#Compare Mortgage interest Rates

Text

Because of the position of our house (and the fact that we have more windows than walls) the sun shines on our verandah/lounge room from the moment it rises until it ducks behind the mountain (3pm in winter 8pm in summer). I think our house gets more sun than anyone else in the suburb, all the other houses are shaded for the majority of the day by trees, other houses, or the mtn because they sit right where the incline increases, but our house is on a v wide corner at the end of the street, so there's no house next to us, the house behind us is MUCH lower (we block their sun lol rip) and the house across the road is v far (the mtn blocks the sun before their house can). Basically we may have bought a house at the worst time in history but we hit the sunshine lottery lol

#i think a lot about how#the circumstances that required us (me) to buy a house at the worst time (my grandparents' care needs) allowed us to actually buy it#(the sale of their house and legally gifting me the money)#as much as everything is SO EXPENSIVE please stop taking my MONEY when i am trying to SURVIVE#our mortgage is so small compared to most peoole who bought a house in the last 3 years#when the news shows how much the latest interest rate rise will affect mortgage repayments#the lowest mortgage loan amount they show is still bigger than our current loan#so i know we have it so much easier than almost everyone#which is horrifying 😩#anyway i always pretend the cost of the house included the minimum 8 hours of sun a day we get#and feel better about it lol ☀️#tp

5 notes

·

View notes

Text

#A home equity line of credit#or HELOC#is a type of loan that allows homeowners to borrow against the equity in their home. It is similar to a credit card#where homeowners can borrow a certain amount of money and make payments over time#but with a HELOC#the interest rates are typically lower and the terms are longer.#To get a home equity line of credit#there are several steps that homeowners need to follow:#Determine your home equity: Home equity is the difference between the value of your home and the amount you owe on your mortgage. To determ#you will need to get an appraisal of your home or use an online tool to estimate its value.#Check your credit score: A good credit score is important when applying for a home equity line of credit. Lenders will use your credit scor#Gather necessary documents: You will need to provide documentation to the lender when applying for a home equity line of credit. This inclu#proof of employment#and proof of your mortgage payments.#Shop around: It is important to shop around and compare rates and terms from different lenders before deciding on a home equity line of cre#Fill out an application: Once you have gathered all of the necessary documentation and chosen a lender#you will need to fill out an application. This will typically include information about your financial situation#your credit history#and the property you are borrowing against.#Wait for approval: After you have submitted your application#the lender will review it and determine whether you are eligible for a home equity line of credit. This process can take a few weeks#and you will be notified once the lender has made a decision.#Sign the loan documents: If your application is approved#you will need to sign the loan documents and agree to the terms of the home equity line of credit. Make sure you understand all of the term#Once you have a home equity line of credit#you can use the funds for any purpose#such as home renovations#paying off debt#or paying for unexpected expenses. Just make sure to make your payments on time and keep your balance within your approved credit limit to#PCLinesOfCredit

0 notes

Text

#life insurance mortgage protection#Compare Mortgage interest Rates#Family financial planning#Get free Life Insurance Quote#Life insurance Quotation#online life insurance quotes

0 notes

Text

Liz Truss is the most disastrous and unpopular leader in modern British history. Mortgage holders and small businesses still loathe her for sending interest rates through the roof. Her short, catastrophic premiership is routinely compared unfavourably to the shelf life of a lettuce. (A comparison first made by the bright leader writers at the Economist to give credit where it is due.)

When Labour wins the next election, its triumph will be in part the result of the public’s reaction against her vast and dogmatic economic folly.

If you were Liz Truss, you might retire from public life. At the very least you would apologize and hang your head in shame.

If readers expect contrition, however, they have yet to learn that being on the radical right means never having to say you are sorry.

Truss’s demotion from national leader to national joke has not embarrassed her in the slightest but pushed deep into paranoid conspiracism.

Her autobiography, bizarrely titled Ten Years to Save the West, as if the fate of liberal democracy depended on the advice of an epic failure, shows that, despite all she did to this country, her eyes still shine with a bright, self-righteous fanaticism, as if the sockets are backlit by an idiot’s lantern,

Chutzpah used to be defined as murdering both your parents and asking the court for clemency because you are an orphan. In Truss’s case it is using the power of the prime minister to crash the economy and then claiming she was a powerless victim of the liberal elite.

Her writing is as lacking in self-awareness as it is powered by self-righteousness.

At one point she says in all innocence that, when Boris Johnson resigned in the summer of 2022, her agent encouraged her to join the race to be prime minister, as the campaign might be good for her profile.

But she reports that he then wisely added “it would be for the best if I came second”.

Later she informs us that during the leadership campaign she “frankly lost trust in many of my erstwhile ministerial colleagues who were supporting my opponent [Rishi Sunak].

“They had spent the last six weeks not just attacking me but seeking to undermine my plans, saying my agenda was unworkable."

Truss never stops to think that the few people who will finish this book will believe that her agent was right, and it would clearly have been for the best if she had never been prime minister.

Nor does she contemplate the possibility that her agenda was indeed “unworkable”, and was proved to be unworkable when her unfunded tax cuts and fuel subsidies sent the price of gilts shooting up, the value of the pound crashing down, and caused a crisis in the pension industry for good measure.

And yet, and yet…Mock her as much as you like. Please don’t hold back on my account. But you cannot dismiss her.

There are two reasons why Truss is still dangerous. The first lies in the strength of the right-wing clique that brought her to power.

It is true that Liz Truss did not become prime minister by winning over Conservative MPs. As with Jeremy Corbyn’s leadership of the Labour party, Truss’s career illustrates the danger of expecting leaders who do not have the support of a plurality of their colleagues to function in a Parliamentary democracy.

But she still beat Rishi Sunak with the votes of 57 percent of Tory members.

And with the honourable exception of the Times, the Tory press was all for her. “In Liz We Trust”, said the Express “Cometh the Hour, Cometh the Woman”, cried the Mail. “Liz Puts Her Foot on the Gas”, cheered the Sun.

Kwasi Kwarteng set off a market panic as he put Truss’s ideas into practice in the mini budget of September 2022. The reaction of right-wing papers was not one of alarm, however, but of adoration.

“At last”, gushed the Daily Mail, “a True Tory Budget”. A Daily Telegraph commentator said it was “the best Budget I have ever heard a British Chancellor deliver”.

Meanwhile the Truss premiership allowed the voodoo economics of the US-influenced (and in all probability US-financed) think tanks to finally impose itself on this luckless country. The Centre for Policy Studies welcomed the mini-budget saying it was “exactly what we would have hoped for”. The Taxpayers’ Alliance called it “the most taxpayer-friendly budget in recent memory”.

Robert Saunders of Queen Mary University made the unarguable point that Truss was not an aberration or some alien figure that had appeared from nowhere to take over the Conservative party.

Follow the money that cascaded in from party donors, he said, and “the Truss premiership begins to look less like the personal failure of a flawed individual, and more like a systemic disaster for which the party bears collective responsibility”.

Those forces will dominate the Conservative party after its defeat and drive it to the radical right. Indeed, in opposition the members, the think tanks, the press and the ideologue donors will become more important, for they will be all the party has.

In a sign of things to come, Truss is already allying with Nigel Farage, and even Rishi Sunak says he will not ban Farage from joining Conservative party.

Despite her failure, Truss remains a potent figure on the radical right because of her championing of revanchism, which is now its dominant emotion.

This isn't a book. It’s a 300-page wail of resentment at a world that will not do as it is told.

I have no problem with conservatives complaining about woke policies taking over institutions. Only a fool or liar maintains that progressive biases among supposedly impartial organisations are an invention of the right,

But the woke conspiracy Truss invokes is of a wholly different order. It is utterly fantastical.

To recap, Truss's unfunded subsidies and tax cuts panicked the bond markets. They would not lend to a country whose leaders lacked plausible means of meeting its debts. Or if they did lend they would demand an additional yield on government bonds, which became known in plain-speaking financial markets as the “moron premium”: the extra cost that comes with lending to a nation run by idiots.

In her apologia Truss, who still poses as a Thatcherite, no longer sees markets as an expression of the wisdom of crowds, but as a conspiracy to do her down.

“I came to realise there is no such thing as ‘the market’ in this sense. Rather, there are groups of influential individuals in the financial establishment, all of whom know and speak to one another in a closed feedback loop. The Treasury, the Bank of England, and the OBR are deeply embedded in these social networks and share the same beliefs in the established economic orthodoxy."

The markets were at fault for not seeing her financial genius. Financial traders were the world’s unlikeliest lefties. Even though she and Kwarteng fired the permanent secretary at the Treasury and cut out the Bank of England and Office for Budget Responsibility from policy making, they were still, somehow, responsible for Tory failure.

“The powerful vested interests there pushed back, made my life very difficult and ultimately got me fired,” Truss concludes.

Older readers may remember a time when Conservatives insisted on personal responsibility. You were not allowed to blame crime on poverty or your failings on a bad childhood. You were accountable.

But the case of Liz Truss proves that these morality tales were only ever for the poor. In her mind, the economy collapsed not because of decisions she made but because of “a sustained whispering campaign by the economic establishment, encouraged and fueled by my political opponents in the Conservative Party who refused to accept my mandate to lead”.

Trumpism is the end point of such conspiracism and revanchism, and Truss goes all the way down the line to the terminus.

She mutters about the “deep state” a Trumpian phrase she uses without irony or self-knowledge.

And even though her support for Ukraine was her redeeming feature during her time as foreign secretary and prime minister, she is now supporting the pro-Putin Trump and his allies in Congress who are denying aid to Kyiv.

Truss is finished. But the resentment born of failure and the fury at modernity ensures Trump is still very much with us.

If he delights Putin and wins in November, the UK and Europe will learn the hard way that the real threat to Western civilisation comes from Liz Truss and her friends.

17 notes

·

View notes

Text

Book Review 64 – Poverty, by America by Mathew Desmond

I read Desmond’s Evicted a while back and found it a really excellent bit of sociology/journalism about the specifics and mechanisms of housing inequality and how modern slumlords exploit the poor. So this has been vaguely on my list for a decent while. Sadly, I found it a bit of a disappointment – more listing of facts and statistics that I already basically knew to support a manifesto than anything new or enlightening to me. Not that it’s bad, but if it was 20 pages instead of 200 I’m not sure much of value would really have been lost. Many such cases, I suppose.

The book is about exactly what it says is, a polemic decrying and investigation into why the United State’s poverty rates, and why extremes of material want are so much more common there than in comparable (poorer, even) western democracies. Refreshingly, Desmond has a clear thesis he doesn’t beat around the bush before saying – self-interest, essentially. The affluent benefit from having an underclass to extract resources from, and from excluding its members from the amenities they share, so they do. The book spends most of its wordcount enumerating and describing what Desmond considers the main problems: direct exploitation (underpayment, predatory financiers, slums, etc), an underresourced and misdirected wellfare state (compare the cost of middle/upper-class targeted programs like the mortgage interest deduction or tax-exempt savings accounts to the cost of adequately ending hunger or providing healthcare) and segregation (both spatial/residential and in terms of access to public or semi-public services).

It’s pretty traditional for a book like this to spend 90% of its wordcount diagnosing problems and then end with some publisher-mandated optimism and a chapter of solutions with a fraction of the care put into them as in the diagnosis. Desmond, to his credit, avoids this – each chapter includes both the problems and he considers the most feasible solutions to them to be. He actually makes a point of it, arguing that having practical, winnable goals that will actually improve things when achieved (and then celebrating them when they are) is a key part of any political organizing with a chance of actually working. Now, what I think of those solutions varies quite wildly, but they’re there and exactly what you’d expect for his politics – and speaking as someone whose been renting my entire life I wholly endorse fucking all the tax benefits you get essentially for having the cash on hand to make a down payment. (Relatedly, the book has a great deal of scorn for comfortable, affluent people whose progressive politics amount to lots of critiquing and zero actual positive action.)

Desmond is clearly writing this from the point of view of a(n inspirational) public intellectual; that is, by writing this he’s trying to call an audience and movement based around it into being. He likes the label Poverty Abolitionist and the central project of the book is basically trying to make it happen as an umbrella term people identify with – especially the affluent well-heeled people who read books like this, and might be persuaded to start boycotting companies for underpaying their employees or union-busting, or campaigning against government subsidies that benefit them instead of the poor. I did appreciate the relative hopeful tone, given the usual coverage of American politics – or, well, is ‘Washington was at least this fucked when it passed the Civil Rights Act or the New Deal” optimistic? Whatever the right word is.

Now, I’m summarized all this in ~500 words, obviously actually making the argument needs more space than that. But it really did not need to be as long as it was – a huge fraction of the wordcount is spent either restating arguments or just throwing around numbers and statistics without really contextualization (anyone who spends so much time comparing expenses and budgets across the decade should be legally required to adjust for inflation imo). There’s a good, well-cited (excessively cited, if anything. The footnotoes are like a fifth of the book) persuasive essay in here, but there is so much fat to cut around it.

Anyway yes, disappointing reading experience, given I was hoping for more sociology and less polemic. But as far as American political polemic goes, it’s pretty decent.

23 notes

·

View notes

Text

Investment Property Loans Made Simple

Investing in property holds the promise of financial freedom, yet navigating the world of investment property loans can seem daunting. With NZ Mortgages as your guide, you can embark on this journey with confidence. Let’s delve into the fundamentals of investment property loans, so that you get clarity and insight to get on the path to realising your financial goals.

Understanding Investment Property Loans

Investment property loans differ from traditional home loans in several key aspects. While both involve borrowing money to purchase property, investment loans are specifically tailored for properties that are not occupied by the owner. These loans typically have higher interest rates and stricter eligibility criteria due to the increased risk associated with investment properties.

Types of Investment Property Loans

Fixed Rate Loans:

With a fixed-rate loan, the interest rate remains constant throughout the loan term, providing stability and predictability in repayments. This option is ideal for investors seeking protection against potential interest rate fluctuations.

Variable Rate Loans:

Variable rate loans are subject to changes in interest rates, which can either increase or decrease over time. While this option offers flexibility and the potential for lower interest rates, it also carries the risk of higher repayments if rates rise.

Interest-Only Loans:

Interest-only loans allow investors to pay only the interest portion of the loan for a specified period, typically five to 10 years. This can provide short-term cash flow benefits by reducing monthly repayments, but borrowers must be prepared for higher repayments once the interest-only period ends.

Eligibility and Requirements

Before applying for an investment property loan, it's essential to understand the eligibility criteria and requirements set forth by lenders. Key factors that lenders consider include:

Credit Score:

A strong credit score demonstrates a borrower's ability to manage debt responsibly and is a crucial factor in determining eligibility for an investment loan.

Debt-to-Income Ratio:

Lenders assess the borrower's debt-to-income ratio to ensure they have sufficient income to cover loan repayments. Lower ratios indicate less financial strain and may improve loan approval chances.

Loan-to-Value Ratio (LTV):

The LTV ratio compares the loan amount to the property's value, with lower ratios typically resulting in more favourable loan terms. Lenders may require a higher deposit for investment loans to mitigate risk.

Benefits of Investing in Property

Investing in property offers numerous benefits that can contribute to long-term financial stability and growth:

Rental Income:

Investment properties generate rental income, providing a steady stream of cash flow that can be used to cover loan repayments and expenses.

Capital Appreciation:

Over time, property values tend to increase, allowing investors to build equity and potentially realise capital gains on selling the property.

Tax Advantages:

Property investors may benefit from tax deductions on mortgage interest, property depreciation, and other expenses, reducing their overall tax liability.

While investment property loans offer opportunities for wealth creation, it's crucial to be aware of potential risks and considerations:

Market Volatility:

Property markets can be subject to fluctuations in supply and demand, economic conditions, and government policies. Investors should conduct thorough market research and risk assessments to mitigate exposure to volatility.

Vacancy and Cash Flow:

Vacancies in rental properties can disrupt cash flow and impact loan repayments. Investors should budget for potential vacancies and have contingency plans in place to cover expenses during lean periods.

Property Maintenance and Management:

Owning an investment property entails responsibilities such as maintenance, repairs, and tenant management. Investors should budget for these expenses and consider outsourcing property management services if needed.

Interest Rate Risks:

Variable rate loans are susceptible to changes in interest rates, which can affect borrowing costs and cash flow. Investors should assess their risk tolerance and consider strategies such as fixing interest rates or creating buffers to mitigate interest rate risks.

Working with NZ Mortgages

NZ Mortgages specialises in helping investors navigate the complexities of investment property loans. With our expertise and personalised approach, we empower clients to make informed decisions and achieve their financial objectives. Our services include:

Loan Comparison:

We offer a wide range of loan options from various lenders, allowing clients to compare rates, terms, and features to find the best fit for their investment strategy.

Expert Advice:

Our team of mortgage professionals provides personalised guidance and support throughout the loan application process, ensuring a smooth and seamless experience from start to finish.

Ongoing Support:

Beyond securing financing, we remain committed to our clients' success, offering ongoing support and resources to help them maximise the return on their investment property portfolio.

Strategies for Success

To maximise returns and mitigate risks when investing in property, consider the following strategies:

Diversification:

Diversifying your investment portfolio across different property types, locations, and asset classes can help spread risk and enhance long-term returns. Consider investing in residential, commercial, and mixed-use properties to diversify your portfolio.

Research and Due Diligence:

Conduct thorough research and due diligence before investing in a property. Evaluate factors such as location, property condition, rental demand, and potential for capital appreciation to make informed investment decisions.

Financial Planning:

Develop a comprehensive financial plan that accounts for your investment goals, risk tolerance, cash flow projections, and exit strategies. Consider working with financial advisers and mortgage brokers to optimise your investment strategy and financing options.

Regular Review and Monitoring:

Regularly review and monitor your investment portfolio to assess performance, identify opportunities for optimisation, and make necessary adjustments to your strategy. Stay informed about market trends, regulatory changes, and economic developments that may impact your investments.

Conclusion:

Investment property loans represent a gateway to financial freedom, and with NZ Mortgages by your side, the journey becomes simpler and more rewarding. By understanding the nuances of investment lending and leveraging the expertise of our team, you can confidently pursue your investment goals and build a brighter financial future. Contact NZ Mortgages today and unlock the potential of property investment.

10 notes

·

View notes

Text

California is facing a record $68 billion budget deficit.

This is largely attributed to a “severe revenue decline,” according to the state's Legislative Analyst's Office (LAO).

While it’s not the largest deficit the state has ever faced as a percentage of overall spending, it’s the largest in terms of real dollars — and could have a big impact on California taxpayers in the coming years.

Here’s what has eaten into the Golden State’s coffers.

Unprecedented drop in revenue

California is dealing with a revenue shortfall partly due to a delay in 2022-2023 tax collection. The IRS postponed 2022 tax payment deadlines for individuals and businesses in 55 of the 58 California counties to provide relief after a series of natural weather disasters, including severe winter storms, flooding, landslides and mudslides.

Tax payments were originally postponed until Oct. 16, 2023, but hours before the deadline they were further postponed until Nov. 16, 2023. In line with the federal action, California also extended its due date for state tax returns to the same date.

These delays meant California had to adopt its 2023-24 budget before collections began, “without a clear picture of the impact of recent economic weakness on state revenues,” according to the LAO.

Total income tax collections were down 25% in 2022-23, according to the LAO — a decline compared to those seen during the Great Recession and dot-com bust.

“Federal delays in tax collection forced California to pass a budget based on projections instead of actual tax receipts," Erin Mellon, communications director for California Gov. Gavin Newsom, told Fox News. "Now that we have a clearer picture of the state’s finances, we must now solve what would have been last year’s problem in this year’s budget.”

The exodus

California has also lost residents and businesses — and therefore, tax revenue — in recent years.

The Golden State’s population declined for the first time in 2021, as it lost around 281,000 residents, according to the Public Policy Institute of California (PPIC). In 2022, the population dropped again by around 211,000 residents — with many moving to other states like Texas, Oregon, Nevada, and Arizona.

Read more: 'It's not taxed at all': Warren Buffett shares the 'best investment' you can make when battling inflation

“Housing costs loom large in this dynamic,” according to the PPIC, which found through a survey that 34% of Californians are considering moving out of the state due to housing costs.

Other factors such as the post-pandemic remote work trend — which has resulted in empty office towers in California’s downtown cores — have also played a role in migration out of the state.

Poor economic conditions

In an effort to tame inflation in the U.S., the Federal Reserve has hiked interest rates 11 times — from 0.25% to 5.5% — since March 2022. These actions have made borrowing more expensive and have reduced the amount of money available for investment.

This has cooled California’s economy in a number of ways. Home sales in the state are down by about 50%, according to the LAO, which it largely attributes to the surge in mortgage rates. The monthly mortgage to buy a typical California home has gone from $3,500 to $5,400 over the course of the Fed’s rate hikes the LAO says.

The Fed’s rate hikes have “hit segments of the economy that have an outsized importance to California,” according to the LAO, including startups and technology companies. Investment in the state’s tech economy has “dropped significantly” due to the financial conditions — evidenced by the number of California companies that went public in 2022 and 2023 being down by over 80% from 2021, the LAO says.

One result of this is that California businesses have had less funding to be able to expand their operations or hire new workers. The LAO pointed out that the number of unemployed workers in the Golden State has risen by nearly 200,000 people since the summer of 2022, lifting the percentage from 3.8% to 4.8%.

Fixing the budget crunch

The LAO suggests that California has various options to address its $68 billion budget deficit — including declaring a budget emergency and then withdrawing around $24 billion in cash reserves.

California also has the option to lower school spending to the constitutional minimum — a move that could save around $16.7 billion over three years. It could also cut back on at least $8 billion of temporary or one-time spending in 2024-25.

However, these are just short-term solutions and may not address the state’s longer term budget issues. In the past, the state has cut back on business tax credits and deductions and increased broad-based taxes to generate more revenue.

Mellon did not reveal any specifics behind the state’s recovery plan in her comments to Fox News. She simply said: “In January, the Governor will introduce a balanced budget proposal that addresses our challenges, protects vital services and public safety and brings increased focus on how the state’s investments are being implemented, while ensuring accountability and judicious use of taxpayer money.”

13 notes

·

View notes

Text

Mortgage Calculator Service in California:

Use the free California Mortgage Calculator to estimate your monthly payment, including taxes, mortgage insurance, principal, and interest.

A mortgage calculator helps in calculating things in a few minutes.

Buying a new home is a time of dreams and opportunity, but navigating the mortgage process can also make it stressful and confusing. Different interest rates and repayment terms can make it difficult to compare mortgage loan offers.

Our mortgage calculator should help you understand everything. This helpful tool makes it easy to find mortgage loans and choose the best deal for you.

How to Use This Calculator:

Our mortgage calculator can help you understand how differences in interest rates and repayment terms affect the size of your monthly payment and the total cost of a home over time. Little information is required to get started. Adding a few more details using the calculator's optional advanced options can give you an even clearer idea of what your monthly mortgage payment might look like for different loans.

- House Price: This is the amount you pay the house seller. If you are in the early stages of home shopping, use the seller's asking price for comparison, but remember that this number is negotiable. If you are shopping in a highly competitive market and expect to be one of several bidders, you may want to bid above the asking price. In slower markets or for properties that have been on the market for a longer period of time, a bid below the asking price could be successful. Work with a real estate professional/ Mortgage Advisor to set your bidding strategy.

- Down Payment: When you enter the house price, the calculator automatically fills in the Down Payment field to reflect 20% of the house price. This is the standard down payment required for most traditional mortgages. Many mortgage lenders, including those who make government-backed loans, will accept lower down payments, usually in exchange for higher interest rates and/or fees - and with the stipulation that you pay for mortgage insurance, which you can factor into the calculator's advanced features.

- Term (in years): Enter the number of years required for the mortgage to be repaid. By default, this calculator assumes a 30-year mortgage, as this is the most common home loan term in America. Other standard mortgage terms include 15 years, 20 years, and 40 years. Adjust this number according to the offer you are evaluating. All things being equal, longer mortgage terms mean lower monthly payments, but also significantly higher interest costs over the life of the loan.

- Interest Rate: Enter the interest rate for the loan you are considering. Be sure to enter the interest rate, not the APR (annual percentage rate). These numbers may be similar, but the APR reflects interest costs plus additional financing costs like fees and mortgage insurance.

#mortgage#term#payments#downpayment#downpay#insurance#usa#united states#canada#advisor#mortgage adviser#financial advisers#calculator#calculations#california#year#loan#house#sale#service

186 notes

·

View notes

Text

Rich People Getting Richer (Part 3 of ?)

To refresh your memory, we're addressing the question of how wealthy people have a lower effective tax rate than moderate income people.

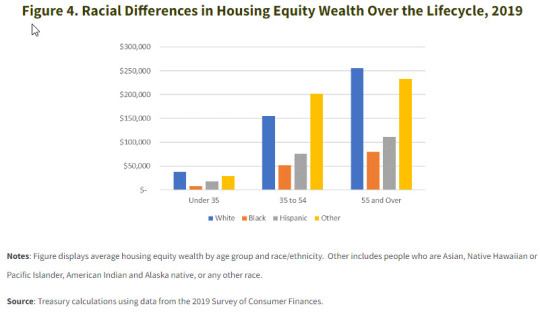

US Government policies supporting home ownership have not only lowered the effective tax rate of those wealthy enough to own a home, they have also contributed to the accumulation of wealth.

Current tax law allows for a couple to deduct the interest on a home mortgage up to $750K (for the first or SECOND home). The current Standard Deduction for a couple is $25,900 (which is greater than many people's home mortgage interest expense and other Itemized Deductions) so most couples will chose the Standard Deduction instead of choosing Itemized Deductions which can include mortgage interest.

For most of my adult life, however, the tax limit on mortgages has been greater ($1M) and the Standard Deduction much lower, so it was advantageous for most homeowners to deduct their mortgage interest. Historically, if you owned a home with a mortgage, your effective tax rate was lower than a comparable couple who rented.

Preferable tax treatment isn't the only way the US encouraged home ownership however. With a few exceptions, loose monetary policy by the Fed has allowed relatively cheap home mortgage interest rates (the current period being one of those exceptions). The US government also established quasi-government agencies Fannie Mae and Ginny Mae, and Freddy Mac to buy mortgages and issue mortgage-backed securities. Collectively, these actions lowered borrowing costs and encouraged home ownership. When you consider the additional benefit of the rise of real estate prices over the last 30 years, the result is a huge accumulation of wealth for those able to purchase a home (mostly white people).

There are good arguments that tax and monetary policies encouraging home ownership are good ideas (stable communities, wealth accumulation for the middle class, economic growth, etc.). Like any other policy however, it favors and rewards some (those who can buy a home) over others. The opportunity costs are those different policies which would have delivered economic benefits to different groups. In other words, the US has pool of economic tools which can incentivize or de-incentivize various activities and has choosen to support home ownership.

Twenty years ago I'd have objected if you said this is a racist policy. After all, the tax policy doesn't say that the home mortgage interest deduction is only available to white people. So how can it be racist?

Here's the question... is a policy racist if the benefits are inequitably distributed to a race, especially if that race is already advantaged? In the case of financially rewarding home ownership, I think you have to say yes. According to the US Treasury:

"In the second quarter of 2022, the homeownership rate for white households was 75 percent compared to 45 percent for Black households, 48 percent for Hispanic households, and 57 percent for non-Hispanic households of any other race."

The seeds of this inequity were sown with "redlining" as described in an NPR article: The redlining maps originated in the aftermath of the Great Depression, when the federal government set out to evaluate the riskiness of mortgages in major metropolitan areas of the country. The maps, created by the federal Home Owners' Loan Corporation, color-coded neighborhoods by credit worthiness. Areas with African-Americans and immigrants were almost always considered the highest risk, and they were marked in red on maps... hence, "redlining."

So follow the logic here... beginning with the redlining after the Great Depression and followed by tax and monetary policies rewarding home ownership, we now see a huge disparity in home ownership wealth. Again from the US Treasury:

I suspect some of you may be questioning the relevance of redlining which occurred ~60 years ago. In fact, studies have confirmed the effects of redlining are still measurable today. Again from the NPR article, the study from the National Community Reinvestment Coalition, the University of Richmond and the University of Wisconsin-Milwaukee analyzed historic redlining maps from 142 urban areas across the U.S. and found "higher rates of poverty, shorter life spans and higher rates of chronic diseases including asthma, diabetes, hypertension, obesity and kidney disease."

I know I've strayed from the original question, but the reality of statistics like these are so troubling. You either have to believe that people of color don't like owning homes and accumulating wealth or the system has disadvantaged them.

I don't think this means that the government shouldn't pursue any policy that inequitably benefits a demographic which is already advantaged, but I do think it means policies should include meaningful, well-funded actions designed to actively grow the participation of the other demographics.

27 notes

·

View notes

Text

Take the housing market. Home sale prices have come off of their 2022 peak, but they're still 47% higher than they were in 2019, according to the S&P CoreLogic Case-Shiller National Home Price Index. Even if you manage to find a deal, getting a loan is going to be costly. Thanks to the Federal Reserve's interest-rate hikes, mortgage rates are much higher than they were just a couple of years ago: somewhere around 7%, compared with just about 2.5% in 2021. Not only do these high rates weigh on prospective buyers, but anyone thinking of selling their home — hello, boomers — is likely to be turned off because their current mortgage rate is probably lower than a new one. With both buyers and sellers feeling the squeeze from higher mortgage rates, and with homebuilders unable to keep up, the inventory of available homes has collapsed. And as much as a lot of people would like to see a housing-market bubble burst, that's probably not in the cards.

The car market is in a similar situation. Vehicles are expensive. Loans are getting tougher to come by, and even if you manage to get credit, elevated interest rates are making financing costly. Car insurance is much more than it used to be, too. The Bureau of Labor Statistics' most recent consumer price index indicates the cost of car insurance is up by more than 20% over the past year.

When it comes to work, the vibe is static, too. Yes, the labor market is strong, but it's not a great time to go looking for a new job. Companies aren't laying people off en masse, but they're also not bringing employees on board quickly. Hiring has slowed significantly from where it was in 2021 and 2022. And, it's much lower than one would expect with the current unemployment rate.

"Employers are hiring as if there's a relatively weak labor market, not a strong one," said Matt Darling, a senior employment-policy analyst at the Niskanen Center, a center-right think tank.

The downshift in hiring has also tipped the balance of power back toward employers. While wages are still on the upswing, switching jobs may not come with as much of a pay bump as it did during the Great Resignation of 2021 and 2022. That may be fine for those who are happy in their jobs, which many people are, but it's not so great for those who are feeling a little antsy or underappreciated. And for those Americans who find themselves out of work and looking for a new gig, it's going to take a minute. Darling told me that for the unemployed, it takes about twice as long to get a job as it did before 2008. A job search that used to take 10 weeks at a similar unemployment rate now takes 20.

"That's obviously a huge source of dissatisfaction, because 20 weeks is a long time," Darling said. "What's that, five months to be looking for a job?"

What this all translates to is a scenario where some Americans feel trapped. They can put food on the table and fill up their gas tanks, albeit at a price they'd rather not be paying. But it's hard and expensive to move up the ladder in many meaningful ways. In a consumerist society that encourages people to want more and a culture that prizes itself on economic mobility, this level of stillness is uncomfortable. While it's still possible to get a better job or a new house, those things feel like they're off in some nebulous future, out of your control.

2 notes

·

View notes

Text

Any property loan for an income-producing asset that is intended to be used for commercial purposes is referred to as a commercial mortgage. Hotel, office, and shopping center purchases can be made with the help of commercial financing.

#free mortgage advisor#mortgage best deals uk#Compare Mortgage interest Rates#compare mortgage deals#health insurance quotes online#get free life insurance quote

0 notes

Text

Unlocking Your Dream Home: How a Melbourne Home Loan Broker Can Help

Introduction:

Finding and financing your dream home can be a daunting task, especially in a dynamic real estate market like Melbourne. Aspiring homeowners often face numerous challenges, from navigating complex mortgage options to securing competitive interest rates. That's where a knowledgeable and experienced home loan broker can make all the difference. At Soniezgroup, we specialize in helping Melbourne residents turn their homeownership dreams into reality. In this blog, we shall explore the invaluable role of a home loan broker and how our services can benefit individuals in suburbs like Tarneit, Hoppers Crossing, and Truganina.

Understanding the Role of a Home Loan Broker:

A home loan broker serves as an intermediary between borrowers and lenders, helping clients find the most suitable mortgage options tailored to their financial circumstances and homeownership goals. Unlike traditional banks or lenders, home loan brokers have access to a wide network of financial institutions, allowing them to offer a diverse range of loan products and competitive rates.

Benefits of Working with a Home Loan Broker:

Expert Guidance and Advice:

Navigating the intricacies of the mortgage market can be overwhelming, especially for first-time homebuyers. A home loan broker offers expert guidance and advice every step of the way, from assessing your borrowing capacity to selecting the right loan product for your needs. Whether you are buying your first home in Tarneit or upgrading to a larger property in Hoppers Crossing, our team at Soniezgroup provides personalized support to help you make informed decisions.

Access to Multiple Lenders and Loan Products:

One of the key advantages of working with a home loan broker is access to a diverse range of lenders and loan products. Instead of being limited to the offerings of a single bank, borrowers can compare rates and terms from multiple financial institutions, ensuring they secure the most competitive deal available. Whether you are interested in fixed-rate mortgages, variable-rate loans, or specialized financing options, our team can help you explore your options and find the best fit for your needs.

Streamlined Application Process:

Applying for a mortgage can be a time-consuming and paperwork-intensive process. A home loan broker simplifies the application process by handling the paperwork on your behalf and liaising with lenders to expedite approvals. From gathering documentation to submitting loan applications, our team at Soniezgroup ensures a smooth and efficient process from start to finish, saving you time and hassle along the way.

Negotiation of Competitive Interest Rates:

Interest rates play a significant role in determining the overall cost of your mortgage. A home loan broker leverages their industry expertise and negotiating skills to secure competitive interest rates on behalf of their clients. Whether you are purchasing a property in Truganina or refinancing an existing mortgage, our team works tirelessly to ensure you receive the most favorable terms possible, saving you money over the life of your loan.

Continued Support and Assistance:

The relationship with a home loan broker does not end at settlement. At Soniezgroup, we provide ongoing support and assistance to our clients throughout the life of their loan. Whether you have questions about your mortgage, need advice on refinancing options, or require assistance with loan modifications, our dedicated team is always here to help. We strive to build long-term relationships with our clients, serving as trusted advisors on all their homeownership journeys.

Conclusion:

Navigating the complexities of the mortgage market can be challenging, but with the guidance of a knowledgeable home loan broker, achieving your homeownership dreams is within reach. From Tarneit to Hoppers Crossing to Truganina, Soniezgroup is committed to helping Melbourne residents unlock their dream homes with personalized service, expert advice, and access to competitive loan options. If you are ready to take the next step towards homeownership, contact us today to schedule a consultation. Let us help you find the perfect mortgage solution tailored to your unique needs and goals.

#Home loan broker in Tarneit#Home loan broker in Hoppers Crossing#Home loan broker in Truganina#Tax accounting in Truganina#Accounting tax in Truganina#Tax consultants in Truganina#Tax return agent in Truganina#Best conveyancer in Tarneit#Conveyancing services in Tarneit#Best conveyancer in Truganina#Conveyancing services in Truganina#Mortgage loan broker in Tarneit#Mortgage finance broker in Hoppers Crossing#Best mortgage broker in Truganina

3 notes

·

View notes

Text

Blue Melon Capital Reviews | 5 Key Factors to Consider When Securing Real Estate Financing

Securing financing for real estate investments is a critical aspect of property ownership and development. Whether you're purchasing your dream home or investing in commercial properties, navigating the complex landscape of real estate financing requires careful consideration of several key factors. Blue Melon Capital Reviews shares some essential elements to keep in mind when seeking financing for your real estate ventures.

1. Creditworthiness and Financial Health

One of the foremost factors lenders consider when assessing real estate financing applications is the borrower's creditworthiness and financial health. Your credit score, debt-to-income ratio, and overall financial stability play pivotal roles in determining the terms of your loan, including interest rates and loan amounts. Before applying for financing, it's crucial to review your credit report, address any discrepancies or outstanding debts, and ensure your financial records reflect a favorable picture. Building a strong credit profile not only enhances your chances of securing financing but also opens doors to more competitive loan options with favorable terms.

2. Property Valuation and Collateral

The value of the property you intend to finance serves as collateral for the loan, influencing the lender's risk assessment and loan-to-value (LTV) ratio. Conducting a thorough property valuation, including appraisal and assessment of market trends, is essential to determine its fair market value accurately. Additionally, lenders may impose specific requirements regarding the type, condition, and location of the property, which can affect financing options. Understanding the collateral requirements and ensuring the property meets these criteria is crucial for securing favorable financing terms and minimizing risks for both parties involved.

3. Loan Terms and Structure

Blue Melon Capital Reviews believes real estate financing encompasses a variety of loan options, each with distinct terms, structures, and repayment schedules. From traditional mortgages to commercial loans, bridge financing, and construction loans, selecting the right loan product tailored to your specific needs is vital. Consider factors such as interest rates, loan duration, down payment requirements, and prepayment penalties when evaluating different financing options. Additionally, understanding the implications of fixed-rate versus adjustable-rate mortgages and the impact of market fluctuations on loan payments is essential for making informed decisions about loan terms and structure.

4. Lender Relationships and Options

Building strong relationships with lenders and exploring diverse financing options can provide valuable insights and opportunities for securing favorable terms. Researching reputable lenders, including banks, credit unions, mortgage brokers, and private lenders, allows you to compare rates, fees, and eligibility criteria to find the best fit for your financing needs. Moreover, cultivating open communication and transparency with lenders throughout the application process can strengthen your negotiating position and increase the likelihood of securing financing on favorable terms. By leveraging diverse lender relationships and exploring alternative financing sources, you can optimize your real estate financing strategy and mitigate potential challenges.

5. Regulatory and Legal Considerations

Navigating the regulatory and legal landscape surrounding real estate financing is paramount to ensure compliance and mitigate risks. Familiarize yourself with applicable laws, regulations, and licensing requirements governing real estate transactions and lending practices in your jurisdiction. Additionally, consult legal professionals specializing in real estate law to review loan agreements, contracts, and disclosure documents thoroughly. Understanding your rights and obligations as a borrower, as well as potential legal implications, empowers you to make informed decisions and safeguard your interests throughout the financing process.

In conclusion, securing real estate financing requires careful consideration of various factors, including creditworthiness, property valuation, loan terms, lender relationships, and regulatory compliance. By prioritizing these key elements and conducting thorough due diligence, borrowers can enhance their chances of securing financing on favorable terms while minimizing risks and maximizing returns on their real estate investments. Remember to seek guidance from financial advisors, real estate professionals, and legal experts to navigate the complexities of real estate financing and make informed decisions aligned with your long-term objectives.

2 notes

·

View notes

Text

Those That Have Will Receive More

In December 2022, the Guardian carried this headline:

“Soaring rents making life ‘unaffordable’ for private UK tenants, research shows." (01/12/22)

A few months later and the BBC ran a news report informing us that rents had increased by over 11.1% compared to the previous year. And in June we read that official government figures showed:

“The median monthly rent in England between October 2021 and September 2022 was £800 – higher than at any other point in history, according to the Office for National Statistics.” (The Big Issue: 19/06/23)

The government response to these massive increases in private rental charges has been to do NOTHING After all, people that rent are far more likely to vote Labour than Tory so there is no gain to be had by offering them rent relief. Indeed, government ministers have gone out of their way to insist there will be no rent price controls.

“Minister confirms government will not consider rent controls in England." (propertyindustryeye: 16/11/22)

Fast forward to yesterday and the Bank of England’s 0.5% lending rate rise and everyone is suddenly concerned about the cost to house owners of future mortgage payments. Homeowners DO tend to vote Tory so Jeremy Hunt has summoned the heads of banks and building societies to a special meeting to see what can be done to help property-owning householders.

I do not for one second underestimate the financial hardship that can be brought about by increases in mortgage repayment loans. What I do object to is a Tory government who does absolutely nothing to help the poorest in society facing an 11% increase in rent rises, but who feign concern for house owners, many of whom are still on fixed rate mortgages, and therefore still protected from immediate increased costs.

Here are some simple facts and figures from the government.

61.5% of the UK population are house owners.

27.1% of the UK population are owner-occupiers without a loan or mortgage.

37.5% of the UK population are owner-occupiers with a loan or mortgage.

34.9 % of the UK population are non-owner-occupants.

In other words the number of households facing massive rent rises is almost the same percentage as those facing higher mortgage repayments.

According to “Money”:

“The cost of renting appears to be significantly greater than mortgage payments throughout the UK. In England, the average monthly mortgage payment is £753 compared to a larger £795 average monthly rent payment.” Money: March2023)

So, renters are already paying a higher proportion of their income on rents than owner-occupiers, yet they are to receive no help.

The population of the UK, is estimated to be just below 69 million. If 34.95% of those are non-owner occupiers, that is a total of 24,080,999 who live in rented accommodation.

As stated earlier many of those who are owner-occupiers and paying monthly mortgage repayments are on fixed rate deals and therefore will experience no immediate rises in their monthly repayments. According to government figures:

“1.4 million households facing bigger mortgage repayments in 2023” (Mortgage Strategy: 09/01/23)

If we assume each household has five persons (an over-estimation) then the total number of people living in a property facing a mortgage increase this year is 7 million. The number of people living in rented accommodation facing rent increases is, as already demonstrated, 24 million.

These 24 million are amongst the poorest in society and moral justice would demand they receive as much (if not more) help from government as owner-occupiers.

Today, (23/06/23) after meeting with the Chancellor of the Exchequer, Jeremy Hunt:

“Mortgage lenders and the UK chancellor, Jeremy Hunt, have agreed that people should be given a 12-month grace period before repossession proceedings start, following yesterday’s shock interest rate hike to 5%” (Guardian: 23/06/23).

Meanwhile renters who fall behind on payments have been facing an entirely different reality:

“Rental evictions in England and Wales surge by 98% in a year… a survey by homelessness charity Crisis indicated that nearly 1 million low-income households across Britain feared eviction in the coming months.” (Guardian: 09/02/23)

The figures, and the government’s callous attitude towards renters, speak for themselves.

#uk politics#renters#owner occupiers#mortgages#Jeremy Hunt. rishi sunak#unfair#evictions#mortgage relief

8 notes

·

View notes

Video

youtube

Housing market 2024 #newhomesource #realestateagent #realtor #realestate...

#HousingMarket2023Finale The U.S. real estate market wrapped up 2023 on a high note, signaling a promising growth trajectory for 2024! #InventoryGrowth - Good news for homebuyers this spring! The housing inventory is gradually increasing compared to last year, offering more choices for prospective buyers. #SalesOnTheRise - The real estate market is buzzing with activity, as more homes enter contracts weekly, highlighting a synchronized climb in both supply and demand. #StableHomePrices - Home prices are gently rising, a stark contrast to the frenzied spikes seen during the pandemic. This stability suggests a comfortable match between current prices, mortgage rates, and buyer interest. If economic headwinds like rising unemployment emerge, the pending sales data will be an early indicator of their impact on the housing market. #PriceReductionTrends - Currently, 34.8% of homes on the market have reduced prices, aligning with the normal range. This trend is expected to evolve as new inventory enters the market in the coming months. Read more at the link in comments or call us 763-746-3997!

2 notes

·

View notes

Text

WASHINGTON, D.C. – Today, the Consumer Financial Protection Bureau (CFPB) issued a new report that suggests consumers tend to pay more for products that have more complex pricing structures. The report is based on experiments with multiple rounds of buyers and sellers interacting in simple markets, and found that participants tended to pay more when prices were broken into sub-parts and were harder to understand. The research has implications for understanding how junk fees impede fair and competitive pricing in markets like auto loans or mortgages, where consumers have to evaluate extended warranties, add-ons, closing costs, and a wide variety of other fees instead of an all-inclusive price.

CFPB researchers had study participants act as buyers and sellers in a series of transactions. In some cases the objects for sale had a single all-in price, while in other cases the prices were split into 8 or 16 sub-prices. In the scenarios with more complex pricing, buyers tended to fare worse. The average selling prices rose, buyers had more difficulty comparing prices across sellers, and the overall amount paid rose. These findings contribute to a growing consensus of research and real-world observations showing that junk fees increase overall prices beyond what a fair and competitive market would allow.

While not expected to exactly mirror real-world transactions, the CFPB found in these experiments that more complex pricing generally led to more detrimental outcomes for consumers:

Higher total prices: Sellers' total asking prices were 60 percent higher in markets with 16 sub-prices than in those with one price.

Comparing prices was more difficult: Buyers were 15 times more likely to select a higher-priced option in markets with 16 sub-prices than in those with one price.

Consumers paid more overall: Transaction prices were 70 percent higher in markets with 16 sub-prices than in those with one price, on average.

The CFPB has previously highlighted how the use of complex terms and pricing can pose challenges for consumers. In many instances, consumers face complex pricing when shopping for financial products and services including:

Credit cards: Credit card pricing often includes a mix of interest rates, late fees, balance transfer fees, annual fees, cash advance fees, and foreign transaction fees. Many credit cards offer introductory 0% APR periods on purchases or balance transfers, but these promotional rates are often followed by much higher standard APRs that can vary based on the cardholder's credit score. Market data suggest that many consumers are selecting credit cards based on rewards, which can similarly be quite complicated, with varying earning and redemption rules.

Checking and savings accounts: Checking and savings account pricing can include a variety of fees, such as monthly maintenance fees, minimum balance fees, overdraft fees, and wire transfer fees. Some banks also offer complex tiered interest rates based on account balances, making it difficult for consumers to compare yields across different institutions. Some checking accounts advertised as “free” may in fact require minimum balances, recurring direct deposits, or other qualifications that could obscure the true cost of the account.

Mortgages: Mortgage pricing can be extremely complex, with a wide range of interest rates, fees, and terms that vary based on factors such as loan type, credit score, or down payment. For example, adjustable-rate mortgages (ARMs) can have pricing structures that include initial fixed-rate periods, adjustment intervals, caps on interest rate changes, and margin rates. And consumers often pay a large number of separate closing costs to obtain a mortgage.

Auto loans: Auto loan pricing can be complex, with interest rates that vary based on factors such as credit score, loan term, down payment, and vehicle type. Some lenders also offer promotional rates or cash-back incentives that can make it difficult for consumers to compare the true cost of financing across different offers. Add-on products, such as extended warranties, gap insurance, and credit life insurance, can significantly increase the overall cost of the loan.

Read the report, Price Complexity in Laboratory Markets.

Consumers can submit complaints about financial products or services by visiting the CFPB’s website or by calling (855) 411-CFPB (2372).

Employees of companies who believe their company has violated federal consumer financial laws are encouraged to send information about what they know to [email protected].

1 note

·

View note

Last Seen Blogs

the-gummy-bear-family-blog

The Gummy Bear Family

zavarof

zavarof

thanhcongcomputer

Thành Công Computer

mitochondr

Untitled

ndnbebeysd

제목 없음