#Inheritance tax planning

Text

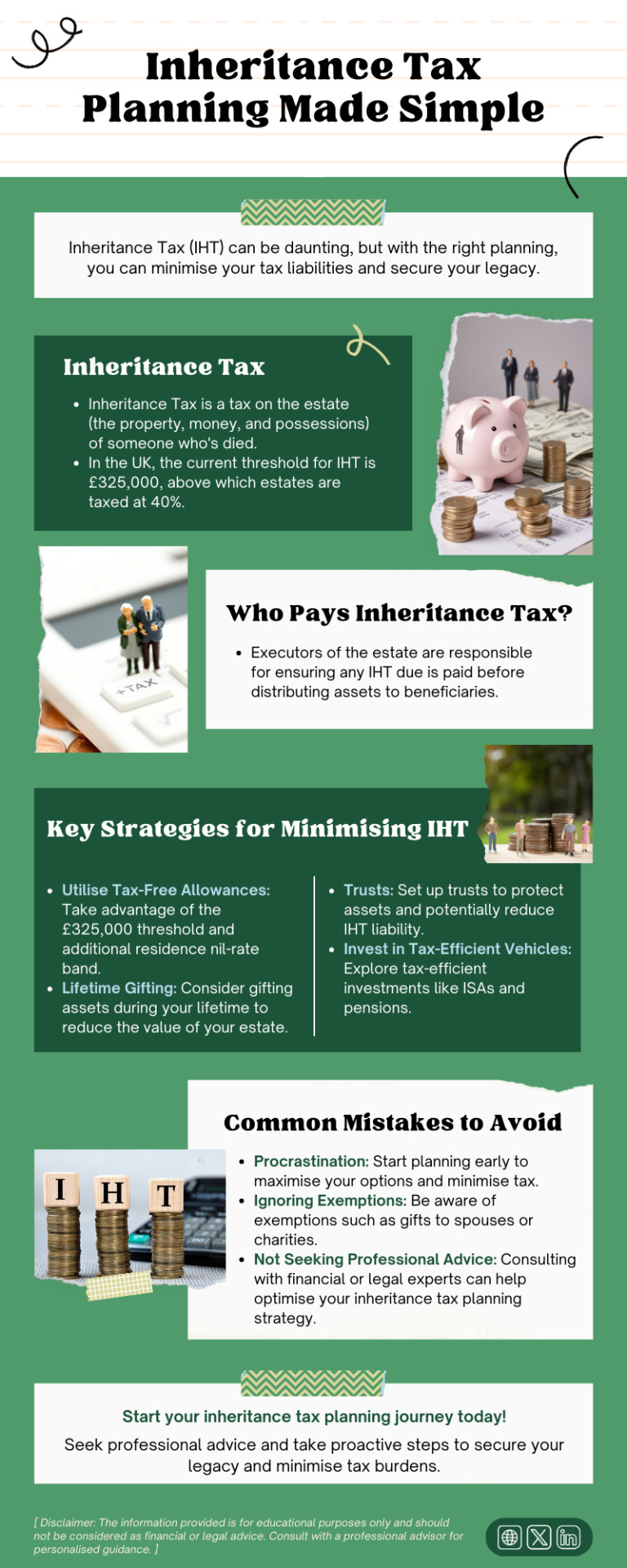

Inheritance Tax (IHT) can be daunting, but with the right planning, you can minimise your tax liabilities and secure your legacy. This infographic provides a simple and straightforward guide to inheritance tax planning.

#Inheritance tax planning#Inheritance tax advice#Inheritance tax advisor#Inheritance tax specialist#inheritance tax advice london#Inheritancetaxplanning

2 notes

·

View notes

Text

youtube

Discover the benefits of using a Family Investment Company (FIC) over a traditional limited company in the UK. Learn how FICs offer tax advantages, estate planning benefits, and greater control over family wealth, making them a strategic choice for family asset management.

#Family Investment Company#inheritance tax planning#tax planning#tax#trust planning#inheritance tax#uk#Youtube

0 notes

Text

Inheritance Tax and What You Can Do To Reduce Your Liability

Inheritance tax (IHT) remains a topic that evokes confusion and concern for many individuals planning their estate. The complexities of the UK’s tax system make obtaining inheritance tax advice a crucial task. This blog describes 3 key strategies to effectively reduce any inheritance tax liability, namely:

Strategic Gifting

Contributing to a Pension and,

Optimising for Business Relief (BR) previously known as Business Property Relief (BPR)

To start off, let’s define Inheritance tax. Inheritance tax is a tax on the estate (the property, investments, and possessions) of someone who has passed away. An estate is not taxed on the first £325,000 known as the nil-rate band (NRB), this increases to £650,000 for a married couple or a couple in a civil partnership.

Furthermore, when passing on a home to direct descendants an estate can claim an additional exempt threshold known as the Residential Nil Rate Band (RNRB) which is a further allowance of £175,000 or £350,000 for a married couple. This means an individual can pass down £500,000 free of inheritance tax on their death, or if married, there’d be no inheritance tax to pay on first death if the beneficial interest passed to the surviving spouse, who could then use a total exempt threshold of £1,000,000, which will not be liable inheritance tax.

Anything above these allowances is taxed at a flat rate of 40%. This means most people in the UK will not face an inheritance tax liability. However, for those that do, there may be several options available to reduce this liability, but expert inheritance tax advice is needed. There are lots of moving parts.

Strategic Gifting

Lifetime gifting is a powerful strategy in IHT planning. By gifting assets during your lifetime, you can significantly reduce the value of your estate over time. There are several exemptions and allowances for gifts, including the:

Annual exemption – £3,000 per year

Small gifts exemption – £250 per person

Gifts in consideration of marriage or civil partnership – £5,000 for a child

These exemptions are too small to make a reasonable dent in a sizeable estate. This is where potential exempt transfers (PETs) and chargeable lifetime transfers (CLTs) come into play, both of which form critical components of inheritance tax advice. PETs refer to gifts made by an individual to another individual (not to a trust or a company) during their lifetime. A PET will only be exempt from inheritance tax if the donor lives for at least seven years after making the gift. There is no limit on how large a PET can be. CLTs refer to gifts made by an individual to a trust during their lifetime, which again, will only be exempt from inheritance tax if the donor survives at least seven years. There is no ‘limit’ per se on how large a CLT can be, however, it is common practice to limit CLTs to £325,000 every 7 years as anything above this would attract a lifetime inheritance tax charge of 20%. A further benefit of settling assets into a trust (CLT) vs. directly gifting to an individual (PET) is 3rd party protection. A gift to an individual will be at risk to divorce settlement claims, creditor claims and general financial mismanagement.

A gift to a trust, provided the trustees are managing the trust well, would provide far greater protection as a trust is a separate legal entity where the individual that the donor wants to benefit can be listed as a beneficiary of the trust, and the trust assets can be controlled by experts and only distributed in accordance with the trust deed and letters of wishes.

Pension Contributions

Pensions can be a potent tool in IHT planning, offering opportunities to pass on wealth outside of one’s estate, thus reducing an inheritance tax liability. A pensions’ primary use case is a vehicle to provide capital and income during retirement. However, if an individual can draw on other assets that are part of the estate first, such as cash, ISAs, and general investment accounts, then withdrawals from the pension can be deferred. In some cases, a pension can be left untouched as because it’s surplus to retirement income and capital needs and in such circumstances the pension becomes a great vehicle for passing on a tax-efficient legacy to chosen beneficiaries. Contributions to a pension attracts upfront tax relief and removes the cash invested from the estate immediately, making them an essential consideration in estate and financial planning.

Business Relief

Business Relief (BR) offers up to 100% relief from inheritance tax on business assets. Qualifying for BPR involves meeting specific criteria, such as holding the assets for at least two years, and ensuring the business is carrying out a trading activity. An investment activity is not considered a trading activity, therefore businesses primarily dealing in property letting and trading securities will not qualify for BPR.

If you own a trading business, it’s likely the shares you own will qualify for BR and the value of the shares will be exempt from inheritance tax. However, if there is any surplus cash on the balance sheet there is a risk this will be treated as an excepted asset. That is an asset that, despite being owned by the business, is not considered necessary for the future success of the business’s trading activities. This can impact the amount of BPR that can be claimed.

People approaching retirement typically look to sell their business. This is great from a cash flow point of view, as one can expect a generous windfall to fund their retirement needs. However, one loses the BR status of the shares sold with cash now sitting in their personal name which is liable to inheritance tax. To mitigate this one can explore deploying the proceeds into investments that qualify for BR such as:

Enterprise Investment Schemes (EIS) - Investments into UK start-ups and early-stage firms that attract very generous tax reliefs (including BR). This tends to be an investment into an unlisted company that in turn invests into crucial infrastructure projects. Provided you’re dealing with a mainstream provided these tend to have lower volatility than investing into an AIM IHT portfolio.

AIM IHT portfolios - Investments into AIM listed shares that qualify for BR.

Navigating the complexities of inheritance tax can seem overwhelming, but with the right inheritance tax advice and IHT planning, it’s possible to significantly reduce the tax burden on your estate. Effective estate planning allows you to pass on more of your wealth to your loved ones, highlighting the importance of seeking professional inheritance tax advice to guide you through the process. Whether it’s making strategic gifts, contributing to a pension scheme, or optimising for business property relief, each strategy offers a pathway to minimising inheritance tax and ensuring more of your estate passes to your children rather than the taxman.

Originally posted by - https://adlestateplanning.co.uk/inheritance-tax-and-what-you-can-do-to-reduce-your-liability/

0 notes

Text

0 notes

Text

What Sets Inheritance Tax Specialists Apart: A Comprehensive Guide

Inheritance Tax Specialists play a crucial role in helping individuals navigate the complexities of inheritance tax laws and regulations. What sets these specialists apart is their in-depth knowledge and expertise in the field, providing comprehensive guidance to clients facing the challenges of estate planning and tax implications. These professionals are well-versed in the intricate details of inheritance tax, staying abreast of the latest legal developments and nuances that can significantly impact an individual's estate.

Inheritance Tax Specialists stand out due to their ability to tailor strategies that align with each client's unique circumstances. Whether it involves minimizing tax liabilities, optimizing estate distribution, or ensuring compliance with ever-evolving tax laws, these specialists employ a personalized approach. Their comprehensive understanding of tax codes enables them to identify opportunities for tax savings and design robust plans that protect the interests of beneficiaries.

Clients benefit from the meticulous attention to detail that Inheritance Tax Specialists bring to the table. From conducting thorough assessments of the estate's assets to considering the family dynamics and individual goals, these specialists leave no stone unturned. This comprehensive approach distinguishes them from general financial advisors, showcasing their specialized focus on the intricacies of inheritance tax planning.

What You Need to Know Before Hiring Inheritance Tax Specialists:

Before embarking on the journey of hiring Inheritance Tax Specialists, individuals must be well-informed about the crucial aspects involved in this decision. Firstly, it is essential to recognize the specific services offered by these specialists, ranging from estate planning to tax optimization. Understanding one's own needs and objectives is paramount to selecting the right professional for the job.

Moreover, individuals should inquire about the qualifications and credentials of potential Inheritance Tax Specialists. Expertise in tax law, financial planning, and estate management are prerequisites, and clients should seek specialists with a proven track record of successful cases. Client testimonials and referrals can provide valuable insights into the specialist's reputation and ability to deliver results.

Transparency in communication is another key factor. Clients should seek Inheritance Tax Specialists who are willing to explain complex concepts in layman's terms, ensuring that clients have a clear understanding of the strategies employed and the potential outcomes. Additionally, a transparent fee structure and ethical business practices contribute to a positive and trustworthy client-specialist relationship.

Overall, individuals should approach the hiring process with a well-defined set of expectations and questions. By doing so, they can make informed decisions that align with their financial goals and aspirations for estate planning and inheritance tax management.

What Makes a Top-notch Inheritance Tax Specialist? Key Traits Unveiled:

Top-notch Inheritance Tax Specialists possess a unique set of traits that distinguish them in the competitive landscape of financial and tax professionals. One key trait is an extensive and up-to-date knowledge of tax laws and regulations. Given the dynamic nature of tax legislation, specialists must stay abreast of changes to provide clients with accurate and timely advice.

Exceptional analytical skills are also a hallmark of top-notch Inheritance Tax Specialists. They must be adept at evaluating complex financial situations, understanding intricate family dynamics, and identifying opportunities for tax optimization. This analytical prowess enables them to craft customized plans that address the specific needs and goals of their clients.

Effective communication is another crucial trait. The ability to convey complex tax concepts in a clear and understandable manner fosters a strong client-specialist relationship. Top-notch specialists take the time to listen to their clients, ensuring a comprehensive understanding of individual circumstances and tailoring their strategies accordingly.

Integrity and ethical conduct are non-negotiable traits for Inheritance Tax Specialists. Clients entrust these professionals with sensitive financial information and rely on their expertise for crucial decisions. Upholding the highest standards of integrity builds trust and credibility, establishing a solid foundation for a long-term partnership.

Lastly, adaptability is a key trait in a field where legislation and financial landscapes are subject to frequent changes. Top-notch Inheritance Tax Specialists embrace innovation, continually updating their methodologies to align with the latest industry trends and technological advancements. This adaptability ensures that clients receive cutting-edge advice and solutions.

In conclusion, a combination of extensive knowledge, analytical skills, effective communication, integrity, and adaptability defines a top-notch Inheritance Tax Specialist. Individuals seeking such professionals should prioritize these traits to ensure they receive the highest quality of service.

What You Should Know About Living Trusts and Inheritance Tax:

Living trusts represent a powerful estate planning tool, and understanding their implications for inheritance tax is crucial for individuals aiming to preserve and pass on their wealth efficiently. One fundamental aspect to grasp is that living trusts are legal entities that hold and manage assets during an individual's lifetime, with a designated successor to manage the trust upon the individual's incapacity or death.

Living trusts, when structured strategically, can provide various benefits related to inheritance tax. One notable advantage is the potential to minimize the probate process, a legal proceeding that validates a will and oversees the distribution of assets. By avoiding probate, the assets held in the living trust may pass to beneficiaries more efficiently, potentially reducing inheritance tax liabilities.

Additionally, living trusts offer flexibility and privacy. Unlike wills, which become public documents during the probate process, living trusts remain private. This confidentiality can be valuable for those who prefer to keep their financial affairs out of the public domain.

However, it is essential to recognize that simply establishing a living trust does not automatically exempt assets from inheritance tax. The effectiveness of a living trust in reducing inheritance tax depends on various factors, including the size of the estate, applicable tax laws, and the specific terms of the trust.

To fully leverage the benefits of living trusts in the context of inheritance tax planning, individuals should work closely with legal and financial professionals. These specialists can help tailor the trust to align with the individual's goals, provide guidance on tax implications, and ensure compliance with relevant laws.

In conclusion, a nuanced understanding of living trusts and their relationship to inheritance tax is vital for individuals seeking comprehensive estate planning. Leveraging the advantages of living trusts requires careful consideration and collaboration with knowledgeable professionals to create a tailored strategy that aligns with individual financial objectives.

What Sets Living Trusts Apart in the Realm of Inheritance Tax Planning:

Living trusts distinguish themselves in the realm of inheritance tax planning through their unique features and benefits. Unlike other estate planning tools, a living trust provides individuals with a high degree of control and flexibility over the distribution of their assets, both during their lifetime and after their passing.

One notable aspect that sets living trusts apart is their ability to bypass the probate process. Probate is a court-supervised procedure that validates a will and oversees the distribution of assets. By placing assets in a living trust, individuals can avoid the delays and costs associated with probate, potentially streamlining the transfer of assets to beneficiaries and minimizing inheritance tax implications.

The revocable nature of living trusts is another distinguishing factor. Unlike irrevocable trusts, which typically offer greater protection but limit control, revocable living trusts allow individuals to make changes to the trust terms during their lifetime. This adaptability ensures that the trust remains aligned with the individual's evolving financial and familial circumstances.

Living trusts also offer continuity in the management of assets. In the event of the trust creator's incapacitation or death, a successor trustee designated in the trust document seamlessly assumes control. This continuity ensures that assets are managed according to the individual's wishes, potentially avoiding disruptions that could impact inheritance tax planning.

0 notes

Text

Discover all you need to know about Wills, Inheritance Tax, Pensions and Investments by attending one of our free public education seminars. Reserve your free place at the seminar of your choice.

#Public Education Seminars#Will Review Seminar#Inheritance Tax Planning#Investment Strategies#Inheritance Tax Seminar#Investments Seminar#Pensions Seminar#Wills & Trusts

0 notes

Text

Here at Fitz Solicitors, we’re proud to offer our services as both corporate and personal solicitors. That being said, to those unfamiliar with UK law,

The major difference between corporate and personal solicitors is that personal solicitors represent individuals.

For example, a personal solicitor will be able to help with issues of family law such as wills, divorces, and child custody. That being said, they’ll also be able to help you in your interactions with businesses.

If you need personal or corporate representation, advice or expertise in the UK, then contact us today at 01753 592 000 for a free initial consultation. To get in touch via email, you can also fill out the contact us form on our website.

0 notes

Text

Inheritance Tax Planning and Strategies | Inheritance-tax.co.uk

Inheritance tax planning and strategies are essential for anyone looking to protect their assets and pass them on to their loved ones. In the UK, inheritance tax is a tax paid by the inheritor on the value of their inheritance, and the more valuable the inheritance, the higher the tax paid. However, there are several ways to reduce or even eliminate inheritance tax, and we have outlined some of them below:

Use Trusts: Trusts are a legal arrangement between you and another person or organization that allows you to give property or money away without having to pay inheritance tax on it. There are several types of inheritance tax planning trusts you can use, including bare trusts, interest in possession trusts, discretionary trusts, accumulation trusts, mixed trusts, trusts for a vulnerable person, and non-resident trusts.

Life Insurance Policy: A life insurance policy can help to pay any inheritance tax due, and placing your policy in a trust can help to ensure that it is not included in your estate for inheritance tax purposes.

Make Pension Plans: Pensions are not included in your estate for inheritance tax purposes, and by making pension plans, you can pay only 20% tax at retirement, as opposed to 40% inheritance tax. You can decide whether to withdraw your pension starting at age 55 or pass it on as an inheritance.

Give Away Gifts: You can give away gifts amounting to £3,000 each tax year, and these gifts will be counted toward your inheritance tax exemption. This can be an effective way to keep your estate tax-free over time.

Donate to Charity: Donating to charity is an excellent way to reduce your inheritance tax liability. Your estate won’t be subject to inheritance tax on anything you leave to charity, and the inheritance tax charged on the remaining part of your estate is reduced from 40% to 36% if you decide to donate at least 10% of your assets to charity.

Alternate Investments Market (AIM): The AIM is a market where you can invest in shares of smaller companies that are not listed on the main stock exchange. By investing in AIM shares that qualify for Business Relief, you can reduce the amount of inheritance tax due on your wealth.

Utilize Business Reliefs: Business reliefs enable you to remove your assets from your estate, relieving you of the burden of inheritance tax. By holding onto your assets for a few years, you can use business reliefs to remove them from your estate.

Overall, it's important to work with a trusted inheritance tax professional for inheritance tax planning advice. They can help you navigate the complex landscape of inheritance tax planning and ensure that your loved ones can pass on their assets without undue financial stress.

For More Information Visit Us: https://inheritance-tax.co.uk/area/inheritance-tax-planning-and-strategies/

#inheritance tax#inheritance#inheritance tax planning#tax planning#tax#property tax#finance#business#planning#inheritance tax specialist#planning and strategies#Estate planning#Paying Inheritance Tax#reduce the inheritance tax#calculate your taxable estate#calculated your taxable estate#inheritance tax advice#inheritance tax advice in London

0 notes

Text

What they don't tell you about losing a parent is that there is so so so so much to do

#speculation nation#my elder sister is gonna be executive of estate (once we get that sorted out bc we couldnt find his WILL)#so i thankfully wont have to deal with as much of the legal stuff#but im still gonna try to help out as much as possible#went through his papers yesterday and set up some preliminary stuff#gonna meet at the funeral home monday to arrange that. tuesday we're going to do some legal stuff for the will establishment#gonna have to take inventory of EVERY. SINGLE. THING. in his house. for tax purposes.#im gonna be inheriting a good amount of things probably. both a blessing and a curse#in that i didnt wanna fucking lose my father for it#but this is the hand we've been dealt and we're dealing with it.#i got excused from my last week of work Thank God so im hanging around longer than originally planned#gonna get my cats today. i fed them enough to last to today but that was when i thought id only be down for 2 days#no work to deal with now. i'll figure it out.#part of me's sad that it really ended just like that. didnt get to properly say goodbye to the store#but at the same time. my dad's death is so much more important. so i'll deal.#it was already gonna be a transitory time. but now it is INTENSELY so.#anyways thats why i havent been around much. i have quite a lot to do.

3 notes

·

View notes

Text

Why Small-Cap Stocks Are a Good Investment for the Long Term [Video]

#InheritanceTax#USAInheritanceTax#EstatePlanning#Inheritance Tax#USA Inheritance Tax#Estate Planning

1 note

·

View note

Text

youtube

Discover the essential steps in selecting an independent trustee for your trust with our comprehensive guide. Learn the key factors to consider, including expertise, reliability, and compatibility with your goals. Make informed decisions for the future of your assets with expert advice in this insightful video.

0 notes

Text

Why Inheritance Tax Planning is Crucial for Your Financial Future in the UK

Inheritance tax planning is not merely a consideration but a necessity for anyone looking to manage their estate effectively. The concept of inheritance tax (IHT) centres around the tax your estate owes upon your death, if the value exceeds certain thresholds set by the government. Understanding the basics of inheritance tax and its implications is crucial, as it directly impacts the legacy you leave behind for your loved ones.

The mechanics of inheritance tax involve several key elements, including thresholds, rates, and available reliefs. Currently, the IHT threshold, also known as the nil-rate band, stands at £325,000 for individuals. This means that estates valued below this figure are exempt from inheritance tax. For estates exceeding this value, the standard IHT rate applied is 40%. However, strategic inheritance tax planning can significantly reduce this liability, leveraging various reliefs such as the spousal exemption and business property relief (BPR). As well as strategic gifting to individuals or trusts during lifetime.

Inheritance tax can affect various types of assets within an estate, from real estate and investments to personal chattels. Real estate, often the most valuable asset individuals own, can significantly increase the overall value of an estate, potentially leading to a sizable inheritance tax bill. Similarly, investments and businesses that do not qualify for BPR (such as companies that own residential property) are also assessable for IHT purposes. Understanding the impact of inheritance tax on these assets is pivotal in inheritance tax & estate planning advice, ensuring beneficiaries receive the maximum possible from their inheritance.

Effective inheritance tax planning involves maximizing your available allowances to minimise the IHT liability. The nil-rate band offers an opportunity to pass on assets up to £325,000 tax-free. For married couples and civil partners, this allowance can be transferred, effectively doubling the nil-rate band to £650,000. Moreover, the residence nil-rate band (RNRB) provides an additional allowance of £175,000 for individuals, and £350,000 for married couples, when passing on a family home to direct descendants. However, the RNRB is tapered down by £1 for every £2 the estate value exceeds £2,000,000, underlining the importance of thorough planning and understanding of these allowances in inheritance tax planning.

For property owners, inheritance tax planning encompasses several innovative strategies to mitigate tax liabilities. A Holdover Gift Trust can offer a structured way to manage and pass on equity in property efficiently, potentially reducing the inheritance tax burden and deferring any capital gains tax liability. Rental income is given up using this strategy though, so section 102 (b)(iii) planning may be a more suitable option if rental income is still required. If an individual, or couple, own a significant amount in property, then structuring the property in a clever alphabet share class company would offer the ideal solution to optimise against inheritance tax. There are several options available to property owners, however, it is critical to seek inheritance tax & estate planning advice as there are different tax implications for each solution that needs to be considered carefully.

At the heart of inheritance tax planning is the creation of a Will, a fundamental document that dictates the distribution of your estate according to your wishes. Without a Will, your estate is subject to the rules of intestacy, which may not align with your intentions. Additionally, Immediate Post-Death Interest (IPDI) trusts represent a sophisticated planning tool, allowing for greater control over how and when assets are distributed, providing a tax-efficient way to manage inheritance.

In conclusion, inheritance tax planning is an indispensable element of financial and estate management. It ensures your assets are passed on to your beneficiaries in the most tax-efficient manner possible. By understanding the nuances of inheritance tax, from thresholds and rates to the impact on different assets, individuals can craft a strategy that aligns with their goals. Maximising allowances, utilising reliefs, strategic gifting, and ensuring the proper legal foundations are in place via a Will and IPDI trusts are all critical steps in safeguarding your estate for future generations. With the right inheritance tax & estate planning advice, you can secure your financial legacy and provide for your loved ones long after you’re gone.

Originally posted by - https://adlestateplanning.co.uk/

0 notes

Text

Get the Best Inheritance Planning in UK

Ensure your legacy is protected with expert inheritance planning in the UK. Our tailored strategies will help minimize inheritance tax and maximize the value of your assets for your loved ones. Visit us now to secure your family's future.

1 note

·

View note

Text

Understanding Inheritance Tax Planning Advice: A Comprehensive Guide

Introduction:

Inheritance tax (IHT) can significantly impact the assets passed down to loved ones after someone passes away. However, with proper planning and advice, individuals can minimize the tax burden on their estate. Let's explore what inheritance tax planning advice entails and how it can benefit you and your family.

How Inheritance Tax Planning Works:

Inheritance tax planning advice involves arranging your finances and assets in a way that minimizes the amount of tax payable on your estate after your death. It aims to maximize the value of the inheritance you leave behind for your beneficiaries.

How to Assess Your Inheritance Tax Liability:

The first step in inheritance tax planning is to assess the value of your estate and determine your potential tax liability. This includes calculating the value of your property, savings, investments, and any other assets you own.

How Inheritance Tax Exemptions and Reliefs Work:

Understanding inheritance tax exemptions and reliefs is essential for effective tax planning. These provisions allow certain assets or transfers to be excluded from the calculation of inheritance tax, thereby reducing the overall tax liability.

How to Utilize Annual Gift Allowances:

One strategy for minimizing inheritance tax is to take advantage of annual gift allowances. These allowances enable you to gift assets or money to your loved ones tax-free up to a certain limit each year.

How Trusts Can Help with Inheritance Planning:

Setting up trusts can be a valuable tool in inheritance tax planning. By transferring assets into a trust, you can remove them from your estate for inheritance tax purposes while still retaining control over how they are managed and distributed.

How to Make Use of Spousal and Charitable Exemptions:

Married couples and civil partners benefit from spousal exemptions, which allow them to pass assets to each other free of inheritance tax. Additionally, charitable donations made in your will or during your lifetime are exempt from inheritance tax.

How to Plan for Business and Agricultural Assets:

Business and agricultural assets may qualify for special reliefs, such as business property relief (BPR) and agricultural property relief (APR), which can reduce or eliminate their inheritance tax liability. Proper planning is crucial to ensure these reliefs are maximized.

How to Structure Life Insurance Policies:

Life insurance policies can play a role in inheritance tax planning by providing funds to cover any tax liabilities without depleting the estate's assets. Setting up policies in trust can ensure that the proceeds are not subject to inheritance tax.

How to Seek Professional Advice:

Given the complexities of inheritance tax planning, seeking professional advice from a qualified financial advisor or estate planning specialist is highly recommended. They can assess your individual circumstances and recommend tailored strategies to minimize your tax liability.

How to Review and Update Your Plan Regularly:

Inheritance tax planning is not a one-time task but an ongoing process. It's essential to review and update your plan regularly to account for changes in your financial situation, tax laws, and personal circumstances.

Conclusion:

Inheritance tax planning advice is vital for anyone concerned about minimizing the tax burden on their estate and maximizing the inheritance they leave behind for their loved ones. By understanding the various strategies and exemptions available and seeking professional advice when needed, individuals can ensure that their assets are passed down as efficiently as possible. Start planning today to secure your family's financial future.

0 notes

Text

Join Wills & Trusts for comprehensive seminars covering wealth management, from Wills and Inheritance Tax to Pensions and Investments. Our free seminars provide valuable insights into estate planning, ensuring you make informed decisions for your financial future. Learn from experts, gain clarity, and confidently plan your legacy.

#financial seminars#wealth management#estate planning#UK inheritance tax#investment advice#pension planning seminars#will preparation advice

0 notes

Text

Inheritance Tax Threshold in UK | Inheritance-tax.co.uk

One of the most important aspects of estate planning is figuring out what the inheritance tax threshold is in the UK. This is a tax that is charged on money and assets that belong to a person and are passed on after they die. Understanding the inheritance tax to pay and IHT thresholds can help you manage your finances and plan for the future, both of which are essential steps in estate planning.

For More Information Visit Us: https://inheritance-tax.co.uk/area/inheritance-tax-threshold/

#inheritance#estate planning#inheritance tax#Inheritance Tax Threshold#Inheritance Tax Threshold in the UK#tax#tax planning

0 notes

Last Seen Blogs

valeriescottt

Belle

girlish-gore

little lady

arielgurevichcine

Ariel Gurevich

deepdreamshoekids

Untitled

largando

Untitled