#i’m honestly not sure if even does. they might have pre-getting launched into a pocket dimension war. they really might have.

Text

even has killed people—though perhaps that depends on your definition of people—and it’s not. how do i put it. it’s never cool, you know? it’s never a moment where this puts them in control of a situation, where they can show off some skill in putting someone down. because even is not, generally, very powerful, and they do not know how to do this.

it just gets messy.

which is one of those terrible reasons why they… well, they don’t like the master, but they have to like that she can do it easy, quick, clean. she can give even the ability to, as well, when she wants. if for no other reason than it means that they won’t have to scrub it raw off their skin later, they appreciate that.

#but if left to their own devices?#what im saying i think is: the doctor 🤝 even: has killed someone with a rock#and of course i say whatever your definition of people is because you’d have to ask if you count daleks as people#i’m honestly not sure if even does. they might have pre-getting launched into a pocket dimension war. they really might have.#very expansive definition of people on account of them not really feeling like they should count as one anyway so therefore if they do. lots#of things must. including the murder trash cans. they’re flesh on the inside aren’t they? they speak they think they hate.#but i think they stop. because it’s better not to. it’s easier. and guiltless too. not like a dalek stops to xonsider your personhood.#but to be very very clear. even has also killed just. guys.#actually i have in my notes here that the tone-setting moment of this whole. arc?#is that it really starts with a jailbreak. predicated on lackluster security for one of the prisoners because they are *just* a human.#and the other is. well. and there’s a war that won’t end that there’s no escape from now to worry about.#but the tone-setting part yeah. is that this really starts with even befriending someone like them through the bars. time lords need#janitors too you know? someone has to clean up around the cells. and they let even out for a minute because of that friendship.#as you can imagine. even is not going back in the cell once they’re out of it. no matter what they promised. and their ‘friend’ is going to#alert someone. and.#you need to understand most of all from this first point. that even doesn’t know that regeneration isn’t A) an inherent trait of gallfrey#rather than a granted one and B) infallible. that’s the cslculation they make. that whatever damage they do won’t matter because they’ll#come back from the dead. ………they do not.#it’s reslly a ‘congratulations! you broke free of the narrative constraints (and safeties) of standing near the doctor! murder is now#unlocked! good luck!’ moment akdhfkshdkfj#anyway. <3 makes their life worse on purpose <3#dw oc

3 notes

·

View notes

Text

✰ –– hero coffee roasters. 2pm, on a tuesday.

this bitch wants a frappu-fuckin’-ccino. murphy blinks and pastes on a smile. jesus. fake-owning this shithole’s getting real old these days. “ oh, hun, of course i can improvise that sugar rush for you. don’t even fret it. we totally keep vats of that fake java just lying around. ” honestly, murph can’t tell what’s worse –– the fact that this cardboard cutout vsco girl even asked, or the fact that she actually believes her.

hero coffee roasters loses a customer that day. as the doorbell jingles shut with the force of the girl’s slam, murphy pops a redhot into her mouth and chews. does nothing to hide her growing smirk. yeah, yeah.

good riddance.

or alternatively : hey demons, it’s me, ya gurl ! back at it again with my very snakey shadow gorl. click that read more to learn about this gorgeous amoral piece of ass. i’m trying out a new intro format, so... bear with me ! i hope y’all enjoy, and pls hmu on discord for plots !

murph is... straight up trouble. so if you want drama ? you want bullshit & compulsive lies ? you want ill-founded rage with no apologies later ? you’ve come to the right place .

this is the story of a girl who cried a river and drowned the whole world . . . just kidding. murphy berman doesn’t shed tears for shit.

— && guests may mistake me as ( zoe kravitz ), but really i am ( murphy berman + cisfemale + she/her ) and my DOB is ( 11/7/1994 ). i am a ( “ coffee shop owner ” ) and would like to stay in suite ( 306 ). i won’t be much of a bother because i am ( + cunning & fierce ), but i can also be ( - acetous & cutthroat ) at times. personally, i like to ( code, flick gum wrappers at pigeons, bring my pet turtle to the movies, sit back and watch shit burn ) when i have the time to relax, and my favorite snack is ( those purple doritos, y'know. chili or whatever the fuck ) to have in my suite. thank you for checking in !

i n s p o .

coffee shop –– hero coffee roasters.

pinterest.

soundcloud –– soul sounds.

soul anthem.

b a c k d r o p . ( tw: drug mentions, alcoholic tendencies, alcohol, crime, allusions to domestic violence, violence, murder. )

2am, bar’s closed. but braids still sits, forearms draped atop the counter, shades askew. as you restock new handles, she raises a finger, like she might say something, then pours herself another bourbon. cutting her off is the least of your worries –– it doesn’t take a genius to tell this cookie can handle her own. and the shit she’s spewing ? something tells you this has never been aired before.

“ so picture the fuck outta this, bub. ” a swig. “ you’re born and before you even got the wherewithal to speak, you’re shipped off to some graham cracker family in the ‘ burbs. you start leapfrogging –– my term, tee-em –– ” a tattooed finger traces the symbol into the air accordingly. “ and after a while, it’s a game. hop a house, stay a while, see how much of their shit you can pocket. ” nostalgic sighs accompany a litany of stolen goods : cash. jewelry. first edition tetris game, hand-fuckin’-held. the hoopers’ prized gold kazoo.

don’t believe her ? onto black marble slides proof.

“ then you land. hard. the fuckin’ landry’s. ” a scornful chuckle. “ miss me with that white picket fence ass shit. but they get you your first comp, so... when they ask to adopt you, you’re like. i dunno, man. sure, i guess ? and guess wrong. ” turns out the landry’s aren’t as warm or welcoming as they claim. their youngest kid dies, freak accident. monkey bars. “ family falls apart worse than that time you tried to make a ball from fresh cigarette ash. you were eleven. ” tattooed over the scar.

braids tells you ‘bout the party being over. the bruising. but she laughs through it, rolls her eyes like she’s talking ‘bout silly old friends instead of terrible old people.

her birth mother finds her. they meet up a few times in a local park, whisks her away when she’s twelve. is it kidnapping ? technically, who gives a fuck. they lived low. under the radar. in apartments above dive bars. spent a summer breaking into parked cars. finally landed with j.j., who turned out to just be a glorified drug mule.

“ new york was fine to me. y’know, fucked off in school. kid shit. ” she shrugs. you won’t know it, but she’ll astutely sidestep the fact that she hacked her first global system at 14. she won’t mention she started accepting paypal offers from obscure reddit threads two weeks later. by 17, she was contracting independently –– a business venture, she’d tell her high school counselor, assigned to keep her from winding up on the streets.

matty, her best friend since the move to new york, decided to kiss her silly after trying shrooms. she liked it. told him maybe he could do that more often.

“ he cleaned up, ” braids purses her lips. “ after high school. stopped messing with his crowd. our crowd. ” she grabs two stirrers from a container dangerously close to your hand. taps ‘em on the counter like she’s stomping out mini fires. “ let him put a ring on me. y’know make bey proud. ”

she won’t mention that while matty gets a job as a cook at a bougie french restaurant, she continued to deal with devils. woman in her high castle. under the guise of cpu-based tetris and a whole lot of freelance web design.

but then roosevelt savings bank gets robbed. and they somehow trace the ip back to her.

it’s an easy mishap to shake. showed ‘em the websites. the code. the computer usage logs. the blues believe her, but matty...

“ trust issues. sad, huh ? thought i was fucking around behind his back. ” with criminals.

“ and then shit gets good, homie. we’re tasting stupid fucking cake. red velvet... ” cue a laugh. bitter. the stirrers stop tapping. “ then i meet aamina and everything goes to shit. i brought it up, you know. like. hey, your fiancée might be a little bit into pussy. ”

for the first time all night, her eyes meet yours. and it’s only then you realize... there’s some heavy fuckin’ sadness swimming in those baby browns. worlds pass through them. alternative stories –– where matty wasn’t high. where he didn’t reach for the knife.

“ he lost it. ” silence. she looks away. “ anyway. ” she launches into why chicago –– why she studied pre-law for two years before tossing in the towel. because “ fuck a judge, man. ” and she’s into the finer things in life. ( she struck you as an arts type. what with the glasses. the vintage band tee worn like a dress. maybe you get a glimmer of pride knowing you were right. she won’t mention that the whole thing’s a farce. )

she launches into why a coffee shop. she’ll tell you the beautiful thing about coffee is it takes no shit. she’ll tell you owning a place gets fuckin’ wild, but she’s in it for the free java and coffee-themed booze. a perk all hourly baristas like her enjoy. “ and we made that top list or whatever. of fly places here. an honor. i’d like to thank god, and also jesus. which i hope you know are my boys bazzi and frank ocean. ”

you’ll google hero coffee roasters later. and find its registered owner goes by brian tubolino. but hey, maybe she’s married.

when braids finally decides it’s time to go, sunlight’s nipping at chicago’s heels.

“ you chill if i ... ? ” before you can answer, she’s takin’ a swig straight from the half-finished bottle of bourbon. picks it up and cradles it under one arm, precious cargo.

“ souvenir, man. in remembrance of you. ”

#intro.#✰ –– don't punish the tiger for taking its prey ! inspo.#✰ –– so ugly but you love me ! she speaks.

2 notes

·

View notes

Photo

Whipped…boyfriend!!!

“Boo!”

Y/N isn’t expecting for Harry to be surprised much, at least not for sneaking up on him.

“Y/N, love! I’ve missed ye’ so much, kitten!”

He tucks his phone into his back pocket before wrapping his arms around her waist and picking her up, a grin so wide and a feeling so comforting that nothing in the world could ruin the moment.

“Missed you loads, too, H!” She whispers into his hair, the feeling of his breath on her neck soothing her instantly.

Harry pecks at her neck before setting her back down, his eyes scanning over her every feature. His heart melts at the way she looks up at him, and when he sees her stand on her tip toes, he leans down to press his lips to hers.

It’s a playful exchange of kisses, with Y/N’s hands gripping at the sides of his printed shirt, and Harry’s large hands cupping her face. Kisses with open eyes and big stupid smiles. Kisses that don’t last longer than three second before their lips separate only to press together again. And in between them, Harry whispers ‘missed ye’ too much’ and 'I love you’ in broken phrases.

Missed. Kiss. Ye’. Kiss. Too. Kiss. Much. Kiss.

He nudges his nose against hers lightly before pressing one last kiss to her forehead and wrapping an arm around her neck so it dangles over her shoulder as they begin to walk.

“Didn’t tell me ye’ were comin’ for a visit, love.”

Not that Harry minds, at all. He just would’ve liked to have been the first person she saw, not some random cabbie or whoever picked her up at the airport.

“Thought it’d be fun to pop by unannounced. Jeff pitched the idea after he overheard Mer talking to me over the phone. Said you could use a little company in that empty hotel room of yours.”

She bumps his hip with hers, giggling for a moment at the famous half smirk he gives her.

“Hm, well if tha’s why ye’ came here then I reckon we should get t’ tha’ empty hotel room, ehh?”

He’s stopped dead in his tracks, moving to stand in front of Y/N to look at her directly. And Harry can visibly see her tense up, the playful look she’d been sporting a few seconds ago gone.

“Y/N-” he begins, eyebrows furrowed into concern, only to be cut off.

“I’m sorry, H. I know it’s taking forever, but it’s just-” and she’s trying so hard not to disappoint him. She knows they’ve been dating far too long for intimacy not to be part of the relationship already, and it makes her mad that she can’t let herself love him in that way. Not because she doesn’t want to, she knows they’re meant to be together, she just doesn’t feel ready yet.

“No. No, kitten, you’ve got nothing t’ apologise for,” Harry’s hands rub at her upper arms soothingly, hoping to assure her that he’s okay with it, “m'not ever g'na rush this. I want ye’ t’ be sure when the time comes that you want it as much as I do.”

“But I know that it’s frustrating and-”

“-and m'g'na wait as long as I’ve got t’. M'not g'na love ye’ less b'cos of it. Jus’ wan’ ye’ t’ be sure, love.”

He gives her that smile. That toothy smile that can make all their problems fade into nothing. And so she smiles, too.

“Tha’s m'girl.”

***

“Well would ye’ look at this lovely picture.”

A 'wuh-PSSSH’ sound follows the comment, a voice too familiar not to notice.

“Still whipped, mate?”

Harry just smiles, unwrapping his arm from around Y/N to stand up and greet his friend in a proper hug.

“Oh, look at this,” Y/N can hear Harry coo before she’s even got the chance to slip out of the booth they’re currently sat at, “Freddie’s here!”

And to say he completely disregarded Louis at this point would be an understatement, he might as well be invisible now.

Harry stretches his arms out, and Louis complies at letting him hold his one year old.

“Nice t’ see ye’ too, Harry. I’ve been great, thanks mate.”

Harry pays the sarcasm no mind as he sets the baby on his hip, and instead smiles and coos at Freddie who looks up at him with happy eyes.

“Don’t worry, did the same to me earlier.” Y/N laughs at the thought of Harry having left her side with out a second thought to hold who she came to find out was an adorable little baby girl named Ruby.

Louis welcomes her into a hug, whispering a low 'outta have kids then’ in her ear.

And that warms her heart. To think that one day, she’ll be lucky enough to welcome a lovely little human that’ll be a mix of her and Harry, she honestly can’t wait. But now she feels even more guilty.

But Harry smiles at her adoringly, baby Freddie in his arms chuckling and trying to grab at Harry’s short but now longer hair.

“I see you two are still disgustingly sweet as usual,” Louis comments.

Just the way Harry looks at you, it’s unreal and anyone who knew you both would swear you were meant for each other, even before either of you realised it. And that’s exactly what your friends thought. Seeing Harry look at you the way he did at the many dinners and house parties everyone would gather for definitely added to those thoughts.

And you two have been practically inseparable ever since New York. You were glad Harry had gathered up the courage to find you that night, don’t know if you’d be in this position if he hadn’t. You were glad he was hell bent on not leaving that hotel room until things were cleared up because “really miss m'best friend. Tell me wha’ I did so I can fix it, kit'en.” And you were glad he’d said those three words that solidified the fact that he was there to make sure you were his, even though you had been all along.

“Will be. So long as this one will have me,” the press of Harry’s lips to Y/N’s has Louis grunting in pretend distaste.

“Better get going, don’ wanna interrupt Harry still being whipped.”

Harry hands Freddie over with a pout.

“Still no complaints though.”

***

To say everything is going perfect would be an understatement. Harry’s music is being praised and appreciated and Y/N can’t explain how happy it makes her that Harry’s happy. His performances are nothing short of amazing, and she loves seeing him gush over “they were singing along, babe! Just a great feelin’!”

She’s been flying back and forth along his side during all this. New York, London, Paris, and then back to New York. And Harry loves sharing this with her. He loves having her watching him from the side lines, singing along as she claps and gives him thumbs up and blows kisses at him for support. He loves getting off stage with so much adrenaline and kissing her so hard because Harry doesn’t take anything for granted, no. He’s thankful he’s getting to do what he loves and even more with his better half by his side.

“A'right. How do I look?” His jazz hands and that big smile plastered on his face are indication of just how hyped he is for this.

“I’ve never seen anyone pull off black better than you, H!”

And it’s true. Harry can pull off any colour. Blue, red, yellow, pink; you name it! But black. Black gives him a sexy sort of mysterious sophistication.

“Think so?” He looks himself over in the mirror, content at his choice.

Y/N looks at him through the mirror from where she’s sat on the couch of his dressing room, nodding a yes as she gets up to stand on the furniture.

“Please no stage diving today?” She’d be all for it, if it weren’t for the fact that he’s already tried it and it didn’t go as planned. She really doesn’t want him or any of the fans getting injured.

Harry only chuckles and nods in embarrassment as he strides over to stand in front of her, his head tilting up just a bit to look at her since she’s standing on the cushions.

“M'serious, Harry!” But she smiles anyway, arms lazily slung over his shoulders and around his neck. She brings a hand to tug at the hairs at the nape of it as Harry sets his at either side on her hips, thumbs rubbing at her hipbones.

It’s the last listening party before the album is released, and Harry’s pretty sure the second he mentions stage diving, Jeff will have him pulled off stage. Or carried because it is Jeff after all.

“I’ll try not to, kit'en.” Harry doesn’t know why it was a good idea to do it in the first place. But he had all that adrenaline and he was just so excited. Y/N of course had scolded him and slapped his arm after he got off stage because, “you could’ve broken something Harry!!” But he’d kissed the small amount of anger away.

“I’ll be watching from the sides?” Every time before a performance or an interview she says that, and every time she does Harry smiles just as big.

***

“Congrats, Ni!!!!!”

Finally, after a few months of all the boys doing their own thing, everyone’s finally got a chance to gather up at a small venue for Harry’s pre-launch party. Jeff had asked Y/N for help in terms of invitees, and it’d be outrageous not to have Liam, Niall, and Louis attend.

And so Niall is the last to arrive, and the moment he walks through the door, a very tipsy Y/N can’t contain her excitement at finally reuniting with another one of her friends.

“Oí, have enough drinks for the rest of us have ya?” Niall just about tumbles back with the sudden weight of her body as she throws herself at him, but he catches her in his arms and steadies her.

“You’re late mister,” she’s slurring just a bit, words somewhat coherent.

“Does 'arry know you’re drunk??”

He wraps an arm around her waist for support, in fear that she might be too over her head to even walk with out tripping and falling.

“Drunk? M'not drunk,” she pokes at his chest, and Niall only now notices the red cup in her hand threatening to spill over his shirt, “you’re just sober.”

He lets out a lively laugh. Drunk Y/N is something else, and he’s only ever seen her like this when Harry’s not really paying attention to her.

She hiccups and continues with a pout, “he’s over somewhere. With some girl,” she motions her hand around and nowhere in particular, again, the drink sploshing around in the red cup.

Harry hadn’t meant to leave her alone, he’d been pulled away from her side by someone he can’t even recall the name of, because that’s how out of it he is. So he’s been handed drink left and right, downing them with out retaliation because he doesn’t wanna seem like a downer. And although he really should go find his Y/N, he doesn’t think she’d mind if she’s having fun too.

But she’s not. At least not as much as she’d like. All she wants is for Harry to kiss her and hold her hand, because they’re both affectionate drunks, and it’s always a plus to annoy their friends in that way. But she hasn’t seen him in a while. Last she caught a glimpse was about an hour or so ago, when he was being led over to a group of people she doesn’t really recognise, and it made her notice how out of it she is. She doesn’t remember inviting half the people in the room, but the little attention Harry seems to be giving her has her drinking with out a purpose.

It reminds her of when they were only friends. In the same circumstance, she’d drink the night away in hopes of erasing the image of Harry smiling wide, eyes crinkled because some girl was whispering god knows what in his ear. He’d be hunched over just a bit to give the girl better access as she mumbled and giggled. And Harry would nod slightly before moving to whisper something back, face too close to her liking. But it, too, was always nothing, because shortly after she would have to turn away. Try to hide the fact that yes, she might have been staring at Harry for much longer than she’d ever admit to. And when he’d catch a glimpse of her doing just the same with a guy, giggling and whispering and smiling like crazy, he’d make his way over. Weaving his way around dancing bodies to get to her. And he’d smile that drink infused crooked smile of his before whispering something like “let’s get ye’ home, pet,” and leading her out of the place with his palm to her lower back.

So yeah, this sort of reminds her of old times. Only this time, they’re actually dating and he’s nowhere to be found.

***

Harry doesn’t remember getting home. He doesn’t remember taking off his clothes either.

In fact, the last thing he remembers is Y/N kissing at his neck and tugging at his pants.

And..oh no. If that’s how…if they were both drunk and-ah shit! Neither of them were suppose to be drunk when it finally happened. Harry wanted to make sure she would be okay with everything going on. He would have wanted to whisper how good she was taking him. Wanted to assure her that he was there with her, that all he wanted was to make her feel good. Harry just wanted to make love to her the right way.

And now he doesn’t even remember half the night.

So he brings his hand over his face, because not only does he not remember, he also doesn’t recognise the room he’s woken up in.

And then he looks beside him at the body under the white sheets.

He doesn’t recognise the person he’s woken up next to.

That’s not his Y/N.

Whipped...Boyfriend!!! Pt.2

#harry styles#harry styles fanfiction#harry styles imagine#harry styles story#harry styles fluff#harry styles smut#harry styles blog#harry styles preferences#harry styles one shot#harry fluff#harry smut#harry blog#harry imagine#whipped friends#whipped boyfriend#whipped series#harry writing

862 notes

·

View notes

Text

The pros and cons of Personal Capital

If you've read money blogs over the past five years, you've heard about Personal Capital. Personal Capital is a free money-tracking tool with a beautiful interface and gasp no advertising. (One of my big complains about Mint is that it shoves ads in your face.)

Many of my friends and colleagues promote the hell out of Personal Capital because the company pays good money when people sign up. (And yes, links to Personal Capital in this review absolutely put money in my pocket. But any Personal Capital link you see anywhere on the web puts money in somebody's pocket.)

I sometimes wonder, though, if any of my pals actually uses Personal Capital, you know? All of their reviews are glowing. While I like Personal Capital, I've been frustrated by the app in the past. Even today, I find that it's not as useful as I'd like.

What are my issues with Personal Capital?

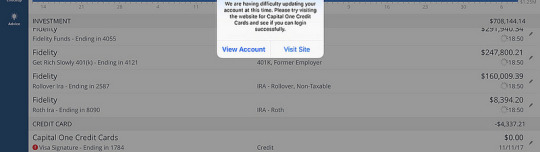

For a long time, I was frustrated trying to get Personal Capital to connect to my accounts. It still won't connect to my credit union, but that's fine. I can enter my balance manually. It was frustrating, though, that for years I couldn't get Personal Capital to connect to my Fidelity investment accounts. They work nowbut I'm always worried that they won't. The app still won't connect to my Capital One credit card and hasn't for over a year, which I find mind-blowing.

Personal Capital, as an app, isn't robust enough to replace something like Quicken or You Need a Budget. The latter tools allow you to track and manage your money on a transaction by transaction level. Okay, maybe you can track your transactions, but you can't do anything meaningful with them, the same way you could with Quicken or YNAB.The phone calls! My god, the phone calls! Here's a not-so-secret secret: The Personal Capital app while beautiful and useful is actually bait. It's a lure. Its aim is to attract high net-worth users to connect their accounts. When they do, Personal Capital (the company) begins a phone campaign in an attempt to recruit the users as clients. Personal Capital isn't actually an app company; it's a wealth-management company. They want people with lots of money to sign up. (I can't comment on whether this is a good deal or not. I don't want a financial advisor. I ignore all of the calls from Personal Capital.)

Personal Capital has pretty reports, but there aren't enough of them. My copy of Quicken 2007 ugly as it is has 23 different reports and 10 different graphs. (Plus, you can customize many more.) Personal Capital has maybenine ways to look at your money? (I can't tell for sure.)The security is over the top. I suppose I should be happy about this, but I'm not. It feels like I'm constantly having to verify my identity via email or text message. Some of my other accounts make me do this occasionally, but it feels like Personal Capital does this multiple times per week. That's crazy!

Now, these complaints aside, here's a confession: I've been using the Personal Capital app for 5+ years. For real. I can't remember when I started, but I do remember being cranky because a Personal Capital rep didn't know who I was at Fincon 2013 in St. Louis. I use your app, I told him. And I have a big blog. (I wince now at the thought of my arrogance.)

Despite the drawbacks, there must be something to it. Right? Today using my current financial situation let's look at the pros and cons of Personal Capital.

Quicken 2007 vs. Personal Capital

As regular readers know, I'm an old fogey. My money management tool of choice is an antiquated copy of Quicken for Mac 2007. This tool is so important to me, in fact, that I'm currently refusing to update my system software to the latest version (Mac OS Mojave) because I'm afraid it'll break Quicken. (Other user experiences are mixed.) How important is Quicken 2007 to me? No joke: I would buy a used Mac laptop just to run that software.

As much as I love Quicken, it has its drawbacks. One of those is that it's a pre-mobile app. Quicken 2007 is almost as old as this blog. It came out roughly one year before the first iPhone. (Get Rich Slowly launched on 15 April 2006. I can't find a release date for Quicken 2007, but it was available by at least 30 August 2006. The iPhone launched on 29 June 2007.) If I want to interact with Quicken, I have to sit down at my desktop computer.

Because I'm a nerd, I'm attached to my mobile devices. I have an iPad. And an iPhone. And an Apple Watch. (Why isn't it an iWatch? I don't know. Apple doesn't give a fig about consistency.) I want to be able to track my money from my mobile devices.

Trust me: I've tried tons of other mobile apps. I don't really like any of them. I do, however, like Personal Capitalwarts and all. I would never ever use it as my only money management tool, but as one piece of a bigger package, it'a actually kind of awesome.

Personal Capital is the only mobile money management app that I use. There are others out there, sure, but for my needs, Personal Capital fills a nicheand fills it well.

Personal Capital as Daily Money Tracker

I use Personal Capital as a daily tracker. Quicken 2007 is my actual go-to tool for entering and analyzing my data, but Personal Capital is what I've used for the past five years to check on my accounts to make sure everything is okay.

Believe it or not, Personal Capital has saved my bacon several times. What? My credit card payment is due today? Whoops! I'd better go pay it. Wait! What's this strange charge on my account? That's not me. Let me call my bank. Whoa! I forgot to pay my garbage bill. I'd better handle that when I get home.

Because Personal Capital connects to (most of) my accounts, I'm able to look at everything from a unified dashboard. I don't have to log in to each credit card and bank account to verify everything. I can do it from one place. (Okay, not my credit union. I still have to go check that separately.)

Here, for instance, is a look at my recent transactions. (I have no idea what the graph is tracking. I'm not sure I care.)

When I shared my financial situation recently, a few readers wondered why I don't count my business finances when tracking my entire money picture. Well, in Personal Capital I do. Because I can connect the app to both personal and business accounts, I can get an idea of the Big Picture. Here you can see that most of my expenses for January so far have been blog related.

I'll admit, it's very nice to have a single app where I can view all of my recent transactions, both personal and business. Although I only take action on this info maybe twice per year, it sets my mind at ease. It takes thirty seconds of my time each day, but that's thirty seconds I'm happy to spend.

Personal Capital as Investment Tracker

Honestly, though, Personal Capital isn't meant to be a daily money-management tool. For that, I'd use something like You Need a Budget. Personal Capital is specifically designed to monitor your investments. Because of this, the Personal Capital app has a variety of tools to help investors.

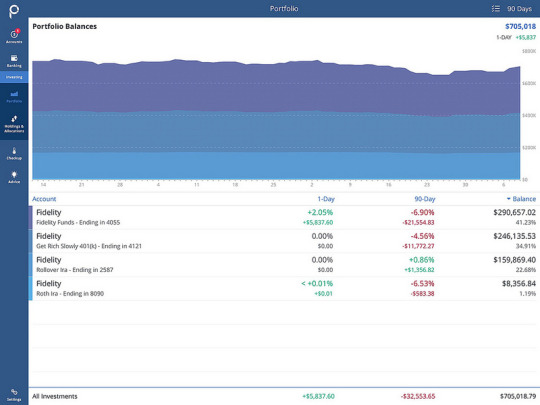

First up, there's the plain ol' portfolio view:

Nothing special here, right? You get a list of your investments and a graph of their performance over the past 90 days. Nothing special, but still easier for me than logging into the Fidelity website (or app).

(As a passive investor, though, I don't actually look at investment performance that often. I might check it once per weekbut a couple of times per month is more likely.)

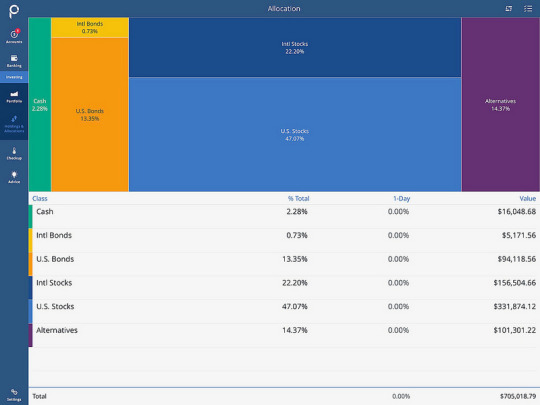

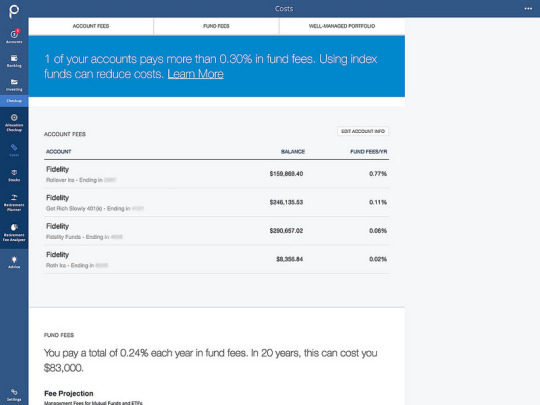

You can also get a breakdown of your asset allocation:

The Personal Capital app also offers something interesting something I think Vanguard and Fidelity should offer. They have a tool that analyzes the fees on your investment accounts. As you probably know, fees are one of the top drags on the average investor's performance. Too many suckers pay 1% or 2% per year (or more!) in mutual fund costs. Index funds have risen to prominence because they promise management fees of 0.20% or 0.10% (or lower).

Personal Capital makes it clear just how much you're paying in fees.

In my case, I'm doing fairly well except in my rollover IRA. But I'm okay with that. That rollover IRA is 100% invested in a real-estate investment trust (or REIT), and those carry higher expense ratios. (True story: That REIT is actually my highest performing investment over the past decade!)

Personal Capital's Retirement Calculator

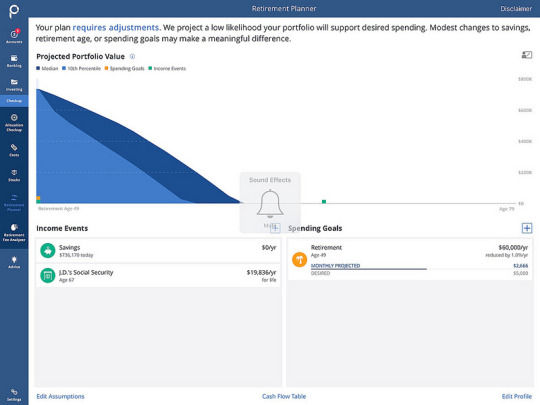

All of these other features are great, but there's one main reason I continue to use Personal Capital: its retirement calculator.

As I mentioned the other day, I hate most retirement calculators. They're overly simplistic. Their assumptions are bogus. They're designed to get users to save more than they need.

The Personal Capital retirement calculator isn't the best tool on the market we'll look at two better tools during the next week but it's pretty damn good for something that's free and built into an otherwise useful app.

This section is going to be the biggest part of this review, and it's going to contain plenty of screenshots. You've been warned.

First up, here's a look at my own personal financial situation as of this morning. (Sorry for the mute notification in the middle of the screenshot. My bad. Not sure why I was muting my iPad, but I can't fix it now.)

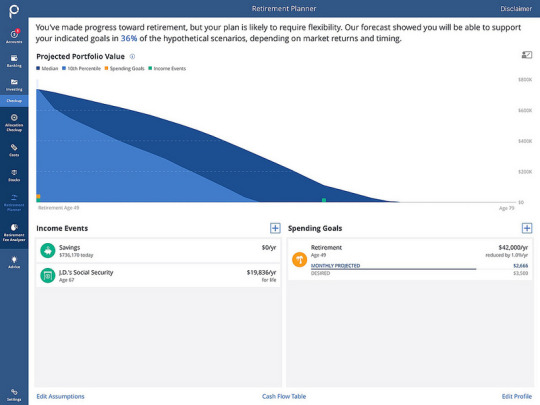

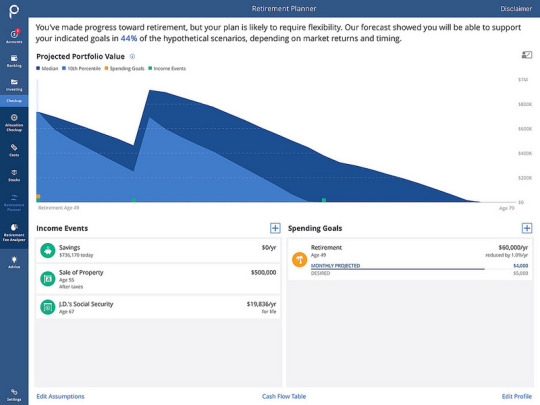

Based on my current situation $736,170 in liquid investments and roughly $60,000 of annual expenses Personal Capital says I'll run out of money at 62. This doesn't differ much from other retirement calculators I've looked at.

But here is where Personal Capital gets fun (and the reason I'm obsessed with it). Do you see those + signs across from Investment Events and Spending Goals? If you click on those, you can add new events. (And if you click on existing events, you can modify those.) This means you can tweak your parameters over and over and over again.

What if, for instance, I decreased my spending from $60,000 per year to $42,000 per year? (This is my aim for 2019.)

Well, look at that. If I re-embrace frugality, my money will likely last until I'm 72 instead of 62. Nice!

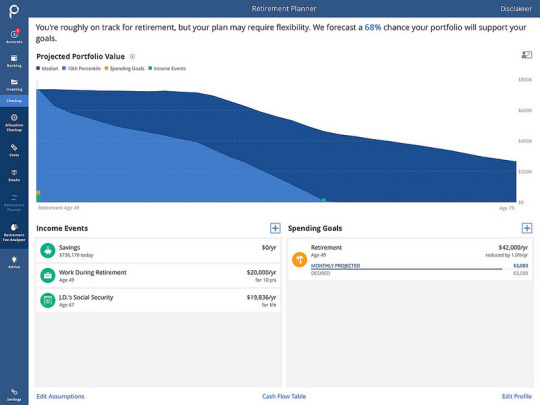

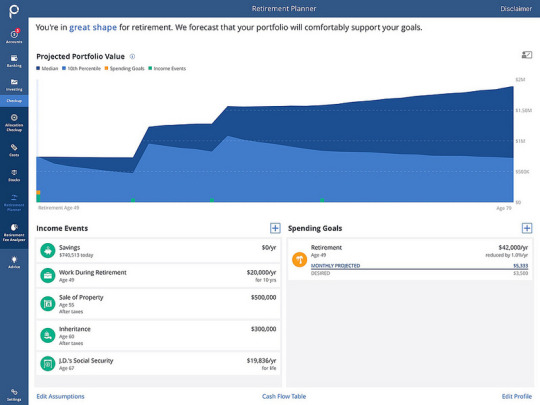

And now that I'm back to work at the box factory, what if I stay there for ten years and earn $20,000 annually?

Holy cats! As you can see, working part-time makes a ginormous difference. If I reduce my spending to $3500 per month while earning $20,000 per year, I'm golden. I shouldn't run out of money before my projected age of demise. (Even in a worst-case scenario, my money would last until age 67.)

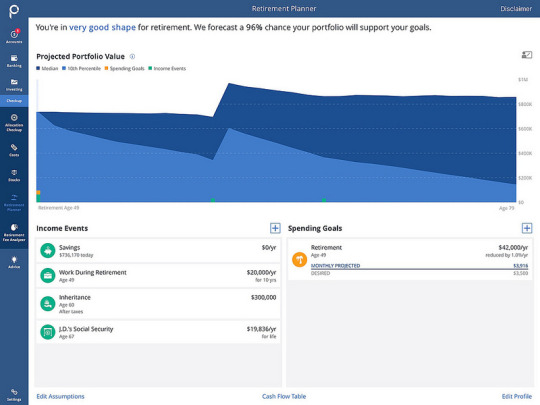

And if I end up with an inheritance? Party time!

Okay, maybe I'm getting a little too out of control there. Let's dial things back. Let's get rid of the inheritance and bring my spending back to current levels. If I work part-time for ten years, what then?

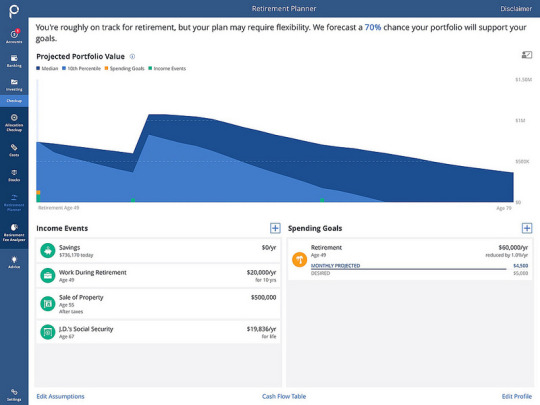

Hm. Not enough to get me to where I want to go, is it? (Plus, I was muting the sound again. What the heck?) Okay, what if I decide to sell this house at some point in the next ten years. What then?

Okay, not bad. That makes me wonder, though, what if I did not decide to go back to work for the family business. What then?

Well, I guess that's not bad, but it's not nearly as good as if I'm bringing in some sort of income.

Okay, let's look at the ultimate optimistic scenario. Let's say I trim my spending from $60,000 per year to $42,000 per year. Let's assume I spend the next decade at the box factory earning $20,000 per year. Let's assume that my mother dies in ten years or so and leaves me an inheritance. Let's assume that Kim and I sell this place after increasing frustration with the never-ending repairs, then move into a rented apartment.

After all those assumptions, what does my future look like?

But that's a future that's far too rosy than the one I think lies ahead.

You get the point, though. Even without the app's other features, I'd love Personal Capital just for its retirement calculator. It's more fun and flexible than 95% of the other retirement calculators on the market. (As I mentioned, we'll take a peek at the 5% that are better over the next few days.)

The Bottom Line

I have been using Personal Capital for five years now. It's nowhere near a complete money-management tool, and I know that. But I don't care. I don't expect it to be the biggest and bestest. I accept it for what it is.

Personal Capital is great at a few things:

Monitoring your money on a daily basis.Tracking (and analyzing) your investment portfolio.Playing with various retirement scenarios.

If you're not interested in these three tasks, Personal Capital probably isn't right for you. If you want a lot of detail and analysis, Personal Capital probably isn't right for you. If you have a lot of money invested and don't want people to pester you with phone calls, Personal Capital probably isn't right for you.

For everyone else, though, Personal Capital is a useful (if imperfect) tool. If you decide to use it, just be aware of its limitations. As I say, I've been using it for five years. It's not my top tool, but it's the one I access most often. That's worth something, I guess.

I'm curious, though. Many GRS readers must also be using Personal Capital. What are your experiences like? Do you recommend it? What are your favorite features? What do you not like? Would you recommend Personal Capital to a friend?

Author: J.D. Roth

In 2006, J.D. founded Get Rich Slowly to document his quest to get out of debt. Over time, he learned how to save and how to invest. Today, he's managed to reach early retirement! He wants to help you master your money and your life. No scams. No gimmicks. Just smart money advice to help you reach your goals.

https://www.getrichslowly.org/personal-capital/

0 notes

Text

The pros and cons of Personal Capital

If you've read money blogs over the past five years, you've heard about Personal Capital. Personal Capital is a free money-tracking tool with a beautiful interface and — gasp — no advertising. (One of my big complains about Mint is that it shoves ads in your face.)

Many of my friends and colleagues promote the hell out of Personal Capital because the company pays good money when people sign up. (And yes, links to Personal Capital in this review absolutely put money in my pocket. But any Personal Capital link you see anywhere on the web puts money in somebody's pocket.)

I sometimes wonder, though, if any of my pals actually uses Personal Capital, you know? All of their reviews are glowing. While I like Personal Capital, I've been frustrated by the app in the past. Even today, I find that it's not as useful as I'd like.

What are my issues with Personal Capital?

For a long time, I was frustrated trying to get Personal Capital to connect to my accounts. It still won't connect to my credit union, but that's fine. I can enter my balance manually. It was frustrating, though, that for years I couldn't get Personal Capital to connect to my Fidelity investment accounts. They work now…but I'm always worried that they won't. The app still won't connect to my Capital One credit card — and hasn't for over a year, which I find mind-blowing.

Personal Capital, as an app, isn't robust enough to replace something like Quicken or You Need a Budget. The latter tools allow you to track and manage your money on a transaction by transaction level. Okay, maybe you can track your transactions, but you can't do anything meaningful with them, the same way you could with Quicken or YNAB.

The phone calls! My god, the phone calls! Here's a not-so-secret secret: The Personal Capital app — while beautiful and useful — is actually bait. It's a lure. Its aim is to attract high net-worth users to connect their accounts. When they do, Personal Capital (the company) begins a phone campaign in an attempt to recruit the users as clients. Personal Capital isn't actually an app company; it's a wealth-management company. They want people with lots of money to sign up. (I can't comment on whether this is a good deal or not. I don't want a financial advisor. I ignore all of the calls from Personal Capital.)

Personal Capital has pretty reports, but there aren't enough of them. My copy of Quicken 2007 — ugly as it is — has 23 different reports and 10 different graphs. (Plus, you can customize many more.) Personal Capital has maybe…nine ways to look at your money? (I can't tell for sure.)

The security is over the top. I suppose I should be happy about this, but I'm not. It feels like I'm constantly having to verify my identity via email or text message. Some of my other accounts make me do this occasionally, but it feels like Personal Capital does this multiple times per week. That's crazy!

Now, these complaints aside, here's a confession: I've been using the Personal Capital app for 5+ years. For real. I can't remember when I started, but I do remember being cranky because a Personal Capital rep didn't know who I was at Fincon 2013 in St. Louis. “I use your app,” I told him. “And I have a big blog.” (I wince now at the thought of my arrogance.)

Despite the drawbacks, there must be something to it. Right? Today — using my current financial situation — let's look at the pros and cons of Personal Capital.

Quicken 2007 vs. Personal Capital

As regular readers know, I'm an old fogey. My money management tool of choice is an antiquated copy of Quicken for Mac 2007. This tool is so important to me, in fact, that I'm currently refusing to update my system software to the latest version (Mac OS Mojave) because I'm afraid it'll break Quicken. (Other user experiences are mixed.) How important is Quicken 2007 to me? No joke: I would buy a used Mac laptop just to run that software.

As much as I love Quicken, it has its drawbacks. One of those is that it's a pre-mobile app. Quicken 2007 is almost as old as this blog. It came out roughly one year before the first iPhone. (Get Rich Slowly launched on 15 April 2006. I can't find a release date for Quicken 2007, but it was available by at least 30 August 2006. The iPhone launched on 29 June 2007.) If I want to interact with Quicken, I have to sit down at my desktop computer.

Because I'm a nerd, I'm attached to my mobile devices. I have an iPad. And an iPhone. And an Apple Watch. (Why isn't it an iWatch? I don't know. Apple doesn't give a fig about consistency.) I want to be able to track my money from my mobile devices.

Trust me: I've tried tons of other mobile apps. I don't really like any of them. I do, however, like Personal Capital…warts and all. I would never ever use it as my only money management tool, but as one piece of a bigger package, it'a actually kind of awesome.

Personal Capital is the only mobile money management app that I use. There are others out there, sure, but for my needs, Personal Capital fills a niche…and fills it well.

Personal Capital as Daily Money Tracker

I use Personal Capital as a daily tracker. Quicken 2007 is my actual go-to tool for entering and analyzing my data, but Personal Capital is what I've used for the past five years to check on my accounts to make sure everything is okay.

Believe it or not, Personal Capital has saved my bacon several times. What? My credit card payment is due today? Whoops! I'd better go pay it. Wait! What's this strange charge on my account? That's not me. Let me call my bank. Whoa! I forgot to pay my garbage bill. I'd better handle that when I get home.

Because Personal Capital connects to (most of) my accounts, I'm able to look at everything from a unified dashboard. I don't have to log in to each credit card and bank account to verify everything. I can do it from one place. (Okay, not my credit union. I still have to go check that separately.)

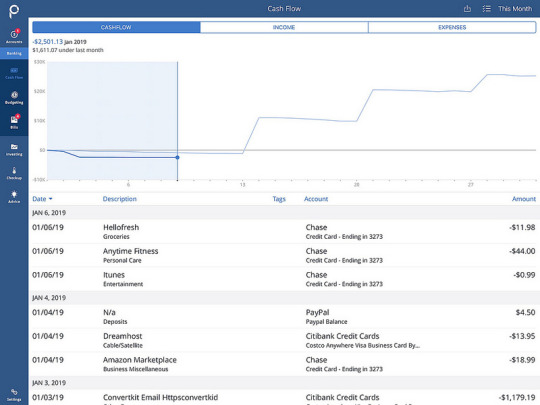

Here, for instance, is a look at my recent transactions. (I have no idea what the graph is tracking. I'm not sure I care.)

When I shared my financial situation recently, a few readers wondered why I don't count my business finances when tracking my entire money picture. Well, in Personal Capital I do. Because I can connect the app to both personal and business accounts, I can get an idea of the Big Picture. Here you can see that most of my expenses for January so far have been blog related.

I'll admit, it's very nice to have a single app where I can view all of my recent transactions, both personal and business. Although I only take action on this info maybe twice per year, it sets my mind at ease. It takes thirty seconds of my time each day, but that's thirty seconds I'm happy to spend.

Personal Capital as Investment Tracker

Honestly, though, Personal Capital isn't meant to be a daily money-management tool. For that, I'd use something like You Need a Budget. Personal Capital is specifically designed to monitor your investments. Because of this, the Personal Capital app has a variety of tools to help investors.

First up, there's the plain ol' portfolio view:

Nothing special here, right? You get a list of your investments and a graph of their performance over the past 90 days. Nothing special, but still easier for me than logging into the Fidelity website (or app).

(As a passive investor, though, I don't actually look at investment performance that often. I might check it once per week…but a couple of times per month is more likely.)

You can also get a breakdown of your asset allocation:

The Personal Capital app also offers something interesting — something I think Vanguard and Fidelity should offer. They have a tool that analyzes the fees on your investment accounts. As you probably know, fees are one of the top drags on the average investor's performance. Too many suckers pay 1% or 2% per year (or more!) in mutual fund costs. Index funds have risen to prominence because they promise management fees of 0.20% or 0.10% (or lower).

Personal Capital makes it clear just how much you're paying in fees.

In my case, I'm doing fairly well except in my rollover IRA. But I'm okay with that. That rollover IRA is 100% invested in a real-estate investment trust (or REIT), and those carry higher expense ratios. (True story: That REIT is actually my highest performing investment over the past decade!)

Personal Capital's Retirement Calculator

All of these other features are great, but there's one main reason I continue to use Personal Capital: its retirement calculator.

As I mentioned the other day, I hate most retirement calculators. They're overly simplistic. Their assumptions are bogus. They're designed to get users to save more than they need.

The Personal Capital retirement calculator isn't the best tool on the market — we'll look at two better tools during the next week — but it's pretty damn good for something that's free and built into an otherwise useful app.

This section is going to be the biggest part of this review, and it's going to contain plenty of screenshots. You've been warned.

First up, here's a look at my own personal financial situation as of this morning. (Sorry for the “mute” notification in the middle of the screenshot. My bad. Not sure why I was muting my iPad, but I can't fix it now.)

Based on my current situation — $736,170 in liquid investments and roughly $60,000 of annual expenses — Personal Capital says I'll run out of money at 62. This doesn't differ much from other retirement calculators I've looked at.

But here is where Personal Capital gets fun (and the reason I'm obsessed with it). Do you see those + signs across from Investment Events and Spending Goals? If you click on those, you can add new events. (And if you click on existing events, you can modify those.) This means you can tweak your parameters over and over and over again.

What if, for instance, I decreased my spending from $60,000 per year to $42,000 per year? (This is my aim for 2019.)

Well, look at that. If I re-embrace frugality, my money will likely last until I'm 72 instead of 62. Nice!

And now that I'm back to work at the box factory, what if I stay there for ten years and earn $20,000 annually?

Holy cats! As you can see, working part-time makes a ginormous difference. If I reduce my spending to $3500 per month while earning $20,000 per year, I'm golden. I shouldn't run out of money before my projected age of demise. (Even in a “worst-case scenario”, my money would last until age 67.)

And if I end up with an inheritance? Party time!

Okay, maybe I'm getting a little too out of control there. Let's dial things back. Let's get rid of the inheritance and bring my spending back to current levels. If I work part-time for ten years, what then?

Hm. Not enough to get me to where I want to go, is it? (Plus, I was muting the sound again. What the heck?) Okay, what if I decide to sell this house at some point in the next ten years. What then?

Okay, not bad. That makes me wonder, though, what if I did not decide to go back to work for the family business. What then?

Well, I guess that's not bad, but it's not nearly as good as if I'm bringing in some sort of income.

Okay, let's look at the ultimate optimistic scenario. Let's say I trim my spending from $60,000 per year to $42,000 per year. Let's assume I spend the next decade at the box factory earning $20,000 per year. Let's assume that my mother dies in ten years or so and leaves me an inheritance. Let's assume that Kim and I sell this place after increasing frustration with the never-ending repairs, then move into a rented apartment.

After all those assumptions, what does my future look like?

But that's a future that's far too rosy than the one I think lies ahead.

You get the point, though. Even without the app's other features, I'd love Personal Capital just for its retirement calculator. It's more fun and flexible than 95% of the other retirement calculators on the market. (As I mentioned, we'll take a peek at the 5% that are better over the next few days.)

The Bottom Line

I have been using Personal Capital for five years now. It's nowhere near a complete money-management tool, and I know that. But I don't care. I don't expect it to be the biggest and bestest. I accept it for what it is.

Personal Capital is great at a few things:

Monitoring your money on a daily basis.

Tracking (and analyzing) your investment portfolio.

Playing with various retirement scenarios.

If you're not interested in these three tasks, Personal Capital probably isn't right for you. If you want a lot of detail and analysis, Personal Capital probably isn't right for you. If you have a lot of money invested and don't want people to pester you with phone calls, Personal Capital probably isn't right for you.

For everyone else, though, Personal Capital is a useful (if imperfect) tool. If you decide to use it, just be aware of its limitations. As I say, I've been using it for five years. It's not my top tool, but it's the one I access most often. That's worth something, I guess.

I'm curious, though. Many GRS readers must also be using Personal Capital. What are your experiences like? Do you recommend it? What are your favorite features? What do you not like? Would you recommend Personal Capital to a friend?

The post The pros and cons of Personal Capital appeared first on Get Rich Slowly.

from Finance https://www.getrichslowly.org/personal-capital/

via http://www.rssmix.com/

0 notes

Last Seen Blogs

trnsnicky

Unique as can be ...

mr-big-guy

Untitled

leech-hearts

#1 crybaby

chxxrybxxmb

Mrs. Inconsistent

mindfulparentingproject

The Mindful Parenting Project