#Who Qualifies for the American Opportunity Credit?

Text

Are education expenses tax deductible ?

Outline:

Introduction

Understanding Tax Deductions

What Are Tax Deductions?

Common Tax Deductions

Education Expenses and Tax Deductions

Eligible Education Expenses

Qualifications for Tax Deductions

The American Opportunity Credit

Who Qualifies for the American Opportunity Credit?

How Much Can You Claim?

The Lifetime Learning Credit

Who Qualifies for the Lifetime Learning Credit?

How Much Can You Claim?

Tuition and Fees Deduction

Who Qualifies for the Tuition and Fees Deduction?

How Much Can You Claim?

Student Loan Interest Deduction

Who Qualifies for the Student Loan Interest Deduction?

How Much Can You Claim?

Employer Tuition Assistance

Tax-Free Educational Assistance

Limits on Employer-Provided Education Benefits

Educational Savings Accounts

Coverdell Educational Savings Account (ESA)

529 Plans

Tax Deductibility of Work-Related Education

Qualifying Work-Related Education Expenses

Exceptions and Limitations

State Tax Deductions for Education Expenses

State-Specific Deductions and Credits

Researching State Tax Laws

Recordkeeping and Documentation

Importance of Proper Documentation

Retaining Education Expense Records

The Impact of Income on Deductibility

Phase-Out Limits for Education Expenses

Other Education-Related Tax Benefits

Student Loan Forgiveness Programs

Employer Student Loan Repayment Assistance

Tax Deductibility of Education Expenses for Self-Employed Individuals

Conclusion

Are Education Expenses Tax Deductible?

Education is a vital aspect of personal and professional growth, but it can also come with a hefty price tag. As individuals pursue higher education, the question of whether education expenses are tax-deductible becomes essential. In this article, we will explore the various tax deductions and credits available to help alleviate the financial burden of educational pursuits.

Understanding Tax Deductions

What Are Tax Deductions?

Tax deductions are specific expenses that taxpayers can subtract from their total income, ultimately reducing the amount of income that is subject to taxation. Deductions lower the overall tax liability, resulting in potential tax savings for eligible individuals.

Common Tax Deductions

Before delving into education-related deductions, it's essential to understand some common deductions available to taxpayers, such as:

Ø Home mortgage interest

Ø Charitable contributions

Ø Medical expenses

Ø State and local taxes

Ø Retirement contributions

Ø Education Expenses and Tax Deductions

Eligible Education Expenses

The Internal Revenue Service (IRS) allows taxpayers to claim certain education expenses as deductions or credits. Eligible expenses often include:

· Tuition and fees for enrollment

· Books, supplies, and required course materials

· Necessary equipment for courses

· Qualified educational software

· Qualifications for Tax Deductions

To qualify for education-related tax deductions, certain criteria must be met. Generally, the education must be for the taxpayer, their spouse, or a dependent. Additionally, the expenses should be related to enrollment in an eligible educational institution.

The American Opportunity Credit

§ Who Qualifies for the American Opportunity Credit?

The American Opportunity Credit is a tax credit that offers substantial financial assistance to eligible students pursuing higher education. To qualify, students must be pursuing a degree or other recognized educational credential and be enrolled at least half-time in their program.

§ How Much Can You Claim?

As of the time of writing, the American Opportunity Credit allows eligible taxpayers to claim up to $2,500 per student per year for the first four years of post-secondary education.

The Lifetime Learning Credit

o Who Qualifies for the Lifetime Learning Credit?

Unlike the American Opportunity Credit, the Lifetime Learning Credit is available to both undergraduate and graduate students, as well as those pursuing professional degrees or taking classes to acquire or improve job skills.

o How Much Can You Claim?

As of the time of writing, the Lifetime Learning Credit permits eligible taxpayers to claim up to 20% of the first $10,000 of qualified education expenses, resulting in a maximum credit of $2,000 per tax return.

Tuition and Fees Deduction

Ø Who Qualifies for the Tuition and Fees Deduction?

The Tuition and Fees Deduction allows eligible taxpayers to deduct qualified education expenses even if they do not itemize deductions on their tax return.

Ø How Much Can You Claim?

As of the time of writing, eligible taxpayers may deduct up to $4,000 from their taxable income.

Student Loan Interest Deduction

I. Who Qualifies for the Student Loan Interest Deduction?

Taxpayers who have taken out student loans to cover qualified education expenses may be eligible for the Student Loan Interest Deduction.

II. How Much Can You Claim?

As of the time of writing, eligible taxpayers can deduct up to $2,500 of student loan interest paid throughout the tax year.

Employer Tuition Assistance

i. Tax-Free Educational Assistance

Employers may offer tuition assistance to employees as part of their benefits package, and in some cases, this assistance may be tax-free up to a certain limit.

ii. Limits on Employer-Provided Education Benefits

While employer-provided tuition assistance can be advantageous, there are specific limitations to be aware of, such as the maximum amount of tax-free assistance allowed per year.

Educational Savings Accounts

· Coverdell Educational Savings Account (ESA)

Coverdell ESAs are tax-advantaged accounts designed to help families save for education expenses.

· 529 Plans

529 Plans are state-sponsored savings plans that offer tax benefits for qualified education expenses, including tuition, books, and room and board.

Tax Deductibility of Work-Related Education

§ Qualifying Work-Related Education Expenses

Expenses related to education undertaken to maintain or improve skills needed in one's current employment or to meet the employer's requirements may be tax-deductible.

§ Exceptions and Limitations

The IRS imposes certain exceptions and limitations on work-related education deductions, which taxpayers should be aware of.

State Tax Deductions for Education Expenses

o State-Specific Deductions and Credits

Apart from federal deductions and credits, some states offer additional tax breaks for education expenses.

o Researching State Tax Laws

It is essential to research the specific tax laws in your state to determine the available deductions and credits related to education expenses.

Recordkeeping and Documentation

ü Importance of Proper Documentation

Maintaining accurate and detailed records of education expenses is crucial when claiming tax deductions or credits.

ü Retaining Education Expense Records

Taxpayers should keep all relevant documents, including tuition statements, receipts, and enrollment records, to support their claims.

The Impact of Income on Deductibility

* Phase-Out Limits for Education Expenses

The availability of certain education-related deductions and credits may be affected by the taxpayer's income level.

Other Education-Related Tax Benefits

Ø Student Loan Forgiveness Programs

Certain federal student loan forgiveness programs may offer tax-free forgiveness of the remaining loan balance.

Ø Employer Student Loan Repayment Assistance

Some employers may provide student loan repayment assistance as an employee benefit.

Ø Tax Deductibility of Education Expenses for Self-Employed Individuals

Self-employed individuals may be eligible to deduct qualified education expenses as business expenses.

Conclusion

Education is a lifelong pursuit that comes with various costs, but the good news is that there are several tax deductions and credits available to help ease the financial burden. From the American Opportunity Credit to employer tuition assistance and state-specific benefits, exploring these options can make a significant difference in managing educational expenses.

Now, take advantage of the tax benefits and invest in your future. Maximize your potential, both personally and professionally, through the power of education.

FAQs

Can I claim tax deductions for my child's education expenses?

Yes, you may be eligible to claim certain education-related deductions or credits for your child's education expenses, depending on your circumstances.

Are student loan interest payments always tax-deductible?

No, the deductibility of student loan interest payments depends on various factors, including your income and filing status.

Can I claim education expenses if I am attending school part-time?

Yes, in some cases, you may still be eligible to claim education-related tax benefits while attending school part-time. Be sure to review the specific requirements for each credit or deduction.

What is the difference between a tax deduction and a tax credit?

Tax deductions reduce your taxable income, while tax credits directly reduce the amount of taxes you owe.

How do I know if my state offers additional education-related tax benefits?

You can visit your state's official tax website or consult with a tax professional to understand the specific education-related tax benefits available in your state.

#Are education expenses tax deductible ?#Outline:#Introduction#Understanding Tax Deductions#What Are Tax Deductions?#Common Tax Deductions#Education Expenses and Tax Deductions#Eligible Education Expenses#Qualifications for Tax Deductions#The American Opportunity Credit#Who Qualifies for the American Opportunity Credit?#How Much Can You Claim?#The Lifetime Learning Credit#Who Qualifies for the Lifetime Learning Credit?#Tuition and Fees Deduction#Who Qualifies for the Tuition and Fees Deduction?#Student Loan Interest Deduction#Who Qualifies for the Student Loan Interest Deduction?#Employer Tuition Assistance#Tax-Free Educational Assistance#Limits on Employer-Provided Education Benefits#Educational Savings Accounts#Coverdell Educational Savings Account (ESA)#529 Plans#Tax Deductibility of Work-Related Education#Qualifying Work-Related Education Expenses#Exceptions and Limitations#State Tax Deductions for Education Expenses#State-Specific Deductions and Credits#Researching State Tax Laws

0 notes

Text

It is so FRUSTRATING trying to explain the problems with Avatar the Way of the Water to people. I’ve been in conversation with people (including people who has said they identity with tribal/indigenous culture) and how the only people who “care” about the casting of the movie are black Americans or Americans in general, and how “we always try to make things about race” and how there’s “no need” for more POC to be on the cast, asking ME what qualifies me to speak on such matters… LIKE BRO. It is AMAZING to hear about all of the time and research that went into trying to accurately represent certain cultures. But that means ABSOLUTELY NOTHING if they are going to go and cast white actors to play these characters. Yes, the movie is about blue alien people and we don’t actually see the faces of the actors, but they were handed the opportunity to uplift POC/indigenous actors and provide them with a possibly breakout role that would’ve jumpstarted their careers and they didn’t. I say this especially in relation to the Metkayina tribe and it’s casting (also Ronal, Kate did an amazing job but again I was shocked af to find they didn’t cast a Poly actress to play her). With the other Na’vi tribes it is a mix of different cultural aspects, but with the Metkayina I could clearly see the influence of Polynesian culture.

More importantly it’s about US medias/Hollywoods inclusion of actors of color in important roles. And I also find the casting kind of ironic given the movies narrative appropriation, colonization, and the erasure/demonization of native people. To not have people or individuals in the main cast, who can identify with these struggles, and tell their story, relate to the character on a more personal level, is a distinct failure within this movie. You may not see their faces when you go to the movies, but you will see them in the press, you will see their faces and read their words in articles and reviews, they are credited for their roles. This could’ve been a HUGE opportunity for POC/indigenous actors in a sphere that already doesn’t acknowledge them.

#avatar the movie#avatar 2#avatar the way of water#avatar#avatar the way of the water#neteyam sully#neteyam#lo’ak sully#lo’ak#kiri sully#kiri#tuk sully#tuktirey#tuk#neytiri sully#neytiri#jake sully#sky people#na’vi#spider socorro#zoey saldana#sam worthington#james cameron#film#movie review#hollywood#acting#poc voices#ewya help us#r1dd1kulus.ramblings

75 notes

·

View notes

Text

important questions for americans who file taxes as independents!

were you in 2022

pursuing an undergrad degree

in your first four years at the beginning of 2022

paying tuition or college related expenses (this includes via student loans in your name)

if so, you probably qualify for the american opportunity tax credit. you can get 40% of the credit (up to $1k!) refunded to you even if you otherwise wouldn’t be refunded anything.

more info here. you can claim it for up to four years! even though i have only paid like $200 a year in taxes bc i don’t make much, i’ve made like $1200 a year back since i started college thanks to this.

also if you’re looking for somewhere to file taxes for free and without a lot of hassle, freetaxusa has been nice to use. they only charge for state taxes, are super easy to navigate, and they ask a lot of questions to make sure you’re maximizing your refund.

40 notes

·

View notes

Text

CPR in Redlands: Promoting Healthier Lives through Education and Certification

Looking for CPR certification in Redlands? Look no further! Palm Desert Resuscitation Education (PDRE) is your trusted provider of healthcare and non-healthcare classes, courses, seminars, and continuing education credits (CEUs) in Southern California. As an authorized training center for renowned organizations such as the American Heart Association (AHA), American Academy of Pediatrics (AAP), and American Red Cross (ARC), PDRE is committed to delivering up-to-date education and information on life-saving techniques.

youtube

PDRE HIGHLAND OFFICE

Valencia Lea Adult Mobile Home

3850 Atlantic Ave. (Hubbard Hall)

Highland, CA 92346

1-909-809-8199

At PDRE, our mission is to reduce the morbidity and mortality rates associated with cardiovascular diseases, strokes, and other medical emergencies. We achieve this by offering evidence-based learning and professional education in accordance with the most current guidelines and recommendations from leading organizations in the field. Our dedicated team of highly qualified professional educators and experienced healthcare personnel ensures that you receive top-notch training and certification.

BLS Certification in Redlands

ACLS in Redlands

Whether you are a healthcare professional, an allied health professional, or a non-healthcare provider, PDRE has the courses and certifications to meet your needs. We offer a comprehensive range of classes, including CPR, first aid, Basic Life Support (BLS), Advanced Cardiovascular Life Support (ACLS), Pediatric Advanced Life Support (PALS), Neonatal Resuscitation Program (NRP), and more. With both classroom-based and online options, we make it convenient for you to acquire the knowledge and skills necessary to save lives.

ACLS Certification in Redlands

PALS in Redlands

When you choose PDRE for your CPR certification in Redlands, you can expect nothing but excellence. Our instructors are passionate about empowering individuals with the confidence to respond effectively in emergency situations. They bring their wealth of experience and expertise to the classroom, ensuring that you receive the highest quality training. Through hands-on practice, interactive discussions, and real-life scenarios, you will gain the practical skills and theoretical knowledge needed to handle emergencies with composure and competence.

PALS Online in Redlands

NRP in Redlands

Not only do we offer certification courses, but we also provide continuing medical education (CME) opportunities. As healthcare guidelines and protocols evolve, it is crucial for professionals to stay updated. PDRE offers CME courses that cover the latest advancements and research in the field of resuscitation and emergency care. By participating in these courses, you can earn valuable credits while enhancing your knowledge and skills.

At PDRE, we believe that everyone has the potential to be a lifesaver. That's why we also cater to novice laypersons who want to learn CPR and first aid skills. By making these courses accessible to the general public, we aim to create a community of individuals who are prepared to respond effectively during emergencies. Whether you are a parent, teacher, caregiver, or concerned citizen, our classes will equip you with the confidence and competence to make a difference.

So, if you're looking for CPR classes in Redlands, PDRE is here to meet your needs. Our commitment to excellence, evidence-based education, and professional certification sets us apart as a leading provider in the region. Join us in our mission to promote healthier lives and make a positive impact on the well-being of our community. Visit our website or contact us today to learn more about our courses and schedule your training. Together, we can save lives.

2 notes

·

View notes

Text

Biden Turbocharges Clean Energy in Underserved Communities

Major developments aimed at tackling energy inequality are happening. The Biden administration is significantly boosting incentives and resources to drive clean energy deployment in underserved communities across America.

The U.S. Department of the Treasury and Internal Revenue Service announced today that applications will open on May 28 for the second year of the Low-Income Communities Bonus Credit Program - a key provision of President Biden's Inflation Reduction Act providing up to a 20 percentage point tax credit boost for solar and wind projects located in low-income areas.

Deputy Treasury Secretary Wally Adeyemo said:

"This groundbreaking incentive created by President Biden's Inflation Reduction Act is creating jobs and opportunity while lowering energy costs for communities that were long underinvested in."

"In the program's first year, we saw sky-high demand for these clean energy investments."

Boosting Capacity and Equity Provisions

Program Enhancements for 2024:

Over 2.1 gigawatts of total capacity available, up from 1.8 GW in 2023

325 additional megawatts rolling over from very high first-year demand

Expanded eligibility criteria and subcategories for equitable distribution

At least 50% of capacity reserved for projects meeting additional criteria

Targeting Low-Income Residential Areas

The program allocates federal tax credits to qualifying solar and wind facilities under 5 megawatts located in low-income residential areas, on tribal lands, or providing direct economic benefits to lower-income households. It aims to lower energy burdens while catalyzing private investment in historically underserved communities.

Ensuring Investments Reach Most In Need

This second program year also incorporates key enhancements based on lessons learned in 2023. Most notably, at least half of the available credits in each category are now reserved for projects meeting additional socioeconomic and community benefit criteria beyond just geographic location.

"The program's impact will grow even more in its second year thanks to the increased available capacity and new provisions to ensure investments reach the communities most in need of affordable clean power,"

said Senior White House Climate Advisor John Podesta.

Turbocharging Clean Energy Investment

This incentive structure has already turbocharged private capital flowing into community solar projects, rooftop installations, microgrids and more across America's urban cores and rural towns. According to a recent Princeton study, low-income areas received over 5 times more proposed solar investments in 2023 compared to 2022 baselines.

Concerns Over Equity Remain

However, some environmental justice advocates argue the program's impact has been inequitably distributed so far, with wealthier communities capturing a disproportionate share of the tax credits. The new 50% set-aside aims to address those concerns.

"While a step in the right direction, we need to see much more from this administration in terms of actually delivering affordable clean energy to the frontline communities who have disproportionately borne the brunt of fossil fuel pollution for decades,"

said Juan Jhones-Lugo, Energy Justice Director at The Oak Collective.

Helping Families Navigate Incentives

The Treasury Department will host a public webinar on May 16 providing additional details and guidance ahead of the May 28 application opening date. All submissions within the first 30 days will be treated equally to ensure fair access.

But beyond the tax credits themselves, the Biden administration is deploying a multi-pronged strategy to ease clean energy access and lower costs for American families - especially in underserved communities.

Multi-Faceted Approach

Key Administration Clean Energy Cost-Saving Initiatives:

$20 billion Greenhouse Gas Reduction Fund to finance community lending

State home energy rebate programs launching this summer, worth up to $8,000 per household

Expanded tax credits of 30% for residential solar, heat pumps, efficiency upgrades

Nonprofit coalition campaigns for consumer education and awareness

Renewed focus on bridging financing gaps for low and middle-income families

Driving Affordability and Sustainability

"We're using every tool available to help families across America save money by tapping into affordable clean energy," Adeyemo stated. "From generous tax credits to innovative financing, this is a top priority for the Biden economic agenda."

As climate impacts escalate and energy costs remain volatile, the administration is betting its "whole-of-government" push can finally unleash clean energy's promise of lower utility bills, efficiency gains, and greener communities from coast to coast.

Access the latest program details, state-by-state information on incentives, and guidance for applicants at www.irs.gov/lowincomecredit.

Sources: THX News, The US Treasury & The White House.

Read the full article

#Bidenadministration#cleanenergy#incentives#low-incomeareas#solar#taxcredit#Treasury#UnderservedCommunities#utilitybills#thxnews

0 notes

Text

Equipment Financing: Quick Funding In Your Small Business

Business equipment financing is usually viewed as a more cost-effective and lower-risk means compared to different types of financing. It permits businesses to maintain their cash reserves as a end result of they do not purchase the equipment outright. You personal the equipment and need to make funds; whereas with a lease, you are renting the equipment and don't personal it. With equipment financing, you'll be able to claim depreciation on your asset to reduce your tax liability. To qualify for a small business loan with Fora Financial, potential borrowers must have six months in business and an annual income of at least $144,000. In addition, the company also states that it is going to not work with any companies which have had a recent chapter.

Equipment loans are the usual option for financing equipment for the explanation that loan is backed by the equipment being bought. They are extensively out there from banks and different lenders, but you might also discover financing choices through the seller. This availability means that business owners should have the ability to discover an option that meets their business���s needs. Depending upon the equipment, lease terms might last from typically three to 10 years. The equipment is owned by the leasing company, which expenses you a flat monthly charge that includes an interest rate of usually 5% to 16%.

We develop solutions that breakdown communication barriers & visualize the end-to-end lending process by empowering members. Through know-how we’ll construct the frictionless course of our clients deserve. Taycor’s hybrid lending strategy permits us to help debtors from throughout the credit score spectrum with timely entry to capital. This method fosters improved productiveness, streamlined processes, and a sustained competitive edge in the market while preserving monetary stability and selling long-term growth. Request equipment financing today and stay ahead of the competitors. Submit a financing request and discover the ability of kit financing for your business.

Use our fast, application-only process for transactions as much as $200,000. Tree felling, pruning, and wood chipping require specialized instruments like chainsaws, logging winches, and chippers. Without the right equipment, tasks become challenging and inefficient — doubtlessly resulting in hazards and losses.

This route permits them to protect cash, acquire the necessary equipment and align funds to the helpful lifetime of the belongings. Equipment financing offers companies with the opportunity to entry state-of-the-art equipment and expertise which may otherwise be financially out of attain. By staying up to date with the newest equipment, businesses can enhance productiveness, high quality, and buyer satisfaction, gaining a aggressive edge out there.

Business house owners can probably get same-day funding for pressing equipment wants. Used equipment can often be purchased at a fraction of the worth of recent. But not all companies and banks are prepared to extend credit score for the acquisition of used equipment. Keystone understands that many companies favor to purchase used equipment to run their companies. Keystone may help you finance used equipment, permitting you to purchase one machine or outfit your entire operation with reasonably priced pre-owned assets. The cost of your Equipment Financing will differ on several elements, such as the amount being financed, your personal credit rating, and your business’s financial well being.

The building industry has been a important piece of the North American financial system for many years. Everything you should know about SBA 7(a) loans, multi functional convenient location. However, before making any business decision, you should seek the guidance of a professional who can advise you based on your individual scenario. Entrepreneurs and trade leaders share their best recommendation on tips on how to take your organization to the subsequent degree. At Team Financial Group, we make use of streamlined, standardized processes when working with our vendor companions, which helps us maximize effectivity. However, we also attempt to balance this strategy by offering as much flexibility as each vendor needs.

equipment finance solutions

Unlike a conventional loan that has set phrases of month-to-month funds, a business line of credit score allows you to borrow solely the precise quantity needed and then repay only that quantity. Plus, as soon as the amount borrowed is paid again, it's out there to borrow again. That is called a revolving line of credit score, very like a credit card. National Funding also presents other forms of lending products apart from simply equipment loans.

For transactions under $1 million, potential shoppers know inside a number of business days. Transactions over $1 million require a extra holistic lessee evaluate, whereby approvals can take as a lot as 2 weeks. The typical vary of opportunities we fund is from $500,000 to $20 million. We additionally companion with banks and different financing organizations to assist companies attain the extent of financing they need. We are right here to make this easy, with a single point of contact and streamlined documentation process. From a dedicated back office to our trade expertise, we serve 1000's of shoppers together with those concerned in development, manufacturing, know-how and the nonprofit sectors.

The approvals are coupled with competitive rates and you have the flexibility to qualify for as a lot as $250,000. You also can request free lease quotes and session if you are weighing a few totally different leasing choices with other companies. 1West provides financing on practically any kind of used or new business equipment.

#equipment financing companies#equipment finance#best equipment financing companies#equipment financing company#equipment funding#equipment finance solutions#equipment loans for new business#equipment financing services#transportation equipment financing

1 note

·

View note

Text

Best Dallas-fort Worth Area Factoring Companies

There are not any curiosity funds to make as a result of invoice factoring doesn’t create loans. Under a non-recourse agreement, the factoring company assumes the chance of nonpayment, and the enterprise just isn't required to buy back any invoices—even those who go unpaid. For this purpose, non-recourse factoring agreements are sometimes dearer and are reserved for industries that pose less risk to factoring companies. The advance fee is the percentage of outstanding invoices the factoring company pays the enterprise upfront. The share usually ranges from 70% to 95% however hovers round 80% for many businesses.

We imagine everybody ought to have the flexibility to make financial choices with confidence. Dallas is house to over sixty five,000 companies, together with hometown-based companies corresponding to American Airlines, Exxon-Mobil, and 21 different Fortune 500 companies. The Dallas-Fort Worth area brings nice range, educational institutions, a various economic system, and social opportunities to companies and professionals.

No matter the sort of account you might have with the company, a great factor will make a diligent effort to gather your invoices. Learn extra about whether or not factoring is cost-effective on your company. Founded in 1986, RTS Financial is one other organization that specializes in the trucking trade. That implies that RTS Financial presents particular perks and benefits that fit your business and unique wants.

Factoring companies for trucking, additionally known as freight factoring companies, give trucking companies cash in trade for excellent invoices. With more than a hundred years of collective experience, the American Bank Business Finance group brings invaluable business, finance and operations insight. Dedicated to serving our purchasers, we measure success by our relationships and the value we deliver your small business. This dedication has allowed us to supply invoice factoring providers to tons of of companies — and we can’t wait to study extra about your small business. Factoring companies play an important role in Chicago’s business panorama, offering businesses with the financial assist they want to thrive. By promoting their invoices to a factoring company, companies can obtain funds inside hours, somewhat than waiting 30, 60, or even ninety days for a customer to pay.

First, companies that need to obtain cash shortly from their invoices to buy inventory or materials in bulk. Second, though a lot less frequent, companies that can’t gather payments from their prospects often. Unlike a number of the factoring companies on our listing, you may have to reach out to a company representative to get qualification requirements. For extra personalised service, be at liberty to succeed in out to us instantly. We’re joyful to attach you with a factoring company tailor-made to your particular business requirements and provide you with a free factoring price quote.

Factoring companies in Dallas

Factoring companies offer invoice factoring to organizations that work on business-to-business models rather than business-to-consumer ones. Companies such as construction contractors and staffing businesses often experience lengthy payment cycles that put a pressure on business operations. Invoice factoring saves the day with fast entry to money to pay for supplies, advertising companies, and salaries. 1st Commercial Credit has all the monetary resources to assist Dallas- primarily based businesses.

Plus, those that qualify can use Apex 24/7 Factoring service to get paid anytime, anyplace via blynk® , including nights, weekends, and bank holidays. Successful companies operating in the San Antonio area are shortly realizing the advantages of invoice factoring. Invoice factoring has grown in reputation amongst all forms of enterprises because it permits the businesses to trade their unpaid invoices in change for immediate cash, or working capital. Overall, Texas offers a variety of factoring companies to help businesses in virtually each trade enhance their money circulate and backside line. Moreover, factoring companies help cut back the danger of business failures because of cash move issues. By buying their invoices, they supply businesses with the money they should proceed their operations, preventing potential bankruptcies and job losses.

Factor charges generally vary from 0.50% to 5% per month an invoice stays excellent and could also be fastened or variable. We are one of the top factoring companies for medical accounts receivable. Whether you've a small practice or a big health care organization, we can present up to $100 million in funding by factoring your outstanding insurance coverage receivables. By working with Riviera, this distributor of golf shirts was able to buy out a personal investor with their first funding. The increased cash flow gained from Riviera’s companies allowed them to keep their funds with suppliers present and to realize growth objectives.

#Dallas factoring company#Dallas factoring companies#Factoring companies in Dallas#Invoice factoring Dallas TX#Invoice factoring Dallas#Factoring companies Dallas TX#Best Dallas factoring company#top Dallas factoring company#Dallas factoring#factoring company in Dallas#Factoring companies in Dallas Texas

1 note

·

View note

Text

Maximizing Deductions: Strategies for Optimizing Your Tax Return

Introduction:

Tax season can be a stressful time for many individuals and businesses alike. However, understanding how to maximize deductions can significantly impact your tax return, potentially saving you money and reducing your taxable income. In this blog post, we will explore various strategies for optimizing your tax return by maximizing deductions. From common deductions to lesser-known opportunities, we'll cover everything you need to know to make the most of tax season.

Understanding Deductions:

Deductions are expenses that you can subtract from your taxable income, reducing the amount of income that is subject to taxation.

Common deductions include:

Mortgage interest

Property taxes

Medical expenses

Charitable contributions

State and local taxes

It's essential to keep accurate records of your deductible expenses throughout the year to ensure you can claim them come tax time.

Keeping Track of Expenses:

Maintaining detailed records of your deductible expenses is crucial for maximizing your deductions.

Utilize software or apps to track expenses, organize receipts, and categorize deductions efficiently.

Be diligent about documenting all potential deductions, including business expenses, unreimbursed work-related costs, and any other eligible expenses.

Leveraging Retirement Contributions:

Contributing to retirement accounts such as a 401(k) or IRA not only helps you save for the future but can also provide immediate tax benefits.

Contributions to traditional retirement accounts are typically tax-deductible, reducing your taxable income for the year.

Take advantage of employer-sponsored retirement plans and consider maximizing contributions to reap the full tax benefits available.

Exploring Education Credits and Deductions:

Education-related expenses can also qualify for tax deductions or credits.

The American Opportunity Tax Credit and the Lifetime Learning Credit are two common credits available to taxpayers who incur higher education expenses.

Additionally, student loan interest may be deductible, providing further opportunities to reduce taxable income.

Maximizing Business Deductions:

If you are a business owner or self-employed individual, there are numerous deductions available to you.

Deductible business expenses may include office supplies, equipment purchases, travel expenses, professional services, and more.

Keep detailed records of all business-related expenses and consult with a tax professional to ensure you are maximizing your deductions while remaining compliant with tax laws.

Taking Advantage of Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs):

Contributions to HSAs and FSAs can provide tax advantages for medical expenses.

Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

FSAs allow you to set aside pre-tax dollars for eligible medical expenses, reducing your taxable income.

Timing Deductions Strategically:

Consider timing your deductions strategically to maximize their impact on your tax return.

For example, if you anticipate significant medical expenses, it may be beneficial to schedule elective medical procedures before the end of the tax year to maximize your deduction.

Similarly, accelerating charitable contributions or prepaying deductible expenses can help boost your deductions in a particular tax year.

Seeking Professional Advice:

Tax laws and deductions can be complex and subject to change, making it essential to seek professional advice.

Consult with a qualified tax professional or accountant to ensure you are taking advantage of all available deductions and credits while minimizing your tax liability.

A tax professional can provide personalized guidance based on your individual financial situation and help you navigate the complexities of the tax code.

Conclusion:

Maximizing deductions is a key strategy for optimizing your tax return and reducing your tax liability. By understanding the various deductions available, keeping detailed records of expenses, and leveraging tax-advantaged accounts and credits, you can make the most of tax season. Whether you're a business owner, individual taxpayer, or somewhere in between, implementing these strategies can help you maximize your deductions and achieve greater financial flexibility. Remember to consult with a tax professional for personalized advice tailored to your specific circumstances. With careful planning and attention to detail, you can take control of your tax return and make tax season a little less daunting.

0 notes

Text

Tax Optimization with John Moakler: Minimizing Tax Liabilities for Medical Professionals

As medical professionals, doctors face unique challenges when it comes to financial planning, with tax optimization being a crucial aspect of their overall strategy. Effective tax planning can help medical professionals minimize their tax liabilities, maximize their savings, and achieve their long-term financial goals. By understanding key tax optimization strategies tailored to their profession, doctors can ensure that they make the most of their hard-earned income while complying with applicable tax laws.

Understanding Tax Deductions and Credits

One of the fundamental aspects of tax optimization for medical professionals is understanding the various deductions and credits available to them. Medical professionals may be eligible for a wide range of deductions, including expenses related to continuing education, professional dues and subscriptions, medical supplies, and equipment purchases. Additionally, they may qualify for tax credits such as the Lifetime Learning Credit or the American Opportunity Tax Credit for educational expenses.

To take full advantage of available deductions and credits, medical professionals should maintain accurate records of their expenses and consult with a qualified tax professional to ensure compliance with tax laws and regulations. By leveraging available tax incentives with the help of experts like John Moakler, doctors can reduce their taxable income and keep more of their earnings for investment and wealth-building purposes.

Maximizing Retirement Contributions

Another effective tax optimization strategy for medical professionals is maximizing contributions to retirement accounts such as 401(k) plans, individual retirement accounts (IRAs), or health savings accounts (HSAs). Contributions to these accounts are often tax-deductible or offer tax-deferred growth, allowing doctors to lower their taxable income and build tax-advantaged savings for retirement.

Medical professionals should aim to contribute the maximum allowable amount to their retirement accounts each year, taking advantage of employer matching contributions and catch-up contributions for those nearing retirement age. By prioritizing retirement savings under the guidance of experts like John Moakler and maximizing contributions to tax-advantaged accounts, doctors can build a substantial nest egg while minimizing their current tax liabilities.

Incorporating Tax-Efficient Investment Strategies

Investment planning is another critical component of tax optimization for medical professionals. By implementing tax-efficient investment strategies, doctors can minimize the tax impact of their investment income and maximize after-tax returns. Strategies such as investing in tax-exempt municipal bonds, utilizing tax-loss harvesting techniques, and allocating assets strategically across taxable and tax-advantaged accounts can help optimize tax efficiency and enhance overall portfolio performance.

Additionally, medical professionals may consider investing in retirement accounts or annuities that offer tax-deferred growth and potentially lower tax rates in retirement. By aligning their investment strategy with their tax objectives and long-term financial goals with the help of experts like John Moakler, doctors can effectively manage their tax liabilities while building wealth over time.

Leveraging Business Structure and Entity Planning

For medical professionals who operate their practices as independent contractors or business owners, choosing the right business structure can have significant tax implications. Incorporating as a professional corporation (PC), limited liability company (LLC), or partnership can offer various tax advantages, including potential deductions for business expenses, liability protection, and flexibility in income distribution.

Additionally, medical professionals should explore opportunities for entity planning, such as establishing a separate entity for administrative or consulting services or creating a management company to handle non-clinical aspects of their practice. By structuring their business operations strategically with the help of experts like John Moakler, doctors can optimize their tax position and minimize their tax liabilities while maintaining compliance with regulatory requirements.

Managing Health Care Costs and Insurance Premiums

Health care costs and insurance premiums can represent significant expenses for medical professionals, but they also offer opportunities for tax optimization. Doctors may be able to deduct qualified medical expenses, including premiums for health insurance, long-term care insurance, and medical malpractice insurance, as well as out-of-pocket costs for medical treatments and procedures.

Moreover, medical professionals should explore options for tax-advantaged health savings accounts (HSAs) or flexible spending accounts (FSAs), which allow for contributions on a pre-tax basis and tax-free withdrawals for qualified medical expenses. By proactively managing their health care costs and insurance premiums, doctors can leverage available tax benefits to reduce their overall tax burden and enhance their financial well-being.

Seeking Professional Guidance and Compliance

Finally, medical professionals should seek professional guidance from qualified tax advisors, accountants, or financial planners to develop and implement a comprehensive tax optimization strategy tailored to their specific needs and circumstances. Tax laws and regulations are complex and subject to change, so it's essential for doctors to stay informed and compliant to avoid potential penalties or liabilities.

Working with experienced professionals who specialize in tax planning for medical professionals can provide valuable insights, personalized recommendations, and ongoing support to optimize tax efficiency and achieve financial goals. By partnering with trusted financial planners like John Moakler and staying proactive in their tax planning efforts, doctors can navigate the complexities of the tax system with confidence and peace of mind.

Tax optimization is a critical aspect of financial planning for medical professionals, offering opportunities to minimize tax liabilities, maximize savings, and achieve long-term financial success. By understanding key tax strategies such as maximizing deductions and credits, maximizing retirement contributions, incorporating tax-efficient investment strategies, leveraging business structure and entity planning, managing health care costs and insurance premiums, and seeking professional guidance and compliance, doctors can optimize their tax position and enhance their overall financial well-being. With careful planning, proactive management, and strategic decision-making, medical professionals can navigate the complexities of the tax system effectively and build a solid foundation for a secure and prosperous future.

0 notes

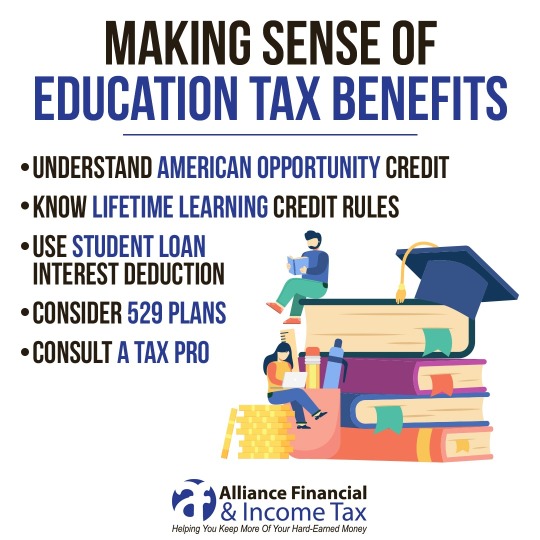

Photo

📚🌟 Maximize Your Savings with Education Tax Benefits! 🌟📚 Are you or your loved ones pursuing higher education? Don’t miss out on valuable tax breaks! 🎓💰 1. American Opportunity Tax Credit (AOTC): Up to $2,500 per student for qualified education expenses. If the credit reduces your tax to less than zero, you may even get a refund! 💸 Ideal for undergraduates seeking a degree. 2. Lifetime Learning Credit (LLC): Available for both degree and non-degree courses. Covers 20% of up to $10,000 in eligible expenses. Perfect for lifelong learners and professionals enhancing their skills. 3. Tuition and Fees Deduction: Deduct up to $4,000 in qualified education expenses. Reduces your taxable income directly. Great for those who don’t qualify for education credits. Remember, education tax benefits can significantly ease the financial burden of tuition, textbooks, and other educational costs. Consult IRS Publication 970 for detailed information and eligibility criteria 12. Share this post with fellow students and learners! Let’s make education more affordable and accessible for everyone. 🙌🎒✨

0 notes

Text

Until you turn 65, are you able to enroll in Medicare?

Soon to be 65? There are so many new opportunities right now. It's important to think about when to enroll in Medicare despite your excitement.

Medicare is the American health insurance program for people 65 and older. While most people become eligible at age 65, enrollment can be put off until later if necessary.

The advantages of enrolling in Medicare at age 65 and the circumstances under which waiting to do so makes sense are discussed in this blog post. We'll talk about Medicare options, as well as eligibility requirements.

Medicare's Advantages for Those Who Enroll at Age 65

The age of Medicare eligibility, 65, might seem like a given. It is for many! There are various advantages to enrolling in Medicare as soon as possible after becoming eligible.

start receiving Medicare benefits at age 65 to ensure full medical protection upon retirement. Now that you know any emergency medical costs will be covered, you can rest easy.

By enrolling before age 65, you can avoid late enrollment costs and penalties. The cost of Medicare Parts B and D could go up as a result of these fines. Saving money on Medicare by enrolling early.

When you first enroll in Medicare at age 65, you have a lot of medicare coverage choices. Dental and vision care are included by some Medigap and Medicare Advantage policies.

Benefit from Medicare's preventative care services by signing up early. Annual wellness checks and tests for cancer and cardiovascular disease can detect health problems early, when they are easier to treat.

Costs of Putting Off Medicare Enrollment

Some people may put off signing up for Medicare until they reach age 65. It's tempting to put off enrolling in Medicare if you have employer-provided insurance or some other form of health coverage. Think about the costs of delaying registration.

The consequences for enrolling in Part B premiums late are substantial. For each complete 12 month period you were eligible but did not enroll in Part B, your monthly premium could increase by 10%. The expense of this penalty might add up quickly.

Both Part B late enrollment fines and Part D pharmacy coverage late enrollment penalties apply. After 63 days without qualifying prescription drug coverage, you may incur a lifetime late-enrollment penalty if you decide to enroll in Medicare Part D.

These costs must be balanced against those of enrolling in Medicare at the age of 65. Although there may be valid reasons to put off enrolling depending on one's individual situation, one should not discount the financial consequences of doing so.

Medicare Delay: When It Makes Sense

Although registering in Medicare at 65 is suggested, there are situations when deferring registration makes sense. If you are still employed, you may be covered enough by your employer's health insurance plan. Due to your primary coverage under your company's plan, you can put off enrolling in Medicare Part B (which pays for non-hospital treatment) until later.

Holders of health plans purchased through the Marketplace could profit by waiting. Keeping your current plan may be less expensive than switching to Medicare if you are eligible for premium tax credits or cost-sharing reductions through the Health Insurance Marketplace.

In cases where a spouse's work provides comprehensive coverage at a reasonable cost, delaying Medicare enrollment may be the best course of action.

You can save money by registering late, but only if you meet the requirements for a Special Registration Period. These fines increase the cost of Medicare Part B and could lead to coverage gaps.

The Medicare eligibility start date is situational. Think about your coverage options and any potential penalties before making a final decision. If you need assistance deciding, go to a qualified medical professional or financial counselor.

Medicare Supplement Plans and Other Insurance Options

There are other healthcare options than the original Medicare. Individuals who meet Medicare's eligibility requirements are eligible for a wide range of benefits.

Medicare Advantage is a common choice among Medicare recipients. Part C plans are offered by private insurance firms, and they supplement Original Medicare (Parts A and B) by covering prescription drugs, dental care, and vision care. In most cases, their out-of-pocket costs are less than those of Medicare.

Alternatives include Medicare Supplement plans (Medigap). Deductibles, copayments, and coinsurance are supplemented by these programs in addition to Original Medicare. For those in need of more comprehensive protection, they can provide financial stability and peace of mind.

Those who are unhappy with their current healthcare system have the option of switching to an HMO or PPO through their employer or the open market. These plans provide access to subsidized networks of medical professionals.

Carefully consider each of these alternatives before settling on a healthcare plan. Cost, provider adaptability, the necessity of prescription drugs, and overall health are all factors that influence the relative merits of each option.

Careful evaluation of your individual needs is required while selecting a Medicare supplemental plan. You can compare policies by consulting a skilled insurance agent or using resources available online.

When to Enroll in Medicare and What to Consider

When to enroll in Medicare is a personal choice. Healthcare coverage is based on individual circumstances and requirements. However, it is important to weigh the advantages of enrolling in Medicare at age 65 against the costs of waiting.

Those who are about to turn 65 are strongly encouraged to enroll in Medicare during the Initial Enrollment Period. Three months prior to your 65th birthday and three months afterward total seven months. If you sign up now, you won't have to worry about paying late fees and will be covered whenever you might need it.

Medicare enrollment delays make sense in some cases. You can postpone enrolling in Part B while still maintaining Part A if you are still actively employed and covered by equivalent employer-sponsored health insurance. When your employment or coverage ends, you have eight months to enroll in Medicare Part B without paying a penalty.

0 notes

Text

After Customer Feedback Delta Adjusts 2024 SkyMiles Program

After Customer Feedback, Delta Adjusts 2024 SkyMiles Program

https://ift.tt/d4e9Ek8

After some thought and promising to make changes “based on customer feedback,” the Atlanta-based carrier announced a new set of changes for SkyMiles flyers, including new loyalty thresholds and changed bonuses for credit card holders.

Earning Status Doesn’t Change, But Bonuses and Opportunities to Earn Medallion Qualifying Dollars Increases

As with other loyalty programs, the way flyers will earn status in 2024 won’t change: Tier level will be based purely on spending. However, the carrier is allowing more pathways for flyers to get status.

The primary way remains through flying: Travelers will earn $1 Medallion Qualifying Dollar per $1 spent on Delta and partner flights. Those who hold the Delta SkyMiles Platinum, Platinum Business, Reserve, or Reserve Business American Express cards will also get a boost on earning MQDs.

With the personal or business versions of the Reserve card, flyers will earn $1 MQD for every $10 spent on the card. On both versions of the Platinum card, flyers get $1 MQD for every $20 spent with the card. Holders of both cards will get a $2,500 MQD headstart in February 2024.

In terms of earning Medallion status, flyers can earn Silver Medallion after $5,000 MQDs, or Gold with $10,000 MQDs. Platinum is available to those who earn $15,000 MQDs, while Diamond Medallion is only available to those earning $28,000 MQDs.

Once flyers earn higher status levels, they will find new Choice Benefit options to select. Flyers can select an MQD accelerator of $1,000 at Platinum and $2,000 at Diamond, while Diamond flyers can choose a Delta SkyClub individual membership for two Choice Benefit selections. Another option is earning bonus miles or taking a travel voucher. Platinum members can receive a one-time bonus of 30,000 miles for their account or to gift elsewhere, while Diamond members can receive a perk of 35,000 miles. If elites want to select a voucher for future travel, Platinum members can get a $300 voucher, while Diamonds can select a $350 voucher.

Flyers will have an opportunity to select how they want to convert their Medallion Qualifying Miles from 2023, as they will no longer be a qualifying factor. Flyers can convert them to SkyMiles, Medallion Qualifying Dollars, or a combination of both. Starting in 2024, flyers will not get any rollover dollars unless they have a card headstart or a Choice Benefit accelerator.

Access to Sky Lounges will also tighten starting on January 1, 2024. Reserve card members will receive 15 day visits per year, defined as “all access to the Sky Club within a 24-hour period after your first check-in at any Delta Sky Club” at the departure, transfer, and landing airport. Those who hold The Platinum Card from American Express will be limited to 10 day visits, while those holding the Delta SkyMiles Platinum Card or flying on a basic economy ticket won’t be able to visit the Sky Club.

How do you feel about the NEW New SkyMiles changes? Share your thoughts on the FlyerTalk Forums.

via FlyerTalk – The world's most popular frequent flyer community https://ift.tt/e054siW

October 20, 2023 at 02:31PM

0 notes

Text

Income Properties Are Trending, But Is Landlord Life for You?

If the thought of investing your money into brick and mortar—or perhaps some stylishly-painted siding—excites you, join the club.

Investing in real estate has long been one of Americans' favorite ways to grow their wealth. In fact, over 70% of single-family rental properties are currently owned by individual investors rather than corporations, according to Census data.1

Moreover, a decade's worth of Bankrate surveys has found that Americans often prefer real estate for long-term wealth building over other investments. According to Bankrate's latest survey, for example, Americans have historically embraced real estate, in part, because of the strong return on investment it can offer—especially to investors willing to stick with a property over time.2 It’s also a popular way to hedge against inflation since both rental income and property values tend to rise in tandem with overall prices.3

Now, as higher interest rates continue to push priced-out homebuyers to the sidelines, a new crop of “mom and pop” investors are eyeing the mushrooming rental market as a potential goldmine.4 Interest in buying a home to both live in and rent is also on the rise, especially amongst cash-strapped buyers looking to supplement their mortgage payments.5

But how do you know if you’re well-suited to take advantage of these real estate investment opportunities? Here are three signs that owning a rental property could be right for you.

YOU'RE A HOMEBUYER WHO WANTS HELP COVERING THE MORTGAGE

If you're looking for a creative way to buy a home without overspending, “house hacking” could be the answer. Increasingly popular with first-time homebuyers and budget-conscious investors, house hacking simply means buying a home that you intend to live in while renting out a portion of it to one or more tenants.5

House hacking also tends to be easier to break into than traditional real estate investing since you don't need as high a credit score or as large a down payment to qualify for a mortgage. In fact, some government-backed mortgage programs will let you buy a primary residence with little to no money down.6 Buying a home you don't plan to live in, by contrast, may require you to put down as much as 15% to 25% to qualify for a loan.7

If you house hack, the money you collect for rent each month can help cover your mortgage and other homeownership expenses. Depending on your setup, you may also be able to save on utility bills by splitting them with your tenant or tacking a portion onto their monthly rent. Another major advantage of house hacking is that it entitles you to certain tax benefits and deductions available only to landlords.8

When it's time to start your search, we can help you find a property that's ideal for house hacking, such as a house with a walkout basement, a multifamily unit, or a home with enough outdoor space to build an accessory dwelling unit or garage apartment.

YOU'RE AN INVESTOR LOOKING FOR STEADY AND RELIABLE INCOME

If you’re not crazy about the idea of a live-in tenant but still desire an additional stream of income, a dedicated long-term rental property could be a better option for you. Besides the monthly proceeds, purchasing a rental home can also add diversity and long-term stability to your investment portfolio and help you build wealth over time.9

According to data from the Federal Reserve, real estate owners have historically prospered. In early 2020, for example, the median home was worth almost triple what it was 30 years prior. Then, during the pandemic-era real estate boom, average home prices grew at an especially frenzied clip, climbing by nearly 50%, on average, in just two and a half years.10

However, the rate of appreciation can be hard to predict, so it’s prudent to invest in a property that also offers positive cash flow, which means the rent you take in exceeds your expenses. This strategy helps to ensure that you’ll put money in your pocket each month, even if the property’s value takes time to grow.

While today’s higher mortgage rates can make it more challenging for landlords to turn a profit, investment opportunities aren’t reserved for cash buyers. In fact, currently, almost 60% of real estate investors take out a loan to finance their purchase, according to Thomas Malone, an economist at the real estate data firm CoreLogic.4 He also notes that more small investors are stepping in to meet demand for rental housing, which has grown since many would-be buyers remain priced out of the purchase market.4

If you want to explore opportunities for a residential rental property that's good for your wallet and attractive to renters, we can help. Reach out with questions or to schedule a free consultation.

YOU'RE AN EXPERIENCED INVESTOR LOOKING TO MAXIMIZE YOUR POTENTIAL RETURNS

Another increasingly popular way to draw income from an investment property is to convert it to a short-term vacation rental. But beware: This strategy can be riskier as some municipalities have tightened rental restrictions and others are suffering from market oversaturation.11,12

With that said, if you're an experienced investor who can afford to take on some uncertainty, then investing in a short-term rental could make sense for you.

If you find the right property, for example, you could earn significantly more renting it short-term on a platform like Airbnb than if you rented the home to a long-term tenant.11

The key is to keep it occupied as much as possible at a premium nightly rate. To do that, you’ll need some marketing savvy, hospitality skills, and business acumen. Of course, you can always hire a professional property manager, but you’ll need to factor the cost into your budget.

The vacation rental market enjoyed a boom during the pandemic, and some inexperienced investors are finding they bit off more than they can chew. As a result, there's an opportunity to snap up some of these properties, but you'll need some cash on hand and a willingness to learn the business.12

We can help you scout opportunities in our local market or, if you’re interested in investing in another area, we can refer you to an agent there for assistance.

BOTTOMLINE

Investing in real estate can be a great way to build your wealth long-term and earn some extra income. But to make the most of your investment, it pays to be strategic.

Call us for a consultation so we can discuss your goals and budget. We'll help you discover neighborhoods with the best income potential, point out the homes most suited to renting, and help you brainstorm the best investment strategy for you.

Before you take the plunge, make sure you can answer “YES”

to these three questions:

Are you ready to be a landlord?

Owning a rental property can take a lot of time and energy. You're not just buying passive income, you're also building sweat equity since the time you spend maintaining, marketing, and managing your rental can add up quickly. So be prepared to do some soul-searching to ensure you’ll not only flourish as a landlord, but actually enjoy it.

If you want to invest in real estate but aren’t prepared to put in the day-to-day effort required, we can refer you to a property management service for help.

Can you afford to invest in real estate?

The last thing you want is to get over-extended with your new real estate venture. Besides the cost of purchasing the property, you’ll need to consider additional expenses, like property taxes, insurance, administrative costs, and maintenance and repairs. You will also need a cash reserve for unexpected issues or potential vacancies.

We can help you run the numbers to determine whether you can charge enough rent to offset your expenditures.

Have you found the right income property?

Even if you’ve got your finances in order and are emotionally ready to invest, your success as a landlord will also depend on the property you buy. The criteria for a good rental home and a good family home are often different, so it’s important to lean on professionals for advice.

We can help you find an ideal rental property, taking into account your budget, risk appetite, and investment goals. If you decide to invest in a different area, we'll connect you with an agent who's more plugged into that community. Reach out today to schedule a free consultation.

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.

Sources:

PR Newswire

Bankrate

Forbes

MarketWatch

Realtor.com

NerdWallet

LendingTree

Quicken Loans

Investors Business Daily

St. Louis Fed FRED Economic Data

Story by J.P. Morgan

Skift

0 notes

Text

The Path to Homeownership: Homes for Sale in Lakeland, TN

Introduction

Owning a home is a lifelong aspiration for many, embodying stability, security, and the realization of the American dream. When considering homeownership in a place like Lakeland, Tennessee, there are several crucial steps and factors to ponder. In this article, we will delve into the various facets of embarking on the journey to homeownership in Lakeland, TN, and offer insights to help you make informed decisions on this exciting path.

Exploring Lakeland, TN

Lakeland, Tennessee, is a picturesque suburb situated in Shelby County, adjacent to the city of Memphis. It is renowned for its tranquil surroundings, close-knit communities, and a harmonious blend of modern conveniences with a touch of Southern charm. Lakeland is celebrated for its top-notch schools, thriving local culture, and a high quality of life, making it an ideal destination for potential homeowners.

Establishing Your Budget

The initial and pivotal step towards homeownership is establishing a well-defined budget. To do this effectively, you must undertake a comprehensive assessment of your financial situation. This includes an evaluation of your income, monthly expenses, savings, and credit score. Gaining clarity about your financial capacity is essential in determining the price range of homes you can realistically afford in Lakeland.

It is crucial to take into account all the costs associated with homeownership, not solely the purchase price of the house. These additional expenses may encompass property taxes, homeowner's insurance, routine maintenance, and monthly mortgage payments. Creating a comprehensive budget will not only prevent you from stretching your finances too thin but also ensure a smooth transition into homeownership.

Mortgage Pre-Approval

Once you have a firm grasp of your budget, the next critical step is obtaining mortgage pre-approval. Mortgage pre-approval provides you with a clear understanding of how much you can borrow and the interest rates available to you. This information is invaluable when commencing your search for homes in Lakeland, as it helps you narrow down your options to properties that are well-aligned with your financial capacity.

Before seeking pre-approval, it is advisable to compare mortgage offers from various lenders to find the one that best suits your needs. A favorable credit score and a stable source of income will enhance your chances of securing a favorable mortgage rate.

Choosing the Right Neighborhood

Lakeland offers a diversity of neighborhoods, each with its unique character and amenities. When seeking homes, it is vital to consider the neighborhood's proximity to your workplace, schools, healthcare facilities, and recreational opportunities. Your lifestyle preferences, whether you prefer a serene, family-oriented environment or a livelier, bustling community, should also factor into your decision.

Furthermore, researching safety and crime rates in different neighborhoods is paramount. Utilize resources such as local authorities' crime statistics and gather insights from residents to make an informed choice about where you want to establish your home in Lakeland.

Leveraging Real Estate Expertise

Navigating Lakeland's real estate market can be a complex endeavor, especially for first-time buyers. Collaborating with a qualified and experienced real estate professional can be a game-changer in your home-buying journey. A knowledgeable agent possesses insights into the local market, can help you identify properties that align with your criteria, and adeptly negotiate on your behalf.

When selecting a real estate agent, scrutinize their track record, review client testimonials, and ascertain their familiarity with Lakeland's neighborhoods. An agent who comprehends your preferences and requirements can streamline the process, ensuring you make informed decisions.

Home Inspection and Appraisal

After identifying a property of interest, it is crucial to conduct a thorough home inspection and appraisal. A home inspection is a pivotal step in ensuring that the property is in good condition and free of concealed defects or issues. Simultaneously, an appraisal assesses the property's value to determine if it corresponds with the property's sale price.

These steps serve as safeguards for your investment. If any issues surface during the inspection, you can negotiate with the seller for necessary repairs or price adjustments. An accurate appraisal guards against overpaying for the property.

Making an Offer and Closing the Deal

Following a successful inspection and appraisal, you can proceed to make an offer on the property. Your real estate agent will assist you in crafting a competitive offer, taking into account market conditions and the property's condition. Negotiations may ensue, and once both parties agree on the terms, you can progress to the closing process.

The closing process involves signing all pertinent documents, including the mortgage agreements, title transfers, and the payment of closing costs. It is essential to meticulously review all documentation and, if necessary, seek legal advice to ensure a seamless and legally sound transaction.

Conclusion

The path to homes for sale in lakeland, TN, comprises a series of well-defined steps and considerations. Establishing your budget, securing mortgage pre-approval, selecting the ideal neighborhood, enlisting the support of a qualified real estate agent, conducting inspections and appraisals, making an offer, and completing the closing process are all integral aspects of this journey.

Throughout this endeavor, it is imperative to remain informed, patient, and diligent. Lakeland offers a diverse range of homes for sale, catering to various preferences and budgets. By adhering to these steps and seeking assistance from professionals well-versed in the local real estate landscape, you can transform the dream of homeownership in Lakeland into a reality.

Lakeland, TN, is not just a place to own a home; it is a community that extends a warm welcome to new residents. As you embark on this exciting journey, you will not only find a house but also a place to belong, connect, and create enduring memories. The path to homeownership in Lakeland is not merely about bricks and mortar; it is about laying the foundation for a brighter, more fulfilling future.

0 notes

Text

The likelihood of experiencing pain differs greatly from state to state.

The prevalence of moderate or severe joint pain due to arthritis varies strikingly across American states, ranging from 6.9% of the population in Minnesota to 23.1% in West Virginia, according to a new study led by a University at Buffalo researcher.

The paper published in the journal PAIN is providing new insights — through its novel combination of individual- and macro-level measures — into geographic differences in pain and their causes.

The prevalence of moderate or severe joint pain due to arthritis varies strikingly across American states, ranging from 6.9% of the population in Minnesota to 23.1% in West Virginia, according to a new study led by a University at Buffalo researcher.

The paper published in the journal PAIN is providing new insights — through its novel combination of individual- and macro-level measures — into geographic differences in pain and their causes.

“The risk of joint pain is over three times higher in some states compared to others, with states in the South, especially the lower Mississippi Valley and southern Appalachia, having particularly high prevalence of joint pain,” says Rui Huang, a sociology PhD student in the UB College of Arts and Sciences, and the paper’s first author. “We also observed educational disparities in joint pain in all states that vary substantially in magnitude, even after adjusting for demographic characteristics.”

The percentage point difference in pain prevalence between people who did not complete high school versus those who obtained at least a bachelor’s degree is much larger in West Virginia (31.1), Arkansas (29.7), and Alabama (28.3) than in California (8.8), Nevada (9.8) and Utah (10.1).

“Education can function as a ‘personal firewall’ that protects more highly educated people from undesirable state-level contexts, while increasing the vulnerability of less educated individuals,” says Huang.

Nearly 59 million people in the U.S. have arthritis, and at least 15 million of them experience severe joint pain because of that condition. Severe joint pain is associated with diminished range of motion, disability and mortality.

While existing research on the social determinants of pain has relied primarily on individual-level data, individuals are embedded in social contexts, such as a specific U.S. state.

Different states can have dramatically different policies that affect many aspects of life including opportunities, resources and social relationships, which can in turn influence individuals’ pain, a potential influence that has gone largely unexplored in previous research.

“Very little research has examined the geography of chronic pain, and virtually none has examined the role of state-level policies in shaping pain prevalence,” says Hanna Grol-Prokopczyk, PhD, UB associate professor of sociology, and a co-author of the study. “We were excited to identify state characteristics that reduce residents’ risk of pain.”

The current study does so by combining data on nearly 408,000 adults (ages 25-80) from the 2017 Behavioral Risk Factor Surveillance System with state-level data about SNAP programs (formerly known as food stamps), Earned Income Tax Credits, income inequality, social cohesion (relationship strength among community members), Medicaid Generosity Scores, and tobacco taxes.

Although SNAP programs exist in all 50 states, some states offer more expansive benefits to qualifying residents than others. States with more generous SNAP benefits had a lower prevalence of pain. The same was true for states with greater social cohesion, indicating that both material resources and social functioning play critical roles in shaping pain risk.

“The increase in the generosity of SNAP benefits could potentially alleviate pain by promoting healthier eating habits and alleviating the life stress associated with food insecurity,” says Huang. “Social factors such as conflict, isolation and devaluation are also among the ‘social threats’ that can lead to physical reactions such as inflammation and immune system changes.”

In addition to providing new information on pain disparities across states, the paper might also fuel a reorientation of pain research that puts equal emphasis on macro- and individual-level factors, according to Huang.

“Chronic pain can — and should — be addressed through macro-level policies, as well as through individual-level interventions,” says Huang. “This study also implies that pain research in general should move towards a greater understanding of the macro contextual factors that shape pain and pain inequalities.”

“The risk of joint pain is over three times higher in some states compared to others, with states in the South, especially the lower Mississippi Valley and southern Appalachia, having particularly high prevalence of joint pain,” says Rui Huang, a sociology PhD student in the UB College of Arts and Sciences, and the paper’s first author. “We also observed educational disparities in joint pain in all states that vary substantially in magnitude, even after adjusting for demographic characteristics.”

The percentage point difference in pain prevalence between people who did not complete high school versus those who obtained at least a bachelor’s degree is much larger in West Virginia (31.1), Arkansas (29.7), and Alabama (28.3) than in California (8.8), Nevada (9.8) and Utah (10.1).

“Education can function as a ‘personal firewall’ that protects more highly educated people from undesirable state-level contexts, while increasing the vulnerability of less educated individuals,” says Huang.