#wkwgroup

Text

528 notes

·

View notes

Text

Global fintech and its future

Fintech has long proven to be one of the fastest-growing areas of innovation. It has already managed to revolutionise several branches of the financial sector. What is the future of this industry, and in what areas will it develop most actively?

My article on Neironix to know more.

413 notes

·

View notes

Text

After a shocking win against #Germany, #Japan fans stayed after the match to clean up the stadium. Truly exemplary where all other fans can learn from them.

Great respect to the Japanese fans! 😍

142 notes

·

View notes

Text

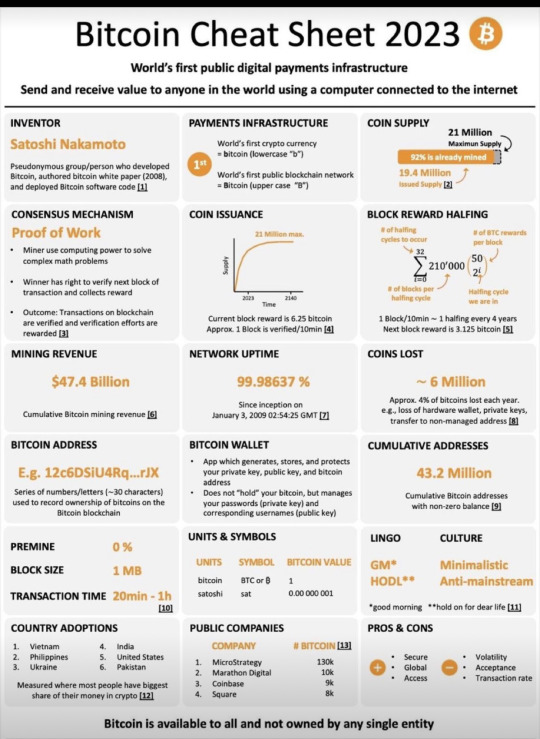

Bitcoin Cheat Sheet 2023

#tumovs#blockchain#тумовс#reinis tumovs#neobankers#crypto#defi#bitcoin#fintech#rtumovs#wkwgroup#crypto market

29 notes

·

View notes

Text

The popular gastronomic guide Taste Atlas has ranked the best national cuisines in 2022. The TOP was formed based on the results of a survey of travelers who voted for food and drinks.

In total, the ranking includes 95 cuisines of the world. Topped the ranking of Italian cuisine

TOP 10 looks like this:

* Italian Cuisine

* Greek cuisine

* Spanish cuisine

* Japanese food

* Indian kitchen

* Mexican cuisine

* Turkish cuisine

* American cuisine

* French cuisine

* Peruvian cuisine

Least of all travelers liked the national cuisines of Latvia (93) - 😩😫😢, Morocco (94th place) and Norway (95th place).

#tumovs#wkwgroup#тумовс#rtumovs#reinis tumovs#cuisine#food#mexican#italia#greek cuisine#italian cuisine#Spanish cuisine#turkish cuisine#japanese cuisine#american cuisine#french cuisine#peruvian cuisine#latvian

43 notes

·

View notes

Text

In 2023, Apple can become the biggest bank

in the world 🤯

Without actually being a bank…

When you think about it, a bank effectively has:

1. A giant balance sheet

2. Lots of data and capabilities to process it

3. Distribution

4. A license and/or regulatory oversight

Apple has it all even without the banking charter.

More importantly, recent moves into Buy Now, Pay Later and Savings accounts are yet another building blocks for the Apple Finance empire showing the tech titan is seriously planning on diving deeper into the financial services sphere.

And it makes a ton of sense for Apple to become a bank (directly or not):

- Revenue diversification 📊 52% of Apple’s revenue today comes from a single product - iPhone. By doubling down on the finance sector, Apple would be able to diversify its revenue streams and tap into a stable and growing market. A case in point here could be Shopify which now makes 73% of its revenue from FinTech solutions.

- Strong brand recognition 🔥 Apple has the most valuable and trusted brand in the world. This brand recognition is a major advantage for the tech giant vs. any other FinTech or challenger bank. Plus, every 6th person in the world already has an iPhone in his/her pocket.

- Strong financial position 💸 Apple is a financially strong company with large cash reserves. With $20.7 billion in profit just in the last quarter and more than $23 billion of cash at hand, the tech giant has all the resources it needs to compete pretty much with anyone in the banking world. Also, with massive valuation declines in both public and private markets, it might be a brilliant time for Apple to go on a buying spree and further solidify its market dominance. Potential acquisitions could be Goldman Sachs’ consumer banking division aka Marcus, Revolut, or Dave.If Apple executes this strategy the way it does its software and hardware, it’s going to be massive.

And a game-changer to FinTech as we know it.

#tumovs#wkwgroup#тумовс#crypto#fintech#blockchain#defi#rtumovs#reinis tumovs#neobankers#apple inc#apple news#applepodcasts

33 notes

·

View notes

Text

How to remain consistent...

Stop rushing your progress for the sake of consistency.

Instead, take that little step in the right direction everyday, no matter how small it all counts.

You will achieve 10x more this way.

108 notes

·

View notes

Text

𝐓𝐇𝐄 𝐄𝐕𝐎𝐋𝐔𝐓𝐈𝐎𝐍 𝐎𝐅 𝐖𝐄𝐁𝟑

The Web3 is an evolution of the world wide web and it might interest you to know how technically sound the features of Web3 are.

Web3 is technically carved of many features and this has made it better than web1 and web2 whose feature is not as powerful as web3.

The Web3 is.

. Decentralized

. Trustless and permissionless

. Artificial Intelligence

. Connectivity and ubiquity

The features of Web3 is very interesting and will make alot of things easy for users on the world wide web (www). and one of this is that the Intelligent Search Engine can collate informations and generate tailored recommendations based on profile and preference, saving you hours of work and stress.

This is just a tip of things among the evolution of Web3 you should know.

Stay connected to learn about Web3.

____________________________________

Please leave comments, subscribe and follow my news on my official social media pages: Telegram, LinkedIn, Facebook, Twitter, Gettr, Reddit, and Tumblr.

🤝 Reinis TUMOVS.

#tumovs#wkwgroup#тумовс#banking#bank#crypto#digitalcurrency#fintech#blockchain#defi#reinis tumovs#blockchain technology#bankers#bts#bitcoin#solana#ethereum#web3#crypto market#technology#finance

63 notes

·

View notes

Text

According to fintech giant CEO Dan Schulman, PayPal's recent move to allow cryptocurrency-related transfers is the first step from a fiat-centric world to a digital currency world.

PayPal in Austin at Consensus 2022

Shulman, who was joined onstage at Consensus 2022 in Austin, #Texas, by PayPal's #crypto chief Jose Fernandez da Ponte, said his firm has been doing a long time with crypto.

According to Shulman, the addition of the ability to buy, sell and hold cryptocurrencies at the end of 2020 has significantly increased the #number of #fintech users. Now further #development in this direction opens up the possibility for them to use #cryptocurrency as another source of funding inside the PayPal #wallet.

“We will instantly take your cryptocurrency and convert it to fiat, and you can use it in any of our 35 million #trading #accounts, so we are trying to add functionality,” Shulman said. “But what we just did with transfers seems like a first step, as you might think of us moving from a fiat-centric #world to a digital currency world.”

At first glance, #PayPal is just another trend-following fintech following Robinhood and other crypto apps. But enabling consumers to receive cryptocurrencies from their PayPal wallets opens up ample opportunities, da Ponte said.

“Suppose there are 100 million crypto #users. PayPal's #network of hundreds of millions of consumers and #millions of #merchants was connected but divided. We have built a bridge between this fiat universe and this crypto universe. And the value of these two networks combined will be much higher,” said da Ponte.

“Cryptocurrency was not the most convenient #solution when it came to the #payment method, but now the possibilities are expanding with the spread of #stablecoins, #regulation of crypto markets and innovations in the field of #digital identity,” Shulman said. “Volatility will decrease over time; the utility will increase.

Echoing some of the other CEOs who spoke this week in Austin, Shulman said this crypto winter is a time to double down. Asked if he owns any cryptocurrency and what he uses it for (especially since PayPal users can send their coins to #MetaMask and buy some #NFTs), Shulman said: “I buy, hold and sell – sometimes outside of PayPal. I don't sell that often."

68 notes

·

View notes

Text

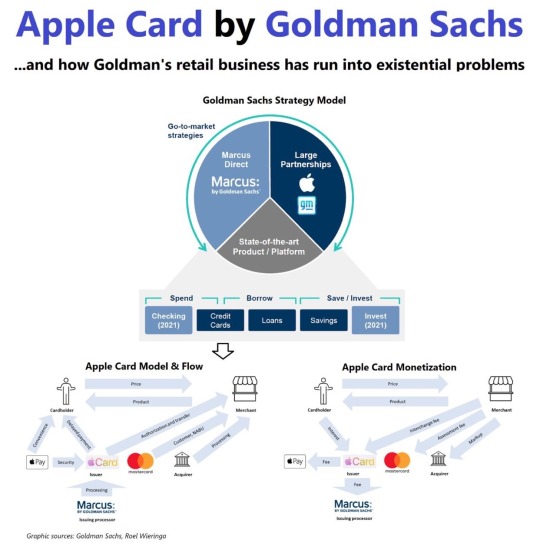

Apple Card responsible for more than $1 billion in losses for Goldman Sachs.

Goldman Sachs submitted a regulatory filing today for its “Platform Solutions” group of businesses that includes Apple Card.

The collection of consumer offerings from Goldman is on track for a loss of $4 billion since 2020 with Apple Card making up more than $1 billion of that.

Reported by Bloomberg, the new performance details from Goldman’s Platform Solutions division paint a grim picture.

In just the first nine months of 2022, the businesses including Apple Card saw a pretax loss of over $1.2 billion.

Looking back to 2020 through the end of September 2022, those losses amounted to $3 billion. But when Q4 results of 2022 are included soon, the number is expected to be close to $4 billion.

The main cause of the losses is said to be from loan-loss provisions (when a bank sets aside money as an expense for future loans it expects won’t be repaid)

____________________________

Please leave comments, subscribe and follow my news on my official social media pages: Telegram, LinkedIn, Facebook, Twitter, Gettr, Reddit, and Tumblr.

🤝 𝐑𝐞𝐢𝐧𝐢𝐬 𝐓𝐔𝐌𝐎𝐕𝐒.

9 notes

·

View notes

Text

Goldman Sachs’ foray into consumer #banking in 2016 was quickly heralded as (and seemed to be) a great success. A few days ago, the bank announced an almost $3 billion loss from that business. Let’s take a look.

Despite the initial skepticism, Marcus proved a huge success: by 2020, Marcus was one of the fastest-growing #digital #banks in the US with more than $80 billion in deposits and $5 billion in loans.

Aggressive pricing, state-of-the-art #technology, reliable customer service and a well-known brand name count among the reasons for the rise. Markus’ success was twice important because - on top of commercial reasons - it exemplified one thing: how traditional financial institutions (Goldman was founded in 1869) can adapt to the #digital age and compete with #fintech players.

Several things have gone wrong:

1) Goldman’s overly aggressive pricing (to gain market share) during the boom years

2) Poor risk #management with more than 25% of card loans going to financially weak customers and a provision rate at subprime levels

3) Expanding defaults as a result of the deteriorating macro environment

4) Bad management decisions such as the one to merge (previously independent) Marcus with the wealth management segment

5) Service quality (i.e. disputes over chargebacks) not being able to keep up with an increasing customer base.

The credit card business is traditionally a hard one to crack, more so for newcomers even if they are called #Goldman_Sachs. And there seems to be no way back for what was once hailed as one the company’s biggest successes. Timing and bad management decisions have proven – once more – an unbeatable combination.

Reawd more, the full article at: 👉

Opinions: my own, Graphic sources: #Goldman Sachs, Roel Wieringa

____________________________

Please leave comments, subscribe and follow my news on my official social media pages: Telegram, LinkedIn, Facebook, Twitter, Gettr, Reddit, and Tumblr.

🤝 𝐑𝐞𝐢𝐧𝐢𝐬 𝐓𝐔𝐌𝐎𝐕𝐒. @reinis_tumovs

#tumovs #reinis #reinis_tumovs #rtumovs #rtgroup #тумовс #banker #neobanker #тумовс_банкир #tumovs_banker

#tumovs#wkwgroup#тумовс#fintech#defi#rtumovs#reinis tumovs#neobankers#goldman#goldman sachs#apple inc#apple news#apple card#bankers#bank#digital currency#digital#digital banking

7 notes

·

View notes

Text

Bank-fintech partnerships have exploded in recent years! Instead of viewing each other solely as competitors, banks and fintechs are choosing to collaborate, working together to build and bring more innovative products to customers. The benefits of these partnerships are clear 🤝

⚡For banks: being able to adopt new technologies faster and cheaper than building them in-house.

⚡For fintechs: banks offer greater resources and the opportunity to reach thousands - perhaps millions - more customers around the world.

And for those customers, bank-fintech partnerships unlock more innovative ways for them to send, spend, and manage their money 💰💳However, these partnerships supported by BaaS providers could be under threat, as examples of companies falling down on compliance have inspired fresh regulatory scrutiny across the #US, UK and #Europe 🚫 Most recently in the #UK, BaaS provider Railsr is being monitored by the Financial Conduct Authority (#FCA) following concerns about the business’ health. Following emergency M&A talks, #Railsr now looks like it will be sold through pre-pack administration. This follows an investigation by Lithuania’s central bank over Railsr’s #AML failures. Regulators may increase oversight of partnerships facilitated by #BaaS providers, but there is a risk that what is in reality isolated incidents could lead to a backlash that makes bank-fintech partnerships appear far riskier than they are, and put banks and fintechs off of them for good ⚠️ Let's not forget that BaaS providers and early-stage fintechs already have limited and often stretched resources. Even for big banks with strong #compliance arms, partnerships may start to look like regulatory quagmires that suck up resources and nullify the biggest benefit of working with a fintech, which is making innovation faster and cheaper 💸💻 The truth is that regulation in its current form should prevent compliance failures and keep customers safe. 📌Regulators can help by providing specific lessons from incidents that allow all banks, fintechs and BaaS providers to revisit their compliance procedures with fresh eyes and make sure they have the tools in place to meet demands. This will give banks and fintechs the confidence to move forward with partnerships, and ensure that the industry and customers around the world continue to benefit from the products and services made possible by cross-industry collaboration in the years to come 🌎🌍🌏 Let's work together to make sure that bank-fintech partnerships continue to drive innovation and provide the best possible services to customers 🙌 _🤝 Dr. 𝐑𝐞𝐢𝐧𝐢𝐬 𝐓𝐔𝐌𝐎𝐕𝐒.

𝘗𝘭𝘦𝘢𝘴𝘦 𝘭𝘦𝘢𝘷𝘦 𝘤𝘰𝘮𝘮𝘦𝘯𝘵𝘴, 𝘴𝘶𝘣𝘴𝘤𝘳𝘪𝘣𝘦 𝘢𝘯𝘥 𝘧𝘰𝘭𝘭𝘰𝘸 𝘮𝘺 𝘯𝘦𝘸𝘴 𝘰𝘯 𝘮𝘺 𝘰𝘧𝘧𝘪𝘤𝘪𝘢𝘭 𝘴𝘰𝘤𝘪𝘢𝘭 𝘮𝘦𝘥𝘪𝘢 𝘱𝘢𝘨𝘦𝘴.

t.me/reinis_tumovs

facebook.com/TUMOVS

linkedin.com/in/tumovs

#tumovs #reinis_tumovs #rtumovs #rtgroup #тумовс #рейнис_тумовс

5 notes

·

View notes

Text

2 notes

·

View notes

Text

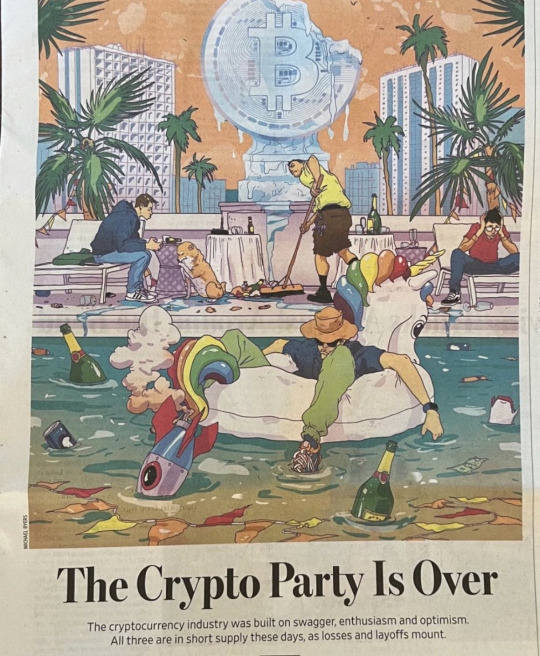

#tumovs#тумовс#rtumovs#reinis tumovs#usa#wall streeet journal#wall street#main street#wkwgroup#neobankers

2 notes

·

View notes

Text

Market Mood...

1 note

·

View note

Text

No comments 🤷♂️

2 notes

·

View notes

Last Seen Blogs

mugen-asia

Mugen Photograph

mim70

A world is full of worms

satan-gaveme-ataco

Just A Simple Girl, Wih Simple Loves

my-happy-little-world

My Happy Little Weird World

grandmofftarkinsuggestions

putting the 'kin' in 'tarkin'