#I have $800/month in student loan payments

Text

man i think i’m 5 seconds away from a mental breakdown

#I’m actually running out of money now despite working 6 days a week and making 6 figures#Because I bought my acreage with my brother and factored him paying 1/3 of the expenses BUT he’s decided to be unemployed for 1.5 years#I pay the mortgage mortgage insurance utilities internet groceries#I have $800/month in student loan payments#I have to spend like $150/week on gas because my commute is 2 hrs round trip every day#I only eat one meal a day usually because I don’t have the time to grocery shop or cook usually and my brother only cooks for himself#I do all of the chores and at least 1/2 of the yard work#I have the heaviest workload of any of my coworkers (which has been acknowledged but my manager says his hands are tied#Because if he took work off of my plate he’s have to give it to someone else and there is no one else)#I’m being severely underpaid at my job ($4 under the STARTING wage for a pharmacist now despite me working there for 3 years.#But I “got the largest raise last year” lmfao#I’ve been seeing someone but he works nights and his schedule is wack and it results in me going to bed at 3am some nights#I’m also on call this week so I have to be ready to answer calls at any time past 11pm#My hair is legit pulling out in clumps and my hair is half of my personality :(#i’m about to mcfuckin lose it#Brain feels like mashed potato#Oh also I’m on my fucking period

13 notes

·

View notes

Text

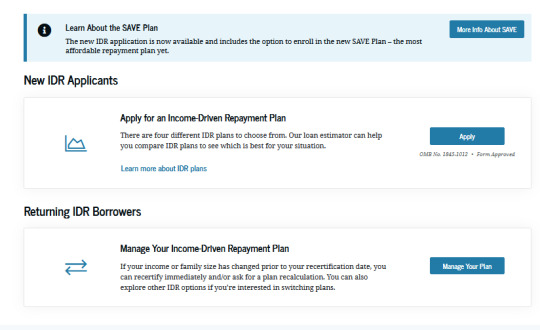

Hey, student loans payments are coming back in October, you should know about the SAVE plan.

this is america-centric but pls spread this around if you think any of ur mutuals could use the info.

If you're currently shitting yourself thinking how you're gonna start making student loan payments again, I suggest taking a deep breath, first off. Get comfy, put on some music and strap in.

If you got your student loans through the Federal Student Aid program FAFSA, then you can apply for an IDR (Income Driven Repayment plan) called SAVE.

what is SAVE?

This got my $115 monthly payment down to $40 a month, if you don't work or you can't afford much, this has the potential to reduce your payment even further.

Alls you need to do is go to https://studentaid.gov/idr/ and log into your federal student aid account, there's a section for both first time applicants and returning borrowers who previously may have had an IDR.

Even if you've done an IDR before! Look into the SAVE plan!! It forgave about 10k of debt for me!

Anyway, first time applicants can click the first option, "Apply for an Income-Driven Repayment Plan" and just go through and answer all their prompts, make sure you have all your financial information on hand (tax returns, most recent pay stub, etc) and go through the prompts until it gives you the option to apply for the SAVE plan. CLICK IT!

It should let you know at the end exactly how much you'll be paying per month and you should get an email confirmation as well. Any account specific questions should be directed to their call center

+1 (800) 433-3243

GOOD LUCK AND BE PATIENT, THE SITE IS SLOW AS SHIT.

DON'T GIVE UP! I BELIEVE IN YOU!!

if you have any questions feel free to DM me btw

#student loans#SAVE plan#FAFSA#student loan forgiveness#IDR#income driven repayment plan#THIS DOES NOT PAUSE INTEREST BTW#adulting#life tips#helpful#resources#websites#og post

426 notes

·

View notes

Text

so I still need help lmao

My last post was getting very long so I’m making a new shorter one to consolidate info

on october 17th, my car spun out and I hit a pole on my way to work, leaving it totaled and forcing me to get a new used car, which I need help paying for and fixing up since I was already barely skirting by financially and my last car was already paid off when it was signed over to me

Payments need to start being made in december. The car was roughly $9000 but I’ve lowered my goal to account for money we got by scrapping the car and from donations received outside of GFM. I work minimum wage and am already drowning under student loan payments for a degree I regret that have skyrocketed to over $500 a month as of the start of november. In addition, the cost of my insurance has gone up so in total the car payments will put me at over $800 a month spent on JUST these three bills. THIS IS NOT FEASIBLE WHEN I MAKE $1200 A MONTH IF I’M LUCKY. THE CAR ALSO NEEDS MAINTENANCE AND NEW TIRES FOR WINTER AS SOON AS POSSIBLE.

WAYS TO HELP (warning for accident photos on the gfm link):

https://www.gofundme.com/f/finch-needs-to-pay-for-their-new-car

p@yp/al: [email protected]

ko-fi: galahawk (ko-fi.com/galahawk)

EDITING TO ADD: I saw someone in the notes mention the student loan forgiveness program and while I appreciate the info and have already applied for relief on my federal loan, something important about my loans is that the big loan that is the actual life-ruining $60,000 one is private, meaning federal relief can’t touch it and never will. I wish I had a better answer than that but unfortunately it is what it is :(

4650/8400 as of january 21st 2023

156 notes

·

View notes

Text

Crazy to me how humans have literally made life so difficult for ourselves for no reason at all. Like why do we have to pay for water monthly when it literally falls from the sky? Why is a super simple one bed, one bath “house” (cheaply made of course) easily between $250k-$400k and someone would have to pay a high monthly payment with a 20% interest rate to have it? Why did we choose these numbers? When did we make prices for food so high, create mortgages, student loans, and car payments? Who created interest rates? Why does my entire future depend on a credit score? A number we ourselves made up. Why did we go the extra mile and decide to tax ourselves? For what purpose? When did we decide that we need to have a certain level of education to succeed and if you don’t have it you are obviously a failure at life. When did we say “yes, this seems good, I want to pay astronomical amounts of money for literally everything and make everything as stressful as possible for no reason at all?” Why do I owe money for having money (taxes)? Why can’t I pay for stuff with rocks? That cat I see sleeping in a warm beam of sunlight (and living a happier life than I) doesn’t have a credit score, it doesn’t have to pay extreme amounts of money for a home, it doesn’t have to pay for water that falls from the sky, it doesn’t have to worry about interest rates, it doesn’t know what the Pythagorean theorem is, it doesn’t have a car payment, a set of tires doesn’t cost it easily $1,000 in one go, it didn’t make applying for a home or a car an exhausting endeavor, it doesn’t have to work 40+ hours a week working on stuff that we made up all for a check that doesn’t even reasonably cover any expenses (that once again we forced on ourselves). So why are we?? Why can’t we help ourselves out and make rent $10 a month? Why can’t a good credit score be a 10 instead of 700-800? Why can’t a mansion be $10,000 instead of a million? Let’s make grocery shopping easier by trading cool rocks and pieces of clay pottery and buttons and other neat things for food. What’s stopping us from doing that? Why did we create the most complicated system? “The entire system would collapse, there would be anarchy, everything would shut down, society would explode!!!” Why?? Over numbers and problems we made up ourselves? It’s all made up!! Why did we make it so hard? We could have made things so easy and have a perfectly workable society. We could have the most bonkers system and could all be schooling life right now if we paid for stuff with pretty things we find in abundance and made houses cost like one pretty vase and a loaf of bread you bought with your cool acorn stash and made cars only cost a packet of tomato seeds with no interest rates in sight, didn’t make the production of goods and supplies so expensive, and if we simply didn’t tax ourselves, and if education/the school system was literally just learning all sorts of things that could help you live a happy, self sufficent, simple, productive life the way you want to live it (if you want to learn about history, languages, how to work on cars, or build robots, or cooking, or music, making pottery, or conducting science experiments, learning about medicine, or playing sports or whatever you could do so) and it wouldn’t cost you your first born child, and if we didn’t have mind numbing jobs trapped in windowless buildings doing things that shouldn’t actually matter or exist but we made them so. Why did we make it so hard??

#I had to get a new car bc the one I had for only 6 years and was relatively new went I got died on me this year#I got another car#like 4 months later the battery in it died so I had to spend almost $300 for it#I have a car payment now when I didn’t with my other car that I was so proud of myself for buying outright all by myself bc I saved & saved#I shouldn’t have had to save that much in the first place#why can’t cars cost a pretty painting you made?#or cost 10 neat rocks a packet of flower seeds and 2 books?#my phone quit on me about a month ago so there goes $300 dollars#my car insurance cost $600 this month#my car already has two nearly bald tires#gonna have to pay almost $500 for two of them#I mean it never ends!#and for what?#why is it so hard and expensive??#why didn’t we make a society that could run in $10.00 houses and pretty rocks for household goods#and not base our lives on a random number we made up#every other animal in the whole kingdom must be laughing at us for being so stupid#I’m just complaining (as per usual)#I’m tired of all my money disappearing the second I get it because literally everything is so expensive#it’s one problem after another! I’m tired!#let’s just suddenly announce all houses are $100.00#but Chief all of society would collapse?!#no it wouldn’t because I say it wouldn’t bc this is all *make believe*#life as we know it is just a game and everbodies losing because a select few keep changing the rules

3 notes

·

View notes

Text

Today's Episode of...

...Sorry Millennials, But There Are a Butt-Ton of us Boomers Who Know EXACTLY What You're up Against. I receive newsletters from a website called "Bon Appetit". It's pretty chi-chi, but it has some fun recipes, and it's free, so there it is. "Bon Appetit" has a series called "The Receipt", articles about what subscribers eat and how much it costs. Today the newsletter contained an article titled "How a 24-year-old Waitress Eats on $18K/Yr". I thought, "Oh, this is going to be good." And by "good" I meant "ungood". It did not disappoint. Or it completely disappointed, depending on POV. I'm not providing a link because: 1) the person who wrote this did so anonymously, so screw them; and 2) drivel like this does not deserve more of a platform than it already has.

The lady in question lives in Durham, North Carolina, and just received her masters in linguistics (Although she says she's still working on her thesis. There was a time when getting a masters before even finishing your thesis, let alone defending it, was a laughable proposition. Further evidence of the crapification of US education, even at a place like Duke.). She is looking for a job in her field, and is supporting herself by waitressing and teaching pottery.

Then she lists her expenses, and the red flags become unmissable. Her rent is $800. In a college town. How many people live in that apartment with her? Or does she live with her parents, and this is the token rent they charge? $76 for car insurance. Which means she doesn't have collision insurance, which means she doesn't have a lender's lien on her title, which means she paid cash for the car. Or somebody did. Or she's just driving one of her parents' cars, and she's paying Daddy a little toward insurance. I'm inclined toward this last option because her budget includes neither maintenance nor fuel.

Speaking of items omitted from her expenses, no health care. No health insurance. She's 24 and just graduated. Bets she's still on Mummy and Daddy's plan? No student loan payments either, not even a projection for them when they kick in in a couple of months. But she tips her hand here, admitting she has $15,000 in savings, the bulk of it being what's left over from what her parents gave her for school. JFC. And let's not forget her pottery teaching. No expenses listed for that. Not studio rental. Not equipment and supplies. Nothing. Which in all probability means Mummy has a pottery hobby, and daughter is free-riding on it.

Which means she isn't living on $18K. She's living on Mummy and Daddy, just like every other "successful" Millennial not engaged in overt criminal activity.

And now a message for my age cohort. Just shut your pie holes with the "Well if she can make it, other Millennials should too" stuff. Seriously, just STFU. If you can't see the parade of bullshit flags flying over articles like this, you don't get to have an opinion. You have no excuse. You're not as senile as the folks or as callow as the kids. You should be seeing this propaganda for what it is. Up your game.

34 notes

·

View notes

Text

Y’all I make under $1600 a month and I have to pay $800 for my car and private student loans and now I have to ALSO include my federal student loan payment in October?? Like seriously how are any of us supposed to survive?? Thank god my mom doesn’t charge rent cuz idk what would happen

5 notes

·

View notes

Text

What about the CARES Act?

In response to the coronavirus pandemic, federal student loans have been placed in automatic forbearance. No interest will be charged to lenders during this time. And now y’all have the tools you need to understand that in almost all situations, this is a fantastic deal.

Please note that this only applies to federal loans owned by the Department of Education. If your loans are private, you’ll have to talk to your private student loan lender. Each one will have their own policies and criteria around forbearance.

If you had a more unconventional federal loan (for example, one with work study requirements), check out this FAQ. If you’re not sure if your loan is covered, ask your student loan servicer by going to StudentAid.gov or calling 1-800-4-FED-AID (TTY: 1-800-730-8913).

And if the federal government extends the program, keep taking advantage of it. If the interest rate‘s nil, don’t pay that bill!

What if I want to keep making a loan payment every month?

You can if you want to! The government will continue to process payments, so there’s nothing stopping you.

However, I would not recommend making payments on federally forborne loans unless you have a great reason for doing so. There’s really no benefit to making payments on such a loan during this time, as opposed to, say, saving the money up and making one big lump payment at the end of forbearance. And there are lots of great ways to reinvest it in better areas.

Start or grow your emergency fund. That’ll give you more cushion if you lose your job or get sick. And once you’re out of the woods, you can still use what you saved during forbearance to pay off the loan.

Eliminate credit carddebt. It almost certainly has a higher interest rate (and thus is more expensive to you in the long run) than your federal student loans.

Direct the funds toward private student loandebt that is not forborne. Odds are good their interest rate is also worse than the federal loans.

Shop locally. If you’re rock solid and you really don’t think you need any of those things, I’d rather you kept the money circulating in your community than sending it back to the federal government. Think of the non-chain stores you want to stay afloat, and buy something from them. Leave huge tips for patio servers and delivery drivers. Become a patron of artists you like. (LIEK US.) Any of those actions would better fulfill the spirit of the CARES Act: to keep the economy moving.

So many markets are unstable right now: jobs, housing, health, supplies… You’ve got six months of borrowed time thanks to student loan forbearance. Use them wisely!

Ask the Bitches: “The Government Put Student Loans in Forbearance. Can I Stop Paying—or Is It a Trap?”

22 notes

·

View notes

Text

If I don't get out of this house and get my own place I am going to kill myself.

I went from one bedroom and an office to one 10x8 bedroom that acts as an office and bedroom. All my belongings are in boxes in a basement. My daily necessities are cluttering up my room so bad I can't function. I have no room for my clothes other than one single dresser (I used to have a closet and three dressers).

Now I am being told I can no longer keep my pillowcases and bedsheets, tampons, pads, extra toothpastes, hand soaps, razors, etc., in the bathroom linen closet because they're suddenly "taking up too much room" and "you don't need more than one bedsheet anyway".

The groceries I buy for myself are getting eaten by others. Or thrown out to make more room for their dinners. Sometimes being straight up put in my bedroom because it's "taking up too much space" in the fridge.

I used to have some mugs. They're now in a box in the basement because "you have too many you don't need those" meanwhile they have TWO full cabinets of THEIR mugs.

Not to mention the molded carpet in the BATHROOM that she is REFUSING to have removed because her "feet get cold" and the green carpet from 1965 that is so old there's holes in it that is also being refused replacement because "it's fine it's just old". Or the mold in the bathroom. Or the termites eating the foundation. Or the superficial tree roots ripping apart the concrete walkways that are full of cracks and missing chunks.

The house is literally falling apart. I am having more and more of my stuff taken away. Being confined to a smaller and smaller amount of room.

And we wonder why my depression has gotten worse.

And we get on my case about that too.

"oh you need to get out of your room more" And go where?

"you need to stop sleeping so much" Why? 90% of the things that made me happy are gone.

"you need to go outside and work out more" glad we're also adding in my weight to this ever increasingly shitty situation. But when I try to buy food for myself that's better and healthier than going out to buy food daily it gets tossed or eaten before I can eat it.

"you need to stop buying things" I know. Because you're just gonna make me get rid of it anyway.

"you need to work more hours" why? So I'm out of the house more? I never leave my room, I'm literally not bothering you at all.

"you need to make more money, find a different job". With a higher pay comes higher stress which I can not handle. I am staying in my lane as far as stress and responsibility goes.

I want to move out but I can't. Not with a Poor rated credit score. No savings. High debt thanks to student loans and past mistakes. And definitely not in this housing market where the average cost of a home in NJ is half a million. And rent is at an average of 3k per month for most pet friendly studio apartments. Which I am automatically disqualified for anyway due to my credit (and also automatically disqualified for home loans as well).

I don't have anyone with good credit to find a place with. Plus my credit score would drag theirs down (both people in the lease means adding both credit scores and dividing by two, with my credit score even someone with an 800, which is pretty much unrealistic and would probably be lower, would be dragged down to the 680s which would determine interest, monthly payments and eligibility).

So basically there's like no point to anything. No assistance. No help. No way of digging out of the hole. No hope.

5 notes

·

View notes

Text

April is killing me, mentally, emotionally, and financially. I make a grand total of $2200 a month. I do get an extra paycheck this month thanks to the way the calendar lines up, so $3300.

April 1 ofc starts with my $1300 rent (cannot wait til my lease is up). At $2000.

I owe $800 in taxes. At $1200.

My cats just had surgery. Low cost clinic, still cost $200. At $1000.

Add in the usual bills, car insurance, rent insurance, internet, electricity, student loan, phone bill, etc. Takes me down to roughly $500.

I had my shipment of cat litter this month (3 month supply), which takes $160 (don't come at me for the price, it's the only litter my pretentious little shits will use. Anything else they'll piss and shit on the floor next to them). That's $340.

The cat food I bought made my cats sick. Had to throw out the $20 bag I got (gave to my mom, her chickens love it) bought a new bag for $30. $310.

Just found out that my insurance no longer covers dental. I have 2 cavities. Basically had to get additional dental insurance just to fix this issue. The first time payment was $90. There's $220 left.

On Tuesday (2 days ago) I'm sitting at work, I have DND on my door because I'm editing video and need to focus. My coworker barges in and starts demanding I do something that isn't part of my job nor do I even know how to do it. Informs me that I'm not entitled to have DND on ever. She could've at least knocked. She scared tf out of me just forcing her way in.

I find out that she's been telling higher ups that I sit in my office and sleep/play video games, which I do neither of. Maybe if I'm clocked out on lunch I'll play some games on my phone. But I'm not on the clock. She's putting my job at risk with her lies.

She also told me I needed to see a psychiatrist and gave me a business card. I'm not in the market for a psychiatrist. Never have been, never said i was. She said it's clear I need to be put on medication.

The Watcher thing happened.

I come home work after the thing with my coworker to find a note on my door. Leasing office is doing inspections today (Thursday). I'm dead in the middle of spring cleaning and my apartment looks like a mess. + my cats are recovering from surgery. I'm just waiting for an inadequate housekeeping charge or something to come onto my account. Plus they're checking blinds and will replace broken ones at a cost to me. I know one needs replaced bc my one cat ripped them up. Additional $35. At $185. And we all know that $185 is gonna go to feeding me, with the bare minimum.

Oh and 2 of my moms cats were stolen and there's no information on where they went. So they're just gone.

0 notes

Text

Moving Question.

I'm going to need to see how much I have to save for a couple of things.

0. Upcoming Expenses:

College Applications: $340.00

Carl and Clyde Care Sitter: $160.00

Plane Ticket / Car Rental: $350.00

Credit Cards, and Student Loan: $200 each.

1. Carl and Clyde's neutering:

$2000, still need to see if it might be $200 with their check ups

2. Carl and Clyde's AirBnb:

Need $2,159.31 to start, will pay per month from

$1,948 Per month

Total: $7,632.63

3. Uhaul Storage and Moving Truck:

$177.29 - Movers, truck, and supplies

$190 - First storage month

Total: ~$370.00

4. New Clothing Style (Golfing):

Cole Haan Oxford Shoes (2 Pairs): $360

Hat: $32

TM Belt (2 in total): $90

TM Shorts (4 in total): $360

TM Shirts (4 in total): $400

TM Other Shirts not $100 each (3 in total): $177.29

Titleist Backpack: $130.00

Total: ~$1,570.00

5. Golf Clubs

Hybrid - $230

Putter - $400

Wedges - $180

Irons - $800

Driver - $700

Bag - $380

Total: ~$2,690.00

6. Mykonos Trip :

7. What to pay:

Capital One - $486.44 - Paying next paycheck

Chase - $490.53 - Paying next paycheck

Student Loans Payment, total - $36,680 ($48.54 Past due / $373.34 Due)

8. Workout stuff, workout clothes, skincare, massages?

Nike Romanelos 4 Weightlifting Shoes - $200.00

Workout shirts (6 Pair)

Workout Shorts

Underwear

Socks

Estimate: $600

IS Neck Complex: $105.00

New Workout Trainers: $130.00

Takeaway, I really need to start saving everything I can.

0 notes

Text

Alice was loud and very energetic in bed that night. I didn’t realize she’d packed a strap-on until it was lubed up and going up my asshole.

I slept hard and woke up to Alice licking my pussy. It felt amazing and she kept going after my first orgasm, so I was saying all kinds of dirty shit when I saw my father approach my bedroom and then turn away quickly. “Sorry dad!” I said.

Alice looked up. “I love that your bedroom doesn’t have a door. Did he see my ass?”

“I think he saw your everything,” I said.

“Good,” Alice smiled.

“Eat my fucking pussy,” I said.

We drove home after breakfast that morning and I went to work at 5. Ivy was miserable because she wasn’t going to make rent and her student loan payment that month “without prostituting myself.”

“So prostitute yourself!” I said. “I’ll pay.”

“Gross,” Ivy said.

“You know I will just pay your rent if you want,” I said.

“You know I will never accept that.”

“What if I had a cheaper apartment for you? Very cheap.”

“Under 800 a month would be dreamy.”

“How about 200 a month?”

“Where?”

“Move in with me.”

“You have a studio apartment.”

“So?”

By the end of the night, Ivy said yes. I jammed $400 in her bra to help her get by in the meantime. She let me kiss her.

“No,” Alice said.

“What do you mean, no?”

“That girl is a closet case. I’ve met her twice and I know that. If you live together, you will fuck her. A lot. And you’re only supposed to fuck me.”

Honestly, I wanted Ivy so bad that I didn’t even know it. I got righteously mad at Alice’s totally correct suspicion. And she laughed in my face. I wanted to punch her.

“Well I don’t know what to do now. Ivy’s packing as we speak.”

“Well, you should start too.”

“What do you mean?”

Alice kissed me hard. I swooned. “Ashley, will you move in with me?”

I said yes, so she pulled my jeans down and ate my ass while I bent over against her kitchen counter.

0 notes

Text

oof. was looking into federal student loan consolidation and while the new SAVE plan *would* save me money in the long run... I'd also have a way higher payment at first because I make a lotta money. And I don't think I can handle several hundred in loan payments, that'll climb to almost a thousand as I (and my fiancé) make more money Dx

I'm glad for the MANY this plan helps (especially those whose plan effectively deletes monthly payments or cancels it today), but it just doesn't do shit for monthly payments if you make much more than the income cap.

like. here's the tea. I make 78,000 a year right now (imo kinda high for right outta college, but I ain't complaining). Min wage here is something like $15.50, so like 32,000 a year at full time pre-tax. When me and my fiancé marry, my FEDERAL loan payments alone would shoot up to $500 a month (currently would be $200 for standard repayment)! On top of my existing private loans (thanks mom! /s), that'd be $800 a month TODAY. Depending on our income it could easily be much higher.

That's just, like, a lot! It'll be a bit easier once my fiance is working as well & can contribute some to rent and groceries and stuff, but like. They want to save for a gemology program. I don't want them to feel like they have to juggle working full time plus the program. Sure, my loans would all be paid off in a few years... but that extra $300+ a month is savings for other things in life. *sigh* maybe I'll apply for standard and then swap to SAVE once my fiancé is working.

Assuming my fiancé's loans aren't hell, too.

and I feel like this is an important side of the SAVE plan discussions. There are some things it does very well - interest doesn't capitalize so long as you make payments (and the $0 payments count to that!), much higher no-payment cutoff, loans get forgiven after like 20-25 years no matter what (in line with other income based repayment plans tbh)...

It's just. scaled weirdly. I would love to apply for it because paying less over the loan is VERY appealing to me, even if my payments are a bit higher. I just wish it wasn't SO much higher that it's better to go standard and toss more money at it when I can, knowing that by default I'll spend an extra 15-20k on those loans if I can't.

ugh. I hate that student loans exist. I hate that the forgiveness got axed, and that they aren't going through other avenues to forgive it (and afaik, not HARD pushing Congress/the Democratic party to make loan forgiveness a BIGGER thing).

No cutoffs. No applications. Just delete some amount from our loans.

#copied from my mastodon#student loans#frustrated with this shit i hate capitalism i hate debt i hate how bullshit this system is and how annoying it's set up

0 notes

Text

ughhhh i tried to make a Wise Financial Decision by pre-paying my student loans over the summer (since i don’t get paid over the summer)

but it has BITTEN me in the ASS because my regular payment ALSO went through and now i have two-digits of bucks in my checking account and a few hundred in savings solely bc my father had pity on me

i know setting up my loans to be over in 5 years was the right long-term decision but oh my god it’s wild what losing an extra 800 dollars has done to my state of mind

AND i won’t get paid again until september hahahahahhahahahhahha

LUCKILY i have no Dire Expenses and I have no risk of going hungry or unhoused or unmedicated but Not Buying Anything At All for two months is uhhhhhhhhhhhhh gonna be rough on my coping mechanisms

0 notes

Text

7 Budgeting Secrets for Debt Relief: Mastering Your Finances 101

Managing your finances effectively is crucial for achieving debt relief and financial freedom. In this article, we will explore seven budgeting secrets that can help you take control of your money, pay off your debts, and build a stronger financial foundation. By following these strategies, you can work towards a debt-free future.

Assessing Your Financial Situation

Unlock the Secrets of Forex Trading: Discover a Free, Yet Powerful Learning Course at ForexFinanceTips.com

- Understanding Your Debt: First, make a list of all your outstanding debts, including credit card balances, student loans, and personal loans. Knowing the exact amount you owe is essential to create an effective debt repayment plan. For example, let's say you have $5,000 in credit card debt, $10,000 in student loans, and a $2,000 personal loan.

- Analyzing Your Income and Expenses: Calculate your total monthly income from all sources. Identify your essential expenses, such as rent or mortgage, utilities, transportation, groceries, and insurance. These are the necessary costs to maintain your daily life. Differentiating between essential and discretionary spending helps you allocate your funds wisely. For instance, if your monthly income is $3,000, and your essential expenses total $2,000, you have $1,000 left for debt repayment and non-essential spending.

Setting Realistic Financial Goals

Learn Python Coding and Django Web Development, 100% Course, Easy to navigate and complete learning road map at dtlpl.com

- Prioritizing Debt Repayment: To start reducing your debt, prioritize which debts to tackle first. Consider factors such as interest rates and payment terms. For instance, high-interest debts can accrue more interest over time, making them costlier in the long run. By focusing on paying off high-interest debts first, you can save money on interest payments.

- Establishing a Debt Payoff Timeline: Set a realistic timeline to pay off your debts. Divide your total debt by the number of months you plan to achieve debt freedom. For example, if you have $17,000 in debt and aim to be debt-free within three years, your monthly debt repayment goal would be approximately $472.

- Creating S.M.A.R.T. Goals: Make your goals Specific, Measurable, Achievable, Relevant, and Time-bound (S.M.A.R.T.). For instance, instead of saying, "I want to pay off my debt," set a specific goal like, "I will pay off $5,000 of credit card debt within the next 12 months by increasing my monthly debt repayment by $417."

Creating a Comprehensive Budget

If you have a Dog, Cat, Bird, or any Pet at home, The Most Informative Pet Blog NiceFarming.com

- Tracking Your Income: Keep track of your income and ensure it covers your essential expenses and debt repayment goals. This will help you avoid overspending and stay on track with your budget.

- Allocating Funds for Essential Expenses: Allocate a portion of your income to cover essential expenses such as housing, utilities, transportation, groceries, and insurance. For instance, if your housing costs amount to $1,200, utilities to $200, transportation to $300, groceries to $400, and insurance to $100, your total essential expenses would be $2,200.

- Trimming Non-Essential Expenses: Identity areas where you can cut back on non-essential spending. For example, reducing dining out expenses, entertainment costs, subscriptions, and unnecessary shopping can free up more money for debt repayment. By prioritizing your financial goals, you can make conscious choices and avoid unnecessary expenses.

- Budgeting for Debt Repayment: Allocate a significant portion of your monthly income towards debt repayment. For instance, if your monthly income is $3,000 and your essential expenses total $2,200, you have $800 left. Aim to allocate at least 20-30% of this amount towards debt repayment, which would be $160-$240 per month.

- Building an Emergency Fund: Creating an emergency fund is crucial to avoid falling back into debt during unforeseen circumstances. Aim to save at least three to six months' worth of living expenses. Start by setting aside a small portion of your income each month until you reach your desired emergency fund amount.

Implementing Effective Budgeting Strategies

- Using the Envelope System: The envelope system is a simple yet effective strategy to manage your spending. Label envelopes with different expense categories such as groceries, transportation, and entertainment. Place the allocated amount of cash in each envelope and spend only from the designated envelope. This method helps you visually track your spending and prevents overspending.

- Applying the 50/30/20 Rule: The 50/30/20 rule suggests allocating 50% of your income towards essential expenses, 30% towards discretionary spending, and 20% towards savings and debt repayment. Following this rule can help you maintain a balanced budget and ensure you're saving and repaying debt consistently.

- Automating Bill Payments: Set up automatic bill payments to avoid late fees and penalties. Automating payments ensures that your essential expenses are covered on time and helps you stay organized and disciplined with your finances.

- Negotiating Lower Interest Rates: Contact your creditors and negotiate lower interest rates on your debts. Lower interest rates can significantly reduce the amount of interest you pay over time and help you pay off your debts faster.

- Seeking Professional Assistance (if needed): If you're struggling to manage your debts or create a budget, consider seeking help from a financial advisor or credit counseling agency. These professionals can provide personalized guidance and support to help you achieve your financial goals.

Staying Committed to Your Budget

- Regularly Reviewing and Adjusting Your Budget: Review your budget regularly to ensure it aligns with your financial goals and reflects any changes in your income or expenses. Adjust your budget accordingly to accommodate unexpected circumstances or changes in your financial situation.

- Finding Accountability and Support: Share your budgeting goals with a trusted friend or family member who can hold you accountable. Having someone to discuss your progress, challenges, and achievements can provide valuable support and motivation.

- Celebrating Milestones and Progress: Celebrate each milestone and progress you make towards your debt relief goals. Whether it's paying off a particular debt or reaching a savings milestone, acknowledging your achievements will keep you motivated and encourage you to keep going.

Frequently Asked Questions

Should I pay off my high-interest debts first?

- Yes, focusing on high-interest debts first can save you money on interest payments and accelerate your debt repayment journey.

How long does it take to become debt-free?

- The time it takes to become debt-free varies depending on your total debt, repayment strategy, and financial situation. Setting realistic goals and consistently sticking to your budget will help you achieve debt freedom sooner.

Is it necessary to have an emergency fund?

- Yes, having an emergency fund is crucial to handle unexpected expenses and avoid resorting to debt during financial emergencies.

Conclusion

By implementing these seven budgeting secrets for debt relief, you can take control of your finances and work towards a debt-free future. Remember, effective budgeting requires discipline and commitment, but the rewards are worth it. Take the first step today, create your budget, and embark on your journey to financial freedom.

We hope this article has provided you with valuable insights and practical strategies to master your finances and achieve your debt relief goals. Feel free to share your thoughts, experiences, and additional tips in the comments section below. Together, let's support each other on this path toward financial well-being.

Read the full article

0 notes

Note

Hi, I'm mid 20s just now trying to build credit. Do you have anything that's like, explain like I'm 5, cause I really don't understand and I'm feeling like I'm playing catch up with my life. From picking a card, to actually building it?

Okay, so building credit sounds super complicated, but I promise that it's not. A lot of the complicated things, like calculating your credit score, are done by other people. Your job is to spend money so responsibly that it impresses the people doing the calculations.

Building credit is very important these days, and no credit score is even worse than a bad credit score. It is important to have a credit card, even if you don't need to borrow money and you have enough. This is so that one day, if you have a $20k medical emergency, or you want to buy a house and you need, like $500k, your bank trusts you enough to give you the money you need.

Credit is something (usually money) that you borrow for something. The example we'll use for this post is money being borrowed to pay for something. Your credit score ranges from 300 to 800, and as long as you're above 700, you have nothing to worry about.

Interest is the money you pay on top of the credit you borrowed. If you borrowed $100 in credit with 10% interest, that means that you will pay the person back $110. The interest depends on so many factors such as how much money you are borrowing and who you are dealing with. So there is no set number.

There are four types of credit:

Revolving Credit - Like a credit card, where you get a certain limit of credit every month. If you use that credit, you can pay it back within that month with no interest, so just the amount of $ you borrowed and nothing else. If you don't, it'll roll over to the next month and you'll have an interest added on top of it.

Charge Cards - They are like credit cards, but you can't roll the credit onto next month. You have no choice but to pay what you borrowed in full that very month. This isn't as common these days but some banks might still offer this option.

Service Credit - When you pay for a month-long or annual service, like a bill. You get that service continuously, but you have to pay for that at a certain point. Think of it like Spotify Premium. You'll probably pay once a month for that, but you can enjoy unlimited music with no ads all month long. The same applies to rent and gym memberships.

Installment Credit - This is where the big money comes in. You use these for student loans and mortgages on your house or car. Assuming you have a good credit score, you might be interested in buying a house. The bank will pay the seller the money they need, and you'll have an agreement with the bank to pay them a certain amount, with interest, every month. The bigger the monthly payment, the smaller the interest, and vice versa.

The reason why everyone is so scared of credit is that if you don't pay your credit on time, the interest starts to pile on, and your credit score plummets. So, if you have an emergency tomorrow and desperately need to borrow money, the bank won't trust you so they won't give you the money you need.

But don't worry! It's not that hard to keep a good credit score! All you have to do is practice the following smart financial habits:

Get a Starter Credit Card. You will probably have a low credit limit, like $500 on it, maybe more, maybe less. But using that card is the first step towards building a credit score. You can set up your account to automatically pay your card in full every month.

Don't Spend What You Don't Have. If you're going to use the credit card, use it for something you were already going to get, like gas for your car. Make sure to pay the card back that day, or automate payments with your online banking accounts. Depending on which bank you're with, they should have an online guide on how to do that, but it's usually done through your credit card settings.

Spend Below 30% of Your Credit Limit. So if your credit card has a limit of $1000, you shouldn't spend any more than $300 a month, and make sure you have enough money in your connected checking account to pay that amount off that month. Some people swear that the magical spending number is 7%, so $70 on a $1000 credit card.

Only Get Loans if They're Unavoidable, and Pay Them Back ASAP. In a perfect world, you'll have enough money that you don't need to borrow a loan. Unfortunately, sometimes you have no choice, like with student loans. Your best bet is to agree on a monthly payment option that is as high as you can comfortably pay with low interest. This way, you pay it back faster and with less money wasted on interest.

To be completely fair, most of what I learned about credit was from the Bitches at @bitchesgetriches so if you have more detailed questions, I cannot recommend them enough.

💋

2K notes

·

View notes

Text

Finances Report: Dec 2021

I start as an attending in a few months, so I've been attempting to get my finances in order. I won't lie. I've spent the last six years with my head in the sand financially. I haven't checked the balance on my federal student loans since I graduated medical school. That is until yesterday when I found a painful balance of approximately $280k. On top of my federal student loans, I have two additional loans--one a $10k institution-specific loan that had crazy low interest, and the second a $20k Sallie Mae loan for residency apps and relocation. I also carry a substantial amount, about $5k, in credit card debt.

During residency, I was paying a collective $800 per month for these debts. Thankfully I lived in a city with crazy low COL, so it actually wasn't that bad. But I didn't have any financial buffer. It was paycheck to paycheck. I'm lucky in that had something financially devastating happened, my parents would have bailed me out. I'm incredibly blessed in that regard.

I started fellowship with a move to a city with a much steeper COL. It only took me a couple of months to realize there was no way I could continue to fork out $800 a month when my rent had quite literally tripled in price. So I put my federal loans into deferral while continuing to pay off my institution-specific loan, the Sallie Mae loan, and credit card.

I've made slow progress in the interim, mostly thanks to YNAB budgeting making me more aware of my unnecessary spending patterns. I got a $19k (after taxes) signing bonus for my attending gig that allowed me to pay off my credit card in whole and stash the remaining $15k in my savings account. I've made regular payments on my institution-specific loan, and its balance now sits at approximately $600. The Sallie Mae loan is probably the biggest financial mistake I've made thus far. The interest is killing me. Despite six years of repayment, I owe just shy of the initial $20k I borrowed. Fuck me. Any med students readers out there, if at all avoidable... PLEASE don't make this same expensive mistake.

So with all this knowledge, I calculated my net worth:

Debts: $302k

Assets: $19k (Checking $3k, Savings 16k)

Net Worth: -$284k

Woof.

Thankfully, I'm lucky enough to be walking into an attending gig with a starting salary that exceeds my debt burden by quite a bit. This is still going to take a while to pay down, especially since I haven't hit my debt ceiling yet. I'm in dire need of a car and will likely be buying a house considering the shit housing market has also made the rental market a complete shit show. So I guess this is my starting point.

16 notes

·

View notes

Last Seen Blogs

cinematic-explorations

Cinematic Explorations

macsap

🌲

bianglalakecil

catatan mrs.z

beatrice-bradley

無標題

lgbt-icons-bruh

We’ll Have A Gay Ol’ Time (SOON...)