#risk management

Photo

Well, there are ways to hurt you that do not involve hurting... you.

#elementary#elementaryedit#elementasquee#rjs*: new#risk management#ele s1#forever actual favorite#ugh it is so good#sherlock holmes#joan watson#brotp: you and i are bound

1K notes

·

View notes

Text

Insurance companies are making climate risk worse

Tomorrow (November 29), I'm at NYC's Strand Books with my novel The Lost Cause, a solarpunk tale of hope and danger that Rebecca Solnit called "completely delightful."

Conservatives may deride the "reality-based community" as a drag on progress and commercial expansion, but even the most noxious pump-and-dump capitalism is supposed to remain tethered to reality by two unbreakable fetters: auditing and insurance:

https://en.wikipedia.org/wiki/Reality-based_community

No matter how much you value profit over ethics or human thriving, you still need honest books – even if you never show those books to the taxman or the marks. Even an outright scammer needs to know what's coming in and what's going out so they don't get caught in a liquidity trap (that is, "broke"), or overleveraged ("broke," again) exposed to market changes (you guessed it: "broke").

Unfortunately for capitalism, auditing is on its deathbed. The market is sewn up by the wildly corrupt and conflicted Big Four accounting firms that are the very definition of too big to fail/too big to jail. They keep cooking books on behalf of management to the detriment of investors. These double-entry fabrications conceal rot in giant, structurally important firms until they implode spectacularly and suddenly, leaving workers, suppliers, customers and investors in a state of utter higgeldy-piggeldy:

https://pluralistic.net/2022/11/29/great-andersens-ghost/#mene-mene-bezzle

In helping corporations defraud institutional investors, auditors are facilitating mass scale millionaire-on-billionaire violence, and while that may seem like the kind of fight where you're happy to see either party lose, there are inevitably a lot of noncombatants in the blast radius. Since the Enron collapse, the entire accounting sector has turned to quicksand, which is a big deal, given that it's what industrial capitalism's foundations are anchored to. There's a reason my last novel was a thriller about forensic accounting and Big Tech:

https://us.macmillan.com/books/9781250865847/red-team-blues

But accounting isn't the only bedrock that's been reduced to slurry here in capitalism's end-times. The insurance sector is meant to be an unshakably rational enterprise, imposing discipline on the rest of the economy. Sure, your company can do something stupid and reckless, but the insurance bill will be stonking, sufficient to consume the expected additional profits.

But the crash of 2008 made it clear that the largest insurance companies in the world were capable of the same wishful thinking, motivated reasoning, and short-termism that they were supposed to prevent in every other business. Without AIG – one of the largest insurers in the world – there would have been no Great Financial Crisis. The company knowingly underwrote hundreds of billions of dollars in junk bonds dressed up as AAA debt, and required a $180b bailout.

Still, many of us have nursed an ember of hope that the insurance sector would spur Big Finance and its pocket governments into taking the climate emergency seriously. When rising seas and wildfires and zoonotic plagues and famines and rolling refugee crises make cities, businesses, and homes uninsurable risks, then insurers will stop writing policies and the doom will become undeniable. Money talks, bullshit walks.

But while insurers have begun to withdraw from the most climate-endangered places (or crank up premiums), the net effect is to decrease climate resilience and increase risk, creating a "climate risk doom loop" that Advait Arun lays out brilliantly for Phenomenal World:

https://www.phenomenalworld.org/analysis/the-doom-loop/

Part of the problem is political: as people move into high-risk areas (flood-prone coastal cities, fire-threatened urban-wildlife interfaces), politicians are pulling out all the stops to keep insurers from disinvesting in these high-risk zones. They're loosening insurance regs, subsidizing policies, and imposing "disaster risk fees" on everyone in the region.

But the insurance companies themselves are simply not responding aggressively enough to the rising risk. Climate risk is correlated, after all: when everyone in a region is at flood risk, then everyone will be making a claim on the insurance company when the waters come. The insurance trick of spreading risk only works if the risks to everyone in that spread aren't correlated.

Perversely, insurance companies are heavily invested in fossil fuel companies, these being reliable money-spinners where an insurer can park and grow your premiums, on the assumption that most of the people in the risk pool won't file claims at the same time. But those same fossil-fuel assets produce the very correlated risk that could bring down the whole system.

The system is in trouble. US claims from "natural disasters" are topping $100b/year – up from $4.6b in 2000. Home insurance premiums are up (21%!), but it's not enough, especially in drowning Florida and Texas (which is also both roasting and freezing):

https://grist.org/economics/as-climate-risks-mount-the-insurance-safety-net-is-collapsing/

Insurers who put premiums up to cover this new risk run into a paradox: the higher premiums get, the more risk-tolerant customers get. When flood insurance is cheap, lots of homeowners will stump up for it and create a big, uncorrelated risk-pool. When premiums skyrocket, the only people who buy flood policies are homeowners who are dead certain their house is gonna get flooded out and soon. Now you have a risk pool consisting solely of highly correlated, high risk homes. The technical term for this in the insurance trade is: "bad."

But it gets worse: people who decide not to buy policies as prices go up may be doing their own "motivated reasoning" and "mispricing their risk." That is, they may decide, "If I can't afford to move, and I can't afford to sell my house because it's in a flood-zone, and I can't afford insurance, I guess that means I'm going to live here and be uninsured and hope for the best."

This is also bad. The amount of uninsured losses from US climate disaster "dwarfs" insured losses:

https://www.reuters.com/business/environment/hurricanes-floods-bring-120-billion-insurance-losses-2022-2023-01-09/

Here's the doom-loop in a nutshell:

As carbon emissions continue to accumulate, more people are put at risk of climate disaster, while the damages from those disasters intensifies. Vulnerability will drive disinvestment, which in turn exacerbates vulnerability.

Also: the browner and poorer you are, the worse you have it: you are impacted "first and worst":

https://www.climaterealityproject.org/frontline-fenceline-communities

As Arun writes, "Tinkering with insurance markets will not solve their real issues—we must patch the gaping holes in the financial system itself." We have to end the loop that sees the poorest places least insured, and the loss of insurance leading to abandonment by people with money and agency, which zeroes out the budget for climate remediation and resiliency where it is most needed.

The insurance sector is part of the finance industry, and it is disinvesting in climate-endagered places and instead doubling down on its bets on fossil fuels. We can't rely on the insurance sector to discipline other industries by generating "price signals" about the true underlying climate risk. And insurance doesn't just invest in fossil fuels – they're also a major buyer of municipal and state bonds, which means they're part of the "bond vigilante" investors whose decisions constrain the ability of cities to raise and spend money for climate remediation.

When American cities, territories and regions can't float bonds, they historically get taken over and handed to an unelected "control board" who represents distant creditors, not citizens. This is especially true when the people who live in those places are Black or brown – think Puerto Rico or Detroit or Flint. These control board administrators make creditors whole by tearing the people apart.

This is the real doom loop: insurers pull out of poor places threatened by climate disasters. They invest in the fossil fuels that worsen those disasters. They join with bond vigilantes to force disinvestment from infrastructure maintenance and resiliency in those places. Then, the next climate disaster creates more uninsured losses. Lather, rinse, repeat.

Finance and insurance are betting heavily on climate risk modeling – not to avert this crisis, but to ensure that their finances remain intact though it. What's more, it won't work. As climate effects get bigger, they get less predictable – and harder to avoid. The point of insurance is spreading risk, not reducing it. We shouldn't and can't rely on insurance creating price-signals to reduce our climate risk.

But the climate doom-loop can be put in reverse – not by market spending, but by public spending. As Arun writes, we need to create "a global investment architecture that is safe for spending":

https://tanjasail.wordpress.com/2023/10/06/a-world-safe-for-spending/

Public investment in emissions reduction and resiliency can offset climate risk, by reducing future global warming and by making places better prepared to endure the weather and other events that are locked in by past emissions. A just transition will "loosen liquidity constraints on investment in communities made vulnerable by the financial system."

Austerity is a bad investment strategy. Failure to maintain and improve infrastructure doesn't just shift costs into the future, it increases those costs far in excess of any rational discount based on the time value of money. Public institutions should discipline markets, not the other way around. Don't give Wall Street a veto over our climate spending. A National Investment Authority could subordinate markets to human thriving:

https://democracyjournal.org/arguments/industrial-policy-requires-public-not-just-private-equity/

Insurance need not be pitted against human survival. Saving the cities and regions whose bonds are held by insurance companies is good for those companies: "Breaking the climate risk doom loop is the best disaster insurance policy money can buy."

I found Arun's work to be especially bracing because of the book I'm touring now, The Lost Cause, a solarpunk novel set in a world in which vast public investment is being made to address the climate emergency that is everywhere and all at once:

https://us.macmillan.com/books/9781250865939/the-lost-cause

There is something profoundly hopeful about the belief that we can do something about these foreseeable disasters – rather than remaining frozen in place until the disaster is upon us and it's too late. As Rebecca Solnit says, inhabiting this place in your imagination is "Completely delightful. Neither utopian nor dystopian, it portrays life in SoCal in a future woven from our successes (Green New Deal!), failures (climate chaos anyway), and unresolved conflicts (old MAGA dudes). I loved it."

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/11/28/re-re-reinsurance/#useless-price-signals

#pluralistic#doom loop#insurance#insuretech#climate#climate risk#climate emergency#the lost cause#market forces#risk management#price signals#control boards#decarbonization#bond vigilantes#climate resilience

262 notes

·

View notes

Text

How dangerous is hypno kink really?

The problem with trying to classify how dangerous hypno play is that different types of hypno play have different risk profiles.

Hypnotising your partner casually for relaxation or party tricks is absolutely very low-risk. This is why I often advertise hypnokink as easy to learn and fun in the bedroom. Tricks like this are easily learned in one workshop and it just opens up so many kinky possibilities.

Intense hypnotic roleplay scenes and edgy sadomasochistic scenes are about as dangerous as shibari and impact play, as in the bottom will need aftercare because they may not be able to care for themselves for a while. The top might need aftercare too btw, I know I've certainly had my moments. Play like this might lead to trauma, despite everyone's best intentions. Now you all know I believe in RACK. I'm not going to say you shouldn't do it. I'm telling you that if you want to do this, you should figure out the risks and the precautions you could take to mitigate those risks. Inform yourself.

Now… Conditioning and brainwashing play, including but not limited to personality play, addiction play and/or online files, can be life-destabilisingly dangerous. Absolutely high risk! And unfortunately, this danger is freely available online with no one to provide a safety net or aftercare. It's hard to tell the "harmless" online files apart from the ones that could fuck you over, especially as a beginner. It's hard to tell the friendly online hypnotists apart from the culty abusive doms that could fuck you over. And it's hard to find help when you've become the victim of one.

If you didn't know, now you know.

23 notes

·

View notes

Text

Since I need to distract myself a bit let me talk about

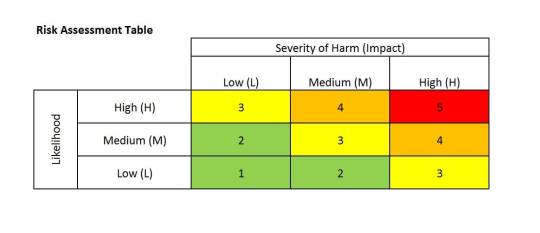

~✨Risk Management ✨~

So, y'all have read the interview of the CEO or something like that of the company that owned the submarine, yeah? He said something like "at a certain point security is useless".

I work in security (ok, cybersecurity but) so I'd like to get on the occasion to explain to everyone what risk is and how it works.

PSA: I'm not defending the guy, i don't care. This is just me taking the ball to explain something. Idk what he meant, I didn't read the whole interview and this is not about the submarine incident.

So, let me define risk first as:

Likehood * Impact

Likehood is the probability that something could happen.

Impact is the damage you get if that thing happens.

Risk is generally classified according to tables similar to this one.

If you're doing a good job you are probably going to create one of this personalised for each "thing" you need to assess.

The thing is: when we assess a risk we need to consider a few things:

What's the worst case scenario?

Do we have a "back-up" plan if things go wrong (-> limits the impact)

What are the most important asset for this thing we want to assess? (Helps identify the impact)

What is the probability that a villain could access the assets? What kind of tools would they need?(likehood)

Is there something we can do about this?

And other things. I'm trying to keep it very generic.

Then we proceed. After we evaluated the risk(s) we could face, we have four choices:

Avoid the risk -> obvious right? We take the steps to eliminate the risk completely;

Mitigate the risk -> reducing the likehood or the impact by taking several measures

Transfer the risk -> you hire someone that takes the risk for you (insurance, anyone?)

Accept the risk.

I know this sounds counterintuitive, but think about it for a second.

You own a car. You did all the controls you could do and consider yourself a moderate and careful driver(mitigation), have a insurance (transference), leave the phone in the backseat (avoidance... kinda)but there is still a residual risk of having an incident, despite all the countermeasures you took.

You can decide to not drive at all, that would land the risk to 0, but you need to go to work, right?

Is reasonable at this point for you to... Not drive entirely? Some of you might say no, for various reasons: it's irrational, need to go to work, you can't use a bike because it's too far...

Companies do the same when evaluating risks. They might decide that, to them, action X doesn't represent a threat (small impact or extremely low likehood).

Consider also that in cybersecurity every layer of defense you create it's literally making someone's job more difficult. Sometimes it's worth it (consider the case of assets that handle personal data or credit card information), sometimes after you did all the assesment you find out that the level of sophistication an attack would require is such improbable, expensive, impractical that you don't take any measure to fix it.

(I recommend the Darknet Diaries "Jeremy from Marketing" episode - it's a really interesting example of what I'm talking about specifically)

Most of the time risks are being mitigated - avoiding a risk entirely is often impossible or would require too much resources. I have a post on "accessibility for the users and security" to write for my cybersecurity portfolio since last year but ok I guess.

Thanks for coming to my ted talk about something no one cares about but I found incredibly interesting.

32 notes

·

View notes

Text

Just read a story of a good samaritan that was killed by an abusive man because she tried to help the victim. She put herself between the abuser and dv victim and got hit and died. It was "manslaughter" because he didn't intend to kill her but she died anyway.

We need to have a conversation about helping dv victims without putting oneself at risk of being harmed in anyway. Most people will not nor should they be expected to risk harm for strangers. For me, I am not risking my life for save anyone that I don't love especially when there is a chance she might go back to her abuser.

Yes, women should support women (as long as it doesn't negatively impact their wellbeing).

How to intervene in violent incidents without risking harm

Call the police

Record the incident and let the perpetrator know you are recording.

Intervene from a distance. Marksmanship: Throw things and/or shoot at the perpetrator.

If you want to go close range, try not to engage alone.

8 notes

·

View notes

Text

Silicon Valley Bank Bailout

youtube

SVB's Risk Management 🙄🙄🙄

#biden collapse#build back better#banking crisis#fraud#Biden's broken brain#margin call#alphabet hire#risk management#bailout

38 notes

·

View notes

Quote

If repression has the role, in cybernetic capitalism, of forestalling the event, prediction is its corollary, insofar as it is for the purpose of eliminating the uncertainty that’s associated with any future. It is the major concern of the statistical technologies. Whereas those of the welfare State were completely focused on the anticipation of risks, calculated or not, those of cybernetic capitalism aim at multiplying the domains of responsibility. The discourse concerning risk is the driver for deploying the cybernetic hypothesis; it is circulated first and then internalized. Because risks are more easily accepted if those exposed to them have the impression they have chosen to take them, feel responsible for them and, furthermore, feel that they have the power to control and master them themselves. But, as one expert admits, ‘zero risk’ does not exist…By virtue of its permanence for the system, risk is an ideal tool for promoting new forms of power that favor the increasing hold of security apparatuses on collectives and individuals. It eliminates any question of conflict by the obligatory drawing together of individuals around the management of threats that are supposed to concern everyone in the same way. The argument that THEY want us to accept is the following: greater security goes hand in hand with an increased production of insecurity. And if you think that the insecurity increases as prediction tends to be infallible, that’s because you are yourself afraid of risks. And if you are afraid of risks, if you don’t trust the system to completely control your life, your fear risks being contagious and in fact may present a very real risk of disloyalty to the system. In other words, to be afraid of risks is already to be seen as a risk to society oneself. The imperative of commodity circulation on which cybernetic capitalism is based morphs into a general phobia, a fantasy of self-destruction. The control society is a paranoiac society, something that is clearly confirmed by the proliferation of conspiracy theories within it. Thus every individual is subjectified in cybernetic capitalism as a risky dividual, as the generic enemy of the balanced society

Tiqqun, The Cybernetic Hypothesis, pg. 74-75

#tiqqun#cybernetic hypothesis#risk#management#risk management#security#neoliberalism#insecurity#responsibility#personal responsibility#dividual#subjectification

75 notes

·

View notes

Text

Financial Planning Worth $1-2 Million US Dollars. I would request you all to go through this guide and share it with everyone you know, so that they can secure their financial future.

#finance planning#finance management#financial freedom#finance#financial security#financial management#retirement planning#how to earn money#financial goals#cashflow#debt management#risk management#investment planner#passive income#passive investing#estate planning#retire early#financial advice#money management#money manifestation#money#cash management

4 notes

·

View notes

Text

The FIRE Movement: A Comprehensive Guide to Financial Independence and Early Retirement

Introduction

In recent years, a revolutionary concept has emerged in the realm of personal finance, captivating the imagination of young adults worldwide. Known as the FIRE movement, which stands for Financial Independence, Retire Early, this philosophy offers more than just financial advice—it proposes a radical shift in lifestyle. This in-depth guide explores the intricacies of the FIRE…

View On WordPress

#asset allocation#budgeting tips#Compound interest#early retirement#financial autonomy#financial freedom#financial independence#Financial planning#FIRE movement#frugality#lifestyle choices#lifestyle inflation#living below means#passive income#personal finance#retire early#retirement planning#Risk management#savings strategies#side hustles#smart investing#Wealth Management

3 notes

·

View notes

Text

Business Continuity Management: Navigating Through Crisis and Disruption

The key element of a company's risk mitigation strategy is business continuity management or BCM. Management refers to the approaches and strategies adopted to ensure that a company can carry on without its operations during as well as after a crisis or disturbance. Companies have to make sure they have a strong BCM structure set up to navigate through these difficulties among emerge victorious on the opposite side, particularly with the increasing severity and frequency of disasters, cyberattacks, and other unforeseen occurrences on the rise.

Finding possible risks and hazards to a business's operations and creating a plan to lessen their effects are the objectives of business continuity management or BCM. The company's vital roles, assets, and dependencies must all be carefully evaluated, as must the possible effects of different outcomes. Businesses can design a plan that will guarantee their survival and continuation in the event of a crisis by identifying possible threats and weaknesses.

Risk management is one of the essential elements of BCM. This entails determining possible dangers and putting precautions in place to lessen their effects. This can involve taking precautions including having backup systems, switching to different suppliers, and having emergency communication procedures. Businesses may lessen the interruption brought on by a crisis and guarantee that critical operations are carried out by putting these safeguards in place.

Crisis management is yet another essential component of business continuity management, in addition to risk management. This entails establishing a crisis response strategy that is precise and well-defined. It ought to have protocols for important stakeholders' coordination, decision-making, and communication. To guarantee this plan's efficacy in a crisis, it should be routinely evaluated and updated.

Also, read: cyber security management

Business recovery is another crucial component of BCM. This has to do with what happens when there is a disturbance to regular operations. In addition to repairing any potential financial or reputational harm, this may entail reinstating crucial systems and procedures. A solid business recovery strategy helps reduce the amount of time lost and money lost during a crisis.

The following are some ways that BCM helps companies overcome obstacles:

1. Crisis Readiness and Preparedness: By providing a framework for predicting and evaluating possible interruptions, business continuity management (BCM) helps companies create proactive plans and preventive actions. Increased durability and quicker action in the instance of an emergency are ensured by these preventive tactics.

2. Business Continuity Plans: Building extensive operational continuity strategies is an essential component underlying business continuity management (BCM). These plans give a business detailed instructions on how to react to particular disruptions, including important actions, accountable teams, and communication tactics.

3. Resource Management and Allocation: BCM makes certain that the people, space, and equipment required to handle disruptions are distributed appropriately. Proactive planning makes companies more equipped to handle emergencies and enables more effective and efficient responses.

4. Communications and Collaboration: Effective BCM facilitates clear and timely communication across various levels of an organization. Enhanced information is essential during moments of emergency since it facilitates integrated operations, ensures timely transmission of data, and maintains the trust of stakeholders.

5. Resilience and Recovery: Although BCM acknowledges that interruptions are a natural part of the company, it additionally provides companies with the tools they need to bounce back fast from setbacks. Companies can boost robustness and come back from crises faster by putting recovery strategies into place, evaluating the impact of delays, and taking experiences from previous crises.

6. Legal and Regulatory Compliance: A lot of businesses need to maintain company continuity to comply with industry-specific regulations or legal obligations. Through BCM, companies may be guaranteed to comply with these regulations and continue to run legally even in times of emergency.

7. Stakeholder Confidence: A company can maintain its ability to provide vital services in the face of interruptions by managing its business continuity management (BCM) strategy effectively, which gives stakeholders trust. Partnerships between vendors, staff members, consumers, and regulators may all profit from that trust.

8. Cost and Reputation Management: Modern proactive business continuity management (BCM) solutions enable firms to reduce the financial and non-financial impacts associated with disruptions. Employers can save expenses related to unwanted publicity and downtime by taking preventive actions to prevent crises or abbreviate their length of impact.

The COVID-19 outbreak has drawn emphasis to just how important BCM is to the state economy now. The malware's unanticipated or severe consequences have forced companies to react swiftly to change and establish remote employment alternatives. Businesses with an effective BCM plan in place were more prepared to cope with the circumstances & carry on business as usual amid the period of disruption.

Visit for more: enterprise risk management

Besides simply assisting you escape an emergency, having a BCM strategy has multiple benefits. In addition, it promotes a company's flexibility and endurance. Companies may be more prepared for future disruptions by proactively mitigating possible hazards and vulnerabilities using awareness and intervention. Following an established BCM plan can assist in promoting a business's credibility along with graphics among consumers because this reveals a dedication to risk management and business continuity.

Conclusion

The management of business continuity is an essential component of every organization's risk management plan. Businesses may navigate through any crisis or disruption with minimum damage by identifying possible dangers, creating a crisis management plan, and setting a path for business recovery. A crucial foundation for preparing companies for a variety of disruptions and emergencies is business continuity management. Companies can react to challenges quickly and efficiently, protect their constituents and resources, & continue providing essential amenities according to their aggressive and integrated strategy. Despite merely offering a rapid response, the practice of business continuity management (BCM) enhances an enterprise's general toughness and viability in a changing and uncertain commercial setting. Possessing an efficient BCM plan executed is a necessity given the recent increase in both the incidence and impact of unplanned instances.

isorobot is an enterprise management solution that will help you automate all the processes to keep ahead of the competition. isorobot has every solution you need to run your business effectively, which includes GRC (Governance, Risk, and Compliance) (Governance, Risk, and Compliance), ERM (Enterprise Risk Management) Health, safety, and quality management, ESG (Environmental, Social, and Governance) (Environmental, Social and Governance) (Environmental, Social, and Governance), etc. We have worked with businesses across a variety of sectors, including manufacturing, healthcare, technology, and more. We provide a range of services, such as strategy formulation, operational improvement, change management, and more. Our group of experts is prepared to assist you in reaching your professional objectives.

email us at: [email protected]

2 notes

·

View notes

Photo

Most puzzles I see from the outside, and it gives me a certain clarity. I am right in the center of this one. It has blurred my vision... to say the least.

#elementary#elementaryedit#elementasquee#rjs*: new#risk management#ele s1#joan watson#sherlock holmes#brotp: you and i are bound#yes i made gifs i had to remake so it's prettier now#this scene is hngalsdkjfalskjdf

349 notes

·

View notes

Text

Accepted a job offer today. I am going to be the Quality Assurance RN for a local nursing home. They are about 6 months into a major revamp and overhaul. I had a long interview with the DON and I really like her vibe. She genuinely seems invested in improving the facility, and I think I will be helpful in that goal.

So I have about a week left of enjoying not working. But I will be happy to be back to work before I would have had to dip into savings to pay the mortgage.

#ha-hh#rn#new job#quality assurance#risk management#quality improvement#post-acute care#nurse#nursing

9 notes

·

View notes

Text

Fire Safety Training in Construction

In the realm of construction, fire safety training is not just a regulatory requirement; it’s a vital practice that safeguards lives and property. This article will delve into why fire safety training in construction is essential, its key components, and how it benefits both workers and construction projects.

Understanding Fire Safety Training in Construction

Understanding fire safety training…

View On WordPress

#construction training#emergency response#equipment maintenance#fire drills#fire prevention#fire safety#hazard identification#project management#property protection#regulatory compliance#Risk Management#Safety Culture#safety protocols#site safety#workforce training

2 notes

·

View notes

Text

The Importance of Diversification in Your Investment Portfolio

Diversification is a critical concept in investment that can help you balance risk and reward. By diversifying your investments, you can mitigate potential losses without significantly impacting potential gains. This article explores the importance of diversification in an investment portfolio and provides some strategies to help you diversify effectively.

What Is…

View On WordPress

#Asset Allocation#Bonds#Diversification#Financial Planning#Investing Strategy#Investment Portfolio#Mutual Funds#Real Estate#Risk Management#Stocks

5 notes

·

View notes

Text

Budget Control in Project Management: Strategies for Success

Unlock the secrets to successful project budget control and avoid overruns with these 10 essential strategies. #ProjectManagement #BudgetControl #CostEstimation #PMStrategies

Effective project management is a multi-faceted skill that requires a delicate balance of various elements, with budget control being a crucial aspect. Project budget overruns can be detrimental to an organization’s financial health and the successful completion of a project. To mitigate the risks associated with budget overruns, project managers need to employ a variety of strategies and…

View On WordPress

#Budget control#budget management#Budget overrun prevention#Change management#contingency planning#Continuous improvement in project management#Cost estimation#Project budget#Project budget tracking#Project cost control#project management#project management best practices#project management software#project management strategies#Project management tools#project planning#Quality control#Resource allocation#Risk management#stakeholder communication

2 notes

·

View notes

Text

#assessment Small#Business asset protection#Business continuity#Business credibility#business finance#Business protection#Commercial insurance#Cyber insurance#Insurance advice#Insurance coverage#Insurance for entrepreneurs#Insurance policies#Insurance tips Risk#Legal requirements#Liability insurance#Professional liability#Property insurance#Risk management#Small business insurance#Worker's compensation

2 notes

·

View notes

Last Seen Blogs

flamemonsterdraws

popeyes diabetic food

ryusanada-blog1

⑴⒮⒯ ⒭⒴⒰ ⒮⒜⒩⒜⒟⒜ ⒜⒞⒞⒪⒰⒩⒯

oksanawww

Untitled

buy4kids

Bez tytułu