calculations to prove it. (Remember what I said about banks creating higher loans to pay off lower loans because of housing inflation? That circle-k?)

They have a decade of data saying that their loans all got paid off.

So when it comes time that the economy can't handle their projections, because they ommitted the data where things like this happened last time. (Too long ago, who cares)

It's easy to say "we couldn't have accounted for this".

And it's plausible because who accounts for data that long ago?

6 notes

·

View notes

Photo

#Accelerationism The current international environment in the countries of foreign reserves diversification of security needs, as well as Europe in the tightening of the demand for U.S. debt slowdown, the exchange rate pressure to the U.S. bond market transmission may become an important market risk within this year to early next year, which also means that the possibility of U.S. bond yields rise overshoot is high. And from recent years, the stability of the U.S. bond and U.S. dollar liquidity market will also stage to become an important concern for the Fed's monetary policy, becoming an important trigger for slowing down interest rate hikes or tapering, typically in September 2019, for example, the turmoil in the U.S. bond and repo markets accelerated the Fed's restart of QE.

9 notes

·

View notes

Text

Crypto Rally Causes $450M Short Trader Losses

The crypto market has been on an upward trend lately, with major cryptocurrencies experiencing significant gains. Unfortunately for traders who had bet against the market, this has resulted in some significant losses. In this article, we’ll take a closer look at what’s behind this crypto market rally, and what it means for traders and investors.

Short Traders Suffer Heavy Losses

According to data from CoinGlass, short traders (those who bet that the market will go down) suffered over $450 million in losses in the past 24 hours. The biggest losses were seen on the OKX exchange, where short traders lost over $241 million, and on Binance, where losses totaled $116 million. This is a clear indication of how much the crypto market has rallied, leaving short sellers in a difficult spot. Not only short traders, but long traders (those who bet that the market will go up) also suffered losses, with over $108 million in long positions being liquidated. The total value of liquidated positions in the past day has exceeded $727 million, a level not witnessed since the crypto market faced troubles on November 8th

Lower Inflation May be a Factor

So, what’s behind this crypto market rally? While a mix of factors may have contributed to the recent crypto rally, one possible explanation is the new data released by the U.S. Department of Labor indicating a cooldown in inflation. Specifically, the annual inflation rate fell to 6.5% in December, compared to 7.1% in November. The month-over-month inflation rate decreased by 0.1%, a contrast to the 0.1% rise seen the previous month. The core Consumer Price Index (CPI), which excludes volatile food and energy prices, dropped to 5.7% from 6% in November

Lower inflation is commonly perceived as a positive development for risky assets like crypto, as it puts pressure on the US Federal Reserve to decrease interest rate hikes. Over the past year, the Fed and other global central banks have been raising interest rates at a fast pace, creating a challenging environment for crypto and other risky assets. As we have seen the crypto market is highly correlated to the global economy and interest rate is one of the key factors that affect the crypto market. This could be one of the reasons why crypto market rallied when there was a sign of lower inflation rate.

Institutional Investors Entering the Market

Another factor worth noting is that there has been a steep rise in activity in the futures market for digital currencies. Crypto Quant’s Ki Young Jun noted that buyers entered the market early Saturday morning, purchasing around $4 billion worth of bitcoin futures. This suggests that institutional investors may be starting to see value in the crypto market and are positioning themselves for the long-term. As the crypto market is maturing and more institutional investors are entering the market, it is becoming more stable and predictable. This could be another reason behind the recent rally.

Risks to Keep in Mind

It’s important to remember that the crypto market is still in its early stages and can be subject to significant volatility. Additionally, the regulatory environment for crypto is still uncertain and could change at any time. Governments around the world are still figuring out how to regulate the crypto market, and this uncertainty can lead to volatility in the market. Investors should be aware of the risks and do their own research before investing in the crypto market.

Conclusion

The recent crypto market rally and the resulting liquidations of short traders is a reminder of the potential volatility and uncertainty in the crypto market. However, it also shows that the crypto market still has significant potential for growth, particularly as more institutional investors enter the market. As the crypto market is maturing and becoming more stable, the potential for growth is increasing. As always, investors should be aware of the risks and do their own research before investing in the crypto market. It’s also worth noting that, while the current crypto market rally is impressive, it’s not without precedent. In 2017, the crypto market experienced a similar rally, with Bitcoin reaching its all-time high of nearly $20,000.

However, it’s important to remember that the crypto market is still relatively new and is subject to significant volatility. While the current rally is a positive sign, it’s not a guarantee of future growth. Investors should approach the crypto market with caution and only invest what they can afford to lose.

In addition, as the crypto market continues to grow, it is important for investors to be aware of the different types of crypto assets available. Bitcoin, the world’s first and largest cryptocurrency, is not the only option. There are now thousands of different cryptocurrencies available, each with their own unique characteristics and potential for growth. Ethereum, for example, is a popular alternative to Bitcoin and is known for its smart contract capabilities.

It’s also worth noting that the crypto market is not just limited to digital currencies. There are now a growing number of crypto-related investments available, such as blockchain-based stocks and crypto-related ETFs. These alternative investments can provide investors with exposure to the crypto market without the volatility associated with digital currencies.

You Might Also Want to Read: Bitcoin Price Rally: What Can it Tell us About the Current Market?

2 notes

·

View notes

Text

As the November 2022 election draws near, a few issues have emerged as the ones most likely to drive voters to the polls. At the top of the list, surprising no one who has read the news in the last year, are inflation and abortion. But voters also have their eyes on many other issues, including education, health care, and climate change.

Recent analysis by experts in Brookings’ Economic Studies program has unpacked the economics of these issues, focusing on practical policy solutions rather than politics. Below, read short summaries of the latest research on these important topics and follow the links to learn more.

Jump to:

Inflation >>

Abortion >>

Climate >>

Health care >>

Education >>

Inflation

How does the government measure inflation?

Bottom line: To calculate the Consumer Price Index (CPI), the most widely cited measure of inflation, the Bureau of Labor Statistics looks at the national costs of 80,000 items in a fixed basket of goods and services, explain Nasiha Salwati and David Wessel. In a June blog, they detail the applications of the CPI, along with Core CPI, PCE, and other important inflation measures.

Learn more: Measuring the cost of housing, which accounts for about a third of the CPI basket of goods, is especially difficult. See this explainer from Sophia Campbell and Wessel for a closer look.

Inflation during the COVID era

Bottom line: A recent Brookings Papers on Economic Activity study found that the Federal Reserve may have to push unemployment much higher than it originally projected in order to return inflation to its 2% target.

Learn more: Listen to episode two of the Brookings Podcast on Economic Activity for an interview with Laurence Ball of Johns Hopkins University, one of the authors of the new study.

Key Takeaways from recent CPI reports

Bottom line: The last several months have seen one disappointing Consumer Price Index report after another, with hopes of seeing Federal Reserve interest rate hikes translating into slower inflation going unrealized. Brookings experts have convened on Twitter following each of the last four Bureau of Labor Statistics releases to break down the numbers.

Learn more: Read four key takeaways on the September report.

How a new EU-US trade agreement could reduce inflation

Bottom line: A free trade agreement like the one pursued during the Obama administration would lower prices, write Sanjay Patnaik and James Kunhardt of the Center on Regulation and Markets, while at the same time mitigating a recession and strengthening democracy.

Learn more: In a recent report, Patnaik and Kunhardt detail the benefits of such a plan and outline a path forward.

What if the Fed’s battle on inflation triggers a recession?

Bottom line: As concerns about recession were rising in April 2022, the Hutchins Center on Fiscal and Monetary Policy and the Hamilton Project published a book focused on lessons from the COVID-19 pandemic and how to prepare for the next economic downturn. In May, Wendy Edelberg and Mitchell Barnes of the Hamilton Project published an inflation-related update to that work, highlighting early evidence that service prices had overtaken goods prices as a key inflationary pressure and that wages were failing to keep up.

Learn more: “Recession Remedies” looks at the various fiscal and monetary responses to the pandemic-induced recession and identifies which should be repeated to support workers and households in the next recession and which were pandemic-specific.

Rising costs with limited choices

Bottom line: Just as inflation was picking up speed this summer, the Supreme Court voted to overturn Roe v. Wade, meaning that parents choices on when to have a child will be limited in many states. New calculations by Isabel Sawhill and Morgan Welch found that due to higher inflation, a middle-income married family with two children will now spend $26,011 more than previously estimated to raise a child.

Learn more: In August, Sawhill, Welch, and Chris Miller explained the new calculation and highlighted reforms to help parents.

Back to top

Abortion

The economics of abortion

Bottom line: Prior to the overturning of Roe v. Wade, Caitlin Knowles Myers and Morgan Welch summarized an amicus brief to the Supreme Court of the United States on the economics of abortion restriction, which reviewed an extensive body of economic literature that shows how abortion access affects women’s education, earnings, careers, and the subsequent life outcomes for their children.

States that would limit choice don’t provide as much support for kids

Bottom line: Using national data on child well-being and state spending, Isabel Sawhill and Morgan Welch showed that states where abortion bans are likely or are already in effect tend to provide less funding for kids and have worse outcomes for children.

Learn more: “The states where children are more likely to be born into the worst circumstances, and are receiving the least support after birth, also tend to be the ones that are restricting a women’s right to choose,” write Sawhill and Welch.

Without Roe, women need more access to family planning services

Bottom line: Many of the states expected to restrict abortion access also have high unplanned pregnancy rates and low contraceptive use. Research summarized by Morgan Welch and Ember Smith shows that access to family planning, whether it be contraception or abortion, has positive effects on women’s long-term outcomes by allowing them to determine whether, when, and under what circumstances to start or grow their families.

Learn more: Welch and Smith highlight research on the impacts of abortion restrictions and policies that could help to mitigate them.

Back to top

Climate

Permitting reform could help enable the clean energy revolution

Bottom Line: The federal permitting process for energy projects is complex, cumbersome, and slow, as Rayan Sud and Sanjay Patnaik document in their recent report explaining the process. Biden’s ambitious clean energy goals, which would require significant clean energy infrastructure investments, have created a renewed sense of urgency to those efforts, write Sud and Patnaik.

Modeling can help policymakers prepare for a changing climate and a changing economy

Bottom Line: To manage the uncertainty and complexity of a changing climate and its impacts, economists and climate researchers rely on complex models and scenarios. Roshen Fernando, Weifeng Liu, and Warwick McKibbin explain the different types of scenarios and key takeaways from recent scenario exercises.

Learn More: “…to effectively use scenarios, policymakers need to understand how scenarios are developed and the strengths and weaknesses of the different modelling approaches,” they write in their latest report.

Jobs for a post-carbon economy

Bottom line: Workers who depend on fossil fuels for a living will have to transition to new livelihoods as the economy increasingly adopts green energy. “Just transition” programs have emerged as a useful way to help them accomplish that change, according to Michaël Aklin and Johannes Urpelainen.

Learn more: In a recent report, Aklin and Urpelainen make the case for national-level support of just transition programs, including the creation of a federal Just Transition Office to coordinate the effort.

The economic risks of climate change

Bottom line: Climate disasters cost the U.S. $95 billion in damages in 2020 alone, and as a result, Sanjay Patnaik explains that climate risk is becoming an increasingly important factor in political and economic decision making.

Back to top

Health care

Eliminating small premiums could increase insurance coverage

Bottom line: Research has shown that premiums of even a few dollars a month can markedly reduce health insurance coverage, likely because of the hassles involved in paying even a small premium. In a recent report, Matthew Fiedler estimates that increasing the premium tax credit to cover an enrollee’s full premium, in cases where the enrollee would otherwise owe a small residual premium, could have increased insurance coverage in the states that use the HealthCare.gov enrollment platform by 48,000 person-years in 2022.

Learn more: Fiedler breaks down the numbers and explains the proposal.

The FDA could do more to promote pharmaceutical competition

Bottom line: A report published by the USC-Brookings Schaeffer Initiative for Health Policy argued that with only modest statutory changes, Congress could give Food and Drug Administration authorities that would help promote generic pharmaceutical drugs and price competition.

Learn more: These changes could have been enacted through the Prescription Drug User Fee Act reauthorization, according to the June report.

Five things to understand about pharmaceutical R&D and innovation

Bottom line: In a recent blog, Richard Frank and Kathleen Hannick reveal key facts on drug development, including using recent data to show that there is only a modest relationship between R&D spending and the supply of new drugs.

Learn more: In relation to pharmaceutical company spending on research and development, “modest changes in the size of payments to the pharmaceutical industry would likely have little impact on the future health of Americans,” write Frank and Hannick.

Biden’s plan for mental health builds on long-standing efforts

Bottom line: In his first State of the Union address, President Biden proposed changes to how America treats mental health. His proposal would establish mental health as a key component of the nation’s health care system, improving mental health treatment for the youth, advancing equity goals in mental health care, and more, explain Richard G. Frank, Vikki Wachino, and Karina Aguilar in this blog from April.

A “critical product list” for health care could help prevent public health crises

Bottom line: The baby formula shortage earlier this year showed that the supply chain’s effect on health is not limited to pandemic-level crises. Adding key products like baby formula and psychotropic medications to the FDA’s critical product list would boost supply chain resilience and help prevent future crises, according to analysis by Marta E. Wosińska and Richard G. Frank.

Learn more: Read the blog by Wosińska and Frank for more on how the critical product list could be amended.

Back to top

Education

How to help boys who have been left behind in education

Bottom line: Young women are more likely than their male counterparts to have a bachelor’s degree, are more likely to graduate high school on time, and perform substantially better on standardized reading tests than boys. Richard Reeves and Ember Smith explore the state level data in a recent blog.

Learn more: One of the solutions highlighted in Reeves’ new book, “Of Boys and Men,” is to give boys across the country the option to “red shirt,” or delay starting kindergarten by a year.

How the racial wealth gap affects college access

Bottom line: The formula that determines how much federal financial aid is offered to prospective college students does not account for primary residency home equity or retirement savings. That means those who hold those assets receive an implicit subsidy for college, write Phil Levine and Dubravka Ritter, and white families hold those assets at a higher rate than Black families. Among families whose children are likely to benefit from this provision (those with middle to high incomes, typical counted assets, and sufficient remaining financial need to qualify for grant-based aid), white students receive an implicit subsidy that is $2,200 per year, on average, more than for Black students.

Learn more: Read the blog for a breakdown of Levine and Ritter’s calculations and proposals to solve the problem. For more on improving college affordability, see Levine’s analysis which shows that doubling the Pell Grant is a more targeted approach than a proposed “Free College” program and would do more to close the college affordability gap.

Student loan debt forgiveness benefitted those who needed help, and those who didn’t

Bottom line: A White House fact sheet explained that student loan debt forgiveness aimed to target relief on low- and middle-income borrowers—particularly Black borrowers, borrowers who didn’t get a degree, and those who have defaulted on their student loans. However, by calculating the full cost of the relief based on average repayment rates for different groups, Adam Looney found that “the administration spent roughly the same amount per borrower on Pell Grant recipients as it did on other borrowers, even though Pell grant recipients are from much more disadvantaged backgrounds.”

Learn more: Looney also recently offered critiques of the Biden administration’s plan to restructure the Income-Driven Repayment program for student loan borrowers – read more here.

The cost of out-of-state college

Bottom line: The share of out-of-state students at public, state flagship universities has risen by an average of 55% since 2002, according to recent analysis by Aaron Klein. “By swapping in-state students for out-of-state students, writes Klein, “universities gain more revenue. The result is more debt for students, higher costs for parents, and no greater educational attainment for society.”

Learn more: Use the interactive map to explore changes in in-state/out-of-state enrollment in each state.

Back to top

3 notes

·

View notes

Video

youtube

Inflation, Europe's energy crisis, and the Fed with Richard Wolff | The Chris Hedges Report

Read the transcript of this interview: https://therealnews.com/richard-wolff...

The Federal Reserve has responded to runaway inflation by hiking up interest rates at the same time that Americans are drowning in historic levels of personal debt. With interest rates up, prices will only rise faster than wages, hitting the vast majority of people with stagnant or declining wages in real terms. The result is yet another upward transfer of wealth to the minority of capitalists responsible for the crisis in the first place. Economist Richard Wolff joins The Chris Hedges Report to discuss the origins of the inflation crisis, the Fed's response, and what this all means for working people.

2 notes

·

View notes

Text

I think the fed interest rate 75 point raise is good, right? Net good, I mean. It feels almost naive to talk about economics now but it usually goes interest rate hike -> tougher to get credit -> less spending -> reduced inflation at the cost of a recession because of tougher credit making it more likely for new companies to fold or sputter, but if so many of those “new companies” are just venture capital investors getting in money fights with each other, it’s not exactly the end of the world if we get less stupid startups. Am I reading the situation correctly?

3 notes

·

View notes

Text

Post: Powell announces new Fed approach to inflation that could keep rates lower for longerFed...

Powell announces new Fed approach to inflation that could keep rates lower for longerFed Chairman Jerome Powell announced a major policy shift Thursday to average inflation targeting.That means the central bank will be more inclined to allow inflation to run higher than the standard 2% target before hiking interest rates.In addition to the inflation change, the Fed shifted its approach to employment in a way that will focus on those at the lower end of the income spectrum. https://www.blaqsbi.com/2ryx

0 notes

Text

CENTRAL BANK CONUNDRUM.

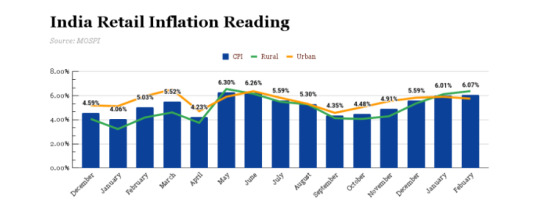

Whenever there is a hike in the interest rate, the economist is apprehensive about its impact on growth. The recent rate hike by RBI also poses the same apprehensions among the economists that these decisions could be growth restrictive as the economy has not revived completely.

If we look at the inflation rate, it was seeing a continuous surge from October, and the recent data of May shows that it has reached 8.6% highest since 1981. This exponential increase in the inflation rate is attributed to the rise in food inflation. Various economists suggest that the R.B.I rate hike will not be able to tame this inflation because of the international phenomenon. Instead, it will hurt the growth prospects.

If we look at the data more carefully, we will find that a fast-forwarded rate hike was unavoidable because of five primary reasons- (Joshi, 2022)

Broad-based inflation- The recent inflation is not just the result of the international phenomenon; various factors have made it long-lasting and broad-based. It’s not just our headline inflation (which includes food and fuel) surging. Our core inflation, too, is hovering around 6.8%. Every commodity in RBI’s basket shows an increase in prices, making inflation broad-based.

Constitutional obligation- Monetary policy committee is constitutionally obligated to keep the interest rate at 4% (+/- 2%); if we look at the graph since January, it has been above the allowed limit, and even the recent R.B.I inflation expectation is showing that it will be 6.7% which means that this fiscal year inflation will be above the allowed threshold. R.B.I. has to give the government reasons for the same as the Monetary policy committee’s primary responsibility is to control inflation.

Negative Real Policy Rate- Our repo rate is still below the pre-pandemic level. If we see our real policy rate, i.e. interest rate minus inflation, we will find that it is negative, which means that the value of money deposited in our bank is getting eroded in real terms; this will have a direct impact on savings pattern.

Higher inflation expectation- The recent RBI inflation expectation survey and IIM Ahmedabad inflation expectation survey show that people feel that inflation will also remain high for the upcoming period. The different studies suggest that higher inflation expectations hurt household expenditure patterns; Juster and Wachter, in 1972, did the research and established that higher inflation expectations result in lower spending on durable goods. (Shankar, 2015)

Increase in interest rate by Federal reserve- With the increase in federal fund rate, India has seen a massive outflow of capital; till the 10th of June, 25 billion dollars had been withdrawn by the foreign portfolio investors. The Fed is expected to increase its fund rate further; hence, RBI must increase its repo rate to tackle the impact.

Though the rate hike was unavoidable, that doesn’t mean we can negate the impact it will create on consumption patterns and demand in the economy. But the normal forecast of monsoon and increase in consumer confidence, as reflected in the RBI survey, does give the cushion to MPC to decide on a rate hike. Also, the allowance of credit cards to be linked to UPI will push the consumption of small, durable goods like laptops, smartphones and other small-ticket items. The risk that this unanchored inflation poses to macroeconomic stability is enormous, and the central bank must be ready to answer these complications.

Joshi, D. (2022, June Friday). Google. Retrieved from Indian express: Dharmakirti Joshi writes: RBI leans harder to rein in inflation, but rebound in services will put upward pressure on prices

Shankar, S. Y. (2015). Inflation Expectations and Consumer spending in India; evidence from consumer confidence survey. Reserve bank of India occasional papers, 41-43.

0 notes

Text

FED President Made a New Statement: What Does It Mean for Cryptocurrencies?

The US Federal Reserve (Fed) announced its interest rate decision and monetary policy yesterday. Investors wondered what impact this statement would have on the cryptocurrency markets. The Fed’s interest rate hike and fears about inflation may cause a decline in cryptocurrency prices. However, optimistic statements that the economy will improve may be a positive development for the cryptocurrency…

View On WordPress

0 notes

Last Seen Blogs

soikeo24h-blog

Soi kèo - nhận định trước trận đấu - cung cấp th

ankhlesbian

MY STRONG POINT IS THAT I WIN

syukri567

Untitled

mithril-and-cast-iron

Tolkien Fan-Blog

batmantheanimatedseriestvseries

Batman: The Animated Series (1992-1995)