#Reynold may have a bat at the ready as well

Text

Cedric: I sleep with knives under my pillow.

Reynold: Weak. I sleep with a sword.

Callisto: Hah. You’re both pathetic.

Cedric: What killer weapon do you sleep with Mr. Badass?

Callisto*smiles proudly*: Penelope.

#I needed to put my big three in some kind of interaction#the three babygirls have united.#mansplain manipulate malewife#manwhore and manslaughter too#Reynold may have a bat at the ready as well#Cedric absolutely sleeps with some kind of weapon#those years of dealing with Callisto’s absolute failures of grimreapers did something to him#Callisto still has his sword right by his bedside#but Penelope is definitely the deadly weapon#ah yes Penelope the killer weapon#*chef's fucking kiss*#penelope eckart#penelope eckhart#callisto regulus#reynold eckart#reynold eckhart#cedric porter#penelope eckart x callisto regulus#penelope x callisto#villains are destined to die#vadd#death is the only ending for a villainess#death is the only ending for the villainess#death is the only ending for the villainess incorrect quotes

97 notes

·

View notes

Note

Hi! if you want to, could you bless us with a few Rayan headcanons? As in, i've been thinking how the story would be if he had a child with Cloe(?) before she died? And speaking of children, how would bring-your-child-to-work day be with Rayan? With his and May's kids or the before-canon child?

Hey, of course!! This is definitely one of my favorite type of asks to answer actually!

I thought about it before, I admit, sometimes I think about how it would be if he had a kid with Chloe before meeting Candy and was a single parent for the last 7 years (in mclul).

Let’s suppose the kiddo was just a baby when she died, so he/she wouldn’t know about their mom, they would know that Rayan is always alone, giving him best as a single parent and still trying to make something of his career. Then one day the kiddo would meet Candy, hit off with her right off the bat and finding her fun to be around, THEN the kid would realize that Rayan also enjoy her company and procced to create plans to make them bond kkkkkk

A little bit like “Definitely, maybe” with Ryan Reynolds (I love that movie), in which the kid of the story just wants her father to be happy, even if it’s without their mom (even if in this case, Rayan’s daughter/son would’ve grown up without really knowing Chloe or missing her properly, just missing the idea of her and having a mom, so they would accept the situation better).

It would be a kid around 7 years old, maybe that would just really enjoy Candy’s company and see in her someone that would care, that could make both them and their father happy and be a family.

I think from Candy’s side and Rayan’s side it would be another uncertainty, another reason to be careful and hesitant, but at the same time, it would also be another thing they would bond over.

Because, I really think that a kid wouldn’t get in the way at all, that they would pass over their doubts (like they actually did canonly in mclul) and be together regardless. If anything, if done right, it could bring them even closer together.

I love picturing “bring-your-child-to-work day” kkkkk part of me believes that Rayan wouldn’t do it super often, maybe every once in a week or even less, maybe more during the exams or during one of his famous field classes.

Melody would be out of a job in those days, because the kid would definitely be Rayan’s little assistant, knowing as much about modern art as a kid around 7 to 6 years could possibly know (May’s and Rayan’s oldest daughter is around 6 years old). All the female students would be dying with cuteness because Rayan would be the proudest and a very caring father, the type that is always watching the kid even while explaining something complex and not losing his focus.

And of course, any kid with Rayan’s genes wouldn’t just have his flawless looks, but also a smart take out in any situation, countless pop references to do, and even a cute sense of maturity charming at most, so they would definitely be a success around the campus. I will always say that kkkkkk always.

In my personal hc Lilly is the one that mostly goes with him, since Daisy is just a baby and May is very protective of her, but I think when Daisy gets around 3/4 years, he would bring her sometimes too, even both of them, since Lilly would be around 9/10 years old.

And I can imagine that this only happens strictly when he is giving notes or receiving papers - sometimes when he is showing a film to the room and it is something that the girls can watch. Because, if he brings both of them ready to give a full 2/3 hours class and expect them to be quiet and well behaved during such long period of time, it wouldn’t end well xD not when they’re together. Maybe with Lilly alone and older, but not with a baby Daisy around like that.

I hope you liked my answer, I feel kinda rusty in answering those kinds of asks G-G it’s been a while since the last time someone asked for headcanons.

9 notes

·

View notes

Text

Vogue 73 questions with Mike Lawson and Ginny Baker

“Hey Mike, what’s going on?”

“Not much, lookin’ forward to doing this interview.”

“I am too. Are you guys ready to answer 73 questions?”

“Sure, let’s go find Ginny.”

It turned out they found her sitting on a lounge by the pool in leggings and a t-shirt.

“So, you guys just finished playing in the World Series, any regrets?”

“No, we were excited to get there again this year,” Mike answered sitting next to Ginny.

“I mean, I hate to lose, but we played hard and that’s all you can do.”

“How many baseball games do you think you’ve played in your life?”

“For me? I have no idea. I’ve been playing since I was 5. That’s 35 years, between little league, AA, AAA and the majors? Let’s just say a lot,” Mike laughed.

“Same, minus 10 years,” Ginny added.

“Which of your competitors has helped you improve your game the most?”

“I would say Aaron Judge, a great hitter always makes me work that much harder for a strike.”

“Nolan, Nolan Arenado. I like to steal, but he keeps me honest.”

“If you could play any other sport, what would it be?”

“Tennis?” Ginny shrugged.

“I’ve always liked hockey.”

“Past or present who would you love to play with?”

“I gotta say Babe Ruth,” Mike said.

“For me, Cy Young or Yogi Berra.”

“What’s are you superstitious about?”

“I like a certain practice cage. I don’t know if it is a superstition, but I always go for that one if it’s available, and Mike used to sleep with his bat on game days.”

“Where do you go when you need to relax?”

“If I told you that, it wouldn’t be relaxing anymore,” Mike joked.

“We spend a lot of time at home, but we just took a vacation to Baja and that was really nice.”

“What is your nickname?”

“I call him old man.”

“And I call her rookie.”

“Who is the funniest person you know?”

“Dwayne,” Ginny answered after a moment of thought.

Mike nodded. “He is great. We were at a fundraiser for his foundation the other day, and everyone at the table was laughing crying.”

“Wait, do you mean Dwayne Johnson?” the interviewer asked.

“Yeah, we met at the Espys and get together every now and then. He throws a great BBQ every year.”

“OK, what is your go to karaoke song?”

“Baker loves anything by Beyoncé or Katy Perry. I stick to the Eagles and Duran Duran.”

“What song always makes you want to dance?”

“He is right. I love Katy Perry and Beyoncé, but Uptown Funk is my jam.”

“I don’t dance much, but no one can resist Love Shack.”

“What is your walk out song?”

“I have a mix I listen to, it’s mostly instrumentals to help me clear my head.”

“I go for the classic, eye of the tiger.”

“If you could only read one book from now on, what would it be?”

“Treasure Island has been my favorite for a long time. I’ve read it 5-6 times, and I wouldn’t mind reading it again.”

“That is really hard for me, because I don’t read things more than once very often, but… I’m going to say Esperanza Rising. I know it is a kid’s book, but I still have the copy I read in 5th grade. Someday I want to be able to share it with my kid.”

“Most absurd rule in baseball?”

“It’s not really a written rule, but there is this thing where everyone must be involved in am on-field fight. When Gin went after the Mountain, our assistant coach had to walk out there and hold onto the other coach. These guys are in their 60’s hugging on the field so it is nice and even numbers. I mean I get it, but it can look pretty silly.”

“Describe your style in one word?”

“Comfy?” Ginny ventured.

“If you could raid anyone’s closet who would it be?”

“David Beckham,” Mike answered quickly.

“Serena Williams.”

“Any hidden talents?”

“I love to knit.”

“No kidding. I can’t tell you how many times she got me with one of her needles on the bus.”

“On purpose?”

“No, he is just clumsy and doesn’t look before he sits down.”

“I did get some cute hats and that blanket over there out of it, though.” He gestured to a knit blue and white blanket with a Padre’s logo on it draped over a leather chair.

“Looks nice, now for a hard one. What is love?”

“Baby don’t hurt me?” Mike joked, Ginny batted his arm. “No, seriously, love is different for different for different people but for me, it is a commitment to something that you care deeply about.”

“That and finding someone to see the best in you even when you can’t see it in yourself.”

“What is the most romantic thing you’ve done for each other?”

“He leaves me notes in my locker on days when we don’t work together.”

“She rubs my back.”

“Best or worst pick up line someone has ever used with you?”

“I thought it was funny when this guy said, I was so distracted by you that I ran into that wall over there. So, I am going to need you name and phone number for insurance purposes.”

“Who said that?” Mike asked.

“Never mind, what’s yours?”

“A girl just walked up, put her hand out and asked me I could hold it while she went for a walk.”

“Did you?” the interviewer asked.

“I did,” Mike smiled, then he reached out and squeezed Ginny’s hand.

“Who was your childhood crush?”

“This guy.”

“She finally admits it. She had my poster on her wall, but now I have hers too.”

“What was the last show you binged?”

“We just got done rewatching all of Brooklyn 99.”

“He was a thing for Rosa.”

“She does too.”

“I mean, doesn’t everyone?”

“Name one thing you can’t live without.”

“Air?” Mike joked.

“A good wifi network,” Ginny groaned. “I hate when I’m on the road and we finally get to a hotel and they have super slow internet. I just want to relax and watch Youtube or scroll tumblr.”

“Name something you are terrible at.”

“Bowling,” Ginny answered.

“I suck at word games, scrabble, boggle, all that stuff. She usually beats me by at least 100 points.”

“What is the most nervous you’ve ever been?”

“My first game in the majors.”

“Same. Mine, not hers. I wasn’t really nervous for her because we didn’t know each other, but I remember almost blacking out the first time I walked onto the field.”

“Name one bad habit you just can’t break.”

“I bite my fingernails, so I have to keep them super short, but that’s fine, because I would have to for pitching anyway.”

“I am an emotional shopper. When things aren’t going well in life, I use retail therapy way too much.”

“He is not kidding. The good thing is he cleans his closet out once every six months and donates a lot of impulse buys to charity.”

“Craziest fan moment?”

“A lady told me she named her baby after me and asked me to sign her. I signed her little shirt, but it was a little weird.”

“What is one phrase you use too much?”

“I’m just sayin’. She keeps reminding me how much it annoys her, but it just rolls off my tongue.”

“That’s ok, I always say my bad, and he hates that, so we are even.”

“If you could be any animal, what would it be?”

“I want to say something bad ass, but really I’m a house cat.”

“I can totally see that. I am a… a bear, but mostly because I just want to sleep and be left alone sometimes.”

“Can you say something in a different language?”

“Que bola? Its Cuban for what’s up. I picked it up from Livan.”

“I speak some Indonesian, from my mom. Tidak apa apa is no worries, which is what I use most in like everyday conversation.”

“What is one cause you care deeply about?”

“It is hard to name one, but I work a lot with our local children’s hospital,” Mike answered.

“I support NAACP legal defense fund, Equal justice initiative and the African wildlife foundation.”

“How do you celebrate your wins?”

“Ice cream or beer depending on the day.”

“How do you deal with loses?”

“I try to figure out what went wrong, so I can do it differently next time,” Ginny said thoughtfully.

“How do you deal with haters?”

Ginny laughed, “You just gotta block’em out.”

“If you could redo one game which would it be?”

“The game where I messed up my knee the first time.”

“Yeah, when I almost got the no hitter and instead messed up my arm, that was pretty bad.”

“Besides baseball what would you like to be remembered for?”

“Being a good person.”

“If you weren’t baseball players, what else would you be?”

“I would do something with cars.”

“I would do something with history? Teaching or maybe be an anthropologist?”

“Do you have a pregame ritual?”

“I have a pump mix but mostly I like to meditate and mentally prepare. I usually go over the lineup one last time with Mike.”

“How many MLB teams can you name in ten seconds?”

“The Padres, the Braves, the Dodgers, the A’s, the Rockies, the Yankees, Sox, Cubs, Phillies, Astros, Mariners…”

Mike took over, “Jays, Giants, Angels, Brewers…”

“And that’s time, good job. Name the best baseball player who ever lived.”

“Babe Ruth.”

“Willie Mays.”

“If you could only eat one thing forever, what would it be?”

“Pizza?” Mike answered.

“Burgers, but they have to come with fries,” Ginny chimed in.

“What movie always makes you cry?”

“Field of dreams.”

“The Lion King.”

“What movie makes you scream in terror?”

“My friends dragged me to the Omen once, which was pretty scary, but mostly I don’t watch scary movies.”

“I watched the exorcist way too young, and that pretty much put me off scary movies for life.”

“What is the most inspirational sports film of all time?”

“I always liked Cinderella Man with Russel Crow.”

“I really liked the Life of Pi.”

“Who do you want to play you in the movie of your life?”

“I don’t know that they would make a movie of my life, but when they make hers I think Ryan Gossling is a good choice, or Ryan Reynolds, or any of the Marvel Chrises.”

“If they made a movie… I would say… Letitia Wright maybe?”

“What’s the stupidest thing you’ve ever done?”

“As a kid I broke my ankle trying to do a skate board trick,” Mike scratched the back of his neck and flushed slightly.

“What is one skill you wish you had but you don’t?”

“I am trying to learn to cook, but Mike still does it most of the time.”

“If you were a super hero, what would your name be?”

“Black Diamond.”

“Beard-Man.”

“Who’s your most famous follower on twitter?”

“I don’t have a twitter.”

“A lot of people follow me to hear about Ginny, I would say Anna Kendrick is the most famous.”

“You travel a lot for work, what are three things you take with you everywhere?”

“My headphones, a neck pillow, and my phone charger.”

“Same.”

“Do you have an pets?”

“We have a dog,” Ginny whistled, and a mini pie ball dachshund call running out. “This is Chip. I named her after the cup from beauty and the beast. She is a super sweet girl.”

“What’s your zodiac sign?”

“I am a Libra and Ginny is a Leo.”

“What is your favorite flavor of ice cream?”

“He likes coffee or half-baked and I like Cherry Garcia.”

“What’s one household chore you hate to do?”

“We both hate the dishes, so we do them together, so we can get it over with quickly.”

“Do you have any collections?”

“I have a snow globe collection, and Mike collects baseball memorabilia.”

“Who is more competitive?“

“Me!” they both said quickly, then looked at the other and laughed.

“What is your go to date night?”

“We like to go see comedians.”

“He just got us tickets to see Ali Wong for our anniversary.”

“If you could go anywhere on vacation where would it be?”

“We are going to Kenya next month, and I am really excited about that,” Ginny answered.

“Me too.”

“What is your love language?”

“I like acts of service and words of affirmation,” Mike answered seriously for once.

“and for me, it is quality time.”

“Sleep in or rise early?”

“Sleep in!” Mike grinned.

“Read a book or watch TV?”

“Watch tv,” they agreed.

“Kiss or hug?”

“Kiss,” they both snapped.

“Strength training or cardio?”

“Cardio,” Ginny answered automatically

“I like strength training,” Mike added.

“You guys recently got married, what was the biggest change?”

“Not really anything? We already lived together.”

“Calling him my husband, is weird sometimes.”

“What was your favorite part of the wedding?”

“When we left?” Ginny laughed.

“What kind of cake did you have?”

“Just plain yellow cake with chocolate frosting,” Mike answered.

“Who caught the bouquet?”

“My agent, Amelia.”

“What song was your first dance to?”

“Unforgettable.”

“What are you doing today?”

“We’re going to the farmer’s market, then coming home for dinner with some friends.” Ginny answered, walking toward the door.

“Can I come along?”

Ginny made a face. “No, thanks for stopping by though.”

#and my homegirl Ginny B#Ginny Baker#ginsanity#pitch#pitch rewatch#pitchwithdrawls#pitch fic#bawson#bawson fanfic#bawson fic#mike lawson#missing mike Lawson

54 notes

·

View notes

Text

May 6

Just awake and already feeling tapped out. The only task I must complete today is emptying out the shower I use for storage and at least rinsing that thing out. Because the stuff is a most likely dusty that will happen early so I can wash up after.

I feel ready to do some writing, just got to be certain I’m ready to go in to that story’s world. I might take the next couple of days to do some prep/inspirational reading and going over the story’s beat sheets to make certain there aren’t places I want to add.

There is a sort of cousin to the story that I could work out more but without an editor or someone else to give me some useful feedback I can’t tell if it cuts too close to the inspiration.

Then again we live in a world where cis gender French robots can adopt Chucky dolls.

I suppose by now we’d know if they wanted to be called Gal or Tamsin. Tamsin being a feminine version of Thomas and he doesn’t strike me as a Tammy. Especially with pop culture memory being that comedy movie and not the Debbie Reynolds movie series. Although why wouldn’t T-Bang want to chose something by princess Lea’s mom?

Point being there’s a story idea in one or both of the Daft Punk robots identifying and living as a woman, and not wanting the press to know, but having to otherwise be a male robot for work.

See, if you actually read my blog you might get inspired for something. That’s the least I can do.

It’s a good thing I’m comfortable bringing things to do with myself, aside from just a phone/tablet, with all the perspective doctor’s appointments I have. As much as I dislike people in waiting rooms and disrupting my time to have to go there I want my aches and pains treated.

It’s kind of like that turn of the century job where I made minimum wage to read and draw and write.

The job where I have no idea how many seizures I was having because if I was staring in to space during the down time or robotically repeating the same actions during work time and obeying the AD’s commands no one would know. I could have all the mood shifts and anxiety attacks I wanted as long as I didn’t make noise and did as I was told.

You’d be amazed how many people can be having a cosmic freak out and you’d never know because we’ve learned to hide it.

Which version of Munch’s Scream did my soul smear come out as again?

It’s the one hanging on the wall behind Neil Inness while he sings ‘Boring’ although I feel Julian Lennon is more on the ‘Slaves of Freedom’ wave because SoF is either an accidental masterpiece or it’s the greatest troll song ever.

Freedom is... the pedestal of purpose in the bathroom of your dreams.

Although if it is ‘Boring’ then Julian has one hell of a Bat Cupboard.

When the mind flows like that in its strange ways I feel so alive. Mentally. Physically I can’t remember when I’ve been pain free or had the energy.

Didn’t crochet yesterday. I did lots of laundry and laundry related activities as well as some moving some of the stuff around in preparation for more moving the stuff around. The Monster High dolls switched tubs, still haven’t opened Nova or Gooliope, and seriously forgot how many of them I have. All first versions of course as I don’t like the new face molds and lack or articulation.

Less books would mean more room for Monsters. Or the Monsters go on top of the cubes but there’s no room for anyone else. Or the Monsters go in the one dollhouse and the furniture for it goes in storage.

Outside of my room you’d never know I lived in this house.

But if I could find an enclosed, cat safe, display case I could put that in a common room and fill it with Monsters.

If I didn’t want to keep the 2 Jacksons I have left, they look like mirror twins with their parts, one would make a good Robert Smith doll. Draculaura with repainted eyes would be a good Mary.

And a note to self it looks like the Heidi Ott dolls have kind of dried up and perhaps that’s good. You wanted that dollhouse kit for your Doctors any way as you have Steampunkish dreams for it.

2 notes

·

View notes

Text

Transiting Sun enters Scorpio

October 22 - November 22, 2017

The transiting Sun is said to shed light on the various sections of our birth charts, with the relevant Zodiac sign acting as a filter. What does the filtered light look like in secretive Scorpio? Given the sign’s reputation, it could be black light, it could be completely dark, it could be just a normal situation with “hiding in plain sight.” Gotta be ready for anything. It’s one long month of whistling in the dark, while Hallowe’en bats and ghoulies flit about menacingly.

After gliding elegantly through a month of pretty, polite Libra, we’re ready for some down-and-dirty icky stickiness. Bloch and George’s Scorpio key phrase is, “My need for deep involvements and intense transformations.” We’ve moved from the wedding ceremony to the “consummation,” to a rawer and more emotionally honest approach to self-expression.

There is, of course, the Scorpio reputation for sexiness. This is the time of year when - if the aspects are there - we can find ourselves mysteriously, powerfully drawn to - something. (And if Sun/Scorpio aspects your Ascendant, you’re going to find people mysteriously, powerfully drawn to you.) “Something” is not necessarily going to be a person; it could be an idea or concept, God/dess, food, cashmere, an occult field - endless possibilities.

The aspects are again evenly balanced between “good” and “bad,” with a slight leaning toward “good.” We’ll find ourselves with many cathartic opportunities to forgive, to transform problems into assets, and to uncover our hidden talents and strengths.

Problems we may encounter involve parental disapproval and/or overinvolvement, with perhaps some old wounds ready to be cauterized and healed. We may also become overbearing parents, ourselves. Let the kid grow up and make her/his own mistakes! She/He won’t repeat your own mistakes because she/he isn’t you.

Celebrities with Sun in Scorpio:

Mark Ruffalo, Leonardo DiCaprio, Katy Perry, Jodie Foster, Julia Roberts, Bill Gates, Grace Kelly, Ryan Gosling, Aishwarya Rai, Drake, Pablo Picasso, Bjork, Ryan Reynolds, Anne Hathaway, Emma Stone, Marie Curie, Marie Antoinette, Gordon Ramsay, Lorde, Vivien Leigh, RuPaul, Albert Camus, Fyodor Dostoyevsky, Sylvia Plath, Martin Scorsese, Whoopi Goldberg, Voltaire, Astrid Lindgren

Thursday, October 26, Jupiter/Scorpio conjunct Sun/Scorpio, 3:31

Maybe the mildest form this can take is you, eating all the Hallowe’en candy?! It’s the beginning of the yearly Sun-Jupiter cycle, in passionate and intense Scorpio - there, there, we know you needed all those mini Trix bars. You may also be in the mood to set some ambitious long-term goals today, in the spirit of “Why the hell not?” House position, as usual, gives the necessary direction for your ambitions. Why the hell not?

Planets/Points affected lie between 2:31 and 4:31 of the signs Taurus*, Cancer, Leo*, Virgo, Scorpio, Capricorn, Aquarius*, and Pisces.

Saturday, October 28, Pallas Rx/Taurus opposite Sun/Scorpio, 5:44

Self-doubt, problems with (probably) Dad, and/or issues of mentorship arise. We can be headstrong and insistent that only we know the correct path, as well. It’s tricky to be open to advice without committing yourself to take it - we don’t want to seem rude by refusing to follow it. And, we need to learn the strategic trick of knowing when to hang on and when to let go.

Planets/Points affected lie between 4:44 and 6:44 of the fixed signs Taurus*, Leo*, Scorpio*, and Aquarius*; and between 19:44 and 21:44 of the mutable signs Gemini*, Virgo*, Sagittarius*, and Pisces*.

Friday, November 3, Neptune Rx/Pisces trine Sun/Scorpio, 11:33

On the eve of the Taurus Full Moon, we have this beautiful, flowing trine to get us in the mood. Redemptive spirituality is the name of the game, and we can more than find it in our hearts to forgive and to love even more powerfully. At the very least, listen to uplifting music or go to a museum! The downside (ugh) is the possibility of losing oneself in a very powerful illusion. The Taurus Moon should be “enough” to keep us nice and grounded, but be careful nevertheless.

Planets/Points affected lie between 10:33 and 12:33 of the yin signs Taurus, Cancer, Virgo, Scorpio, Capricorn, and Pisces.

Saturday, November 4, Ceres/Leo square Sun/Scorpio, 12:41

Cut the damned apron strings already. Whether or not you’ve tethered yourself to your parents, or to your kids, stop! So much of our nurturing ability depends on the condition of our own self-worth. Perhaps we could take this intensity, this almost desperation to do right by our kids, and apply it to our own “inner child.” Like the Neptune trine, this is bound up with the Taurus Full Moon - go ahead and give yourself the TLC you usually bestow upon others.

Planets/Points affected lie between 11:41 and 13:41 of the fixed signs Taurus*, Leo*, Scorpio*, and Aquarius*; and between 26:41 and 28:41 of the mutable signs Gemini*, Virgo*, Sagittarius*, and Pisces*.

Wednesday, November 8, Juno/Capricorn sextile Sun/Scorpio, 16:08;

Thursday, November 9, Pluto/Capricorn sextile Sun/Scorpio, 17:16

Both Juno and Pluto are associated with Scorpio, which makes this a very uxorious couple of days. Go on, look it up. If we’re in a relationship, this energy is fantastic for building trust, and for committing to common goals. Those of us who are single can use the vibes to work on behalf of the powerless (a Juno “thing,” which the Sun and Pluto are more than fine with). And although there’s a chance of becoming a little too cold-blooded about it, we can look around for potential partners today.

Planets/Points affected lie between 15:08 and 18:16 of the yin signs Taurus, Cancer, Virgo, Scorpio, Capricorn, and Pisces.

Saturday, November 11, North Node/Leo square Sun/Scorpio, 19:33;

South Node/Aquarius square Sun/Scorpio, 19:33

The Scorpio pitfalls of negativity, scorched-earth style destructiveness, suspicion, and cruelty serve to trip us up - those nastier traits get in our way of being and doing our best. Whether or not we’re reluctant to give up the idea of our own importance in the overall Cosmos - and on some level we’re all at least a bit pissed that we aren’t in complete control of Everything - we’re incapable of covering all the bases; we’re far too weak and puny for even the most tentative grasp of how “things” ought to be. We need to clean up our own acts, before bending the Universe to our whims.

Planets/Points affected lie between 18:33 and 20:33 of the fixed signs Taurus*, Leo*, Scorpio*, and Aquarius*; and between 3:33 and 5:33 of the cardinal signs Aries*, Cancer*, Libra*, and Capricorn*.

Thursday, November 16, Chiron Rx/Pisces trine Sun/Scorpio, 24:28

Today’s vibes are most auspicious for warm fuzzy feelings - we also get Venus trine Neptune, maturing a mere 27 minutes before this trine does! It’s almost like US Thanksgiving Day a week early, with a little Valentine’s Day thrown in as well. Redemptive spirituality! The danger, of course, is that rose-colored glasses aren’t necessarily conducive to successfully navigating a working day. We aren’t quite as grounded as we’d like to be. Still, Scorpio’s control-freak tendencies (as well as its cynicism) will probably keep life from becoming too impractically euphoric.

Planets/Points affected lie between 23:28 and 25:28 of the yin signs Taurus, Cancer, Virgo, Scorpio, Capricorn, and Pisces.

31 notes

·

View notes

Text

4.7% Dividend Champion Looks Like A Buy

New Post has been published on http://web-hosting-top12.com/2018/08/23/4-7-dividend-champion-looks-like-a-buy/

4.7% Dividend Champion Looks Like A Buy

This research report was produced by The REIT Forum with assistance from Big Dog Investments.

Altria Group’s (MO) share price has struggled over the last year. The fundamentals for the tobacco giant remains strong.

The weakness in the share prices should be viewed simply as a buying opportunity. Management continues to forecast aggressive growth over the next few years and solid growth well into the future. They were asked on the Q2 earnings call about their growth in the coming years:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay, thanks, and then just one final quick question for me on your guidance. The revised guidance certainly suggests you have increased visibility for the year, but I’m curious if you still expect that your EPS growth rates in FY 2019 and 2020 will be above your long-term 7% to 9% EPS growth aspirations, as you stated earlier this year. Thanks.

Howard A. Willard – Altria Group, Inc.

At this point, there’s no change to that expectation.

Altria Group’s earnings could be pressured modestly from the domestic release of IQOS. Their marketing expenses should run significantly higher around the release time. Getting customers familiar with the product will be important Altria Group. Here was a great Q&A from the earnings call:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay. That’s helpful. And then switching over to IQOS, and just maybe any update on timing of approval. I know you touched on this, but it just seems like you might think it could be any day now based on your remarks. And I guess I’m also suggesting this, and I’m aware that you guys have been certainly trying to secure additional shelf space at retail. So, I’d like to hear it from you how you think these efforts have gone, and then are you getting the space you need for IQOS? And has it been mainly incremental?

And then finally on this topic, I just would like to hear how you guys are thinking about the rollout of IQOS, now that BAT just received substantial equivalent approval from the FDA for their Eclipse heat-not-burn product. So, just wondering how you think about the positioning of IQOS relative to that brand, and are you concerned at all that IQOS may lose its first-mover advantage?

Howard A. Willard – Altria Group, Inc.

Sure. I’ll start off with the fact that we have been ready for quite some time to launch IQOS into the U.S. market, and we are really just waiting for FDA approval. And as is often the case with FDA, they move at their own pace. So, I don’t know that we can make a good forecast of that, but we certainly have taken advantage of the time we’ve had to make sure that we’ve got a very solid launch plan for IQOS in the U.S. market. We’ve been learning from all of the experiences that PMI has had overseas, and we will be ready with a very compelling marketing offering in the marketplace.

You are right that we have been contracting to gain additional space for innovative products at retail. And certainly that space would be available for IQOS, for e-vapor, and for a range of other innovative products we’re bringing to the marketplace. We think that would give us plenty of room to display the portfolio of products that we have in the marketplace, and we’ve been quite pleased with our success in securing that space.

I did read in the BAT announcement about the SE they got on what I guess is an improved version of the Reynolds product. And I think in some respects, probably there’s some benefit to having a number of different heated tobacco products in the market. And I have to tell you, given the success that the IQOS heat-not-burn format has had around the world, I’m happy to compete in the market with IQOS against that BAT product. And we’re just eager for the opportunity to begin marketing.

We are bullish on Altria Group because the company is trading at a low multiple of earnings and carries a high dividend yield. Further, we expect earnings growth to continue at a significant rate for at least the next few years. We believe the temporary pressure on margins from introducing IQOS will give way to greater earnings growth in future periods. We believe it is likely that the FDA will support IQOS as a reduced risk technology and encourage more smokers to switch to IQOS. Philip Morris (PM) has seen great success with the IQOS product internationally. Take Korea for example:

Source: PM

This growth is not unique to Korea. Here’s the EU region:

Source: PM

Japan has also seen exceptional growth. Analyst projections had IQOS sale growing at a massive rate. Reductions in their expectations for growth drove share prices lower.

More reasons to like Altria Group

MO has great margins:

Source: MO

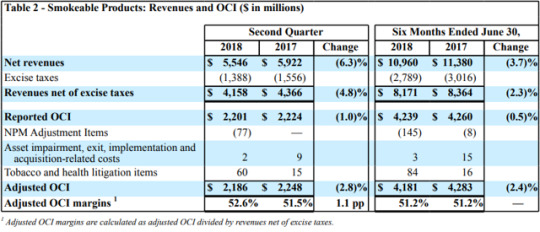

MO has great margins which is a positive for the company. However, there has been a decline in net revenues as lower volume was partially offset by higher pricing and lower promotional investments. There has also been a decline in reported OCI:

Source: MO

There has been a decline across the cigarette category, so the decline here makes sense. MO also lapped the California state excise tax increase to further exacerbate the decline. However, MO still raised the lower end of their guidance for 2018. It is now $3.94 to $4.03.

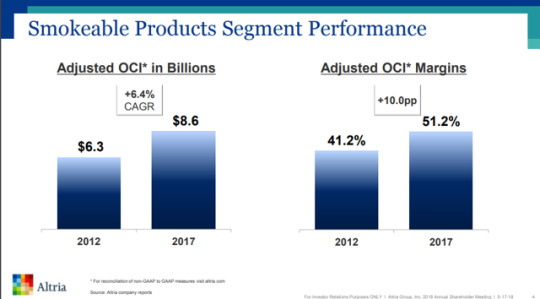

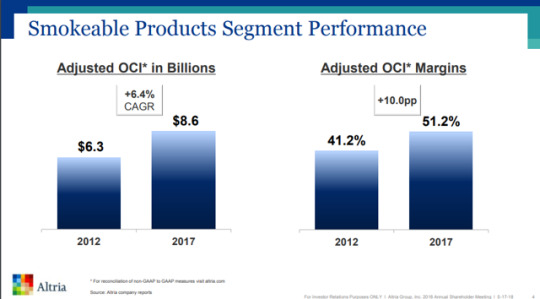

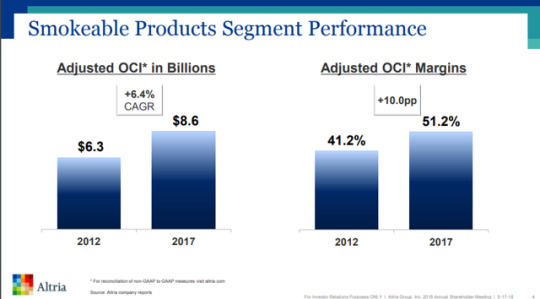

If we’re looking at the big picture, MO has a massive market share and continues to perform with their smokeable products:

Source: MO

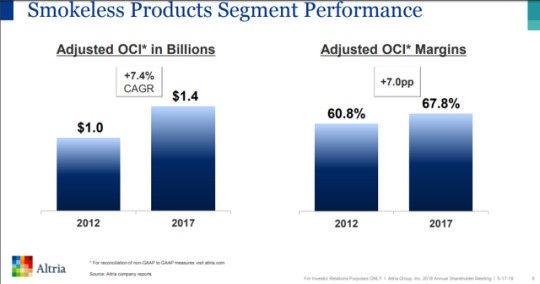

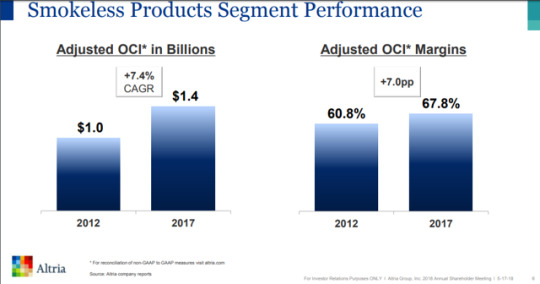

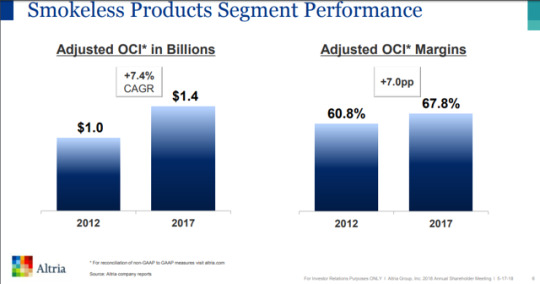

They’ve also had success with their smokeless products:

Source: MO

With Altria Group’s price decline recently, the company capitalized on the market overreaction by repurchasing approximately 7.6 million shares during the second quarter at an average share price of $57.65. This is a way for management to reward shareholders. In May, the board authorized another $1 billion towards the repurchase program. Altria Group management expects their current $2 billion ($1 billion remaining) repurchase program to be complete in Q2 2019.

Finals thoughts

The growth in margins should provide a little extra tailwind for MO after the initial marketing expenses. Further, Altria Group is repurchasing their stock at a very attractive price. The reduction in shares outstanding drives further growth in earnings and operating cash flows per share. Some investors think buying back stock is financial engineering, but it is a powerful way to improve dividend growth per share. When a dividend champion trades at a high dividend yield and is easily covering the dividend, they should repurchase some of their shares to reduce the total dividends they need to pay.

If you enjoyed reading this article and want to receive updates on our latest research, click “Follow” next to my name at the top of this article.

CWMF’s The REIT Forum

Prices will be going up on September 1st

The REIT Forum is a service dedicated to equity REITs, mortgage REITs, preferred shares, and the occasional dividend champions. We focus on income, retirement, and trading opportunities. If you’re looking to invest in REITs, The REIT Forum will give you subsector analysis along with a deep dive on the individual companies and their fundamentals.

Here are our 2 newest 5-star reviews to add to the collection of 70+ 5 stars:

Subscribing to The REIT Forum includes access to spreadsheets comparing every security we cover, along with a look at CWMF’s personal portfolio updated in real-time. It is our objective to find the best investments at the best entry price. Don’t miss the next real-time alert! You can try out our service, or find more information, by clicking HERE.

Disclosure: I am/we are long MO, PM.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 notes

Text

4.7% Dividend Champion Looks Like A Buy

New Post has been published on http://web-hosting-top12.com/2018/08/23/4-7-dividend-champion-looks-like-a-buy/

4.7% Dividend Champion Looks Like A Buy

This research report was produced by The REIT Forum with assistance from Big Dog Investments.

Altria Group’s (MO) share price has struggled over the last year. The fundamentals for the tobacco giant remains strong.

The weakness in the share prices should be viewed simply as a buying opportunity. Management continues to forecast aggressive growth over the next few years and solid growth well into the future. They were asked on the Q2 earnings call about their growth in the coming years:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay, thanks, and then just one final quick question for me on your guidance. The revised guidance certainly suggests you have increased visibility for the year, but I’m curious if you still expect that your EPS growth rates in FY 2019 and 2020 will be above your long-term 7% to 9% EPS growth aspirations, as you stated earlier this year. Thanks.

Howard A. Willard – Altria Group, Inc.

At this point, there’s no change to that expectation.

Altria Group’s earnings could be pressured modestly from the domestic release of IQOS. Their marketing expenses should run significantly higher around the release time. Getting customers familiar with the product will be important Altria Group. Here was a great Q&A from the earnings call:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay. That’s helpful. And then switching over to IQOS, and just maybe any update on timing of approval. I know you touched on this, but it just seems like you might think it could be any day now based on your remarks. And I guess I’m also suggesting this, and I’m aware that you guys have been certainly trying to secure additional shelf space at retail. So, I’d like to hear it from you how you think these efforts have gone, and then are you getting the space you need for IQOS? And has it been mainly incremental?

And then finally on this topic, I just would like to hear how you guys are thinking about the rollout of IQOS, now that BAT just received substantial equivalent approval from the FDA for their Eclipse heat-not-burn product. So, just wondering how you think about the positioning of IQOS relative to that brand, and are you concerned at all that IQOS may lose its first-mover advantage?

Howard A. Willard – Altria Group, Inc.

Sure. I’ll start off with the fact that we have been ready for quite some time to launch IQOS into the U.S. market, and we are really just waiting for FDA approval. And as is often the case with FDA, they move at their own pace. So, I don’t know that we can make a good forecast of that, but we certainly have taken advantage of the time we’ve had to make sure that we’ve got a very solid launch plan for IQOS in the U.S. market. We’ve been learning from all of the experiences that PMI has had overseas, and we will be ready with a very compelling marketing offering in the marketplace.

You are right that we have been contracting to gain additional space for innovative products at retail. And certainly that space would be available for IQOS, for e-vapor, and for a range of other innovative products we’re bringing to the marketplace. We think that would give us plenty of room to display the portfolio of products that we have in the marketplace, and we’ve been quite pleased with our success in securing that space.

I did read in the BAT announcement about the SE they got on what I guess is an improved version of the Reynolds product. And I think in some respects, probably there’s some benefit to having a number of different heated tobacco products in the market. And I have to tell you, given the success that the IQOS heat-not-burn format has had around the world, I’m happy to compete in the market with IQOS against that BAT product. And we’re just eager for the opportunity to begin marketing.

We are bullish on Altria Group because the company is trading at a low multiple of earnings and carries a high dividend yield. Further, we expect earnings growth to continue at a significant rate for at least the next few years. We believe the temporary pressure on margins from introducing IQOS will give way to greater earnings growth in future periods. We believe it is likely that the FDA will support IQOS as a reduced risk technology and encourage more smokers to switch to IQOS. Philip Morris (PM) has seen great success with the IQOS product internationally. Take Korea for example:

Source: PM

This growth is not unique to Korea. Here’s the EU region:

Source: PM

Japan has also seen exceptional growth. Analyst projections had IQOS sale growing at a massive rate. Reductions in their expectations for growth drove share prices lower.

More reasons to like Altria Group

MO has great margins:

Source: MO

MO has great margins which is a positive for the company. However, there has been a decline in net revenues as lower volume was partially offset by higher pricing and lower promotional investments. There has also been a decline in reported OCI:

Source: MO

There has been a decline across the cigarette category, so the decline here makes sense. MO also lapped the California state excise tax increase to further exacerbate the decline. However, MO still raised the lower end of their guidance for 2018. It is now $3.94 to $4.03.

If we’re looking at the big picture, MO has a massive market share and continues to perform with their smokeable products:

Source: MO

They’ve also had success with their smokeless products:

Source: MO

With Altria Group’s price decline recently, the company capitalized on the market overreaction by repurchasing approximately 7.6 million shares during the second quarter at an average share price of $57.65. This is a way for management to reward shareholders. In May, the board authorized another $1 billion towards the repurchase program. Altria Group management expects their current $2 billion ($1 billion remaining) repurchase program to be complete in Q2 2019.

Finals thoughts

The growth in margins should provide a little extra tailwind for MO after the initial marketing expenses. Further, Altria Group is repurchasing their stock at a very attractive price. The reduction in shares outstanding drives further growth in earnings and operating cash flows per share. Some investors think buying back stock is financial engineering, but it is a powerful way to improve dividend growth per share. When a dividend champion trades at a high dividend yield and is easily covering the dividend, they should repurchase some of their shares to reduce the total dividends they need to pay.

If you enjoyed reading this article and want to receive updates on our latest research, click “Follow” next to my name at the top of this article.

CWMF’s The REIT Forum

Prices will be going up on September 1st

The REIT Forum is a service dedicated to equity REITs, mortgage REITs, preferred shares, and the occasional dividend champions. We focus on income, retirement, and trading opportunities. If you’re looking to invest in REITs, The REIT Forum will give you subsector analysis along with a deep dive on the individual companies and their fundamentals.

Here are our 2 newest 5-star reviews to add to the collection of 70+ 5 stars:

Subscribing to The REIT Forum includes access to spreadsheets comparing every security we cover, along with a look at CWMF’s personal portfolio updated in real-time. It is our objective to find the best investments at the best entry price. Don’t miss the next real-time alert! You can try out our service, or find more information, by clicking HERE.

Disclosure: I am/we are long MO, PM.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 notes

Text

4.7% Dividend Champion Looks Like A Buy

New Post has been published on http://web-hosting-top12.com/2018/08/23/4-7-dividend-champion-looks-like-a-buy/

4.7% Dividend Champion Looks Like A Buy

This research report was produced by The REIT Forum with assistance from Big Dog Investments.

Altria Group’s (MO) share price has struggled over the last year. The fundamentals for the tobacco giant remains strong.

The weakness in the share prices should be viewed simply as a buying opportunity. Management continues to forecast aggressive growth over the next few years and solid growth well into the future. They were asked on the Q2 earnings call about their growth in the coming years:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay, thanks, and then just one final quick question for me on your guidance. The revised guidance certainly suggests you have increased visibility for the year, but I’m curious if you still expect that your EPS growth rates in FY 2019 and 2020 will be above your long-term 7% to 9% EPS growth aspirations, as you stated earlier this year. Thanks.

Howard A. Willard – Altria Group, Inc.

At this point, there’s no change to that expectation.

Altria Group’s earnings could be pressured modestly from the domestic release of IQOS. Their marketing expenses should run significantly higher around the release time. Getting customers familiar with the product will be important Altria Group. Here was a great Q&A from the earnings call:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay. That’s helpful. And then switching over to IQOS, and just maybe any update on timing of approval. I know you touched on this, but it just seems like you might think it could be any day now based on your remarks. And I guess I’m also suggesting this, and I’m aware that you guys have been certainly trying to secure additional shelf space at retail. So, I’d like to hear it from you how you think these efforts have gone, and then are you getting the space you need for IQOS? And has it been mainly incremental?

And then finally on this topic, I just would like to hear how you guys are thinking about the rollout of IQOS, now that BAT just received substantial equivalent approval from the FDA for their Eclipse heat-not-burn product. So, just wondering how you think about the positioning of IQOS relative to that brand, and are you concerned at all that IQOS may lose its first-mover advantage?

Howard A. Willard – Altria Group, Inc.

Sure. I’ll start off with the fact that we have been ready for quite some time to launch IQOS into the U.S. market, and we are really just waiting for FDA approval. And as is often the case with FDA, they move at their own pace. So, I don’t know that we can make a good forecast of that, but we certainly have taken advantage of the time we’ve had to make sure that we’ve got a very solid launch plan for IQOS in the U.S. market. We’ve been learning from all of the experiences that PMI has had overseas, and we will be ready with a very compelling marketing offering in the marketplace.

You are right that we have been contracting to gain additional space for innovative products at retail. And certainly that space would be available for IQOS, for e-vapor, and for a range of other innovative products we’re bringing to the marketplace. We think that would give us plenty of room to display the portfolio of products that we have in the marketplace, and we’ve been quite pleased with our success in securing that space.

I did read in the BAT announcement about the SE they got on what I guess is an improved version of the Reynolds product. And I think in some respects, probably there’s some benefit to having a number of different heated tobacco products in the market. And I have to tell you, given the success that the IQOS heat-not-burn format has had around the world, I’m happy to compete in the market with IQOS against that BAT product. And we’re just eager for the opportunity to begin marketing.

We are bullish on Altria Group because the company is trading at a low multiple of earnings and carries a high dividend yield. Further, we expect earnings growth to continue at a significant rate for at least the next few years. We believe the temporary pressure on margins from introducing IQOS will give way to greater earnings growth in future periods. We believe it is likely that the FDA will support IQOS as a reduced risk technology and encourage more smokers to switch to IQOS. Philip Morris (PM) has seen great success with the IQOS product internationally. Take Korea for example:

Source: PM

This growth is not unique to Korea. Here’s the EU region:

Source: PM

Japan has also seen exceptional growth. Analyst projections had IQOS sale growing at a massive rate. Reductions in their expectations for growth drove share prices lower.

More reasons to like Altria Group

MO has great margins:

Source: MO

MO has great margins which is a positive for the company. However, there has been a decline in net revenues as lower volume was partially offset by higher pricing and lower promotional investments. There has also been a decline in reported OCI:

Source: MO

There has been a decline across the cigarette category, so the decline here makes sense. MO also lapped the California state excise tax increase to further exacerbate the decline. However, MO still raised the lower end of their guidance for 2018. It is now $3.94 to $4.03.

If we’re looking at the big picture, MO has a massive market share and continues to perform with their smokeable products:

Source: MO

They’ve also had success with their smokeless products:

Source: MO

With Altria Group’s price decline recently, the company capitalized on the market overreaction by repurchasing approximately 7.6 million shares during the second quarter at an average share price of $57.65. This is a way for management to reward shareholders. In May, the board authorized another $1 billion towards the repurchase program. Altria Group management expects their current $2 billion ($1 billion remaining) repurchase program to be complete in Q2 2019.

Finals thoughts

The growth in margins should provide a little extra tailwind for MO after the initial marketing expenses. Further, Altria Group is repurchasing their stock at a very attractive price. The reduction in shares outstanding drives further growth in earnings and operating cash flows per share. Some investors think buying back stock is financial engineering, but it is a powerful way to improve dividend growth per share. When a dividend champion trades at a high dividend yield and is easily covering the dividend, they should repurchase some of their shares to reduce the total dividends they need to pay.

If you enjoyed reading this article and want to receive updates on our latest research, click “Follow” next to my name at the top of this article.

CWMF’s The REIT Forum

Prices will be going up on September 1st

The REIT Forum is a service dedicated to equity REITs, mortgage REITs, preferred shares, and the occasional dividend champions. We focus on income, retirement, and trading opportunities. If you’re looking to invest in REITs, The REIT Forum will give you subsector analysis along with a deep dive on the individual companies and their fundamentals.

Here are our 2 newest 5-star reviews to add to the collection of 70+ 5 stars:

Subscribing to The REIT Forum includes access to spreadsheets comparing every security we cover, along with a look at CWMF’s personal portfolio updated in real-time. It is our objective to find the best investments at the best entry price. Don’t miss the next real-time alert! You can try out our service, or find more information, by clicking HERE.

Disclosure: I am/we are long MO, PM.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 notes

Text

4.7% Dividend Champion Looks Like A Buy

New Post has been published on http://unchainedmusic.com/4-7-dividend-champion-looks-like-a-buy/

4.7% Dividend Champion Looks Like A Buy

This research report was produced by The REIT Forum with assistance from Big Dog Investments.

Altria Group’s (MO) share price has struggled over the last year. The fundamentals for the tobacco giant remains strong.

The weakness in the share prices should be viewed simply as a buying opportunity. Management continues to forecast aggressive growth over the next few years and solid growth well into the future. They were asked on the Q2 earnings call about their growth in the coming years:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay, thanks, and then just one final quick question for me on your guidance. The revised guidance certainly suggests you have increased visibility for the year, but I’m curious if you still expect that your EPS growth rates in FY 2019 and 2020 will be above your long-term 7% to 9% EPS growth aspirations, as you stated earlier this year. Thanks.

Howard A. Willard – Altria Group, Inc.

At this point, there’s no change to that expectation.

Altria Group’s earnings could be pressured modestly from the domestic release of IQOS. Their marketing expenses should run significantly higher around the release time. Getting customers familiar with the product will be important Altria Group. Here was a great Q&A from the earnings call:

Bonnie L. Herzog – Wells Fargo Securities LLC

Okay. That’s helpful. And then switching over to IQOS, and just maybe any update on timing of approval. I know you touched on this, but it just seems like you might think it could be any day now based on your remarks. And I guess I’m also suggesting this, and I’m aware that you guys have been certainly trying to secure additional shelf space at retail. So, I’d like to hear it from you how you think these efforts have gone, and then are you getting the space you need for IQOS? And has it been mainly incremental?

And then finally on this topic, I just would like to hear how you guys are thinking about the rollout of IQOS, now that BAT just received substantial equivalent approval from the FDA for their Eclipse heat-not-burn product. So, just wondering how you think about the positioning of IQOS relative to that brand, and are you concerned at all that IQOS may lose its first-mover advantage?

Howard A. Willard – Altria Group, Inc.

Sure. I’ll start off with the fact that we have been ready for quite some time to launch IQOS into the U.S. market, and we are really just waiting for FDA approval. And as is often the case with FDA, they move at their own pace. So, I don’t know that we can make a good forecast of that, but we certainly have taken advantage of the time we’ve had to make sure that we’ve got a very solid launch plan for IQOS in the U.S. market. We’ve been learning from all of the experiences that PMI has had overseas, and we will be ready with a very compelling marketing offering in the marketplace.

You are right that we have been contracting to gain additional space for innovative products at retail. And certainly that space would be available for IQOS, for e-vapor, and for a range of other innovative products we’re bringing to the marketplace. We think that would give us plenty of room to display the portfolio of products that we have in the marketplace, and we’ve been quite pleased with our success in securing that space.

I did read in the BAT announcement about the SE they got on what I guess is an improved version of the Reynolds product. And I think in some respects, probably there’s some benefit to having a number of different heated tobacco products in the market. And I have to tell you, given the success that the IQOS heat-not-burn format has had around the world, I’m happy to compete in the market with IQOS against that BAT product. And we’re just eager for the opportunity to begin marketing.

We are bullish on Altria Group because the company is trading at a low multiple of earnings and carries a high dividend yield. Further, we expect earnings growth to continue at a significant rate for at least the next few years. We believe the temporary pressure on margins from introducing IQOS will give way to greater earnings growth in future periods. We believe it is likely that the FDA will support IQOS as a reduced risk technology and encourage more smokers to switch to IQOS. Philip Morris (PM) has seen great success with the IQOS product internationally. Take Korea for example:

Source: PM

This growth is not unique to Korea. Here’s the EU region:

Source: PM

Japan has also seen exceptional growth. Analyst projections had IQOS sale growing at a massive rate. Reductions in their expectations for growth drove share prices lower.

More reasons to like Altria Group

MO has great margins:

Source: MO

MO has great margins which is a positive for the company. However, there has been a decline in net revenues as lower volume was partially offset by higher pricing and lower promotional investments. There has also been a decline in reported OCI:

Source: MO

There has been a decline across the cigarette category, so the decline here makes sense. MO also lapped the California state excise tax increase to further exacerbate the decline. However, MO still raised the lower end of their guidance for 2018. It is now $3.94 to $4.03.

If we’re looking at the big picture, MO has a massive market share and continues to perform with their smokeable products:

Source: MO

They’ve also had success with their smokeless products:

Source: MO

With Altria Group’s price decline recently, the company capitalized on the market overreaction by repurchasing approximately 7.6 million shares during the second quarter at an average share price of $57.65. This is a way for management to reward shareholders. In May, the board authorized another $1 billion towards the repurchase program. Altria Group management expects their current $2 billion ($1 billion remaining) repurchase program to be complete in Q2 2019.

Finals thoughts

The growth in margins should provide a little extra tailwind for MO after the initial marketing expenses. Further, Altria Group is repurchasing their stock at a very attractive price. The reduction in shares outstanding drives further growth in earnings and operating cash flows per share. Some investors think buying back stock is financial engineering, but it is a powerful way to improve dividend growth per share. When a dividend champion trades at a high dividend yield and is easily covering the dividend, they should repurchase some of their shares to reduce the total dividends they need to pay.

If you enjoyed reading this article and want to receive updates on our latest research, click “Follow” next to my name at the top of this article.

CWMF’s The REIT Forum

Prices will be going up on September 1st

The REIT Forum is a service dedicated to equity REITs, mortgage REITs, preferred shares, and the occasional dividend champions. We focus on income, retirement, and trading opportunities. If you’re looking to invest in REITs, The REIT Forum will give you subsector analysis along with a deep dive on the individual companies and their fundamentals.

Here are our 2 newest 5-star reviews to add to the collection of 70+ 5 stars:

Subscribing to The REIT Forum includes access to spreadsheets comparing every security we cover, along with a look at CWMF’s personal portfolio updated in real-time. It is our objective to find the best investments at the best entry price. Don’t miss the next real-time alert! You can try out our service, or find more information, by clicking HERE.

Disclosure: I am/we are long MO, PM.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 notes

Text

Alabama Republicans Threaten Retaliation for Disloyalty to Moore

New Post has been published on http://usnewsaggregator.com/alabama-republicans-threaten-retaliation-for-disloyalty-to-moore/

Alabama Republicans Threaten Retaliation for Disloyalty to Moore

WASHINGTON — Republicans in Washington may be abandoning Roy Moore by the droves. But in Alabama, the GOP has Moore’s back and is threatening retribution against defectors.

The chairwoman of the Alabama Republican Party warned she’s ready to enforce strict rules on party purity in the state’s Senate race, even if it means kicking GOP candidates off the ballot in future elections.

“It would be a serious error for any current elected GOP official or candidate to publicly endorse another party’s candidate, an independent, a third party or a write in candidate in a general election as well,” Alabama GOP Chairwoman Terry Lathan told the Alabama Political Reporter. “I have heard of no GOP elected official or candidate that is even considering this option.”

A write-in is one of the only ways Republican opponents could stop Moore at this point, since it’s too late to change the ballots.

Lathan did not respond to requests for comment but the threat is being taken seriously in Alabama, since party rules — as Lathan pointedly noted — can be severe.

Alabama GOP bylaws give the party “the right to deny ballot access to a candidate for public office” to any elected official who “either publicly participated in the primary election of another political party or publicly supported a nominee of another political party.”

The provision applies for six years, meaning Alabama Republican officeholders who run against Moore or support a challenger could theoretically be barred from running again on the Republican ticket until 2023 — a political death sentence in deep-red Alabama.

“As long as Roy Moore is our nominee, a Republican cannot wage a write-in campaign under Alabama Republican Party rules and be on the ballot as a Republican in the future,” Rep. Mo Brooks, R-Ala., told reporters when asked if he was considering a run himself.

Related: Desperate GOP Looks to Write-In Candidate to Beat Moore

But Alabama Republicans likely don’t need much arm-twisting anyway to stick with Moore through the December 12 election.

Even as their counterparts in Washington ramp up pressure on the Senate candidate following recent allegations of sexual misconduct, few if any prominent Republicans inside Alabama have split with Moore, exposing a major rift between the state and national parties.

Moore, who has denied all the allegations, was defiant Tuesday after Senate Majority Mitch McConnell called him “obviously not fit to be in the United States Senate.”

McConnell at the Bat

Republican Primary 8/15: STRIKE 1

Republican Runoff 9/26: STRIKE 2

General Election 12/12: TBD

3 STRIKES AND YOU’RE OUT, MITCH. #ALSEN

— Judge Roy Moore (@MooreSenate) November 14, 2017

The Republican National Committee dropped out of a joint fundraising agreement with Moore late Tuesday, according to a document filed with the FEC. It also ended its field operations in the state, where it deployed 11 operatives, NBC News confirmed.

That leaves Moore’s campaign and the Alabama Republican Party alone in the fundraising arrangement.

Some Alabama Republicans think the pressure from Washington will only help Moore energize his base, noting he beat McConnell’s favored candidate by 9 percentage points in the party primary by running against the GOP establishment.

Paul Reynolds, a Republican National Committeeman from Alabama, said any Alabama Republican who wages a write-in campaign against Moore could kiss their career in the state politics goodbye

“The next move they’d try to make is to find a home in the metro Atlanta area and get out of the state, because they’d be dead politically here,” Reynolds said.

Alabama Republicans, regardless of how they personally feel about Moore, are also keenly aware that they will have to appeal to the same voters who are currently sticking with him in their own primaries next year.

Related: Sexual Harassment Spotlight Shines on Capitol Hill

“This is the political tightrope of the century,” said Alabama GOP strategist David Ferguson. “How do these elected officials answer the allegations against Roy Moore, in a hyper-political environment, without isolating their Republican base and without disregarding the very serious charges that are on the table all seven months before another heated round of statewide primaries?”

At an appearance Tuesday evening at the “God Save America Revival Conference” at a Baptist Church in Jackson, Moore portrayed himself as standing up for religious liberty against critics from the establishment GOP and Democrats. He only directly mentioned the allegations at one point in the around 30-minute speech.

“What do you think I’m going to do? Why do you think they’re giving me this trouble? Why do you think I’m being harassed by media — and by people pushing forth allegations, in the last 28 days of this election?” Moore asked the congregation.

“After 40-something years of fighting this battle, I’m now facing allegations — and that’s all the press wants to talk about,” he said. “But I want to talk about the issues. I want to talk about where this country’s going, and if we don’t come back to God, we’re not going anywhere.”

He told the crowd at Walker Springs Road Baptist Church that “obviously I’ve made a few people mad — I’m the only one that can unite Democrats and Republicans, because I seem to be opposed by both.”

“They’ve done everything they could, and now they’re together, to try to keep me from going to Washington,” he said.

Also Tuesday, it was revealed that at least one person in Alabama received a robocall from someone claiming to be a reporter for the Washington Post seeking to pay money for claims against Moore — a fake call that was condemned by the newspaper. The call was first reported by CBS station WKRG of Mobile, who spoke to a pastor who got the call.

The newspaper denied making the call.

“The Post has just learned that at least one person in Alabama has received a call from someone falsely claiming to be from The Washington Post. The call’s description of our reporting methods bears no relationship to reality,” Post Executive Editor Marty Baron said in a statement.

“We are shocked and appalled that anyone would stoop to this level to discredit real journalism,” Baron said.

Alex Seitz-Wald and Alex Moe reported from Washington, D.C., Phil Helsel from Los Angeles, and Vaughn Hillyard from Alabama.

Original Article:

Click here

0 notes

Text

Every playoff team’s one big lineup question – SweetSpot

Let’s look at the 10 teams currently holding down a playoff position and what lineup questions they might still need to resolve as we inch closer to the postseason.

Los Angeles Dodgers: Who starts in the outfield? Depth is fun, until everyone stops hitting and the manager doesn’t know who to play. I think we can determine this: Chris Taylor will start in center field (and hit leadoff) and Yasiel Puig will start in right field. Taylor has struggled in September (.212, 19 strikeouts, three walks), but he has been the regular starter in center field ever since Joc Pederson was demoted in mid-August, making some starts at shortstop only because Corey Seager has rested a sore elbow at times.

So that leaves left field. Curtis Granderson is still the likely starter against right-handed pitchers, even though he has hit .126 in 101 plate appearances since coming over from the Mets. That’s a scary number, and I’m sure manager Dave Roberts would love to see Granderson have a couple of big games before fully committing to him. That leaves two other options in a platoon with Kike Hernandez, Cody Bellinger (with Adrian Gonzalez playing first base) or Andre Ethier. I have trouble seeing those as realistic options. Ethier has barely played the past two seasons; you don’t know how he can move out there and you’re basically expecting him to fall out of bed after two years of injuries and expect him to hit. Gonzalez doesn’t look healthy and has barely played in September; he probably doesn’t even make the postseason roster.

As an aside: Please, Dodgers fans, quit complaining that Granderson ruined the team chemistry. It’s a ridiculous and embarrassing excuse for a team-wide slump.

Washington Nationals: Who starts in the outfield? The good news is that Bryce Harper took batting practice on the field Sunday for the first time since injuring his knee in August; he did some running and said he’s aiming to be ready for Game 1 of the National League Division Series. Obviously the Nationals would love to get him some game action before then, but for now it appears he’s on target to play.

With Michael Taylor in center field, that leaves manager Dusty Baker multiple options in left field. The Nationals have started five different left fielders in September, plus three more players who started in right field. That’s eight options! The sentimental favorite would be veteran Jayson Werth, but he has hit just .133 in 13 games since returning from the disabled list in late August. Werth really hasn’t hit right-handers since 2014, so I would consider him a viable option only against lefties.

That leaves Howie Kendrick and Adam Lind as the best options. Kendrick has hit well since coming over from the Phillies, while Lind has had a terrific season as a bench bat, hitting .306/.361/.508. He hadn’t played the outfield consistently since 2010 but has started 23 games in left; his ability to hit righties means he could draw some starts out there, even as a defensive liability.

An intriguing bench option might be 20-year-old rookie Victor Robles, who could beat out Andrew Stevenson, Rafael Bautista or Alejandro De Aza for a final spot. He has only nine major league at-bats after hitting .300 in the minors with 27 steals, but his speed makes him a pinch running option. Baker hasn’t ruled out the idea of Robles making the roster. “If I didn’t think so, I wouldn’t play him at all,” Baker told MLB.com the other day.

As an aside: If Harper makes it back, Baker would be wise to hit Harper or Anthony Rendon second instead of a lesser hitter. Rendon has occupied the sixth spot for most of the season before Harper was injured.

Chicago Cubs: Where does Ian Happ play? Joe Maddon’s head might explode with all of his options. Happ has hit his way into a regular role — somewhere — with 22 home runs and a .507 slugging mark. Addison Russell just returned from his foot injury and was making Gold Glove-caliber plays at shortstop, so the Cubs’ best defensive lineup would be Russell at short and Javier Baez at second.

That could mean the switch-hitting Happ ends up in the outfield. Since returning from the minors, Kyle Schwarber has hit .253/.338/.567, and you know Maddon will want that bat in the lineup against right-handers. The power that Happ and Schwarber offer would help offset the lower OBPs Russell and Baez bring to the table. There’s also Maddon favorite Ben Zobrist and Albert Almora Jr. (.910 OPS against left-handed pitchers) to consider. Most likely scenario: Schwarber and Almora platoon in the outfield, with Happ switching back-and-forth between center and left. That leaves Zobrist, Jon Jay and Tommy La Stella coming off the bench. It’s a deep roster with lots of flexibility and pinch-hitting options.

An aside: For most of August, Maddon hit Kris Bryant third and Anthony Rizzo fourth. The past few games he has gone back to Bryant second and Rizzo third. Willson Contreras has been hot in the second half (.320/.412/.670), so Maddon might stick with him in the cleanup spot.

Arizona Diamondbacks: Is Chris Iannetta the unlikeliest No. 2 hitter for a playoff team? Yes. Iannetta hit .188 with the Angels in 2015. He hit .210 with the Mariners in 2016. Now he’s a 34-year-old catcher suddenly hitting second for the first time in his career (he has started 21 games in that spot in his career, 18 of them coming this season). Of the past 14 games he has started, 13 have seen him hitting in the 2-hole (he hit cleanup in the other game). Obviously getting away from that marine layer in Seattle and Anaheim has helped rejuvenate the bat, and he has crushed lefties in particular with a .902 OPS.

One thing to note: The odd thing about manager Torey Lovullo’s lineups is that he has Paul Goldschmidt and J.D. Martinez in the fourth and fifth spots, no matter the pitcher. Jake Lamb and A.J. Pollock rotate hitting third. Lamb, however, has collapsed in the second half (.195/.315/.369), so it would make sense to move him down and get Goldschmidt/Martinez up earlier.

Colorado Rockies: Where does Ian Desmond play? He doesn’t. The first year of a five-year, $70 million contract has been a disaster as Desmond has hit .275/.322/.368, with the hand fracture he suffered in spring training perhaps limiting his ability to drive the ball. Mark Reynolds will play first, Gerardo Parra will play left and Carlos Gonzalez, finally heating up, will play right, especially with righty Zack Greinke the likely wild-card game starter for Arizona.

As an aside, I’d bat DJ LeMahieu leadoff and Charlie Blackmon second to give Blackmon a few more runners on base, but there’s also nothing wrong with starting the game with a 1-0 lead.

Cleveland Indians: Who plays in the outfield? With Bradley Zimmer likely out for the playoffs with a broken bone in his left hand, and Michael Brantley slow to heal from his ankle injury (he hasn’t played since Aug. 8), manager Terry Francona’s options in the outfield are suddenly limited. Almost by default, it seems we’ll get Jay Bruce in right, Austin Jackson in center and Lonnie Chisenhall in left.

Jackson has primarily been used as a platoon starter this season (almost half his plate appearances have come against lefties), but without Zimmer, he’s Cleveland’s best option for center field. Chisenhall doesn’t play much against lefties — although he has hit them well in limited time this year — so the Indians will likely carry Brandon Guyer as a platoon partner, or perhaps September call-up Greg Allen, a switch-hitter who hit .356 from the right side in Double-A. Allen doesn’t have any power, but has speed and defensive ability.

All that seemed reasonably straightforward … and then Jason Kipnis returned from the DL and started in center field on Sunday. That was his first game there in the majors, but he was a center fielder in college at Arizona State. He has had a bad season, battling a strained rotator cuff coming out of spring training and then landing on the DL twice with hamstring injuries, so he might be a utility guy in the playoffs with Jose Ramirez remaining at second and Yandy Diaz at third. If he can play center, that gives Francona options such as pinch hitting for Jackson or even starting Kipnis against a right-hander. Still, the defensive problems in center that hurt the Indians last October — including the Game 7 loss to the Cubs — could mean Francona plays it safe out there.

Houston Astros: Who bats second? With Carlos Correa back, manager A.J. Hinch looks like he’s back to his preferred order of Jose Altuve hitting third and Correa cleanup. It looks like the second spot will be shared by Josh Reddick (versus right-handers) and Alex Bregman (versus lefties). Reddick has quietly had a superb season at the plate, hitting .317/.365/.483, while Bregman has had a big second half (.308/.360/.515). Hinch lost some versatility when defensive whiz Jake Marisnick fractured his thumb, so that leaves George Springer in center on a regular basis with Marwin Gonzalez and Cameron Maybin in left.

The weak spot in the lineup is actually designated hitter Carlos Beltran. If the Astros keep a third catcher, that means Evan Gattis could get some starts there.