#bank of america cryptocurrency

Text

#cryptocapitalism#cryptocurrencies#currencies#currency#virtual currencies#virtual currency vs cryptocurrency#bank of america cryptocurrency#crypto news#crypto

0 notes

Text

#Stocks drop on #bank fears

View On WordPress

#America#bank run#banking#banks#Credit Suisse#crypto#cryptocurrency#europe#meme#memes#money#news#stock market#stocks#tech#technology#united states

46 notes

·

View notes

Text

Spot Bitcoin ETFs Introduced to Portfolios by Bank of America and Wells Fargo

Two financial advisors on Wall Street are set to back direct Bitcoin Exchange-Traded Funds (ETFs) almost two months following their introduction on prominent American stock exchanges. Clients holding brokerage accounts at Bank of America’s Merrill Lynch and Wells Fargo will be permitted to engage in transactions involving direct Bitcoin (BTC) ETFs, following a surge in demand amounting to billions, eight weeks post their market debut. According to Bloomberg, which obtained information from anonymous insiders familiar with the situation, this move marks a significant shift. Issuers of direct Bitcoin ETFs comprise some of the United States' largest asset management firms, including BlackRock and Fidelity. Nonetheless, initially, traditional banks and brokerage houses hesitated to make these products available to their clientele. N

Read more on Spot Bitcoin ETFs Introduced to Portfolios by Bank of America and Wells Fargo

#Bank of America#bitcoin#blockchain#cryptocurrency#cryptomarket#cryptonewstoday#news#regulations#Spot Bitcoin

0 notes

Text

0 notes

Text

Family offices are a $ 6 trillion behemoth in investments and deals

Family offices are a $ 6 trillion behemoth in investments and deals

The post-pandemic wealth boom triggered an explosion in family offices, creating a new gold rush for Wall Street firms, private equity funds and investment advisors to manage the fortunes of the world’s richest families. Family offices now manage more than $ 6 trillion in wealth, according to some estimates, surpassing the estimated $ 4 trillion managed by hedge funds. They quickly became a…

View On WordPress

#Bank of America Corp#behemoth#business news#Citigroup Inc#Credit Suisse Group AG#Cryptocurrency#deals#Deutsche Bank AG#Family#Financial sector regulation#Goldman Sachs Group Inc#Investment strategy#investments#JPMorgan Chase & Co#Leon Cooperman#Mergers and acquisitions#Morgan Stanley#offices#Real estate#SEC#Singapore#trillion#UBS AG Group#Wealth

1 note

·

View note

Text

Intuit: “Our fraud fights racism”

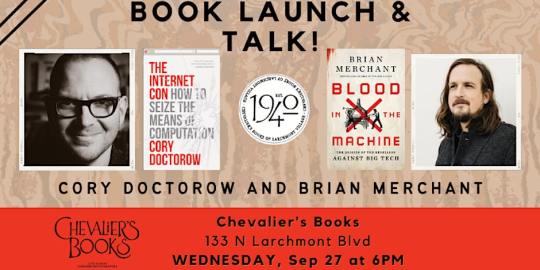

Tonight (September 27), I'll be at Chevalier's Books in Los Angeles with Brian Merchant for a joint launch for my new book The Internet Con and his new book, Blood in the Machine. On October 2, I'll be in Boise to host an event with VE Schwab.

Today's key concept is "predatory inclusion": "a process wherein lenders and financial actors offer needed services to Black households but on exploitative terms that limit or eliminate their long-term benefits":

https://journals.sagepub.com/doi/10.1177/2329496516686620

Perhaps you recall predatory inclusion from the Great Financial Crisis, when predatory subprime mortgages with deceptive teaser rates were foisted on Black homeowners (who were eligible for better mortgages), resulting in a wave of Black home theft in the foreclosure crisis:

https://prospect.org/justice/staggering-loss-black-wealth-due-subprime-scandal-continues-unabated/

Before these loans blew up, they were styled as a means of creating Black intergenerational wealth through housing speculation. They turned out to be a way to suck up Black families' savings before rendering them homeless and forcing them into houses owned by the Wall Street slumlords who bought all the housing stock the Great Financial Crisis put on the market:

https://pluralistic.net/2022/02/08/wall-street-landlords/#the-new-slumlords

That was just an update on an old con: the "home sale contract," invented by loan-sharks who capitalized on redlining to rip off Black families. Back when banks and the US government colluded to deny mortgages to Black households, sleazy lenders created the "contract loan," which worked like a mortgage, but if you were late on a single payment, the lender could seize and sell your home and not pay you a dime – even if the house was 99% paid for:

https://socialequity.duke.edu/wp-content/uploads/2019/10/Plunder-of-Black-Wealth-in-Chicago.pdf

Usurers and con-artists love to style themselves as anti-racists, seeking to "close the racial wealth gap." The payday lending industry – whose triple-digit interest rates trap poor people in revolving debt that they can never pay off – styles itself as a force for racial justice:

https://pluralistic.net/2022/01/29/planned-obsolescence/#academic-fraud

Payday lenders prey on poor people, and in America, "poor" is often a euphemism for "Black." Payday lenders disproportionately harm Black families:

https://ung.edu/student-money-management-center/money-minute/racial-wealth-gap-payday-loans.php

Payday lenders are just unlicensed banks, who deploy a layer of bullshit to claim that they don't have to play by the rules that bind the rest of the finance sector. This scam is so juicy that it spawned the fintech industry, in which a bunch of unregulated banks sprung up to claim that they were too "innovative" to be regulated:

https://pluralistic.net/2023/05/01/usury/#tech-exceptionalism

When you hear "Fintech," think "unlicensed bank." Fintech turned predatory inclusion into a booming business, recruiting Black spokespeople to claim that being the sucker at the table in the cryptocurrency casino was actually a form of racial justice:

https://www.nytimes.com/2021/07/07/business/media/cryptocurrency-seeks-the-spotlight-with-spike-lees-help.html

But not all predatory inclusion is financial. Take Facebook Basics, Meta's "poor internet for poor people" program. Facebook partnered with telcos in the Global South to rig their internet access. These "zero rating" programs charged subscribers by the byte to reach any service except Facebook and its partners. Facebook claimed that this would "bridge the digital divide," by corralling "the next billion internet users" into using its services.

The fact that this would make "Facebook" synonymous with "the internet" was just an accidental, regrettable side-effect. Naturally, this was bullshit from top to bottom, and the countries where zero-rating was permitted ended up having more expensive wireless broadband than the countries that banned it:

https://www.eff.org/deeplinks/2019/02/countries-zero-rating-have-more-expensive-wireless-broadband-countries-without-it

The predatory inclusion gambit is insultingly transparent, but that doesn't stop desperate scammers from trying it. The latest chancer is Intuit, who claim that the end of its decade-long, wildly profitable "free tax prep" scam is bad for Black people:

https://www.propublica.org/article/turbotax-intuit-black-taxpayers-irs-free-file-marketing

Some background. In nearly every rich country on Earth, the tax authorities send every taxpayer a pre-filled tax return, based on the information submitted by employers, banks, financial planners, etc. If that looks good to you, you just sign it and send it back. Otherwise, you can amend it, or just toss it in the trash and pay a tax-prep specialist to produce your own return.

But in America, taxpayers spend billions every year to send forms to the IRS that tell it things it already knows. To make this ripoff seem fair, the hyper-concentrated tax-prep industry, led by the Intuit, creators of Turbotax, pretended to create a program to provide free tax-prep to working people.

This program was called Free File, and it was a scam. The tax-prep cartel each took a different segment of Americans who were eligible for Freefile and then created an online house of mirrors that would trick those people into spending hours working on their tax-returns until they were hit with an error message falsely claiming they were ineligible for the free service and demanding hundreds of dollars to file their returns.

Intuit were world champions at this scam. They blocked their Freefile offering from search-engine crawlers and then bought ads that showed up when searchers typed "freefile" into the query box that led them to deceptively named programs that had "free" in their names but cost a fortune to use – more than you'd pay for a local CPA to file on your behalf.

The Attorneys General of nearly every US state and territory eventually sued Intuit over this, settling for $141m:

https://www.agturbotaxsettlement.com/Home/portalid/0

The FTC is still suing them over it:

https://www.ftc.gov/legal-library/browse/cases-proceedings/192-3119-intuit-inc-matter-turbotax

We have to rely on state AGs and the FTC to bring Intuit to justice because every Intuit user clicks through an agreement in which we permanently surrender our right to sue the company, no matter how many laws it breaks. For corporate criminals, binding arbitration waivers are the gift that keeps on giving:

https://pluralistic.net/2022/02/24/uber-for-arbitration/#nibbled-to-death-by-ducks

Even as the scam was running out, Intuit spent millions lobby-blitzing Congress, desperate for action that would let it continue to privately tax the nation for filling in forms that – once again – told the IRS things it already knew. They really love the idea of paying taxes on paying your taxes:

https://pluralistic.net/2023/02/20/turbotaxed/#counter-intuit

But they failed. The IRS has taken Freefile in-house, will send you a pre-completed tax return if you want it. This should be the end of the line for Intuit and other tax-prep profiteers:

https://pluralistic.net/2023/05/17/free-as-in-freefile/#tell-me-something-i-dont-know

Now we're at the end of the line for the scam, Intuit is playing the predatory inclusion card. They're conning Black newspapers like the Chicago Defender into running headlines like "IRS Free Tax Service Could Further Harm Blacks,"

https://defendernetwork.com/news/opinion/irs-free-tax-service-could-further-harm-blacks/

The only named source in that article? Intuit spokesperson Derrick Plummer. The article went out on the country's Black newswire Trice Edney, whose editor-in-chief did not respond to Propublica's Paul Kiel's questions.

Then Black Enterprise got in on the game, publishing "Critics Claim The IRS Free Tax Prep Service Could Hurt Black Americans." Once again, the only named source for the article was Plummer, who was "quoted at length." Black Enterprise declined to tell Kiel where that article came from:

https://www.blackenterprise.com/critics-claim-the-irs-free-tax-prep-service-could-hurt-black-americans/

For Intuit, placing op-eds is a tried-and-true tactic for laundering its ripoffs into respectability. Leaked internal Intuit memos detail the company's strategy of "pushing back through op-eds" to neutralize critics:

https://www.documentcloud.org/documents/6483061-Intuit-TurboTax-2014-15-Encroachment-Strategy.html

Intuit spox Derrick Plummer did respond to Kiel's queries, denying that Intuit was paying for these op-eds, saying "with an idea as bad as the Direct File scheme we don’t have to pay anyone to talk about how terrible it is."

Meanwhile, ex-NAACP director (and No Labels co-chair) Benjamin Chavis has used his position atop the National Newspaper Publishers Association to publish op-eds against the IRS Direct File program, citing the Progressive Policy Institute, a pro-business thinktank that Intuit's internal documents describe as part of its "coalition":

https://www.documentcloud.org/documents/6483061-Intuit-TurboTax-2014-15-Encroachment-Strategy.html

Chavis's Chicago Tribune editorial claimed that Direct File could cause Black filers to miss out on tax-credits they are entitled to. This is a particularly ironic claim given Intuit's prominent role in sabotaging the Child Tax Credit, a program that lifted more Americans out of poverty than any other in history:

https://pluralistic.net/2021/06/29/three-times-is-enemy-action/#ctc

It's also an argument that can be found in Intuit's own anti-Direct File blog posts:

https://www.intuit.com/blog/innovative-thinking/taxpayer-empowerment/intuit-reinforces-its-commitment-to-fighting-for-taxpayers-rights/

The claim is that because the IRS disproportionately audits Black filers (this is true), they will screw them over in other ways. But Evelyn Smith, co-author of the study that documented the bias in auditing says this is bullshit:

https://siepr.stanford.edu/publications/working-paper/measuring-and-mitigating-racial-disparities-tax-audits

That's because these audits of Black households are triggered by the IRS's focus on Earned Income Tax Credits, a needlessly complicated program available to low-income (and hence disproportionately Black) workers. The paperwork burden that the IRS heaps on EITC recipients means that their returns contain errors that trigger audits.

As Smith told Propublica, "With free, assisted filing, we might expect EITC claimants to make fewer mistakes and face less intense audit scrutiny, which could help reduce disparities in audit rates between Black and non-Black taxpayers."

Meanwhile, the predatory inclusion talking points continue to proliferate. Nevada accountants and the state's former controller somehow coincidentally managed to publish op-eds with nearly identical wording. Phillip Austin, vice-chair of Arizon's East Valley Hispanic Chamber of Commerce, claims that free IRS tax prep "would disproportionately hurt the Hispanic community." Austin declined to tell Propublica how he came to that conclusion.

Right-wing think-tanks are pumping out a torrent of anti-Direct File disinfo. This surely has nothing to do with the fact that, for example, Center Forward has HR Block's chief lobbyist on its board:

https://thehill.com/opinion/finance/4125481-direct-e-file-wont-make-filing-taxes-any-easier-but-it-could-make-things-worse/

The whole thing reeks of bullshit and desperation. That doesn't mean that it won't succeed in killing Direct File. If there's one thing America loves, it's letting businesses charge us a tax just for dealing with our own government, from paying our taxes to camping in our national parks:

https://pluralistic.net/2022/11/30/military-industrial-park-service/#booz-allen

Interestingly, there's a MAGA version of predatory inclusion, in which corporations convince low-information right-wingers that efforts to protect them from ripoffs are "woke." These campaigns are, incredibly, even stupider than the predatory inclusion tale.

For example, there's a well-coordianted campaign to block the junk fees that the credit card cartel extracts from merchants, who then pass those charges onto us. This campaign claims that killing junk fees is woke:

https://pluralistic.net/2023/08/04/owning-the-libs/#swiper-no-swiping

How does that work? Here's the logic: Target sells Pride merch. That makes them woke. Target processes a lot of credit-card transactions, so anything that reduces card-processing fees will help Target. Therefore, paying junk fees is a way to own the libs.

No, seriously.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/09/27/predatory-inclusion/#equal-opportunity-scammers

299 notes

·

View notes

Note

I love el salvador because its proof that you can literally just disregard left wing ideology completely, do the exact opposite of what (((they))) say we can't/arent allowed to do, and the end result is objective improvement lol based president bukakke is /ourguy/

lol

>>Despite Bukele presenting his administration as “populist” he is anything but a political outsider or a champion of “the people.” After getting kicked out of the then-ruling Farabundo Martí National Liberation Front (FMLN) for allegedly assaulting a female party official, Bukele, a former advertising executive, joined the Grand Alliance for National Unity (GANA) whose founding members came from the aforementioned Nationalist Republican Alliance (ARENA). Furthermore, Bukele’s rise to power took place during an election in which nearly 50% of eligible Salvadoran voters abstained. It’s even possible that Bukele was appointed in response to the FMLN government’s friendlier relationship with China. For example, in exchange for breaking ties with Taiwan and recognizing Beijing as the official capitol of China, FLMN received $150 million and a donation of 3,000 tons of rice from the Chinese Communist Party. Likewise, during the Trump administration’s 2019 attempt to oust Venezuelan president Nicolas Maduro on behalf of the neoliberal reactionary Juan Guaido, the FMLN took the side of the Chavistas.

In America, Bukele is best known for establishing Bitcoin as Salvadoran legal tender alongside the US dollar. Cryptobros like to portray this as an attempt by a “based” technocrat unpersuaded by “ideology” to get his nation off of fiat currency and away from the control of central banks. This narrative is a total inversion of the truth; In 2020 Bukele sent 40 soldiers into the Legislative Assembly building and forced opposition politicians at gunpoint to approve a loan request of $109 million from the American government for his “Territorial Control Plan.” This plan, using COVID-19 as a pretext, deployed thousands of military personnel to work alongside local police in establishing martial law throughout El Salvador. Bukele’s government insists this led not only to a successful quarantine but a significant reduction in homicides by organized crime. However, the Territorial Control Plan relies on alliances with Salvador’s gangs, as a report by El Faro exposed. “The pandemic was a blessing for Bukele,” Carlos López Bernal, a professor of history at the University of El Salvador, told The Guardian. “He presented an apocalyptic scenario to which the only solution, supposedly, was to give the president everything he asked for. More money and more power.”

In 2021, Bukele’s party “won” a supermajority in El Salvador’s congress, supposedly with 65% of the vote. He then fired five Salvadoran Supreme Court Justices and the attorney general before the Legislative Assembly voted to accept Bitcoin as legal tender. This decision was influenced by Bukele’s close relationship to Strike CEO Jack Mallers, the descendant of Chicago finance royalty and a member of Forbes 30 under 30. According to Slate: “Bukele’s government rolled out a digital crypto wallet in app form, called Chivo (Salvadoran slang for cool), which came preloaded with $30 of Bitcoin to encourage adoption. Many who downloaded it found it confusing and buggy, or that their $30 had already been stolen by identity thieves. A study by economists at the University of Chicago, Penn State and Yale found that of those who managed to access it, most cashed out their $30 and didn’t use Chivo again.”

Towards the start of May, cryptocurrency experienced its worst crash yet. This ongoing crash has already wiped out $400 billion in market capitalization and bankrupted innumerable investors. As Slate notes, “El Salvador is on the verge of defaulting on its debts, which amount to close to 100 percent of its gross domestic product. This is exacerbated by the loss of value of the country’s Bitcoin holdings, which Bukele bragged he would trade with public funds on his phone while in the bathroom. As of now, he has personally cost the Treasury about $40 million—an amount equal to its next foreign debt payment, due to bondholders in June.”

Just before the epic crypto crash, Bukele unveiled plans for a city, “funded by the sale of a Bitcoin bond and powered by geothermal energy from the nearby Conchagua volcano.” Now, the country’s bonds are trading at 40% of their original value. But like any good con artist, cult leader, or multi-level marketing guru, Bukele has doubled down on his Bitcoin “gamble.” In the midst of the crypto crash, El Salvador hosted a “financial inclusion conference” attended by “44 central bankers from developing countries around the world.” This conference was organized by the Alliance for Financial Inclusion, formed in 2008 by central bankers in Mexico, Kenya, the Philippines, Indonesia and Thailand in “close collaboration” with the Bill and Melinda Gates Foundation. In 2013, Bill Gates spoke at a meeting hosted by the United Nations General Assembly to tout the merits of “digital financial inclusion” via digital payment systems. The invite reads:

“Today 2.5 billion adults are excluded from the formal financial services sector. Yet governments, the development community and the private sector make billions of dollars in cash payments to people in emerging economies, many of them poor and financially excluded. Shifting these salaries, pensions, social welfare stipends and emergency relief payments from cash to electronic has the potential to improve the livelihoods of low-income people by advancing financial inclusion and helping people save.

During the upcoming United Nations General Assembly, UNDP, UNCDF and the Better Than Cash Alliance are hosting an event on how partnerships between governments, private sector and development organizations are helping to promote inclusive growth. It will focus on how digital payments can catalyze financial inclusion, and as a result, can be a driver of inclusive growth and development.”

In January 2021 the Bank of International Settlements issued a report stating, “Most central banks are exploring central bank digital currencies (CBDCs), and their work continues apace amid the Covid-19 pandemic. As a whole, central banks are moving into more advanced stages of CBDC engagement, progressing from conceptual research to practical experimentation.” Since 2017, “the share of central banks actively engaging in some form of CBDC work grew by about one third and now stands at 86%.” The BIS report found that 56 central banks are now researching or developing some form of digital currency.

During the early stages of the pandemic in 2020 programmers well versed in COBOL, a 40 year old programming language, were in high demand. This demand mainly came from state governments, who still use COBOL to dispense unemployment benefits. “Literally, we have systems that are 40-plus-years-old,” New Jersey governor Chris Murphy told CNBC. “There’ll be lots of postmortems. and one of them on our list will be, how did we get here where we literally needed COBOL programmers?” Murphy’s concerns were echoed by Kansas governor Laura Kelly: “So many of our Departments of Labor across the country are still on the COBOL system; you know very, very old technology.” Connecticut, California, New York, and Pennsylvania “still rely on decades-old mainframe systems based on the COBOL language as well.”

If all of this still sounds banal or benign to you, consider the following:

PRISM, the massive NSA surveillance machine “exposed” by Islamaphobic Ayn Rand fanboy and descendant of numerous lifelong feds Edward Snowden, is the direct descendant of PROMIS, a tracking software developed by a “former” NSA fed working in the private sector through his firm Inslaw. Inslaw originally developed PROMIS to help the Department of Justice and local law enforcement agencies across America “update” their prehistoric filing systems in the mid-1980s. PROMIS was later stolen by Mossad spies and infamously distributed by Robert Maxwell, father of Ghislaine Maxwell, before making its way back to its homeland. In the meantime, the same NSA that was building PRISM and had produced PROMIS was working on the hash algorithm that made Bitcoin possible.

------

Covid Imperialism, Crypto Colonialism, and the Real “Great Reset” – Beyond_Lies_The_Wub (wordpress.com)

12 notes

·

View notes

Text

FTX's very bad november

here are some bullet points of the key things that happened to stupid 'it turns out it was never actually a business' 40 billion dollar cryptocurrency exchange FTX this month. very funny please read more!

FTX is the 'smart, legal, pro-regulation' bitcoin exchange (a bank) beloved by athletes and US Senators alike. They are one of the five largest businesses in the crypto space, and are valued at up to $32,000,000,0000 (32B USD).

1b. FTX mints its own token, 'FT Token / FTT', which has a use-case for their advanced trading services as well as serving as a speculative asset that represents consumer trust.

2. FTX establishes a sister firm, "Alameda Research", which acted as its own market actor and research publisher. Alameda Research also have massive resources on their balance sheet.

3. When the Terra / Luna stablecoin disastrously lost its peg to the dollar earlier this year, crypto lost $60B of valuation. Everything fell, but unlike some stuff, FTT recovered.

3b. during this crisis, Alameda stepped in as a 'lender of last resort'; bailing out the liquidity-crisis-shocked crypto businesses by selling them emergency loans.

4. On November 02 (two weeks ago!) Coindesk published an exposé showing that a lot of Alameda Research's balance sheet was, basically, IOU's from FTX - the lender of last resort was a shell game.

5. at this point (i'm hazy on details!) the three FTX founders - "the Crypto King" "SBF"; Gary; and Nishad - start fighting a lot on twitter about something offline, in particular with their competitors Binance, the #1 company in the crypto space.

6. Binance sells all the FTT in its vaults. Billions of dollars' worth?

7. The market value of an FTT drops from $24 USD to $3. (an 87.5% drop in value)

8. 36 hours later, seeing FTX about to declare bankruptcy, Binance offers to buy FTX in a bailout. Binance lawyers ask to see FTX's most secret internal accounting documents.

8b. FTX provides something, which Binance aren't happy with, and Binance backs out of their offer to buy FTX.

9. a "hacker" steals between $300M-$500M USD worth of various coins and tokens from not only FTX's 'hot wallet' (actual liquid funds) but ALSO from its 'cold wallets' (which an outside hacker has no access to).

9b. in transferring these funds out of FTX and into a wallet for Tether (a stablecoin), the "hacker" doesn't have enough "TRX" to pay the gas to actually move the money. so they panic and uses TRX from their own wallet.

10. That wallet was on the Kraken ecosystem, and TRX is for the Tron Network, and both Tron and Kraken have KYC ('know your customer') ID requirements to use their systems, linking the wallet used to facilitate the theft to a driver's license and banking and contact information etc.

10b. the head of security for Kraken posts on twitter "We know the identity of the user."

11. the Bahamaian police (they spent company money on a big poly mansion on the Bahamas and so this all happens there) detain the three FTX founders

12. FTX goes from being worth $30-40 billion USD to bankrupt, nothing, goose egg, kanye voice: couldn't give a homeless guy change, its principals arrested, detained by island police as foreign billionaires, investigated by the Bahamaian money laundering authorities (lmao), investigated by America for the Tether theft (lmfao)

13. lmfao

47 notes

·

View notes

Text

https://mediamonarchy.com/wp-content/uploads/2024/05/20240514_MorningMonarchy.mp3

Download MP3

Devastating hits, Bezos’ DARPA grandad and Pokémon maps + this day in history w/U.S. moves Jerusalem Embassy and our song of the day by Macklemore on your #MorningMonarchy for May 14, 2024.

Notes/Links:

Are BRICS Bucks coming soon? BRICS: Prepare for US Dollar Collapse, IMF Warns

https://watcher.guru/news/brics-prepare-for-us-dollar-collapse-imf-warns

Australia’s Tax Office Tells Crypto Exchanges to Hand Over Transaction Details of 1.2 Million Accounts: Reuters; The ATO said the data will help identify traders who failed to report their cryptocurrency-related activities.

https://www.coindesk.com/policy/2024/05/07/australias-tax-office-tells-crypto-exchanges-to-hand-over-transaction-details-of-12-million-accounts-reuters/

FTX customers get good-bad news as the bankrupt exchange rides the crypto rally

https://sherwood.news/snacks/crypto/ftx-customers-get-good-bad-news-as-the-bankrupt-exchange-rides-the-crypto/

GameStop shares surge 70% as meme stock craze returns

https://www.cnbc.com/2024/05/14/gamestop-amc-shares-jump-another-40percent-in-premarket-trading-as-meme-stock-craze-returns.html

Full list of closures as major bank to shut 36 branches and cut hundreds of jobs

https://news.sky.com/story/tsb-to-close-36-branches-and-cut-hundreds-of-jobs-13131574

Video: TSB to close 36 branches with 250 jobs devastatingly hit (Audio)

https://www.youtube.com/watch?v=9juP3_SZxAk

Laura Loomer Accuses Democrat Politician Who Told Trump to ‘Go Back to Court’ of Illicit Profiteering from Hush Money Trial

https://archive.ph/Og5Ny

Elon Musk, David Sacks Holds Secret ‘Anti-Biden’ Gathering of Billi

https://californiaglobe.com/fr/elon-musk-david-sacks-holds-secret-anti-biden-gathering-of-billionaires/

Melinda French Gates steps down from Gates Foundation, retains $12.5 billion for additional philanthropy; The Gates Foundation has, over three decades, made $77.6 billion in charitable contributions, making it one of the world’s largest donor organizations.

https://www.nbcnews.com/business/business-news/melinda-gates-stepping-down-from-gates-foundation-rcna152001

FBI File on Jeff Bezos’ Grandfather, a DARPA Co-Founder, Has Been Destroyed

https://vigilantnews.com/post/fbi-file-on-jeff-bezos-grandfather-a-darpa-co-founder-has-been-destroyed/

Video: America’s Book Of Secrets: DARPA’s Secret Mind Control Technology (Audio)

https://www.youtube.com/watch?v=wZRkfBsTTt8

EU’s Controversial Digital ID Regulations Set for 2024, Mandating Big Tech Compliance by 2026

https://reclaimthenet.org/eus-controversial-digital-id-mandating-big-tech-compliance-by-2026

UK airports latest: ‘Queues only getting bigger’

https://news.sky.com/story/uk-airports-latest-queues-only-getting-bigger-after-london-and-manchester-confirm-nationwide-border-system-issue-13131330

Marvel Rivals apologises after banning negative reviews

https://www.bbc.com/news/articles/cd1wwlvd9yko

28 years later, unopenable door in Super Mario 64’s Cool, Cool Mountain has been opened without hacks

https://www.tomshardware.com/video-games/28-years-later-unopenable-door-in-super-mario-64s-cool-cool-mountain-has-been-opened-without-hacks

Pokémon Go players are altering public map data to catch rare Pokémon

https://arstechnica.com/gaming/2024/05/pokemon-go-players-are-altering-public-map-data-to-catch-rare-pokemon/

Video: Pokemon Go Versus OpenStreetMap (Audio)

https://www.youtube.com/watch?v=fLPyXy39Sv0

Image: @Hybrid’s Cover Art – Pokemon Go’s ‘Modern Solutions’

https://mediamonarchy.com/wp-content/uploads/2024/05/20240514_MorningMonarchy.jpg

May 2014 – Page 6 – Media Monarchy

https://mediamonarchy.com/2014/5/page/6/

Flashback: Americans Will Never Have the ‘Right to Be Forgotten’ (May 14, 2014)

https://mediamonarchy.com/americans-will-never-have-right-to-be/

Flashback: Modern Pope Gets Old School On The Devil (May 14, 2014)

https://mediamonarchy.com/modern-pope-gets-old-school-on-devi/

Flashback: Frugal US Consumers Make It Tough for F...

View On WordPress

#alternative news#cyber space war#Macklemore#media monarchy#Morning Monarchy#mp3#podcast#Songs Of The Day#This Day In History

2 notes

·

View notes

Text

#SignatureBank shut

View On WordPress

#America#banking#business#crypto#cryptocurrency#meme#memes#money#news#shut#signature bank#united states

16 notes

·

View notes

Text

Itau, BTG Embrace Blockchain Ahead of Brazil Digital Currency Launch

Brazil’s biggest lenders are getting behind the country’s central bank as it prepares to launch a digital version of the nation’s currency.

Itau Unibanco, BTG Pactual and Santander Brasil are all ramping up headcount and adding resources in preparation of the nationwide rollout of the digital Brazilian real, called the Drex. The accompanying blockchain platform will boost the market for digital assets in Latin America’s largest economy, the banks say.

The Drex marks the latest embrace of digital assets by central bank chief Roberto Campos Neto, who has backed the technology even as many of his peers have cracked down on it. Since taking the bank’s top job in 2019, he has argued that blockchain helps the financial system and that the technology is here to stay.

So-called distributed ledger technologies — typically used for cryptocurrencies — are already being experimented with in various parts of the financial industry. The Drex platform, both created and regulated by the central bank, will use the technology to create a new system where financial instruments — from stocks to bonds — can be “tokenized,” or represented digitally.

Continue reading.

#brazil#brazilian politics#politics#economy#monetary policy#banking#mod nise da silveira#image description in alt#central bank

2 notes

·

View notes

Text

Alternative Payment Methods (APMs) for Online Transactions

In the past decade, the world of online payments has witnessed a significant transformation. With the rise of e-commerce and the increasing preference for mobile shopping, customers now have more choices than ever when it comes to payment methods. This shift has led to the emergence of alternative payment methods (APMs) that offer customers greater convenience and flexibility. In this article, we will explore the different types of APMs, their popularity across the globe, the benefits of accepting these methods for businesses, and how to choose the best APMs for your business.

Understanding Alternative Payment Methods

Alternative payment methods refer to any form of payment that does not involve cash or traditional credit card systems like Visa, Mastercard, or American Express. These methods include domestic cards, digital wallets, bank transfers, prepaid cards, and more. Unlike traditional payment methods, APMs offer unique advantages such as enhanced security, faster processing times, and ease of use. They have become particularly popular for online transactions, with many countries seeing a significant shift towards APM usage.

Types of Alternative Payment Methods

Prepaid cards: Prepaid cards are loaded with funds by consumers and can be used for purchases until the balance is depleted. They are not directly linked to a bank account and are a popular choice for individuals who want to control their spending.

Cash-based payments: Cash-based payment methods allow customers to generate a barcode or unique reference number for their payment and then complete the transaction by paying in cash at a participating retail location. This method is particularly popular in regions with a large unbanked population.

Real-time bank transfers: Real-time bank transfers enable customers to make online payments directly from their bank accounts. This method offers instant settlement and minimal friction for customers, making it a convenient choice for many.

Direct Debit: Direct debit allows merchants to pull funds directly from customers' bank accounts for recurring payments. This method is commonly used for subscription-based services and offers a seamless and automated payment experience.

Domestic card schemes: Domestic card schemes operate similarly to global card schemes but are limited to specific markets. These schemes cater to the unique needs of consumers in their respective markets and often provide lower processing costs for merchants.

Electronic wallets (e-wallets): E-wallets allow customers to store funds digitally and use them for various transactions, both online and offline. They offer convenience, security, and often provide additional features like peer-to-peer transfers and cross-border payments.

Mobile wallets: Mobile wallets are digital wallets that are specifically designed to be used on mobile devices. Customers can load funds into their mobile wallets through various methods and make payments conveniently through their smartphones.

Digital wallets: Digital wallets are used to store payment card information securely and generate tokenized card numbers for each transaction. They offer a convenient and secure way to shop online without the need to enter card details repeatedly.

Buy now, pay later (BNPL): BNPL services allow customers to defer payments or split the cost of a purchase into installments. This method is gaining popularity for its flexibility and convenience, particularly for high-value purchases.

Cryptocurrencies and stablecoins: Cryptocurrencies like Bitcoin have gained attention in recent years, offering an alternative form of payment. Stablecoins, which are cryptocurrencies linked to fiat currencies or government bonds, aim to reduce volatility and make transactions easier.

Popular APMs Worldwide

The popularity of APMs varies across different regions and countries. Here are some notable trends:

North America

In North America, digital wallets have become the most popular payment method, surpassing credit and debit cards. Apple Pay and Google Pay are widely used, while services like PayPal and Venmo are gaining traction among the younger generation. APMs account for a significant portion of e-commerce transactions in the region.

South America

APMs are gaining ground in South America, with a projected increase in their usage for digital commerce transactions. Credit cards still dominate, but alternative online payment solutions, such as e-cash methods, are becoming more widespread. Cash on delivery is also popular, especially in countries with a large unbanked population.

Europe

In Europe, digital wallets have surpassed credit and debit cards as the preferred online payment method. Domestic debit cards, like Bancontact in Belgium and Cartes Bancaires in France, are popular alongside global card schemes. Bank transfer methods, such as iDEAL in the Netherlands and Przelewy24 in Poland, are also preferred by a significant number of consumers.

Africa

In Africa, mobile wallets have gained popularity due to the lack of bank branch infrastructure and a large rural population. Cash on delivery remains the preferred method, especially in Nigeria and South Africa. Digital wallets are also seeing growth, particularly in Kenya and Nigeria.

Middle East

Cash has traditionally been the dominant payment method in the Middle East. However, the region is experiencing a shift towards mobile wallets due to increased smartphone penetration and concerns over the transmission of cash during the pandemic. Mobile wallet adoption is supported by the expansion of international brands and government-backed payment networks.

Asia Pacific

China has its own domestic card scheme, UnionPay, which accounts for a significant portion of global card spending. Mobile payments, particularly through Alipay and WeChat Pay, are widely used in China. Other countries in the region, such as Singapore, Indonesia, and Thailand, have their own popular alternative payment methods, including GrabPay and OVO Wallet.

The Benefits of Accepting APMs for Businesses

Not accepting customers' preferred payment methods can have a negative impact on conversion rates and lead to shopping cart abandonment. Research shows that a significant percentage of consumers are deterred from completing a purchase if their preferred payment method is not available. By accepting a variety of APMs, businesses can improve customer satisfaction, increase conversion rates, and stay ahead of their competitors.

APMs offer several benefits for businesses:

Increased conversion rates: By offering a wide range of payment methods, businesses can cater to the preferences of different customer segments, leading to higher conversion rates and reduced shopping cart abandonment.

Improved customer experience: APMs provide convenience and flexibility for customers, allowing them to choose the payment method that suits their needs and preferences. This enhances the overall customer experience and fosters loyalty.

Expanded customer base: Accepting popular local and global APMs enables businesses to reach a wider customer base, including those who prefer alternative payment methods over traditional options.

Reduced fraud and chargebacks: Many APMs incorporate advanced security features, such as biometric authentication and tokenization, which help reduce the risk of fraud and chargebacks for businesses.

Access to valuable insights: APM providers often offer detailed transaction data and analytics, providing businesses with valuable insights into consumer behavior and preferences. This data can be leveraged to optimize marketing strategies and improve customer targeting.

Choosing the Best APMs for Your Business

Selecting the right APMs for your business requires a thorough understanding of your target market, customer preferences, and business requirements. Here are some steps to guide you in choosing the best APMs:

Research customer preferences: Conduct market research to identify the most popular payment methods among your target audience. Consider factors such as geography, demographics, and shopping habits to determine the most relevant APMs for your business.

Evaluate business needs: Assess your business requirements, including cost per transaction, setup and management complexity, regulatory compliance, and compatibility with your existing payment infrastructure. Choose APMs that align with your business goals and objectives.

Partner with the right providers: Work with payment service providers that offer comprehensive coverage of the APMs you wish to integrate. Ensure they have the necessary capabilities to support your business's growth and adapt to evolving customer preferences.

Test and optimize: Implement APMs in a phased approach and continuously monitor their performance. Analyze transaction data and customer feedback to identify any pain points or areas for improvement. Regularly optimize your APM strategy to maximize conversions and customer satisfaction.

By embracing the growing trend of APMs and selecting the right mix of payment methods for your business, you can enhance the payment experience for your customers and drive growth in your online sales.

Conclusion

Alternative payment methods have revolutionized the world of online transactions, offering customers greater convenience and flexibility. From digital wallets and mobile payments to real-time bank transfers and buy now, pay later services, APMs cater to a wide range of customer preferences. Businesses that embrace APMs can benefit from increased conversion rates, improved customer experience, and access to valuable insights. By understanding customer preferences, evaluating business needs, and partnering with the right providers, businesses can choose the best APMs to drive growth and success in the digital marketplace. Stay ahead of the competition by embracing the changing landscape of online payments and offering customers the payment methods they prefer.

#high risk merchant account#high risk payment gateway#offshore merchant account#payments#merchant account

3 notes

·

View notes

Text

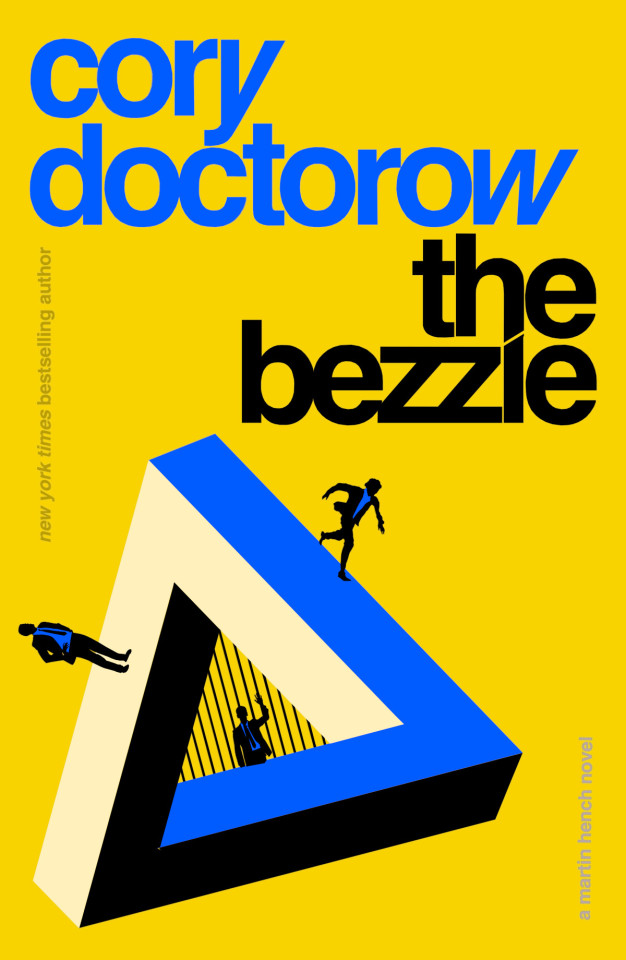

An excerpt from The Bezzle

I'm on tour with my new novel The Bezzle! Catch me next in SALT LAKE CITY (Feb 21, Weller Book Works) and SAN DIEGO (Feb 22, Mysterious Galaxy). After that, it's LA, Seattle, Portland, Phoenix and more!

Today, I'm bringing you part one of an excerpt from Chapter 14 of The Bezzle, my next novel, which drops on Feb 20. It's an ice-cold revenge technothriller starring Martin Hench, a two-fisted forensic accountant specialized in high-tech fraud:

https://us.macmillan.com/books/9781250865878/thebezzle

Hench is the Zelig of high-tech fraud, a character who's spent 40 years in Silicon Valley unwinding every tortured scheme hatched by tech-bros who view the spreadsheet as a teleporter that whisks other peoples' money into their own bank-accounts. This setup is allowing me to write a whole string of these books, each of which unwinds a different scam from tech's past, present and future, starting with last year's Red Team Blues (now in paperback!), a novel that whose high-intensity thriller plotline is also a masterclass in why cryptocurrency is a scam:

https://us.macmillan.com/books/9781250865854/redteamblues

Turning financial scams into entertainment is important work. Finance's most devastating defense is the Shield Of Boringness (h/t Dana Clare) – tactically deployed complexity designed to induce the state that finance bros call "MEGO" ("my eyes glaze over"). By combining jargon and obfuscation, the most monstrous criminals of our age have been able to repeatedly bring our civilization to the brink of collapse (remember 2008?) and then spin their way out of it.

Turning these schemes into entertainment is hard, necessary work, because it incinerates the respectable suit and tie and leaves the naked dishonesty of the finance sector on display for all to see. In The Big Short, they recruited Margot Robbie to explain synthetic CDOs from a bubble-bath. And John Oliver does this every week on Last Week Tonight, coming up with endlessly imaginative stunts and gags to flense the bullshit, laying the scam economy open to the bone.

This was my inspiration for the Hench novels (I've written and sold three of these, of which The Bezzle is number two; I've got at least two more planned). Could I use the same narrative tactics I used to explain mass surveillance, cryptography and infosec in the Little Brother books to turn scams into entertainment, and entertainment into the necessary, informed outrage that might precipitate change?

The main storyline in The Bezzle concerns one of the most gruesome scams in today's America: prison-tech, which sees America's vast army of prisoners being stripped of letters, calls, in-person visits, parcels, libraries and continuing ed in favor of cheap tablets that bilk prisoners and their families of eye-watering sums for every click they make:

https://pluralistic.net/2024/02/14/minnesota-nice/#shitty-technology-adoption-curve

But each Hench novel has a variety of side-quests that work to expose different kinds of financial chicanery. The Bezzle also contains explainers on the workings of MLMs/Ponzis (and how Gerry Ford and Betsy DeVos's father-in-law legalized one of the most destructive forces in America) and the way that oligarchs, foreign and domestic, use Real Estate Investment Trusts to hide their money and destroy our cities.

And there's a subplot about music-royalty theft, a form of pernicious wage theft that is present up and down the music industry supply-chain. This is a subject that came up a lot when Rebecca Giblin and I were researching and writing Chokepoint Capitalism, our 2022 book about creative labor markets:

https://chokepointcapitalism.com/

Two of the standout cases from that research formed the nucleus of the subplot in The Bezzle, the case of Leonard Cohen's batshit manager who stole millions from him and then went to prison for stalking him, leaving him virtually penniless and forced to keep touring to keep himself fed:

https://www.theguardian.com/music/2012/apr/19/leonard-cohen-former-manager-jailed

The other was George Clinton, whose manager forged his signature on a royalty assignment, then used the stolen money to defend himself against Clinton's attempts to wrestle his rights back and even to sue Clinton for defamation for writing about the caper in his memoir:

https://www.musicconnection.com/the-legal-beat-george-clinton-wins-defamation-case/

That's the tale that this excerpt – which I'll be serializing in six parts over the coming week – tells, in fictionalized form. It's not Margot Robbie in a bubble-bath, it's not a John Oliver monologue, but I think it's pretty goddamned good.

I'm leaving for a long, multi-city, multi-country, multi-continent tour with The Bezzle next Wednesday, starting with an event at Weller Bookworks in Salt Lake City on the 21st:

https://www.wellerbookworks.com/event/store-cory-doctorow-feb-21-630-pm

I'll in be in San Diego on the 22nd at Mysterious Galaxy:

https://www.mystgalaxy.com/22224Doctorow

And then it's on to LA (with Adam Conover), Seattle (with Neal Stephenson), Portland, Phoenix and beyond:

https://pluralistic.net/2024/02/16/narrative-capitalism/#bezzle-tour

I hope you'll come out for the tour (and bring your friends)!

Between 1972 and 1978, Steve Soul (a.k.a. Stefon Magner) had a string of sixteen Billboard Hot 100 singles, one of which cracked the Top 10 and won him an appearance on Soul Train. He is largely forgotten today, except by hip-hop producers who prize his tracks as a source of deep, funky grooves. They sampled the hell out of him, not least because his rights were controlled by Inglewood Jams, a clearinghouse for obscure funk tracks that charged less than half of what the Big Three labels extracted for each sample license.

Even at that lower rate, those license payments would have set Stefon up for a comfortable retirement, especially when added to his Social Security and the disability check from Dodgers Stadium, where he cleaned floors for more than a decade before he fell down a beer-slicked bleacher and cracked two of his lumbar discs. But Stefon didn’t get a dime. His former manager, Chuy Flores, forged his signature on a copyright assignment in 1976. Stefon didn’t discover this fact until 1979, because Chuy kept cutting him royalty checks, even as Stefon’s band broke up and those royalties trickled off. In Stefon’s telling, the band broke up because the rest of the act—especially the three-piece rhythm section of two percussionists and a beautiful bass player with a natural afro and a wild, infectious hip-wiggle while she played—were too coked up to make it to rehearsal, making their performances into shambling wreckages and their studio sessions into vicious bickerfests. To hear the band tell of it, Stefon had bad LSD (“Lead Singer Disease”) and decided he didn’t need the rest of them. One thing they all agreed on: there was no way Stefon would have signed over the band’s earnings to Chuy, who was little more than a glorified bookkeeper, with Stefon hustling all their bookings and even ordering taxis to his bandmates’ houses to make sure they showed up at the studio or the club on time. Stefon remembered October of ’79 well. He’d been waiting with dread for the envelope from Chuy. The previous royalty check, in July, had been under $250. The previous quarter’s had been over $1,000. This quarter’s might have zero. Stefon needed the money. His 1972 Ford Galaxie needed a new transmission. He couldn’t keep driving it in first.

The envelope arrived late, the day before Halloween, and for a brief moment, Stefon was overcome by an incredible, unbelieving elation: Chuy’s laboriously typewritten royalty statement ended with the miraculous figure of $7,421.16. Seven thousand dollars! It was more than two years’ royalties, all in one go! He could fix the Galaxie’s transmission and get the ragtop patched, and still have money left over for his back rent, his bar tab, his child support, and a fine steak dinner, and even then, he’d end the month with money in his savings account.

But there was no check in the envelope. Stefon shook the envelope, carefully unfolded the royalty statement to ensure that there was no check stapled to its back, went downstairs to the apartment building lobby and rechecked his mailbox.

Finally, he called Chuy.

“Chuy, man, you forgot to put a check in the envelope.”

“I didn’t forget, Steve. Read the paperwork again. You gotta send me a check.”

“What the fuck? That’s not funny, Chuy.”

“I ain’t joking, Steve. I been advancing you royalties for more than three years, but you haven’t earned nothing new since then—no new recordings. I can’t afford to carry you no more.”

“Say what?”

Chuy explained it to him like he was a toddler. “Remember when you signed over your royalties to me in ’76? Every dime I’ve sent you since then was an advance on your future recordings, only you haven’t had none of those, so I’m cutting you off and calling in your note. I’m sorry, Steve, but I ain’t a charity. You don’t work, you don’t earn. This is America, brother. No free lunches.”

“After I did what in ’76?”

“Steve, in 1976 you signed over all your royalties to me. We agreed, man! I can’t believe you don’t remember this! You came over to my spot and I told you how it was and you said you needed money to cover the extra horns for the studio session on Fight Fire with Water. I told you I’d cover them and you’d sign over all your royalties to me.”

Stefon was briefly speechless. Chuy had paid the sidemen on that session, but that was because Chuy owed him a thousand bucks for a string of private parties they’d played for some of Chuy’s cronies. Chuy had been stiffing him for months and Stefon had agreed to swap the session fees for the horn players in exchange for wiping out the debt, which had been getting in the way of their professional relationship.

“Chuy, you know it didn’t happen that way. What the fuck are you talking about?”

“I’m talking about when you signed over all your royalties to me. And you know what? I don’t like your tone. I’ve carried your ass for years now, sent you all that money out of my own pocket, and now you gotta pay up. My generosity’s run out. When you gonna send me a check?”

Of course, it was a gambit. It put Stefon on tilt, got him to say a lot of ill-advised things over the phone, which Chuy secretly recorded. It also prompted Stefon to take a swing at Chuy, which Chuy dived on, shamming that he’d had a soft-tissue injury in his neck, bringing suit for damages and pressing an aggravated-assault charge.

He dropped all that once Stefon agreed not to keep on with any claims about the forged signature; Stefon went on to become a good husband, a good father, and a hard worker. And if cleaning floors at Dodgers Stadium wasn’t what he’d dreamed of when he was headlining on Soul Train, at least he never missed a game, and his boy came most weekends and watched with him. Stefon’s supervisor didn’t care.

But the stolen royalties ate at him, especially when he started hearing his licks every time he turned on the radio. His voice, even. Chuy Flores had a fully paid-off three-bedroom in Eagle Rock and two cars and two ex-wives and three kids he was paying child support on, and Stefon sometimes drove past Chuy Flores’s house to look at his fancy palm trees all wrapped up in strings of Christmas lights and think about who paid for them.

ETA: Here's part two!

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/02/17/the-steve-soul-caper/#lead-singer-disease

#pluralistic#the bezzle#martin hench#marty hench#red team blues#fiction#crime fiction#crime thrillers#thrillers#technothrillers#novels#books#royalties#wage theft#creative labor

99 notes

·

View notes

Text

The collapse of FTX, the world’s second largest crypto-exchange, raises major questions about the viability of cryptocurrency and the state of America’s financial regulatory system. While the debate on whether FTX’s collapse means crypto should be more regulated or kept further out of the regulatory safety net rages, we must ensure that those who might have broken the law at FTX be aggressively prosecuted. Failure to prosecute individuals who broke the law is a key lesson from the last financial crisis that we must not forget as we enter the crypto crisis.

It’s clear that the 2008 global financial crisis continues to shape reaction to what some are calling crypto’s ‘Lehman Brothers’ moment. However, the more accurate analogies for FTX are the massive corporate frauds such as Enron, Tyco, and MCI WorldCom. These firms cooked their books as it seems likely that FTX did. FTX’s misdeeds appear more akin to Bernie Maddoff’s ponzi scheme and MF Global’s illegal use of customer money to fund their own speculative investments.

For those who argue that more regulation of crypto would have prevented FTX’s implosion, recall that MF Global, Lehman Brothers, and Bear Sterns were all regulated by the Securities and Exchange Commission (SEC). Similarly, Bernie Madoff who ran the largest ponzi scheme at the time in American history was well known to regulators, having served as Chairman of the NASDAQ stock exchange. FTX was not exactly out of America’s financial regulatory system either, it was licensed and registered with the Commodities Future Trading Commission (CFTC). There is no guarantee that had FTX been more closely regulated it would not have stolen customer funds like MF Global or potentially run a ponzi scheme like Madoff. Ultimately, regulation alone cannot stop people from acting illegally and unethically. Laws define what is illegal but law enforcement is required to catch and prosecute criminals.

Congress’s decision to hold hearings to uncover facts, expose wrongdoing, and amass evidence for prosecution is the right first step. These hearings will likely uncover more misfeasance in the crypto space. Potential domino contagion within crypto is quite possible, witness another crypto exchange BlockFi halting redemptions in the wake of FTX’s collapse. When consumer confidence is shaken, investors will run. The lack of regulatory safeguards and transparency into other crypto exchanges and currencies could mean that FTX is not the last or even the largest player to fail. Recall after Enron went MCIWorldComm, after Lehman went AIG.

How should the government respond? Enron executives went to jail. So did Bernie Madoff. However, almost no bank executives were personally prosecuted after the financial crisis, despite widespread misconduct. This was a major mistake in ensuring greater public confidence and accountability in how our financial system operates.

FTX is a critical opportunity for the government to get it right. Even if prosecution is more challenging because crypto’s status under the law is unclear and FTX was operating through multiple offshore enterprises, it is critical that the government use every mechanism possible to ensure personal accountability when illegal activity takes place and investors have their money stolen. One reason given during the financial crisis for the lack of prosecution was that prosecutors were afraid of losing cases. It is far better for the public to see the government attempt and fail prosecution than to not try at all. If the laws are insufficient to convict, then failed prosecutions will help build political support to change the law.

Will Congress act to regulate crypto? There had been growing bipartisan support for draft legislation on stablecoins and for crypto exchanges. Those proposals need to be fundamentally rethought in the wake of FTX’s implosion. Many on the left and right want to keep cryptocurrencies out of the regulatory system. FTX’s implosion can justify keeping crypto out of the regulated system just as it can be argued that its implosion means regulation is more urgently needed.

Crypto remains in the netherworld of financial regulation, caught between traditional definitions of securities, commodities, assets, money, and payments. As former CFTC Chairman Tim Massad pointed out the problems of our regulatory system’s fragmentation back in 2019, writing that while both the Securities and Exchange Commission and the CFTC have: “some authority over crypto-assets, neither has sufficient jurisdiction, nor do they together.” Although crypto exploded in popularity between Massad’s paper and FTX’s implosion, new regulatory authority was not given to either agency. Federal bank regulators generally tried to keep crypto out of the regulatory system, which so far seems to have limited the contagion from FTX’s implosion to the broader financial system. New York’s financial regulator never gave FTX the license necessary to operate in the Empire State, a decision that saved New Yorkers a lot of money. Sometimes the right answer by a regulator is no.

Congress should not rush to regulate crypto, nor treat the industry with a broad brush assuming all crypto is as corrupt as FTX appears to have been. As legislators take the time necessary to figure out what the right regulatory system is, prosecutors need to step up. Americans lost a lot of money in FTX, just as they did in many other large corporations that broke the law. People need to be held accountable to restore faith in the system. Let’s do a better job this time than in 2008.

5 notes

·

View notes

Text

Who controls of our whole money ?

I'm gonna start this article with a quote. Henry Ford once said, it is well enough that the people of the nation do not understand our banking and monetary system. For if they did, I believe there would be a revolution before tomorrow morning. I quote this because it encapsulates the fact that the contents of this article may be unsettling compared to the articles that I normally make.

I still feel compelled to make this article because I've been exploring the financial world for the last four years and it's definitely given me a more complete view of the world I want to share some of what I've come across with you guys. I'm also going to do a article about cryptocurrencies like Bitcoin in the future and to understand why Bitcoin and other cryptocurrencies may continue to rise. It's critical that you understand the contents of this articles. I hope that you find this topic interesting and that inspires you to do your own research afterwards.

Now, with that said, let's begin. So who controls all of our money? It's a simple question. We all know that you and I don't control it. Our employees don't control it. The companies that they work for don't control it. So who does? Where does it even come from in the 1st place?

I'll give you a hint. Money does not come from the government. It's a seemingly obvious question that's never asked or taught in schools for some reason. Unfortunately, most people's lives are basically dedicated to money. It's all people ever worry about or talk about. We go to school to learn basically how to go to university to learn the skills to get a good job so that we can trade hours of our lives all for this thing called money. So why wouldn't you want to know where money comes from and who issues it Today in this very special article you're about to find out the answer to the question of who controls all of our money?

People today can tell something isn't quite right with our financial system, but they just can't put their finger on it. Some people think it's the failure of government, others think that it's the failure of capitalism itself. This article should clarify a few things.

The year is 1694 and England had just suffered through 50 years of war. Exhausted the English Government needed loans to fund their political means. Brainchild of Scottish banker William Paterson. It was decided that a privately owned bank that could issue the money to the government out of thin air was to be the solution. This was the very first modern central banking system in the world. Central banking is more influential than laws, governments and politicians, but strangely not the focus of the general public. Fast forward to the early 20th century and after two failed attempts, a group of bankers wanted to put a central bank in the United States of America. It was December of 1910 and Senator Nelson Aldridge ordered a private train car in New York with six others. The six were not to be spotted by any news reporters to avoid questions. Their destination, Jekyll Island, off the coast of Georgia. The meeting went for 9 days and from that they created the Federal Reserve System. This is all documented and a matter of public record. Some of them went on to write about the meetings in their personal biographies.

Here's a quote from Frank Vanderlip, president of the National City Bank of New York, February 9th, 1935, in the Saturday Evening Post. " I was a secretive indeed as furtive as any conspirator discovery we knew simply must not happen, or else all our time and effort would be wasted. If it were to be exposed that our particular group had got together and written a banking bill, that bill would have no chance whatever a passage by Congress." The six men that Nelson Aldridge brought together included the head of Banks branches of government, such as the Treasury and some of the richest people on Earth at the time. To give you an idea of how rich they were in 1910, these six men represented 1/4 of the world's worth. The bankers told the American public that the purpose of the system was to stabilize the economy and to stop the grip of the Wall Street banks over America, the problem was the guys that wrote the bill were the very same people. They said they'd stop if they succeeded. It will give a small group of men the ability to create money from nothing and loan it to the American government with interest. So why was it done in secret?

Because the American people didn't want a central bank back then unlike today, people knew what central banks were and understood them very well everywhere a central bank went. There'll be wealth inequality wild swings between economic booms and pass, and after each passed, those are the top of society mysteriously came out richer while everyone else got poorer. Europe was the running example of this at the time.

The Federal Reserve was originally drafted as the Aldridge bill, but when it came into Congress, they recognised Senator Aldridge's name and smelt a rat. The bankers needed better cover. They decided to send two millionaire friends to carry the bill. To quell the suspicions of Congress and renamed it the Federal Reserve Act. Next, in the textbook lesson of the state, the bank is set out to fool the American people through disinformation in the newspapers of the day, the bank is screened and protested against the new Federal Reserve bill. It would ruin the banks, they exclaimed. The average person read the protesting articles of the bankers and thought to themselves if the bankers hate it, it must be good. And then they ended up unknowingly supporting a Trojan horse.

The bankers also fall Congress by putting clauses in the bill that limited their power, only to remove them once the bill was passed. A double head fake of the public and Congress was all it took. The bill was passed on December 23rd, 1913, while most of Congress was out on holiday, and with that a small group had complete monopoly over the issuing and creation of American money.

Today, the Federal Reserve is the most powerful entity in the United States and they're not ashamed to admit it either. Here's former Fed chairman Alan Greenspan, " What should be the proper relationship between the chairman of the Fed and a President of the United States? Well, first of all, the Federal Reserve is an independent agency, and that means, basically, that. There is no other agency of government which can overrule actions that we take, what the relationships are, don't frankly matter."

In addition to this, it seems that the Fed can't even be touched by investigating parties. " So I'm asking you if your agency has in fact, according to Bloomberg's extended $9 trillion in credit, which, by the way works out to $30,000 for every single man, woman, and child in this country, I'd like to know if you're not responsible for investigating that who is." " we actually we have responsibility for The federal reserves programs and operations. Audits to conduct Audits and investigations in that area. In terms of who's responsible for investigating Would you mind repeating the question one more time? Mr. Chairman, my my time is up but I have to tell you honestly I am shocked to find out that nobody at the Federal Reserve, including Inspector General, is keeping track of this."

So what does all of this have to do with me, you might be asking. I don't even live in the US. Well, two reasons #1 the central banking model from the Bank of England and the United States has now been put in all countries and even consolidated power in parts of Europe as the European Central Bank, or ECB, this united separate countries under one economic policy, the only places in the world that don't have central banks are North Korea, Iran, and Cuba. In 2000, this list suspiciously included Afghanistan, Iraq, and Libya.

And #2. Since the end of World War Two, the US dollar has been the reserve currency of the world. This means that all central banks hold U.S. dollars in their reserves. In other words, all other currencies are backed by the US dollar. This directly links your country to the Federal Reserve monetary policy in America. More on this lighter. When the post World War Two monetary system called the Bretton Woods system was created, all U.S. dollars were backed by an exchangeable for gold. A byproduct of this was that currencies used to be very stable in relation to each other. Before that, All the countries the exchange rates were fixed and year after year you could predict what prices were going to be. You could start a business elsewhere, know if you were, you know you could calculate profits business was. much much easier before floating Exchange rates.

Unfortunately, in 1971, due to a falling U.S. dollar, international capital flows into gold and the funding of the Vietnam War. President Nixon took the US dollar off the gold standard. " I have directed Secretary Connolly to suspend temporarily the convertibility of the dollar into gold or other reserve assets." said by Nixon. Now the dollar was floating and backed by nothing and has been ever since. OK, so let's think a little if the US dollar is backed by nothing but the world reserved are backed by the US Doller.

Intrinsically since 1971, doesn't this mean that all currencies are now backed by nothing tangible, only trust in the American government? Well, this is correct. Money backed by nothing is known as Fiat currency. Fiat in Latin means let it be done. In other words, the government says it is money, so it is.

A consequence to having money backed by nothing is that whenever the Federal Reserve creates money, it dilutes the currency supply of all other nations because their reserves are backed by the US dollar. All countries reserves are worth less each time money is created.

In the past few years, the Federal Reserve has printed trillions of dollars, and countries like Russia and China have noticed this as a reaction to the money printing. These countries have been selling U.S. dollar reserves and buying gold over the same period.

But wait a second, some of you clever thinkers out there may have asked yourself if every currency on Earth is backed by nothing. How am I able to pay for things? Well, as it turns out, the whole economic system today is running because it's backed by faith. Faith that you can exchange your unit of currency for goods or services. In a way part of that faith comes from the fact that not many people actually know where money comes from. We're about to find that out in this article.

A central bank is essentially the entity that manages a nation's money supply, and it can loan money to the government with interest. In the United States and most other countries, it works like this. When the government needs more money than they receive from taxes, they ask the Treasury Department for money. The Treasury then receives an IOU or bond from the government. The Treasury, through the banks, gives this IOU to the Federal Reserve. The Fed then writes a check for this IOU and hands it to the banks at this exchange at the banks, money is created and it can be used to pay government bills.

So hang on, where does the Fed get the money to be able to write this check? They get this money from nowhere. They literally just invent it. Here's a quote from the Boston Federal Reserve quote. When you or I write a cheque, there must be sufficient funds in our account to cover the check. But when the Federal Reserve writes a check, there is no bank deposit on which that check is drawn. When the Federal Reserve writes a check, it is creating money End Quote.

So in essence, they're writing a check and creating money from an account that has no money in it. The money the Federal Reserve creates can be used as legal tender to buy things and eventually makes its way into the real economy. If you and I did, that would go to jail for fraud, but they can do it because they invented the system. This is the same system used throughout the world today.

Another part of this money creation happens at the Commercial bank side. Every time you take out a loan to buy a house, car or TV, banks create money out of nowhere to give you this loan and you still have to pay interest on it. And don't just believe me when I say that. Hear it for yourself from the horse's mouth, the people running the system. Graham Towers, former governor of the Central Bank of Canada, states quote, " each and every time a bank makes a loan. New credit is created. New deposits brand new money" End Quote. Paul Tucker, Deputy governor of the Bank of England, quote " banks extend credit by simply increasing the borrowing customers current account" End Quote. So what they're basically saying is that each time the bank makes a loan, the bank doesn't use other people's deposited money and give it to you. It creates new money in modern times. This means typing digits into a computer.

97% of all money is digitally created like this. Only three percent is the physical cash and coins that we carry. Another crazy thing that commercial banks can do is lend out 10 times more money than they actually have in reserves. This is called fractional reserve lending.

So who wrote this ridiculous system into law?

So who wrote this ridiculous system into law ? For the United States is was part of the Federal Reserve System, drafted in 1913, and again this is the same system used throughout the world.

So what's the issue? Why should I even care?

Who was consequences? When more lines are given out, more money is created and the rest of the money in circulation is worth less and less as the years go on. This is known as inflation. In a way, inflation is basically a tax that we all pay for the fraud of money printing easy money now in exchange for tax on our future generations.

It's also why in 1950 a house used to cost $7000 and a car $2000. Obviously this is no longer the same today. Things will always keep getting more expensive as long as this system is in place.

This was actually kind of OK because wages grew in relation to inflation until about 2008. Why this stopped happening is a story for another day. So things are already pretty crazy, but they get even crazier the more you look into it the stranger things become. So remember how we're talking about how central banks and commercial banks can create money out of nothing?

This procedure actually does create something. It creates debt. Let me explain. When you take out a loan, it's written down as an asset in the bank as a negative form, kind of like a negative value of money or otherwise known as debt. Under this system, debt is actually money.

And again, don't just listen to me. Marriner Eccles, former governor of the Federal Reserve states quote. " If there were no debts in our money system, there wouldn't be any money." So in essence, instead of gold being the backbone of our economy, it's now debt.

The system we're under now is sometimes referred to as the debt based monetary system. It requires that debt always grows countries and people must become deeper in debt so that there's more money in the system, because remember, debt is money.

If people in government stop borrowing money and pay back loans, the debt doesn't grow. The money supply shrinks and the system falters. It truly is bizarre, but we all live in this system each and every day. The Federal Reserve and other central banks control money by adjusting its supply and how much it costs to borrow money, otherwise known as the interest rate. With these tools, and as a consequence of human group psychology, central banks can create booms and busts in the economy at will, and also to store and derail an economy by messing with it. Let's take a quick case study in the year 2000, Federal Reserve Chairman Alan Greenspan cut interest rates to 1%. He did this to try and fight off recession from the dot com bubble and encourage people to borrow money when interest rates are low. If you're borrowing money, you save a whole lot on repaying mortgages. Since the 1% interest rate hadn't been seen at the time since the 1950s. It was a pretty good deal. Greenspan's idea was that he could create a wealth effect. People would start to buy houses. The prices would go up, and the people would feel wealthier and spend more money in the economy and stimulate it. Greenspan sure succeeded in getting people to borrow money to buy houses, but they borrowed too much and the result was the 2008 housing bubble. This is a prime example of what can go wrong when central banks mess with an economy. Yes, corrupt bankers have a lot to answer for on their role in the 2008 crisis, but the Fed has a far bigger long term impact.

Even crazier things are happening in Japan. Their central bank is buying so many stocks that they were the number one buyer of Japanese stocks in 2016, so they have part ownership of companies with money that they created from nothing.

So in essence, it is the central banks that control our economy and the central and commercial banking system together that control all of our money. The difference is central banks can create money at will while commercial banks need loans to create money.