#insuretech

Text

Your car spies on you and rats you out to insurance companies

I'm on tour with my new, nationally bestselling novel The Bezzle! Catch me TOMORROW (Mar 13) in SAN FRANCISCO with ROBIN SLOAN, then Toronto, NYC, Anaheim, and more!

Another characteristically brilliant Kashmir Hill story for The New York Times reveals another characteristically terrible fact about modern life: your car secretly records fine-grained telemetry about your driving and sells it to data-brokers, who sell it to insurers, who use it as a pretext to gouge you on premiums:

https://www.nytimes.com/2024/03/11/technology/carmakers-driver-tracking-insurance.html

Almost every car manufacturer does this: Hyundai, Nissan, Ford, Chrysler, etc etc:

https://www.repairerdrivennews.com/2020/09/09/ford-state-farm-ford-metromile-honda-verisk-among-insurer-oem-telematics-connections/

This is true whether you own or lease the car, and it's separate from the "black box" your insurer might have offered to you in exchange for a discount on your premiums. In other words, even if you say no to the insurer's carrot – a surveillance-based discount – they've got a stick in reserve: buying your nonconsensually harvested data on the open market.

I've always hated that saying, "If you're not paying for the product, you're the product," the reason being that it posits decent treatment as a customer reward program, like the little ramekin warm nuts first class passengers get before takeoff. Companies don't treat you well when you pay them. Companies treat you well when they fear the consequences of treating you badly.

Take Apple. The company offers Ios users a one-tap opt-out from commercial surveillance, and more than 96% of users opted out. Presumably, the other 4% were either confused or on Facebook's payroll. Apple – and its army of cultists – insist that this proves that our world's woes can be traced to cheapskate "consumers" who expected to get something for nothing by using advertising-supported products.

But here's the kicker: right after Apple blocked all its rivals from spying on its customers, it began secretly spying on those customers! Apple has a rival surveillance ad network, and even if you opt out of commercial surveillance on your Iphone, Apple still secretly spies on you and uses the data to target you for ads:

https://pluralistic.net/2022/11/14/luxury-surveillance/#liar-liar

Even if you're paying for the product, you're still the product – provided the company can get away with treating you as the product. Apple can absolutely get away with treating you as the product, because it lacks the historical constraints that prevented Apple – and other companies – from treating you as the product.

As I described in my McLuhan lecture on enshittification, tech firms can be constrained by four forces:

I. Competition

II. Regulation

III. Self-help

IV. Labor

https://pluralistic.net/2024/01/30/go-nuts-meine-kerle/#ich-bin-ein-bratapfel

When companies have real competitors – when a sector is composed of dozens or hundreds of roughly evenly matched firms – they have to worry that a maltreated customer might move to a rival. 40 years of antitrust neglect means that corporations were able to buy their way to dominance with predatory mergers and pricing, producing today's inbred, Habsburg capitalism. Apple and Google are a mobile duopoly, Google is a search monopoly, etc. It's not just tech! Every sector looks like this:

https://www.openmarketsinstitute.org/learn/monopoly-by-the-numbers

Eliminating competition doesn't just deprive customers of alternatives, it also empowers corporations. Liberated from "wasteful competition," companies in concentrated industries can extract massive profits. Think of how both Apple and Google have "competitively" arrived at the same 30% app tax on app sales and transactions, a rate that's more than 1,000% higher than the transaction fees extracted by the (bloated, price-gouging) credit-card sector:

https://pluralistic.net/2023/06/07/curatorial-vig/#app-tax

But cartels' power goes beyond the size of their warchest. The real source of a cartel's power is the ease with which a small number of companies can arrive at – and stick to – a common lobbying position. That's where "regulatory capture" comes in: the mobile duopoly has an easier time of capturing its regulators because two companies have an easy time agreeing on how to spend their app-tax billions:

https://pluralistic.net/2022/06/05/regulatory-capture/

Apple – and Google, and Facebook, and your car company – can violate your privacy because they aren't constrained regulation, just as Uber can violate its drivers' labor rights and Amazon can violate your consumer rights. The tech cartels have captured their regulators and convinced them that the law doesn't apply if it's being broken via an app:

https://pluralistic.net/2023/04/18/cursed-are-the-sausagemakers/#how-the-parties-get-to-yes

In other words, Apple can spy on you because it's allowed to spy on you. America's last consumer privacy law was passed in 1988, and it bans video-store clerks from leaking your VHS rental history. Congress has taken no action on consumer privacy since the Reagan years:

https://www.eff.org/tags/video-privacy-protection-act

But tech has some special enshittification-resistant characteristics. The most important of these is interoperability: the fact that computers are universal digital machines that can run any program. HP can design a printer that rejects third-party ink and charge $10,000/gallon for its own colored water, but someone else can write a program that lets you jailbreak your printer so that it accepts any ink cartridge:

https://www.eff.org/deeplinks/2020/11/ink-stained-wretches-battle-soul-digital-freedom-taking-place-inside-your-printer

Tech companies that contemplated enshittifying their products always had to watch over their shoulders for a rival that might offer a disenshittification tool and use that as a wedge between the company and its customers. If you make your website's ads 20% more obnoxious in anticipation of a 2% increase in gross margins, you have to consider the possibility that 40% of your users will google "how do I block ads?" Because the revenue from a user who blocks ads doesn't stay at 100% of the current levels – it drops to zero, forever (no user ever googles "how do I stop blocking ads?").

The majority of web users are running an ad-blocker:

https://doc.searls.com/2023/11/11/how-is-the-worlds-biggest-boycott-doing/

Web operators made them an offer ("free website in exchange for unlimited surveillance and unfettered intrusions") and they made a counteroffer ("how about 'nah'?"):

https://www.eff.org/deeplinks/2019/07/adblocking-how-about-nah

Here's the thing: reverse-engineering an app – or any other IP-encumbered technology – is a legal minefield. Just decompiling an app exposes you to felony prosecution: a five year sentence and a $500k fine for violating Section 1201 of the DMCA. But it's not just the DMCA – modern products are surrounded with high-tech tripwires that allow companies to invoke IP law to prevent competitors from augmenting, recongifuring or adapting their products. When a business says it has "IP," it means that it has arranged its legal affairs to allow it to invoke the power of the state to control its customers, critics and competitors:

https://locusmag.com/2020/09/cory-doctorow-ip/

An "app" is just a web-page skinned in enough IP to make it a crime to add an ad-blocker to it. This is what Jay Freeman calls "felony contempt of business model" and it's everywhere. When companies don't have to worry about users deploying self-help measures to disenshittify their products, they are freed from the constraint that prevents them indulging the impulse to shift value from their customers to themselves.

Apple owes its existence to interoperability – its ability to clone Microsoft Office's file formats for Pages, Numbers and Keynote, which saved the company in the early 2000s – and ever since, it has devoted its existence to making sure no one ever does to Apple what Apple did to Microsoft:

https://www.eff.org/deeplinks/2019/06/adversarial-interoperability-reviving-elegant-weapon-more-civilized-age-slay

Regulatory capture cuts both ways: it's not just about powerful corporations being free to flout the law, it's also about their ability to enlist the law to punish competitors that might constrain their plans for exploiting their workers, customers, suppliers or other stakeholders.

The final historical constraint on tech companies was their own workers. Tech has very low union-density, but that's in part because individual tech workers enjoyed so much bargaining power due to their scarcity. This is why their bosses pampered them with whimsical campuses filled with gourmet cafeterias, fancy gyms and free massages: it allowed tech companies to convince tech workers to work like government mules by flattering them that they were partners on a mission to bring the world to its digital future:

https://pluralistic.net/2023/09/10/the-proletarianization-of-tech-workers/

For tech bosses, this gambit worked well, but failed badly. On the one hand, they were able to get otherwise powerful workers to consent to being "extremely hardcore" by invoking Fobazi Ettarh's spirit of "vocational awe":

https://www.inthelibrarywiththeleadpipe.org/2018/vocational-awe/

On the other hand, when you motivate your workers by appealing to their sense of mission, the downside is that they feel a sense of mission. That means that when you demand that a tech worker enshittifies something they missed their mother's funeral to deliver, they will experience a profound sense of moral injury and refuse, and that worker's bargaining power means that they can make it stick.

Or at least, it did. In this era of mass tech layoffs, when Google can fire 12,000 workers after a $80b stock buyback that would have paid their wages for the next 27 years, tech workers are learning that the answer to "I won't do this and you can't make me" is "don't let the door hit you in the ass on the way out" (AKA "sharpen your blades boys"):

https://techcrunch.com/2022/09/29/elon-musk-texts-discovery-twitter/

With competition, regulation, self-help and labor cleared away, tech firms – and firms that have wrapped their products around the pluripotently malleable core of digital tech, including automotive makers – are no longer constrained from enshittifying their products.

And that's why your car manufacturer has chosen to spy on you and sell your private information to data-brokers and anyone else who wants it. Not because you didn't pay for the product, so you're the product. It's because they can get away with it.

Cars are enshittified. The dozens of chips that auto makers have shoveled into their car design are only incidentally related to delivering a better product. The primary use for those chips is autoenshittification – access to legal strictures ("IP") that allows them to block modifications and repairs that would interfere with the unfettered abuse of their own customers:

https://pluralistic.net/2023/07/24/rent-to-pwn/#kitt-is-a-demon

The fact that it's a felony to reverse-engineer and modify a car's software opens the floodgates to all kinds of shitty scams. Remember when Bay Staters were voting on a ballot measure to impose right-to-repair obligations on automakers in Massachusetts? The only reason they needed to have the law intervene to make right-to-repair viable is that Big Car has figured out that if it encrypts its diagnostic messages, it can felonize third-party diagnosis of a car, because decrypting the messages violates the DMCA:

https://www.eff.org/deeplinks/2013/11/drm-cars-will-drive-consumers-crazy

Big Car figured out that VIN locking – DRM for engine components and subassemblies – can felonize the production and the installation of third-party spare parts:

https://pluralistic.net/2022/05/08/about-those-kill-switched-ukrainian-tractors/

The fact that you can't legally modify your car means that automakers can go back to their pre-2008 ways, when they transformed themselves into unregulated banks that incidentally manufactured the cars they sold subprime loans for. Subprime auto loans – over $1t worth! – absolutely relies on the fact that borrowers' cars can be remotely controlled by lenders. Miss a payment and your car's stereo turns itself on and blares threatening messages at top volume, which you can't turn off. Break the lease agreement that says you won't drive your car over the county line and it will immobilize itself. Try to change any of this software and you'll commit a felony under Section 1201 of the DMCA:

https://pluralistic.net/2021/04/02/innovation-unlocks-markets/#digital-arm-breakers

Tesla, naturally, has the most advanced anti-features. Long before BMW tried to rent you your seat-heater and Mercedes tried to sell you a monthly subscription to your accelerator pedal, Teslas were demon-haunted nightmare cars. Miss a Tesla payment and the car will immobilize itself and lock you out until the repo man arrives, then it will blare its horn and back itself out of its parking spot. If you "buy" the right to fully charge your car's battery or use the features it came with, you don't own them – they're repossessed when your car changes hands, meaning you get less money on the used market because your car's next owner has to buy these features all over again:

https://pluralistic.net/2023/07/28/edison-not-tesla/#demon-haunted-world

And all this DRM allows your car maker to install spyware that you're not allowed to remove. They really tipped their hand on this when the R2R ballot measure was steaming towards an 80% victory, with wall-to-wall scare ads that revealed that your car collects so much information about you that allowing third parties to access it could lead to your murder (no, really!):

https://pluralistic.net/2020/09/03/rip-david-graeber/#rolling-surveillance-platforms

That's why your car spies on you. Because it can. Because the company that made it lacks constraint, be it market-based, legal, technological or its own workforce's ethics.

One common critique of my enshittification hypothesis is that this is "kind of sensible and normal" because "there’s something off in the consumer mindset that we’ve come to believe that the internet should provide us with amazing products, which bring us joy and happiness and we spend hours of the day on, and should ask nothing back in return":

https://freakonomics.com/podcast/how-to-have-great-conversations/

What this criticism misses is that this isn't the companies bargaining to shift some value from us to them. Enshittification happens when a company can seize all that value, without having to bargain, exploiting law and technology and market power over buyers and sellers to unilaterally alter the way the products and services we rely on work.

A company that doesn't have to fear competitors, regulators, jailbreaking or workers' refusal to enshittify its products doesn't have to bargain, it can take. It's the first lesson they teach you in the Darth Vader MBA: "I am altering the deal. Pray I don't alter it any further":

https://pluralistic.net/2023/10/26/hit-with-a-brick/#graceful-failure

Your car spying on you isn't down to your belief that your carmaker "should provide you with amazing products, which brings your joy and happiness you spend hours of the day on, and should ask nothing back in return." It's not because you didn't pay for the product, so now you're the product. It's because they can get away with it.

The consequences of this spying go much further than mere insurance premium hikes, too. Car telemetry sits at the top of the funnel that the unbelievably sleazy data broker industry uses to collect and sell our data. These are the same companies that sell the fact that you visited an abortion clinic to marketers, bounty hunters, advertisers, or vengeful family members pretending to be one of those:

https://pluralistic.net/2022/05/07/safegraph-spies-and-lies/#theres-no-i-in-uterus

Decades of pro-monopoly policy led to widespread regulatory capture. Corporate cartels use the monopoly profits they extract from us to pay for regulatory inaction, allowing them to extract more profits.

But when it comes to privacy, that period of unchecked corporate power might be coming to an end. The lack of privacy regulation is at the root of so many problems that a pro-privacy movement has an unstoppable constituency working in its favor.

At EFF, we call this "privacy first." Whether you're worried about grifters targeting vulnerable people with conspiracy theories, or teens being targeted with media that harms their mental health, or Americans being spied on by foreign governments, or cops using commercial surveillance data to round up protesters, or your car selling your data to insurance companies, passing that long-overdue privacy legislation would turn off the taps for the data powering all these harms:

https://www.eff.org/wp/privacy-first-better-way-address-online-harms

Traditional economics fails because it thinks about markets without thinking about power. Monopolies lead to more than market power: they produce regulatory capture, power over workers, and state capture, which felonizes competition through IP law. The story that our problems stem from the fact that we just don't spend enough money, or buy the wrong products, only makes sense if you willfully ignore the power that corporations exert over our lives. It's nice to think that you can shop your way out of a monopoly, because that's a lot easier than voting your way out of a monopoly, but no matter how many times you vote with your wallet, the cartels that control the market will always win:

https://pluralistic.net/2024/03/05/the-map-is-not-the-territory/#apor-locksmith

Name your price for 18 of my DRM-free ebooks and support the Electronic Frontier Foundation with the Humble Cory Doctorow Bundle.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/03/12/market-failure/#car-wars

Image:

Cryteria (modified)

https://commons.wikimedia.org/wiki/File:HAL9000.svg

CC BY 3.0

https://creativecommons.org/licenses/by/3.0/deed.en

#pluralistic#if you're not paying for the product you're the product#if you're paying for the product you're the product#cars#automotive#enshittification#technofeudalism#autoenshittification#antifeatures#felony contempt of business model#twiddling#right to repair#privacywashing#apple#lexisnexis#insuretech#surveillance#commercial surveillance#privacy first#data brokers#subprime#kash hill#kashmir hill

2K notes

·

View notes

Photo

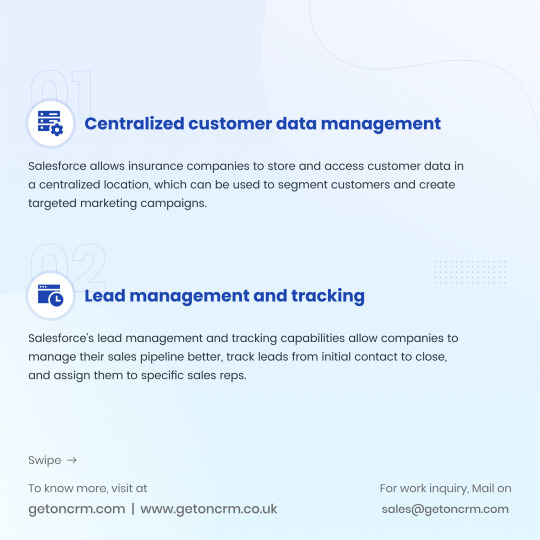

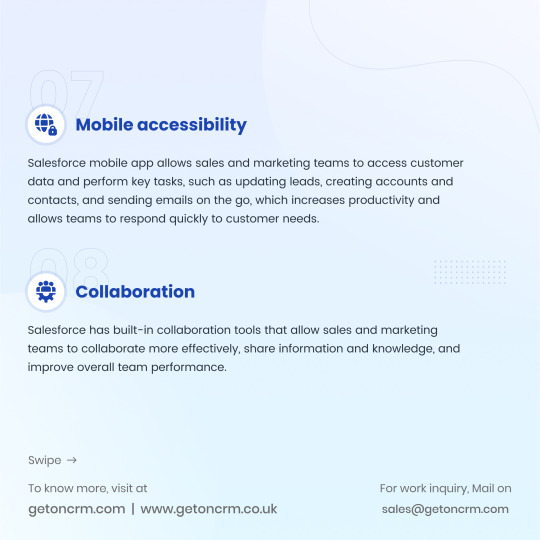

Salesforce can greatly benefit insurance companies by automating their sales and marketing processes. GetOnCRM's expertise in Salesforce can help insurance companies streamline their workflow, increase efficiency, improve their customer experience, and achieve better results.

#salescloud#salesforce#CRM#crmintegration#marketingcloud#insuretech#insurance#getoncrmuk#insuranceindustry#finance#fintech#sales#customerexperience#marketing#help

5 notes

·

View notes

Text

What if insurance was as easy as shopping on Amazon?

InsureMe is a manifestation of the modern insurance solution!

The insurance mobile app solution makes it pain-free to manage policies, file claims, and get instant support with its user-friendly design and insurance technology.

Get the complete picture of InsureMe

0 notes

Text

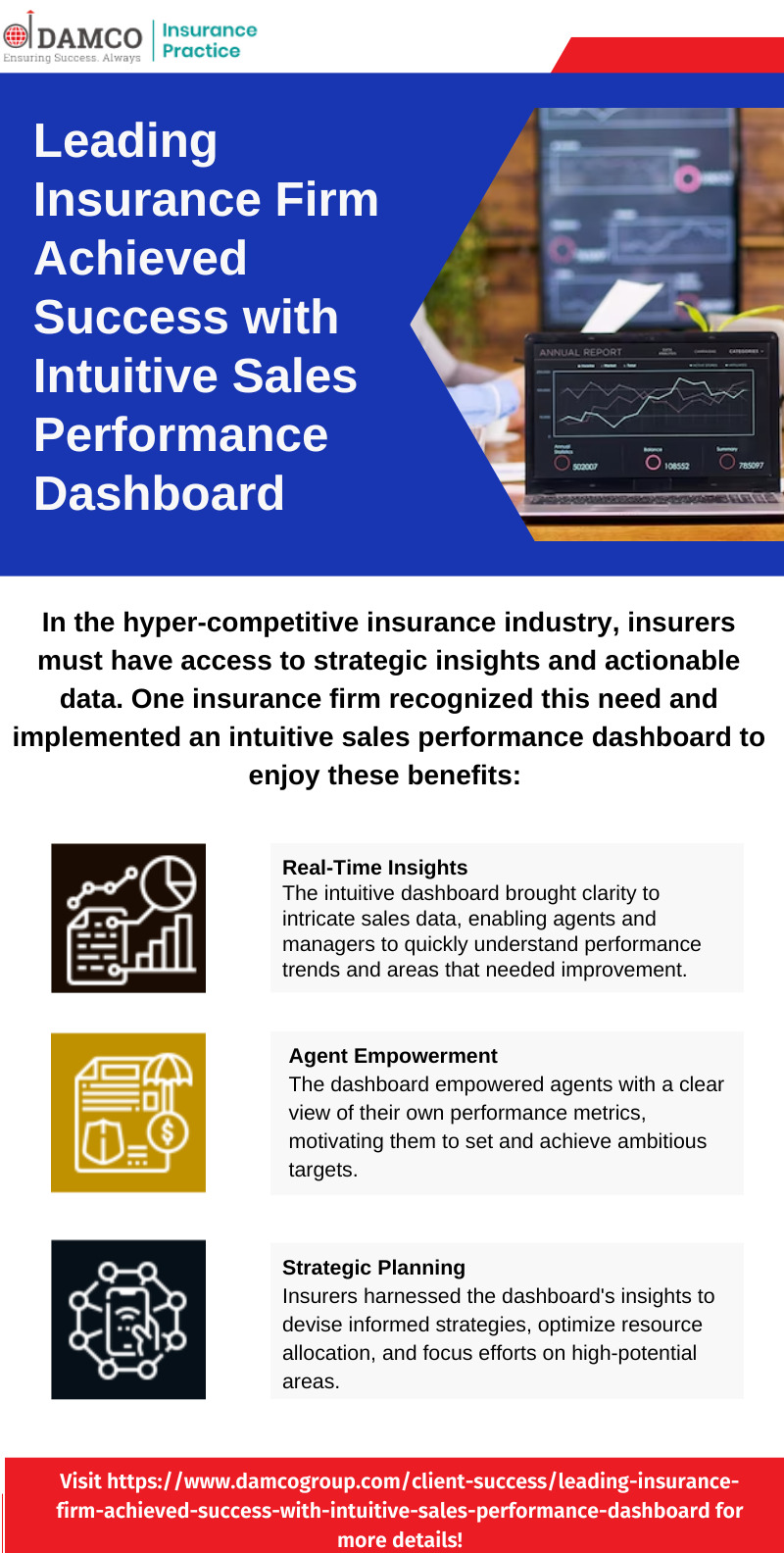

Check out the infographics to learn how embracing an intuitive sales performance dashboard helped a law firm achieve remarkable outcomes.

Visit 👉 https://www.damcogroup.com/client-success/leading-insurance-firm-achieved-success-with-intuitive-sales-performance-dashboard for more details!

0 notes

Text

An Overview to Embedded Insurance

Introduction

We’re building a great, major insurance company. If you’re interested in building a revolutionary insurance company, please join Tesla

ELON MUSK

Is Tesla, the pioneer in electric vehicles, diverging to become an Insurance Company? Let us look further into his statement.

Insurance is a good example of a product that’s made by our internal applications team. We make the insurance product and connect it to the car, look at the data, calculate the risk. This is all done internally — basically it’s an internal software application.

ELON MUSK

In my recent blog on IoT in risk assessment in Insurance, I have touched upon the usability-based Insurance and Mobility for assessing driver’s risk rate based on driving behavior with data collected from embedded systems.

Tesla is leveraging the data collected from its vehicle’s embedded system to foray into the Insurance Industry through embedded Insurance. Tesla predicts that embedded Insurance could deliver 30–40% of Tesla’s total value in the future. Research says that forty percent of insurance is going to be embedded over the next 10 to 20 years.

When a consumer purchases a product or service, bundling and selling insurance coverage or protection directly to the consumer at the POS is termed embedded insurance.

Embedded Insurance is changing the way people buy insurance by expanding opportunities and building strong customer journeys, making it easier for customers to access insurance or warranty products throughout the purchase cycle.

It is all about offering affordable, relevant, and customized insurance to customers when they need it most.

Some examples of embedded Insurance are:

Car Insurance when buying a car

Theft insurance on a new cellular device

Travel insurance when you book a flight

Insurance Coverage for new appliances

Home insurance when taking a home loan

Car rental companies offering accident coverage

What is Embedded Insurance

What is Embedded insurance — It allows any third-party provider or developer to effortlessly, quickly, and affordably integrate novel insurance products into its customers’ buying journeys. This is accomplished by abstracting insurance functionality into technology.

By collaborating with distributors and insurers in real time, Embedded Insurance makes it possible to distribute insurance at the point of need. This makes the process simple and, more significantly, reliable.

Embedded insurance isn’t a new concept. Banks were selling Insurance products from as early as 1980. Embedding insurance is profitable for both, where banks earn more revenue by selling insurance products and insurance companies expand their customer base without hiring more sales force.

Technology Approach

Application program interface (API) allows for the integration of an embedded insurance platforms into an existing system. APIs can enable insurers in analyzing data and offering the appropriate coverage at the point of sale. APIs also allow them to meet customers on their preferred channel, whether it be a PC, laptop, mobile device, or call center.

An API integrates two separate systems to provide the user with a unified shopping experience. Using pre-built, production-ready smartphones and web apps, an insurer may directly sell insurance and services to potential customers.

Embedded insurance has the potential to transform the insurance sector by assisting insurers in reaching the right customers at the right time with the right coverage.

For the advantage of all market participants, embedded insurance is emerging as a fresh, seamless method of distributing insurance services. By concentrating more on the mid-market, insurers have a trillion-dollar chance to develop new revenue streams and reduce distribution costs.

Types of Embedded Insurance

Related embedding

Related embedding is to offer insurance to the customer in any digital space in an online retailer’s selling platforms. Here, insurance can get a digital placeholder where there is a related value bridging from the core product to insurance. However, it’s not dependent on a transaction between the retailer and the customer.

An example is a car dealer offering advice on a blog post about finding the best car insurance.

Linked embedding

Linked embedding aims to turn the partner’s point of sale into an insurance sales channel. The end-user interacts with the insurance product as an extension to your partner’s sales flow, in other words. An instance of linked embedding is when an electronics store links a TV or a smartphone’s extended warranty insurance.

Bundled embedding

Bundled embedded insurance is a part of the product that the customer buys. It is inseparable from the product or service. In the automobile sector, bundled embedding is popular since it makes an all-inclusive package that includes vehicle financing, auto servicing, and auto insurance.

Benefits of embedded Insurance

For customers, it is easy, flexible, fast, and convenient, provides personalized coverage, a straightforward claims process, and protection from uninsured losses

For insurers, It opens up the possibility of lower-cost distribution to more consumers and businesses, accesses to more data to improve product innovation, and lower underwriting risks.

Third-party organizations embedded insurance can improve value offers while also generating new income streams.

It offers opportunities for investors and IT entrepreneurs to launch worthwhile new businesses.

For society, it aids in bridging the insurance protection gap as a whole, which is the discrepancy between the degree of insurance that is economically and socially advantageous and what is actually on the ground.

Enabling embedded Insurance

To understand the ecosystem of embedded insurance and to identify the spaces that are relevant to your offerings.

To create flexible products that can be more easily sold through embedded channels

To create developer platforms to distribute products and tools

To create software products and tools to embed in the target digital platforms

To acquire or diverge in companies that align with business goals to embed Insurance products

Wrapping up

Embedded insurance is going to be the largest distribution channel in the next 10 years. The existing digital channels of distribution are comparatively very expensive for insurers. Embedded insurance will fast-track in evolving Insurance-as-a-Service (IaaS) in the near future.

This post was originally published in: https://www.purpleslate.com/an-overview-to-embedded-insurance/

0 notes

Link

AI and ML adoption in InsureTech drives growth, curbs fraud, and automates processes. Explore implementation challenges and opportunities.

Read more: https://www.linkedin.com/pulse/adopting-ai-ml-insuretech-complete-insight-challenges/

#InsureTech#AI and ML in insurance#AI Implementation in insurance#automated insurance projects#automation of the insurance sector#Insurance business process#machine learning in insurance#Insurance ecosystem

0 notes

Text

Insurance Meets Blockchain

Insurance is an essential sector that helps people in difficult situations, and blockchain technology is changing the game in this sector. With blockchain, insurance companies can reap the benefits of faster payouts, cost savings, and fraud prevention while enhancing transparency and efficiency.

Do you think integrating blockchain into the insurance business is worthwhile? If so, connect with a leading blockchain consulting company for better assistance.

Keep reading to learn how blockchain technology drives growth and positive change in the insurance industry.

Blockchain Blocks False Claims

The insurance industry suffers significantly from fraudulent claims, leading to annual losses worth billions of dollars. Blockchain technology’s inherent feature of capturing time-stamped transactions with complete audit trials makes it difficult for fraudsters to commit fraud. Blockchain replaces authenticity certificates and stops duplicate claims, artificial replacements, and fake insurance claims.

Enhances Customer Experience

Insurance providers need to offer innovative solutions to win customers’ trust without compromising on price margins. Blockchain enables automated processing using smart contracts, where business agreements are built into the blockchain, and payments are auto-triggered when certain conditions are fulfilled. This way, customers can have a seamless experience while enjoying the benefits of automation.

Are you looking for an expert team to develop blockchain? Seek assistance from the best blockchain development company at affordable prices.

Improves Trustworthiness

One of the significant advantages of using blockchain in insurance is to create trust between different entities. Consensus algorithms built into blockchain allow immutability and audits, making creating smart contracts on the blockchain easier. Moreover, smart contracts enable timely, transparent, and trustworthy transactions, reducing fraud and making auditing more seamless.

Empowers More Automation

Smart contracts streamline the insurance process and enable transparent transactions. The entire insurance claims process works smoothly as the blockchain executes on the smart contract terms. Automation is a massive benefit for insurance companies, as blockchain saves time, effort, and money by lowering administrative costs.

Helps Collect And Store Useful Data

Blockchain collects usage data using artificial intelligence (AI) and Internet of Things (IoT) technologies. This data can be used to make informed decisions on insurance premiums and help monitor vehicles to qualify insureds for safe driver discounts.

5 Top Use Cases Of Blockchain In The Insurance Industry

Smart contracts eliminate the need for intermediaries and human intervention, reducing the risks of unauthorized manipulation and contract errors and increasing efficiency.

On-demand insurance is a flexible insurance model where policyholders can turn on and off their insurance policies with just a click. This model requires underwriting, buyer’s records, policy documents, and other stakeholders’ interactions, making it a perfect use case for blockchain technology.

Fraud detection and prevention can be significantly improved using blockchain technology to track and monitor high-value items like jewelry. This way, the insurance industry can avoid duplicate claims, fake replacements, and fake insurance claims.

Health insurance claims processing can be faster and more efficient using blockchain technology to store and share patients’ data between healthcare providers and insurance companies.

P2P insurance allows individuals to pool their risks and insure themselves without intermediaries. Blockchain technology can enable secure transactions and transparency between individuals, making P2P insurance a viable option.

Closing Words

Blockchain benefits to the insurance industry are numerous and significant. From fraud detection and prevention to enhanced customer experience, blockchain technology can bring about positive changes and growth in the industry. With the industry’s projected increase in the years ahead, now is the perfect time for blockchain developers to unlock the potential of blockchain and grow their businesses.

Get the finest enterprise blockchain development services from our experts.

#blockchain development#blockchain solutions#enterprise blockchain development#Impact of Blockchain on Insurance#Blockchain Development Services#Blockchain Development Company#Blockchain App Development Services#enterprise blockchain#enterprise blockchain development company#enterprise blockchain development services#custom blockchain development#End to end blockchain development service#End to end blockchain development Company#End-to-End Blockchain Development#Blockchain Insurance#InsureTech#Smart Contracts#Risk Management#Fraud Prevention#Peer-to-Peer#Claim Processing#Policy Management

0 notes

Text

Blockchain In Insurance: Driving Growth And Positive Change

Insurance is an essential sector that helps people in difficult situations, and blockchain technology is changing the game in this sector. With blockchain, insurance companies can reap the benefits of faster payouts, cost savings, and fraud prevention while enhancing transparency and efficiency.

Do you think integrating blockchain into the insurance business is worthwhile? If so, connect with a…

View On WordPress

#blockchain app development services#blockchain development#Blockchain Development Company#Blockchain development services#Blockchain Insurance#blockchain solutions#Claim Processing#custom blockchain development#End to end blockchain development Company#End to end blockchain development service#End-to-End Blockchain Development#Enterprise blockchain#enterprise blockchain development#enterprise blockchain development company#Enterprise blockchain development services#Fraud Prevention#Impact of Blockchain on Insurance#InsureTech#Peer-to-Peer#Policy Management#Risk Management#Smart Contracts

0 notes

Text

InsureTech Connect 2022 | USA Event | WNS

Join WNS at one of the biggest insurance industry events of the year in Las Vegas! Learn how WNS’ innovative solutions are driving impactful outcomes for global insurers.

Get more details on insuretech connect 2022 reach to our website and request for free demo

0 notes

Link

We are living in an era where technologies are shaping our lives in a better way. From morning to night, we take assistance from machines in our day-to-day tasks.

New technologies are coming each day to further improve the current scenario of people’s lives. Such new technology is Artificial intelligence that has shaken the whole world with its vast potential.

Whether it is the finance sector, education sector, healthcare sector, or e-commerce sector, AI has made its presence felt anywhere.

Business owners are now utilizing AI for maximum outputs with its limitless potential to transform the business of any kind.

#ai#artificial intelligence#tumblr#technology#fintech#coding#enginner#insuretech#tech in healthcare#startups#smallbusiness#development#hire service#ai engineer

0 notes

Text

Insurance companies are making climate risk worse

Tomorrow (November 29), I'm at NYC's Strand Books with my novel The Lost Cause, a solarpunk tale of hope and danger that Rebecca Solnit called "completely delightful."

Conservatives may deride the "reality-based community" as a drag on progress and commercial expansion, but even the most noxious pump-and-dump capitalism is supposed to remain tethered to reality by two unbreakable fetters: auditing and insurance:

https://en.wikipedia.org/wiki/Reality-based_community

No matter how much you value profit over ethics or human thriving, you still need honest books – even if you never show those books to the taxman or the marks. Even an outright scammer needs to know what's coming in and what's going out so they don't get caught in a liquidity trap (that is, "broke"), or overleveraged ("broke," again) exposed to market changes (you guessed it: "broke").

Unfortunately for capitalism, auditing is on its deathbed. The market is sewn up by the wildly corrupt and conflicted Big Four accounting firms that are the very definition of too big to fail/too big to jail. They keep cooking books on behalf of management to the detriment of investors. These double-entry fabrications conceal rot in giant, structurally important firms until they implode spectacularly and suddenly, leaving workers, suppliers, customers and investors in a state of utter higgeldy-piggeldy:

https://pluralistic.net/2022/11/29/great-andersens-ghost/#mene-mene-bezzle

In helping corporations defraud institutional investors, auditors are facilitating mass scale millionaire-on-billionaire violence, and while that may seem like the kind of fight where you're happy to see either party lose, there are inevitably a lot of noncombatants in the blast radius. Since the Enron collapse, the entire accounting sector has turned to quicksand, which is a big deal, given that it's what industrial capitalism's foundations are anchored to. There's a reason my last novel was a thriller about forensic accounting and Big Tech:

https://us.macmillan.com/books/9781250865847/red-team-blues

But accounting isn't the only bedrock that's been reduced to slurry here in capitalism's end-times. The insurance sector is meant to be an unshakably rational enterprise, imposing discipline on the rest of the economy. Sure, your company can do something stupid and reckless, but the insurance bill will be stonking, sufficient to consume the expected additional profits.

But the crash of 2008 made it clear that the largest insurance companies in the world were capable of the same wishful thinking, motivated reasoning, and short-termism that they were supposed to prevent in every other business. Without AIG – one of the largest insurers in the world – there would have been no Great Financial Crisis. The company knowingly underwrote hundreds of billions of dollars in junk bonds dressed up as AAA debt, and required a $180b bailout.

Still, many of us have nursed an ember of hope that the insurance sector would spur Big Finance and its pocket governments into taking the climate emergency seriously. When rising seas and wildfires and zoonotic plagues and famines and rolling refugee crises make cities, businesses, and homes uninsurable risks, then insurers will stop writing policies and the doom will become undeniable. Money talks, bullshit walks.

But while insurers have begun to withdraw from the most climate-endangered places (or crank up premiums), the net effect is to decrease climate resilience and increase risk, creating a "climate risk doom loop" that Advait Arun lays out brilliantly for Phenomenal World:

https://www.phenomenalworld.org/analysis/the-doom-loop/

Part of the problem is political: as people move into high-risk areas (flood-prone coastal cities, fire-threatened urban-wildlife interfaces), politicians are pulling out all the stops to keep insurers from disinvesting in these high-risk zones. They're loosening insurance regs, subsidizing policies, and imposing "disaster risk fees" on everyone in the region.

But the insurance companies themselves are simply not responding aggressively enough to the rising risk. Climate risk is correlated, after all: when everyone in a region is at flood risk, then everyone will be making a claim on the insurance company when the waters come. The insurance trick of spreading risk only works if the risks to everyone in that spread aren't correlated.

Perversely, insurance companies are heavily invested in fossil fuel companies, these being reliable money-spinners where an insurer can park and grow your premiums, on the assumption that most of the people in the risk pool won't file claims at the same time. But those same fossil-fuel assets produce the very correlated risk that could bring down the whole system.

The system is in trouble. US claims from "natural disasters" are topping $100b/year – up from $4.6b in 2000. Home insurance premiums are up (21%!), but it's not enough, especially in drowning Florida and Texas (which is also both roasting and freezing):

https://grist.org/economics/as-climate-risks-mount-the-insurance-safety-net-is-collapsing/

Insurers who put premiums up to cover this new risk run into a paradox: the higher premiums get, the more risk-tolerant customers get. When flood insurance is cheap, lots of homeowners will stump up for it and create a big, uncorrelated risk-pool. When premiums skyrocket, the only people who buy flood policies are homeowners who are dead certain their house is gonna get flooded out and soon. Now you have a risk pool consisting solely of highly correlated, high risk homes. The technical term for this in the insurance trade is: "bad."

But it gets worse: people who decide not to buy policies as prices go up may be doing their own "motivated reasoning" and "mispricing their risk." That is, they may decide, "If I can't afford to move, and I can't afford to sell my house because it's in a flood-zone, and I can't afford insurance, I guess that means I'm going to live here and be uninsured and hope for the best."

This is also bad. The amount of uninsured losses from US climate disaster "dwarfs" insured losses:

https://www.reuters.com/business/environment/hurricanes-floods-bring-120-billion-insurance-losses-2022-2023-01-09/

Here's the doom-loop in a nutshell:

As carbon emissions continue to accumulate, more people are put at risk of climate disaster, while the damages from those disasters intensifies. Vulnerability will drive disinvestment, which in turn exacerbates vulnerability.

Also: the browner and poorer you are, the worse you have it: you are impacted "first and worst":

https://www.climaterealityproject.org/frontline-fenceline-communities

As Arun writes, "Tinkering with insurance markets will not solve their real issues—we must patch the gaping holes in the financial system itself." We have to end the loop that sees the poorest places least insured, and the loss of insurance leading to abandonment by people with money and agency, which zeroes out the budget for climate remediation and resiliency where it is most needed.

The insurance sector is part of the finance industry, and it is disinvesting in climate-endagered places and instead doubling down on its bets on fossil fuels. We can't rely on the insurance sector to discipline other industries by generating "price signals" about the true underlying climate risk. And insurance doesn't just invest in fossil fuels – they're also a major buyer of municipal and state bonds, which means they're part of the "bond vigilante" investors whose decisions constrain the ability of cities to raise and spend money for climate remediation.

When American cities, territories and regions can't float bonds, they historically get taken over and handed to an unelected "control board" who represents distant creditors, not citizens. This is especially true when the people who live in those places are Black or brown – think Puerto Rico or Detroit or Flint. These control board administrators make creditors whole by tearing the people apart.

This is the real doom loop: insurers pull out of poor places threatened by climate disasters. They invest in the fossil fuels that worsen those disasters. They join with bond vigilantes to force disinvestment from infrastructure maintenance and resiliency in those places. Then, the next climate disaster creates more uninsured losses. Lather, rinse, repeat.

Finance and insurance are betting heavily on climate risk modeling – not to avert this crisis, but to ensure that their finances remain intact though it. What's more, it won't work. As climate effects get bigger, they get less predictable – and harder to avoid. The point of insurance is spreading risk, not reducing it. We shouldn't and can't rely on insurance creating price-signals to reduce our climate risk.

But the climate doom-loop can be put in reverse – not by market spending, but by public spending. As Arun writes, we need to create "a global investment architecture that is safe for spending":

https://tanjasail.wordpress.com/2023/10/06/a-world-safe-for-spending/

Public investment in emissions reduction and resiliency can offset climate risk, by reducing future global warming and by making places better prepared to endure the weather and other events that are locked in by past emissions. A just transition will "loosen liquidity constraints on investment in communities made vulnerable by the financial system."

Austerity is a bad investment strategy. Failure to maintain and improve infrastructure doesn't just shift costs into the future, it increases those costs far in excess of any rational discount based on the time value of money. Public institutions should discipline markets, not the other way around. Don't give Wall Street a veto over our climate spending. A National Investment Authority could subordinate markets to human thriving:

https://democracyjournal.org/arguments/industrial-policy-requires-public-not-just-private-equity/

Insurance need not be pitted against human survival. Saving the cities and regions whose bonds are held by insurance companies is good for those companies: "Breaking the climate risk doom loop is the best disaster insurance policy money can buy."

I found Arun's work to be especially bracing because of the book I'm touring now, The Lost Cause, a solarpunk novel set in a world in which vast public investment is being made to address the climate emergency that is everywhere and all at once:

https://us.macmillan.com/books/9781250865939/the-lost-cause

There is something profoundly hopeful about the belief that we can do something about these foreseeable disasters – rather than remaining frozen in place until the disaster is upon us and it's too late. As Rebecca Solnit says, inhabiting this place in your imagination is "Completely delightful. Neither utopian nor dystopian, it portrays life in SoCal in a future woven from our successes (Green New Deal!), failures (climate chaos anyway), and unresolved conflicts (old MAGA dudes). I loved it."

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/11/28/re-re-reinsurance/#useless-price-signals

#pluralistic#doom loop#insurance#insuretech#climate#climate risk#climate emergency#the lost cause#market forces#risk management#price signals#control boards#decarbonization#bond vigilantes#climate resilience

262 notes

·

View notes

Photo

Insurtech VCA Software Launches New Digital Insurance Claims Payments in 2022

https://www.prittleprattlenews.com/technology/insurtech-vca-software/

0 notes

Text

Cloud computing insuretech market is expected to reach USD 8,526.60 million by 2028 witnessing market growth at a rate of 10.50% in the forecast period of 2021 to 2028. Data Bridge Market Research report on cloud computing insuretech market provides analysis and insights regarding the various factors expected to be prevalent throughout the forecast period while providing their impacts on the market’s growth.

#Cloud Computing Insuretech Market#Cloud Computing Insuretech Market Share#Cloud Computing Insuretech Market Size#Cloud Computing Insuretech Market Growth#Cloud Computing Insuretech Market Trends#Cloud Computing Insuretech Market Players.

0 notes

Text

The Blockchain Revolution: A New Era for the Insurance Industry.

Introduction:

Imagine a world where the insurance industry is transparent, secure, and decentralized. That's the promise of blockchain technology, a groundbreaking innovation that's reshaping the insurance sector.

This article delves into the transformative power of blockchain, its benefits, and how insurance companies can harness its potential.

1. Enhanced Security and Privacy:

Blockchain, with its cryptographic techniques, offers a decentralized and transparent ledger, significantly reducing the risk of data breaches and unauthorized access. This heightened security fosters trust among customers, encouraging them to share their personal information with insurance companies with greater confidence (Mqougayar, 2016)

2. Simplifying Claims Processing:

Claims processing, often a complex and time-consuming procedure, is being simplified by blockchain's smart contracts. These contracts automate the process, eliminating manual intervention and enabling faster, more accurate settlements. The result? Lower administrative costs and happier customers due to quick and efficient claim resolutions (Tapscott & Tapscott, 2016)

3. Building Transparency and Trust:

Blockchain's inherent transparency allows all parties involved - customers, insurers, and regulators - to access the same data in real-time. This shared source of truth enhances transparency throughout the insurance value chain, fostering collaboration and trust among participants (Mougayar, 2016).

4. Detecting and Preventing Fraud:

Fraudulent activities, such as duplicate claims or falsified documents, are a significant drain on the insurance industry. Blockchain's immutable nature and traceability enable insurers to detect and prevent fraud more effectively, saving resources (Tapscott & Tapscott, 2016).

How to Implement Blockchain in Insurance Companies:

For companies yet to adopt blockchain technology, here are some steps to consider:

1. Education and Awareness:

Invest in educating your team about blockchain technology, its benefits, and potential applications within the insurance industry. This knowledge will help stakeholders embrace the technology with confidence (Mougayar, 2016).

2. Collaboration and Consortia:

Join forces with industry peers, technology providers, and regulatory bodies to accelerate blockchain adoption. By joining consortia or partnerships, insurance companies can pool resources, share knowledge, and develop common standards for blockchain implementation (Tapscott & Tapscott, 2016).

3. Pilot Projects and Proof of Concepts:

Test the waters with pilot projects and proof of concepts. These initiatives allow insurers to assess the feasibility and benefits of implementing blockchain technology in specific areas, such as claims processing or customer onboarding, before scaling up (Mougayar, 2016).

Regulation of Data and Enhanced Client Service:

Blockchain technology provides a transparent and auditable system, facilitating robust data regulation. With blockchain, insurers can ensure compliance with data protection regulations like GDPR. Moreover, customers have more control over their personal data, enhancing data privacy and security (Tapscott & Tapscott, 2016).Blockchain also improves client service by enabling self-service options and real-time access to policy information. Customers can manage their policies, file claims, and track their status effortlessly, improving their overall experience with insurers.Enabling New

Technological Advancements:

Blockchain's distributed and programmable nature paves the way for new technological advancements within the insurance industry. For instance, blockchain can facilitate the integration of Internet of Things (IoT) devices, creating new opportunities for personalized and dynamic insurance products (Mougayar, 2016).

References:Mougayar, W. (2016). The Business Blockchain:

Promise, Practice, and Application of the Next Internet Technology. Wiley.Tapscott, D., & Tapscott, A. (2016). Blockchain Revolution: How the Technology Behind Bitcoin Is Changing Money, Business, and the World. Penguin.

1 note

·

View note

Text

Next-Gen Insurance Solutions for All Your Needs

Looking for insurance solutions that are both innovative and reliable? Our Insuretech solutions combine cutting-edge technology with personalized service to meet your unique needs. Trusted and experienced digital insurance solutions company at your disposal. Book a demo and get an in-depth overview from our product experts.

1 note

·

View note

Text

Odie Pet Insurance partners with Tigerless Insurance

New Post has been published on https://petn.ws/WiNCW

Odie Pet Insurance partners with Tigerless Insurance

Odie Pet Insurance See full company profile “> announced a partnership with Tigerless Insurance, an insurance agency serving people living in the US with different visas. Through this partnership, Tigerless will add pet insurance to its marketplace, which includes life, health, auto, and renter insurance. “Odie was created with the vision to enable other Insuretech […]

See full article at https://petn.ws/WiNCW

#PetInsuranceNews

0 notes

Last Seen Blogs

sullivanreed

— ❛ i choose me now.

malikturmcn

do it for love

amerilistprintingservices

Amerilist Printing

mintesprig

Minte