#Inheritance tax advice

Text

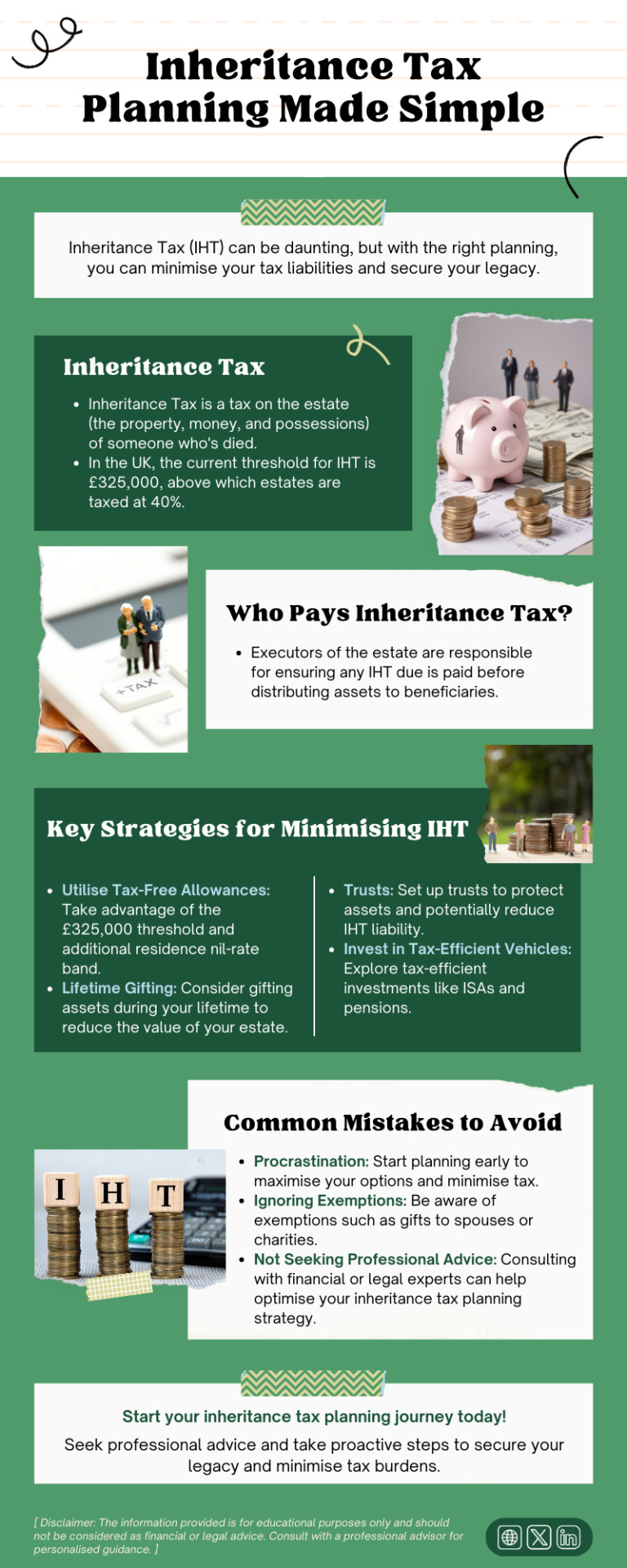

Inheritance Tax (IHT) can be daunting, but with the right planning, you can minimise your tax liabilities and secure your legacy. This infographic provides a simple and straightforward guide to inheritance tax planning.

#Inheritance tax planning#Inheritance tax advice#Inheritance tax advisor#Inheritance tax specialist#inheritance tax advice london#Inheritancetaxplanning

2 notes

·

View notes

Text

Inheritance Tax Planning and Strategies | Inheritance-tax.co.uk

Inheritance tax planning and strategies are essential for anyone looking to protect their assets and pass them on to their loved ones. In the UK, inheritance tax is a tax paid by the inheritor on the value of their inheritance, and the more valuable the inheritance, the higher the tax paid. However, there are several ways to reduce or even eliminate inheritance tax, and we have outlined some of them below:

Use Trusts: Trusts are a legal arrangement between you and another person or organization that allows you to give property or money away without having to pay inheritance tax on it. There are several types of inheritance tax planning trusts you can use, including bare trusts, interest in possession trusts, discretionary trusts, accumulation trusts, mixed trusts, trusts for a vulnerable person, and non-resident trusts.

Life Insurance Policy: A life insurance policy can help to pay any inheritance tax due, and placing your policy in a trust can help to ensure that it is not included in your estate for inheritance tax purposes.

Make Pension Plans: Pensions are not included in your estate for inheritance tax purposes, and by making pension plans, you can pay only 20% tax at retirement, as opposed to 40% inheritance tax. You can decide whether to withdraw your pension starting at age 55 or pass it on as an inheritance.

Give Away Gifts: You can give away gifts amounting to £3,000 each tax year, and these gifts will be counted toward your inheritance tax exemption. This can be an effective way to keep your estate tax-free over time.

Donate to Charity: Donating to charity is an excellent way to reduce your inheritance tax liability. Your estate won’t be subject to inheritance tax on anything you leave to charity, and the inheritance tax charged on the remaining part of your estate is reduced from 40% to 36% if you decide to donate at least 10% of your assets to charity.

Alternate Investments Market (AIM): The AIM is a market where you can invest in shares of smaller companies that are not listed on the main stock exchange. By investing in AIM shares that qualify for Business Relief, you can reduce the amount of inheritance tax due on your wealth.

Utilize Business Reliefs: Business reliefs enable you to remove your assets from your estate, relieving you of the burden of inheritance tax. By holding onto your assets for a few years, you can use business reliefs to remove them from your estate.

Overall, it's important to work with a trusted inheritance tax professional for inheritance tax planning advice. They can help you navigate the complex landscape of inheritance tax planning and ensure that your loved ones can pass on their assets without undue financial stress.

For More Information Visit Us: https://inheritance-tax.co.uk/area/inheritance-tax-planning-and-strategies/

#inheritance tax#inheritance#inheritance tax planning#tax planning#tax#property tax#finance#business#planning#inheritance tax specialist#planning and strategies#Estate planning#Paying Inheritance Tax#reduce the inheritance tax#calculate your taxable estate#calculated your taxable estate#inheritance tax advice#inheritance tax advice in London

0 notes

Text

Understanding the Basics of Trust Fund Inheritance Tax: A Beginner's Guide

Trust fund inheritance tax is a complex topic that many people find confusing. However, understanding the basics of trust fund inheritance tax is essential for effective estate planning. In this beginner's guide, we'll break down the key concepts and provide clarity on this important aspect of wealth transfer.

What Is Trust Fund Inheritance Tax?

Trust fund inheritance tax, also known as estate tax, is a tax imposed on the transfer of assets from one individual to another through a trust fund upon the death of the grantor or beneficiary. The tax is based on the value of the trust assets at the time of transfer and is subject to applicable tax laws and regulations.

Key Components of Trust Fund Inheritance Tax:

Taxable Estate: The taxable estate includes all assets held in trust at the time of the grantor's or beneficiary's death, including real estate, investments, cash, and personal property. Certain deductions and exemptions may apply, depending on the jurisdiction and the size of the estate.

Tax Rates: Inheritance tax rates vary by jurisdiction and are subject to change over time. The tax rates may be progressive, meaning that higher-value estates are subject to higher tax rates. It's essential to consult with tax professionals familiar with local tax laws to understand the applicable rates.

Exemptions and Deductions: Certain exemptions and deductions may apply to reduce the taxable value of the estate for inheritance tax purposes. Common exemptions include the marital deduction, charitable deduction, and annual exclusion gifts. Understanding these provisions can help minimize tax liabilities.

Filing Requirements: Executors or trustees responsible for administering the trust fund may be required to file inheritance tax returns, such as the IHT100 form in the United Kingdom. Compliance with filing requirements is essential to avoid penalties and ensure proper tax reporting.

Tax Planning Strategies: Various tax planning strategies can help minimize trust fund inheritance tax liabilities, such as establishing irrevocable trusts, utilizing annual exclusion gifts, and exploring charitable giving options. Working with inheritance tax planning specialists can help you develop a comprehensive tax strategy tailored to your specific needs.

By understanding the basics of trust fund inheritance tax and implementing effective tax planning strategies, you can navigate the complexities of estate planning with confidence. Take proactive steps to protect your assets and ensure a smooth transfer of wealth to future generations.

0 notes

Text

Inheritance Tax and What You Can Do To Reduce Your Liability

Inheritance tax (IHT) remains a topic that evokes confusion and concern for many individuals planning their estate. The complexities of the UK’s tax system make obtaining inheritance tax advice a crucial task. This blog describes 3 key strategies to effectively reduce any inheritance tax liability, namely:

Strategic Gifting

Contributing to a Pension and,

Optimising for Business Relief (BR) previously known as Business Property Relief (BPR)

To start off, let’s define Inheritance tax. Inheritance tax is a tax on the estate (the property, investments, and possessions) of someone who has passed away. An estate is not taxed on the first £325,000 known as the nil-rate band (NRB), this increases to £650,000 for a married couple or a couple in a civil partnership.

Furthermore, when passing on a home to direct descendants an estate can claim an additional exempt threshold known as the Residential Nil Rate Band (RNRB) which is a further allowance of £175,000 or £350,000 for a married couple. This means an individual can pass down £500,000 free of inheritance tax on their death, or if married, there’d be no inheritance tax to pay on first death if the beneficial interest passed to the surviving spouse, who could then use a total exempt threshold of £1,000,000, which will not be liable inheritance tax.

Anything above these allowances is taxed at a flat rate of 40%. This means most people in the UK will not face an inheritance tax liability. However, for those that do, there may be several options available to reduce this liability, but expert inheritance tax advice is needed. There are lots of moving parts.

Strategic Gifting

Lifetime gifting is a powerful strategy in IHT planning. By gifting assets during your lifetime, you can significantly reduce the value of your estate over time. There are several exemptions and allowances for gifts, including the:

Annual exemption – £3,000 per year

Small gifts exemption – £250 per person

Gifts in consideration of marriage or civil partnership – £5,000 for a child

These exemptions are too small to make a reasonable dent in a sizeable estate. This is where potential exempt transfers (PETs) and chargeable lifetime transfers (CLTs) come into play, both of which form critical components of inheritance tax advice. PETs refer to gifts made by an individual to another individual (not to a trust or a company) during their lifetime. A PET will only be exempt from inheritance tax if the donor lives for at least seven years after making the gift. There is no limit on how large a PET can be. CLTs refer to gifts made by an individual to a trust during their lifetime, which again, will only be exempt from inheritance tax if the donor survives at least seven years. There is no ‘limit’ per se on how large a CLT can be, however, it is common practice to limit CLTs to £325,000 every 7 years as anything above this would attract a lifetime inheritance tax charge of 20%. A further benefit of settling assets into a trust (CLT) vs. directly gifting to an individual (PET) is 3rd party protection. A gift to an individual will be at risk to divorce settlement claims, creditor claims and general financial mismanagement.

A gift to a trust, provided the trustees are managing the trust well, would provide far greater protection as a trust is a separate legal entity where the individual that the donor wants to benefit can be listed as a beneficiary of the trust, and the trust assets can be controlled by experts and only distributed in accordance with the trust deed and letters of wishes.

Pension Contributions

Pensions can be a potent tool in IHT planning, offering opportunities to pass on wealth outside of one’s estate, thus reducing an inheritance tax liability. A pensions’ primary use case is a vehicle to provide capital and income during retirement. However, if an individual can draw on other assets that are part of the estate first, such as cash, ISAs, and general investment accounts, then withdrawals from the pension can be deferred. In some cases, a pension can be left untouched as because it’s surplus to retirement income and capital needs and in such circumstances the pension becomes a great vehicle for passing on a tax-efficient legacy to chosen beneficiaries. Contributions to a pension attracts upfront tax relief and removes the cash invested from the estate immediately, making them an essential consideration in estate and financial planning.

Business Relief

Business Relief (BR) offers up to 100% relief from inheritance tax on business assets. Qualifying for BPR involves meeting specific criteria, such as holding the assets for at least two years, and ensuring the business is carrying out a trading activity. An investment activity is not considered a trading activity, therefore businesses primarily dealing in property letting and trading securities will not qualify for BPR.

If you own a trading business, it’s likely the shares you own will qualify for BR and the value of the shares will be exempt from inheritance tax. However, if there is any surplus cash on the balance sheet there is a risk this will be treated as an excepted asset. That is an asset that, despite being owned by the business, is not considered necessary for the future success of the business’s trading activities. This can impact the amount of BPR that can be claimed.

People approaching retirement typically look to sell their business. This is great from a cash flow point of view, as one can expect a generous windfall to fund their retirement needs. However, one loses the BR status of the shares sold with cash now sitting in their personal name which is liable to inheritance tax. To mitigate this one can explore deploying the proceeds into investments that qualify for BR such as:

Enterprise Investment Schemes (EIS) - Investments into UK start-ups and early-stage firms that attract very generous tax reliefs (including BR). This tends to be an investment into an unlisted company that in turn invests into crucial infrastructure projects. Provided you’re dealing with a mainstream provided these tend to have lower volatility than investing into an AIM IHT portfolio.

AIM IHT portfolios - Investments into AIM listed shares that qualify for BR.

Navigating the complexities of inheritance tax can seem overwhelming, but with the right inheritance tax advice and IHT planning, it’s possible to significantly reduce the tax burden on your estate. Effective estate planning allows you to pass on more of your wealth to your loved ones, highlighting the importance of seeking professional inheritance tax advice to guide you through the process. Whether it’s making strategic gifts, contributing to a pension scheme, or optimising for business property relief, each strategy offers a pathway to minimising inheritance tax and ensuring more of your estate passes to your children rather than the taxman.

Originally posted by - https://adlestateplanning.co.uk/inheritance-tax-and-what-you-can-do-to-reduce-your-liability/

0 notes

Text

Understanding Inheritance Tax Planning Advice: A Comprehensive Guide

Introduction:

Inheritance tax (IHT) can significantly impact the assets passed down to loved ones after someone passes away. However, with proper planning and advice, individuals can minimize the tax burden on their estate. Let's explore what inheritance tax planning advice entails and how it can benefit you and your family.

How Inheritance Tax Planning Works:

Inheritance tax planning advice involves arranging your finances and assets in a way that minimizes the amount of tax payable on your estate after your death. It aims to maximize the value of the inheritance you leave behind for your beneficiaries.

How to Assess Your Inheritance Tax Liability:

The first step in inheritance tax planning is to assess the value of your estate and determine your potential tax liability. This includes calculating the value of your property, savings, investments, and any other assets you own.

How Inheritance Tax Exemptions and Reliefs Work:

Understanding inheritance tax exemptions and reliefs is essential for effective tax planning. These provisions allow certain assets or transfers to be excluded from the calculation of inheritance tax, thereby reducing the overall tax liability.

How to Utilize Annual Gift Allowances:

One strategy for minimizing inheritance tax is to take advantage of annual gift allowances. These allowances enable you to gift assets or money to your loved ones tax-free up to a certain limit each year.

How Trusts Can Help with Inheritance Planning:

Setting up trusts can be a valuable tool in inheritance tax planning. By transferring assets into a trust, you can remove them from your estate for inheritance tax purposes while still retaining control over how they are managed and distributed.

How to Make Use of Spousal and Charitable Exemptions:

Married couples and civil partners benefit from spousal exemptions, which allow them to pass assets to each other free of inheritance tax. Additionally, charitable donations made in your will or during your lifetime are exempt from inheritance tax.

How to Plan for Business and Agricultural Assets:

Business and agricultural assets may qualify for special reliefs, such as business property relief (BPR) and agricultural property relief (APR), which can reduce or eliminate their inheritance tax liability. Proper planning is crucial to ensure these reliefs are maximized.

How to Structure Life Insurance Policies:

Life insurance policies can play a role in inheritance tax planning by providing funds to cover any tax liabilities without depleting the estate's assets. Setting up policies in trust can ensure that the proceeds are not subject to inheritance tax.

How to Seek Professional Advice:

Given the complexities of inheritance tax planning, seeking professional advice from a qualified financial advisor or estate planning specialist is highly recommended. They can assess your individual circumstances and recommend tailored strategies to minimize your tax liability.

How to Review and Update Your Plan Regularly:

Inheritance tax planning is not a one-time task but an ongoing process. It's essential to review and update your plan regularly to account for changes in your financial situation, tax laws, and personal circumstances.

Conclusion:

Inheritance tax planning advice is vital for anyone concerned about minimizing the tax burden on their estate and maximizing the inheritance they leave behind for their loved ones. By understanding the various strategies and exemptions available and seeking professional advice when needed, individuals can ensure that their assets are passed down as efficiently as possible. Start planning today to secure your family's financial future.

0 notes

Text

Join Wills & Trusts for comprehensive seminars covering wealth management, from Wills and Inheritance Tax to Pensions and Investments. Our free seminars provide valuable insights into estate planning, ensuring you make informed decisions for your financial future. Learn from experts, gain clarity, and confidently plan your legacy.

#financial seminars#wealth management#estate planning#UK inheritance tax#investment advice#pension planning seminars#will preparation advice

0 notes

Text

“If you are waiting for an inheritance; you don’t deserve one.”

- M. McGirr

#morgan

0 notes

Text

Learn effective strategies to minimize or eliminate capital gains tax on inherited property. Discover tips and techniques to navigate tax laws, including step-up in basis, qualified small business stock exclusion, and using 1031 exchanges to defer taxes. Safeguard your inheritance and maximize your financial gains. For more information visit our website or read out our blog.

0 notes

Note

hi! apologies if you've been asked this before, but do you have any advice for first time online store owners? i'm thinking about opening one to sell sculptures of my own but i've got no idea where to start, and was wondering if you had any tips to share.

anyways, i love your charming little clay fellows and i hope you have an excellent new year 🤎

i may have been asked it but i can always answer again! tagging this with "clay ask" so you can review past answers

tips:

it's fine to start small and go slow and not optimize everything right away. sculptures are a luxury good and they will usually not immediately start flying off the shelves.

that said: it's nice to track what time you're spending on what. just block it out on google calendar after you're done so you can tot it up at a later time. this tip is super hypocritical but i've done it in the past

i use and like big cartel for my storefront. it doesn't have the fees of etsy or the will sell your stuff twice if people buy it really fast of storenvy. it also doesn't have the discoverability of either, so you'll have to try harder on other social media, but it's a worthwhile tradeoff for me. i don't know anything about shopify and i won't learn

i like pirate ship for shipping labels; it talks directly to big cartel (and a lot of other storefronts!), gets good rates, lets you preview hypothetical packages to check shipping costs, and lets you save package presets. i have a shipping label printer but you should be fine with a regular printer + packing tape.

try to make some reliable size classes of sculpture so you can use a few package settings and not recalculate shipping every time

i try not to buy shipping material from uline because they love trump soooooo soo much. if you have anything local, that's generally a smart call for last minute supply runs, especially because shipping on boxes is spendy. i like upaknship.com for jazzy bubble mailers. i haven't researched their politics but at least they aren't uline

do not put anything particularly delicate in a bubble mailer. i assume you can guess this but a friend once mailed me a plant pot in like. a plastic bag with some shredded paper. so i don't trust what people know about distribution of force in packaging.

you want pressure to be pretty evenly distributed. you don't want anything to be able to twist or bend or snap or rub against itself. you want your packed mailers and boxes to not make any noise when you shake them or to "clunk!" when you drop them on a table from a foot or two up. if you're worried about dropping them that far you have not packed them right.

people will often give you packaging materials if you say you're collecting them

it's nice to have a tape gun... i inherited mine from a childhood neighbor who was a wonderful lesbian

take very careful notes on expenses and income. expect about 25% of $ that comes in to go to taxes (i'm in CA, this might vary)

have a cute logo :) just for fun

these are my THOUGHTS. enjoy!!

#clay ask#long post#this doesnt even get into the nightmare that is product photography <3#oh also if you're doing pricing/profit math paypal and stripe eat about 4% iirc.

94 notes

·

View notes

Text

Si Vis Amari Ama

I. Twin Flames

SERIES MASTERLIST

Pairings: Rooster (Roman Name: Gallus) x Female Reader (Roman Name: Sabina), featuring Hangman (Roman Name: Carnifex) x Phoenix

Summary: A girl whose freedom was stolen to pay her father’s debts. A gladiator enslaved for the entertainment of Rome. A love they never thought possible.

Author’s Note: I hope you guys are excited for Gallus and Sabina’s story! I know that I’m very excited to tell it. Please think of this chapter as a Prologue of sorts, where you’ll get a little glimpse into the histories of our hero and heroine.

Word Count: 2k

Warnings: Slavery in the ancient world, parental death, references to physical abuse, allusions to atrocities committed during a Roman raid, angst.

You could never escape your debts.

There wasn’t much that you remembered about your father, but you could recall those words falling from his lips, clear as a bell. He’d said them so often when you were a little girl that they were permanently ingrained in your brain, rather like the brand that now marred the skin of your left shoulder.

He was right. You couldn’t escape your debts. Even in death, they came to haunt those you left behind, the weight of them falling on shoulders not strong enough to bear the burden.

If only your father had heeded his own advice.

But you were only a child then. At six years old, what could you know of the expenses your father was piling up, the creditors he owed, the tax collectors he evaded?

Perhaps he knew all along. Perhaps he knew he would never escape those debts, never outrun them. And so perhaps Fortuna, the only god he had ever had any use for, had smiled upon him when she sent the fever that robbed him of his life breath.

But why did she have to take Mater, too?

At six years old, you knew nothing. Nothing but pain and loss.

If only you had known that that was just the beginning.

What could you have known of the debts your father owed? Death may have allowed him to escape them, but it didn’t afford you the same luxury.

Rome had been your home your entire life, but when you needed her the most, she turned her back on you, just as your father had done. Just, as it seemed, Fortuna had. The most powerful empire in the world had no pity in her heart for poor orphans, especially not orphans who had inherited a lifetime’s worth of debt, orphans whose fathers’ foolishness had robbed the empire’s coffers.

It was a strange thing, being swept up and sold off, like you were of no more worth than the tapestries and vases that went with you off to market.

Everything was to be sold, you’d overheard the men saying, those frightening men with their faces that looked like the marble you’d seen in the Temple of Jupiter and their eyes as cold as the frigid waters of the Tiber in the dead of winter. If they fetched a good enough price for your childhood home and everything that lay within it, it might just settle your father’s accounts, so they said.

You could never escape your debts.

Or, in this case, you could never escape the debts of others.

Maybe you should have known that moment would come, the moment when your freedom was swallowed up forever. Maybe the signs had been there all along, as the augurs in the temples were so wont to remind people.

Had your parents known all along that this would be your fate when they bestowed your name upon you at birth? Sabina, a name derived from the Sabine women, the very women who had been robbed of their freedom when they were unwillingly carried off by the brutal hands of Rome.

You had never been one for portents and signs, but perhaps this one had been staring you in the face all along.

From Sabina, the freeborn Roman to Sabina, the slave.

How quickly the hands of fate could turn.

Days turned to weeks, and weeks to months, and months to years, until freedom itself seemed only to be a distant memory, like the sound of your mother’s voice and the joy of the games you’d played as a small child.

Your childhood and your freedom had been stolen, stolen to satisfy the debts of the man who was supposed to protect and defend you. And yet, you couldn’t find it in yourself to let the bitterness and resentment build. You’d seen the way it festered in others, the way it gnawed at their bones until nothing remained but a hollow shell. You couldn’t allow that to happen.

Because then what was left of you would be stolen, too, and you really would be nothing.

So long as that tiny flicker of peace remained, then a part of you remained as well, and nobody, not even Rome herself, could take that away from you.

Through every indignity, through every punishment and beating and degradation, you clung to that tiny piece of your heart that you stubbornly refused to let be stained by the world. Through every change of hands, when your body was treated like a commodity to be bought and sold, your very humanity ignored and denied, you retreated to that small place inside, that place where you were still you and always would be.

At night, when you dreamed, it wasn’t of the horrors of your circumstances or the brutality of your days. When you dreamed, it was always of the same pair of arms that held you close and kept you safe. They were strong arms. Scarred arms. Arms that had carried the weight of burdens too heavy to bear, just as you had. You didn’t know who they belonged to—you could never see his face—but you trusted him more than anyone you had ever known. And though you woke each morning alone and cold, you knew with a surety borne only of a deep-seated need that his warmth would find you again when you closed your eyes.

No matter where you went, no matter what household you were sold to, your strong-armed protector followed you in your dreams. And so you weren’t afraid when, after the death of the dominus you’d served for many years, you were sold off to the household of Atticus Cornelius Juventus. For though he was well known to be a lanista, a dealer in the most brutal of gladiators, you felt a strange sense of certainty that you would be safe there.

Your father had taught that you could never escape your debts.

You had learned that you could never escape the fetters of slavery.

But maybe, just maybe, there was still a part of you, no matter how small, that could be free.

Honor and pride were all a man had.

His father had been a great warrior. Honor and pride were the two things he had lived by, the things that had fueled him.

He didn’t really remember his father.

His mother had told him about him when he was small, but he didn’t really remember her either.

He could recall her in flashes—the feel of her arms as she rocked him to sleep, the sound of her voice as she hummed a tune he could no longer remember the words of, the look of pain that flickered in her eyes when she spoke of his father.

But every time he tried to cling to those memories, to solidify her face in his mind’s eye and tattoo it on his heart, they disappeared like the morning mist, taking all the fleeting echoes of home with them.

Home.

Britannia had been home once, but was it any longer?

It was the land his father had died for, the land he’d been cut down defending.

It was the land where his mother had given him life, nurturing him and raising him to be a man of honor and pride, as his father had been.

But he hadn’t been a man, not then.

He hadn’t been a man when the Romans came and raided his village. He hadn’t been a man when they burned the only home he’d ever known, not caring that his mother was still inside. He hadn’t been a man when they raped and pillaged, destroying everything he’d ever held dear in their mad thirst for power and control.

He hadn’t been a man when they rounded him up with the other few survivors and carted him off to the slave markets of Rome, the foul center of their even fouler empire.

He hadn’t been a man then, but he became one.

And as he grew under the watchful eyes of Rome, so did his bitterness. As his body grew stronger, so did his hatred for the people who had made him a slave to their savage empire.

The Romans liked to claim that his people were the savages, yet he had never seen a people as thirsty for blood as the citizens of this hellish kingdom. His father had only ever fought out of devotion to his family and his homeland. These people fought for the pure joy of bloodlust.

He hated them.

He hated them and he hated everything they represented.

But most of all, he hated himself for not being able to break free of them. He hated himself for having to submit to their fetters and chains.

One day, he told himself, he would break free. And so he worked hard every day, not for the benefit of Rome, but for the benefit of himself. He built up his muscles and his stamina, he built up his endurance and his strength. He built himself up so that no one would ever be able to hurt him and get away with it.

But perhaps that had been his mistake.

He built himself up so much that it began to attract talk—and attention.

It started out harmlessly enough. His dominus—how he hated that word—would set up street brawls with drunkards and other slaves and collect bets on the outcome of the fights. He might not have been proud to admit it, but it served as an outlet for the rage he’d been bottling up inside since he was a small boy. Each man he fought was the man who had run his father through with a Roman sword, or the soldier who had laughed as his mother screamed in agony while the flames engulfed her. With each swing of his massive fists, he avenged his parents and his people.

But as the fights became more popular, more people began to take notice. And he was too brash and impulsive, too young and stupid, to realize just how dangerous that was.

He would never forget the day that Atticus Cornelius Juventus came to watch him fight, the rich man’s dark, beady eyes never blinking as he watched him destroy his opponents, beating them to within an inch of their lives. At the end of the bout, when he was bloodied and panting and soaked with sweat, the man even smiled, one corner of his cunning mouth quirking up into a satisfied grin.

“I’ll take him, Linus,” he had said, throwing a hefty bag of clinking coins in the direction of his smirking dominus.

His former dominus.

From that day forward, he became the property of Atticus Cornelius Juventus and he knew that he would never taste freedom again.

He had built himself up so that they could never destroy him, and he ended up destroying himself.

From street brawls with drunkards, to armed combat in local arenas, to the public spectacles of the Colosseum, the years passed and his fame grew. “The Barbarian from Britannia” was what they loved to call him. He was their champion, their hero, their undefeated victor. They loved him, worshiped him, adored the ground he walked on.

He hated them.

He hated their cheers, he hated the way they fawned over him, he hated the way they had forced their sword into his hand, the same sword that had slaughtered his father and his people.

He no longer cared whether he lived or died. In fact, he rather wished that death would finally come to claim him one of these days.

What did he have to live for?

It certainly wasn’t the hope of freedom. He no longer hoped for that. He no longer hoped for anything. His life was not his own, and it never had been.

There were moments when he was by himself late at night, brief and fleeting moments when he felt himself reaching out for something—or someone. It was a desperate ache, a longing deep inside his chest for something he didn’t quite understand.

It didn’t matter. He would root that longing out of his heart, just as he had rooted out every other feeling beyond bitterness and hatred.

Honor and pride were all a man had, and his had been trampled into the dust.

He would never return to his homeland.

He would never escape the blood and sand of the Colosseum.

He would never again be free.

#bradley rooster bradshaw#rooster x reader#x reader#x female reader#top gun#top gun: maverick#miles teller#hannix#hangman x phoenix#Ancient Rome AU#si vis amari ama ⚔️

253 notes

·

View notes

Text

2 monopoly 2 au: driftmark edition

viserys, in his usual well meaning naïveté, proposes a family game night.

larys is the one who suggests monopoly because he loves watching the world burn (literally). he does not actually participate, though, instead acting as the bank and giving viserys financial advice so horrid the poor man ends up completely insolvent after ten minutes.

rhaenyra makes a bunch of shitty investments, somehow profits enough to not completely lose and gives larys the finger every time her event cards require her to pay even a cent. larys’ tax system, that some hundred years later will be adopted by one tyrion lannister and spectacularly blow up in his face, is not acknowledged by the realm’s delight, which kind of goes without saying.

daemon owns all brown, pink and light blue properties which end up making him a fortune. he, too, refuses to pay taxes. seated between rhaenyra and viserys, every once in a while, whenever no one is looking, he reaches across the table and steals their money. alicent is the only one who sees this and is subsequently gaslit into believing she’s going insane by him when he brings it up. rhaenyra refuses to count her money out of principle.

rhaenys is in a spectacularly bad mood and the one with her dragon in the closest proximity, which is why no one even bothers to ask her to pay when she lands on someone’s property. of course she doesn’t pay taxes.

rhaena and baela have teamed up, own all orange properties and are specifically hell bent on bankrupting aegon. they’re the only ones that rhaenys actually pays. they, too, evade taxes.

jacaerys announces insolvency after ten minutes and proposes to lucerys, who accepts. this does not better their financial situation whatsoever, considering they have inherited their mother’s financial incompetence but not her stupid luck with dice. at least they’re smart enough not to pay taxes.

alicent has two dollars to her name, is the only one who respects the tax system and is royally pissed off when she finds out that the only reason that rhaenyra has more money than her is her rampant tax evasion (“where is duty? where is sacrifice?”). after a ten minute tangent about how all she has ever done is what was expected of her and snide comments about the parentage of absolutely EVERYONE in the room with her, she is reminded by rhaenys that, considering larys’ utter leniency regarding the tax system, she could just… you know… stop paying? this causes alicent to excuse herself to the kitchen and scream for five minutes straight.

two minutes into the game, daeron is jailed and never released again.

aegon is so heavily indebted that he starts offering sexual favours in exchange for loan forgiveness. the tone in which larys says “i’ll hold you to that, sweet prince!” makes rhaena audibly retch.

helaena makes everyone’s lives hell with double hotels on all her properties. no one knows where she gets all that money from. halfway through the game, she reverts to only speaking latin. her voice has dropped several octaves. lightning strikes whenever she rolls the dice. alicent, back from her screaming break, starts quietly exorcising her under the table. everyone is relieved when she eventually declares something cryptic in what may just have been german and leaves, only to return half an hour later covered in primordial goo. she walks straight past everyone to her room and for once, the entirety of house targaryen sits in silent agreement: they will never speak of this again.

aemond fights lucerys, jacaerys, baela and rhaena tooth and nail over every single one of their properties while hurling every insult he can think of at them.

about two hours in, rhaenyra and daemon barter over pennsylvania avenue in a manner so intense it makes them both horny, and they excuse themselves to the guest room. the noises that follow permanently scar alicent and turn larys on so much he doesn’t notice aegon swiping twenty dollars from the bank, which he rolls into a joint as he disappears from the table.

rhaenys sacks both rhaenyra’s and daemon’s property and adds it to that of helaena, which she has already taken for herself twenty minutes ago, effectively making her the westerosi equivalent to jeff bezos.

aemond manages to buy the boardwalk and calls baela several slurs, none of them accurate to her gender identity, sexuality or mental wellbeing, which leads to lucerys, jacaerys and rhaena chasing him with both proverbial and literal pitchforks and torches, god knows where they found those, as he makes a break for it. criston cole, who has been lounging on alicent’s handpicked ikea loveseat, model söderhamn if you’re wondering, puts down the hurling match he’s been intently watching for the last two hours and follows them.

this turns out to be an excellent call, because only ten minutes later, a hysterically sobbing aemond is missing an eye, god knows how a very much seven year old lucerys has manged to enucleate him, and alicent, actually violently swearing for the first time in her fourtysomething years of life, drives him to the emergency room.

this leaves rhaenys and viserys at the table. “just like old times, huh?” viserys says, smiling. “cut the shit, bitch.” rhaenys retaliates as she swipes alicent’s remaining funds, then grabs the bank carton, and finally relieves viserys of his money and properties as well as his crown, declaring herself the winner.

#hotd#house of the dragon#fire and blood#rhaenyra targaryen#alicent hightower#viserys targaryen#daemon targaryen#lucerys velaryon#jacaerys velaryon#rhaena targaryen#baela targaryen#aegon ii targaryen#helaena targaryen#aemond targaryen#daeron targaryen#larys strong

48 notes

·

View notes

Note

Dear Resident Rohan Expert:

I'm not sure if you have given any thought to this, but I could sure use your help! What are your thoughts about how Rohan's government is structured, specifically the King's council at Edoras? I have assumed the King rules with full authority, but with the help of a council of advisors... but how do you think those advisors are selected? How many? Are they military men? Nobility? Elected? Appointed? Are they inherited titles?

Any of your thoughts would be appreciated since your grasp of Rohirrim culture is sounder than of anyone around! Thank you in advance! 😊

Ooh, this comes very close to giving me the chance to answer the question, “What was Éomer’s tax policy?” 😂 (Which, as a public policy major, is something I wouldn’t mind knowing about!) I have thought about Rohan’s government, and I hope you find my answer useful or at least interesting—it’s always my goal to live up to the praise you give me and to make my Rohan even close to being as well contextualized as your Mirkwood universe!!!

I’ve tried to keep a general structure for Rohan’s government in my mind that is at least quasi-related to the way that Anglo Saxon lands were governed, since they were Tolkien’s model. The big deviations are: 1) there is no mixing of religion and government like the Anglo Saxons did, since Rohan has no organized religion; and 2) I like to keep my Rohan government a little more democratic in the sense that everything isn’t based solely on nobility, inheritance or wealth. That’s partly because I don’t vibe with that approach, but also I feel like Tolkien gave us hints that the Rohirrim are pretty laid back about stuff like that anyway (like, Théoden is shockingly casual about the whole issue of royal succession, and he’s totally willing to take advice from guys like Háma or Wídfara even though we have no reason to believe they’re particularly wealthy or elite nobles).

So, the king has ultimate authority in Rohan and, starting with Éomer, that power is equally shared with the queen (I have to believe that he really took in what he learned about Éowyn’s experience in Rohan and would want things to change, starting with his own wife!). The monarchs exercise their authority with the help of a council. That council is comprised of: 1) the advisors of the royal household, a small group that is at Meduseld with the king and queen every day; and 2) the officers of the court, a bigger group who are out in the towns and villages as representatives of the crown. The entire council meets formally a few times a year to discuss and make recommendations on significant issues, though the king and queen can call them more often if needed. And when the officers of the court are back at their homes in between formal council meetings, the advisors of the royal household give the day-to-day advice or handle emergencies that crop up.

The royal household advisors are chosen by the king/queen and would generally include trusted family members as well as others who have distinguished themselves as being particularly skilled in relevant subjects. There would normally be 7 of these, with each specializing in a particular area: defense, diplomacy, justice/law, treasury, trade, infrastructure (roads, bridges, etc.) and public welfare (care of orphans, famine relief, what passed for public health in those days). But there could be more or less depending on the priorities of the particular king/queen, and the individual advisors might have their own staffs to help them.

The royal household advisors would often be members of the most prominent families in Rohan, if only because those are the people with the most access to the education and experience needed to become good at these things, but anyone can be chosen. And younger people of any background who are identified as being particularly bright and with a lot of potential might be referred to extra schooling/study with the idea of training them to be advisors, or work for them, in the future. (In my fics, this is how Gríma ended up in an advisor role – he failed out of éored training, but the brilliance of his mind was recognized, he was given the additional education to become an advisor on diplomatic affairs, got too close to Isengard and everything went to hell.) (It’s a good process, even though the one example I’ve just given is one where things did not work out well!)

The officers of the court who are spread throughout the land are chosen by their communities, though the king/queen can refuse to seat one that they don’t like or trust.* The king and queen decide how many officers there are, adding or subtracting as the population shifts, but there are generally 5 each from the West-mark and the East-mark and 3 from Edoras and its surrounding lands. These officers not only sit on the council that helps the king/queen set law and policy, but they’re also the first line administrators who see those policies carried out around the country (so, they hire the tax collectors in Dunharrow or the work crews that build the new road between Aldburg and Grimslade or whatever). That makes them kind of the face of the crown in most parts of Rohan where regular people are never going to see the king or queen (or, at least, not often). They can also draw on the expertise and knowledge of the royal household advisors as needed when carrying out royal policy.

Thank you again for the opportunity to write something that’s probably far too long about a niche topic that I find very interesting!! If anyone has their own ideas and thoughts—either complementary or conflicting—I would love to hear them. More Rohan for everyone! 👑🐎🗡️♥️

*A king/queen should really try to avoid doing this, especially if the person in question is really popular in their community and has any kind of independent power base. Don’t get me started on how Helm Hammerhand really fucked this up with a member of his own council and got a war started as a result.

#asks#answered asks#lotr#lord of the rings#rohan#governments of middle earth#bless you for giving me a chance to blather about stuff that I like!!!

28 notes

·

View notes

Text

The impact of Inheritance Tax on small business owners | Inheritance-tax.co.uk

As a small business owner, you have spent years building your company from the ground up. You have invested countless hours and money into your business, and it has become a significant part of your life. However, have you considered the impact of inheritance tax on your business? Inheritance tax is a tax levied on an estate after a person's death, and it can have a significant impact on small business owners. In this post, we will explore the impact of inheritance tax on small business owners and provide advice on how to navigate this tax.

Inheritance tax can be a significant burden on small business owners.

Small business owners are often cash-poor, and their businesses represent a significant portion of their wealth. Inheritance tax can be a significant burden on small business owners, as it requires the payment of tax on the value of the business at the time of the owner's death. This tax can be especially challenging to pay for small business owners who have little liquidity, and it can force the sale of the business to cover the tax bill. This can be a devastating outcome for small business owners who have spent years building their company and do not want to see it sold.

Planning ahead can mitigate the impact of inheritance tax on small business owners.

Planning ahead is crucial for small business owners who want to mitigate the impact of inheritance tax on their business. There are several strategies that small business owners can use to reduce their inheritance tax liability. For example, small business owners can transfer ownership of their business to family members or employees before their death, reducing the value of their estate and the amount of inheritance tax due. Additionally, small business owners can use trusts and other estate planning tools to reduce their inheritance tax liability.

Professional inheritance tax advice can help small business owners navigate the tax system.

Inheritance tax is a complex tax, and small business owners may benefit from professional inheritance tax advice UK. An inheritance tax specialist can provide small business owners with advice on how to structure their estate to reduce their tax liability. Additionally, an inheritance tax specialist can provide guidance on the use of trusts and other estate planning tools to mitigate the impact of inheritance tax on small business owners.

Business property relief can be a valuable tax break for small business owners.

Business property relief is a valuable tax break for small business owners, as it can provide relief from inheritance tax on the value of qualifying business assets. Qualifying business assets include shares in unlisted companies, and business property such as buildings and land used for the purposes of the business. Small business owners should be aware of the rules surrounding business property relief and ensure that their business qualifies for the relief.

The impact of inheritance tax on small business owners can be mitigated with life insurance.

Life insurance can be a valuable tool for small business owners looking to mitigate the impact of inheritance tax on their business. Small business owners can take out life insurance policies that pay out on their death, providing the funds necessary to pay their inheritance tax bill without having to sell their business. This can provide small business owners with peace of mind knowing that their business will not have to be sold to cover the tax bill.

Conclusion

In conclusion, inheritance tax can have a significant impact on small business owners, but there are strategies that can be used to mitigate its impact. Planning ahead, seeking professional inheritance tax advice UK, and utilizing tax breaks such as business property relief can help small business owners reduce their tax liability. Additionally, life insurance can be a valuable tool for small business owners looking to ensure that their business is not sold to cover the tax bill. By taking proactive steps to address the impact of inheritance tax on their business, small business owners can ensure that their hard work and investment are protected for future generations.

#Inheritance tax#inheritance tax advice UK#inheritance tax specialist#tax planning#tax#property tax#finance#inheritance

1 note

·

View note

Text

So I’ve been thinking about my female Caranthir agenda, specifically in relation to the thing about lembas being the queen’s purview and the only thing the elves seem to have rigid gender roles over. Lembas is indicated to be pretty important but the Noldor in Beleriand didn’t have a queen so who would be in charge of the distribution of it?

If Caranthir was a woman and Lalwen and Findis did not exist (like in the Silm version of canon) I think there’s a real case to be made that the position would go to her because, as the Feanorians (mainly Celegorm and Curufin because they’re petty as fuck) insist, Maedhros abdicated the position of High King; nothing was ever said about their other titles and as the eldest grandaughter of Finwë Caranthir is the highest ranking nís of the Noldor and in the absence of Fingolfin’s wife the essential roles of a queen are her right.

It’s not as if there are too many other candidates either, I can’t see Aredhel or Galadriel, since she’d be off in Doriath and very much not looking to be involved further in Noldorin politics, fighting for the position (again, how are there so few women in this family? How does that even happen? There are fourteen grandchildren of Finwë. I’d need to make all the Arafinweans and Nolofinweans women just to make it equal.) so Fingolfin doesn’t really have any alternatives to suggest.

So they end up in a situation where the High King of the Noldor is a Nolofinwean but there is now a precedent for the position of Massánië (the Quenya for the queen’s role as breadgiver) of the Noldor to stay in the eldest line of Finwë’s sons when the High King doesn’t have a wife, meaning that suddenly female descendants of Feanor are technically higher ranking than any of the male ones. No Feanorian High Queen can inherit the crown of the Noldor because that would be counted as the same as the Kingship covered in the abdication but the position of Massánië has become isolated from that of the queen and in a technical sense ranks just below a Crown Prince or Princess.

This isn’t of particular importance to Caranthir but you know she is exploiting the complete fucking life out of having all her kin dependent on her for yet another valuable resource, as if all the trade routes weren’t enough. The taxes on lembas going to Dorothion are extortionate. In his letters to his cousins Maedhros responds that he cannot interfere with his sister’s independent role and it is entire her own initiative to do what she wishes in this particular area.

In his letters to Caranthir he is giving her very useful advice on how to use this tactically to best strengthen their factions’ economy based on his knowledge of political situations and sometimes when someone (often Celegorm) pisses him off. This makes the top three of schemes Maedhros and Caranthir are running through their encrypted letters to each other that though unbeknownst to the rest of Beleriand have ridiculously wide reaching effects on the entire economic and geopolitical landscape. They make a scarily good (if slightly less malicious than C and C’s) team.

(Also down the line this could be another title for a genderqueer Elrond to be playing hot potato with because they can’t even use being adopted by the Feanorians that abdicated as an excuse here and it in fact only bolsters their pre-existing claim as Idril’s descendant. If they end up accepting it they and Gil Galad would seize the opportunity to be more ambiguous about their relationship than they already are as half their own court doesn’t even know if Elrond has accepted the position based on lineage or whether they’re now Gil Galad’s consort.

The foreign diplomats and future historians have no idea what was going on. Gil Galad does not help matters by using every opportunity to refer to Elrond, maybe teasingly, maybe not, as his queen.)

#silmarillion#tolkien#caranthir#meta#genderbending#rule 63#lembas#maedhros#female caranthir#Elf politics#Fingolfin#elrond peredhel#gil galad/elrond#ereinion gil galad#I’m oddly fixated on this#I might include it in a fic at some point

26 notes

·

View notes

Text

Why Inheritance Tax Planning is Crucial for Your Financial Future in the UK

Inheritance tax planning is not merely a consideration but a necessity for anyone looking to manage their estate effectively. The concept of inheritance tax (IHT) centres around the tax your estate owes upon your death, if the value exceeds certain thresholds set by the government. Understanding the basics of inheritance tax and its implications is crucial, as it directly impacts the legacy you leave behind for your loved ones.

The mechanics of inheritance tax involve several key elements, including thresholds, rates, and available reliefs. Currently, the IHT threshold, also known as the nil-rate band, stands at £325,000 for individuals. This means that estates valued below this figure are exempt from inheritance tax. For estates exceeding this value, the standard IHT rate applied is 40%. However, strategic inheritance tax planning can significantly reduce this liability, leveraging various reliefs such as the spousal exemption and business property relief (BPR). As well as strategic gifting to individuals or trusts during lifetime.

Inheritance tax can affect various types of assets within an estate, from real estate and investments to personal chattels. Real estate, often the most valuable asset individuals own, can significantly increase the overall value of an estate, potentially leading to a sizable inheritance tax bill. Similarly, investments and businesses that do not qualify for BPR (such as companies that own residential property) are also assessable for IHT purposes. Understanding the impact of inheritance tax on these assets is pivotal in inheritance tax & estate planning advice, ensuring beneficiaries receive the maximum possible from their inheritance.

Effective inheritance tax planning involves maximizing your available allowances to minimise the IHT liability. The nil-rate band offers an opportunity to pass on assets up to £325,000 tax-free. For married couples and civil partners, this allowance can be transferred, effectively doubling the nil-rate band to £650,000. Moreover, the residence nil-rate band (RNRB) provides an additional allowance of £175,000 for individuals, and £350,000 for married couples, when passing on a family home to direct descendants. However, the RNRB is tapered down by £1 for every £2 the estate value exceeds £2,000,000, underlining the importance of thorough planning and understanding of these allowances in inheritance tax planning.

For property owners, inheritance tax planning encompasses several innovative strategies to mitigate tax liabilities. A Holdover Gift Trust can offer a structured way to manage and pass on equity in property efficiently, potentially reducing the inheritance tax burden and deferring any capital gains tax liability. Rental income is given up using this strategy though, so section 102 (b)(iii) planning may be a more suitable option if rental income is still required. If an individual, or couple, own a significant amount in property, then structuring the property in a clever alphabet share class company would offer the ideal solution to optimise against inheritance tax. There are several options available to property owners, however, it is critical to seek inheritance tax & estate planning advice as there are different tax implications for each solution that needs to be considered carefully.

At the heart of inheritance tax planning is the creation of a Will, a fundamental document that dictates the distribution of your estate according to your wishes. Without a Will, your estate is subject to the rules of intestacy, which may not align with your intentions. Additionally, Immediate Post-Death Interest (IPDI) trusts represent a sophisticated planning tool, allowing for greater control over how and when assets are distributed, providing a tax-efficient way to manage inheritance.

In conclusion, inheritance tax planning is an indispensable element of financial and estate management. It ensures your assets are passed on to your beneficiaries in the most tax-efficient manner possible. By understanding the nuances of inheritance tax, from thresholds and rates to the impact on different assets, individuals can craft a strategy that aligns with their goals. Maximising allowances, utilising reliefs, strategic gifting, and ensuring the proper legal foundations are in place via a Will and IPDI trusts are all critical steps in safeguarding your estate for future generations. With the right inheritance tax & estate planning advice, you can secure your financial legacy and provide for your loved ones long after you’re gone.

Originally posted by - https://adlestateplanning.co.uk/

0 notes

Text

[“Many landlords were part-timers: machinists or preachers or police officers who came to own property almost by accident (through inheritance, say) and saw real estate as a side gig. But the last forty years had witnessed the professionalization of property management. Since 1970, the number of people primarily employed as property managers had more than quadrupled. As more landlords began buying more property and thinking of themselves primarily as landlords (instead of people who happened to own the unit downstairs), professional associations proliferated, and with them support services, accreditations, training materials, and financial instruments. According to the Library of Congress, only three books offering apartment-management advice were published between 1951 and 1975. Between 1976 and 2014, the number rose to 215. Even if most landlords in a given city did not consider themselves “professionals,” housing had become a business.

The evening’s speaker was Ken Shields, from the Self Storage Brokers of America. After selling his insurance company, Shields had begun looking for a way to get into real estate. He started out with rooming houses, which meant he started out renting mainly to poor single men. “Very nice cash flow. But I no longer have them.” The room chuckled. “I made some good money, and I mean, I love to get money, but I’m still just as happy not running around and dealing with some of these dregs of society who live in rooming houses.”Sherrena, who owned a couple of rooming houses, laughed along with the room. Then Shields found self-storage. “It’s got the residual incomes of an apartment building, but,” he lowered his voice, squinted, “you don’t have the people. You just got their stuff!…This is the sweetest spot in the whole American economy. A receptacle for an enormous cascade of money.”

The landlords loved Ken Shields, even if he did live in Illinois. When he finished his speech, the room broke into applause. The RING president, a mustached man with a full pouch for a stomach, stood up clapping. When there wasn’t a speaker, he often organized round robins. One such evening, a woman from Lead and Asbestos Information Center, Inc., had started off by announcing, “There is money to be made on lead,” to a room of landlords who more often lost money trying to abate it. One landlord asked whether he would have to report the presence of asbestos to the city or the tenants if he tested for it. “No, you don’t,” the woman had said.

The conversation moved on and someone else had asked about garnishing wages. A lawyer informed the room that a landlord was allowed to garnish a tenant’s bank account and up to 20 percent of his or her income, but the last $1,000 was exempt. And welfare recipients were off-limits.

“How about intercepting their tax refund?” Sherrena had asked.

The lawyer looked a bit stunned. “Noooo, only the government can do that.”

Sherrena already knew that. She had looked into it before. Her question wasn’t a question; it was a message to Eric, Mark, Kathy, and everyone else in the room that she would do almost anything to get the rent. Many white landlords knew money could be made in the inner city, where property was cheap, but the thought of collecting payments on the North Side, let alone passing out eviction notices, made them nervous. Sherrena wanted them to know that she could help.”]

matthew desmond, from evicted: poverty and profit in the american city, 2016

145 notes

·

View notes

Last Seen Blogs

romania-huntz

things aren't always as they seem.

norma12

Untitled

quininee

Putri Amalia✨

romanticoffee

Untitled

quadrantmodelquotes

Quadrant Model Quotes from 2013 Lectures