#canada mortgage rates

Text

Embark on your journey towards homeownership with confidence!

0 notes

Text

Navigating Mortgage Rates in Ontario: A Comprehensive Guide for Homebuyers

In the ever-evolving landscape of the Ontario real estate market, understanding mortgage rates is crucial for anyone looking to buy a home. Mortgage rates can significantly impact your monthly payments and the total interest paid over the life of your loan. This comprehensive guide aims to demystify mortgage rates in Ontario, providing you with the knowledge needed to navigate the market confidently.

Understanding Mortgage Rates

Mortgage rates are essentially the interest rates charged by lenders for borrowing money to purchase a home. These rates can vary based on several factors, including the Bank of Canada’s policy interest rate, the health of the economy, and the borrower's financial situation.

In Ontario, mortgage rates fluctuate due to the dynamic nature of the Canadian economy and the real estate market. Homebuyers can choose between fixed-rate mortgages, where the interest rate remains the same for the term of the mortgage, and variable-rate mortgages, where the rate can change based on market conditions.

Factors Influencing Mortgage Rates in Ontario

Several key factors influence mortgage rates in Ontario:

Economic Indicators: The overall health of the economy, including inflation rates, employment figures, and GDP growth, can impact mortgage rates. A stronger economy typically leads to higher rates, as the demand for borrowing increases.

Bank of Canada Rates: The central bank’s interest rate decisions directly affect prime rates set by banks, which in turn influence mortgage rates.

Real Estate Market Conditions: Supply and demand dynamics in the housing market can also affect mortgage rates. A high demand for homes can lead to higher rates, while an oversupply may lead to lower rates.

Borrower’s Credit Score: Lenders consider your credit score as an indicator of your ability to repay the loan. Higher credit scores can help secure lower mortgage rates.

Current Trends in Ontario's Mortgage Rates

As of my last update, Ontario, like the rest of Canada, has experienced fluctuations in mortgage rates due to economic uncertainties and policy changes by the Bank of Canada. It's important for prospective homebuyers to stay informed about current trends and forecasts by consulting financial news, speaking with mortgage professionals, and using online mortgage calculators.

How to Get the Best Mortgage Rate in Ontario

Securing the best possible mortgage rate can save you thousands of dollars over the life of your loan. Here are some tips to help you get the most favorable rate:

Shop Around: Don’t settle for the first rate you're offered. Compare rates from different lenders, including banks, credit unions, and mortgage brokers.

Improve Your Credit Score: Pay down debt and ensure your credit report is accurate. A higher credit score can lead to better mortgage offers.

Consider the Term and Type: Think about what mortgage term (the length of time you commit to a rate) and type (fixed or variable) best suit your financial situation.

Negotiate: Don’t be afraid to negotiate with lenders. Often, there is some room for negotiation on the interest rate or other terms of the mortgage.

Lock in Your Rate: If you anticipate that rates will increase, consider locking in your rate with a pre-approval. This can protect you from rising rates while you shop for your home.

The Impact of Mortgage Rates on Ontario's Housing Market

Mortgage rates have a direct impact on Ontario’s housing market. Lower rates make borrowing cheaper, potentially increasing the demand for homes and driving up prices. Conversely, higher rates can cool down the market by making borrowing more expensive, reducing demand.

Future Outlook

Predicting future mortgage rates involves considering various economic and political factors, including inflation, global economic trends, and Bank of Canada policy decisions. While it's impossible to predict rates with certainty, staying informed about these factors can help you make more educated decisions when managing your mortgage.

Conclusion

Understanding and navigating mortgage rates in Ontario is a complex process that requires diligence and research. By staying informed about the factors that influence rates and following strategic steps to secure the best possible rate, homebuyers can save significant amounts of money and make their dream of homeownership a more affordable reality.

Remember, consulting with financial advisors and mortgage professionals can provide personalized advice tailored to your financial situation, helping you to navigate the complexities of the Ontario mortgage landscape with confidence.

#Mortgage Rates#Mortgage Rates on Ontario#Best Mortgage Rate#fixed-rate mortgages#Bank of Canada#best possible rate

0 notes

Text

Navigating the Canadian Mortgage Landscape: Understanding Mortgage Rates

Securing a mortgage is a significant financial decision, and understanding the nuances of mortgage rates in Canada is paramount for prospective homebuyers. As one of the key elements in determining the cost of homeownership, mortgage rates can influence the overall affordability and financial feasibility of purchasing a property. In this guide, we delve into the factors that shape mortgage rates in Canada, guide about mortgage calculator and offer insights to help you make informed decisions in your homebuying journey.

The Basics of Mortgage Rates:

Mortgage rates represent the interest charged by lenders on the amount borrowed for a home loan. In Canada, these rates can be fixed or variable, each carrying its own set of advantages and considerations.

Influence of the Bank of Canada:

The Bank of Canada plays a pivotal role in shaping mortgage rates. The central bank's decisions regarding the overnight lending rate directly impact the interest rates offered by financial institutions. Understanding the Bank of Canada's rate movements is crucial for predicting trends in mortgage rates.

Fixed-Rate Mortgages:

Fixed-rate mortgages in Canada maintain a constant interest rate throughout the mortgage term. This stability offers predictability for homeowners, allowing them to budget effectively without being affected by fluctuations in interest rates.

Variable-Rate Mortgages:

Variable-rate mortgages, on the other hand, are linked to the prime rate set by financial institutions. These rates can change in response to shifts in the economy, making them potentially more flexible but also subject to market volatility.

Economic Factors Impacting Mortgage Rates:

Various economic factors influence mortgage rates in Canada. Factors such as inflation, employment rates, and global economic conditions can all play a role in shaping the interest rates offered by lenders.

Credit Scores and Mortgage Rates:

The creditworthiness of a borrower is a key determinant in the interest rate they are offered. Individuals with higher credit scores often qualify for lower mortgage rates, highlighting the importance of maintaining good credit health.

Market Competition Among Lenders:

The Canadian mortgage market is competitive, with numerous lenders vying for borrowers' attention. This competition can lead to variations in mortgage rates, providing homebuyers with opportunities to secure favorable terms through diligent comparison shopping.

Rate Comparison and Negotiation:

Homebuyers are encouraged to compare mortgage rates offered by different lenders. Negotiation is a valuable tool in securing a competitive rate, and borrowers should feel empowered to discuss terms with their lender to achieve the most favorable outcome.

Timing the Market:

Timing plays a role in securing favorable mortgage rates. Monitoring market conditions and being aware of potential shifts can empower homebuyers to lock in rates when they are advantageous.

Conclusion:

Navigating the landscape of mortgage rates in Canada requires a blend of economic awareness, financial acumen, and strategic decision-making. As you embark on your homeownership journey, understanding the factors that influence mortgage rates will empower you to make informed choices, ensuring that your mortgage aligns with your financial goals and circumstances. Whether opting for the stability of a fixed-rate mortgage or the potential flexibility of a variable-rate mortgage, knowledge is the key to securing a mortgage that suits your needs in the dynamic Canadian real estate market.

#savemaxcanada#save max realestate#savemax#canada#realestate#homes for sale#save max#real estate#houses for sale#realestatecanada#mortgage rates#mortgage calculator

0 notes

Text

Expected wave of mortgage renewals contributed to latest rate hold: Bank of Canada

The large number of mortgages coming up for renewal at higher rates is one reason why the Bank of Canada decided to leave its target rate unchanged at 5.00% last month.

Bank of Canada Governor Tiff Macklem made the comment Wednesday while testifying before the Standing Senate Committee on Banking, Commerce and the Economy.

“One of the important reasons why we held our policy rate at 5% is that we…

View On WordPress

0 notes

Text

2023 Mortgage Rate Trends: What to Expect?

It’s already September, and 2023 is coming to an end. We have to revise some crucial 2023 mortgage market trends before the year-end.

There has been a lot of rise and fall in the Canadian housing market in 2023. However, there is a consistency in the overall trends that dominate the mortgage market. This article is about the changes in the mortgage market trends and what it means for you as a home buyer. We’ll discuss the effects of a volatile market on home purchase mortgage rates. The readers will know what to expect from the overall home mortgage scene and can brace themselves.

0 notes

Text

Exploring Current Mortgage Rates in Canada: A Comprehensive Guide

Are you considering buying a home or refinancing your existing mortgage in Canada? One crucial factor to consider is the current mortgage rates. Mortgage rates play a significant role in determining the cost of borrowing and can have a substantial impact on your overall financial situation. In this blog post, we will dive into the world of mortgage rates in Canada, providing you with valuable insights and up-to-date information to help you make informed decisions. Let's explore the current mortgage rates in Canada and understand the factors that influence them.

Understanding Mortgage Rates in Canada:

What are mortgage rates?

Mortgage rates refer to the interest rates charged by lenders on mortgage loans. They determine the cost of borrowing and affect your monthly mortgage payments. Mortgage rates can be either fixed or variable, with fixed rates remaining constant throughout the mortgage term and variable rates fluctuating based on market conditions.

Factors influencing mortgage rates:

Various factors contribute to the determination of mortgage rates in Canada. These include:

a. Economic conditions: Mortgage rates are influenced by broader economic factors such as inflation, unemployment rates, and the overall health of the economy.

b. Bank of Canada's policy rate: The Bank of Canada's key interest rate, known as the overnight rate, directly impacts mortgage rates. Lenders base their rates on this benchmark rate, which is set to manage inflation and promote economic stability.

c. Bond yields: Canadian mortgage rates are closely tied to bond yields. When bond yields rise, it typically leads to higher mortgage rates, and vice versa.

d. Lender competition: Mortgage rates can also vary based on the level of competition among lenders. Some lenders may offer promotional rates or special deals to attract borrowers.

e. Borrower's creditworthiness: Your credit score, income stability, and debt-to-income ratio can influence the mortgage rate you qualify for. Lenders typically offer lower rates to borrowers with strong credit profiles.

How to find current mortgage rates:

To access current mortgage rates in Canada, you can:

a. Visit lender websites: Many banks and mortgage brokers provide up-to-date information on their websites, allowing you to compare rates from different lenders.

b. Utilize rate comparison websites: Online platforms provide the convenience of comparing rates from multiple lenders in one place. This helps you find competitive offers and narrow down your options.

c. Consult with a mortgage broker: Mortgage brokers have access to multiple lenders and can provide personalized guidance based on your financial situation. They can help you find the best rates and mortgage terms suited to your needs.

d. Stay informed through financial news sources: Newspapers, financial publications, and online news portals often report on changes in mortgage rates, offering valuable insights.

Conclusion:

Keeping yourself updated on the current mortgage rates in Canada is essential when making significant financial decisions related to homeownership. Understanding the factors that influence these rates and exploring various sources to find the best rates for your specific needs can help you secure a mortgage that aligns with your financial goals. Remember, mortgage rates are subject to change, so regular monitoring and careful consideration are crucial. By staying informed and seeking expert advice, you can navigate the world of mortgage rates in Canada with confidence and make well-informed decisions for your future.

0 notes

Text

GT Mortgages offers the lowest mortgage rates in Canada. Our knowledgeable team assists you in securing affordable rates that are suited to your financial objectives. Call us right away!

0 notes

Video

Mortgages Montreal

If you are looking for the best rate in Montreal on a mortgage or other purchase in the Montreal CA area. Then Mortgages Montreal is one of the best Mortgage refinancing companies in the Montreal CA region. We are always looking to provide our customers with more choices and access to hundreds of mortgage products.

#mortgage montreal#purchase montreal#mortgage broker montreal#best mortgage rates montreal#specialiste hypothecairec#mortgage brokers Montreal#mortgage refinancing Canada#Home refinancing companies Canada#mortgage refinancing brokerage Montreal#Mortgage refinancing Montreal#mortgage loan refinancing Canada#Refinancing for home loan Montreal

1 note

·

View note

Text

Debunking the Myths and Misconceptions of Getting a Mortgage: Understanding Your Mortgage Options in Canada

When it comes to mortgages, there are a lot of myths and misconceptions that can lead to confusion. Whether you're a first-time homebuyer or an experienced investor, understanding what is true and what isn't can make all the difference when it comes to making sound financial decisions about your mortgage. This article will look at Canada's most common mortgage myths and misconceptions to help readers make informed choices about their financial future. So without further ado, let's get started!

Myth 1 - First time home buyers are the only people who can put 5% down

When it comes to mortgages, one of the most common myths is that only first-time home buyers are allowed to put down a 5% deposit. However, contrary to popular belief, anyone seeking to buy a house - even if they previously owned one - can put down as little as 5% for their owner-occupied residence.

At this point, I've lost track of how many times someone has called me and been misled about the fact that they needed 20% down to purchase an owner-occupied house simply because they weren't first-time homebuyers.

It's important to remember that mortgage insurance must be obtained in all cases when putting down less than 20%, so it's important to factor this into your budget and understand the costs associated with taking out an insured mortgage. Don't hesitate to contact us if you have questions about your downpayment or any associated insurance premiums will cost.

Refer to our reliable and convenient mortgage calculators to accurately determine your mortgage payment based on the downpayment you provide. For those just starting in their home-buying journey or for the seasoned veterans who need a refresher, our Mortgage 101 video will explain all of the fundamentals of mortgages.

youtube

Myth 2 - Refinancing a mortgage prior to its maturity does not make financial sense when prepayment penalties are involved.

Prepayment penalties are one of a mortgage's most misunderstood elements, and many believe that these fees make it impossible to refinance a loan before maturity. Contrary to popular belief, not all lenders impose heavy prepayment charges. There are plenty of loan providers who have less severe penalties than others.

It is essential to be aware of the potential pre-penalty costs when deciding on your mortgage, in addition to merely focusing on obtaining the lowest rate. From my observations, I have noticed that in recent years approximately 60% of homeowners have chosen to terminate their contracts prematurely. Undoubtedly, this was due to the rising home prices.

If borrowers have fixed mortgages, they can expect to face three months interest penalty or an IRD penalty. Certain lenders have huge IRD penalties; while I won't name names, it's possible that you currently have part of your savings in one of these institutions.😉

IRD

The Interest Reduction Deposit (IRD) is based on the amount of your prepayment and the interest rate difference between your original mortgage rate and what lenders can charge for loans with a similar remaining term. Each lender has its own way of calculating IRD penalties.

If you are looking for an effective way to consolidate debt, then refinancing your mortgage and only paying the three-month interest might be a wise choice. The benefits of this approach outweigh any other methods of debt repayment that you may consider. If you have been fortunate enough to secure a reasonable mortgage with beneficial terms, this could be an effective way of consolidating your debts quickly and efficiently. Even if you face an IRD penalty, some lenders calculate these much more forgivingly than others. It is important to note that variable-rate mortgages are subject to three-month interest penalties, which explains why many people who anticipate selling or refinancing their homes early opt for a variable-rate mortgage.

I can't stress this enough you must take the time to thoroughly review and comprehend the fine print in your mortgage agreement before signing, as this ensures you are familiar with any prepayment penalties lurking down the line.

Myth 3 - Private mortgages are only for people with bad credit

Private mortgages are a viable option that is often overlooked due to the misconception that they are only for people with bad credit. This could not be further from the truth! Private mortgages are an excellent choice for individuals with good credit who need a little help getting their mortgage approved.

One of the primary advantages of opting for a private mortgage is that you can receive financing quickly, sometimes within 48 hours! Banks are notorious for taking weeks – if not months – to approve mortgages. With a private mortgage, however, you can be approved and ready to purchase your dream home much faster.

When you take the private route, lenders may be more likely to overlook any home-related imperfections, such as a bad roof or unfinished construction.

Private mortgages can be a great option if you are self-employed or an entrepreneur without traditional income streams. Many of these types of loans don't require proof of income.

If your current liabilities have caused a high total debt service ratio, private mortgage lenders may be more willing to approve you for financing. Typically, private lenders don't focus as heavily on borrowers' debt when approving loans and instead are interested in the property's value and equity.

However, one of the drawbacks is that private mortgages usually carry higher interest rates than traditional ones. Therefore, you should research and compare the terms of different lenders before deciding.

Overall, private mortgages can be an effective way to finance a home, and they should not be overlooked due to the misconception that they are only for those with poor credit.

To ensure you get the best mortgage for your needs, you must arm yourself with facts and knowledge. Start by carefully researching the different private mortgage options available so you can choose the best one for you. Then, if you're ready to get started on getting a private mortgage, read our private mortgage page here. And if you need some help navigating this process, don't hesitate to reach out and chat with one of our helpful mortgage experts today!

Myth 4 – Self-employed individuals have a more challenging time qualifying for a mortgage

Self-employed individuals may face unique challenges when qualifying for a mortgage, but that does not mean it's harder. The truth is self-employed people qualify for mortgages all the time, provided they can demonstrate their income and financial stability.

When applying for a mortgage with an A+ lender as self-employed, you must demonstrate that you can repay the loan. To do this, applicants must submit various documents such as two years of T1 generals, business statements displaying their net profit and Notice of assessments indicating taxes paid. These lenders consider your average net income from the past two years while also allowing us to gross up that income by an additional 15%, depending on your field.

By taking advantage of tax write-offs, some alternative lenders can allow you to use your six-month bank statement and gross it annually. We need to examine the expenses that you have incurred, but this route usually provides a higher net income which will enable you to qualify for larger loans.

When dealing with alternative lenders, interest rates may be 1% higher than A+ lenders and come with additional fees. But taking into account the entire picture, these increased costs could be offset by your tax write-offs at the end of the year if your income warrants it. Although there may be an additional cost on your mortgage loan, this could result in substantial savings in the long run.

Please remember that it is essential to speak with a mortgage professional and an accountant before making any decisions so that they can give you the best advice and help you make an informed decision.

In conclusion, many myths and misconceptions about mortgages in Canada can lead to confusion for potential borrowers. Here, we have debunked four mortgage myths:

Only first-time home buyers can put 5% down - FALSE.

Refinancing a mortgage before maturity does not make financial sense when prepayment penalties are involved. - FALSE.

Private mortgages are for only those with bad credit – again, FALSE.

And lastly, self-employed individuals have a more challenging time qualifying for a mortgage loan, absolutely not TRUE!

We hope this article increases your understanding of mortgages and encourages you to ask more questions as you embark on your home journey. Good luck, and as always, if you have any questions or require clarification about the mortgage process, don't hesitate to contact us.

Dallas Martin

519-495-7250

The Mortgage Firm

License # 13466

Mortgage Agent -M17001133

www.newlifemortgages.ca

0 notes

Text

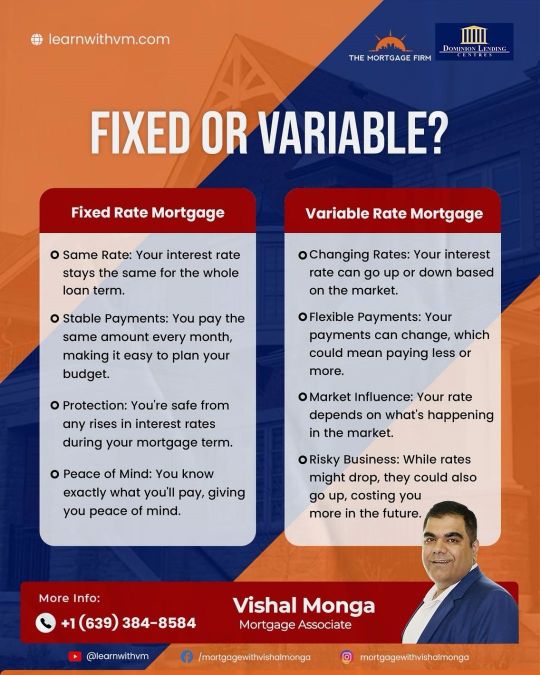

Unlock Your Dream Home with Your Best Mortgage Broker in Brampton

Looking to secure the keys to your dream home in Brampton? Look no further than Vishal Monga Mortgage, your trusted partner in navigating the complexities of mortgages. With years of expertise and a dedication to client satisfaction, Vishal Monga Mortgage stands out as the premier choice for individuals and families seeking the best mortgage solutions in Brampton. Our personalized approach ensures that each client receives tailored advice and assistance, guiding them through every step of the mortgage process with clarity and confidence. Whether you're a first-time buyer or a seasoned homeowner, Vishal Monga Mortgage is committed to finding the perfect mortgage option to suit your needs. Experience the difference with the best mortgage broker in Brampton - contact Vishal Monga Mortgage today and let's make your homeownership dreams a reality.

0 notes

Text

The market consensus on the mortgage rate forecast in Canada (as of October 13, 2022), is for the Canada Mortgage Rates increase by another 1.00%, to a 4.25% high in 2022, with a potential for further increases in 2023 if inflation is not on track to drop less than 4.25%.

0 notes

Text

What is the Average Age to Buy Your First Home in Canada?

For many Canadians, buying a home is a significant milestone in their lives. However, the average age at which Canadians buy their first home can vary depending on several factors. In this blog post, we will explore the average age of first-time homebuyers in Canada, the factors that influence this age, and tips for those looking to buy their first home.

Factors Affecting the Average Age of First-time Homebuyers:

Several factors influence the average age at which Canadians buy their first home. The first factor is the affordability of housing. The cost of homes in Canada's major cities, such as Vancouver and Toronto, has increased significantly in recent years, making it challenging for first-time buyers to enter the market.

The second factor is the economic climate. When the economy is doing well, and employment rates are high, more people can afford to buy their first homes. Conversely, during periods of economic uncertainty, people may delay purchasing a home until they feel more secure about their finances.

The third factor is cultural attitudes towards homeownership. Some cultures prioritize homeownership as a marker of success and independence, while others view it as less important. These cultural differences can influence the average age at which people buy their first homes.

Regional Variations in the Average Age of First-time Homebuyers:

The average age of first-time homebuyers in Canada varies by region. According to a report by the Canadian Mortgage and Housing Corporation (CMHC), the average age of first-time homebuyers in Toronto is 35. In Vancouver, it is 33, while in Calgary, it is 32.

In contrast, in smaller cities and rural areas, the average age of first-time homebuyers is lower. For example, in Halifax, the average age is 29, while in St. John's, it is 28.

Tips for First-time Homebuyers in Canada:

If you are a first-time homebuyer in Canada, there are several things you can do to make the process smoother. Here are some tips to keep in mind:

Determine your budget: Before you start looking for a home, it's essential to determine how much you can afford to spend. Consider your income, expenses, and any other financial commitments you have.

Get pre-approved for a mortgage: Getting pre-approved for a mortgage can give you an idea of how much you can borrow and help you narrow down your search for a home.

Work with a real estate agent: A real estate agent can help you find properties that meet your needs and budget and guide you through the buying process.

Consider the location: The location of a property can impact its value and your quality of life. Consider factors like proximity to public transportation, schools, and amenities.

Conclusion:

The average age at which Canadians buy their first home varies depending on several factors, including affordability, economic climate, and cultural attitudes. Regional variations also exist, with younger first-time homebuyers in smaller cities and rural areas. For first-time homebuyers in Canada, determining your budget, getting pre-approved for a mortgage, working with a real estate agent, and considering the location can help make the process smoother.

0 notes

Text

Mortgage Trigger Rate Explained

Mortgage Trigger Rate Explained

The Bank of Canada has raised interest rates for the 5th time in 2022, on October 26. The overnight rate is now sitting at 3.75%. Back in January, it was 0.25%. With galloping inflation, the Bank of Canada made no secrets it would continue raising interest rates. Most economists believe the overnight rate will be 4% by the end of 2022.

An increase -or decrease- in the overnight rate impacts…

View On WordPress

#bank of canada#fixed mortgage canada#interest rates#money#mortgage#mortgage canada#overnight rate canada#prime rate canada#trigger point#trigger rate#variable mortgage canada#variable rate canada

1 note

·

View note

Text

It is the fear of falling house prices which are making central banks change course

It is the fear of falling house prices which are making central banks change course

It was only a few short weeks ago that the headlines were telling us this.

Traders ramped up wagers on the scale of interest-rate hikes by the Bank of England in the short term, to deal with markets in turmoil over the government’s economic plans.

Money markets priced in more than 200 basis points of increases by the BOE’s next meeting in November, four times the size of its last hike. The…

View On WordPress

#Australia#Bank of Canada#Bank of England#business#Canada#economy#Finance#house prices#Interest Rates#mortgage rates#Reserve Bank of Australia

0 notes

Text

News Wrap: U.S. sanctions Iran's 'morality police' after young woman's death

News Wrap: U.S. sanctions Iran’s ‘morality police’ after young woman’s death

In our news wrap Thursday, the U.S. imposes sanctions on Iran’s morality police as protests continue over the death of a young woman in custody, Republicans in the Senate blocked action on forcing the disclosure of “dark money” donors to political causes and average rates on 30-year mortgage rates have hit their highest level since 2007.

Stream your PBS favorites with the PBS…

View On WordPress

#anti-hijab protests#Bermuda#Canada#Congress#dark money#extreme weather#house#hurricane fiona#Iran#morality police#puerto rico#rising mortgage rates#russia#russian invasion of ukraine#Senate#U.S. sanctions of Iran#Ukraine#UN General Assembly#UN security council

1 note

·

View note

Last Seen Blogs

petrklic-art

Petrklicek the Third

tarikuy

Tarikuy

worship-my-body

I'll worship yours

reinekoya

Rei/ Roy

poopballs-blog

death at sea—she's hooked.