#InternetBanking

Text

How to Build a Digital Banking Platform?

Over the last two years, your workplace may have undergone significant digitization. But have your banking services kept pace? For the 78% of Americans who prefer banking online, navigating financial tasks through various apps has become the norm.

Financial giants are already adapting to this change, with a 2022 survey revealing that over half of consumers use their bank or credit union’s mobile app for banking activities. However, creating these digital platforms is challenging without the necessary infrastructure for data collection, integration with other software, secure communication, and fraud detection.

To mitigate risks and delays, many banks utilize Digital Banking Platforms, ensuring a smooth transition for employees and customers to online services across diverse channels and market sectors. But how do you choose the right Online banking solutions for your needs? This article will guide you through everything you need to consider.

What Is a Digital Banking Platform?

Digital banking platforms are utilized by banks, credit unions, and financial institutions to offer customers online access for carrying out conventional banking tasks and operations. With the appropriate partner, most banking services can be transformed into digital formats. Different Online banking solutions cater to various needs; some focus on loan and wealth management, while others are tailored towards everyday banking activities, such as transferring funds, managing savings and checking accounts, and tracking transactions.

Additionally, these platforms can enhance a bank's core systems with new features through API integrations, automation, and the use of no-code or low-code tools for developing pages and functionalities. Financial institutions of all sizes leverage these platforms, from smaller banks aiming to attract more customers, to large international banks streamlining processes into automated workflows.

Features of Digital Banking Platforms

Digital banking platforms provide financial institutions with a suite of comprehensive features. Based on specific needs, you can choose the financial products and services that best serve your customers.

These platforms offer the flexibility for banks to create specialized services through API integrations with fintech partners, allowing customers to expand their online and mobile applications with additional functionalities beyond what the platform originally offers.

Key features commonly found in Online banking solutions include:

Opening and managing financial accounts

Dashboards for financial management

Processes for online applications and approvals

Security measures and fraud prevention

Conducting money transfers

Facilitating bill payments

Providing budgeting tools

Sending alerts and notifications

Enabling third-party integrations

Offering options for customizable branding

Best Digital Banking Platforms

Selecting the best digital banking platform is crucial for financial institutions aiming to meet the evolving demands of modern banking. The ideal platform combines seamless user experience with robust security features, extensive financial management tools, and flexible integration capabilities. Here are some leading Digital payment platforms known for their comprehensive functionalities and adaptability:

nCino Bank Operating System

The nCino Bank Operating System is a comprehensive digital solution adopted by financial institutions to enhance the digital handling of loans and deposits for their customers. It is equipped with a suite of tools designed to streamline loan processing times and improve efficiency in managing customer relationships, content, workflows, and reporting. Positioning itself as an all-encompassing platform, nCino addresses a wide range of banking requirements, including asset finance and leasing, customer engagement, treasury management, and portfolio analysis, offering an end-to-end solution for modern banking needs.

Finacle Digital Engagement Suite

The Finacle Digital Engagement Suite caters to banks seeking to offer their customers comprehensive support across multiple channels, including customer onboarding, engagement, product sales, and the delivery of ongoing banking services. This platform is designed to enhance the banking experience for customers, employees, and external partners alike, featuring a range of solutions that span core banking functionalities, trade finance, liquidity management, blockchain-based payments, and beyond.

Finflux

Finflux is a cloud-based platform dedicated to lending services, supporting more than four million borrowers with a variety of needs such as loan management, origination, debt collection, and liability management, among others. Its extensive suite of API integrations allows financial institutions to effortlessly gather and analyze data from diverse sources, enabling the customization of digital experiences for customers across various loan categories.

Alkami Platform

The Alkami Platform offers a comprehensive digital banking solution designed to assist banks and credit unions in attracting and maintaining relationships with both retail and business clientele. It has successfully introduced innovative digital experiences for major credit unions, including the Idaho Central Credit Union, which boasts over 400,000 members. This platform provides lenders with a user-friendly mobile application experience, enabling users to manage payments, open new accounts, and interact virtually with customer support representatives with ease.

NCR Digital Insight

NCR Digital Insight offers an all-encompassing platform for digital transformation initiatives, encompassing a wide range of applications from digital banking to point-of-sale systems and the virtualization of stores. Its technology is utilized by banks and credit unions to integrate various banking services — such as consumer, retail, or business banking — into a unified application accessible on both desktop and mobile devices.

When it comes to choosing the best digital banking platform, the Market Intelligence Report by Quadrant Knowledge Solutions proves invaluable. This report offers deep insights into market trends, competitor analysis, and emerging technologies, assisting institutions in making informed decisions. It highlights the importance of adopting platforms with low-code application development capabilities, given their significant market share and growth potential. According to the report, the "Market Share: Digital banking platforms, 2022, Worldwide" indicates a robust and expanding market, while the "Market Forecast: Digital banking platforms, 2022-2027, Worldwide" predicts substantial growth over the next five years. This growth underscores the shift towards platforms that enable rapid development and deployment of digital banking services, making it easier for institutions to adapt to market changes and customer needs. By leveraging such market intelligence, financial institutions can strategically choose a Digital payment platform that not only meets their current requirements but also positions them for future growth and innovation.

Conclusion

This guide is the culmination of our extensive experience in crafting mobile banking solutions. As highlighted in the article, initiating with thorough research and setting clear strategic objectives for your business are crucial first steps. These foundational actions guarantee that your approach to creating a digital banking platform is aligned with your business goals. Once you've established a comprehensive overview and a blueprint for the forthcoming application, collaboration with DevOps, DevSecOps, and other relevant teams can commence. The development process is intricate and often lengthy. Therefore, we advise partnering with IT firms that offer a full range of services and oversee every phase of fintech software development.

#OnlineBanking#MobileBanking#Fintech#DigitalFinance#InternetBanking#DigitalPayments#VirtualBanking#DigitalWallets#BankingTechnology

0 notes

Text

Payment service provider in india

In the rapidly evolving digital landscape of India, the growth of Payment Service Providers (PSPs) has been nothing short of revolutionary. As businesses continue to transition online, the need for efficient, secure, and versatile payment solutions has become paramount. At Zyro, we understand the importance of staying ahead in the digital curve, and in this blog, we'll dive into the world of PSPs in India, exploring how they are changing the face of business transactions and what you need to know to make the most of these services.

know more :- https://zyro.in/blog/business/payment-service-provider-in-india/

#banking#turbanking#investmentbanking#onlinebanking#mobilebanking#digitalbanking#bankinglife#privatebanking#betterbanking#islamicbanking#urbankings#landbanking#communitybanking#hasanahbankingpartner#openbanking#urbanking#netbanking#internetbanking#bankingandfinance#cordbloodbanking#businessbanking#investmestbanking#ebanking#weekendbanking#inhomebanking#smartbanking#mortgagebanking#syariahdigitalbanking#womeninbanking#mbanking

0 notes

Photo

RFP Template for e-Banking Platform Implementation https://fintechrfps.com/product/rfp-template-for-e-banking-platform/?utm_source=tumblr&utm_medium=social&utm_campaign=fintech+policies+templates

0 notes

Text

Der fast gläserne Paypal Kunde

With Whom we share Personal Information

Diesen Bericht kann man kurz gestalten. Paypal, der weltweite Zahlungsdienstleister, sagt selbst - wie es rechtlich auch sein sollte - welche Daten seiner Kunden das Unternehmen mit welcher anderen Firma oder Behörde teilt. Übersichtlich ist noch die Liste der Staaten in den die Empfänger der Daten sitzen: France, Germany, Ireland, Spain, Netherlands, Bulgaria, Italy, Poland, Cyprus, Sweden, Austria, the United Kingdom, Tunisia, Egypt, El Salvador, the Philippines and the United States.

Die Liste der Unternehmen, die als Empfänger der Daten auftreten hat leider keine Nummerierung. Importiert in ein Open Office Dokument ist sie 87 Seiten lang. Vielleicht hat Paypal angenommen, dass bei dieser Menge sowieso niemand mehr genauer hinschauen wird. Unterteilt wird sie in 587 Zeilen, was aber wenig aussagt, da fast jede Zeile mehrere Unternehmen auflistet.

Der "beliebteste" Grund zum Weitergeben der Daten ist: To verify identity and carry out checks for the prevention and detection of crime including fraud and/or money laundering

also: Überprüfung der Identität und Durchführung von Kontrollen zur Verhinderung und Aufdeckung von Straftaten einschließlich Betrug und/oder Geldwäsche

Das wäre ja ein Grund, den man in einigen Fälle sogar verstehen könnte. Schwerer verständlich sind dann solche Gründe: To enable secure data transfer, also um eine sichere Datenübertragung zu ermöglichen. Die Datenübertragung wird sicher nicht sicherer, wenn ich mehr Institutionen mit Daten versorge ...

Welche Daten die aufgelisteten Unternehmen erhalten, ändert sich je nach Zweck, enthält aber meist: Email, names, accounting information. Die Menge kann sich aber auch erhöhen bis zu: Name, email, IP address, phone number, business banem business ID, business owner, IP address, user name, gender, date of Birth, Country Location, Place of Birth and Nationalitydevice identification, iZettle customers with personal accounts containing full name, details of account liabilities, debts and amounts owed to us, credit history information, repayment history, Merchant information and account history, VAT number, card/payment information, Organization_uuids, transactions, transaction value, details of user funding instruments, and government identification, customer’s spoken words, customer keyboard and cursor behaviour when using PayPal website or App, Social media login’s or identity tokens ...

Nach den "spoken words" - Jede/r von uns hat die Ansage "dieser Anruf wird zur Qualitätssicherung aufgezeichnet" schon einmal gehört - und den Tastaturanschlägen ist uns dann die Lust am Sammeln vergangen und wir überlassen die Liste den Kunden von Paypal, die sie wahrscheinlich zu 99% nie anschaut haben. Nichts davon hat jetzt schockiert aber unsere Vorbehalte gegen Internet Banking sind damit nicht kleiner geworden.

Mehr dazu bei https://www.paypal.com/ie/webapps/mpp/ua/third-parties-list

Kategorie[21]: Unsere Themen in der Presse Short-Link dieser Seite: a-fsa.de/d/3yh

Link zu dieser Seite: https://www.aktion-freiheitstattangst.org/de/articles/8643-20240107-der-fast-glaeserne-paypal-kunde.html

Link im Tor-Netzwerk: http://a6pdp5vmmw4zm5tifrc3qo2pyz7mvnk4zzimpesnckvzinubzmioddad.onion/de/articles/8643-20240107-der-fast-glaeserne-paypal-kunde.html

Tags: #Paypal #InternetBanking #Bankdaten #Verhaltensänderung #Datenweitergabe #Liste #Transparenz #Informationsfreiheit #Anonymisierung #Verbraucherdatenschutz #Datenschutz #Datensicherheit #Tastaturanschläge #CreditCard

#Paypal#InternetBanking#Bankdaten#Verhaltensänderung#Datenweitergabe#Liste#Transparenz#Informationsfreiheit#Anonymisierung#Verbraucherdatenschutz#Datenschutz#Datensicherheit#Tastaturanschläge#CreditCa

1 note

·

View note

Text

Intellect Design Arena Ltd-Transforming Digital Banking Solutions

Intellect Design Arena Ltd, a global financial technology company, offers a digital banking platform that enables banks and financial institutions to deliver innovative and personalized digital experiences to their customers. The platform is designed to help institutions streamline their operations, reduce costs, and improve efficiency. It includes a range of digital banking solutions, such as mobile banking, internet banking, digital lending, and digital payments. The platform is built on a modern, cloud-native architecture that provides high scalability, reliability, and security. It also supports open banking and APIs, enabling institutions to integrate third-party services and offer a wider range of products and services to their customers. Overall, Intellect Design Arena Ltd's digital banking platform is a comprehensive solution that empowers financial institutions to stay competitive in the rapidly evolving digital landscape.

#DigitalBankingPlatform#DigitalBanking#Fintech#BankingSolutions#PersonalizedExperience#CloudNative#InternetBanking#DigitalLending#DigitalPayments#APIs#FinancialTechnology#BankingSoftware#BankingPlatforms#DigitalTransformation

0 notes

Photo

(via Internet Banking)

#bankingsolutions#onlinefinance#ebanking#VirtualBanking#securebanking#bankingtechnology#fintechservices#digitalfinance#onlinebanking#internetbanking

0 notes

Text

Online Banking System: A Convenient and Secure Way to Manage Your Finances

Online banking is a system that allows guests of a bank or other fiscal institution to conduct a range of fiscal deals through the fiscal institution's website or mobile app. These deals can include Checking account balances Viewing recent deals Transferring plutocrat between accounts Making bill payments Depositing checks Opening new accounts Applying for loans Setting up cautions and announcements Online banking allows you to manage your finances from anywhere, at any time, with the peace of mind that your information is safe and secure. It allows you to do your banking from anywhere, at any time. You can also save time by avoiding the need to visit a bank branch. How does online banking work? Online banking workshop by using a secure connection between your computer or mobile device and the bank's website or app. This connection is defended by encryption, which means that your particular and fiscal information is safe from unauthorized access. When you log in to your online banking account, you'll be suitable to see your account balances, recent deals, and other account information. You can also use online banking to transfer plutocrats between accounts, make bill payments, and set up cautions and announcements. The benefits of online banking offer a variety of benefits, similar to Global access You can manage your finances from anywhere in the world,24/7. Security Online banking is veritably secure, with features like encryption and fraud protection. This makes people feel confident that their fiscal information is safe. Cost-effectiveness Online banking can save people, plutocrats, on freights. For illustration, numerous banks waive the figure for online bill payments. Inflexibility Online banking allows people to choose the features that work stylishly for them. For illustration, some people may only need to check their account balances online, while others may want to be suitable to transfer plutocrats between accounts and pay bills. The security of online banking is veritably secure, with features like encryption and fraud protection. still, there are some effects you can do to cover your account indeed further, similar as produce a secure word and updating it constantly. Don't partake your word with anyone. Be aware of the particular information you partake in online. cover your bias with security software. Conclusion Online banking allows you to manage your finances from anywhere, at any time, with peace of mind that your information is safe and secure. It's a great option for people who want to save time and plutocrats, and who want to be suitable to bank from anywhere, at any time. still, I recommend giving it a pass, If you aren't formerly using online banking. It's a great way to take control of your finances and save time. In addition to the benefits mentioned over, online banking can also help you to Track your spending Online banking makes it easy to see where your plutocrat is going. This can help you to see where your plutocrat is going, so you can make informed opinions about where to cut back. Set fiscal pretensions Online banking can help you to track your progress toward your fiscal pretensions. This can help you to see your progress toward your pretensions, which can help you to stay motivated and on track. Get cautions and announcements Online banking can shoot you cautions and announcements about your account exertion. This can help you to stay informed about your finances and to take action snappily if there's a problem. Overall, online banking is an accessible, secure, and protean way to manage your finances. I would suggest that you try online banking if you aren't formerly using it. It's a great way to take control of your finances and save time.

#onlinebanking#mobilebanking#internetbanking#digitalbanking#fintech#bankingtechnology#bankingapp#bankingsecurity#bankingtips

1 note

·

View note

Link

#digital#E-banking#efektif#InternetBanking#Keuangan#ManajemenKeuangan#manfaat#mengelola#PengelolaanKeuangan#perkembanganinternet#secara#technology#teknologi#tutorial

0 notes

Text

Internet Banking Laws in India: Key Regulations & Guidelines

This article on 'Internet Banking Laws in India: Key Regulations and Guidelines' was written by an intern at Legal Upanishad.

Introduction

Net banking, or Internet banking, helps a customer do financial transactions through the Internet. It provides almost all kinds of services to a customer who has an account at a bank. For instance, transfers, payment of bills, recharges, deposits, etc all these services can be accessed sitting at home through a click on a mobile phone. The customer can also track those transactions on a real-time basis in a secure mode. This article will discuss the laws that regulate Internet banking in our country. Laws protect the customers’ interests and give them the confidence to engage in such internet activities. Moreover, this article will analyse whether there is a need for better laws as compared to the present legal framework.

Internet Banking: Meaning and Concept

The meaning of Internet banking is that the services of banks are provided via the Internet. It includes all sorts of financial transactions. The customer can control and manage the bank electronically and there is no need to go to the branch of their bank for every single work. It is also known as web banking, e-banking, or "online banking. Most people prefer this as it is an easy, accessible, and convenient way of transacting.

The main feature of Internet banking is its accessibility; a customer can easily manage their bank accounts. For instance, being able to check their account details online without actually going to the bank also allows them to update their deposit, loan, etc. Also, it allows the customer to transfer funds through an online platform, which is an easy and quick way. Moreover, a person can pay all sorts of bills and other expenses directly through their mobile phones. Additionally, it provides security to customers through pins, biometrics, passwords, and many other ways.

How does Internet banking work?

It’s an online platform provided by the bank. Here, a customer has to register his account in order to use net banking by filling out an application form provided by the bank. Moreover, the bank also provides user authentication. There are a number of services provided by the bank that a person can avail of.

Laws Regulating Net Banking

There are various laws and regulations made to protect and secure the customer's financial transactions and sensitive information.

- The Information Technology Act, 2000 is the main legislation for electronic transactions in India. It includes web or net banking. There are penalties for unauthorized transactions by cyber criminals. It also gives recognition to any electronic document, signature, record, etc.

- Section 43 of the IT Act lays down penalties and compensation for any sort of damage to computer software. It also includes unauthorised access to computers and the net banking system.

- Section 43A of the IT Act deals with sensitive data in cases where a corporate body deals with the sensitive data of customers and fails to manage such sensitive data, which results in losses to customers. Because of such negligence, the corporate body will be held liable under this section.

- Section 66 of the IT Act deals with offences like hacking, identity theft, viruses, and malware in computer software or systems.

- Sections 66C and 66D of the IT Act deal with identity theft and impersonation. The cybercriminal dishonestly uses passwords, signatures, or any other things of customers in order to fraud or deceive.

- Section 72A of the IT Act deals with breaches of legal or lawful contracts. The offender who discloses information that contains sensitive information without the consent of such a person shall be punished under this section.

- Reserve Bank of India Guidelines: These guidelines include customer protection measures and high-security standards for those banks that offer net banking services to their customers.

- The Payment and Settlement System Act, 2007 provides the legal framework for the supervision and regulation of the payment system in our country. This includes net banking transactions and any electronic fund transfers.

- Banking Regulation Act, 1949: This act empowers the RBI to supervise other banks’ operations in our country. Some provisions talk about the confidentiality of customer information, their protection, and other such practices related to net banking.

- The Consumer Protection Act, 2019 deals with protecting consumers’ rights while they use net banking. It resolves complaints related to banking services, provides remedies, and provides fair treatment.

- Securities and Exchange Board of India Regulations: It issues guidelines related to trading and investment. It sets the standards for better online trading platforms that are provided by any financial institution.

- The Indian Penal Code, the Criminal Procedure Code, and the Indian Evidence Act have provisions related to cybercrimes that are related to web banking. For instance, Section 419 of the IPC deals with cheating by personation, when a person impersonates someone else and cheats. Section 420 deals with cheating and dishonestly inducing delivery of property by making false promises, and sections 463 and 471 deal with forgery and forged documents as genuine, respectively.

- Section 154 of the CrPC is related to the first information report if a person finds that an offence has been committed against him that is related to net banking. He can approach a nearby police station. Hence, criminal proceedings will begin. And Section 156 of the CrPC empowers the police to investigate cognizable offences on the basis of a complaint.

These are the primary laws that regulate net banking in our country to safeguard and protect customers. The Reserve Bank of India periodically provides guidelines related to risks and security.

Suggestions and Conclusion

Every bank has its own distinct characteristics. Different banks offer various services to their customers. Without a question, Internet banking is convenient and accessible to everyone. However, there are certain risks involved. As a result, we must take reasonable efforts to protect sensitive or financial information. One of the most common concerns in Internet banking is identity theft. In this case, the thief steals a customer's personal information, impersonates that customer, and gains access to the bank. As a result, fraudulent transactions occur.

Phishing is another prevalent practise in which a criminal appears to be a member of a reputable institution. In addition, the customer is duped into providing critical information over the phone. Personal information might be leaked in the form of viruses and malware that infect the customer's mobile device. The data can be stolen in a variety of ways.

To avoid similar instances, the author recommends keeping software up to date, using strong passwords, being vigilant about phone calls and emails, installing anti-virus software, notifying the bank immediately when such incidents occur, and taking precautions.

List of references:

- Rohit Jain, “Legal Framework of Internet Banking in India”, 4(1) International Journal of Law Management and Humanities (2021)

- Raunak Sood, “The legal structure of e-banking in India, iPleaders Blog”, 8 November 2021, available at: https://blog.ipleaders.in/the-legal-structure-of-e-banking-in-india/ (last visited on 10 June 2023)

- Rao, Internet Banking in India, Mondaq, 11 April 2003, available at: https://www.mondaq.com/india/finance-and-banking/20687/internet-banking-in-india (last visited on 10 June 2023)

The Information Technology Act of 2000

Indian Penal Code 1860

Criminal Procedure Code 1974

Read the full article

0 notes

Link

0 notes

Text

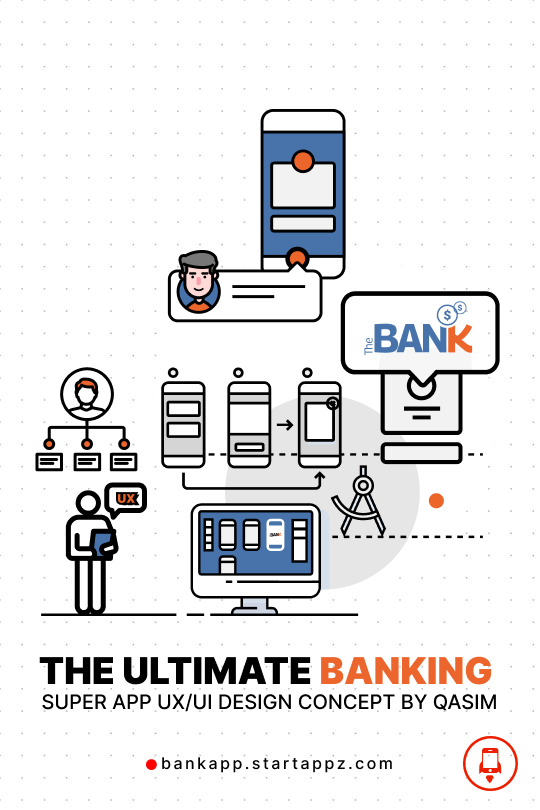

Modern technology has taken banking to a whole new level. Ease, speed, enjoyment, and convenience are rewriting the history of the user experience in banking. While many banks still struggle to digitize their products, new Neobanks have rapidly emerged, changing the game's rules. One of the biggest challenges is how to create and develop a banking ecosystem that could organically deliver dozens of products as a connected user flow with the possibility to scale up into the bank-as-a-platform.

The ultimate banking super app UX/UI design concept shows how any finance company could upgrade its mobile banking ecosystem with ten banking trends.

To reach our primary goal of transforming complex digital banking solutions into something inspiring for users, we challenged ourselves to build the most straightforward, delightful, and enjoyable mobile banking app design. Our mobile banking UX case study strove to prove that beautiful app design is achievable without losing a wide variety of banking functions and products.

In this mobile banking case study, we invite you to explore our journey to a new strategy of designing financial products that are unlike anything you have ever seen. This mobile banking UX design concept does not try to be the ’perfect’ banking solution. Instead, its goal is to present an innovative customer-centered approach to financial services design.

Don't you think the idea of an old-time bank facility is in the past? If you thought of that, you weren't tumbling, we are living in the digital world right now, and life is so fast; if you didn't catch up, you would be behind a lot of successful businesses, with online banking becoming the actual trend, we are gladly happy to inform you.

Startappz is jumping on a new level of digital transformation platforms specializing in banking financial activities; whenever you want to pay your bills, it's one click away; wherever you are.

If you are looking for ATM nearby, it is there to support you in identifying their locations. If you are planning for a weekly or monthly budget, the app monitors your payment record to help you reach your payment plan as per your request.

Much more than that, it's incredibly safer than before; through time, we have developed the most suitable banking platforms that have made your financial life easier, faster, and safer.

#mobilebanking#banking#onlinebanking#digitalbanking#fintech#bank#finance#money#digitalbank#business#banks#financialservices#mobileapp#bankingapp#internetbanking#mobilepayments#payments#smartphone#financialtechnology#shipping#regtech#mobiletherminal#mobileprinter#printerminithermal#parking#printermurah#portableprinter#printerbluetooth#kurir#layananpengiriman

1 note

·

View note

Text

Business banking service/solution provider

In the dynamic and often complex landscape of business, efficient financial management is critical to success. As businesses grow and evolve, so do their banking needs. This is where choosing the right business banking service provider becomes paramount. At zyro, we understand the importance of making informed decisions in every aspect of your business, including banking. In this blog, we’ll explore key considerations for selecting a business banking service or solution provider that aligns with your company's unique needs.

know more :- https://zyro.in/blog/banking-providers/business-banking-service-solution-provider/

#banking#turbanking#investmentbanking#onlinebanking#mobilebanking#digitalbanking#bankinglife#privatebanking#betterbanking#islamicbanking#urbankings#landbanking#communitybanking#hasanahbankingpartner#openbanking#urbanking#netbanking#internetbanking#bankingandfinance#cordbloodbanking#businessbanking#investmestbanking#ebanking#weekendbanking#inhomebanking#smartbanking#mortgagebanking#syariahdigitalbanking#womeninbanking#mbanking

0 notes

Photo

RFP Template for Internet Banking Implementation https://fintechrfps.com/product/rfp-template-for-internet-banking-implementation/?utm_source=tumblr&utm_medium=social&utm_campaign=fintech+policies+templates

0 notes

Text

Digital Currencies Are Not Regulated

A few years ago, when the first internet based companies began to spring up, one of the first things that people noticed was the ease with which they could transfer money across the globe. In many cases this was done through an online bank account, and the transactions were carried out using a credit card or a debit card. This was great because it meant that people could get access to their money anywhere in the world, and this was possible without having to leave home.

However, as more and more people began to use these services, there was a problem. The system that they used was not very secure. This meant that if someone wanted to steal your information they would be able to do so, and once they had your information, they could go on to take your money. Of course, you could always change banks, but this was inconvenient and often expensive.

So, the next thing that people started to look into was a way of carrying out these transactions securely. This was something that people had been trying to do for a long time, and the technology had just not been available. However, as the internet became more popular, the ability to carry out transactions securely became more important than ever before.

As a result, the idea of using digital currencies began to emerge. These are currencies that are only used online, and they are completely anonymous. They can be used to pay for goods and services, and they are also a great way of transferring money across the globe.

The problem with these types of currencies is that they are not regulated by any central authority. So, they are not backed by any government, and they are not backed by any central bank either. This means that they are completely unregulated, and this makes them very volatile. As a result, they tend to fluctuate quite a lot.

Because of this, it is important that you only invest in these types of currencies if you know what you are doing. It is easy to lose your money if you are not careful. However, if you do know what you are doing, then you stand to make a lot of money from these types of investments.

https://popscrypto.com/index.php/2023/01/15/digital-currencies-are-not-regulated/

0 notes

Photo

Bancos digitais: sete vantagens para aderir aos serviços . Fotos: Pixabay e Freepik . https://www.gentedesucessovip.com.br/gente-que-faz/empreendedorismo/4131-bancos-digitais-saiba-vantagens #internetbanking #bancosdigitais #bankpay https://www.instagram.com/p/CfWzCLgO81s/?igshid=NGJjMDIxMWI=

0 notes

Last Seen Blogs

bugtrainerolive

bug party

carolynsweet87

Carolynsweet87

astro-rainbow777

Astro-Rainbow777

stardustmaiden

*。⋆ ☾ ° —— ┋a song of fallen stars

babyivyx

babyivyx